Archive for October, 2015

Out of the Woods?

In the middle of the 24/7 news cycle, many investors get distracted by the headline du jour, much like a baby gets distracted by a shiny new object. While investor moods have been swinging violently back and forth, October’s performance has bounced back like a flying tennis ball. So far, the reversal in the S&P 500 performance has more than erased the -9% correction occurring in August and September. Could we finally be out of the woods, or will geopolitics and economic factors scare investors through Halloween and year-end?

Given recent catapulting stock prices, investor amnesia has erased the shear horror experienced over the last few months – this is nothing new for emotional stock market participants. As I wrote in Controlling the Lizard Brain, human brains have evolved the almond-shaped tissue in our brains (amygdala) that controlled our ancestors’ urge to flee ferocious lions. Today the urge is to flee scary geopolitical and economic headlines.

I expanded on the idea here:

“When the brain in functioning properly, the prefrontal cortex (the front part of the brain in charge of reasoning) is actively communicating with the amygdala. Sadly, for many people, and investors, the emotional response from the amygdala dominates the rational reasoning portion of the prefrontal cortex. The best investors and traders have developed the ability of separating emotions from rational decision making, by keeping the amygdala in check.”

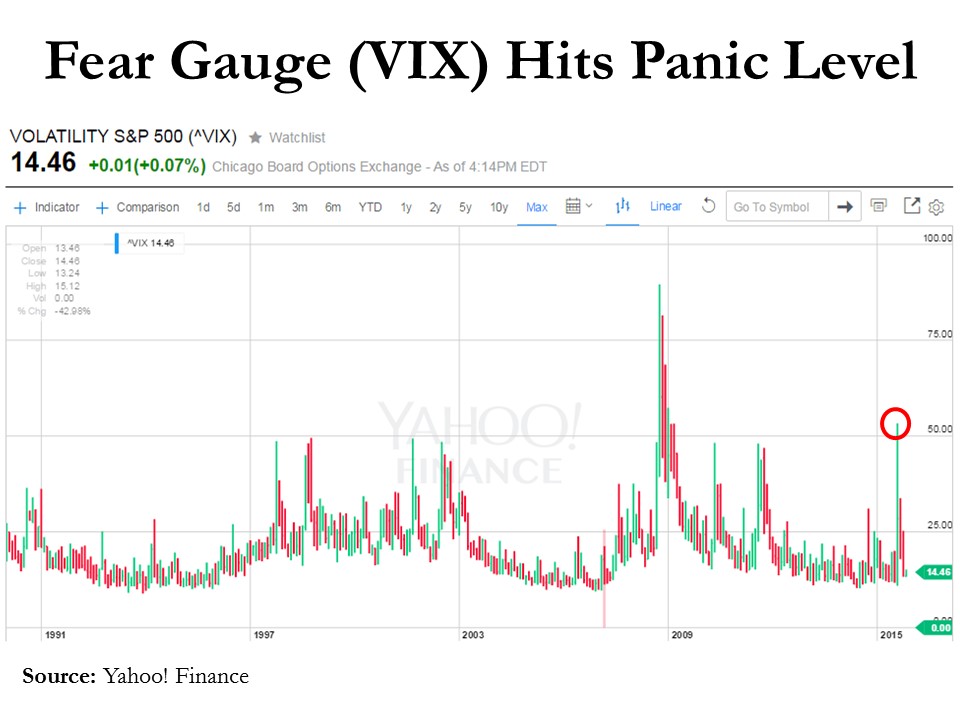

Evidence of lizard brains fear for flight happened just two months ago when the so-called “Fear Gauge” (VIX – Volatility Index) hit a stratospherically frightening level of 53 (see chart below), reached only once over the last few decades (2008-09 Financial Crisis).

Just as quickly as slowing China growth and a potential Fed interest rate hike caused investors to crawl underneath their desks during August (down –11% in four days), while biting their fingernails, investors have now sprung outside to the warm sunshine. The end result has been an impressive, mirror-like +11% increase in stock prices (S&P 500) over the last 18 trading days.

Has anything really changed over the last few weeks? Probably not. Economists, strategists, analysts, and other faux-soothsayers get paid millions of dollars in a fruitless attempt to explain day-to-day (or hour-by-hour) volatility in the stock markets. One Nobel Prize winner, Paul Samuelson, understood the random nature of stock prices when he observed, “The stock market has forecast nine of the last five recessions.” The pundits are no better at consistently forecasting stock prices.

As I have reiterated many times before, the vast majority of the pundits do not manage money professionally – the only people you should be paying attention to are successful long-term investors. Even listening to veteran professional investors can be dangerous because there is often such a wide dispersion of opinions based on varying time horizons, strategies, and risk tolerances.

Skepticism remains rampant regarding the sustainability of the bull market as demonstrated by the -$100 billion+ pulled out of domestic equity funds during 2015 (Source: ICI). The Volatility Index (VIX) shows us the low-hanging fruit of pessimism has been picked with the metric down -73% from August. With legislative debt ceiling and sequestration debates ahead in the coming weeks, we could hit some more choppy waters. Short-term volatility may resurrect itself, but the economy keeps chugging along, interest rates remain near all-time lows, and stock valuations, broadly speaking, remain reasonable. Investors may not be out of the woods yet, but one thing remains certain…an ever-changing stream of fearful headlines are likely to continue flooding in, which means we must all keep our lizard brains in check.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Fallibility of Tangibility

Why do so many star athletes end up going bankrupt? Rather than building a low-cost, tax-efficient, diversified portfolio of stocks and bonds that could help generate significant income and compounded wealth over the long-term (yawn…boring), many investors succumb to the allure of over-exposing themselves to costly, illiquid, tangible assets, while assuming disproportionate risk.

After all, it’s much more exciting to brag about the purchase of a car wash, apartment building or luxury condo than it is to whip out a brokerage statement and show a friend a bond fund earning a respectable 4% yield.

Many real estate investors in my Southern California backyard (epicenter of the 2008-2009 Financial Crisis) have experienced both ruin and riches over the last few decades. The appeal and pitfalls associated with owning tangible assets like real estate are particularly exemplified with professional athletes (see also Hidden Train Wreck). Consider the fate suffered by these following individuals:

- Mike Tyson: Famous boxer Mike Tyson tore through $300 million on multiple homes, cars, jewels and pet tigers before filing for bankruptcy in 2003.

- Julius Erving: Hall of Fame NBA player Julius “Dr. J” Erving went financially belly-up in 2010 after his Celebrity Golf Club International was pushed into foreclosure. Dr. J. was also forced to auction off coveted NBA memorabilia (including championship uniforms, trophies, and rings) along with foreclosing on his personal $2 million, 6,600-square foot Utah home.

- Mark Brunell: Pro Bowl quarterback Mark Brunell was estimated to have earned over $50 million during his career. Due to failed real estate ventures and business loans, Brunell filed for bankruptcy in 2010.

- Evander Holyfield: Heavyweight boxing champion Evander Holyfield burned through a mountain of money estimated at $230 million, including a 235-acre Utah estate, which had 109 rooms and included at least one monthly electric bill of $17,000.

Caveat Emptor

Inclusion of real estate as part of a diversified portfolio makes all the sense in the world – this is exactly what we do for clients at Sidoxia. But unfortunately, many investors mistake the tangibility of real estate with “lower risk,” even though levered real estate is arguably more volatile than the stock market – evidenced by the volatility in publicly traded REIT share prices. For example, the Dow Jones SPDR REIT (RWR) declined by -78% from its 2007 high to its 2009 low versus the S&P 500 SPDR (SPY) drop of -57% over the comparable period. Private real estate investors are generally immune from the heart-pumping price volatility rampant in the public markets because they are not bombarded with daily, real-time, second-by-second pricing data over flashing red and green colored screens.

Without experiencing the emotional daily price swings, many real estate investors ignore the risks and costs associated with real estate, even when those risks often exceed those of traditional investments (e.g., stocks and bonds). Here are some of the important factors these real estate investors overlook:

Leverage: Many real estate investors don’t appreciate that the fact that 100% of a 10% investment (90% borrowed) can be wiped out completely (i.e., lose -100%), if the value of a property drops a mere -10%. Real estate owners found this lesson out the hard way during the last housing downturn and recession.

Illiquidity: Unlike a stock and bond, which merely takes a click of a mouse, buying/selling real estate can take weeks, if not months, to complete. If a seller needs access to liquidity, they may be forced to sell at unattractively low, fire-sale prices. Pricing transparency is opaque due to the variability and volume of transactions, although online services offered by Zillow Group Inc. (Z).

Costs: For real estate buyer, the list of costs can be long: appraisal fee, origination fee, pre-paid interest, pre-paid insurance, flood certification fee, tax servicing fee, credit report fee, bank processing fee, recording fee, notary fee, and title insurance. And once an investment property is officially purchased, there are costs such as property management fees, property taxes, association dues, landscaping fees and the opportunity costs of filling vacancies when there is tenant turnover. And this analysis neglects the hefty commission expenses, which generally run 5-6% and split between the buying and selling agent. Add all these costs up, and you can understand the dollars can become significant.

Concentration Risk: It’s perfectly fine to own a levered, cyclical asset in a broadly diversified portfolio for long-term investors, but owning $1.3 million of real estate in a $1.5 million total portfolio does not qualify as diversified. If a portfolio is real estate heavy, hopefully the real estate assets are at least diversified across geographies and real estate type (e.g., residential / commercial / multi-family / industrial / retail mall / mortgages / etc).

Stocks Abhorred, Gold & Real Estate Adored

With the downdraft in the stock market that started in late August, a recent survey conducted by CNBC showed how increased volatility has caused wealthy investors to sour on the stock market. More specifically, the All-America Survey, conducted by Hart-McInturff, polled 800 wealthy Americans at the beginning of October. Unsurprisingly, many investors automatically correlate temporary weakness in stocks to a lagging economy. In fact, 32% of respondents believed the U.S. economy would get worse, a 6% increase from the last poll in June, and the highest level of economic pessimism since the government shutdown in 2013 (as it turned out, this was a very good time to buy stocks). These gloom and doom views manifested themselves in skeptical views of stocks as well. Overall, 46% of the public felt it is a bad time to invest in stocks, representing a 12% gain from the last survey.

With investor appetites tainted for stocks, hunger for real state has risen. Actually, real estate was the top investment choice by a large margin, selected by 39% percent of the investors polled. Real estate has steadily gained in popularity since the depths of the recession in 2008. Jockeying for second place have been stocks and gold with the shiny metal edging out stocks by a score of 25% to 21%, respectively.

Successful long-term investors like Warren Buffett understand the best returns are earned by going against the grain. As Buffett said, “Be fearful when others are greedy and greedy when others are fearful,” and we know stock investors are fearful. Along those same lines, Bill Miller, the man who beat the S&P 500 index for 15 consecutive years (1991 – 2005), believes now is a perfect time to buy stocks. Investing in real estate is not a bad idea in the context of a diversified portfolio, but investors should not forget the fallibility of tangibility.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) including SPY, but at the time of publishing, SCM had no direct position in Z, RWR, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

E.M.s Want Cake & Eat It Too

Since the end of 2010, the emerging markets (E.M.) have gotten absolutely obliterated (MSCI Emerging Markets index –25%) compared to a meteoric rise in U.S. stocks (S&P 500 index +60%) over the same period.

Source: Financial Times

Slowing global growth, especially with resource-hungry China going on a crash diet, has caused commodity-exporting emerging markets like Brazil to suffer economic starvation. Rising inflation, expanding debt, decelerating Chinese growth, collapsing commodity prices, and political corruption allegations are all factors pressuring the Brazilian economy. Weak emerging market economies like Brazil are contributing to global GDP forecast reductions. As you can see from the chart below, global GDP growth rates have been steadily declining since 2010, and the IMF recently lowered their 2015 forecast from +3.5% down to 3.1%.

Source: Financial Times

Beginning in late 2008, when Ben Bernanke first announced his QE 1 (Quantitative Easing) money printing binge, the U.S. dollar remained relatively weak against other global currencies for years. The weak dollar provided a nice tailwind to U.S. exporters (i.e., American manufactured goods were more cost competitive for foreign buyers).

Multinationals loved the export lift, but emerging international politicians and investors cried foul. They complained the U.S. was starting a “currency war” by artificially deflating the value of the U.S. dollar, thereby making international markets less competitive. At the time, the thought process was the emerging markets (e.g., China, Russia, Brazil et.al.) would be disproportionately impacted because their economies are export-driven. In a 2010 article from the Guardian (World Gripped by International Currency War) Brazilian finance minister Guido Mantega explicitly stated, “We’re in the midst of an international currency war, a general weakening of currency. This threatens us because it takes away our competitiveness.”

This “currency war” griping stayed in place until the end of 2013 when the Fed announced its plans to begin “tapering” bond buying (i.e., pull away the financial punch bowl). We all know what has happened since then…the U.S. dollar has spiked by about +20% and the Brazilian real has depreciated by a whopping -37%. This is good news for emerging markets like Brazil, right? Wrong!

A few years ago, emerging market investors were initially worried about the depressing effects of a strong currency on exports, but now that emerging market currencies have depreciated, fears have shifted. Now, investors are concerned whether E.M. countries can pay off foreign borrowed debt denominated in pricey U.S. dollars (paid with vastly weaker E.M. currencies). Moreover, with foreign governments holding dramatically lower valued currency, investors are worried about the ability of these E.M. countries to raise additional capital or refinance existing debt. SocGen’s head of emerging market strategy, Guy Stear, summed it up by noting, “Prevailing risks of a deterioration of the external financing environment and disruptive capital flow and asset price shifts that increase volatility in the respective bond and currency markets, make a rapid rebound in EM growth over the next months unlikely.”

So which one is it…do E.M. investors want a weak currency to power exports, or a strong currency to pay down debt and raise additional capital? Unfortunately, investors can’t have their cake and eat it too – you can’t have a depreciating and appreciating currency at the same time.

While anxiety has shifted from strong emerging market currencies to the issues associated with weak currencies, India is one E.M that has reaped the rewards from a declining rupee (-20% since 2013). In other words, India is benefiting from a stronger trade balance via a boost in exports and reduction in imports – interestingly, the U.S. has experienced the exact opposite. Regardless, eventually, other emerging markets will benefit from these same positive trends as India – that will finally be a tasty slice of cake.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) including EWZ, but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Marathon Market Gets a Cramp

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (October 1, 2015). Subscribe on the right side of the page for the complete text.

“Anyone can run a hundred meters, it’s the next forty-two thousand and two hundred that count.”

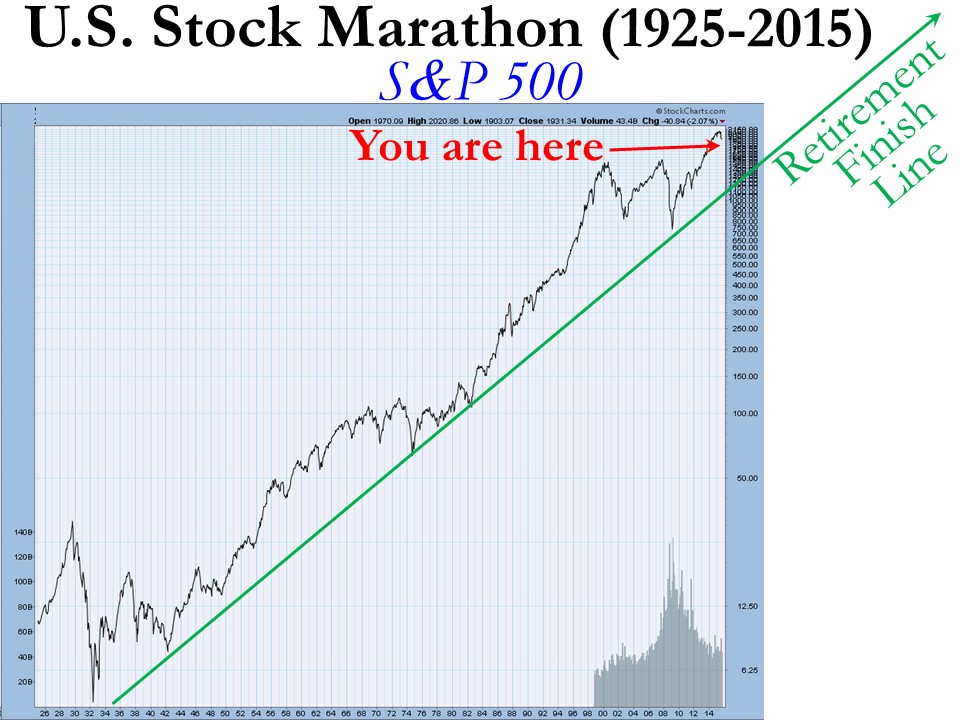

Investing is a lot like running a marathon…but it’s not a sprint to the retirement finish line. The satisfaction of achieving your long-term goal can be quite rewarding, but attaining ambitious objectives does not happen overnight. Along the hilly and winding course, there can be plenty of bumps and bruises mixed in with the elation of a runner’s high. While stocks have been running at a record pace in recent years, prices have cramped up recently as evidenced by the -2.6% decline of the S&P 500 stock index last month.

But the recent correction should be placed in the proper perspective as you approach and reach retirement. Since the end of the 2008 Financial Crisis the stock market has been racing ahead at a brisk rate, as you can see from the total return performance below (excluding 2015):

This performance is more indicative of a triumph than a catastrophe, but if you turned on the TV, listened to the radio, or surfed the web, you may come to a more frightening conclusion.

What’s behind the recent dip? These are some of the key concerns driving the recent price volatility:

- China: Slowing growth in China and collapse in Chinese stock market. China is suffering from a self-induced slowdown designed to mitigate corruption, prick the real estate bubble, and shift its export-driven economy to a more consumer-driven economy. These steps diminish short-term growth (albeit faster than U.S. growth), but nevertheless the measures should be constructive for longer-term growth.

- Interest Rates: Uncertainty surrounding the timing of a 0.25% target interest rate increase by the Federal Reserve. The move from 0% to 0.25% is like walking from the hardwood floor onto the rug…hardly noticeable. The inevitable move by the Fed has been widely communicated for months, and given where interest rates are today, the move will have a negligible impact on corporate borrowing costs. Like removing a Band-Aid, the initial action may cause some pain, but should be comfortably received shortly thereafter.

- Politics: Potential government shutdown / sequestration. The epic political saga will never end, however, as I highlighted in “Who Said Gridlock is Bad?,” political discourse in Washington has resulted in positive outcomes as it relates to our country’s fiscal situation (limited government spending and declining deficits). The government shutdown appears to have been averted for now, but it looks like we will be blanketed with brinkmanship nonsense again in a few months.

- Biotech/Pharmaceuticals: Politics over lofty drug prices and the potential impact of future regulation on the biotech sector. Given the current Congressional balance of power, any heavy-handed Democratic proposals is likely to face rigorous Republican opposition.

- Emerging Markets: Emerging market weakness, especially in Latin America (e.g., Brazil). These developments deserve close monitoring, but the growth in the three largest economic regions (U.S., Europe, and China) will have a much larger effect on the direction of global economic expansion.

- Middle East: Destabilized Middle East and Syria. Terrorist extremism and cultural animosity between various Middle East populations has existed for generations. There will be no silver bullet for a peaceful solution, so baby steps and containment are critical to maintain healthy global trade activity with minimal disruptions.

Worth noting, this current list of anxieties itemized above is completely different from six months ago (remember the Greece crisis?), and the list will change again six months into the future. Investing, like any competitive challenge, does not come easy…there is always something to worry about in the land of economics and geopolitics.

Here’s what the world’s top investor Warren Buffett said a few decades ago (1994) on the topic of politics and economics:

“We will continue to ignore political and economic forecasts which are an expensive distraction for investors and businessmen. Thirty years ago, no one could have foreseen the huge expansion of the Vietnam War, wage and price controls, two oil shocks, the resignation of a president, the dissolution of the Soviet Union, a one-day drop in the Dow of 508 points, or treasury bill yields fluctuating between 2.8% and 17.4%.”

In a world of 7.3 billion people and 196 countries there will never be a shortage of fear, uncertainty, and doubt (F.U.D.) – see events chart in The Bungee Market. In an ever-increasing, globally connected world, technology and the media continually amplify molehills into mountains, thereby making the next imagined Armageddon a simple click of a mouse or swipe of a smartphone away.

Today’s concerns are valid but in the vast majority of cases the issues are completely overblown, sensationalized and over-emphasized without context. Context is an integral part to investing, but unfortunately context usually cannot be explained in a short soundbite or headline. On the flip side, F.U.D. thrives in the realm of soundbites and headlines.

While investors may feel fatigued from a strong flow of headline headwinds, financial market race participants should take a break at the water stop to also replenish themselves with a steady tailwind of positive factors, including the following:

- Employment: The unemployment rate has been cut from a recession peak of 10.0% down to 5.1%, and the economy has been adding roughly +200,000 new monthly jobs on a fairly consistent basis. On top of that, there are a record 5.8 million job openings versus 3.7 million two years ago – a sign that the economy continues to hum along.

- Housing/Commercial Real Estate/Mortgage Rates: Housing prices have rebounded by about +30% from the 2012 lows; Housing starts have increased by +25% in the past year and 120% in the past four years; and 30-Year Fixed mortgage interest rates sit at 3.85% – a highly stimulative level within a spitting distance from record lows.

- Auto Sales: Surged to a post-recession record of 17.8 million units in August.

- Interest Rates: Massively stimulative and near generational lows, even if the Fed hikes its interest rate target by 0.25% in October, December or sometime in 2016.

- Capital Goods Orders: Up for three consecutive months.

- Rail Shipments/Truck Tonnage: Both these metrics are rising by about 3-4%.

- Retail Sales: Rising at a very respectable pace of 7% over the last six months.

- Low Energy & Commodity Prices: Inflation has remained largely in check thanks to plummeting commodity prices. Low oil and gas prices are benefiting consumers in numerous ways, including the contribution to car sales, home sales, and/or debt reduction.

While the -10% dip in stock prices from mid-August might feel like a torn knee ligament, long-term investors know -10% corrections historically occur about one-time per year, on average. So, even though you may be begging for a wheelchair, the best course of action is to take a deep breath, stick to your long-term investment plan, rebalance your portfolio if necessary, and continue staying on course towards your financial finish line.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) , but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}