Archive for June, 2010

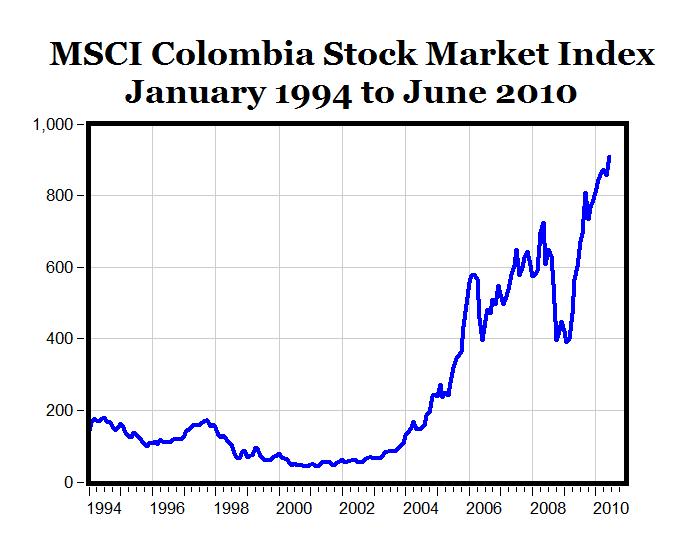

Colombia: The Hidden Latin American Gem

Judging by the all the volatility in the markets and the gloomy headlines blanketing business periodicals, one would think the global walls of capitalism and democracy were crumbling into oblivion. That’s why it’s a nice diversion to discover a diamond in the rough, shining through the darkness in the form of the Colombian stock market. How special is this South American gem? An +1,845% return over 10 years sounds pretty exceptional to me. Those are the results that Professor Dr. Mark J. Perry from the University of Michigan calculated in a posting he recently wrote about the MSCI Colombia stock market index in his blog, Carpe Diem.

Source: Carpe Diem

Fueling the surge in the equity markets has been a right-leaning, free market government with a hawkish defense stance, led by President Álvaro Uribe for the last eight years. The voters voted to continue Uribe’s mandate by voting in his former defense minister, Juan Manuel Santos, who promises to keep the disruptive guerilla forces operating under Revolutionary Armed Forces of Colombia (FARC) in check.

Colombia has been a close ally of the United States, thanks to their support of a joint crackdown on drug smuggling into the U.S. In return for their support, Colombia has received a nice fat $600 million check from the U.S. each year. What would even make our relationship tighter is an approval stamp placed on an awaiting U.S.-Colombia free trade agreement, which Congress has inexplicably kept on the backburner.

The U.S. and Colombia also agree on something else…their mutual disdain for Venezuelan leader, Hugo Chavez. Mr. Chavez poses a threat to the region, but Santos and the wave of free market leaders in the territory are more likely to wreak havoc on the Venezuelan leader according to Investor’s Business Daily:

“But Santos is probably most dangerous for Chavez, because Colombia’s rags-to-riches success story is so dramatic — showing that any beat-up nation can drag itself out of misery through markets — and because Venezuela and Colombia are such close neighbors. Word gets out about how well things are going in Colombia and it spreads fast in Venezuela. Santos need never fire a shot at Venezuela to slay Chavez’s revolution because the power of the markets will do it for him.”

Colombia’s Gross Domestic Product (GDP) is not overly large relative to some more developed neighbors, but the World Bank estimated the country’s 2008 GDP at $244 billion, almost triple the figure from five years earlier. The explosive economic growth explains how this market was the highest returning market in the world over the last decade, even eclipsing white hot markets like China, Russia, Brazil, Peru, India, and Turkey, among many others.

How does one invest in this Colombian gem? One way to gain exposure is through an exchange traded fund (ETF): Global X/InterBolsa FTSE Colombia 20 ETF (GXG). This particular ETF is concentrated into 20 positions, with heavy weightings in financial, energy, and industrial stocks. So, as you continue to read about the so-called inevitable “double-dip” recession and collapse of the U.S. dollar as the global reserve currency, please do not forget there are some brilliant free market economies, like Colombia, that are growing brilliantly and producing sparkling returns.

Read Professor Perry’s complete article on the Colombia market

Read the WSJ article written on the subject

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct positions in GXG, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Dividends: From Sapling to Abundant Fruit Tree

Dividends are like fruit and an investment in stock is much like purchasing a sapling. When purchasing a stock (sapling) the goal is two-fold: 1) Buy a sapling (tree) that is expected to bear a lot of fruit; and 2) Pay a cheap or fair price. If the right saplings are purchased at the right prices, then investors can enjoy a steady diet of fruit that has the potential of producing more fruit each year. Fruit can come in the form of future profits, but as we will see, the sweetness of a profitable company also paying dividends can prove much more fruitful over the long-term.

Investing in growth equities at reasonable prices seems like a pretty intelligent strategy, but of late the vast majority of fresh investor capital has been piling into bonds. This is not a flawed plan for retirees (and certain wealthy individuals) and should be a staple in all investment portfolios, to a degree (some of my client portfolios contain more than 80%+ in fixed income-like securities), but for many investors this overly narrow bond focus can lead to suboptimal outcomes. Right now, I like to think of bonds like a reliable bag of dried fruit, selling for a costly price. However, unlike stocks, bonds do not have the potential of raising periodic payments like a sapling with strong growth prospects. “Double-dippers” who are expecting the economy to spiral into a tailspin, along with nervous snakebit equity investors, prefer the reliability of the bagged dry fruit (bonds)… no matter how high the price.

How Sweet is the Fruit? How Does a +2,300% Yield Sound?

Not only do equities offer the potential of capital appreciation, but they also present the prospect of dividend hikes in the future – important characteristics, especially in inflationary environments. Bonds, on the other hand, offer static fixed payments (no hope of interest rate hikes) with declining purchasing power during periods of escalating general prices.

Given the possibility of a “double-dip” recession, one would expect corporate executives to be guarding their cash with extreme stinginess. On the contrary, so far in 2010, companies have shown their confidence in the recovery by increasing or initiating dividends at a +55% higher clip versus the same period last year. Underpinning these announcements, beyond a belief in an economic recovery, are large piles of cash growing on the balance sheets of nonfinancial companies. According to Standard & Poor’s (S&P), cash hit a record $837 billion at the end of March, up from $665 billion last year.

The S&P 500 dividend yield at 2.06% may not sound overwhelmingly high, but with CDs and money markets paying next to nothing, the Federal Funds rate at effectively 0%, and the 10-Year Treasury Note yielding an uninspiring 3.11%, the S&P yield looks a little more respectable in that light.

If the stock market yield doesn’t enthuse you, how does a +2,300% yield sound to you? That’s roughly what a $.05 (split adjusted) purchase of Wal-Mart (WMT) stock in 1972 would be earning you today based on the current $1.21 dividend per share paid today. That return alone is mind-blowing, but this analysis doesn’t even account for the near 1,000-fold increase in the stock price over the similar timeframe. That’s what happens if you can find a company that increases its dividend for 37 consecutive years.

Procter & Gamble (PG) is another example. After PG increased its dividend for 54 consecutive years, from a split-adjusted $.01 per share in 1970 to a $1.93 payout today, original shareholders are earning an approximate 245% yield on their initial investment (excluding again the massive capital appreciation over 40 years). There’s a reason investment greats like Warren Buffett have invested in great dividend franchises like WMT, PG, KO, BUD, WFC, and AXP.

Bad Apples do Exist

Dividend payment is not guaranteed by any means, as evidenced by the dividend cuts by financial institutions during the 2008-2009 crisis (e.g., BAC, WFC, C) or the discontinuation of BP PLC’s (BP) dividend after the Gulf of Mexico oil spill disaster. Bonds are not immune either. Although bonds are perceived as “safe” investments, the interest and principal payment streams are not fully insured – just ask bondholders of bankrupt companies like Lehman Brothers, Visteon, Tribune, or the countless other companies that have defaulted on their debt promises.

This is where doing your homework by analyzing a company’s competitive positioning, financial wherewithal, and corporate management team can lead you to those companies that have a durable competitive advantage with a corporate culture of returning excess capital to shareholders (see Investing Caffeine’s “Education” section). Certainly finding a WMT and/or PG that will increase dividends consistently for decades is no easy chore, but there are dozens of budding possibilities that S&P has identified as “Dividend Aristocrats” – companies with a multi-year track record of increasing dividends. And although there is uncertainty revolving around dividend taxation going into 2011, I believe it is fair to assume dividend payment treatment will be more favorable than bond income.

Apple Allocation

Growth companies that reinvest profits into new value-expanding projects and/or hoard cash on the balance sheet may make sense conceptually, but dividend paying cultures instill a self-disciplining credo that can better ensure proper capital stewardship by corporate boards. All too often excess capital is treated as funny money, only to be flushed away by overpaying for some high-profile acquisition, or meaningless share buybacks that merely offset generous equity grants to employees.

So, when looking at new and existing investments, consider the importance of dividend payments and dividend growth potential. Investing in an attractively priced sapling with appealing growth prospects can lead to incredibly fruitful returns.

Read the Whole WSJ Article on Dividends

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and WMT, but at the time of publishing SCM had no direct positions in BAC, WFC, C, BP, PG, KO, BUD, WFC, AXP, Lehman Brothers, Visteon, Tribune, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Forecasting Recipe: Trend Analysis & Sustainability

Forecasting financial performance of a company requires a fairly simple recipe: one part trend analysis and one part determining sustainability. On the surface, forecasting sounds pretty easy. While discovering certain financial trends can be straightforward, the ability to ascertain the durability of a trend can become endlessly complex.

Before you become Nostradamus and spreadsheet your way to the Wall Street Hall of Fame, an accurate forecaster must first build a firm understanding of a company and the underlying industry. Unfortunately for the predictor, not all companies and industries are created equally. Evaluating the profit dynamics of Cheesecake Factory Inc. (CAKE), an upscale casual chain of restaurants, is quite different from deciphering the financials of 3SBio (SSRX), a Chinese biotech company focused on recombinant products. Regardless of the thorniness of the company or industry, before you can truly look out into the future, the investor should learn the language of the company. For example, learning the importance of “comparable store sales” and “sales per square foot” for CAKE may be just as important as learning about the “Phase III FDA trial endpoint” and “pipeline” for SSRX.

Because you could spend a lifetime following just one company – for instance General Electric Co. (GE) or Microsoft Corp. (MSFT) – and never make an investment, you would probably be better served by applying a framework that allows you to research and analyze multiple industries and companies. There are various tools, whether you consider Harvard professor Michael Porter’s Five Forces or SWOT analysis (Strengths Weaknesses Opportunities Threats), and each provides a template or process to use when tearing apart specific companies and industries.

Nuts & Bolts of Forecasting

Before you can identify a trend, you first need to gather the data. For all companies I examine, I first compile a quarterly and annual income statement, balance sheet, and cash flow statement – those that have followed me know the extreme importance I place on the cash flows of a business. In general a good start is to create common size financial statements for the income statement and balance sheet. Basically, this exercise creates an income statement and balance sheet in percentage terms – usually expressed as a percentage of net sales (income statement) and as a percentage of total assets (balance sheet). Earnings forecasts are often used as a logical starting point for driving the shape of future results across the financials, but further insight can be gleaned by comparing year-over-year (this year vs. last) and sequential (this quarter vs. last quarter) growth rates for key figures.

These common statements will then serve as the foundation of identifying the trends, and force the forecaster to seek answers to random questions like these?

- Why is depreciation expense going down even though the company is expanding retail stores?

- Gross margins increased for seven consecutive quarters for a total of 250 basis points (2.5%), however in the recent quarter margins declined by 175 basis points…why?

- Long-term debt increased by $200 million in the current quarter, but if the company just issued $325 million in equity last quarter, then why do they need new capital?

Many of these types of questions may have logical explanations, but by getting answers the analyst will be in a position to better understand the business issues affecting financial performance and to better forecast future economic values.

Forecasting Your Way to Wrongness

A lot can go wrong with forecasting, principally in the assumptions used for the forecast. As the character Felix Unger from the Odd Couple stated, “You should never “assume.” You see, when you “assume,” you make an “ass”… out of “you”… and “me.”” Often assumptions do not consider the inclusion of important economic shocks or unexpected factors, such as recessions, currency fluctuations, management turnover, lawsuits, accounting changes, new products, restructurings, acquisitions, divestitures, flash crashes, Greek debt downgrades, regulatory reform…yada…yada…yada (you get the idea). To get a better sense for a range of outcomes, sensitivity analysis can be employed to determine a “base case” outcome in conjunction with a rosier “upside case” and more conservative “downside case.” Worth noting is the impact debt levels can have on the variance of outcomes – I think Bear Stearns and Lehman Brothers would concur with this point.

Pinpointing variable financial figures is quite difficult. Different companies and industries inherently have more or less predictable attributes. Predicting when the sun will rise and set is quite a bit more predictable than predicting what Intel Corp’s (INTC) gross margins will be on a quarterly basis. As mentioned earlier, layering on debt can increase the volatility of earnings forecasts as well.

Forecasting is essential in the investment world, but even if you were the best forecaster in the world, investors cannot disregard the importance of valuation skills. The art of valuation is just as important, if not more important than being right on your financial scenarios.

All in all, the recipe of forecasting sounds simple if you look at the basic ingredients of trend and sustainability analysis. However, before the ultimate forecast comes out of the oven, this straightforward recipe requires a lot of preparation, whether it is slicing and dicing cash flow figures, whipping up some margin trends, or measuring up sales growth. Any way you cut it, systematically following a recipe of trend and sustainability analysis is a non-negotiable requirement if you want to heat up superior financial results.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct positions in GE, MSFT, CAKE, SSRX, INTC, JPM/Bear Stearns, Lehman Brothers, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

The Accomplished Mole – Seth Klarman

I do quite a bit of reading and in my spare time I came across something very interesting. Here are some of the characteristics that describe this unique living mammal: 1) You will rarely see this creature in the open; 2) It roams freely and digs in deep, dark areas where many do not bother looking; and 3) This active being has challenged eyesight.

If you thought I was talking about a furry, burrowing mole (Soricomorpha Talpidae) you were on the right track, but what I actually was describing was legendary value investor Seth Klarman. He shares many of the same features as a mole, but has made a lot more money than his very distant evolutionary cousin.

The Making of a Legend

Photo source: SuperInvestorDigest.com

Before becoming the President of The Baupost Group, a Boston-based private investment partnership which manages about $22 billion in assets on behalf of wealthy private families and institutions, he worked for famed value investors Max Heine and Michael Price of the Mutual Shares (purchased by Franklin Templeton Investments). Klarman also published a classic book on investing, Margin of Safety, Risk Averse Investing Strategies for the Thoughtful Investor, which is now out of print and has fetched upwards of $1,000-2,000 per copy in used markets like Amazon.com (AMZN).

Klarman chooses to keep a low public profile, but recently his negative views on stock market and inflation risk have filtered out into the public domain. Nonetheless, he is still optimistic about certain distressed opportunities and believes the financial crisis has cultivated a more favorable, less competitive environment for investment managers due to the attrition of weaker investors.

Philosophy

Klarman despises narrow mandates – they are like shackles on potential returns. Opportunities do not lay dormant in one segment of the financial markets. Investors are fickle and fundamentals change. He believes superior results are achieved through a broadening of mandates. He prefers to invest in areas off the proverbial beaten path – the messier and more complicated the situation, the better. Currently his funds have significant investments in distressed debt instruments, many of which were capitulated forced sales by funds that are unable to hold non-investment grade debt.

In order to make his wide net point to investing, Klarman uses real estate as an illustration device. For example, investors do not need to limit themselves to publicly traded REITs (Real Estate Investment Trusts) – they can also invest in the debt of a REIT, convertible real estate debt, equity of property (such as own building), bank loan on a building, municipal bond that’s backed by real estate, or commercial/residential mortgage backed securities.

Klarman summarizes his thoughts by saying:

“If you have a broader mandate, they let you own all kinds of debt, all kinds of equity. Perhaps some private assets, like real estate. Perhaps hold cash when you can’t find anything great to do. You now have more weapons at your disposal to take advantage of conditions in the market.”

Klarman’s 3 Underlying Investment Pillars

Besides mentors Heine and Price, Klarman is quick to highlight his investment philosophy has been shaped by the likes of Warren Buffett and Benjamin Graham, among others. In addition to many of the basic tenets espoused by these investment greats, Klarman adds these three main investment pillars to his repertoire:

1) Focus on risk first (the probability of loss) before return. Determine how much capital you can lose and what the probability of that loss is. Also, do not confuse volatility with risk. Volatility creates opportunities.

2) Absolute performance, not relative performance, is paramount. The world is geared towards relative performance because of asset gathering incentives. Wealthy investors and institutions are more focused on absolute returns. Focus on benchmarks will insure mediocrity.

3) Concentrate on bottom-up research, not top down. Accurately forecasting macroeconomic trends and also profiting from those predictions is nearly impossible to do over longer periods of time.

These are great, but represent just a few of his instructional nuggets.

Performance

I did some digging regarding Klarman’s performance, and given the range of markets experienced over the last 25+ years, the results are nothing short of spectacular. Here is what I dug up from the Outstanding Investor Digest:

“Since its February 1, 1983 [2008] inception through December 31st, his Baupost Limited Partnership Class A-1 has provided its limited partners an average annual return of 16.5% net of fees and incentives, versus 10.1% for the S&P 500. During the “lost decade”, Baupost obliterated the averages, returning 14.8% and 15.9% for the 5 and 10-year periods ending December 31st versus -2.2% and -1.4%, respectively, for the S&P.”

Here is some additional color from Market Folly on Klarman’s incredible feats:

“Despite Klarman’s typically high levels of cash [sometimes in excess of 50%], Baupost has still generated astonishing performance. It was up 22% in 2006, 54% in 2007, and around 27% in 2009. During the crisis in 2008, Klarman’s funds lost “between 7% and the low teens.” Still though, he certainly outperformed the market indices and much of his investment management brethren in a time of panic.”

Although Seth Klarman has plowed over the competition and remained underground from the mass media, it’s still extremely difficult to ignore the long-term record of success of this accomplished mole. In the short-run, volatility may hurt his performance – especially if holding 20-30% cash. But as I was told at a young age by my grandmother, it is not prudent to make mountains out of molehills. Apparently, Klarman’s grandma taught her mole-like grandson how to make mountains of money from hills of opportunities. Klarman’s investors certainly stand to benefit as he continues to dig for value-based gems.

Watch interesting but lengthy presentation video given by Seth Klarman

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, and AMZN, but at the time of publishing SCM had no direct positions in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Debt Control: Turn Off Costly Sprinklers When Raining

By living in Southern California, I am acutely aware of the water shortage issues we face in this region of the country. We all have our pet peeves, and one that eats at me repeatedly occurs when I drive by a neighbor’s house and notice they are blasting the sprinklers in the pouring rain. I get the same sensation when I read about out-of control government spending confronting our current and future generations in light of the massive debt loads we presently carry.

I, like most people, love free stuff, whether it comes in the form of tooth-pick skewered, teriyaki meatball samples at Costco Wholesale Corp. (COST), or free government education from our school systems. But in times of torrential downpours, at a minimum, we need to be a little more cost conscious of our surroundings and turn off the spending sprinklers.

Certainly, when it comes to government spending, there’s no getting around the entitlement elephant in the room, which accounts for the majority of our non-discretionary government spending (see D-E-B-T: New Four Letter Word article). Unfortunately, layering on new entitlements on top of already unsustainable promises is not aiding our cause. For example, showering our Americans with free drugs as part of Medicare Part D program, and paying for tens of millions into a fantasy-based universal healthcare package (purported to save money…good luck) only serves to fatten up the elephant squeezed into our room.

Reform is absolutely necessary and affordable healthcare should be made available to all, but it is important to cut spending first. Then, subsequently, we will be in a better position to serve the needy with the associated savings. Instead, what we chose appears to have been a jamming of a massive, complex, divisive bill through Congress.

Slome’s Spending Rules

In an effort to guide ourselves back onto a path of sensibility, I urge our government legislators to follow these basic rules as a first step:

Rule #1 – Don’t Pay Dead People: I know we have an innate maternal/paternal instinct to help out others, but perhaps our government could stop doling out taxpayer dollars to buried individuals underground or those people incarcerated in jail? Over the last three years the government sent $180 million in benefit checks to 20,000 corpses, and also delivered $230 million to 14,000 convicted felons (read more).

Rule #2 – Pay for Our Own First: Before we start spending money on others outside our borders, I propose we tend to our flock first. For starters, our immigration policies are a disaster. As I wrote earlier (read Our Nation’s Keys to Success), I am a big proponent of legal immigration for productive, higher-educated individuals – not elitist, just practical. If you don’t believe me, just count the jobs created by the braniac immigrant founders at the likes of Google Inc. (GOOG), Intel Corp. (INTC), and Yahoo! Inc. (YHOO). These are the people who will create jobs and out-battle scrappy, resourceful international competitors that want to steal our jobs and our economic leadership position in the world. What I don’t support is illegal immigration – paying for the healthcare and education of foreign criminals with our country’s maxed-out credit cards. This is the equivalent of someone breaking into my house, and me making their bed and feeding them breakfast…ridiculous. I do not support the immigration law passed in Arizona, but this unfortunate chain of events thankfully puts a spotlight on the issue.

Rule #2a. – Stop Being the Globe’s Free Police: If we are going to comb the caves of Tora Bora as part of funding two wars and chasing terrorists all over the world, then we not only should be spending our defense budget more efficiently (non-Cold War mentality), but also charging freeloaders for our services (directly or indirectly). We are spending a whopping 20 cents of each federal tax dollar on defense, so let’s spend it wisely and charge those outside our borders benefiting from our monetary and physical sacrifices. And, oh by the way, sending $400 million to the territory controlled by Hamas (read more) doesn’t sound like the brightest decision given our fiscal and human challenges at home. I sure hope there are some tangible, accountable benefits accruing to the right people when we have 25 million people here in the U.S. unemployed, underemployed, or discouraged from finding a job.

Rule #3: Put the Obese Elephant on a Diet – As I alluded to above, our government doesn’t need to serve our overweight, entitlement-fed elephant more chocolate, pizza, and ice cream in the form of more entitlements we are not capable of funding. Let’s cut our spending first before we buy off the voters with new spending.

There are obviously a wide ranging set of economic, political, and even religious perspectives on the best ways of managing our hefty debt and deficits. I do not pretend to have all the answers, but what I do know is it is not wise to blast the sprinklers when it is pouring rain outside.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, and GOOG, but at the time of publishing SCM had no direct positions in COST, YHOO, INTC, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Marathon Investing: Genesis of Cheap Stocks

It was Mark Twain who famously stated, “The reports of my death have been greatly exaggerated.” So too has the death of equities been overstated. Long-term stock bulls don’t have a lot to point to since the market, as measured by the S&P 500 index, has done absolutely nothing over the last 12 years (see Lost Decade). Over the last 10 years, the market is actually down about -20% without dividends (and about flat if you account for reinvested dividends). So if equities belong at the morgue, why not just short the market, burn your dollars, and hang out in a cave with a pile of gold? Well, behind the scenes, and off the radar of nanosecond, high frequency, day-trading CNBC junkies, there has been a quiet but deliberate strengthening in the earnings foundation of the market. In the investing world it’s difficult to move forward through sand. Even without a sturdy running foundation, sprinters can race to the front of the pack, but those disciplined runners who systematically train for marathons are the ones who successfully make it to the finish line.

Prices Chopped in Half

What many pundits and media mavens fail to recognize is S&P corporate profits have virtually doubled since 1998 (a historically elevated base), despite market prices stuck in quicksand for a dozen years. What does this say about the valuation of the market when prices go nowhere and profits double? Simple math tells us that all stock market inventory is selling for -50% off (the market multiple has been chopped in half). That’s exactly what we have seen – the June 1998 market multiple (valuation) stood around 27x’s earnings and today’s 2010 earnings estimates imply a multiple of about 13.5 x’s projected profits. With the rear-view mirror assisting us, it’s easy to understand why pre-2000 (tech bubble) valuations were expensive. By coupling more reasonable valuations with a 10-Year Treasury Note trading at 3.19% and lofty bond prices, I would expect stocks to be poised for a much better decade of relative performance versus bonds. The case becomes even stronger if you believe 2011 S&P 500 estimates are achievable (12x’s earnings).

In order to make the decade long valuation contraction more apparent, I wanted include a random group of stocks (mixture of healthcare, media, retailer, consumer non-discretionary, and financial services) to liven up my argument:

Data sources: S&P, ADVFN & Yahoo! Finance

What Next?

From a stock market standpoint, there are certainly plenty of believable “double dip” scenarios out there along with thoughtful observers who question the attainability of next year’s earnings forecasts. With that said, I do have problems with those bears like John Mauldin (read The Man Who Cries Wolf) who just last year pointed to a market trading at a “(negative) -467” P/E ratio, only to subsequently watch stocks advance some 80%+ over the following months.

Regardless of disparate economic views, I contend objective market observers (even bearish ones) have trouble indicating the market is ridiculously expensive with a straight face – based on current corporate profit expectations. At the end of the day, sustainable earnings and cash flow growth are what ultimately drive durable, long-term price appreciation. As Peter Lynch stated with technical precision, “People may bet on hourly wiggles of the market but it’s the earnings that waggle the wiggle long term.”

Running a marathon is always challenging, but with a sturdy foundation in which prices have been chopped in half (see also Market Dipstick article), reaching the goal and finish line for long-term investors will be much more achievable.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, WMT, and PAYX, but at the time of publishing SCM had no direct positions in ABT, CI, DIS, FRX, KO, KSS, MDT or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Private Equity Sitting on Stuffed Wallet

The clock is ticking and private equity (PE) firms need to put some $445 billion in their wallets to work. Otherwise, the dreams of outsized returns and hefty fees will have to wait for another Golden Era of deal making. Why such a hurry to use the cash? According to Andrea Auerbach, a Managing Director at Cambridge Associates, “Most funds legally have five or six years to invest that capital…it’s use it or lose it.”

Shop ‘til Wallet Drops

As easy as it sounds, spending half a trillion dollars can be difficult. Here’s how IBD’s Norm Alster characterizes the challenge:

“To realize the outsize profits investors expect, private equity firms would have to borrow two or three times that amount. But for the most part, credit spigots for such deals are still dry. At the same time, pinning down buyout targets is not that easy. Many potential sellers are balking at parting with corporate assets in the midst of a serious downturn.”

The 2010 private equity environment is quite a bit different than the LBO boom era from a handful of years ago, as you can see from the chart below. Thanks to cheap, free-flowing funding from the banks, $1.4 trillion worth of deals were consummated in 2006 and 2007, including large deals like First Data Corp. ($27 billion deal – KKR); Alltel ($28 billion – Goldman Sachs/ Texas Pacific Group); and Harrah’s ($30 billion – Apollo Management/Texas Pacific Group). Unfortunately, deals done during this period were done when valuations and leverage were at extremely high historical levels.

Chart source: Thomson Reuters via IBD

Deal Timeout

What’s causing the current dearth of deals? In many instances, business owners have not calibrated valuation expectations downward enough to account for the bruising financial crisis. Given the 77 leveraged buyout defaults in 2009, investors have become more reticent in committing capital as well. Refinancing the mountains of debt associated with the troubled 2006-07 vintage of deals will require patience and creative financing skills from the banks.

Because of the logjam of deals created by the financial crisis, PE firms are actively looking for exit strategies relating to their portfolio companies. Since private equity inherently involves illiquid investments, typically the industry creates liquidity through initial public offerings (IPOs), merger & acquisitions, and/or recapitalization structures that partially or fully return investor capital.

If the economic malaise lingers and valuations remain depressed, I have no doubt owners will eventually return to the negotiating table while waving a white towel in hand. Until then, private equity firms will continue begging for capital from the banks (i.e., using “other peoples’ money”) and beating down sellers into submission with regards to price expectations. If PE firms are not successful in using that wad of cash by the end of the fund’s term, then investors will be free to walk away with their money without paying lucrative fees to the PE firms.

Don’t Forget Benefits

The PE field is facing its fair share of trials and tribulations, but PE’s diversification benefits should not be forgotten. The success of the “Yale Model,” implemented by David Swensen, has come under attack with the recent bursting of the credit bubble, but with the ever-swinging performance pendulum of various asset classes/styles moving in and out of favor, I am confident a consistent strategy integrating PE as a portion of a diversified portfolio will yield respectable risk-adjusted returns over the long-run. Like other areas in the financial services industry, fees are being scrutinized and transparency requests by investors (limited partners) have been on the rise. But first things first – before attractive PE profits can be made as part of a diversified portfolio, the wad of cash in the wallets of PE firms must find a home in portfolio companies.

Read Norm Alster’s full IBD article originally referenced on TRB

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including S&P 500-like positions), but at the time of publishing SCM had no direct positions in GS, Harrah’s or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Ray Allen, the VIX, and the Rule of 16

Photo Source: Babble.com

Ray Allen gets paid a lot of money for running into people and bouncing an orange ball around a wooden floor, but even his game can appreciate the importance volatility can play in a high stakes game. First, Allen set an NBA Final’s basketball record of eight three-pointers made (including seven in a row) in Game 2, and then followed up in the next game with an astonishingly dismal “O” for thirteen performance – the second worst shooting performance during a Final’s game in 32 years. The emotional rollercoaster ride for the Celtics fans resembles a volatility chart of the VIX (Volatility Index) in recent weeks.

Chart Source: Yahoo! Finance

In the last 40 trading days the VIX has moved more than +/- 5% on 30 different trading sessions (75% of the time), including seventeen +/- 10% trading days. The +32% spike in the VIX on the day of the “Flash Crash” (May 6, 2010) would have even generated a smirk on the face of Ray Allen, not to mention the face changing impact of the other three +/- 30% move days that occurred within a month of the Flash Crash trading debacle. Even though the VIX has settled down from a short-term peak last month (48.20 on May 21st) to a lower level (28.79), the fear gauge still stands at almost double the rate of the multi-year low just a few months ago (15.23 on April 12th).

The VIX and the Rule of 16

No, this VIX is not the same as the Vicks vapor rub medication placed on your chest to relieve cough symptoms, rather this VIX indicator calculates inputs from various call and put options to create an approximation of the S&P 500 index implied volatility for the next 30 days. Put simply, when fear is high, the price of insurance catapults upwards as measured by the VIX – just like we saw when the VIX spiked above 80 during the 2008 financial crisis and above 40 during the more fresh Greek debt disaster. I’m not in the position to bust out some differential calculus to explain the nuances of a complex VIX formula, but what I can do is regurgitate a helpful formula relating to the VIX, called the Rule of 16. What the Rule of 16 allows laymans to do is understand the relationship between the VIX and daily volatility.

This is how Jeff Luby of Green Faucet describes the Rule of 16:

• VIX of 16 – 1/3 of the time the SPX will have a daily change of at least 1%

• VIX of 32 – 1/3 of the time the SPX will have a daily change of at least 2%

• VIX of 48 – 1/3 of the time the SPX will have a daily change of at least 3%

To put these VIX numbers in perspective, industry citations put the long-term VIX average around a level of 20. With a VIX hovering around 30 now, we are approaching the 2nd bucket of expectations (2%+ moves in the market 1/3 of the time). The price moves don’t correlate directly with the Dow Jones Industrial Average index, but I think about the current VIX levels equating to about a +/- 200 point move in the Dow one or two times per week…uggh.

Generally, I would prefer lower volatility, but I continually remind myself volatility is not necessarily a bad thing – volatility creates opportunities. I’m not sure if I can apply the Rule of 16 to Ray Allen’s scoring output, however based on last night’s 5-10 shooting performance, perhaps volatility in the market and Ray Allen’s shooting game will begin to normalize toward historical ranges.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including S&P 500-like positions), but at the time of publishing SCM had no direct positions in SPX, VIX-related securities, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Margin Surplus Retake

Like a B-rated horror movie using the same old cliques (i.e., girl home alone with serial killer on the loose or a concealed intruder hidden in the back seat of a car), one of the financial cliques that persists today is the belief that the United States trade deficit will result in financial ruin for our economy. The recent widening of the trade deficit to $40.3 billion makes this economic issue a topical discussion. Enter Andy Kessler, former hedge fund manager and author of Running Money. He believes the stale, exploding trade deficit arguments are hogwash, primarily due to his “margin surplus” theory articulated in his book and Wall Street Journal article entitled, We Think, They Sweat.

Profiting from Trade Deficits

The absolute numbers used by Kessler in his Toshiba laptop example might have changed since his book was first published in 2004, but this margin surplus theory example is just as relevant today as it was back then. Here is an excerpt from his book:

“Let’s open up that Toshiba laptop. With a $300 Intel chip (which has at least $250 in profit for Intel) and a $50 Windows license ($49.95 margin to Microsoft), the laptop is then sold by Toshiba back into the U.S. for $1,000. Toshiba and every other supplier are lucky if they make $50 profit, combined, on the deal.”

In this illustration, government statistics would recognize a $1,000 contribution to our bloating trade deficit figures, even though nearly 90% of the laptop profits would be flowing (“surplus-ing”) back to the U.S. Hmmm, maybe this trade deficit thing isn’t as evil as it is portrayed in the popular media, or perhaps we are measuring it incorrectly? Kessler makes the case that Gross Domestic Product (GDP) is not the most important economic gauge, but rather the real crucial GDP metric is actually Gross Domestic PROFIT. He adds the best indicator for economic profits is the stock market, and as foreigners seek more productive returns on their cash beyond the 3% Treasury yields, they will eventually filter back their dollar currency reserves into stocks and other more productive asset classes.

Brain Driven Economy

You don’t have to be a brain surgeon to realize our roots as an industrial economy have shifted to an intellectual property economy. So while we may be exporting low-skilled labor jobs to China and other low-cost regions, our country is also creating higher-skilled, higher-paying jobs at innovative growing companies such as Google Inc. (GOOG) and Apple Inc. (AAPL). Case in point, flip an Apple iPod over and read the fine print on the back – it reads, “Assembled in China…Designed by Apple in California.” Once again, the commoditized aspects of slapping together a widget have been outsourced to workers in far-off lands for a small fraction of what American workers earn. If improving the standard of living is our goal, then transferring low paying jobs to foreigners should not be a concern. According to Kessler, $70 in iPod profits (versus $4 for the Chinese assemblers) from this unique, differentiated device has generated millions in profits, which in turn can be used for the creation of desirable, high-paying jobs here in the U.S.

Selling the Farm

Warren Buffets has a different view about our trade deficits and the directional value of the U.S. dollar. He perceives our economy as a fixed size farm that is selling $2 billion pieces of the farm to foreigners on a daily basis. Buffet adds:

“We’re like a very rich family; we own a farm the size of Texas but want to consume more. If you force-feed $2 billion a day to the rest of the world, they get somewhat less enthusiastic over time – and the dollar is worth less.”

Over time, Buffett believes future generations will resent paying for the gluttony of consumption by prior generations and foreigners will demand a higher interest rate for their loans. What I believe Buffet fails to consider is that the farm is not static. As we sell off $2 billion chunks of the farm, portions of those proceeds are being used to adjoin additions, buy new farms, build adjacent wind turbines, and/or incorporate other productive uses. Now if the proceeds were used to solely purchase bon-bons and doughnuts, then indeed we would be in trouble. Ultimately, the financial markets will be the true arbiter of how efficiently the foreign capital is being invested and will dictate the level of rates paid on the loans. From a pure cash management standpoint, stretching out payables (net imports) is a sound practice (i.e., it’s desirable to collect early and pay late).

The flip side of the argument explains how the farm sale proceeds from our asset sales to foreigners (such as our real estate, our Treasuries, and our stocks) can be employed in a productive manner. The Buffett argument states that our farm will eventually be completely sold to foreigners or they will hold a gun to our head asking for higher interest rates to fund our deficits. The problem with that argument is that the money received from the farm sales (Treasuries, stocks, real estate, etc.) can be (and is) used to build new farms. And that is the key question…are all these deficit building dollars being used to create new, innovative, job creating companies like Google and Apple, or are these dollars being redeployed into unproductive uses (e.g., worthless t-shirts and lead-filled toys from China, or funding of bailouts and cash-for-clunkers waste) ?

At the end of the day, money goes where it is treated best – meaning global capital seeks the royal treatment in markets where profits reign supreme. So rather than relying on rusty, obsolete statistics measuring the balance of trade (i.e., trade deficits and GDP), investors would be better served by taking a page from Andy Kessler’s book. Following the principles of “margin surplus” will increase the probabilities of profiting from global capital flows.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, Treasury securities, GOOG, and AAPL, but at the time of publishing SCM had no direct positions in Toshiba, INTC, BRKA/B or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Microchip: Selling Electronic Cake Mix to the World

Microchip Technology Inc. (MCHP) is not in the business of selling cakes. Rather, Microchip is more akin to a chef selling cake mix in the form of microcontrollers to hungry designers with a sweet tooth. All that the customers need to do is add some water to the mix, and voila they have all the ingredients necessary to make a cake.

Endless Opportunities

Making a cake may sound simple, but the real magic comes as a result of the baking chef exploring the endless possibilities across colors, flavors, sizes, frostings, and accessories. The microcontroller business is similar in many respects. Microchip provides the essential tools (ingredients) to efficiently and cost-effectively build solutions for an almost infinite number of applications. Microcontrollers can be found in a diverse mix of products and gizmos, ranging in size from an iPod Nano (AAPL) and Tickle Me Elmo toy to a Whirlpool (WHR) washing machine and a butt-warming car seat in a Porsche 911 Turbo. From a verticals standpoint, Microchip services more than 60,000 customers globally (75% of revenues internationally) in the automotive, aerospace, communications, computing, consumer, and industrial control markets, among others.

What the Heck is a Microcontroller?

You can think of a microcontroller as a computer-on-a-chip, and these mini-computers, which are embedded into all types of applications, allow designers to create all types of products. The low-cost computer chips handle simple functions such as turning products on and off and setting speeds in consumer products, cars, telecommunications and office equipment. More specifically, these microcontrollers provide designers with the ability to introduce or expand functionality, reduce power consumption, and create further efficient designs, thereby potentially leading to lower costs and higher profits. Even though talking about the digital world of 1’s and 0’s sounds sexy, in the real world we are surrounded by analog factors like time, temperature, sound, music, and video – analog functions that require the heavy lifting of a microcontroller to process digital data after it has been converted from analog.

These microcontrollers aren’t multi-hundred dollar microprocessors manufactured in multi-billion fabrication facilities at Intel Corp. (INTC) – rather these more mundane (although essential) components sell often for a few bucks each. What’s more, the pricing in microcontroller and analog land is more stable at Microchip relative to the annual -20-30% price cuts common in the microprocessor world.

On top of performance (speed, power, heat, etc.) and cost, ease of design is a way Microchip gains market share away from competitors through its PIC architecture – the software platform that designers program Microchip’s microcontrollers. The company devotes extensive resources to spreading the PIC gospel to designers around the world and Microchip engineers are constantly upgrading the programming software. To date, Microchip has almost shipped 1,000,000 development tools to designers and developers. The software and design kits add to the company’s revenues, but the real profitability kicks in when the customers reorder chips related to multiyear product life cycles. For example, you can think of a television company that must order a microcontroller for a five-year old, broken TV remote control that a child stepped on…hmm, sounds familiar.

Expanding Pie (or Cake)

This is no puny market; the overall microcontroller segment of the semiconductor market is estimated to have generated $10.7 billion in sales during 2009. Microchip has managed to not only become the 800 pound gorilla in the 8-bit microcontroller space, but in recent years they have also made significant headroom in the higher functionality/performance markets of 16-bit and 32-bit microcontrollers. In total, Microchip offers its customers more than 650 flavors of its microcontroller products.

One would think the company is busy enough with its core microcontroller business, but Microchip is not sitting on its hands. They are employing a Velcro strategy by attaching other embedded features on its “computer-on-a-chip,” including analog, memory, DSP (digital signal processing), and other capabilities. Already, Microchip’s analog business has grown to more than 10% of the company’s revenues (about 600 analog products and > 14,000 customers), and Microchip’s foray into the digital signal controller sector (dsPIC product family) is expanding the company’s total addressable market as well. Consistent with this Velcro strategy, Microchip recently purchased Silicon Storage Technology Inc. (SST) for $354 million, focusing on SST’s high margin flash memory licensing business. Thanks to shrewd negotiating and jettisoning of non-core SST segments, the deal will solidify Microchip’s embedded solution positioning and is expected to add $.14 – $.18 cents to Microchip’s 2011 earnings per share (EPS).

The Head Chef

The head chef of the technology kitchen is Steve Sanghi, and in 1990 (after 10 years of employment at Intel Corp.), when he took over as President of Microchip, the kitchen was a complete mess. Not only was the company losing money, but they were spread too thin across disparate technologies. His accomplishments were recognized immediately and Sanghi became CEO shortly thereafter in 1991. Microchip, which was originally founded in 1989 as a spinoff from General Instrument, eventually went public in 1993. Despite a tough technology market post the technology crash of 2000, Microchip has managed to gain market share from struggling competitors like Atmel Corp. (ATML). Under Sanghi’s leadership, Microchip has more than doubled profits over the last decade and sales have almost multiplied 12-fold to $950 million since the company went public 17 years ago.

Cash Machine

Besides pumping out microcontrollers, Microchip pumps out a lot of cash as well. In their recently completed fiscal year (ending in March), the company generated close to $400 million in free cash flow (cash from operations minus capital expenditures), by my definition. With a market capitalization of around $5 billion this relationship implies an almost 8% free cash flow yield – a bit nicer than the 3.17% yield recently offered on the federal government’s 10-year Treasury Note. Microchip’s cash metrics look even that much more impressive when you consider the company has more than $1.1 billion in net cash piled up on the balance sheet. Since the capital intensity of the microcontroller and analog businesses is so much less demanding than the microprocessor world, Microchip has plenty of flexibility in paying a nice, big fat, 5%+ dividend (about $1.37 per share annually), which has increased modestly in each of the last three quarters. On a Price-Earnings basis (P/E), Microchip’s share price is currently trading at an attractive 13 x’s the company’s $2.11 consensus Earnings-Per-Share (EPS) estimate.

Risks

Microchip is not a risk-free Treasury investment and the company faces significant cyclical sensitivity to global macroeconomic trends, as we saw in fiscal 2009 (ending March). The pace of global design activity will generally be responsive to overall business confidence. In spite of Microchip’s dominance in the 8-bit market, some skeptics also question Microchip’s ability to gain market share in the 16-bit and 32-bit markets.

In addition to those concerns, another hazard relates to the company overpaying for future, potential acquisitions. Traditionally Microchip has focused on internal growth, however in recent years the company’s appetite for acquisitions has increased – most notably the failed merger of Atmel Corporation for roughly $2.3 billion in early 2009. If history serves as a guide, Microchip has been prudent in acquisitions – for example, the timely $183 million purchase of Gresham, Oregon manufacturing plant in 2002 for cents on the dollar or the recent opportunistic and accretive SST deal.

Momentum and Visibility Improving

With the global upturn occurring, Microchip has seen a +189% increase in its backlog (orders in hand for future delivery) to $528 million. Having these orders in hand allows Microchip to plan and invest more appropriately for growth in the coming year. Fourth quarter sales (without SST’s contribution) increased by more than +60% from last year and Non-GAAP earnings mushroomed by more than +200% on a year-over-year basis.

The ease and affordability of new product design will be an accelerating trend of new product proliferation. As I wrote in an earlier article (Revenge of David), the simplicity of design has become dramatically easier. A laptop and internet connection affords any designer the ability of downloading free design software, building a prototype with a 3-D printer, ordering Chinese manufacturing services through Taobao.com (parent Alibaba Group), and waiting for UPS to deliver the product to their doorstep in fairly short order. This design tailwind only serves to increase demand for Microchip’s microcontroller solutions over time.

Ever since the company’s IPO (Initial Public Offering), Microchip has had a phenomenal track record of success led by Steve Sanghi’s direction. Microchip is a much more mature company since going public in 1993 at a stock price of $0.57 per share (split-adjusted), but if the stock price can appreciate a fraction of the +4,623% already achieved, then my clients and I should be able to purchase a lot of cake mix.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, MCHP, AAPL, and Treasury securities, but at the time of publishing SCM had no direct positions in WHR, Porsche, Volkswagen, INTC, ATML, SST, UPS, General Instrument, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}

{kind=link}