Archive for July, 2014

NVEC: A Cash Plump Activist Target…For Icahn?

Some might call Carl Icahn a greedy capitalist, but at the core, the 78 year old activist has built his billions in fortunes by unlocking shareholder value in undervalued companies. His targets have come in many shapes and sizes, but one type of target is cash bloated companies without defined capital allocation strategies. A recent high profile example of a cash ballooned target of Icahn was none other than the $591+ billion behemoth Apple Inc. (AAPL).

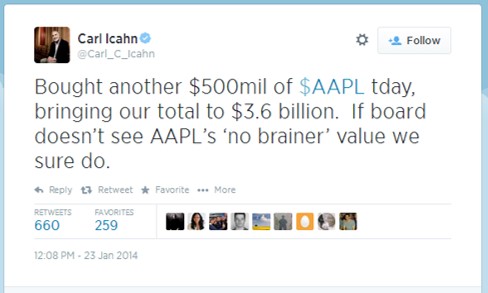

His initial tweet on August 13, 2013 announced his “large position” in the “extremely undervalued shares” of Apple ($67 split adjusted). We have been long-term shareholders of Apple ourselves and actually beat Carl to the punch three years earlier when the shares were trading at $35 – see Jobs: The Gluttonous Cash Hog. Icahn doesn’t just nonchalantly make outrageous claims…he puts his money where his mouth is. After Icahn’s initial proclamation, he went onto build a substantial $3.6 billion Apple position by January 2014.

Icahn initially demanded Apple’s CEO Tim Cook to execute a $150 billion share repurchase program before downgrading his proposal to a $50 billion buyback. After receiving continued resistance, Icahn eventually relented in February 2014. But Icahn’s blood, sweat, and tears did not go to waste. His total return in Apple from his initial announcement approximates +50%, in less than one year. And although Icahn wanted more action taken by the company’s management team, Apple has repurchased about $50 billion in stock and paid out $14 billion in dividends to investors over the last five quarters. Despite the significant amount of capital returned to shareholders over the last year, Apple still holds a gargantuan net cash position of $133.5 billion, up approximately $3 billion from the 2013 fiscal third quarter.

Icahn’s Next Cash Plump Target?

Mr. Icahn is continually on the prowl for new targets, and if he played in the small cap stock arena, NVE Corp. (NVEC) certainly holds the characteristics of a cash bloated company without a defined capital allocation strategy. Although I rarely write about my hedge fund stock holdings, followers of my Investing Caffeine blog may recognize the name NVE Corp. More specifically, in 2010 I picked NVEC as my top stock pick of the year (see NVEC: Profiting from Electronic Eyes, Nerves & Brains). The good news is that NVEC outperformed the market by approximately +25% that year (+36% vs 11% for the S&P 500). Over the ensuing years, the performance has been more modest – the +42% return from early 2010 has underperformed the overall stock market.

Rather than rehash my whole prior investment thesis, I would point you to the original article for a summary of NVE’s fundamentals. Suffice it to say, however, that NVE’s prospects are just as positive (if not more so) today as they were five years ago.

Here are some NVE data points that Mr. Icahn may find interesting:

- 60% operating margins (achieved by < 1% of all non-financial companies FINVIZ)

- 0% debt

- 15% EPS growth over the last seven years ($1.00 to $2.29)

- Cutting edge, patent protected, market leading spintronic technology

- +7% Free Cash Flow yield ($13m FCF / $194 adjusted market value) $294m market cap minus $100m cash.

- $100 million in cash on the balance sheet, equal to 34% of the company’s market value ($294m). For comparison purposes to NVE, Apple’s $133 billion in cash currently equates to about 23% of its market cap.

Miserly Management

As I noted in my previous NVE article, my beef with the management team has not been their execution. Despite volatile product sales in recent years, it’s difficult to argue with NVE CEO Dan Baker’s steering of outstanding bottom-line success while at the helm. Over Baker’s tenure, NVE has spearheaded meteoric earnings growth from EPS of $.05 in 2009 to $2.29 in fiscal 2013. Nevertheless, management not only has a fiduciary duty to prudently manage the company’s operations, but it also has a duty to prudently manage the company’s capital allocation strategy, and that is where NVE is falling short. By holding $100 million in cash, NVE is being recklessly conservative.

Is there a reason management is being so stingy with their cash hoard? Even with cash tripling over the last five years ($32m to $100m) and operating margins surpassing an incomprehensibly high threshold (60%), NVE still has managed to open their wallets to pursue these costly actions:

- Double Capacity: NVE doubled their manufacturing capacity in fiscal 2013 with minimal investment ($2.8 million);

- Defend Patents: NVE fought and settled an expensive patent dispute against Motorola spinoff (Everspin) as it related to the company’s promising MRAM technology;

- R&D Expansion: The company shored up its research and development efforts, as evidenced by the +39% increase in fiscal 2014 R&D expenditures, to $3.6 million.

The massive surge in cash after these significant expenditures highlights the indefensible logic behind holding such a large cash mound. How can we put NVE’s pile of cash into perspective? Well for starters, $100 million is enough cash to pay for 110 years of CAPEX (capital expenditures), if you simply took the company’s five year spending average. Currently, the company is adding to the money mountain at a clip of $13,000,000 annually, so the amount of cash will only become more ridiculous over time, if the management team continues to sit on their hands.

To their credit, NVE dipped half of a pinky toe in the capital allocation pool in 2009 with a share repurchase program announcement. Since the share repurchase was approved, the cash on the balance sheet has more than tripled from the then $32 million level. To make matters worse, the authorization was for a meaningless amount of $2.5 million. Over a five year period since the initial announcement, the company has bought an irrelevant 0.5% of shares outstanding (or a mere 25,393 shares).

A Prudent Proposal

The math does not require a Ph.D. in rocket science. With interest rates near a generational low, management is destroying value as inflation eats away at the growing $100 million cash hoard. I believe any CFO, including NVE’s Curt Reynders, can be convinced that earning +7% on NVE shares (or +15% if earnings compound at historical rates for the next five years) is better than earning +2% in the bank. Or in other words, buying back stock by NVE would be massively accretive to EPS growth. Conceptually, if NVE used all $100 million of its cash to buy back stock at current prices, NVE’s current EPS of $2.59 would skyrocket to $3.63 (+40%).

A more reasonable proposal would be for NVE management to buy back 10% of NVE’s stock and simultaneously implement a 2% dividend. At current prices, these actions would still leave a healthy balance of about $75 million in cash on the balance sheet by the end of the fiscal year, which would arguably still leave cash at levels larger than necessary.

Despite the capital allocation miscues, NVE has incredibly bright prospects ahead, and the recently reported quarterly results showing +37% revenue growth and +57% EPS growth is proof positive. As a fellow long-term shareholder, I share management’s vision of a bright future, in which NVE continues to proliferate its unique and patented spintronic technology. With market leadership in nanotechnology sensors, couplers, and MRAM memory, NVE is uniquely positioned to take advantage of game changing growth in markets such as nanotechnology biosensors, electric drive vehicles (EDVs), consumer electronic compassing, and next generation MRAM technology. If NVE can continue to efficiently execute its business plan and couple this with a consistent capital allocation discipline, there’s no reason NVE shares can’t reach $100 per share over the next three to five years.

While NVE continues to execute on their growth vision, they can do themselves and their shareholders a huge favor by implementing a shareholder enhancing capital return plan. Carl Icahn is all smiles now after his successful investments in Apple and Herbalife (HLF), but impatient investors and other like-minded activists may be lurking and frowning, if NVE continues to irresponsibly ignore its swelling $100 million cash hoard.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in Apple Inc. (AAPL), NVE Corp. (NVEC), and certain exchange traded funds, but at the time of publishing SCM had no direct position in TWTR, MOT, Everspin, HLF, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Day Trading Your House

By several measures, this economic recovery has been the slowest, most-challenging expansion since World War II. Offsetting the painfully slow recovery has been a massive bull market in stocks, now hovering near all-time record highs, after about tripling in value since early 2009. Unfortunately, many investors have missed the boat (see Markets Soar – Investors Snore and Gallup Survey) with stock ownership near a 15-year low.

But it’s not too late for the “sideliners” to get in…is it? (see Get out of Stocks!*). Milfred and Buford are asking themselves that same question (see Investor Wake-Up Call). Milfred and Buford are like many other individuals searching for the American Dream and are looking for ways to pad their retirement nest egg. The seasoned couple has been around the block a few times and are somewhat familiar with one get-rich-quick strategy…day trading stocks. Thankfully, they learned that day trading stocks didn’t work out too well once the technology boom music ended in the late 1990s. Here’s what the SEC has to say about day trading on their government site:

Be prepared to suffer severe financial losses. Day traders typically suffer severe financial losses in their first months of trading, and many never graduate to profit-making status. Given these outcomes, it’s clear: day traders should only risk money they can afford to lose. They should never use money they will need for daily living expenses, retirement, take out a second mortgage, or use their student loan money for day trading.

Milfred & Buford Day Trade House

Milfred: “Now, Buford, I know we lost of our IRA retirement money day trading tech stocks, but if technical analysis works and all the financial news shows and talking babies on TV say it will make us a lot of cabbage, maybe we should try day trading our house?”

Buford: “Now I know why I married you 60 years ago – it’s that brilliant mind of yours that complements that sexy figure!”

Veteran readers of Investing Caffeine know I’ve been a skeptic of technical analysis (see Technical Analysis: Astrology or Lob Wedge), but a successful investor has to be open to new ideas, correct? So, if technical analysis works for stocks, then why not for houses? The recovery in housing prices hasn’t been nearly as robust as we’ve seen in stocks, so perhaps there’s more upside in housing. If I can get free stock charting technicals from my brokerage firm or online, there’s no reason I couldn’t access free charting technicals from Zillow (or Trulia) to make my fortunes. Case in point, I think I see a double-bottom and reverse head-and-shoulders pattern on the home price chart of Kim Kardashian’s house:

Source: Zillow

Of course, day trading isn’t solely dependent on random chart part patterns. Pundits, bloggers, and brokerage firms would also have you believe instant profits are attainable by trading based on the flow of news headlines. This is how Milfred and Buford would make their millions:

Milfred: “Snookums, it’s time for you to pack up all our stuff.”

Buford: “Huh? What are you talking about honey buns?”

Milfred: “Didn’t you see?! The University of Michigan consumer confidence index fell to a level of 81.3 vs. Wall street estimates of 83.0, bringing this measure to a new 4-month low.”

Buford: “I can’t believe I missed that. Nice catch ‘hun’. I’ll start packing, but where will we stay after we sell the house?”

Milfred: “We can hang out at the Motel 6, but it shouldn’t be long. I’m expecting the Philly Fed Manufacturing index to come in above 23 and I also expect a cease fire in Ukraine and Gaza. We can buy a new house then.”

I obviously frame this example very tongue-in-cheek, but buying and selling a house based on squiggly lines and ever-changing news headlines is as ridiculous as it sounds for trading stocks. The basis for any asset purchase or sale should be primarily based on the cash flow dynamics (e.g., rent, dividends, interest, etc., if there are any) of the asset, coupled with the appreciation/depreciation expectations based on a rigorous long-term analysis.

When Day Trading Works

Obviously there are some differences between real estate and stocks (see Stocks & Real Estate), including the practical utility of real estate and other subjective factors (i.e., proximity to family, schools, restaurants, beach, crime rates, etc.). Real estate is also a relatively illiquid and expensive asset to buy or sell compared to stocks. – However, that dynamic is rapidly changing. Like we witness in stocks, technology and the internet is making real estate cheaper and easier to match buyers and sellers.

Does day trading a stock ever work? Sure, even after excluding the factor of luck, having a fundamental information advantage can lead to immediate profits, but one must be careful how they capture the information. Raj Rajaratnam used this strategy but suffered the consequences of his insider trading conviction. Furthermore, the information advantage game can be expensive, as proven by Steven Cohen’s agreement to pay $1.2 billion to settle criminal charges. While I remain a day trading and technical analysis skeptic, I have noted a few instances when I use it.

Whatever your views are on the topics of day trading and technical analysis, do Milfred and Buford a favor by leading by example…invest for the long-term.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds, but at the time of publishing SCM had no direct position in Z, TRLA, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Thrill of the Chase

Men (and arguably women to a lesser extent) enjoy the process of hunting for a mate. Chasing the seemingly unattainable event aligns with man’s innate competitive nature. But the quest for the inaccessible is not solely limited to dating. When it comes to other aspirational categories, humans also want what they cannot have because they revel in a challenge. Whether it’s a desirable job, car, romantic partner, or even an investment, people bask in the pursuit.

For many investment daters and trading speculators, 2008-2009 was a period of massive rejection. Rather than embracing the losses as a new opportunity, many wallowed in cash, CDs, bonds, and/or gold. This strategy felt OK until the massive 5-year bull market went on a persistent, upward tear beginning in 2009. Now, as the relentless bull market has continued to set new all-time record highs, the negative sentiment cycle has slowly shifted in the other direction. Back in 2009, many investors regretted owning stocks and as a result locked in losses by selling at depressed prices. Now, the regret of owning stocks has shifted to remorse for not owning stocks. Missing a +23% annual return for five years, while getting stuck with a paltry 0.25% return in a savings account or 3-4% annual return achieved in bonds, can harm the psyche and make savers bitter.

Greed hasn’t fully set in like we witnessed in the late period of the 1990s tech boom, but nevertheless, some of the previous overly cautious “sideliners” feel compelled to now get into the stock game (see Get Out of Stocks!*) or increase their equity allocation. Like a desperate, testosterone-amped teen chasing a prom date, some speculators are chasing stocks, regardless of the price paid. As I’ve noted before, the overall valuation of the stock market seems quite reasonable (see PE ratio chart in Risk Aversion Declining – S. Grannis), despite selective pockets of froth popping up in areas like biotech stocks, internet companies, and junk bonds.

Even if chasing is a bad general investment practice, in the short-run, chasing stocks (or increasing equity allocations) may work because overall prices of stocks remain about half the price they were at the 2000 bubble peak (see Siegel Bubblicious article). How can stocks be -50% off when stock prices today (S&P 500) are more than +25% higher today than the peak in 2000? Plain and simply, it’s the record earnings (see It’s the Earnings Stupid). In the latest Sidoxia newsletter we highlighted the all-time record corporate profits, which are conveniently excluded from most stock market discussions in the blogosphere and other media outlets.

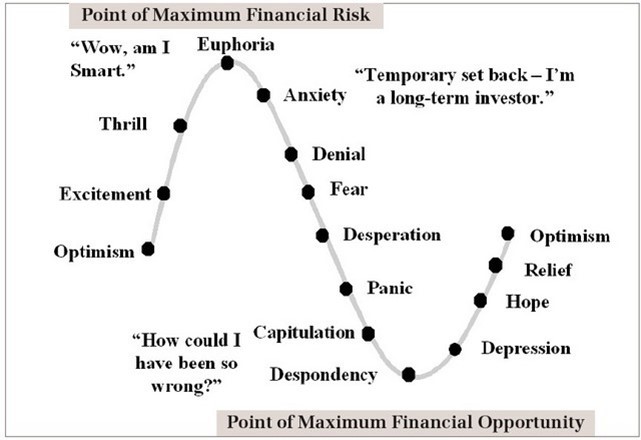

The Investor’s Emotional Roller Coaster (Perceived Risk vs Actual Risk)

The “Thrill of the Chase” is but a single emotion on the roller coaster sentiment spectrum (see Barry Ritholtz chart in Sentiment Cycle of Fear and Greed). The problem with the above chart is many investors confuse actual risk from perceived risk. Many investors perceive the “euphoric” stage of an economic cycle (top of the chart) as low-risk, when in actuality this point reflects peak risk. One can look back to the late 1990s and early 2000 when technology shares were priced at more than 100x years in earnings and every hairdresser, cabdriver and relative were plunging their life savings into stocks. The good news from my vantage point is we are a ways from that euphoric state (asset fund flows and consumer confidence are but a few data points to support this assertion).

The key to reversing the sentiment roller coaster is to follow the thought process of investment greats who learned to avoid euphoria in up markets:

“I’m always more depressed by an overpriced market in which many stocks are hitting new highs every day than by a beaten-down market in a recession.” -Peter Lynch

“Be fearful when others are greedy, and be greedy when others are fearful.” –Warren Buffett

While the “Thrill of the Chase” can seem exciting and a rational strategy at the time, successful long-term investors are better served by remaining objective, unemotional, and numbers-driven. If you don’t have the time, interest, or emotional fortitude to be disciplined, then find an experienced investment manager or advisor to assist you. That will make your emotional roller coaster ride even more thrilling.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Winning via Halftime Adjustments

This article is an excerpt from a previously released Sidoxia Capital Management complementary newsletter (July 1, 2014). Subscribe on the right side of the page for the complete text.

In the game of sports and investing there are a lot of unanticipated dynamics that occur during the course of a game, season, or year. With the second quarter of 2014 now coming to a close, we have reached the half-way point of the year. Along the way, the coach (and investors) may need to make some strategic halftime adjustments. Reassessing or reflecting on the positioning of your investment portfolio once or twice per year in the context of your investment objectives, time horizon, and risk tolerance level is never a bad idea – especially when there are unforeseen events continually materializing during the game.

During the first half of the year, the financial markets have experienced numerous surprises:

- Declining Interest Rates: Under the auspices of a massive 2013 gain in stock prices, expectations were for an accelerating economy and rising interest rates in 2014. Instead, the 10-Year Treasury Note has seen its yield counterintuitively plunge from 3.03% to 2.52%.

- Geopolitical Tensions (Ukraine/Syria/Iraq): The stock market has ground higher this year in spite of geopolitical tensions in Ukraine, Syria, and now Iraq. These skirmishes make for great TV, radio, and blog content, but the reality is these conflicts will likely be forgotten/ignored in favor of other fresher clashes in the coming months and quarters.

- Unabated Tapering: It’s true the Federal Reserve signaled the reduction in its bond buying stimulus program last year, however the more surprising aspect has been the pace of the taper. From the beginning of the year, the $85 billion program has already been reduced to $35 billion and will likely be reduced to $0 by the fall.

- Polar Vortex/GDP: Weather is very unpredictable, and regardless of your views on global warming, the unseasonably cold weather on the eastern half of the country had a severely negative impact on first half GDP (Gross Domestic Product). In fact, first quarter GDP was revised lower to a contraction of -2.9%. The good news is expectations are for an improved second half of the year according to Merrill Lynch.

While it would be wonderful to live in Utopia, unfortunately for investors, there is always uncertainty and risk. These elements come with the investing territory. Of course, you can always compensate for that unwanted uncertainty by accepting low interest-paying options (e.g., stuffing your money under a mattress, in a CD, savings account, Treasury bonds, etc.).

Despite the unexpected first half events, the market continues to grind higher. During the first half of the year, the S&P 500 index rose 6.1% (+1.9% in June); the Dow Jones Industrials edged higher by +1.5% (+0.7% in June); and the Nasdaq climbed +5.5% (+3.9% in June). But stocks weren’t the only winning investment team in town – bonds tasted victory during the first half also, notching gains of +2.8% (AGG – Aggregate Bond), almost double the Dow’s performance.

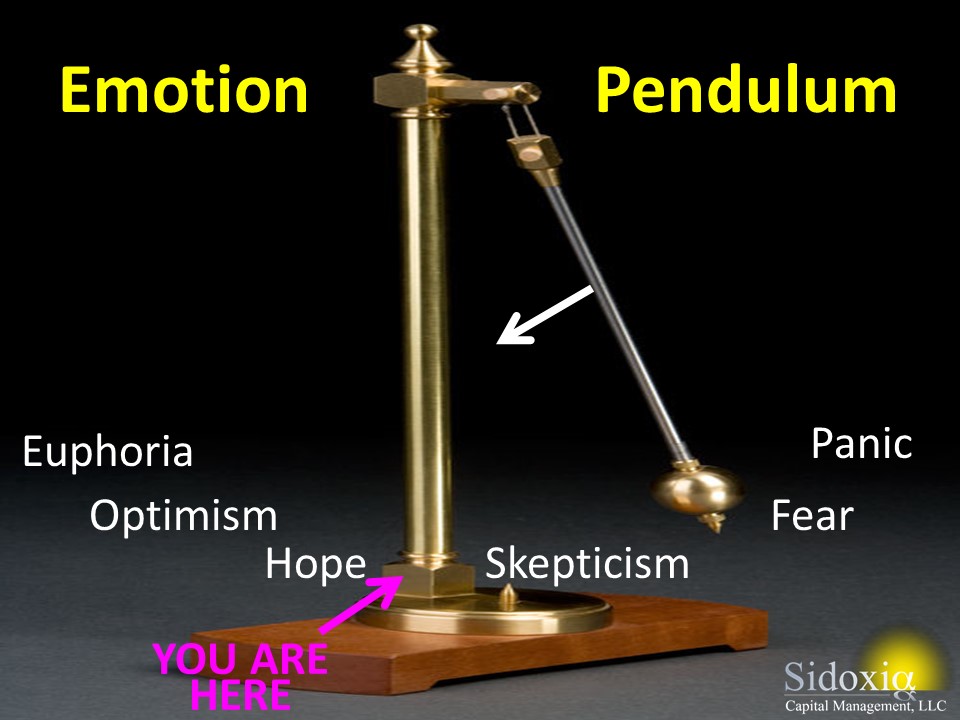

Investor Psyche Pendulum Swinging in Positive Direction

As I have written in the past, investor psyches continually swing along an emotional pendulum (see also Sentiment Pendulum article) from a state of “Panic” to “Euphoria”. While the pendulum has clearly swung in a positive direction, away from the emotional states of “Panic & Fear,” we appear to now be between “Skepticism & Hope.” The timing of when we get to the latter stages of “Optimism & Euphoria” is dependent on the pace of the economic recovery, risk appetites of consumers/businesses, and the trajectory of risky assets like stocks. Just because the ride has been fun for the last five years, does not mean the ride is over. However, as the pendulum continues to swing to the left, long-term investors need to fight the tempting urge to increase risk appetite just as the allure of high stock returns appears more achievable.

During the second half of this economic cycle, before the next recession, investors need to be more cognizant of controlling risk (the probability of permanent losses) by paying closer attention to valuations, diversification, and rebalancing too heavily weighted equity portfolios.

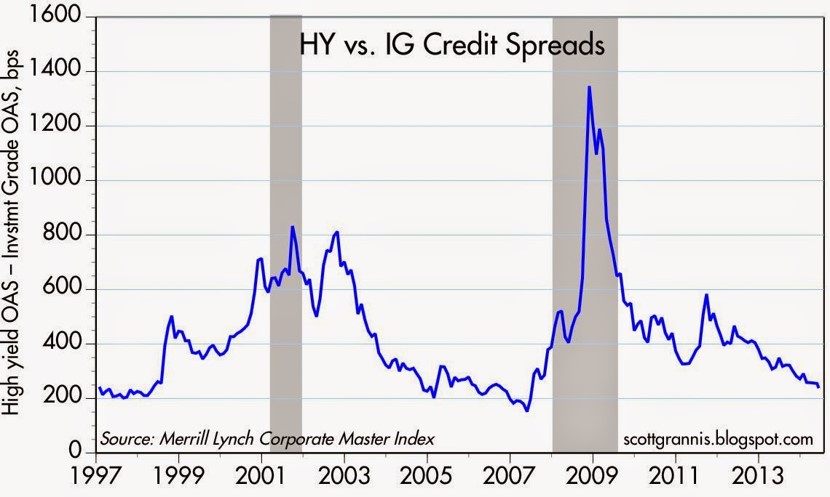

Besides rising stock prices and the beginning of positive fund flows, investors’ increasing appetite for risk is evidenced by the yield chasing occurring in junk bonds, which has raised prices of the lowest quality bonds to lofty levels. The chart below shows this phenomenon happening with the yields narrowing between high yield (HY) bonds and investment grade (IG) corporate bonds.

Source: Calafia Beach Pundit

Even though I pointed out a number of disconcerting surprises in the first half of the year, as you consider making halftime adjustments to your portfolios, do not forget some of the underlying positive currents that are leading to a winning halftime score.

Here are some of the constructive factors supporting stock prices, which have nearly tripled in value from the 2009 lows (S&P 500 – 666 to 1,960):

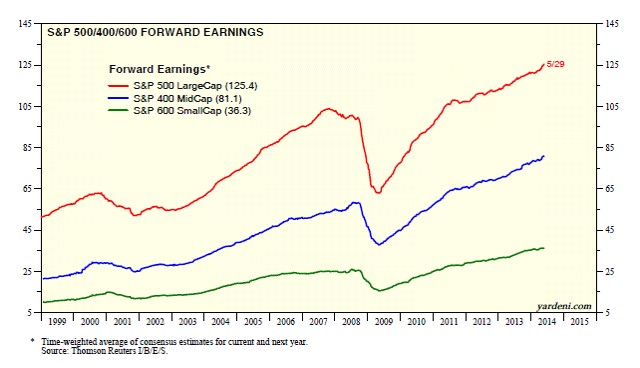

Record Corporate Profits: I constantly bump into skeptics who fail to realize the fundamental power of record profits driving stock prices higher (see chart below). As the late John Templeton stated, “In the long run, the stock market indexes fluctuate around the long-term upward trend of earnings per share.”

Source: Dr. Ed’s Blog

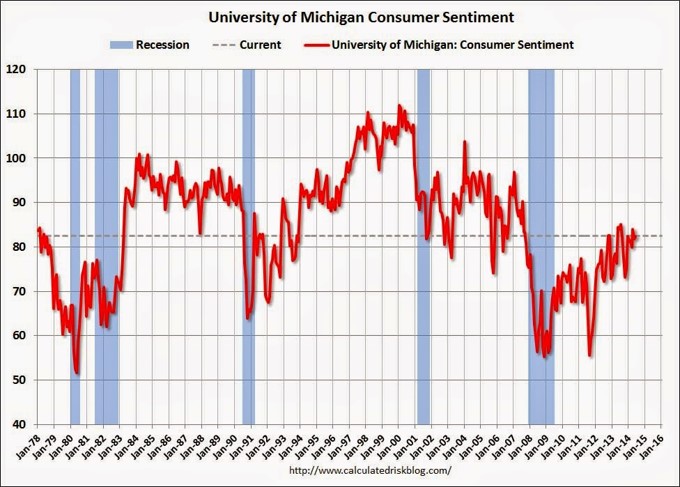

Improving Consumer Confidence: The University of Michigan consumer sentiment index increased to 82.5 for June from May. The confidence score came in above the consensus forecast of 82.0. Confidence has increased significantly from the 2009 lows but as the chart below shows, there is plenty of room for this metric to advance – consistent with the emotion pendulum discussed previously.

Source: Calculated Risk

Dividends & Share Buybacks Near Record Levels: A bird in the hand is worth two in the bush. Corporations have realized this investor desire and as a result companies are returning record levels of money (“capital”) to stock shareholders via increasing dividends and share buybacks (see chart below).

Source: Dr. Ed’s Blog

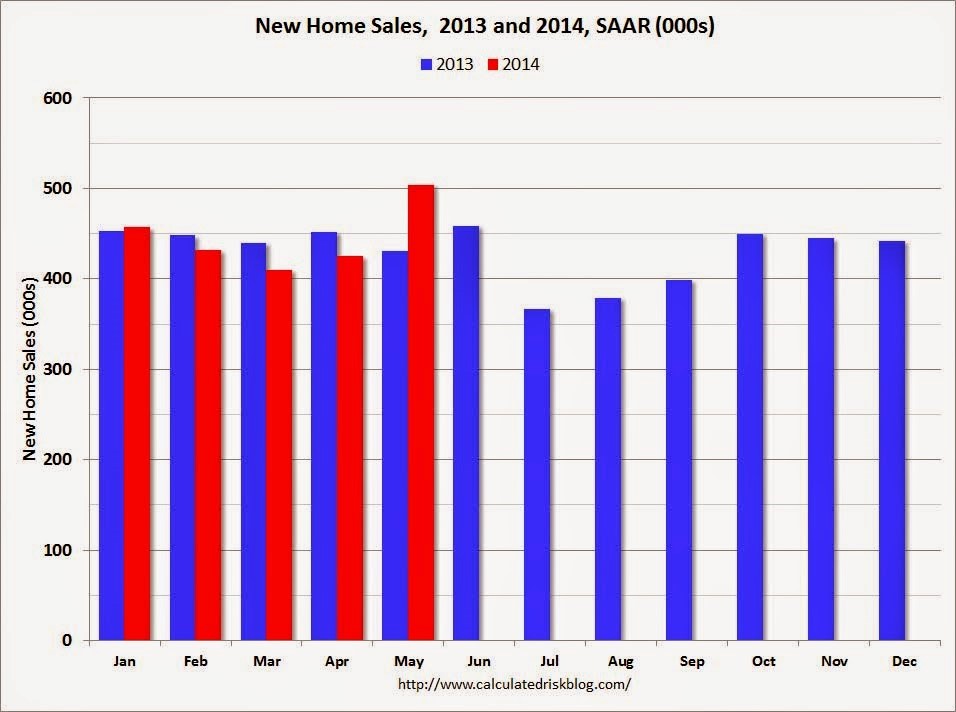

Housing on the Mend: The housing market has improved in fits and starts, but the most recent data point of new home sales shows significant improvement. More specifically, May’s new home sales were up +18.6% from the previous month (see chart below), the highest level seen since 2008. Although this data is encouraging, there is still plenty of room for improvement, as current sales remain more than 50% below 2005 peak levels.

Source: Calculated Risk

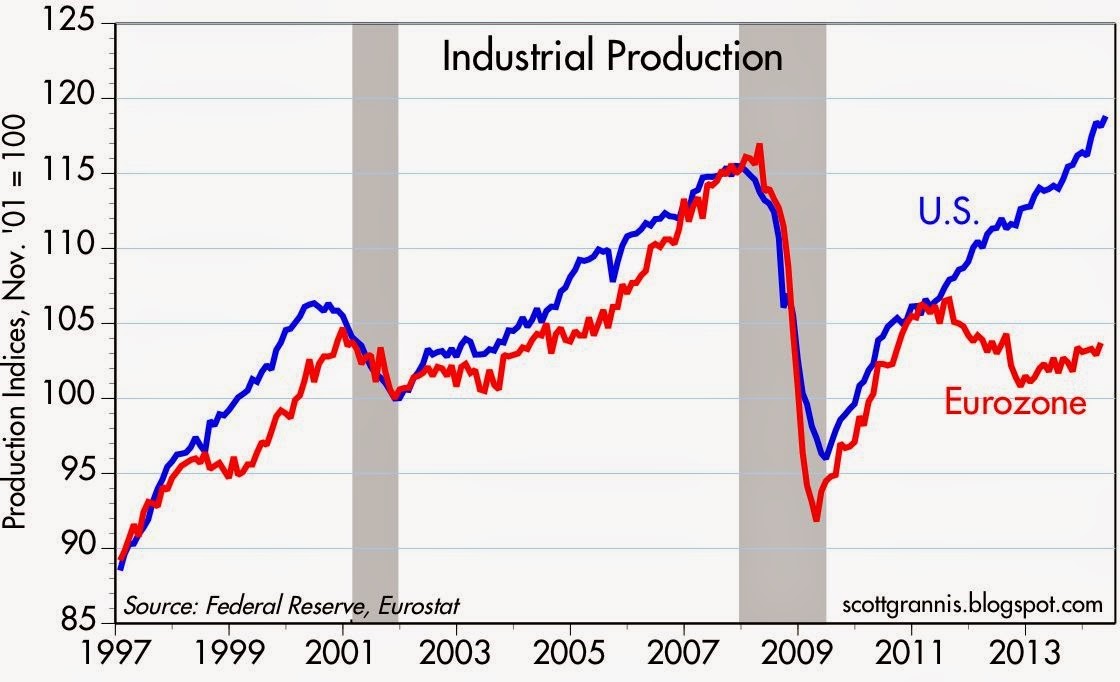

Record Industrial Production: Adding support to the improving economic outlook are the industrial production figures, which also hit a record (see chart below). This data also adds credence to why the U.S. stock market has outperformed the European markets during the economic recovery from 2009.

Source: Calafia Beach Pundit

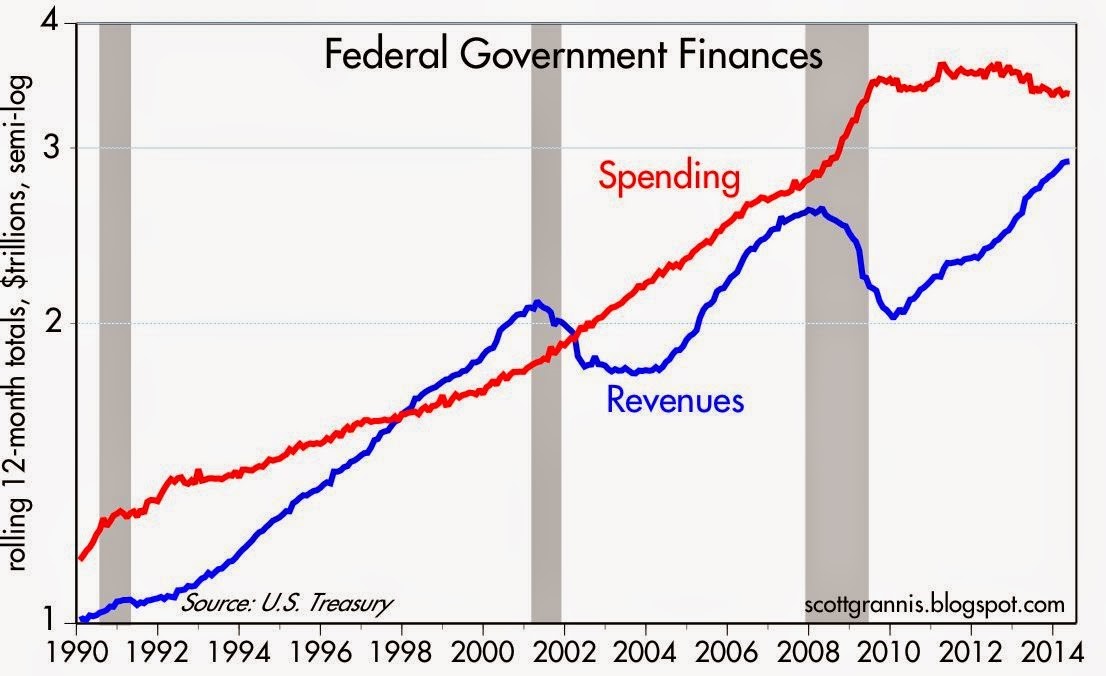

Declining Federal Deficit: The federal deficit continues to narrow (i.e., tax revenues growing faster than government spending), so previous fiscally panicked screams have quieted down. We’re not out of the woods yet, but the trends are encouraging (see chart below):

Source: Calafia Beach Pundit

There have been plenty of bombshells during the first half of 2014 (no pun intended), and there are bound to be plenty more during the second half of the year. By definition, nobody can be fully prepared for a surprise, or else it wouldn’t be called a “surprise”. For those skeptical investors sitting on the sidelines, the record breaking stock market performance has also been astonishing. Regardless of what happens over the next six months, periodically making adjustments to your financial plan is important, whether it’s during the pre-game, post-game, or halftime. And if you’re not interested or capable of making those adjustments yourself, find a professional advisor/coach to assist you.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds and AGG, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}