Can You Retire? Getting to Your Number

February 22, 2015 at 10:13 am Leave a comment

What’s “your number?” The catchy phrase has been tried on 30-second television commercials before, but the fact remains, most Americans have no clue how much they need to save for retirement. The ever-shifting and imprecise variables needed to compute the size of your needed nest egg can seem overwhelming: lifespan; career span; inflation; college tuition; healthcare expenses; rising insurance costs; social security; employer benefits; inheritance; child support; parental support; etc. The list goes on and with near-zero interest rates, and stock prices at record highs, the retirement challenge has only gotten riskier and more difficult.

I understand this task may not be easy and could eat into your House of Cards viewing, Candy Crush playing, or football watching. However, if you can spend two weeks planning a family vacation, you certainly can afford devoting a few hours to scribbling down some numbers as it relates to the lifeblood of your financial future. The project is definitely doable.

Here are some key steps to finding “your number.” If you’re not single, then calculate the figures for your household:

1). Calculate Your Budget: Where to start? A good place to begin is with is a boring budget (or your monthly expenses). The budget does not need to be down to the penny, but you should be able to estimate your monthly spend with the help of your bank and credit card statements. Make sure to include estimates for periodic unforeseen potential expenses like annual auto repairs, home repairs, or emergency hospital visits. Once you determine your monthly spend, extrapolating your annual spend shouldn’t be too difficult.

2). Compute Your Income: Your sources of income should be fairly straightforward. For most people this includes your salary and potential bonus. Some people will also generate income from investments, a business, and/or real estate. Before getting too excited about all the income you are raking in, don’t forget to subtract out taxes collected by Uncle Sam, and include a possible scenario of rising tax rates during your working years. Obviously, the economy can also have a positive or negative impact on your income projections, nevertheless, if you conservatively plan for some potential future setbacks, you will be in a much better position in forecasting the amount of savings needed to reach “your number.”

3). Planned Retirement Date: The date you pick may or may not be realistic, but by choosing a specific date, you can now evaluate how much savings will be necessary to reach your required nest egg number. The difference between your annual income (#2) and annual budget (#1) is your annual savings, which you can multiply by the number of years you plan to work until retirement. For example, assume you wanted to retire 15 years from now and were able to save/invest $20,000 each year while earning a 6% annualized return. By the year 2030 these savings would equate to about $465,000 and could be added to any other savings and other retirement income (pension, 401(k), Social Security, inheritance, etc.) to meet your retirement needs.

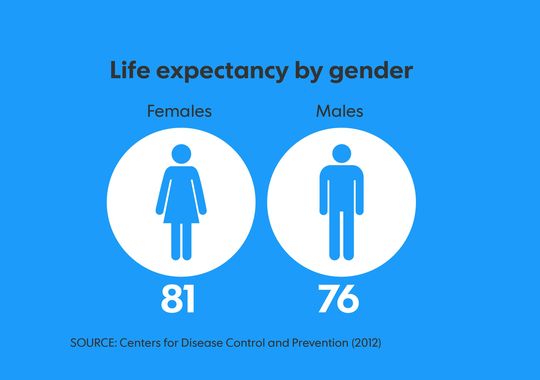

4). Life Expectancy: After you have determined when you want to retire, now comes the tricky part. How long are you going to live? Assuming you are currently healthy, you can use actuarial tables for life expectancy. According to a new report on American mortality from the Centers for Disease Control and Prevention’s National Center for Health Statistics, the average life expectancy is 81 for females and 76 for males (see graphic below). The estimates are a little rosier, if you have lived to age 65, in which case females are expected to live past 85 years old and males to about 83 years. You can adjust these figures higher or lower based on personal information and family history, but if you consider yourself “average,” then you better plan to have at least 15 years of fire power in your savings nest egg (see example at bottom of article).

Source: USA Today

Empty Retirement Wallets & Purses

The harsh realities are Americans are not saving enough. It‘s true, you can survive off a smaller nest egg, if you plan to live off of cat food and vacation in Tijuana, but most Americans and retirees have become accustomed to a higher standard of living. A New York Times article highlighted that 75% percent of Americans nearing retirement age had less than $30,000 in their retirement accounts – that’s not going to buy you that winter home on Maui or leave enough to cover your golf dues at the local country club.

Control the things that make a difference.

- Save. Pay yourself first by tucking money away each month. If you haven’t established an IRA (Individual Retirement Account) or savings account, make sure you contribute to your employer’s matching 401(k) plan to the fullest extent possible, if available. This is free money your employer is offering you and by not participation you are shooting yourself in the foot.

- Spend prudently. Review your monthly / annual budgets and determine where there is room to cut expenses. Every budget has fat in it, so it’s just a matter of cutting excessive and less important items, without sacrificing dramatic changes to your standard of living.

- Manage your career. Invest in yourself with education, apply for that promotion, or look for other employment alternatives if you are unhappy or not being paid your proper value.

- Push Retirement Out: If you are healthy and enjoy your work, extending your working years can have profoundly positive benefits to your retirement. Not only will you have more money saved up for retirement, but you will also receive higher Social Security benefits by delaying retirement (see Social Security benefit estimator).

The bottom-line is if you are like most working Americans, you will need to save more and invest more prudently (e.g., in a low-cost, tax-efficient manner like strategies offered by Sidoxia).

Use Your Thumb to Get Started

Rules of thumb are never perfect, but are not a bad place to start before fine-tuning your estimates. Some retirement pundits begin by using an 80% “income replacement ratio” rule as a retirement guide. In other words, you should not need 100% of your pre-retirement income during retirement because a number of your major living expenses should be reduced. For example, during retirement your tax expenses should decrease (because you are not working); your mortgage payment should be lower (i.e., house is paid off); your kids should be independent and off the family payroll; and you may be in the position to downsize your home (e.g., empty-nesters often decide to move to a lower square footage residence).

Another rule of thumb is the “15x Rule,” which says you will need an investment account equivalent to at least 15-times your pre-retirement income. Therefore, if your after-tax income is $100,000 before retirement and you need to replace $80,000 during retirement (80% replacement ratio), this means you actually only need to replace about $60,000 per year. We arrive at the lower $60,000 figure by further assuming the $80,000 can be reduced by about $20,000 flowing in annually from Social Security. Through the mighty powers of division, we can then apply the 4% Sustainable Withdrawal Rate rule (SWR) to reverse engineer the estimate of “our number.” In this example, our ultimate nest egg needed is $1,500,000 (equal to $60,000 / 4% or $60,000 x 25 years), which is estimated to last for 25 years of retirement. As you can see, there are quite a few assumptions baked into this scenario, including a retirement investment portfolio that beats inflation by 4%, but nevertheless this line of thinking creates an understandable framework to operate under.

Of course, for all the non-math Investing Caffeine readers, life could have been made easier by simply multiplying the $100,000 pre-retirement income by 15x to arrive at our $1.5 million nest egg. More elegant, but less fun for this nerdy math author.

We’ve covered a lot of ground, but I’m absolutely confident if you have read this far, you can definitely come up with “your number.” If this all seems too overwhelming, there is no need to worry, just find an experienced investment advisor or financial planner…I’m sure I could help you find one 🙂 .

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Entry filed under: Financial Planning. Tags: 4% Rule, 401k, budget, Budgeting, college savings, healthcare, life expectancy, Nest Egg, Retirement, social security, withdrawal rate.

{kind=link}

Trackback this post | Subscribe to the comments via RSS Feed