Archive for January, 2015

Draghi Provides Markets QE Beer Goggles

While the financial market party has been gaining momentum in the U.S., Europe has been busy attending an economic funeral. Mario Draghi, the European Central Bank President is trying to reverse the somber deflationary mood, and therefore has sent out $1.1 trillion euros worth of quantitative easing (QE) invitations to investors with the hope of getting the eurozone party started.

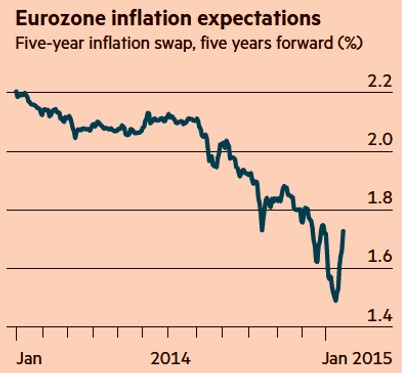

Draghi and the stubborn party-poopers sitting on the sidelines have continually been skeptical of the creative monetary punch-spiking policies initially implemented by U.S. Federal Reserve Chairman Ben Bernanke (and continued by his fellow dovish successor Janet Yellen). With the sluggish deflationary European pity party (see FT chart below) persisting for the last six years, investors are in dire need for a new tool to lighten up the dead party and Draghi has obliged with the solution…“QE beer goggles.” For those not familiar with the term “beer goggles,” these are the vision devices that people put on to make a party more enjoyable with the help of excessive consumption of beer, alcohol, or in this case, QE.

Source: The Financial Times

Although here in the U.S. “QE beer goggles” have been removed via QE expiration last year, nevertheless the party has endured for six consecutive years. Even an economy posting such figures as an 11-year high in GDP growth (+5.0%); declining unemployment (5.6% from a cycle peak of 10.0%); and stimulative effects from declining oil/commodity prices have not resulted in the cops coming to break up the party. It’s difficult for a U.S. investor to admit an accelerating economy; improving job additions; recovering housing market; with stronger consumer balance sheet would cause U.S. 10-Year Treasury Note yields to plummet from 3.04% at the beginning of 2014 to 1.82% today. But in reality, this is exactly what happened.

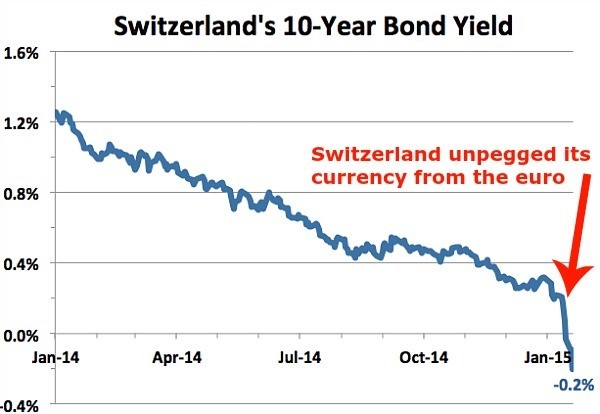

To confound views on traditional modern economics, we are seeing negative 10-year rates on Swiss Treasury Bonds (see chart below). In other words, investors are paying -1% to the Swiss government to park their money. A similar strategy could be replicated with $100 by simply burning a $1 bill and putting the remaining $99 under a mattress. Better yet, why not just pay me to hold your money, I will place your money under my guarded mattress and only charge you half price!

Does QE Work?

Debate will likely persist forever as it relates to the effectiveness of QE in the U.S. On the half glass empty side of the ledger, GDP growth has only averaged 2-3% during the recovery; the improvement in the jobs upturn is arguably the slowest since World War II; and real wages have declined significantly. On the half glass full side, however, the economy has improved substantially (e.g., GDP, unemployment, consumer balance sheets, housing, etc.), and stocks have more than doubled in value since the start of QE1 at the end of 2008. Is it possible that the series of QE policies added no value, or we could have had a stronger recovery without QE? Sure, anyone can make that case, but the fact remains, the QE training wheels have officially come off the economy and Armageddon has still yet to materialize.

I expect the same results from the implementation of QE in Europe. QE is by no means an elixir or panacea. I anticipate minimal direct and tangible economic benefits from Draghi’s $1+ trillion euro QE bazooka, however the psychological confidence building impacts and currency depreciating effects are likely to have a modest indirect value to the eurozone and global financial markets overall. The downside for these unsustainable ultra-low rates is potential excessive leverage from easy credit, asset bubbles, and long-term inflation. Certainly, there may be small pockets of these excesses, however the scars and regulations associated with the 2008-2009 financial crisis have delayed the “hangover” arrival of these risk possibilities on a broader basis. Therefore, until the party ends or the cops come to break up the fun, you may want to enjoy the gift provided by Mario Draghi to global investors…and strap on the “QE beer goggles.”

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own a range of positions, including positions in certain exchange traded funds positions , but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Supply & Demand: The Lesson of a Lifetime

Between all the sporting events, road trips, and parties, I had a difficult time balancing my academic responsibilities just like any other college student. Nonetheless, after a few jobs and a few decades post my graduation, it is refreshing to see my economics college degree was able to teach me one valuable lesson…”supply & demand” actually works.

Emotions and animal spirits can separate fact from fiction in the short-run, but over the long-run, the economic forces of “supply & demand” will ultimately determine the direction of asset prices. If you can think of any bubble market, ranging from tulips and tech stocks (see Bubbles and Naps) to commodities and houses, sooner or later new supply will enter the market, and/or some other factor, which will prick the demand side of the bubble equation.

The same economic rules apply to currencies. Gut-based, day-traders may be skeptical, but economics’ longest enduring axiom shined last week when we saw the Swiss franc spike +20% against the euro in a single day. On the heels of a weakening euro currency and heightened demand for the franc, the Swiss National Bank (SNB) decided to remove its artificial peg to the euro. Effectively, the SNB has been selling francs and buying $490 billion in reserves (the majority of which is in euros and U.S. dollars). As a result, exports of Swiss army knives, watches, and industrial equipment will be more expensive now, which could potentially crimp demand for the country’s goods and services. The SNB, however, could no longer afford to buy euros and dollars to artificially depress the franc. Swiss bankers were very worried about the possible amplified costs of a currency war in the face of this week’s expected European Central Bank (ECB) announcements on quantitative easing (QE) monetary stimulus, so they decided to allow the franc to free-float versus global currencies.

Another asset class heavily impacted by volatile supply-demand dynamics has been the oil market. Weaker demand from Europe/Russia combined with the higher supply from U.S. shale has created a recipe for a crude price collapse (> -50% declines over the last year). Thus far, OPEC (Organization of Petroleum Exporting Countries) has remained committed to maintaining its supply/production levels.

Interest Rates and Supply-Demand

Not every asset price is affected by direct supply-demand factors. Take for example the stock market. I have been writing and commentating about the fascinating persistence and accelerated decline in global interest rates recently (see Why 0% Rates?). Near-0% rates are important because interest rates are just another name for the “cost of money” (or “opportunity cost of money”). When the Prime Rate was 20% in the early 1980s, the cost of money was high and a 16% CD at the bank looked pretty attractive relative to rolling the dice on volatile/risky stocks. Any economics, finance, or accounting student knows through their studies of the “time value of money” that interest rates have a tight inverse correlation to asset values (i.e., lower interest rates = higher asset values, and vice versa).

More practically speaking, we see stock prices supported by the lower borrowing costs tied to low interest rates. Just look at the $500,000,000,000+ conducted in share buybacks over the past 12 months (chart below). Economics works quite effectively when you can borrow at 3% and then purchase your own stock yielding 6% (the inverse percentage of the current 16x P/E ratio). What makes this mathematical equation even more accretive for corporate CFOs is the 6% rate earned today should double to 12% in 10 years, if a company resembles an average S&P 500 company. In other words, S&P 500 earnings have historically grown at a 7% annual clip, therefore the 6% earnings yield should double to 12% in about a decade, based on current prices. This basic arbitrage strategy is a no-brainer for corporate execs because it provides instantaneous EPS (earnings per share) growth with minimal risk, given the current bullet proof status of many blue-chip company balance sheets.

Source: Financial Times

I have provided a few basic examples of how straightforward supply-demand dynamics can be used to analyze market relationships and trends. Although supply-demand analysis is a great rudimentary framework at looking at markets and various asset classes, unanticipated exogenous factors such regulation, terrorism, politics, weather, and a whole host of other influences can throw a wrench into your valuation conclusions. Until rates normalize, the near-0% interest rates we are experiencing now will continue to be a significant tailwind for stock prices. As interest rates have been declining for the last three and a half decades, it appears I still have time before I will need to apply the other important concept I learned in college…mean reversion.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own a range of positions, including positions in certain exchange traded funds positions , but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Stretching the High Yield Rubber Band

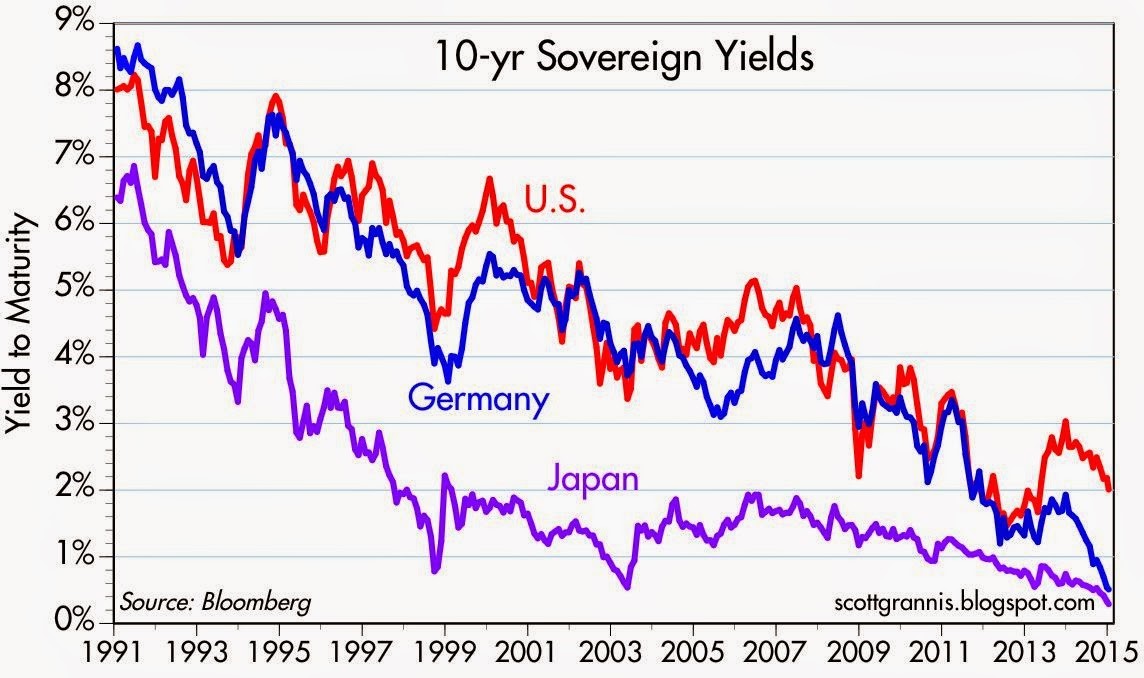

The 10-Year Treasury note recently pierced below the all-important psychological 2% level (1.97%), which has confounded many investors, especially if you consider these same rates were around 4% before the latest mega-financial crisis hit the globe. Some of the rate plunge can be explained by sluggish global growth, but the U.S. just logged a respectable +5.0% GDP growth quarter; corporate profits are effectively at all-time record highs; and the economy has added about 11 million private sector jobs over the last five years (unemployment rate of 10.0% has dropped to 5.6%). So what gives…why such low interest rates? Well, as I noted in a recent article (Why 0% Rates?), there is a whole host of countries with lower rates, which acts like an anchor dragging down our rates with them. Scott Grannis encapsulates this multi-decade, worldwide rate decline in the chart below:

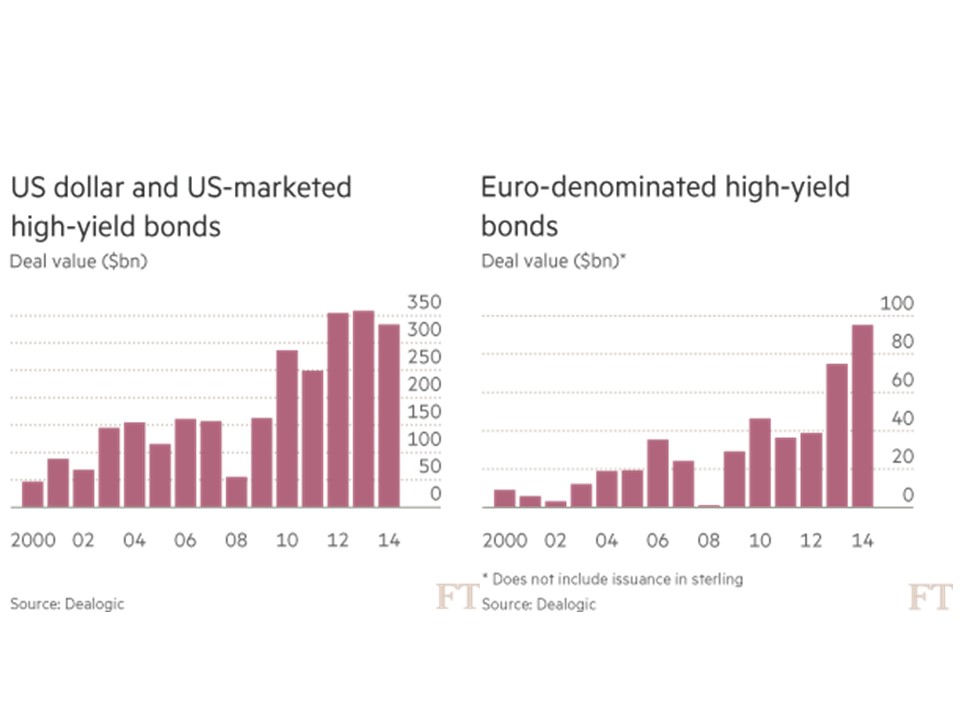

It should come as no surprise to many that these abnormally low rates have had a massive ripple effect on other asset classes… including of course high-yield bonds (aka “junk bonds”). It doesn’t take a genius or rocket scientist to discern the effects of an ultra-low interest rate environment. Quite simply, investors are forced to hunt for yield. When a Bank of America (BAC) customer is forced into earning less than 1/10th of 1 cent for every dollar invested in a CD, you can easily understand why the smile in their CD advertisement looks more like a grimace. Rather than accept $8 in annual interest on a $10,000 investment, post-crisis investors frightened by the stock market have piled into junk bonds. If you don’t believe me, check out the analysis provided by the Financial Times (data from Dealogic) in the chart below, which shows about $1 trillion in U.S. high-yield debt issuance over the last three years. Europe has experienced an even more dramatic growth rate in junk issuance compared to the U.S.

Stretching High-Yield Band

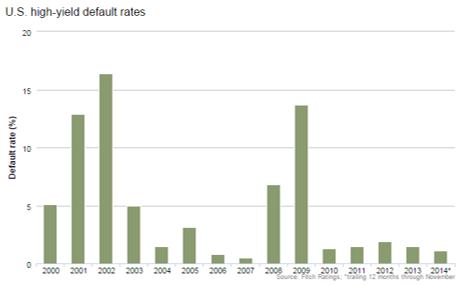

A rubber band can only stretch so far before the elasticity forces it too snap. We are getting closer to the snapping point, as more complacent investors lend money to riskier borrowers and also accept more lenient terms from issuers (e.g., cov-lite loans). Although default rates on high yield bonds remain near decade lows (1.1% through November 2014), high-yield investors keep on inching towards an ultimate day of reckoning. Thanks to a continually improving economy, Fitch Ratings is still projecting a benign default rate environment for high-yield bonds in 2015 – somewhere in the 1.5% – 2.0% range (see chart below). However, high-yield credit spreads did widen in 2014 with the help of crude oil prices getting chopped by more than -50% over the last year. Given the energy sector accounts for about 17% of the high-yield market (Barron’s), it would be natural to expect a larger number of energy company defaults to occur over the next 12-18 months, especially if crude oil prices remain depressed.

Source: Fitch Ratings

While it makes sense for you to hold a portion of your portfolio in high-yield bonds, especially for diversification purposes, don’t forget the power of mean reversion. The uncharacteristically low default rates will eventually revert towards historical averages. Stated differently, the increased risk profile of the high-yield bond market continues to stretch, so make sure you are not overly exposed to the sector because this segment will eventually snap.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own a range of positions, including positions in certain exchange traded funds positions (JNK, HYG), and BAC, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

After 2014 Stock Party, Will Investors Have a 2015 Hangover?

This article is an excerpt from a previously released Sidoxia Capital Management complementary newsletter (January 2, 2015). Subscribe on the right side of the page for the complete text.

Investors in the U.S. stock market partied their way to a sixth consecutive year of gains during 2014 (S&P 500 +11.4%; Dow Jones Industrial Average +7.5%; and NASDAQ +13.4%). From early 2009, at the worst levels of the crisis, the S&P 500 has more than tripled – not too shabby. But similar to recent years, this year’s stock bubbly did not flow uninterrupted. Several times during the party, neighbors and other non-participants at the stock party complained about numerous concerns, including the Fed Tapering of bond purchases; the spread of the deadly Ebola virus; tensions in Ukraine; the rise of ISIS; continued economic weakness across the eurozone; the decline of “The Fragile Five” emerging markets (Brazil, India, Indonesia, Turkey and South Africa), and other headline grabbing stories to name just a few. In fact, the S&P 500 briefly fell -10% from its mid-September level to mid-October before a Santa Claus rally pushed the index higher by +4% in the last quarter of the year.

Even though the U.S. was partying hardy in 2014, it was not all hats and horns across all segments of the market. Given all the geopolitical trepidation and sluggish economic growth abroad, international markets as measured by the Total World Stock ETF (VT) gained a paltry +1.2% for the year. This dramatic underperformance was also seen in small capitalization stocks (Russell 2000 Index ETF – IWM), which only rose +3.7% last year, and the Total Bond Market (BND), which increased +2.9%.

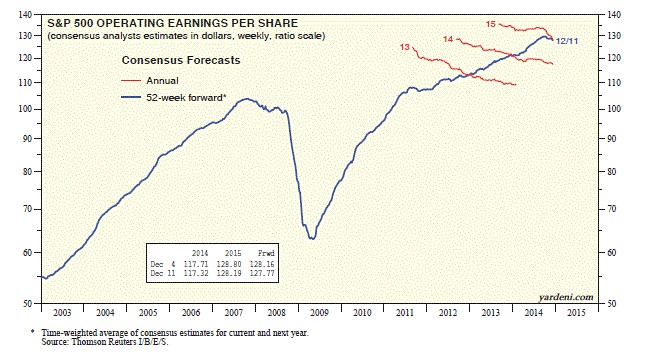

Despite these anxieties and the new Federal Reserve Chairwoman Janet Yellen removing the Quantitative Easing (QE) punchbowl in 2014, there were still plenty of festive factors that contributed to gains last year, which should prevent any hangover for stocks going into 2015. As I wrote in Don’t Be a Fool, corporate profits are the lifeblood for stock prices. Fortunately for investors, the news on this front remains positive (see chart below). As strategist Dr. Ed Yardeni pointed out a few weeks ago, profit growth is still expected to accelerate to +9.3% in 2015, despite the recent drag from plummeting oil prices on the energy sector.

Source: Dr. Ed’s Blog

While a -50% decline in oil prices may depress profits for some energy companies, the extra discretionary spending earned by consumers from $2.24 per gallon gasoline at the pump has been a cheery surprise. This consumer spending tailwind, coupled with the flow-through effect to businesses, should provide added stimulative benefit to the economy in 2015 too. Let’s not forget, this economic energy boost comes on the heels of the best economic growth experienced in the U.S. in over a decade. More specifically, the recently reported third quarter U.S. GDP (Gross Domestic Product) statistics showed growth accelerating to +5%, the highest rate seen since 2003.

Another point to remember about lower energy prices is how this phenomenon positively circulates into lower inflation and lower interest rate expectations. If energy prices remain low, this only provides additional flexibility to the Federal Reserve’s monetary policy decisions. With the absence of any substantive inflation data, Chairwoman Yellen can remain “patient” in hitting the interest rate brakes (i.e., raising the Federal Funds rate) in 2015.

Geographically, our financial markets continue to highlight our country’s standing as one of the best houses in a sluggish global growth neighborhood. Not only do we see this trend in our outperforming stock indexes, relative to other countries, but we also see this in the rising value of the U.S. dollar. It is true that American exports become less competitive internationally in a strong dollar environment, but from an investment standpoint, a rising dollar makes U.S. stock markets that much more attractive to foreign investors. To place this dynamic into better perspective, I would note the U.S. Dollar index rose by approximately +13% in 2014 against a broad basket of currencies (including the basket case Russian Rouble). With the increasing likelihood of eurozone Quantitative Easing to take place, in conjunction with loose monetary policies in large developed markets like Japan, there is a good chance the dollar will continue its appreciation in the upcoming year.

On the political front, despite the Republicans winning a clean sweep in the midterm elections, we should still continue to expect Washington gridlock, considering a Democrat president still holds the all-important veto power. But as I have written in the past (see Who Said Gridlock is Bad?), gridlock has resulted in our country sitting on a sounder financial footing (i.e., we have significantly lower deficits now), which in turn has contributed to the U.S. dollar’s strength. At the margin however, one can expect any legislation that does happen to get passed by the Republican majority led Congress will likely be advantageous for businesses and the stock market.

When Will the Party End?

What could cause the party to come to a screeching halt? While I can certainly point out some obvious potential negative scenarios (e.g., European financial mayhem, China economic speed bump, interest rate spike), history shows us it is usually unforeseen events (surprises) that cause significant downdrafts in stock market prices. The declines rarely come from factors you read in current newspaper headlines or hear on television.

Just like any party, this year is likely to include high points and low points in the financial markets – and of course some lull periods mixed in as well. However, with the economy improving and risk appetites increasing, we are bound to see more party poopers on the sidelines come join the celebration in 2015. It will be a while before the cops arrive and stop the party, so there should be plenty of time to prepare for any hypothetical hangover.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own a range of positions, including positions in certain exchange traded funds positions (including BND), but at the time of publishing SCM had no direct position in VT, IWM or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}