Archive for June, 2017

Sports, Stocks, & the Magic Quadrants

Picking stocks is a tricky game and so is sports betting. With the NFL and NCAA football seasons only a few months away, we can analyze the professional sports-betting industry to better understand the complexities behind making money in the stock market. Anybody who has traveled to Las Vegas, and bet on a sporting event, understands that simply choosing a game winner is not enough for a casino to pay you winnings. You also need to forecast how many points you think a certain team will win or lose by (i.e., the so-called “spread”) – see also What Happens in Vegas, Stays on Wall Street. In the world of stocks, winning/losing is not measured by spreads but rather equities are measured by valuation (e.g., Price/Earnings or P/E ratios).

To make my point, here is a sports betting example from some years back:

Florida Gators vs. Charleston Southern Buccaneers: Without knowing a lot about the powerhouse Southern Buccaneers squad from South Carolina, 99% of respondents polled before the game are likely to unanimously select the winner as Florida – a consistently dominant, nationally ranked powerhouse program. The tougher question becomes trickier if football observers are asked, “Will the Florida Gators win by more than 63 points?”(see picture below). Needless to say, although the Buccs kept it close in the first half, and only trailed by 42-3 at halftime, the Gators still managed to squeak by with a 62-3 victory. Importantly, if you had bet on this game and placed money on the Florida Gators, the overwhelming pre-game favorite, the 59 point margin of victory would have resulted in a losing wager. In order for Gator fans to win money, they would have needed Florida to win by 64 points.

If investing and sports betting were easy, everybody would do it. The reason sports betting is so challenging is due to very intelligent statisticians and odds-makers that create very accurate point spreads. In the investing world, a broad swath of traders, market makers, speculators, investment bankers, and institutional/individual investors set equally efficient valuations over the long-term.

The goal in investing is very similar to sports betting. Successful professionals in both industries are able to consistently identify inefficiencies and then exploit them. Inefficiencies occur for a bettor when point spreads are too high or low, while investors identify inefficient prices in the marketplace by shorting expensive stocks and buying cheap stocks (i.e., undervalued or overvalued).

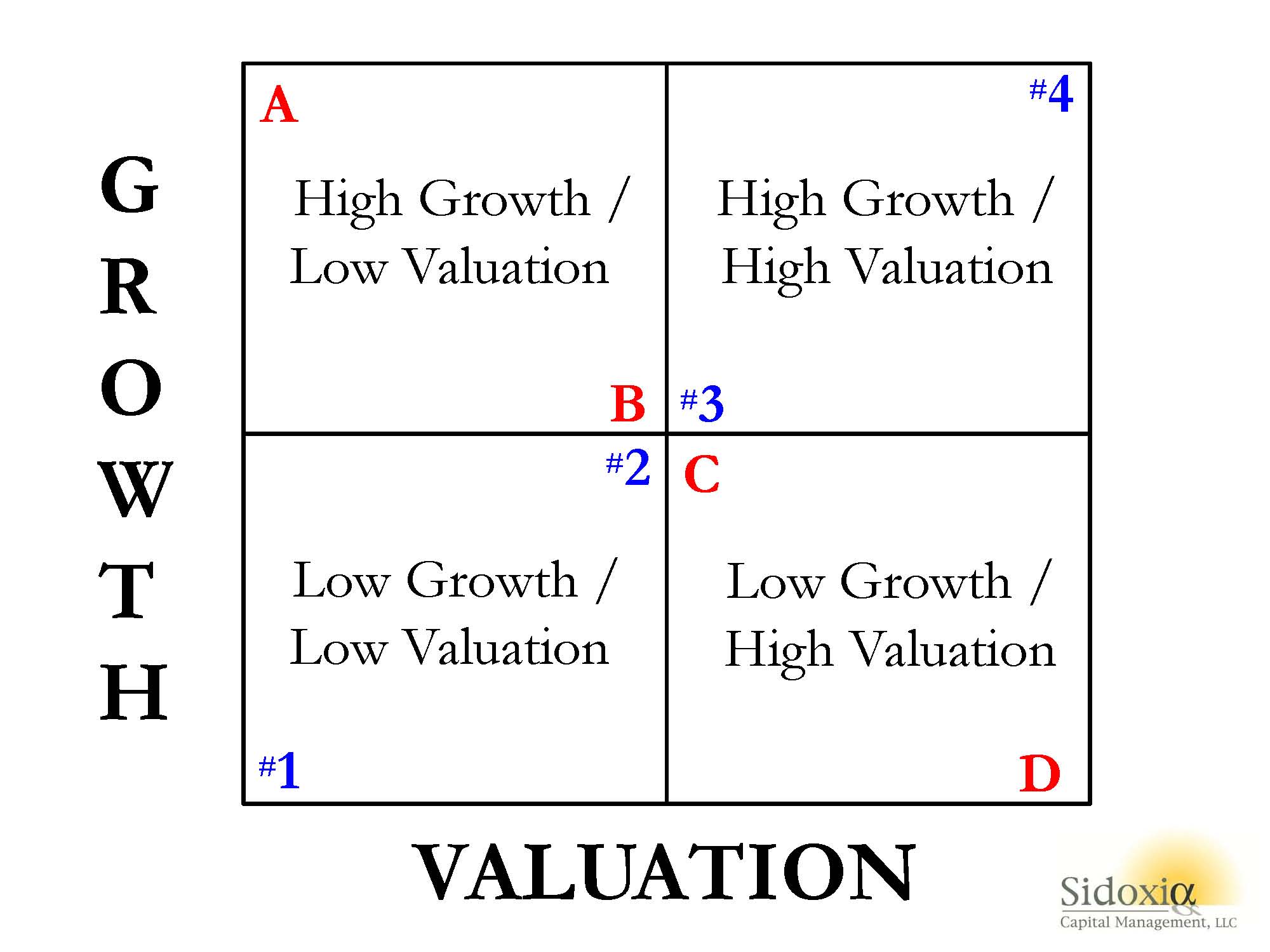

To illustrate my point, let’s take a look at Sidoxia’s “Magic Quadrant“:

A-B-Cs & 1-2-3s

A-B-Cs & 1-2-3s

What Sidoxia’s “Magic Quadrant” demonstrates is a framework for evaluating stocks. By devoting a short period of time reviewing the quadrants, it becomes apparent fairly quickly that Stock A is preferred over Stock B, which is preferred over Stock C, which is preferred over Stock D. In each comparison, the former is preferred over the latter because the earlier letters all have higher growth, and lower (cheaper) valuations. The same relative attractive relationships cannot be applied to stocks #1, #2, #3, and #4. Each successive numbered stock has higher growth, but in order to obtain that higher growth, investors must pay a higher valuation. In other words, Stock #1 has an extremely low valuation with low growth, while Stock #4 has high growth, but an investor must pay an extremely high valuation to own it.

While debating the efficiency of the stock market can escalate into a religious argument, I would argue the majority of stocks fall in the camp of #1, #2, #3, or #4. Or stated differently, you get what you pay for. For example, investors are paying a much higher valuation (high P/E) for Tesla Motors, Inc (TSLA) for its rapid electric car growth vs. paying a much lower valuation (low P/E) for Pitney Bowes Inc (PBI) for its more mature mail equipment business.

The real opportunities occur for those investors capable of identifying companies in the upper-left quadrant (i.e., Stock A) and lower-right quadrant (i.e., Stock D). If the analysis is done correctly, investors will load up on the undervalued Stock A and aggressively short the expensive Stock D. Sidoxia has its own proprietary valuation model (Sidoxia Holy Grail Ranking – SHGR or a.k.a. “SUGAR”) designed specifically to identify these profitable opportunities.

The professions of investing and sports betting are extremely challenging, however establishing a framework like Sidoxia’s “Magic Quadrants” can help guide you to find inefficient and profitable investment opportunities.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and TSLA, but at the time of publishing, SCM had no direct position in PBI, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is the information to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Art & Science of Successful Investing

As I described in my book, How I Managed $20,000,000,000.00 by Age 32, I believe successful investing is achieved by integrating aspects of both art and science. The science aspect of investing is fairly straightforward – most of the accounting and valuation math involved could be solved by a 7th grader. The more challenging aspect to successful investing is controlling the vacillating emotions of fear and greed when searching for attractive investments.

When people ask me about my investment philosophy, I do not like to be pigeon-holed into one style box because normally my portfolios hold investments that outsiders would deem both value and growth oriented. Since I am an absolute return investor, I am more concerned about how I can maximize upside returns while minimizing downside risk for my investors.

Because valuation is such an important factor in my process (price always matters), the most accurate description of my style would likely be “high octane GARP” (Growth At a Reasonable Price). While many GARP investors limit themselves to current or historical valuation metrics, my process has allowed me to take a more long-term, forward looking analysis of valuations, which has directed me to participate in some large winners, like Amazon (AMZN), Apple (AAPL), and Google/Alphabet (GOOGL), to name a few. To many observers, positions like these have traditionally been falsely considered “expensive” growth stocks.

Case in point is Google/Alphabet, which went public at $85 per share in 2004. At the time, the broad Wall Street consensus was the IPO (Initial Public Offering) price was way overheated. As it turned out, the stock has reached $1,000 per share and the Price-Earnings ratio (P/E) was a steal at less than 3x had you bought Google at the IPO price. ($85 2004 price/$33.98 2017 EPS estimate). Google is a perfect example of a dominant market leader that has been able to grow earnings dramatically for many years. In short order after going public, Google’s earnings ended up more than quintupling in less than three years and the stock price quintupled as well, proving that ill-advised focus on stale, traditional valuation metrics can lead you to wrong conclusions. Certainly, finding stocks that can increase in value by more than 11x fold is easier said than done, however, applying longer-term valuation metrics to dominant growth leading franchises will allow you to occasionally find monster winners like Google.

The greatest long-term winners don’t start off as the largest weightings, but due to the compounding of returns, position sizes can explode over time. As Peter Lynch states,

“You don’t need a lot of good hits every day. All you need is two to three good stocks a decade.”

Google/Alphabet proves what can appear expensive in the short-run is, in many cases, wildly cheap based on future earnings growth. Earnings tomorrow may be significantly larger than earnings today. Lynch emphasizes the importance of earnings over current prices,

“People concentrate too much on the ‘P’ (Price), but the ‘E’ (Earnings) really makes the difference.”

“Just because a stock is cheaper than before is no reason to buy it, and just because it’s more expensive is no reason to sell.”

The Google/Alphabet chart below shows the incredible price appreciation that can be realized from compounding earnings growth.

The Google example also underscores the importance of patience. Although the stock has been a massive home-run since its IPO, the stock barely budged from late 2006 through 2011. Accurately picking the perfect timing to make an investment is nearly impossible. I concur with Bill Miller when he stated,

“We expect the stocks we buy today to contribute to our performance several years hence. While it’s nice if they contribute to this year’s performance, this year’s performance should be driven by decisions we made in previous years. If we keep doing this, we hope that we will provide adequate returns in the future.”

Regarding timing, Miller adds,

“Nobody buys at lows and sells at highs except liars.”

The Sidoxia Philosophy

Over time, as I have fine-tuned my investment philosophy, I have not been bashful in borrowing winning ideas from growth gurus like Peter Lynch, Phil Fisher, William O’Neil, and Ron Baron, to name a few. By the same token, I am not shy about stealing ideas from value veterans like Warren Buffett, Seth Klarman, and Bill Miller as well.

While I don’t agree with Warren Buffett’s “forever” time horizon, I do believe in the power of compounding he espouses, which requires a longer-term investment horizon. The power of compounding is accelerated not only by committing to a long-term horizon, but also by the benefits accrued from lower trading costs and taxes. What’s more, taking a long view lowers your blood pressure and creates fewer ulcers. Legendary growth manager, T. Rowe Price, captures the essence of this idea here:

“The growth stock theory of investing requires patience, but is less stressful than trading, generally has less risk, and reduces brokerage commissions and income taxes.”

The Science of Investing

As discussed earlier, successful investing is an endeavor that involves the practices of both art and science – too much of either approach can be detrimental to your financial health. Quantitative screening can be an excellent tool for identifying new securities for research along with streamlining the fundamental analysis process. However, many investment funds rely too heavily on the quantitative science. The adage that “correlation does not equal causation” is an important credo to follow when reviewing various quantitative models (see Butter in Bangladesh).

The collapse of the infamous, multi-billion Long Term Capital Management hedge fund should also be a lesson to everyone (see When Genius Failed ). If world renowned Nobel Prize winners, Robert Merton and Myron Scholes, can single-handedly bring the global market to its knees as a result of using inconsistent and unreliable quantitative models, then I feel validated for my fundamentally-based investment approach.

While there are some artistic facets to valuation techniques, in large part, the valuation science is a fairly straightforward mathematical exercise. Unfortunately, the market consists of emotional and unpredictable individuals who continually change their opinions. Eventually the financial markets prod prices in the right direction, but over shorter time intervals, proper investment analysis requires some imperfect estimation.

Emotions regularly result in individuals overpaying for stocks, and this tendency is a risky strategy for any investment. In many cases investors chase darling stocks highlighted in news headlines, but regrettably these pricy investments often end up performing poorly. When it comes to hot stocks, I’m on the same page as famed value investor Bill Miller,

“If it’s in the papers, it’s in the price. One needs to anticipate, not react.”

Usually a news event that makes headlines is already factored into the stock price. The financial markets are generally forward looking mechanisms, not backward looking.

The Art of Investing

“It’s tough to make predictions, especially about the future.”

-Yogi Berra

Investing is undoubtedly a challenging undertaking, but like almost any profession, the more experience one has, the better results generally achieved. Experience alone does not guarantee extraordinary performance, in large part due to emotional pressures. Investing would be much easier for everyone, if you didn’t have to worry about controlling those pesky emotions of fear and greed. The best investment decisions, and frankly any decision, are rarely made under these heightened emotions.

The most successful set of investors I have studied and modeled my investment process after are professionals who have married the quantitative science with the fundamental art of investing. At Sidoxia, we use a disciplined cash flow based valuation approach, along with thorough fundamental analysis to identify attractively valued, market leading franchises that can sustain above average growth. It sounds like a mouthful, but over time, it has worked well for the benefit of my clients and me.

The market leading franchises we invest in tend to have a competitive advantage, whether in the form of superior research and development, low-cost manufacturing, leading marketing, and/or other exceptional functions in the company that allow the entity to consistently garner more growth and more market share from its competitors. Quality franchises tend to also employ first-class management teams that have a proven track record, along with thoughtful, systematic processes in place to maintain their competitive edge. These competitive advantages are what allow companies to produce exceptional earnings growth for extended periods of time, thereby producing outstanding long-term performance for shareholders.

Finding sustainable growth in competitive niche markets is nearly impossible, and that is why I center my attention on large or emerging sectors of the economy that can support long runways of growth. When analyzing companies with durable, long runways of earnings growth, I concentrate on those developing, share-taking companies and dominant market leaders. In other words, disruptive companies that are entering new markets with vast potential and established companies that are gaining significant share in large markets. Well-known growth authority, Phil Fisher summarized the objective,

“The greatest investment rewards come to those who by good luck or good sense find the occasional company that over the years can grow in sales and profits far more than industry as a whole.”

I am privileged and honored to manage the hard earned investments of my clients. If this was a simple profession, everyone would do it, and I would not be employed as an investment manager. I have developed what I believe is a superior way of managing money, but I realize my investment process is not the only way to make money. If you were to assemble 10 different investment managers in the same room, and ask them, “What is the best way to invest money?,” you are likely to get 10 different answers. Having been in the investment industry and managed money for over 25 years, my experience has shown me that the vast majority of professional managers have underperformed the passive benchmarks. However, there are investment managers who have survived the test of time. For those veterans incorporating a disciplined, systematic approach that integrates the artistic and scientific aspects of investing, exceptional long-term returns can be achieved and have been achieved.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, AMZN, GOOG/GOOGL, and AAPL, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Head Fakes Surprise as Stocks Hit Highs

In a world of seven billion people and over 200 countries, guess what…there are a plethora of crises, masses of bad people, and plenty of lurking issues to lose sleep over.

The fear du jour may change, but as the late-great investor Sir John Templeton correctly stated:

“Bull markets are born on pessimism and they grow on skepticism, mature on optimism, and die on euphoria.”

And for the last decade since the 2008-2009 Financial Crisis, it’s clear to me that the stock market has climbed a lot of worry, pessimism, and skepticism. Over the last decade, here is a small sampling of wories:

With over five billion cell phones spanning the globe, fear-inspiring news headlines travel from one end of the world to the other in a blink of an eye. Fortunately for investors, the endless laundry list of crises and concerns has not broken this significant, multi-year bull market. In fact, stock prices have more than tripled since early 2009. As famed hedge fund manager Leon Cooperman noted:

“Bull markets don’t die from old age, they die from excesses.”

On the contrary to excesses, corporations have been slow to hire and invest due to heightened risk aversion induced by the financial crisis. Consumers have saved more and lowered personal debt levels. The Federal Reserve took unprecedented measures to stimulate the economy, but these efforts have since been reversed. The Fed has even signaled its plan to reduce its balance sheet later this year. As the expansion has aged, corporations and consumer risk aversion has abated, but evidence of excesses remains paltry.

Investors may no longer be panicked, but they remain skeptical. With each subsequent new stock market high, screams of a market top and impending recession blanket headlines. As I pointed out in my March Madness article, stocks have made new highs every year for the last five years, but continually I get asked, “Wade, don’t you think the market is overheated and it’s time to sell?”

For years, I have documented the lack of stock buying evidenced by the continued weak fund flow sales. If I could summarize investor behavior in one picture, it would look something like this:

Corrections have happened, and will continue to occur, but a more significant decline will likely happen under specific circumstances. As I point out in Half Empty, Half Full?, the time to become more cautious will be when we see a combination of the following trends occur:

- Sharp increase in interest rates

- Signs of a significant decline in corporate profits

- Indications of an economic recession (e.g., an inverted yield curve)

- Spike in stock prices to a point where valuation (prices) are at extreme levels and skeptical investor sentiment becomes euphoric

Attempting to predict a market crash is a Fool’s Errand, but more important for investors is periodically reviewing your liquidity needs, time horizon, risk tolerance, and unique circumstances, so you can optimize your asset allocation. There will be plenty more head fake surprises, but if conditions remain the same, investors should not be surprised by new stock highs.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Political Showers Bring Record May Stock Flowers

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (June 1, 2017). Subscribe on the right side of the page for the complete text.

There has been a massive storm of political rain that has blanketed the media airwaves and internet last month, however, the stock market ignored the deluge of headlines and focused on more important factors, as prices once again pushed to new record highs. Over the eight-year bull market, the old adage to “sell in May, and go away,” once again was not a very successful strategy. Had investors heeded this advice, they would have missed out on a +1.2% gain in the S&P 500 index during May (up +7.7% for 2017) and a +2.5% surge in the technology-driven NASDAQ index (+15.1% in 2017).

Keeping track of the relentless political storm of new headlines and tweets almost requires a full-time staff person, but nevertheless we have summarized some of the political downpour here:

French Elections: In the wake of last year’s U.K. “Brexit”, fears of an imminent “Frexit” (French Exit) resurfaced ahead of the French presidential. Emmanuel Macron, a 39-year-old former investment banker, swept to a decisive victory over National Front candidate Marine Le Pen by a margin of 66% to 34%.

Firing of FBI Director: President Trump fired FBI Director James Comey based on the recommendation of deputy attorney general Rod Rosenstein, who cited Comey’s mishandling of Hillary Clinton’s private email server investigation. The president’s critics claim Trump was frustrated with the FBI’s investigation into the administration’s potential ties with Russian officials in relation to the 2016 presidential elections. Comey is expected to testify next week to Congress, where he will likely address reports that President Trump asked him to drop the FBI’s investigation into former National Security Advisor Michael Flynn during a February meeting.

Trump Classified Leak to Russians: Reports show that President Trump revealed classified information regarding the Islamic State (ISIS) to the Russian foreign minister during an Oval Office meeting. The ISIS related information emanating from Syria reportedly had been passed to the U.S. from Israel, with the provision that it not be shared.

Impeachment Talk and Appointment of Independent Special Prosecutor: Heightened reports of Russian intervention coupled with impeachment cries from the Democratic opposition coincided with Deputy Attorney General Rod Rosenstein’s announcement that former FBI director Robert Mueller III would take on the role as an independent special counsel in the investigation of Russian interference in the 2016 election. Rosenstein had the authority to make the appointment after Attorney General Jeff Sessions recused himself after admitting contacts with Russian officials. The White House, which has denied colluding with the Russians, issued a statement from President Donald Trump looking forward “to this matter concluding quickly.”

Kushner Under Back Channel Investigation: President Trump’s son-in-law and senior advisor, Jared Kushner, is under investigation over discussions to set up a back channel of communication with Russian officials. At the heart of the probe is a December meeting Kushner held with Sergey Gorkov, an associate of Russian President Vladimir Putin and the head of the state-owned Vnesheconombank, a Russian bank subject to sanctions imposed by President Obama. Back channels have been legally implemented by other administrations, but the timing and nature of the discussions could make the legal interpretation more difficult.

Trump’s First Foreign Trip: A whirlwind trip by President Trump through the Middle East and Europe, resulted in commitments to Middle East peace, multi-billion contract signings with the Saudis, pledges to fight Muslims extremism, calls for NATO members to pay their “fair share,” and demands for German President Angela Merkel to address the elevated trade deficit with the U.S.

Subpoenas Issued to Trump Advisors: The House Intelligence Committee issued subpoenas to ousted National Security Adviser Michael Flynn and President Trump’s personal attorney, Michael Cohen, as it relates to potential Russian interference in the presidential campaign. Flynn reportedly plans to invoke his Fifth Amendment rights in response to a separate subpoena issued by the Senate Intelligence Committee.

Repeal and Replace Healthcare: The Republican-controlled House of Representatives narrowly passed a vote to repeal and replace the Affordable Care Act after prior failed attempts. The bill, which allows states to apply for a waiver on certain aspects of coverage, including pre-existing conditions, received no Democratic votes. While the House passage represents a legislative victory for President Trump, Senate Republicans must now take up the legislation that addresses conclusions by the nonpartisan Congressional Budget Office (CBO). More specifically, the CBO found the revised House health care bill could leave 23 million more Americans uninsured while reducing the federal deficit by $119 billion in the next decade.

North Korea Missile Tests: If domestic political turmoil wasn’t enough, North Korea conducted an unprecedented number of medium-to-long-range missile tests in an effort to develop an intercontinental ballistic missile (ICBM) capable of hitting the mainland United States. Due to the rising tensions, the U.S. and South Korea have been planning nuclear carrier drills off the coast of the Korean peninsula.

Wow, that was a mouthful. While all these politics may be provocative and stimulating, long-time followers of mine understand my position…politics are meaningless (see Politics-Schmolitics). While a terrorist or military attack on U.S. soil would undoubtedly have an immediate and negative impact, 99% of daily politics should be ignored by investors. If you don’t believe me, just take a look at the stock market, which continues to make new record highs in the face of a hurricane of negative political headlines. What the stock market really cares most about are profits, interest rates, and valuations:

- Record Profits: Stock prices follow the direction of earnings over the long-run. As you can see below, profits vacillate year-to-year. However, profits are currently surging, and therefore, so are stock prices – despite the negative political headlines.

Source: Dr. Ed’s Blog

- Near Generationally Low Interest Rates: Generally speaking, most asset classes, including real estate, commodities, and stock prices are worth more when interest rates are low. When you could earn 15% on a bank CD in the early 1980s, stocks were much less attractive. Currently, bank CDs almost pay nothing, and as you can see from the chart below, interest rates are near a generational low – this makes stock prices more attractive.

- Attractive Valuations: The price you pay for an asset is always an important factor, and the same principle applies to your investments. If you can buy a $1.00 for $0.90, you want to take advantage of that opportunity. Unfortunately, the value of stocks is not measured by a simple explicit price, like you see at a grocery store. Rather, stock values are measured by a ratio (comparing an investment’s price relative to profits/cash flows generated). Even though the stock market has surged this year, stock values have gotten cheaper. How is that possible? Stock prices have risen about +8% in the first quarter, while profits have jumped +15%. When profits rise faster than prices appreciate, that means stocks have gotten cheaper. From a multi-year standpoint, I agree with Warren Buffett that prices remain attractive given the current interest rate environment. To read more about valuations, check out Ed Yardeni’s recent article on valuations.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}