Posts tagged ‘social security’

Can You Retire? Getting to Your Number

What’s “your number?” The catchy phrase has been tried on 30-second television commercials before, but the fact remains, most Americans have no clue how much they need to save for retirement. The ever-shifting and imprecise variables needed to compute the size of your needed nest egg can seem overwhelming: lifespan; career span; inflation; college tuition; healthcare expenses; rising insurance costs; social security; employer benefits; inheritance; child support; parental support; etc. The list goes on and with near-zero interest rates, and stock prices at record highs, the retirement challenge has only gotten riskier and more difficult.

I understand this task may not be easy and could eat into your House of Cards viewing, Candy Crush playing, or football watching. However, if you can spend two weeks planning a family vacation, you certainly can afford devoting a few hours to scribbling down some numbers as it relates to the lifeblood of your financial future. The project is definitely doable.

Here are some key steps to finding “your number.” If you’re not single, then calculate the figures for your household:

1). Calculate Your Budget: Where to start? A good place to begin is with is a boring budget (or your monthly expenses). The budget does not need to be down to the penny, but you should be able to estimate your monthly spend with the help of your bank and credit card statements. Make sure to include estimates for periodic unforeseen potential expenses like annual auto repairs, home repairs, or emergency hospital visits. Once you determine your monthly spend, extrapolating your annual spend shouldn’t be too difficult.

2). Compute Your Income: Your sources of income should be fairly straightforward. For most people this includes your salary and potential bonus. Some people will also generate income from investments, a business, and/or real estate. Before getting too excited about all the income you are raking in, don’t forget to subtract out taxes collected by Uncle Sam, and include a possible scenario of rising tax rates during your working years. Obviously, the economy can also have a positive or negative impact on your income projections, nevertheless, if you conservatively plan for some potential future setbacks, you will be in a much better position in forecasting the amount of savings needed to reach “your number.”

3). Planned Retirement Date: The date you pick may or may not be realistic, but by choosing a specific date, you can now evaluate how much savings will be necessary to reach your required nest egg number. The difference between your annual income (#2) and annual budget (#1) is your annual savings, which you can multiply by the number of years you plan to work until retirement. For example, assume you wanted to retire 15 years from now and were able to save/invest $20,000 each year while earning a 6% annualized return. By the year 2030 these savings would equate to about $465,000 and could be added to any other savings and other retirement income (pension, 401(k), Social Security, inheritance, etc.) to meet your retirement needs.

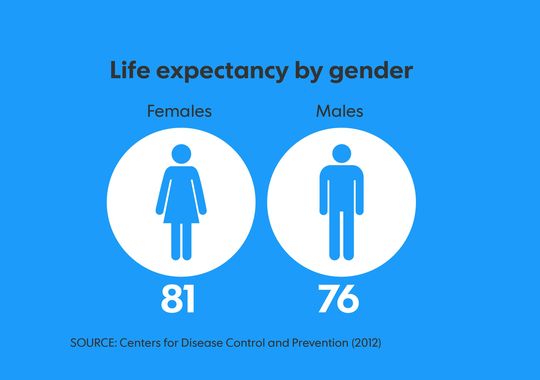

4). Life Expectancy: After you have determined when you want to retire, now comes the tricky part. How long are you going to live? Assuming you are currently healthy, you can use actuarial tables for life expectancy. According to a new report on American mortality from the Centers for Disease Control and Prevention’s National Center for Health Statistics, the average life expectancy is 81 for females and 76 for males (see graphic below). The estimates are a little rosier, if you have lived to age 65, in which case females are expected to live past 85 years old and males to about 83 years. You can adjust these figures higher or lower based on personal information and family history, but if you consider yourself “average,” then you better plan to have at least 15 years of fire power in your savings nest egg (see example at bottom of article).

Source: USA Today

Empty Retirement Wallets & Purses

The harsh realities are Americans are not saving enough. It‘s true, you can survive off a smaller nest egg, if you plan to live off of cat food and vacation in Tijuana, but most Americans and retirees have become accustomed to a higher standard of living. A New York Times article highlighted that 75% percent of Americans nearing retirement age had less than $30,000 in their retirement accounts – that’s not going to buy you that winter home on Maui or leave enough to cover your golf dues at the local country club.

Control the things that make a difference.

- Save. Pay yourself first by tucking money away each month. If you haven’t established an IRA (Individual Retirement Account) or savings account, make sure you contribute to your employer’s matching 401(k) plan to the fullest extent possible, if available. This is free money your employer is offering you and by not participation you are shooting yourself in the foot.

- Spend prudently. Review your monthly / annual budgets and determine where there is room to cut expenses. Every budget has fat in it, so it’s just a matter of cutting excessive and less important items, without sacrificing dramatic changes to your standard of living.

- Manage your career. Invest in yourself with education, apply for that promotion, or look for other employment alternatives if you are unhappy or not being paid your proper value.

- Push Retirement Out: If you are healthy and enjoy your work, extending your working years can have profoundly positive benefits to your retirement. Not only will you have more money saved up for retirement, but you will also receive higher Social Security benefits by delaying retirement (see Social Security benefit estimator).

The bottom-line is if you are like most working Americans, you will need to save more and invest more prudently (e.g., in a low-cost, tax-efficient manner like strategies offered by Sidoxia).

Use Your Thumb to Get Started

Rules of thumb are never perfect, but are not a bad place to start before fine-tuning your estimates. Some retirement pundits begin by using an 80% “income replacement ratio” rule as a retirement guide. In other words, you should not need 100% of your pre-retirement income during retirement because a number of your major living expenses should be reduced. For example, during retirement your tax expenses should decrease (because you are not working); your mortgage payment should be lower (i.e., house is paid off); your kids should be independent and off the family payroll; and you may be in the position to downsize your home (e.g., empty-nesters often decide to move to a lower square footage residence).

Another rule of thumb is the “15x Rule,” which says you will need an investment account equivalent to at least 15-times your pre-retirement income. Therefore, if your after-tax income is $100,000 before retirement and you need to replace $80,000 during retirement (80% replacement ratio), this means you actually only need to replace about $60,000 per year. We arrive at the lower $60,000 figure by further assuming the $80,000 can be reduced by about $20,000 flowing in annually from Social Security. Through the mighty powers of division, we can then apply the 4% Sustainable Withdrawal Rate rule (SWR) to reverse engineer the estimate of “our number.” In this example, our ultimate nest egg needed is $1,500,000 (equal to $60,000 / 4% or $60,000 x 25 years), which is estimated to last for 25 years of retirement. As you can see, there are quite a few assumptions baked into this scenario, including a retirement investment portfolio that beats inflation by 4%, but nevertheless this line of thinking creates an understandable framework to operate under.

Of course, for all the non-math Investing Caffeine readers, life could have been made easier by simply multiplying the $100,000 pre-retirement income by 15x to arrive at our $1.5 million nest egg. More elegant, but less fun for this nerdy math author.

We’ve covered a lot of ground, but I’m absolutely confident if you have read this far, you can definitely come up with “your number.” If this all seems too overwhelming, there is no need to worry, just find an experienced investment advisor or financial planner…I’m sure I could help you find one 🙂 .

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Retirement Epidemic: Poison Now or Later?

We live in an instant gratification society. The house, the car, and annual vacation take precedence over contributions to retirement and savings accounts. It therefore comes as no surprise to me that Americans spend more time on planning for vacation than they do on planning for retirement.

Given the choice of spending or saving, Americans in large part choose, “spend now, save later.” Or in other words, Americans choose to drink $10 margaritas now (spend) and swallow the more expensive poison (save) later. Spending now and saving later sounds good in theory until you reach your mid-60s and realize you’re going to have to work as a Wal-Mart Stores (WMT) greeter into your 80s while eating cat food in your tent.

To make matters worse, you don’t have to be a genius to see irresponsible government spending and globalization has compromised the health of our countries entitlements (Social Security and Medicare). Benefits are likely to be reduced over time and age eligibility requirements are likely to increase. If you fold in the dynamic of exploding healthcare costs and broad-based inflationary pressures, one can quickly realize savings habits need to change. The traditional model of working for 40 years and then relying on a pension and Social Security payments to cover a blissful multi-decade retirement just doesn’t apply to current reality. On top of the disappearance of plump pensions, life expectancy is rising (around 80 years in the U.S.), so the realistic risk of outliving your savings has a larger probability of occurring.

Surely I am overly dramatizing the situation by sounding the investing alarm bells out of self-interest…right? Wrong. As a geeky, financial numbers guy, I can objectively rely on numbers, and the statistics aren’t pretty.

Here’s a sampling:

- Empty Savings Cupboard: A 2013 study by the Employee Benefit Research Institute found that nearly half of workers had less than $10,000 saved, and according to Blackrock Inc (BLK), CEO, Larry Fink, the average American has saved only $25,000 for retirement

- Food Stamp Living: Almost half of middle-class workers, will be forced into a poor retirement lifestyle, living on a food budget of about $5 a day.

- 401(k) Will Not Save the Day: Compared to other forms of savings, the average 401(k) balance reached $89,300 at the end of 2013 – that’s the good news. The bad news is that only about half of all companies offer their employees 401(k) benefits, and for the approximately 60 million people that participate, about a fourth withdraw these 401(k) funds before retirement – out of necessity or for frivolous reasons. Even if you cheerily accept the size of the average balance, sadly this dollar amount is still massively deficient in meeting retirement needs. It’s believed that your savings should approximate 15-20 times your annual retirement expenses that aren’t covered by outside sources of income, such as social security or a pension.

If these figures aren’t scary enough to get you saving more, then just use common sense and understand the future is very uncertain. A 2012 New York Times article sarcastically captured how easy it is to plan for retirement:

First, figure out when you and your spouse will be laid off or be too sick to work. Second, figure out when you will die. Third, understand that you need to save 7 percent of every dollar you earn. (30 percent of every dollar [if you are 55 now].) Fourth, earn at least 3 percent above inflation on your investments, every year. (Easy. Just find the best funds for the lowest price and have them optimally allocated.) Fifth, do not withdraw any funds when you lose your job, have a health problem, get divorced, buy a house or send a kid to college. Sixth, time your retirement account withdrawals so the last cent is spent the day you die.

What to Do?

The short answer is save! Simplistically, this can be achieved in one of two ways: cut expenses or raise income. I won’t go into the infinite ways of doing this, but adjusting your mindset to live within your means is probably the first necessary step for most.

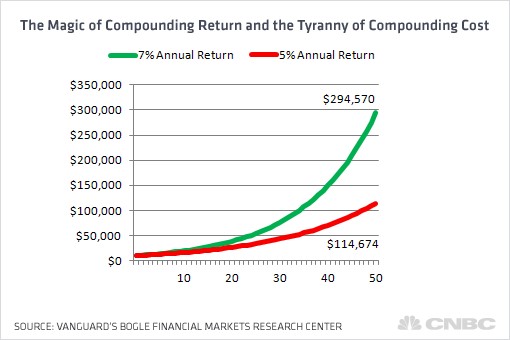

As it relates to your investments, fees should be your other major area of focus. The godfather of passive investing, Jack Bogle, highlighted the dramatic impact of fees on retirement savings. As you can see from the chart below, the difference between making 7% vs. 5% over an investing career by reducing fees can equate to hundreds of thousands of dollars, and prevent your nest egg from collapsing 2/3rd in value.

Source: CNBC

Lastly, if you are going to use an investment advisor, make sure to ask the advisor whether they are a “fiduciary” who legally is required to place your interests first. Sidoxia Capital Management is certainly not the only fiduciary firm in the industry, but less than 10% of advisors operate under this gold standard.

Investing and saving is a lot like dieting…easy to understand the concept but difficult to execute. The numbers speak for themselves. Rather than dealing with a crisis in your 70s and 80s, it’s better to take your poison now by investing, and reap the rewards of your hard work during your golden years.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds (ETFs), and WMT, but at the time of publishing SCM had no direct discretionary position in BLK, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

USA Inc.: Buy, Hold or Sell?

If the U.S. was a company, would you buy, hold, or sell the stock? A voluminous report put out last year by Mary Meeker sought to answer that very question. Since we’re in the thick of the presidential elections, why not review the important financial state of our great nation.

For those of you who may not know who she is, Mary Meeker is the well-known partner at Kleiner Perkins Caufield & Byers, who is also affectionately known as the “Queen of Internet.” Apparently, beyond her renowned expertise in analyzing and valuing tech companies and start-ups, she also has the knack of dissecting government statistics and distilling wonky numbers down to understandable terms for the masses. “Distilling” may be a generous term, given the massive size of her 460-page report, USA Inc., but nevertheless, I am going to attempt to synthesize this gargantuan report even further.

As a visual learner, I think some key cherry-picked slides from her report will help put our multi-trillion debts and deficits in context, so here goes…

The Scope of the Problem

If one spends a few hundred billion dollars here, and a few hundred billion dollars there, before you know it, a trillion dollars will have piled up. Currently our government has run $1 trillion+ budget deficits for three years, and the estimated deficit is for another trillion dollar deficit this fiscal year. If you have ever wondered how many football fields it takes to fill with a trillion dollars of cash, then today is your lucky day. The answer: 217 football fields.

Financial Statements: The Health Thermometer

In order to determine the relative health of USA Inc., Meeker created financial statements for our country, starting with the income statement. As you can see from the chart below, unfortunately USA Inc.’s expenses have been significantly larger than its revenues, creating a “discouraging” trend of negative cash flows (deficits). An entity that takes in $2.2 trillion in revenue and spends $3.5 trillion, cannot sustainably continue this trend for long, before significant financial problems arise. The largest contributing factor to our country’s losses (deficits) has been the exploding costs of entitlements, including Medicare, Medicaid, and Social Security.

As the pie chart shows, the major categories of entitlements comprise a whopping 58% of USA Inc.’s 2010 total expenditures.

Trillion dollar deficits have been the norm over the last three years.

Why Entitlement Spending is a Problem

Why are entitlements such a massive problem? The plain and simple answer to why entitlements are a major issue is that government expenditures are growing too fast. You can’t have expenses growing significantly faster than revenues for 45 years and expect to be in happy financial place.

Another reason for the abysmal spending record is due to politicians horrendous forecasting abilities. Future promises are made by politicians to garner votes today, and when they make overly rosy estimates about the costs of those promises, future generations are left holding the underfunded bag. Meeker points out that when Medicare was instituted in 1966, total future spending of $110 billion turned out to be about 10x more expensive (see chart below) than originally planned…ouch!

No Defense for Defense

Trillion dollar deficits and debts can’t be solely blamed on entitlements, but $700 billion in annual defense expenditures is not exactly chump change. The inopportune timing of the financial crisis in 2008-2009 didn’t help either, while two unfunded wars were being fought. Even if you strip out the wars, defense spending is still obscenely high. Given our poor state of financial affairs, we cannot afford to be the globe’s babysitter (see Impoverished Global Babysitter). Legacy Cold War spending on obsolete ground warfare needs to be reprioritized to 21st Century threats (i.e. focus on unmanned drones and coordinated intelligence). When a government spends more than the top 25 countries combined (see chart below), that country can certainly find some defense fat to trim.

Demographic Headwinds

The out-of-control gluttonous government spending is a threat to our national security, and although I wish I could say time alone will heal our fiscal wounds, unfortunately the opposite is true. Time is our enemy because the ticking demographic time bomb is about to explode, unless government acts to solve our spending problems. For starters, Americans are living longer, which means entitlement spending has accelerated faster than revenues collected, and life expectancy consistently continues to rise. As you can see below, life expectancy has outpaced Social Security age adjustments by +23% over a 74 year period.

Another self inflicted problem contributing to our colossal health care costs is the obesity epidemic. Over an 18 year period, the rate of obesity more than doubled to 32%. Individuals can and should shoulder more of the burden for these belt-busting costs, and government should spend more on prevention and education in this area. Bad drivers pay higher premiums for their auto insurance, so why not have bad eaters pay higher premiums? Genetics certainly can play a role in obesity, but so to do eating habits. The same accountability principle should be applied to smokers who overly burden our healthcare system too.

The USA spends more on healthcare than all OECD countries combined and 3x the OECD per capita average, yet as you can see from the chart below, the USA is not getting a life expectancy bang for its buck. The argument that the U.S. has the best healthcare in the world may be true in some instances, but the overall data doesn’t support that assertion.

The Rubber Hits the Road

The problem is easy to identify: Government spending going out the door is running faster than the revenues coming in via taxes. The solution is easy to identify too: Politicians need to cut spending, increase taxes, and/or do a combination of the two options. Like dieting, the solutions are easy to identify but difficult to execute.

Source: Calafia Beach Pundit – Scott Grannis

Almost everyone wants the government to spend less, but at the same time nobody wants their benefits cut. You can’t have your cake and eat it too. Citing two different studies, Meeker shows how 80% of Americans want a balanced budget as a national priority, but only 12% are willing to cut spending on Medicare and Social Security.

The rubber will hit the road in the next few months when politicians in a post-presidential election period will be forced to face these difficult “Fiscal Cliff” choices – $700 billion+ in tax hikes and spending increases that jeopardize the current recovery and our fiscal future.

Source: PIMCO

As market maven Mary Meeker recognizes, our fiscal situation is quite “discouraging”. With that said, although USA Inc. may have earned a current “Sell” rating, Meeker acknowledges that our country can become a positive turnaround situation. If voters actively push politicians to making difficult but necessary financial decisions to lower deficits and debt, investors around the globe will be ready to “Buy” USA Inc.’s stock.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct positions in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Securing Your Bacon and Oreo Future

Stuffing money under the mattress earning next to nothing (e.g., 1.3% on a on a 1-year CD or a whopping 1.59% on a 5-year Treasury Note) may feel secure and safe, but how protected is that mattress money, when you consider the inflation eating away at its purchasing power?

We’ve all been confronted by older friends and family members proudly claiming, “When I was your age, (“fill in XYZ product here”) cost me a nickel and today it costs $5,000!” Well guess what…you’re going to become that same curmudgeon, except 20 or 30 years from now, you’re going to replace the product that cost a “nickel” with a “$15 3-D movie,” “$200 pair of jeans” and “$15,000 family health plan.” Chances are these seemingly lofty priced products and services will look like screaming bargains in the years to come.

The inflation boogeyman has been relatively tame over the last three decades. Kudos goes to former Federal Reserve Chairman Paul Volcker, who tamed out-of-control double-digit inflation by increasing short-term interest rates to 20% and choking off the money supply. Despite, the Bernanke printing presses smoking from excess activity, money has been clogged up on the banks’ balance sheets. This phenomenon, coupled with the debt-induced excess capacity of our economy, has led to core inflation lingering around the low single-digit range. Some even believe we will follow in the foot-steps of Japanese deflation (see why we will not follow Japan’s Lost Decades).

The Essentials: Oreos and Bacon

Even if you believe movie, jeans, and healthcare won’t continue inflating at a rapid clip, I’m even more concerned about the critical essentials – for example, indispensable items like Oreos and bacon. Little did you probably know, but according to ProQuest’s Historic newspaper database, a package of Oreos has more than quadrupled in price over the last 30 years to over $4.00 per package – let’s just say I’m not looking forward to spending $16.00 a pop for these heavenly, synthetic, hockey-puck-like, creamy delights.

Beyond Oreos, another essential staple of my diet came under intense scrutiny during my analysis. I’ve perused many an uninspiring chart in my day, but I must admit I experienced a rush of adrenaline when I stumbled across a chart highlighting my favorite pork product. Unfortunately the chart delivered a disheartening message. For my fellow pork lovers, I was saddened to learn those greasy, charred slices of salty protein paradise (a.k.a. bacon strips), have about tripled in price over a similar timeframe as the Oreos. Let us pray we will not suffer the same outcome again.

Sliced Bacon Prices (per lb.) – Source (Bureau of Labor Statistics)

It’s Not Getting Any Easier

Volatility aside, investing has become more challenging than ever. However, efficiently investing your nest egg has never been more critical. Why has efficiently managing your investments become so vital? First off, let’s take a look at the entitlement picture. Not so rosy. I suppose there are some retirees that will skate by enjoying their fully allocated Social Security check and Medicare services, but for the rest of us chumps, those luxurious future entitlements are quickly turning to a mirage.

What the financial crisis, rating agency conflicts, Madoff scandal, Lehman Brothers bankruptcy, AIG collapse, Goldman Sachs hearings, FinReg legislation, etc. taught us is the structural financial system is flawed. The system favors institutions and penalizes the investor with fees, commissions, transactions costs, fine print, and layers of conflicts of interests. All is not lost however. For most investors, the money stuffed under the mattress earning nothing needs to be resourcefully put to work at higher returns in order to offset rising prices. Putting together a diversified, low-cost, tax-efficient portfolio with an investment management firm that invests on a fee-only basis (thereby limiting conflicts) will put you on a path of financial success to cover the imperative but escalating living expenses, including of course, Oreos and bacon.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in KFT, GS, Lehman Brothers, AIG (however own derivative tied to insurance subsidary), or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Tips for Survival and Prosperity in Challenging Economic Times

Survival requires multiple strategies

We have all been impacted in some shape or form by the worst financial crisis experienced in a generation. The question now becomes what did we learn from this mess and how can we better prepare for a more prosperous financial future?

Here are some important tips to follow:

Save and Invest: Before paying others, pay yourself first. You can achieve this goal by saving and investing your money. Given the weak state of our government “safety net” programs, such as Medicare and Social Security, it has become more important than ever to save. Life spans are extending as well, meaning a larger “nest egg” is needed for retirement. If you don’t have the time, discipline, or emotional make-up to manage your own money, then seek out a fee-only advisor* who does not have a conflict of interest in regards to building your wealth.

Tighten Belt: In order to save and invest you need to be in a position where you are creating excess income. Cutting costs is one way to generate additional income. Eating out less, buying used, taking more affordable vacations, conserving energy, purchasing private label goods are a few easy ways to save money that will accumulate over time. If those efforts are still not adequate, one should then contemplate adjusting their living situation (i.e., down-size) or pursue additional income opportunities – either through a pay raise or higher paying job alternatives.

Pay Down Debt: If your credit card company is charging you a 15-20% rate on unpaid credit card balances and gouging you for late-fees and cash advances, then look for other sources of affordable financing. A home equity line of credit or second mortgage may make sense for some, if the fees and lower interest rates make economic sense. Contact a financial planner or tax professional to determine the appropriateness of these debt alternatives. Ultimately, the goal is to reduce debt and create more financial flexibility.

Take Free Money: If your employer offers matching payments to your retirement plan contributions, they are effectively offering you free money. Take it! The government offers you some tax deferral savings through IRA (Individual Retirement Account) contributions, so take advantage of that benefit as well.

Form a 6-Month Emergency Fund: The economy may be in a bottoming-out phase; however we are not out of the woods yet. Unemployment is approaching 10% and many companies and industries continue to struggle. Build a protective financial cushion should you or your family hit a bump in the road.

Invest in Yourself: Investing for retirement is crucial, however investing in yourself is just as, if not more, important than traditional investing. What I’m referring to is job training, education, and health awareness. We live in a globalized economy and in order to compete against those starving for our jobs, we need to improve our skills and education. Lastly, we cannot neglect our health. Finances need to be put in perspective. Our health should be a top priority and a disciplined balance between diet and exercise will not only reduce stress, but it will also improve mental health.

Times have been challenging, but when the going gets rough, the tough go saving. Take control of your financial future rather than letting economic circumstances control you. Financial success however should not come at the expense of your health, so also focus on a balanced program of diet and exercise. There are no free lunches in this world, but following these steps will help lead you on a path to prosperity – even in these challenging economic times.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Wade W. Slome, CFA, CFP is President and Founder of Sidoxia Capital Management, LLC (www.Sidoxia.com), a fee-only Registered Investment Advisory firm headquartered in Newport Beach, California.

Debt: The New Four-Letter Word

D-E-B-T, our country’s new four-letter word, used to be a fun toy the masses played and danced with to buy all kinds of goods and services. Debt was creatively utilized for all types of things, including, our super-sized McMansions purchased with Option ARM (Adjustable Rate Mortgage) Countrywide loans; our 0% financing car binges (thanks to now-bankrupt Chrysler and General Motors); and our no-payment-for-two-years, big screen plasma TVs (financed at now-bankrupt Circuit City). Eventually consumers, corporations, and governments realized excessive debt creates all kinds of lingering problems – especially in recessionary periods. We are by no means out of the woods yet, but consumers are now spending less than they are taking in, as evidenced by a positive and rising savings rate. This slowdown in spending is bad for short-term demand, but eventually these savings will be recycled into our economy leading to productive and innovative value creating jobs that will jumpstart the economy back on a path to sustainable growth.

Click Here For Excellent Article from the Peterson Foundation

In our hot-cold society, where the pendulum of greed and fear swing dramatically from one side to the next, we are also observing an unhealthy level of risk aversion by financial institutions. This excessive caution is unfortunately choking off the health of legitimate businesses that need capital/debt in order to survive. As we continue to see a pickup in the leading indicators for an economic recovery, banks should loosen up the credit purse strings to provide capital for profitable, growing businesses – even if there are hiccups along the way.

National Debt “Blob” Must Be Slowed

In the famous 1958 sci-fi horror film, “The Blob”, a gelatinous, ever-growing creature from outer space threatens to take over the town of Downingtown, Pennsylvania by methodically engulfing everything in its path. Steve McQueen eventually learns that freezing the Blob will halt its progression. In our country, entitlements, in the form of Medicare and Social Security, serve as our 21st century Blob. As the chart above shows, entitlements have expanded dramatically over the last 40 years and stand to expand faster, as the 76 million Baby Boomers reach retirement and demand more Social Security and Medicare benefits. Clearly the current path we are travelling on is not sustainable, and beyond breakthroughs in technology, the only way we can suitably address this problem is by cutting benefits or raising taxes. We only dug ourselves in a deeper financial hole with the enactment of Medicare Part D (prescription drug benefits for Medicare participants). I must admit I have great difficulty in understanding how we are going to expand health care coverage for the vast majority of Americans in the face of exploding deficits and debt burdens. I eagerly await specifics.

With an enlarging national debt burden and widening deficits, the U.S. is only becoming more reliant on foreign investors to finance our shortcomings. This trend too cannot last forever (see chart below). At some point, foreigners will either balk by not providing us the financing, or demanding prohibitively high interest rates on any funding we request – thereby negatively escalating our already high interest payment streams to bondholders.

Regardless of your political view, the problem pretty simply boils down to elementary school math. The government either needs to cut expenses or raise revenue (taxes or growth initiatives). Politically, the stimulative spending path is easier to rationalize, but as we see in California, eventually the game ends and tough cuts are forced to be made.

Regardless of your political view, the problem pretty simply boils down to elementary school math. The government either needs to cut expenses or raise revenue (taxes or growth initiatives). Politically, the stimulative spending path is easier to rationalize, but as we see in California, eventually the game ends and tough cuts are forced to be made.

Let’s hope the painful lessons learned from this financial crisis will steer us back on path to more responsible borrowing – a point where D-E-B-T is no longer considered a dirty four-letter word.

{kind=link}