Archive for June, 2016

Brexit Briefing

Pair of British Briefs

There is no shortage of Brexit articles, but as I compile information for my monthly newsletter later this week (subscribe at Investing Caffeine – right column), here are some of my favorite links:

1) How to Make Sense of the Brexit Turmoil (FiveThirtyEight)

2) Brexit Meltdown Charts (Ritholtz)

3) House of Commons UK-EU Economic Relations Report (Parliament Research Briefings)

4) What is article 50 and why is it so central to the Brexit debate? (The Guardian)

5) The Difference Between the EU and Euro Zone (Moody’s)

6) Brexit’s First 100 Days (Bloomberg)

7) Brexit Impact on Wimbledon Paychecks (Fox Sports)

8) Relationship Between the U.K., Britain, England, Great Britain, Ireland, Northern Island, Wales, and British Isles (Project Britain)

9) Brexit Voting Results by Age (Ben Riley-Smith – Twitter)

10) Brexit Impact on Global Economy (Wall Street Journal)

11) Brexit is Not the End of the World (Calafia Beach Pundit)

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds , but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The New Abnormal: Living with Negative Rates

Pimco, the $1.5 trillion fixed-income manager located a stone’s throw distance from my office in Newport Beach, famously (or infamously) coined the phrase, “New Normal”. As former Pimco CEO (Mohamed El-Erian) described years ago, around the time of the Great Recession, the New Normal “reflects a growing realization that some of the recent abrupt changes to markets, households, institutions, and government policies are unlikely to be reversed in the next few years. Global growth will be subdued for a while and unemployment high.”

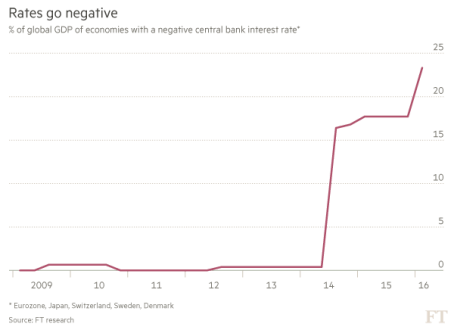

As it turns out, El-Erian was completely wrong in some respects and shrewdly prescient in others. For instance, although the job recovery has been one of the slowest in a generation, 14.5 million private sector jobs have been added since 2010, and the unemployment rate has been more than halved from 10% in early 2009, to below 5% today. However, the pace of global growth has been relatively weak since the 2008-2009 financial crisis, which has forced central banks all over the world to lower interest rates in hope of stimulating growth. Monetary policies around the globe have been cut so much that almost 25% of global GDP is tied to countries with negative interest rates (see chart below).

Source: Financial Times

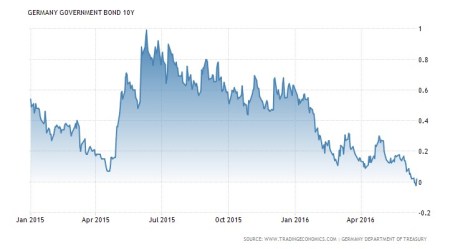

The European central banks started the sub-zero trend in 2014, and the Bank of Japan recently joined the central banks of Denmark, Sweden and Switzerland in negative territory. The negative short-term rate virus has spread further to long-term bonds as well, as evidenced by the 10-Year German Bund (sovereign bond) yield, which crossed into negative territory last week (see chart below).

Source: TradingEconomics.com

The New Abnormal

The unprecedented post-crisis move to a 0% Fed Funds rate target, along with the implementation of Quantitative Easing (QE) by former Federal Reserve Chairman Ben Bernanke, was already pushing the envelope of “normal” stimulative monetary policy. Nevertheless, central banks pushing rates to a negative threshold takes the whole stimulus discussion to another level because investors are guaranteed to lose money if they hold these bonds until maturity.

As we enter this new submerged rate phase, this activity can only be described as abnormal…not normal. Preserving money at a 0% level and losing value to inflation (i.e., essentially stuffing money under the proverbial mattress) is a bitter enough pill to swallow. Paying somebody to lend them money gives “insanity” a good name.

The stimulative objectives of negative interest policies established by central bankers may be purely intentioned, however there can be plenty of unintentional consequences. For starters, negative rates can produce too much of a good thing, in the form of excess borrowing or leverage. In addition, retirees and savers across a broad spectrum of ages are getting crushed by the paltry rates, and bank profit margins (net interest margins) are getting squeezed to boot.

Another unintended consequence of negative rate policies could be a polar opposite outcome to the envisioned stimulative design. Scott Mather, a co-portfolio manager of the $86 billion PIMCO Total Return Fund (PTTRX) is making the case that these policies could be creating more economic contractionary effects than invigorating expansion. More specifically, Mather notes, “It seems that financial markets increasingly view these experimental moves as desperate and consequently damaging to financial and economic stability.”

Eventually, the cheap money deliberately created by central banks will result in a glut of risk-taking and defaults. However, despite all the cries from hawks protesting money printing policies, cautious bank lending behavior coupled with regulatory handcuffs have yet to create widespread debt bubbles. Certainly, oceans of cheap money can create pockets of problems, as I have identified and discussed in the private equity market (see also Dying Unicorns), but supply and demand rule the day at some point.

In the end, as I have repeatedly documented, money goes where it is treated best. Realizing guaranteed losses while trapped in negative rate bonds is no way to treat your investment portfolio over the long-run. In the short-run, the safety and stability of short duration bonds may sound appealing, but ultimately rational and efficient behavior prevails. Why settle for 0% or negative rates when yields of 2%, 4%, and 6% can be found in plenty of other responsible investment alternatives?

Arguably, in this post financial crisis world we live in, we have transitioned from the New Normal to a New Abnormal environment of negative rates. Pundits and prognosticators will continue spewing fear-filled cautionary advice, but experienced, long-term investors will continue taking advantage of these risk averse markets by investing in a quality, diversified portfolio of superior yielding investments. For now, there are plenty of opportunities to choose from, until the next phase of this economic cycle… when the New Abnormal transitions to the New Normalized.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds , but at the time of publishing had no direct position in PTTRX, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Rise of the Robots

We’re losing our jobs to robots, and they will destroy our economy. It makes for a great news soundbite, but has no factual basis in reality, if you look at the actual trajectory of automation and technology innovations throughout history. The global economy did not collapse when the steam engine replaced the oar; the automobile supplanted the horse; the computer became a substitute for the abacus; and the combine killed off the farmer. The same notion holds true today as robots become more ubiquitous in our daily commercial and personal lives.

From the early, post-revolutionary birth of our country in the 18th century, the agrarian economy accounted for upwards of 90% of jobs and financial activity…until farming technology evolved (see chart below). As new agricultural advancements were introduced, like the cotton gin, plow, scythe, chemical fertilizers, tractors, combine harvesters, and genetically engineered seeds, human capital (jobs) were redeployed into other growth sectors of the economy (e.g., factories, aerospace, semiconductors, medicine, etc.).

Source: Carpe Diem

Given that human labor accounts for about 2/3 of an average company’s expense structure, it should come as no surprise that corporations are looking to reduce costs by introducing more robotics and automation into their processes. The advantages to robotics adoption are numerous and I describe many of the reasons in my article, Chainsaw Replaces Paul Bunyan:

A robot won’t ask for a raise; it always shows up on time; you don’t have to pay for its healthcare; it can work 24/7/365 days per year; it doesn’t belong to a union; dependable quality consistency is a given; it produces products near your customers; and it won’t sue for discrimination or sexual harassment.

At Sidoxia Capital Management we opportunistically identified this growing trend quite early as evidenced by our initial 2012 investment in KUKA AG (Ticker: KUKAF), a German manufacturer of industrial robots. KUKA has recently made headlines due to a bid received from Chinese home-appliance company (Midea Group: Ticker – 000333.SZ) that values the dominant German robotics leader at $5 billion. Despite KUKA’s +273% share price appreciation from the end of 2012, not many people have heard of the company. While KUKA may not have caught the attention of many U.S. investors, the company has captured a bevy of blue-chip global customers, including Daimler, Airbus Group, Volkswagen, Fiat, Boeing, and Tesla.

Rather than sitting on its hands, KUKA has done its part to develop a higher profile. In fact, President Barack Obama and German Chancellor Angela Merkel recently received a robotics demonstration from KUKA’s CEO Till Reuter at the world’s largest industrial technology trade fair in Hannover, Germany this April (picture below)

Source: Bloomberg

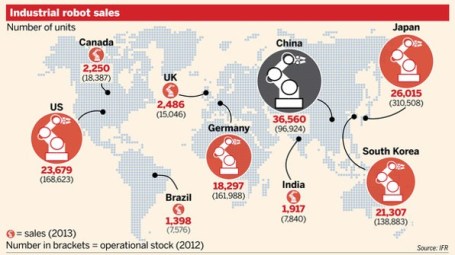

The recent multi-billion dollar bid by Midea Group has turned some onlookers’ heads, but what the potential deal really signals is the vast opportunity for robotics expansion in Asia. Rising labor costs in China, coupled with the enormous efficiency benefits of automation, have pushed China to become the largest purchasing country of robots in the world, ahead of the U.S., Japan, Korea and Germany (see chart below). However, according to the International Federation of Robotics (IFR), in 2015, Japan remained the country with the largest number of installed robots. IFR does not expect Japan to remain the “king” of the installed robotics hill forever. Actually, IFR estimates China will leapfrog Japan over the next few years to become both the largest purchaser of robots, along with maintaining the largest installed base of robots.

Source: Financial Times

In the coming months and years, there will be a steady stream of sensationalist headlines talking about the rise of the robots, and the destruction of jobs. We’ve repeatedly seen this movie before throughout history. Rather than a scary bloodbath ending, over the long-run we’ll likely see another happy ending. Any potential job losses will likely be outweighed by productivity gains, coupled with the benefits associated with more efficiently deployed labor to new growth sectors of the economy.

Even KUKA realizes the automation dynamics of the 21st century will serve as a net labor enhancer not detractor. If you don’t believe me, just ask Timo Boll, world champion table tennis player, who tested this theory vs. a KUKA robot (see video below). Ultimately, the rise of robots will lead to the rise of global growth and productivity.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), KUKAF, BA, and TSLA, but at the time of publishing had no direct position in Daimler, Airbus Group, Volkswagen, Fiat Chrysler, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Cleaning Out Your Investment Fridge

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (June 1, 2016). Subscribe on the right side of the page for the complete text.

Summer is quickly approaching, but it’s not too late to do some spring cleaning. This principle not only applies to your cluttered refrigerator with stale foods but also your investment portfolio with moldy investments. In both cases, you want to get rid of the spoiled goods. It’s never fun discovering a science experiment growing in your fridge.

Over the last three months, the stock market has been replenished after a rotten first two months of the year (S&P 500 index was down -5.5% January through February). The +1.5% increase in May added to a +6.6% and +0.3% increase in March and April (respectively), resulting in a three month total advance in stock prices of +8.5%. Not surprisingly, the advance in the stock market is mirroring the recovery we have seen in recent economic data.

After digesting a foul 1st quarter economic Gross Domestic Product (GDP) reading of only +0.8%, activity has been smelling better in the 2nd quarter. A recent wholesome +3.4% increase in April durable goods orders, among other data points, has caused the Atlanta Federal Reserve Bank to raise its 2nd quarter GDP estimate to a healthier +2.9% growth rate (from its prior +2.5% forecast).

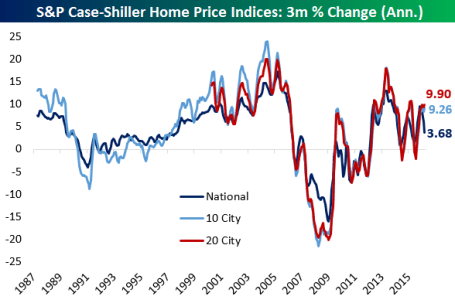

Consumer spending, which accounts for roughly 70% of our country’s economic activity, has been on the rise as well. The improving employment picture (5.0% unemployment rate last month) means consumers are increasingly opening their wallets and purses. In addition to spending more on cars, clothing, movies, and vacations, consumers are also doling out a growing portion of their income on housing. Housing developers have cautiously kept a lid on expansion, which has translated into limited supply and higher home prices, as evidenced by the Case-Shiller indices charted below.

Source: Bespoke

Spoiling the Fun?

While the fridge may look like it’s fully stocked with fresh produce, meat, and dairy, it doesn’t take long for the strawberries to get moldy and the milk to sour. Investor moods can sour quickly too, especially as they fret over the impending “Brexit” (British Exit) referendum on June 23rd when British voters will decide whether they want to leave the European Union. A “yes” exit vote has the potential of roiling the financial markets and causing lots of upset stomachs.

Another financial area to monitor relates to the Federal Reserve’s monetary policy and its decision when to further increase the Federal Funds interest rate target at its June 14th – 15th meeting. With the target currently set at an almost insignificantly small level of 0.25% – 0.50%, it really should not matter whether Chair Janet Yellen decides to increase rates in June, July, September and/or November. Considering interest rates are at/near generational lows (see chart below), a ¼ point or ½ point percentage increase in short-term interest rates should have no meaningfully negative impact on the economy. If your fridge was at record freezing levels, increasing the temperature by a ¼ or ½ degree wouldn’t have a major effect either. If and when short-term interest rates increase by 2.0%, 3.0%, or 4.0% in a relatively short period will be the time to be concerned.

Source: Scott Grannis

Keep a Fresh Financial Plan

As mentioned earlier, your investments can get stale too. Excess cash sitting idly earning next-to-nothing in checking, savings, CDs, or in traditional low-yielding bonds is only going to spoil rapidly to inflation as your savings get eaten away. In the short-run, stock prices will move up and down based on frightening but insignificant headlines. However, in the long-run, the more important issues are determining how you are going to reach your retirement goals and whether you are going to outlive your savings. This mindset requires you to properly assess your time horizon, risk tolerance, income needs, tax situation, estate plan, and other unique circumstances. Like a balanced diet of various food groups in your refrigerator, your key personal financial planning factors are dependent upon you maintaining a properly diversified asset allocation that is periodically rebalanced to meet your long-term financial goals.

Whether you are managing your life savings, or your life-sustaining food supply, it’s always best to act now and not be a couch potato. The consequences of sitting idle and letting your investments spoil away are a lot worse than letting the food in your refrigerator rot away.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}