Archive for March, 2014

Passive vs. Active Investing: Darts, Monkeys & Pros

Bob Turner is founder of Turner Investments and a manager of several funds at the investment company. In a recent article he reintroduces the all-important, longstanding debate of active management (“hands-on”) versus passive management (“hands off”) approaches to investing. Mr. Turner makes some good arguments for the active management camp, however some feel differently – take for example Burton Malkiel. The Princeton professor theorizes in his book A Random Walk Down Wall Street that “a blindfolded monkey throwing darts at a newspaper’s stock page could select a portfolio that would do just as well as one carefully selected by experts.” In fact, The Wall Street Journal manages an Investment Dartboard contest that stacks up amateur investors’ picks against the pros’ and random stock picks selected by randomly thrown darts. In many instances, the dartboard picks outperform the professionals. Given the controversy, who’s right…the darts, monkeys, or pros? Distinguishing between the different categorizations can be difficult, but we will take a stab nevertheless.

Arguments for Active Management

Turner contends, active management outperforms in periods of high volatility and he believes the industry will be entering such a phase:

“Active managers historically have tended to perform best in a market in which the performance of individual stocks varies widely.”

He also acknowledges that not all active managers outperform and admits there are periods where passive management will do better:

“The reason why most active investors fail to outperform is because they in fact constitute most of the market. Even in the best of times, not all active managers can hope to outperform…The business of picking stocks is to some degree a zero-sum game; the results achieved by the best managers will be offset at least somewhat by the subpar performance of other managers.”

Buttressing his argument for active management, Turner references data from Advisor Perspectives showing an inconclusive percentage (40.5%-67.8%) of the actively managed funds trailing the passively managed indexes from 2000 to 2008.

The Case for Passive Management

Turner cites one specific study to support his active management cause. However, my experience gleaned from the vast amounts of academic and industry data point to approximately 75% of active managers underperforming their passively managed indexes, over longer periods of time. Notably, a recent study conducted by Standard & Poor’s SPIVA division (S&P Indices Versus Active Funds) discovered the following conclusions over the five year market cycle from 2004 to 2008:

- S&P 500 outperformed 71.9% of actively managed large cap funds;

- S&P MidCap 400 outperformed 79.1% of mid cap funds;

- S&P SmallCap 600 outperformed 85.5% of small cap funds.

Read more about the dirty secrets shrinking your portfolio. According to the Vanguard Group and the Investment Company Institute, about 25% of institutional assets and about 12% of individual investors’ assets are currently indexed (passive strategies). If you doubt the popularity of passive investment strategies, then look no further than the growth of Exchange Traded Funds (ETFs – see chart), index funds, or Vanguard Groups more than $1 trillion dollars in assets under management.

Although I am a firm believer in passive investing, one of its shortcomings is mean reversion. This is the idea that upward or downward moving trends tend to revert back to an average or normal level over time. Active investing can take advantage of mean reversion, conversely passive investing cannot. Indexes can get very top-heavy in weightings of outperforming sectors or industries, meaning theoretically you could be buying larger and larger shares of an index in overpriced glamour stocks on the verge of collapse. We experienced these lopsided index weightings through the technology bubbles in the late 1990s and financials in 2008. Some strategies may be better than other over the long run, but every strategy, even passive investing, has its own unique set of deficiencies and risks.

Professional Sports and Investing

As I discuss in my book, there are similarities that can be drawn between professional sports and investing with respect to active vs. passive management. Like the scarce number of .300 hitters in baseball, I believe there are a select few investment managers who can consistently outperform the market. In 2007, AssociatedContent.com did a study that showed there were only 22 active career .300 hitters in Major League Baseball. I recognize in the investing world there can be a larger role for “luck,” which is difficult, if not impossible, to measure (luck won’t help me much in hitting a 100 mile per hour fastball thrown by Nolan Ryan). Nonetheless, in the professional sports arena, there are some Hall of Famers (prospects) that have proved they could (can) consistently outperform their peers for extended durations of time. Experience is another distinction I would highlight in comparing sports and investing. Unlike sports, in the investment world I believe there is a positive correlation between age and ability. The more experience an investor gains, generally the better long-term return achieved. Like many professions, the more experience you gain, the more valuable you become. Unfortunately, in many sports, ability deteriorates and muscles atrophy over time.

Size Matters

Experience alone will not make you a better investor. Some investors are born with an innate gift or intellect that propels them ahead of the pack. However, most great investors eventually get cursed by their own success thanks to accumulating assets. Warren Buffet knows the consequences of managing large amounts of dollars, “gravity always wins.” Having managed a $20 billion fund, I fully appreciate the challenges of investing larger sums of money. Managing a smaller fund is similar to navigating a speed boat – not too difficult to maneuver and fairly easy to dodge obstacles. Managing heftier pools of money can be like captaining a supertanker, but unfortunately the same rapid u-turn expectations of the speedboat remain. Managing large amounts of capital can be crippling, and that’s why captaining a supertanker requires the proper foresight and experience.

Room for All

As I’ve stated before, I believe the market is efficient in the long run, but can be terribly inefficient in the short-run, especially when the behavioral aspects of emotion (fear and greed) take over. The “wait for me, I want to play too” greed from the late 1990s technology craze and the credit-based economic collapse of 2008-2009 are further examples of inefficient situations that can be exploited by active managers. However, due to multiple fees, transaction costs, taxes, not to mention the short-term performance/compensation pressures to perform, I believe the odds are stacked against the active managers. For those experienced managers that have played the game for a long period and have a track record of success, I feel active management can play a role. At Sidoxia Capital Management, I choose to create investment portfolios that blend a mixture of passive and active investment strategies. Although my hedge fund has outperformed the S&P 500 in 4 of the last 5 years, that fact does not necessarily mean it’s the appropriate sole approach for all clients. As Warren Buffet states, investors should stick to their “circle of competence” so they can confidently invest in what they know. That’s why I generally stick to the areas of my expertise when I’m actively investing in stocks, and fill in the remainder of client portfolios with transparent, low-cost, tax-efficient equity and fixed income products (i.e., Exchange Traded Funds). Even though the actively managed Turner Funds appear to have a mixed-bag of performance numbers relative to passively managed strategies, I appreciate Bob Turner’s article for addressing this important issue. I’m sure the debate will never fully be resolved. In the meantime, my client portfolios will aim to mix the best of both worlds within active and passive management strategies in the eternal quest of outwitting the darts, monkeys, and other pros.

Read the full Bob Turner article on Morningstar.com

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds but had no direct position in stocks mentioned in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

The Buyback Bonanza Boost

With the S&P 500 off -1% from its all-time record high, many bears have continued to wait for and talk about a looming crash. For the naysayers, the main focus has been on the distorted monetary policies instituted by the Federal Reserve, but as I pointed out in Fed Fatigue is Setting In, QE and tapering talk are not the end-all, be-all of global financial markets. One need not look further than the dozen or so countries listed in the FT that have bond yields below the abnormally low yields we are experiencing in the U.S. (10-Year Treasury +2.75%).

Although there are many who believe a freefall is coming, much like a trampoline, a naturally occurring financial mechanism has provided a relentless bid to boost stock prices higher…a buyback bonanza! How significant have corporate stock repurchases been to spring prices higher? Jason Zweig, in his Intelligent Investor column, wrote the following:

In the Russell 3000, a broad U.S. stock index, repurchased $567.6 billion worth of their own shares—a 21% increase over 2012, calculates Rob Leiphart, an analyst at Birinyi Associates, a research firm in Westport, Conn. That brings total buybacks since the beginning of 2005 to $4.21 trillion—or nearly one-fifth of the total value of all U.S. stocks today.

To further put this gargantuan buyback bonanza into perspective, a recent Fox Business article described it this way:

Companies spent an estimated $477 billion on share buybacks last year. That’s enough to buy every NFL team 12 times over, run the federal government for 50 days or host the next nine Olympic Games with several billion left to spare. This year, companies are expected to ramp up buybacks by 35%, according to Goldman Sachs.

The bears continue to scream, while purple in the face, that the Fed’s QE and zero interest rate program (ZIRP) shenanigans are artificially propping up stock prices. The narrative then states the tapering and inevitable Fed Funds rate reversal will cause the market to come crashing down. While there is some truth behind this commentary, history reminds us that not all rate rising cycles end in bloodshed (see 1994 Bond Repeat or Stock Defeat?). Even if you believe in Armageddon, this rate reversal scenario is unlikely to happen until mid-2015 or beyond.

And for those worshipping the actions of Ms. Yellen at the Fed altar, believe it or not, there are other factors besides monetary policy that cause stock prices to go up or down. In addition to stock buybacks, there are dynamics such as record corporate profits, rising dividends, expanding earnings, reasonable valuations, improving international economies, and other factors that have contributed to this robust bull market.

At the end of the day, as I have continued to argue for some time, money goes where it is treated best – and generally that is not in savings accounts earning 0.003%. There is no reason to be a perma-bull, and I have freely acknowledged the expansion of froth in areas such as social media, biotech, Bitcoin and other areas. Regardless, there is, and will always be areas of speculation, in bull and bear markets (e.g., gold in the 2008-2009 period).

Magical Math

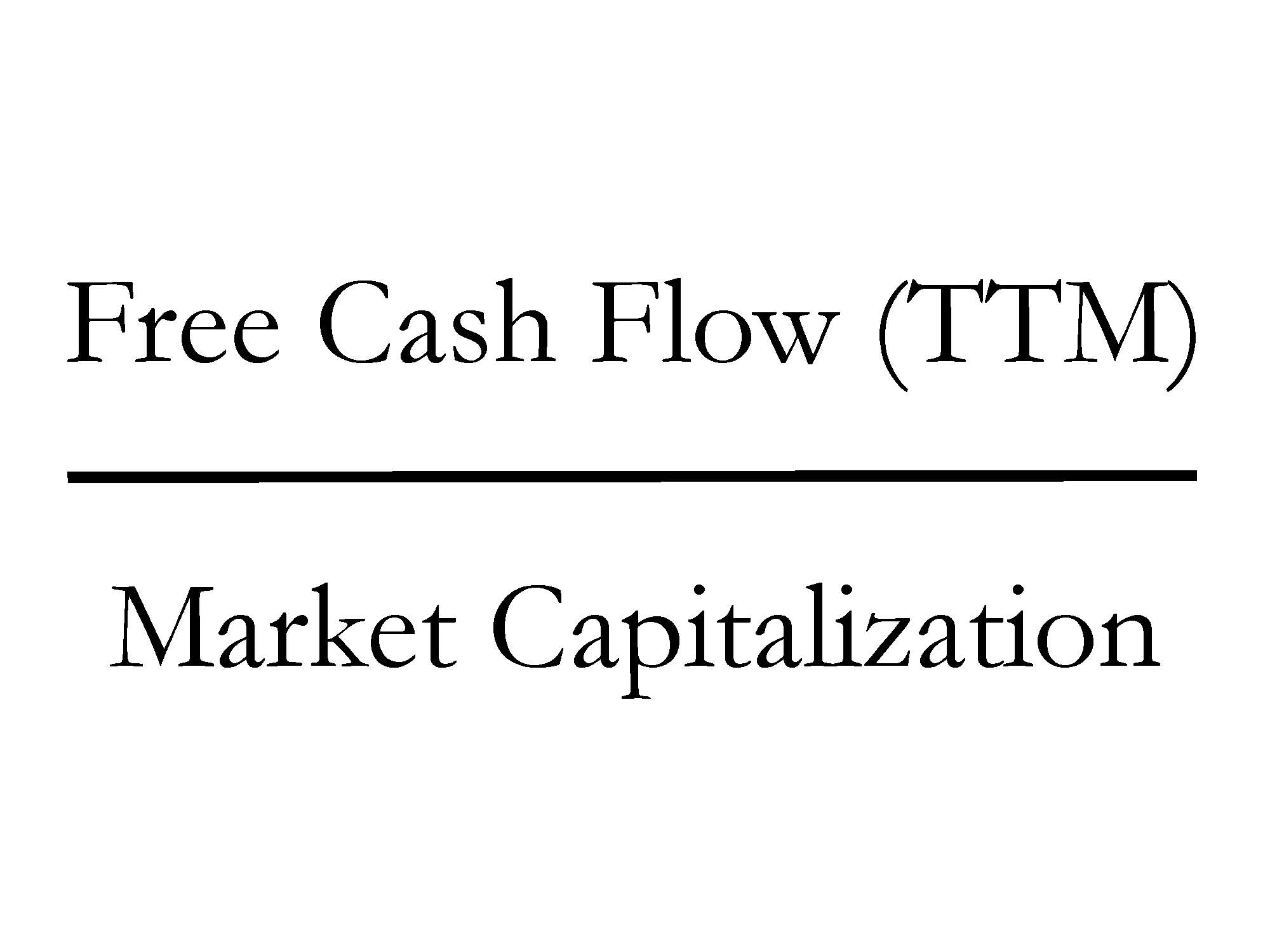

Investing involves a mixture of art and science, but with a few exceptions (i.e., fraud), numbers do not lie, and using math when investing is a good place to start. A simple but powerful mathematical formula instituted at Sidoxia Capital Management is the “Free Cash Flow Yield”, which is a metric we integrate into our proprietary SHGR (a.k.a.,“Sugar”) quantitative model (see Investing Holy Grail).

Quite simply, Free Cash Flow (FCF) is computed by taking the excess cash generated by a company after ALL expenses/expenditures (marketing, payroll, R&D, CAPEX, etc.) over a trailing twelve month period (TTM), then dividing that figure by the total equity value of a company (Market Capitalization). Mechanically, FCF is calculated by taking “Cash Flow from Operations” and subtracting “Capital Expenditures” – both figures can be found on the Cash Flow Statement. The Free Cash Flow ratio may sound complicated, but straightforwardly this is the leftover cash generated by a business that can be used for share buybacks, dividends, acquisitions, investments, debt pay-down, and/or placed in a banking account to pile up.

The great thing about FCF yields is that this ratio (%) can be compared across asset classes. For example, I can compare the FCF yield of Apple Inc – AAPL (+9.5%) versus a 10-Year Treasury (+2.75%), 1-year CD (+0.85%), Tesla Motors – TSLA (0.0%), Netflix, Inc – NFLX (-0.001%), or Twitter, Inc – TWTR (-0.003%). For growth and capital intensive companies, I can make adjustments to this calculation. However, what you quickly realize is that even if you assume massive growth in the coming years (i.e., $100s of millions in FCF), the prices for many of these momentum stocks are still astronomical.

An important insight about the current corporate buyback bonanza is that much of this price boost is being fueled by the colossal free cash flow generation of corporate America. Sure, some companies are borrowing through the debt markets to buy back stock, but if you were the Apple CFO sitting on $159,000,000,000 in cash earning 1%, it doesn’t make a lot of sense to sit on the cash earning nothing. It also doesn’t take a genius (or Carl Icahn) to figure out borrowing at record low rates (2.75% 10-year) while earning +10% on a stock buyback will increase shareholder value and earnings per share (EPS). More specifically, when Apple borrowed $17 billion at interest rates ranging from 0.5% – 3.9%, a shrewd, rational human being would borrow to the max all day long at those rates, if you could earn +10% on that investment. It is true that Apple’s profitability could drop and the numerator in our FCF ratio could decrease, but with $45 billion smackers coming in every year on top of $142 billion in net cash on the balance sheet, Apple has a healthy margin of safety to make the math work.

Where the math doesn’t compute is in insanely priced deals. For example, the recent merger in which Facebook Inc (FB) paid $19 billion (1,000 x’s the estimated 2013 annual revenues) for a 50-person, money-losing company (WhatsApp) that is offering a free service, makes zero financial sense to me. Suffice it to say, the FCF yield on WhatsApp could cause Warren Buffett to have a coronary event. Yes, diamond covered countertops would be nice to have in my kitchen, but I probably wouldn’t get much of a return on that investment.

Share buybacks are not a magical elixir to endless prosperity (see Share Buybacks & Bathroom Violators), but given the record profits and record low interest rates, basic math shows that even if stock prices correct (as should be expected), the trampolining effect of this buyback bonanza will provide support to the market.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds (ETFs), AAPL and a short position in NFLX, but at the time of publishing SCM had no direct position in TSLA, TWTR, FB, Bitcoin, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Investing, Housing, and Speculating

We all know there was a lot of speculation going on in the housing market during 2005-2007 as risk-loving adventurists loaded up on NINJA loans (No Income, No Job, and No Assets) and subprime CDS (Credit Default Swap) securities. But there is a different kind of speculation going on now, and it isn’t tied directly to housing. Instead of buying a house with no down payment and a no interest loan, speculators are leaping into other hazardous areas of danger. Like a frog jumping from lily pad to lily pad, speculators are now hopping around onto money-chasing industries, including biotech, social media, Bitcoin, and alternative energy.

As French novelist Jean-Baptise Alphonse Karr noted, “The more things change, the more they stay the same.” Irrespective of the painful consequences of the bubble-bursting aftermaths, human behavior and psychology addictively succumb to the ever-seductive emotion of greed. Over the last 15 years, massive fortunes have been gained and lost while chasing frothy financial dreams in areas like technology, housing, and gold.

Most get-rich-quick dream chasers have no idea of how to invest in or value a stock, but they sure know a good story when they hear one. Chasing top performing stocks is lot like jumping off a bridge – anyone can do it, and it feels exhilarating until you hit the ground. However, there is a better way to create wealth. Despite rampant speculation, most individuals understand the principles behind buying a house, which if applied to stocks, can make you a superior investor, and assist you in avoiding dangerous, speculative investments.

Here are some valuable housing insights to improve your stock buying:

#1.) Price is the Almighty Variable: Successful real estate investors don’t make their fortunes by chasing properties that double or triple in value. Buying a rusty tool shed for $1 million makes about as much sense as Facebook paying $19 billion (1,000 x’s the estimated 2013 annual revenues) for a money-losing company, WhatsApp. Better to buy real estate when there is blood in the street. Like the stock market, housing is cyclical. Many traders believe that price patterns are more important than the actual price. If squiggly, technical price moving averages (see Technical Analysis article) make so much money for stock-renting speculators, then how come day traders haven’t used their same crossing-lines and Point & Figure software in the housing market? Yes, it’s true that the real estate transactions costs and illiquidity can be costly for real estate buyers, but 6% load fees, lockup periods, 20% hedge fund fees, and 9% margin rates haven’t stopped stock speculators either.

#2). Cash is King: It doesn’t take a genius to purchase a rental property – I know because practically half the people I know in Southern California own rental properties. For example, if I buy a rental property for $1 million cash, is it a good purchase? Well, it depends on how much after-tax cash I can collect by renting it out? If I can only net $3,000 per month (3.6% annualized return), and be responsible for replacing roofs, fixing toilets, and evicting tenants, then perhaps I would be better off by collecting 6.5% from a low-cost, tax-efficient exchange traded real estate fund, without having to suffer from all the headaches that physical real estate investing brings. Forecasting future asset price appreciation is tougher, but the point is, understanding the underlying cash flow dynamics of a company is just as important as it is for housing purchases.

#3). Debt/Leverage Cuts in Both Directions: Adding debt (or leverage) to a housing or stock investment can be fantastic if prices go up, and disastrous if prices go down. Putting a 20% down payment on a $1 million house works out wonderfully, if the price of the house increases to $1.2 million. My $200,000 down payment is now worth $400,000, or up +100%. The same math works in reverse. If the price of the home drops to $800,000, then my $200,000 down payment is now worth $0, or down -100% (ouch). Margin debt on an equity brokerage account works in a similar fashion, but usually a 50% down payment is needed (less risky than real estate). That’s why I always chuckle when many real estate investors tell me they steer clear of stocks because they are “too risky”.

#4). Growth Matters: If you buy a home for $1 million, is it likely to be worth more if you add a kitchen, tennis court, swimming pull, third floor, and putting green? In short, the answer is yes. The same principle applies to stocks. All else equal, if a company based in Los Angeles, establishes new offices in New York, London, Beijing, and Rio de Janeiro, and then acquires a profitable competitor at a discounted price, chances are the company will be much more valuable after the additions. The key concept here is that asset values are not static. Asset valuations are impacted in both directions, whether we are talking about positive growth opportunities or negative disruptions.

Overall, speculatively chasing performance is tempting, but if you don’t want your financial foundation to crumble, then build your successful investment future by sticking to the fundamentals and financial basics.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct discretionary position in FB, Bitcoin, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Speculative Animal (Hamster) Spirits on the Rise

“Winning is a habit. Unfortunately, so is losing.”

– Vince Lombardi

And one thing is for sure…day traders have a habit of losing. Like a hamster on a spinning wheel, day traders use a lot of energy in creating loads of activity, but end up getting nowhere in the process. This subject is important because the animal (hamster) spirits are on the rise as evidenced by the 22% and 17% increase in average client trades per day reported last month by TD Ameritrade (TD) and Charles Schwab (SCHW), respectively.

The statistics speak for themselves, and the numbers are not pretty. An often cited study by Terrence Odeon (U.C. Berkely) and Brad Barber (U.C. Davis) showed that 80% of active traders lose money. The duo came to this conclusion over six years of research by studying 66,465 accounts. More importantly, they “found that if you were to look at the past performance of these traders, only 1 percent of them could be called predictably profitable.” Uggh!

How can this horrendous performance be? Especially when we are continually bombarded with the endless commercials of talking babies and perpetual software bells & whistles that shamelessly promote and pledge a simple path to prosperity. The answer to why active trading fails for the overwhelming masses is the following:

- Taxes/Capital Gains

- Transactions costs/commissions

- Research costs/software

- Lack of institutional advantages (speed, beneficial rates, I.T./automation, execution, etc.)

- Impact costs (buying handicaps returns by pushing purchase prices higher, and selling handicaps returns by pushing sale prices lower)

- Absence from participation in long-term upward drift in equity prices

After considering the horrible odds stacked against the active trader, the atrocious results are not surprising.

The Blemished Investing Brain

So far, we’ve discussed the mechanics behind the money-losing results of active trading, but the underlying reasons can be further explained by the three-pound, 100,000,000,000 amalgamation of cells located between our ears. Evolution has formed our brains to seek pleasure and avoid pain, and trading stocks can create a rush like no other activity. Similar to the orgasmic emotions triggered by making a quick buck at the blackjack table in Las Vegas or scratching off a winning number on a lottery ticket, buying and selling stocks creates comparable effects.

Through the use of high-powered, multi-million imaging technology (i.e., functional-MRI), Brian Knutson, a professor of neuroscience and psychology at Stanford University discovered that active trading for money impacts the brain in a similar fashion as do sex and drugs. The data is pretty compelling because you can see the pleasure center images of the brain light up dynamically in real time.

To put the results of his human trading experiments in context, Knutson noted:

“We very quickly found out that nothing had an effect on people like money — not naked bodies, not corpses. It got people riled up. Like food provides motivation for dogs, money provides it for people.”

Brokerage firms and casinos have figured out the greed-seeking weakness in human brains and exploited this vulnerability to the maximum. By rigging the system in their favor, mega-billion dollar financial institutions and gaming empires continue to sprawl around the globe.

The emotional high experienced by day traders is one explanation for the excessive trading, but there is another contributing factor. The inherent human cognitive bias that behavioral finance academics call overconfidence (or illusory superiority) helps fuel the destructive behavior. Surveys that ask people if they are above-average drivers highlight the overconfidence phenomenon by showing the mathematical impossibility of having 93% of a population as above-average drivers. Similarly, a study of Stanford MBA students showed 87% of the respondents rating their academic performance above median.

Even, arguably the greatest trader of all-time, Jesse Livermore realized the negative impacts of emotions and active trading when he said, “It was never my thinking that made big money for me. It always was my sitting.” As I’ve written in the past, active trading is hazardous to your long-term wealth. Rather than succumbing to the endless pitfalls of day trading and getting nowhere like a hamster on a spinning wheel, it’s better to use a long-term, objective and unemotional investing process to achieve investment success.

See also: Brain Scans Show Link Between Lust for Sex and Money

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct discretionary position in TD, SCHW, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Market Expands and So Does Sidoxia’s Team

This article is an excerpt from a previously released Sidoxia Capital Management complementary newsletter (March 3, 2014). Subscribe on the right side of the page for the complete text.

After a brief pause at the beginning of the year, the stock market built on the tremendous gains of 2013 (S&P 500 up +30%) by reaching record highs again in February by expanding another +4.3% for the month. My investment management and financial planning firm, Sidoxia Capital Mangement, LLC, has been expanding as well. Just this last month, we added a key investment and financial planning professional (Keith C. Bong, CFA, CPA Press Release) with more than 25 years of experience in the fields.

The Record Setting Advance Continues

Now entering the sixth year of this record setting bull market, many investors and pundits have been surprised by the strength and duration of the advance. At the nadir of the financial crisis, the stock market reached a multi-year low of 666 on March 9, 2009. For comparison purposes, the S&P 500 recently closed at 1,845, almost tripling in value since the crisis lows. Pessimists and skeptics, who locked in losses during the crisis plunge, have watched the explosive gains while sitting on their hands. While I freely admit, the low-hanging fruit has been picked, many of the doubters are still calling for a collapse as “troubling news continues to pour in from all over the planet.” However, what the naysayers neglect to acknowledge is the fact that S&P 500 reported profits, the lifeblood of bull markets, have also tripled in value. Despite what the bears say, not everything is a speculative house of cards.

Late to the Party Because of Uncertainty

Although the stock party has lasted five years thus far, individuals have only begun buying for about one year (see ICI fund flows data in Here Comes the Dumb Money) – about +$28 billion of new money in 2013 and another +$12 billion so far this year (ICI data through February 19th). After approximately six years and -$600 billion in stock sales (2007-2012), it’s no wonder investors have been slow to reverse course. Adding to the angst, investors have been bombarded with an endless stream of political and economic concerns on a daily basis, leading to the late arrival of most individuals to the stock investing party. While it’s true that more people have joined the party in recent months, floods of investors are still waiting outside in the cold. Here are a few reasons for the tardiness:

- Geopolitical Concerns: Most recently it was Syria, Iran, and Argentina that got short-term traders chewing their fingernails…now it’s the Ukraine. Just yesterday, I had to spend about 10 minutes locating the Ukranian province of Crimea on a map. For those who have not been keeping track, after days of civil unrest that left some 75 protesters dead, Ukrainian President Viktor Yanukovych fled the capital city of Kiev and agreed with opposition leaders to reduce his powers and hold early presidential elections later this year. For context, in 1954, the former Soviet Union leader Nikita Khrushchev transferred Crimea from the Russian Soviet republic to Ukraine on the basis of economic ties that were closer with Kiev than with Moscow. Prior to that transfer, Russia seized Crimea from the declining Ottoman Empire in the 18th century. Fast forward to today, and fresh off a successful Olympics in Sochi, Russia, Russian President Vladimir Putin hasn’t been happy about the citizen uprising in neighboring Ukraine, so he has decided to flex his muscles and move Russian troops into Crimea. The situation is very fluid and the U.S., along with other global leaders, are crying foul. Time will tell if this situation escalates into a military conflict like the 2008 Georgia-Russia crisis, or if cooler heads prevail.

- Fed Policy Concerns: Federal Reserve Chair Janet Yellen gave her inaugural address last month before Congress, where she signaled continuity in policy with former Fed Chair Ben Bernanke. Indications remain strong that the reduction of bond buying stimulus (i.e., “tapering”) will continue in the months ahead, despite mixed economic results. The “Polar Vortex” occurring on the East Coast, coupled with a record draught on the West Coast contributed to the recent reduction of Q4-2013 GDP growth figures, which were revised lower to +2.4% growth (from +3.2%).

- Domestic Politics: In a sharply politically divided country like the U.S., is there ever a complete hugs & kisses consensus? In short, “no”. How can there be 100% agreement when sharply divisive issues like Obamacare, immigration, tax reform, entitlements, budgets, and foreign affairs are always in flux? Layer on a Congressional midterm election this November and you have a recipe for uncertainty.

Because of all this uncertainty, there are still literally trillions of dollars in cash sitting on the sidelines, waiting to come join the fun. But uncertainty is a relative term because there is always doubt surrounding geopolitics, economics, and Washington D.C. Sentiment moves like a pendulum from fear to greed. Eventually panic/fear sways back the other direction as business/consumer confidence overshadow the deep scarred emotions of 2008-09. As the stock markets have grinded to record highs, fear and skepticism have slowly begun to erode.

Sidoxia Uncertainty

Speaking of uncertainty, I too encountered many doubters and skeptics when I started my firm, Sidoxia Capital Management, LLC in early 2008. Great timing, I thought at the time, as our economy entered the worst recession and financial crisis in a generation and the walls of our nation’s financial system were caving in.

With virtually no company assets or revenues at the time, this was the backdrop as I embarked on my entrepreneurial journey. Seemingly secure investment banking pillars like Bear Stearns and Lehman Brothers, which each had been around for more than a century, crumbled within the blink of an eye. As bailouts were occurring left and right, in conjunction with recurring multi-hundred point collapses in the Dow Jones Industrial index, cynics would repeatedly ask me, “Wade it’s great that you have a lot of experience, but how are you going to gain clients?” It was a fair and reasonable question at the time, but perseverance and hard work have allowed Sidoxia to beat the odds. Publishing several books, conducting numerous media appearances, and gaining thousands of social media followers (InvestingCaffeine.com) hasn’t hurt in building Sidoxia’s brand either.

After achieving record growth in the first five years of the firm, Sidoxia more than doubled its assets under management again in 2013. More important than all of the previously mentioned achievements has been our ability to service our clients with a disciplined, customized process that has demonstrated strong long-term results and helped solidify our valued relationships.

A Few Party Animals Getting Reckless at the Stock Party

Success for Sidoxia or any investor has not come easy over the last six years. As I wrote in a Series of Unfortunate Events, we’ve had to navigate our clients’ investment assets through the following events and more:

- Flash Crash

- Debt Ceiling Debates-Brinksmanship

- U.S. Debt Downgrade

- European Recession

- Arab Spring – Tunisia, Libya, Egypt

- Greek Crisis and Potential Exit from EU

- Uncertain U.S. Presidential Elections

- Sequestration

- Cyprus Financial Crisis

- Income Tax Hikes

- Federal Reserve Tapering

- Syrian Civil War / Military Threat

- Government Shutdown

- Obamacare & Its Glitches

- Iranian Nuclear Threat

- Argentinian Currency Collapse

- Polar Vortex

- Ukrainian Instability

It is no small feat that stock markets have made new records in the face of these daunting concerns. But simply ignoring scary headlines won’t earn you an investing trophy. Successful investing also requires controlling temptation and greed. At a celebratory bash, there are always irresponsible party animals, just like there are always reckless speculators gambling in the financial markets. It certainly is possible to party responsibly without getting crazy during festivities and still have fun. Even though the majority of investors currently are behaving well, as substantiated by the reasonable P/E ratio being paid (15x’s estimated 2014 profits) there are a few foolish players. Pockets of speculative fervor can be found in several areas of the financial markets. Here are a few:

- Bitcoin Breakdown: The world’s largest Bitcoin exchanged filed for bankruptcy after it lost 750,000 Bitcoin units, worth about $477,000,000, based on current exchange rates. The popularity of this speculative virtual currency seems eerily similar to the great Dutch Tulip-Mania of the 1630s.

- Biotech Bliss: Ignorance is a bliss, and apparently so is buying biotech stocks. There’s no need to speculate on gold or Bitcoins when you can invest in the Biotechnology Index (BTK), which has already advanced +21% this year on top of a 51% gain in 2013. Over the last 5+ years, the index has more than quadrupled.

- Facebook Folly: WhatsApp with Facebook Inc’s (FB) $19 billion acquisition of the cellphone texting company? CEO Mark Zuckerberg is claiming he got a bargain by paying almost 1,000x’s the estimated annual revenue of WhatsApp ($20 million). When only a fraction of the 450 million users are paying for the service, I’m OK going out on a limb and calling this deal kooky.

- High Ticket Tesla: Tesla Motors Inc (TSLA) has become a cult stock. The company has a price tag of $30 billion despite burning $7 million in cash last year. The announcement of a $4-5 billion battery “Gigafactory” added to the company’s recent hype. To put things into perspective, General Motors (GM) has revenues 75x’s larger than Tesla and GM generated over $5 billion in 2013 free cash flow. Nevertheless, GM is only valued at 1.9x’s the market value of Tesla…head scratch.

- Social Media Silliness: Maybe not quite as wacky as the $19 billion price tag paid for WhatsApp, but the $30 billion value placed on Twitter Inc (TWTR) for a company that burned $30 million of cash in their most recent financial report is silly too. Yelp Inc (YELP) is another multi-billion valued company that is losing money. I love all these services, but great services don’t always make great stocks. Investors from the dot-com era vividly remember what happened to those overvalued stocks once the bubble burst.

Fear and greed are omnipresent, and some of these speculative areas may continue to appreciate in value. However, controlling or ignoring the powerful emotions of fear and greed will help you in achieving your financial goals. As the markets (and Sidoxia’s team) expand, our disciplined investment process should allow us to objectively identify attractive investment opportunities without succumbing to the pitfalls of panic-selling or performance-chasing.

Other Recent Investing Caffeine Articles:

Retirement Epidemic: Poison Now or Later?

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in FB, TWTR, YELP, TSLA, BTK, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Sidoxia Adds 25-Year Veteran to Team

NEWPORT BEACH, CA – (Wire-Business) – Keith C. Bong, CFA, CPA, has recently joined Sidoxia Capital Management, LLC (“Sidoxia”) as Vice President of Investments and Financial Planning. Keith brings over 25 years of experience to Sidoxia’s investment team, having worked as a Financial Consultant with Merrill Lynch, before founding the investment firm Topper Capital Management in Irvine, California.

“We are truly excited to bring such a high caliber individual like Keith on board,” stated Wade W. Slome, CFA, CFP®, President and Founder of Sidoxia Capital Management. “We’re confident that Keith’s unique experience and knowledge will bring tremendous value to Sidoxia’s clients as our firm continues to expand.”

For over a decade, while managing his former advisory firm, Keith has worked closely with business owners, corporations, and individuals, assisting these clients with critical investment planning, tax planning, and financial planning goals.

“I believe my experience in building corporate retirement plan solutions meshes well with Sidoxia’s successful investment platform,” noted Keith. “I’m thrilled to join an independent firm like Sidoxia that places clients’ needs first, unlike some other financial institutions.”

To learn more about Sidoxia and Keith Bong’s background, please visit http://www.Sidoxia.com and reference the “Investment Team” section.

Click here to download a copy of the press release.

Plan. Invest. Prosper.

DISCLOSURE: No information provided here constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}