Archive for October, 2013

Sitting on the Sidelines: Fear & Selective Memory

Fear is a motivating (or demotivating) emotion that can force individuals into suboptimal actions. The two main crashes of the 2000s (technology & housing bubbles) coupled with the mini-crises (e.g., flash crash, European crisis, debt ceiling, sequestration, fiscal cliff, etc.) have scared millions of investors and trillions of dollars to sit on the sidelines. Financial paralysis may be great in the short-run for bruised psyches and egos, but for the passive onlookers, the damage to retirement accounts can be crippling.

Selective memory is a great coping mechanism for those investors sitting on the sidelines as well. Purposely forgetting your wallet at a group dinner may be beneficial in the near-term, but repeated incidents will result in lost friends over the long-run. Similarly, most gamblers frequenting casinos tend to pound their chests when bragging about their wins, however they tend to conveniently forget about all the losses. These same reality avoidance principles apply to investing.

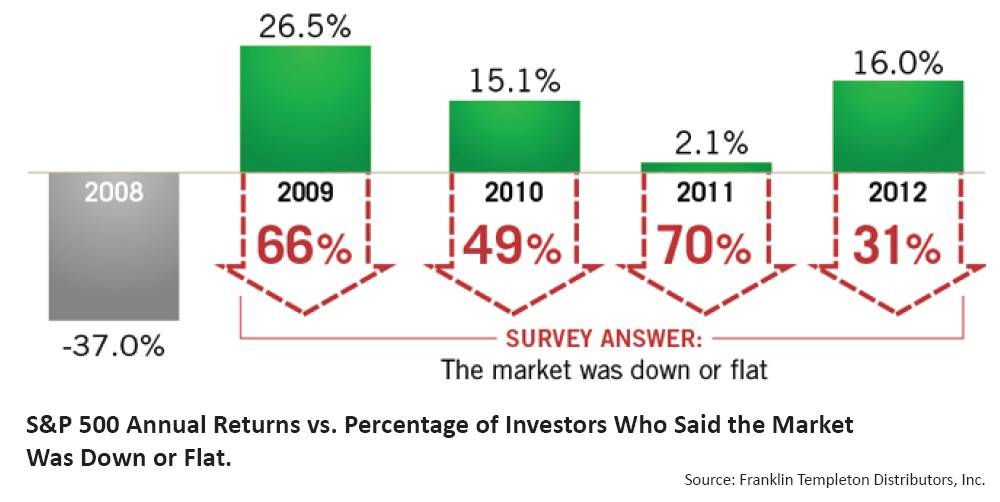

A recent piece written by CEO Bill Koehler at Tower Wealth Managers, entitled The Fear Bubble highlights a survey conducted by Franklin Templeton. In the study, investors were asked how the stock market performed in 2009-2012. As you can see from the chart below, perception is the polar opposite of reality (actual gains far exceeded perceived losses):

Source: Franklin Templeton via Tower Wealth Managers

With so many investors sitting on the sidelines in cash or concentrated in low-yielding bonds and gold, I suppose the results shouldn’t be too surprising. Once again, selective memory serves as a wonderful tool to bury the regrets of missing out on a financial market recovery of a lifetime.

Humans also have a predisposition to seek out people who share similar views, even though accumulating different viewpoints ultimately leads to better decisions. Morgan Housel at The Motley Fool just wrote an article, Putting a Gap Between You and Stupid, explaining how individuals should seek out others who can help protect them from harmful biases. A scientific study referenced in the article showed how the functioning of biased brains literally shuts down:

“During the 2004 presidential election, psychologist Drew Westen of Emory University and his colleagues studied the brains of 15 “committed” Democrats and 15 “committed” Republicans with an MRI scanner. Each group was shown a collection of contradictory statements made by George W. Bush and John Kerry. Not surprisingly, the partisans were quick to call out contradictions made by the opposing party, and made up all kinds of justifications to rationalize quotes made by their own side’s candidate. But here’s what’s scary: The participants weren’t just being stubborn. Westen found that areas of their brains that control reasoning and logic virtually shut down when confronted with a conflicting view of their preferred candidate.”

Rather than letting emotions rule the day, the proper approach is to stick to unbiased numbers like valuations, yields, fees, and volatility. If you continually make mistakes; you aren’t disciplined enough; or you don’t like investing; then find a trusted advisor who uses an objective financial approach. Opportunistically taking advantage of volatility, instead of knee-jerk reactions is the preferred approach. For those people sitting on the sidelines and using selective memory, you may feel better now, but you will eventually have to get in the game, if you don’t want to lose the retirement account game.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is the information to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Teflon Market

At the pace of all this head-scratching going on, our population is likely to turn completely bald. One thing is for certain, nothing has scratched this Teflon stock market. If you want to have fun with a friend, family member or co-worker, just ask them how they feel about politics and then ask them how stocks have done this year? You’re bound to get some entertaining responses. Despite a Congress that has a lower favorability rating than cockroaches, lice, root canals, and colonoscopies , the S&P 500 index is up a whopping +22% and the NASDAQ index + 30% this year, both records. The USA Today ran with the Teflon theme and had this to say:

“This year alone the stock market has survived the recent brush with a U.S. debt default. It has also survived a government shutdown. Tax hikes. Government spending cuts. The threat of war. Terror at the Boston Marathon. A spike in interest rates. Plunging Apple shares. Stock exchange glitches. Fears of a less-friendly Federal Reserve. And a narrow escape from going over the “fiscal cliff.” Nothing bad seems to stick.”

The reason nothing is sticking to this Teflon market is because the market is more sensitive to reality rather than perception. Here are some come current discrepancies between these two states:

Perception: The economy is on the verge of a recession. Reality: The economy has grown GDP for 15 of the last 16 quarters. The private sector has added about 7.5 million jobs and the unemployment rate has been cut by about three percentage points.

Perception: Corporations are struggling. Reality: Corporations are actually posting record profits; increasing dividends significantly; buying back stock; and registering record profit margins.

Perception: The Federal Reserve controls the economy. Reality: Federal Reserve Chairman Ben Bernanke has little to no influence on decisions made by companies like Google Inc (GOOG), Facebook Inc (FB), McDonald’s Corp (MCD), Tesla Motors Inc (TSLA), and Target Corporation (TGT) (see also The Greatest Thing Since Sliced Bread). Interest rates are actually higher than when QE1 (quantitative easing) was first implemented, yet growth persists.

These types of mental mistakes occur outside the realm of financial markets as well. For example, most people fail to correctly answer the question, “Which animal is responsible for the greatest number of human deaths in the U.S.?”

A.) Alligator; B.) Bear; C.) Deer; D.) Shark; and E.) Snake

The ANSWER: C) Deer.

Deer colliding into cars trigger seven times more deaths than alligators, bears, sharks, and snakes combined, according to Jason Zweig at the Wall Street Journal (see also Alligators & Airplane Crashes). Other mental disconnects include the belief that planes are more dangerous than cars. In fact, people are 65 times more likely to get killed in your own car versus a plane. Also, misconceptions exist that guns are more dangerous than smoking, or that tornadoes are more dangerous than asthma – both beliefs wrong.

Party Not Over Yet

Long-time followers and readers of Investing Caffeine know that I’ve been an active participant in this bull market that started in 2009, evidenced by my critical views of Armageddonists like Peter Schiff, John Mauldin, Nouriel Roubini, Meredith Whitney, and other doom & gloomers.

I fully recognize there’s no honor in being Pollyannaish or a perma-bull just for the sake of it. However, it’s also very clear that excessive fear exercised by many investors proved very painful as S&P 500 level 666 has exploded to 1,744. The extreme panic that reached a pinnacle in 2009 has now morphed into an insidious skepticism (see Sentiment Pendulum ). Investor emotions continually swing from fear to greed, and with the political shenanigans going on in Washington DC, the skeptical pendulum has a long way before reaching euphoric levels. Or stated differently, the pre-party is over (see my article from earlier this year, Those Who Missed the Pre-Party), but the DJ is still playing and the cops aren’t here to break up the party yet.

I agree that we’ve had a Teflon market for a handful of years. There have been a few minimal scratches and a few hand burns along the way, but for the most part, those investors who have stayed invested and ignored the endless manufactured crisis headlines have been rewarded handsomely. Investing in stocks will always cause some heartburn, but if you don’t want your long-term retirement to get grilled, seared, pan-fried, or flambéed, then you want to make sure you still have some stocks in your Teflon pan.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), AAPL and GOOG, but at the time of publishing, SCM had no direct position in FB, TGT, TSLA, MCD, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is the information to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Nail Not in Emerging Market Coffin Yet

I wouldn’t say the nail is in the emerging market coffin quite yet. During the financial crisis, the EMSCI Emerging Market Index (EEM) was left for dead (down -50% in 2008) before resurrection in 2009 and 2010 (up +74% and +16%, respectively). For the last two years however, the EMSCI index has underperformed the S&P 500 Index massively by more than -30%. Included in this international index are holdings from China, Russia, India, Brazil, South Korea, and South Africa, among others.

The question now becomes, can the emerging markets resurrect themselves from the dead again? Recent signs are flashing “yes”. Over the last three months, the emerging markets have outperformed the S&P 500 by more than +8%, but these stocks still have a lot of ground to make up before reaching the peak levels of 2007. Last year’s slowing growth in China and a European recession, coupled with talks of the Federal Reserve’s “tapering” of monetary stimulus, didn’t provide the EMSCI index any help over the last few years.

With all the distracting drama currently taking place in Washington D.C., it’s a relief to see some other indications of improvement. For starters, China’s most recent PMI manufacturing index results showed continued improvement, reaching a level of 51.1 – up from August and signaling a reversal from contraction earlier this year (levels above 50 point to expansion). Chinese government leaders are continuing their migration from an externally export-driven economy to an internally consumer-driven economy. Despite the shift, China is still targeting a respectable +7.5% GDP economic growth target, albeit a slower level than achieved in the past.

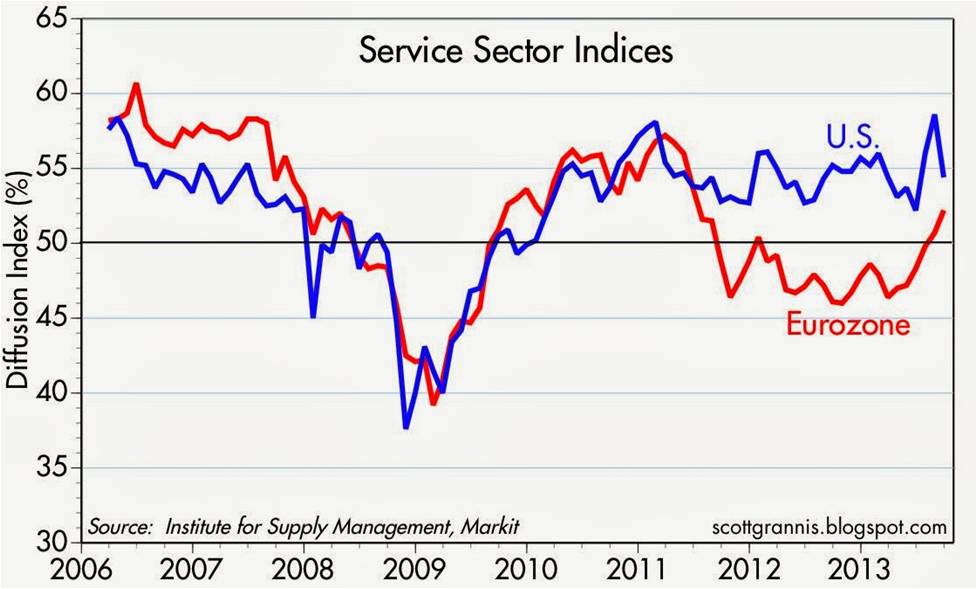

Adding to emerging market optimism is Europe’s apparent economic turnaround (or stabilization). As you can see from the chart below, the European Institute for Supply Management (ISM) service sector index has lately shown marked improvement. If the European and Chinese markets can sustain these recovering trends, these factors bode well for emerging market financial returns.

Source: Calafia Beach Pundit

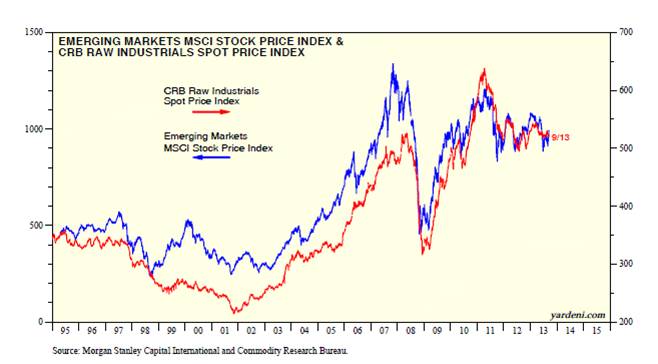

While it is clear these developments are helping the rebound in emerging market indices, it is also clear the supply-demand relationship in commodities will coincide with the next big up or down move in developing markets. Ed Yardeni, strategist and editor of Dr. Ed’s Blog, recently wrote a piece showing the tight correlation between emerging market stock prices and commodity prices (CRB Index). His conclusions come as no surprise to me given these resource-rich markets and their dependence on Chinese demand along with commodity needs from other developed countries. Expanding populations and rising standards of living in emerging market countries have and will likely continue to position these countries well for long-term commodity price appreciation. The development of new, higher-value service and manufacturing sectors should also lead to sustainably improved growth in these emerging markets relative to developed economies.

Source: Dr. Ed’s Blog

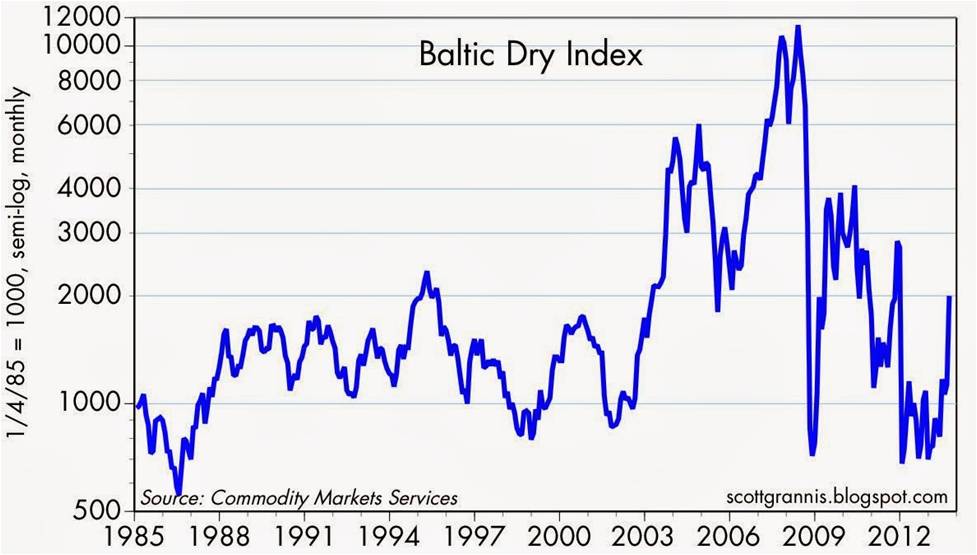

Adding fuel to the improving emerging market case is the advancement in the Baltic Dry Index (see chart below). The recent upward trajectory of the index is an indication that the price for moving major raw materials like coal, iron ore, and grains by sea is rising. This statistical movement is encouraging, but as you can see it is also very volatile.

Source: Calafia Beach Pundit

While the emerging markets are quite unpredictable and have been out-of-favor over the last few years, a truly diversified portfolio needs a healthy dosage of this international exposure. You better check a pulse before you put a nail in the coffin – the emerging markets are not dead yet.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) including emerging market ETFs, but at the time of publishing, SCM had no direct position in EEM, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is the information to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Take Me Out to the Stock Game

This article is an excerpt from a previously released Sidoxia Capital Management complementary newsletter (October 1, 2013). Subscribe on the right side of the page for the complete text.

The Major League Baseball playoffs are just about to start, and the struggling U.S. economy is also trying to score some more wins to make the postseason as well. In 2008 and early 2009, the stock market looked more like The Bad News Bears with the S&P 500 index losing -58% of its value from the peak to the trough. The overleveraged (debt-laden) financial system, banged by a speculative housing bubble, swung the global economy into recession and put a large part of the economic team onto the disabled list.

Since the lows of 2009, S&P 500 stocks have skyrocketed +152%, including an +18% gain in 2013, and a +3% jump in September alone. With that incredible track record, one might expect a euphoric wave of investors pouring into the stock market stadium, ready to open their wallets at the financial market concession stand. Au contraire. Despite the dramatic winning streak, investors remain complacent skeptics, analyzing and critiquing every political, economic, and financial market movement and gyration.

Unfortunately, as stock prices have scored massive gains, many market followers have been too busy eating peanuts and drinking beer, rather than focusing on the positive economic statistics in the scorebook, such as these:

15/16 Quarters of Positive GDP Growth:

|

| Source: Crossing Wall Street |

Precipitous Drop in Unemployment Claims: The lowest level since 2007 (7.5 million private sector jobs added since employment trough).

|

| Source: Bespoke |

All-Time Record Corporate Profits:

|

| Source: Ed Yardeni |

Financially Healthier Consumer – Lower Debt & Higher Net Worth:

|

| Source: Scott Grannis |

Improving Housing Market:

|

| Source: Scott Grannis |

While you can see a lot of financial momentum is propelling Team USA, there are plenty of observers concerned more about potential slumps and injuries emanating from a lineup of uncertainties. Currently, the fair-weather fans who are sitting in the bleachers are more interested in the uncertainty surrounding a government shutdown, debt ceiling negotiations, Syrian unrest, Iranian nuclear discussions, Obamacare defunding, and an imminent tapering of the Federal Reserve’s QE bond purchasing program (see Perception vs. Reality). The fearful skepticism of the fans has manifested itself in the form of a mountain of cash ($7 trillion), which is rapidly eroding to inflation and damaging millions of retirees’ long-term goals (see chart below). The fans sitting in the bleachers are less likely to buy long-term season tickets until some of these issues are settled.

|

| Source: Scott Grannis – $3 trillion added since crisis. |

The aforementioned list of worries are but a few of the concerns that have investors biting their nails. While there certainly is a possibility the market could be thrown a curve ball by one of these issues, veteran all-star investors understand there are ALWAYS uncertainties, and when the current list of concerns eventually gets resolved or forgotten, you can bet there will be plenty of new knuckle-balls and screw-balls (i.e., new list of worries) to fret over in the coming weeks, months, and years (see Back to the Future I, II,& III). Ultimately, the vast majority of concerns fade away.

Yoooouuuuuu’rrrreee Out!

The politicians in Washington are a lot like umpires, but what our country really needs are umpires who can change and improve the rules, especially the silly, antiquated ones (see also Strangest Baseball Rules). The problem is that bad rules (not good ones) often get put in place so the umpires/politicians can keep their jobs at the expense of the country’s best interest.

When umpires (politicians) cannot agree on how to improve the rules, gridlock actually is the next best outcome (see Who Said Gridlock is Bad?). The fact of the matter is that deficits and debt/GDP ratios have declined dramatically in recent years due in part to bitter political feuds (see chart below). When responsible spending is put into action, good things happen and a stronger economic foundation can be established to cushion future crises.

|

| Source: Scott Grannis |

There is plenty of room for improvement, but the statistics speak for themselves, which help explain why patient fans/investors have been handsomely rewarded with a homerun over the last four years. October historically has been a volatile month for the stock market, and the looming government shutdown and $16.7 trillion debt ceiling negotiations may contribute to some short-term strike-outs. However, if history proves to be a guide, stocks on average rise +4.26% during the last three months of the year (source: Bespoke), meaning the game may just not be over yet. With plenty of innings remaining for stocks to continue their upward trajectory, I still have ample time to grab my hot dog and malt during the 7th inning stretch.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in TSLA, PBI, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is the information to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}