Archive for February, 2013

Monitoring the Tricks Hidden Up Corporate Sleeves

As Warren Buffett correctly states, “If you are in a poker game and after 20 minutes, you don’t know who the patsy is, then you are the patsy.” The same principle applies to investing and financial analysis. If you are unable to determine who is cooking (or warming) the books via deceptive practices, then you will be left holding a bag of losses as tears of regret pour down your face. The name of the stock investing game (not speculation game) is to accurately gauge the financial condition of a company and then to correctly forecast the trajectory of future earnings and cash flows.

Unfortunately for investors, many companies work quite diligently to obscure, hide, and distort the accuracy of their current financial condition. Without the ability of making a proper assessment of a company’s financials, an investor by definition will be unable to value stocks.

There are scores of accounting tricks that companies hide up their sleeves to mislead investors. Many people consider GAAP (Generally Accepted Accounting Principles) as the laws or rules governing financial reporting, but GAAP parameters actually provide companies with extensive latitude in the way accounting reports are implemented. Here are a few of the ways companies exercise their wiggle room in disclosing financial results:

Depreciation Schedules: Related to GAAP accounting, adjustments to longevity estimates by a company’s management team can tremendously impact a company’s reported earnings. For example, if a $10 million manufacturing plant is expected to last 10 years, then the depreciation expense should be $1 million per year ($10m ÷ 10 years). If for some reason the Chief Financial Officer (CFO) suddenly changes his/her mind and decides the building should last 40 years rather than 10 years, then the company’s annual expense would miraculously decrease -75% to $250,000. Voila, an instant $750,000 annual gain created out of thin air! Other depreciation tricks include the choice of accelerated or straight-line depreciation.

Capitalizing Expenses: If you were a management team member with a goal of maximizing current reported profitability, would you be excited to learn that you are not required to report expenses on your income statement? For many the answer is absolutely “yes”. A common example of this phenomenon occurs with companies in the software industry (or other companies with heavy research and development), where research expenses normally recognized on the income statement get converted instead to capitalized assets on the balance sheet. Eventually these capitalized assets get amortized (recognized as expenses) on the income statement. Proponents argue capitalizing expenses better matches future revenues to future expenses, but regardless, this scheme boosts current reported earnings, and delays expense recognition.

Stuffing the Channel: No, this is not a personal problem, but rather occurs when companies force their goods on a distributor or customer – even if the goods (or service) are not requested. This deceitful practice is performed to drive up short-term revenue, even if the reporting company receives no cash for the “stuffing”. Ballooning receivables and substandard cash flow generation can be a sign of this cunning, corporate custom.

Accounts Receivable/Loans: Ballooning receivables is a potential sign of juiced reported revenues and profits, but there are more nuanced ways of manipulating income. For instance, if management temporarily lowers warranty expenses and product return assumptions, short-term profits can be artificially boosted. In addition, when discussing financial figures for banks, loans can also be considered receivables. As we experienced in the last financial crisis, many banks under-provisioned for future bad loans (i.e. didn’t create enough cash reserves for misled/deadbeat borrowers), thereby overstating the true, underlying, fundamental earnings power of the banks.

Inventories: As it relates to inventories, GAAP accounting allows for FIFO (First-In, First-Out) or LIFO (Last-In, Last-Out) recognition of expenses. Depending on whether prices of inventories are rising or falling, the choice of accounting method could boost reported results.

Pension Assumptions: Most companies like their employees…but not the expenses they have to pay in order to keep them. Employee expenses can become excessively burdensome, especially for those companies offering their employees a defined benefit pension plan. GAAP rules mandate employers to contribute cash to the pension plan (i.e., retirement fund) if the returns earned on the assets (i.e., stocks & bonds) are below previous company assumptions. One temporary fix to an underfunded pension is for companies to assume higher plan returns in the future. For example, if companies raise their return assumptions on plan assets from 5% to a higher rate of 10%, then profits for the company are likely to rise, all else equal.

Non-GAAP (or Pro Forma): Why would companies report Non-GAAP numbers on their financial reports rather than GAAP earnings? The simple answer is that Non-GAAP numbers appear cosmetically higher than GAAP figures, and therefore preferred by companies for investor dissemination purposes.

Merger Magic: Typically when a merger or acquisition takes place, the acquiring company announces a bunch of one-time expenses that they want investors to ignore. Since there are so many moving pieces in a merger, that means there is also more opportunities to use smoke and mirrors. The recent $8.8 billion write-off of Hewlett-Packard’s (HPQ) acquisition of Autonomy is evidence of merger magic performed.

EBITDA (Earnings Before Interest Taxes Depreciation & Amortization): Skeptics, like myself, call this metric “earnings before all expenses.” Or as Charlie Munger says, Warren Buffett’s right-hand man, “Every time you see the word EBITDA, substitute it with the words ‘bulls*it earnings’!”

This is only a short-list of corporate accounting gimmicks used to distort financial results, so for the sake of your investment portfolio, please check for any potential tricks up a company’s sleeve before making an investment.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in HPQ/Autonomy, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Beware: El-Erian & Gross Selling Buicks…Not Chevys

As my grandmother always told me, “Be careful where you get your advice!” Or as renowned Wall Street trader Gerald Loeb once said, “The Buick salesman is not going to tell you a Chevrolet will fit your needs.” In other words, when it comes to investment advice, it is important to realize that opinions and recommendations are often biased and steeped with inherent conflicts of interest. Having worked in the financial industry over several decades, I have effectively seen it all.

However, one unique aspect I have grown accustomed to is the nauseating and fatiguing over-exposure of PIMCO’s dynamic bond duo, CEO Mohamed El-Erian and founder Bill Gross. Over the last four years and 13 consecutive quarters of GDP growth (likely 14 after Q4 revisions), I and fellow CNBC viewers have been forced to endure the incessant talk of the “New Normal” of weak economic growth to infinity. Actual results have turned out quite differently than the duet’s cryptic and verbose predictions, which have piled up over their seemingly non-stop media interview schedule. Despite the doomsday rhetoric from the bond brothers, El-Erian and Gross have witnessed a more than doubling in equity prices, which has soundly trounced the performance of bonds over the last four years.

After being mistaken for such a long period, certainly the PIMCO marketing machine would revise their pessimistic outlook, right? Wrong. In true biased fashion, El-Erian cannot admit defeat. Just this week, El-Erian argues stocks are artificially high due to excessive liquidity pumped into the financial system by central banks (see video below). I’m the first one to admit Federal Reserve Chairman Ben Bernanke is explicitly doing his best to force investors into risky assets, but doesn’t generational low interest rates help bond prices too? Apparently that mathematical fact has escaped El-Erian’s bond script.

Source: Yahoo! Finance (Daily Ticker)

El-Erian’s buddy, Bill Gross, can’t help himself from jumping on the stock rain parade either. Just six weeks ago Gross followed the bond-pumping playbook by making another dour prediction that the market would rise less than 5% in 2013. Unfortunately for Gross, his crystal ball has also been a little cloudy of late, with the S&P 500 index already up more than +6.5% this year. Since doomsday outlooks are what keeps the $2 trillion PIMCO machined primed, it’s no surprise we hear about the never-ending gloom. For those keeping score at home, let’s please not forget Bill Gross’s infamously wrong Dow 5,000 prediction (see article).

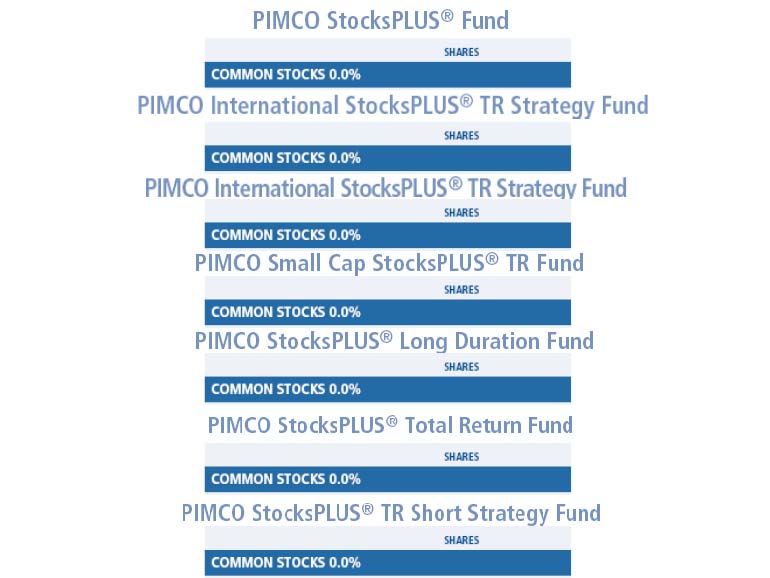

PIMCO Smoke & Mirrors: Stock Funds with NO Stocks

Just when I thought I had seen it all, I came across PIMCO’s Equity-Related funds. Never in my career have I seen “equity” mutual funds that invest solely in “bonds.” Well, apparently PIMCO has somehow creatively figured out how to create stock funds without investing in stocks. I guess that is one strategy for a bond-centric company of getting into the equity fund market? This is either ingenious or bordering on the line of criminal. I fall into the latter camp. How the SEC allows the world’s largest bond company to deceivingly market billions in bond-filled stock funds to individual investors is beyond me. After innocent people got fleeced by unscrupulous mortgage brokers and greedy lenders, in this Dodd-Frank day and age, I can’t help but wonder how PIMCO is able to solicit a StockPlus Fund that has 0% invested in common stocks. You can judge for yourself by reviewing their equity-related funds on their website (see also chart below):

PIMCO Equity-Related Funds with No Equity

PIMCO Active Equity Funds Struggle

With more than 99% of PIMCO’s $2 trillion in assets under management locked into bonds, company executives have made a half-hearted effort of getting into the equity markets, even though they’ve enjoyed high-fiving each other during the three-decade-long bond bull market (see Downhill Marathon Machine). In hopes of diversifying their bond-heavy revenue stream, in 2009 they hired the head of the high-profile $700 billion, government TARP program (Neil Kashkari). Subsequently, PIMCO opened its first set of actively managed funds in 2010. Regrettably for PIMCO, the sledding has been quite tough. In 2012, all six actively managed equity funds lagged their benchmarks. Moreover, just a few weeks ago, Kashkari their rock star hire decided to quit and pursue a return to politics.

Mohamed El-Erian and Bill Gross have never been camera shy or bashful about bashing stocks. PIMCO has virtually all their bond eggs in one basket and their leaderless equity division is struggling. What’s more, like some car salesmen, they have had a creative way of describing the facts. If it’s a Chevy or unbiased advice you’re looking for, I recommend you steer clear from Buick salesmen and PIMCO headquarters.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in PIMCO funds, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Vice Tightens for Those Who Missed the Pre-Party

The stock market pre-party has come to an end. Yes, this is the part of the bash in which an exclusive group is invited to enjoy the fruits of the festivities before the mobs arrive. That’s right, unabated access to the nachos; no lines to the bathroom; and direct access to the keg. For those of us who were invited to the stock market pre-party (or crashed it on their own volition), the spoils have been quite enjoyable – about a +128% rebound for the S&P 500 index from the bottom of 2009, and a +147% increase in the NASDAQ Composite index over the same period (excluding dividends paid on both indexes).

Although readers of Investing Caffeine have received a personal invitation to the stock market pre-party since I launched my blog in early 2009, many have shied away, out of fear the financial market cops may come and break-up the party.

Rather than partake in stock celebration over the last four years, many have chosen to go down the street to the bond market party. Unlike the stock market party, the fixed-income fiesta has been a “major-rager” for more than three decades. However, there are a few signs that this party has gotten out-of-control. For example, crowds of investors are lined up waiting to squeeze their way into some bond indulgence; after endless noise, neighbors are complaining and the cops are on their way to shut the party down; and PIMCO’s Bill Gross has just jumped off the roof to do a cannon-ball into the pool.

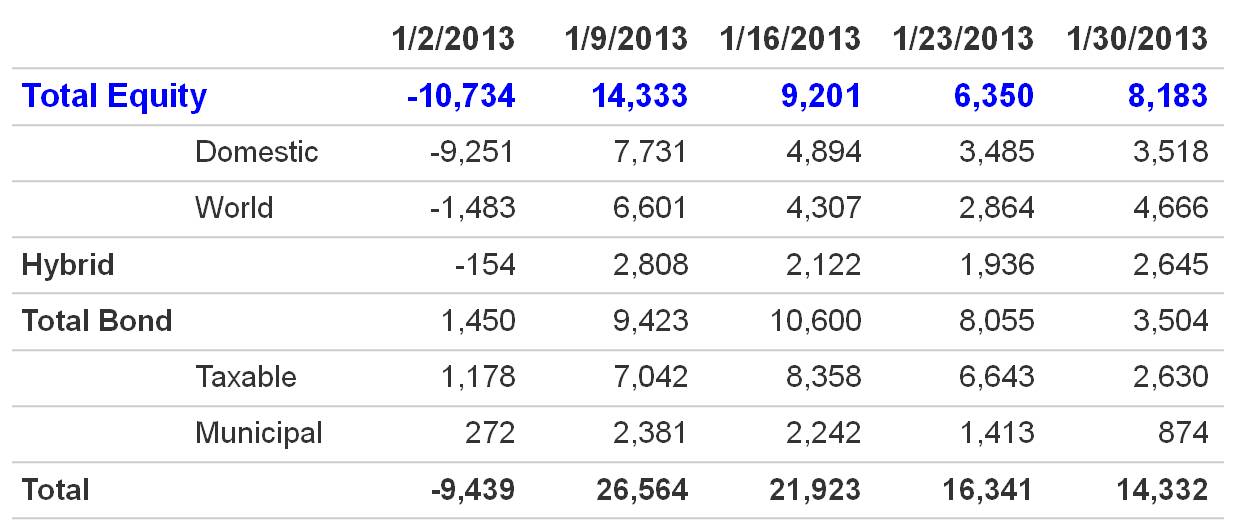

Even though the stock-market pre-party has been a blast, stock prices are still relatively cheap based on historical valuation measurements, meaning there is still plenty of time for the party to roll on. How do we know the party has just started? After five years and about a half a trillion dollars hemorrhaging out of domestic funds (see Calafia Beach Pundit), there are encouraging signs that a significant number of party-goers are beginning to arrive to the party. More specifically, as it relates to stocks, a fresh $10 billion has flowed into domestic equity mutual funds during this January (see ICI chart below). This data is notoriously volatile, and can change dramatically from month-to-month, but if this month’s activity is any indication of a changing mood, then you better hurry to the stock party before the bouncer stops letting people in.

Source: Investment Company Institute (ICI)

Vice Begins to Tighten on Party Outsiders

Many stock market outsiders have either been squeezed into the bond market, hidden in cash, or hunkered down in a bunker with piles of gold. While some of these asset classes have done okay since early 2009, all have underperformed stocks, but none have performed worse than cash. For those doubters sitting on the equity market sidelines, the pain of the vice squeezing their portfolios has only intensified, especially as the economy and employment picture slowly improves (see chart below) and stock prices persist directionally upward. For years, fear-mongering stock skeptics have warned of an imploding dollar, exploding inflation, a run-away deficit/debt, a reckless money-printing Federal Reserve, and political gridlock. Nevertheless, none of these issues have been able to kill this equity bull market.

Source: Calafia Beach Pundit

But for those willing and able investors to enter the stock party today, one must realize this party will only get riskier over time. As we exit the pre-party and enter into the main event, you never know who may join the party, including some uninvited guests who may steal money, get sick on the carpet, participate in illegal activities, and/or ruin the fun by clashing with guests. We have already been forced to deal with some of these uninvited guests in recent years, including the “flash crash,” debt ceiling debate, European financial crisis, fiscal cliff, and lastly, sequestration is about to arrive as well (right after parking his car).

New investors can still objectively join the current equity party, but it is necessary to still be cognizant of not over-staying your welcome. However, for those party-pooping doubters who already missed the pre-party, the vice will continue to tighten, leaving stock cynics paralyzed as they watch additional missed opportunities enjoyed by the rest of us.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in HLF, Japanese ETFs, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Sidoxia Debuts Video & Goes to the Movies

Article is an excerpt from previously released Sidoxia Capital Management’s complementary February 1, 2013 newsletter. Subscribe on right side of page.

The red carpet was rolled out for the stock market in January with the Dow Jones Industrial Average rising +5.8% and the S&P 500 index up an equally impressive +5.0% (a little higher rate than the 0.0001% being earned in bank accounts). Movie stars are also strutting their stuff down the red carpet this time of the year as they collect shiny statues at ritzy award shows like the Golden Globes and Oscars. Given the vast volumes of honors bestowed, we thought what better time to put on our tuxes and create our own 2013 nominations for the economy and financial markets. If you are unhappy with our selections, you are welcome to cast your own votes in the comments section below.

By award category, here are Sidoxia’s 2013 selections:

Best Drama (Government Shutdown & Debt Ceiling): Washington D.C. has provided no shortage of drama, and the upcoming blockbusters of Shutdown & Debt Ceiling are worthy of its Best Drama nomination. If Congressional Democrats and Republicans don’t vote in favor of a new “Continuing Resolution” by March 27th, then our United States government will come to a grinding halt. At issue is Republican’s desire for additional government spending cuts to lower our deficit, which is likely to exceed $1 trillion for the fifth consecutive year. If you like more heart pumping drama, the Senate has just passed a Debt Ceiling extension through May 18th…mark those calendars!

Best Horror Film (Sequestration): Most people have already seen the scary prequel, The Fiscal Cliff, but the sequel Sequestration deserves the horror film honors of 2013. This upcoming blood-filled movie about broad, automatic, across-the-board government cost cuts will make any casual movie-watcher scream in terror. The $1.2 trillion in spending cuts (over 10 years) are so gory, many viewers may voluntarily leave the theater early. If you are waiting for the release, Sequestration is coming to a theater near you on March 1st, unless Congress, in an unlikely scenario, cancels the launch.

Best Director (Ben Bernanke): Federal Reserve Chairman Ben Bernanke’s film, entitled, The U.S. Economy, had a massive budget of about $16 trillion dollars, based on estimates of last year’s GDP (Gross Domestic Product). Nevertheless, Bernanke managed to do whatever it took (including trillions of dollars in bond buying) to prevent the economic movie studio from collapsing into bankruptcy. While many movie-goers were critical of his directorial debut, inflation has remained subdued thus far, and he has promised to continue his stimulative monetary policies (i.e., keep interest rates low) until the national unemployment rate falls below 6.5% or inflation rises above 2.5%.

Best Foreign Film (China): Americans are not the only people who produce movies globally. A certain country with a population of nearly 1.4 billion people also makes movies too…China. In the most recently completed 4th quarter, China’s economy experienced blockbuster growth in the form of +7.9% GDP expansion. This was the fastest pace achieved by China in two whole years. To put this metric into perspective, compare China’s heroic growth to the bomb created by the U.S. economy, which registered a disappointing -0.1% contraction at the economic box office. China’s popularity should bring in business all around the globe.

Best Special Effects (Japan): After coming out with a series of continuous flops, Japan recently launched some fresh new special effects in the form of a $116 billion emergency stimulus package. The country also has plans to superficially enhance the visual portrayal of its economy by implementing its own faux money-printing program modeled after our country’s quantitative easing actions (i.e., the Federal Reserve stimulus). As a result of these initiatives, the Japanese Nikkei index – their equivalent of our Dow Jones Industrial index – has risen by +29% in less than 3 months to a level of 11,138.66 (click here for chart). But don’t get too excited. This same Nikkei index peaked at 38,957 in 1989, a far cry from its current level.

Best Action Film (Icahn vs. Ackman): This surprisingly entertaining action film features a senile 76-year-old corporate raider and a white-haired, 46-year-old Harvard grad. The investment foes I am referring to are the elder Carl Icahn, Chairman of Icahn Enterprises, and junior Bill Ackman, CEO of Pershing Square Capital Management. In addition to terms such as crybaby, loser, and liar, the 27-minute verbal spat (view more here) between Icahn (his net worth equal to about $15 billion) and Ackman (net worth approaching $1 billion) includes some NC-17 profanity. The clash of these investment titans stems from a decade-old lawsuit, in addition to a recent disagreement over a controversial short position in Herbalife Ltd. (HLF), a nutritional multi-level marketing firm.

Best Documentary (Europe): As with a lot of reality-based films, many don’t receive a lot of attention. So too has been the commentary regarding the eurozone, which has been relatively peaceful compared to last spring. Despite the comparative media silence, European unemployment reached a new high of 11.8% late last year. This European documentary is not one you should ignore. European Central Bank (ECB) President Mario Draghi just stated, “The risks surrounding the outlook for the euro area remain on the downside.”

Best Original Song (National Anthem): We won’t read anything politically into Beyonce’s lip-synced rendition of The Star-Spangled Banner at the presidential inauguration, but she is still worthy of the Sidoxia nomination because music we hear in the movies is also recorded. I’m certain her rapping husband Jay-Z agrees whole-heartedly with this viewpoint.

Best Motion Picture (Sidoxia Video): It may only be three minutes long, but as my grandmother told me, “Great things come in small packages.” I may be a little biased, but judge for yourself by watching Sidoxia’s Oscar-worthy motion picture debut:

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in HLF, Japanese ETFs, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}