Archive for May, 2017

Investors Slowly Waking to Technology Tailwinds

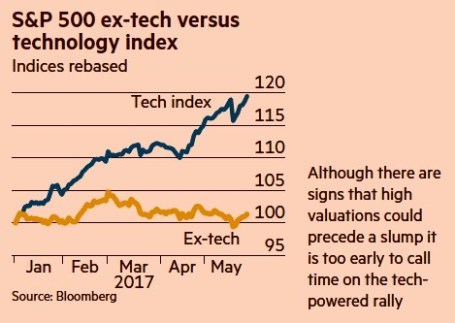

In recent years, investors have been overwhelmingly been distracted by geopolitical headlines and risk aversion caused by the worst financial crisis in a generation. In the background, the tailwinds of technological innovation have been silently gaining momentum. Although this topic is nothing new for Investing Caffeine followers, the outperformance of technology stocks has been pretty stunning in 2017 (see chart below), with the S&P 500 Technology sector rising almost +20% versus the Non-Tech sector eking out a little more than +1% return. Peered through the style lenses of Growth versus Value, technology’s contribution is also evident by the Russell 1000 Growth index’s 2017 outperformance over the Russell 1000 Value index by +11% (approximately +14% vs +3%, respectively).

Source: Bloomberg via The Financial Times

More specifically, what’s driving a significant portion of this outperformance? Robin Wigglesworth from The Financial Times highlighted a key contributing trend here:

“Facebook, Apple, Amazon and Netflix have all gained over 30 per cent this year, and Google is up 24 per cent. Their total market capitalisation now stands at $2.4 trillion. That makes them bigger than the French CAC 40 or Germany’s Dax, and nearly as large as the FTSE 100.”

Technology’s domination has been even more impressive since the cycle bottom of stock prices in 2009, if one contrasts the stark difference in the performance of the tech-heavy NASDAQ versus the more sector-balanced S&P 500. Over this timeframe, the NASDAQ has more than quadrupled in value and beaten the S&P 500 by more than +120%.

While the mass media likes to talk about technology bubbles, artificial money printing by global central banks, and imminent recessions, for years I have been highlighting the importance of the technology revolution and its beneficial impact on stock prices. Here are a few examples:

Technology Does Not Sleep in a Recession (2009)

Technology Revolution Raises Tide (2010)

NASDAQ and the R&D Tech Revolution (2014)

NASDAQ 5,000…Irrational Exuberance Déjà Vu? (2014)

The Traitorous 8 and Birth of Silicon Valley (2016)

As I have explained in many of my previous writings, the important factors of technology, globalization, and demographics have been the key driving forces behind the stock bull market and multi-decade decline in interest rates – not Quantitative Easing (QE) and/or rising debt levels.

Eventually, undoubtedly, euphoria and over-investment will lead to a cyclically-driven recession caused by excess capacity (supply exceeding demand). Regardless of the timing of future economic cycles, the continued multi-generational advance in new technological innovations will continue to drive economic growth, disinflation, improved standards of living, and higher stock prices. Until the animal spirits of the masses fully embrace this technological trend, Sidoxia and its clients will enjoy the tailwind of innovation as I continue to discover attractive investment opportunities.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own FB, AAPL, AMZN, GOOG/L, certain exchange traded funds, and short position in NFLX, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Predictions – A Fool’s Errand

Making bold predictions is a fool’s errand. I think Yogi Berra summed it up best when he spoke about the challenges of making predictions:

“It’s tough to make predictions, especially about the future.”

While making predictions might seem like a pleasurable endeavor, the reality is nobody has been able to consistently predict the future (remember the 2012 Mayan Doomsday?), besides perhaps palm readers and Nostradamus. The typical observed pattern consists of a group of well-known forecasters bunched in a herd coupled with a few extreme outliers who try to make a big splash and draw attention to themselves. Due to the law of large numbers, a few of these extreme outlier forecasters eventually strike gold and become Wall Street darlings…until their next forecasts fail miserably.

Like a broken clock, these radical forecasters can be right twice per day but are wrong most of the time. Here are a few examples:

Peter Schiff: The former stockbroker and President of Euro Pacific Capital has been peddling doom for decades (see Emperor Schiff Has No Clothes). You can get a sense of his impartial perspective via Schiff’s reading list (The Real Crash: America’s Coming Bankruptcy, Financial Armageddon, Conquer the Crash, Crash Proof – America’s Great Depression, The Biggest Con: How the Government is Fleecing You, Manias Panics and Crashes, Meltdown, Greenspan’s Bubbles, The Dollar Crisis, America’s Bubble Economy, and other doom-instilled titles.

Meredith Whitney: She made an incredible bearish call on Citigroup Inc. (C) during the fall of 2007, alongside her accurate call of Citi’s dividend suspension. Unfortunately, her subsequent bearish calls on the municipal market and the stock market were completely wrong (see also Meredith Whitney’s Cloudy Crystal Ball).

John Mauldin: This former print shop professional turned perma-bear investment strategist has built a living incorrectly calling for a stock market crash. Like perma-bears before him, he will eventually be right when the next recession hits, but unfortunately, the massive appreciation will have been missed. Any eventual temporary setback will likely pale in comparison to the lost gains from being out of the market. I profiled the false forecaster in my article, The Man Who Cries Bear.

Nouriel Roubini: This renowned New York University economist and professor is better known as “Dr. Doom” and as one of the people who predicted the housing bubble and 2008-2009 financial crisis. Like most of the perma-bears who preceded him, Dr. Doom remained too doom-ful as the stock market more than tripled from the 2009 lows (see also Pinning Down Roubini).

Alan Greenspan: The graveyard of erroneous forecasters is so large that a proper summary would require multiple books. However, a few more of my favorites include Federal Reserve Chairman Alan Greenspan’s infamous “Irrational Exuberance” speech in 1996 when he warned of a technology bubble. Although directionally correct, the NASDAQ index proceeded to more than triple in value (from about 1,300 to over 5,000) over the next three years. – today the NASDAQ is hovering around 6,100.

Robert Merton & Myron Scholes: As I chronicled in Investing Caffeine (see When Genius Failed), another doozy is the story of the Long Term Capital Management hedge fund, which was run in tandem with Nobel Prize winning economists, Robert Merton and Myron Scholes. What started as $1.3 billion fund in early 1994 managed to peak at around $140 billion before eventually crumbling to a capital level of less than $1 billion. Regrettably, becoming a Nobel Prize winner doesn’t make you a great predictor.

Words From the Wise

Rather than paying attention to crazy predictions by academics, economists, and strategists who in many cases have never invested a penny of outside investor money, ordinary investors would be better served by listening to steely investment veterans or proven prediction practitioners like Billy Beane (minority owner of the Oakland Athletics and subject of Michael Lewis’s book, Moneyball), who stated the following:

“The crime is not being unable to predict something. The crime is thinking that you are able to predict something.”

Other great quotes regarding the art of predictions, include these ones:

“I can’t recall ever once having seen the name of a market timer on Forbes‘ annual list of the richest people in the world. If it were truly possible to predict corrections, you’d think somebody would have made billions by doing it.”

-Peter Lynch

“Many more investors claim the ability to foresee the market’s direction than actually possess the ability. (I myself have not met a single one.) Those of us who know that we cannot accurately forecast security prices are well advised to consider value investing, a safe and successful strategy in all investment environments.”

–Seth Klarman

“No matter how much research you do, you can neither predict nor control the future.”

–John Templeton

“Stop trying to predict the direction of the stock market, the economy or the elections.”

–Warren Buffett

“In the business world, the rearview mirror is always clearer than the windshield.”

–Warren Buffett

In the global financial markets, Wall Street is littered with strategists and economists who have flamed out after brief bouts of fame. Celebrated author Mark Twain captured the essence of speculation when he properly identified, “There are two times in a man’s life when he should not speculate: when he can’t afford it and when he can.” Instead of attempting to predict the future, investors will avoid a fool’s errand by simply seizing opportunities as they present themselves in an ever-changing world.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Ignoring Economics and Vital Signs

As stock prices sit near all-time record highs, and as we enter year nine of the current bull market, I remain amazed and amused at the brazen disregard for important basic economic concepts like supply & demand, interest rates, and rising profits.

If the stock market was a doctor’s patient, over the last decade, bloggers, pundits, talking heads, and pontificators have been ignoring the improving, healthy patient’s vital signs, while endlessly predicting the death of the resilient stock market.

However, let’s be clear – it has not been all hearts and flowers for stocks – there have been numerous -10%, -15%, and -20% corrections since the Financial Crisis nine years ago. Those corrections included the Flash Crash, debt downgrade, Arab Spring, sequestration, Taper Tantrum, Iranian Nuclear Threat, Ukrainian-Crimea annexation, Ebola, Paris/San Bernardino Terrorist Attacks, multiple European & Chinese slowdowns and more.

Despite the avalanche of headlines and volatility, we all know the net result of these events – a more than tripling of stock prices (+259%) from March 2009 to new all-time record highs. With the incessant stream of negative news, how could prices appreciate so dramatically?

Over the years, the explanations by outside observers have changed. First, the recovery was explained as a “dead cat bounce” or a short-term cyclical bull market within a long-term secular bear market. Then, when stock prices broke to new records, the focus shifted to Quantitative Easing (QE1, QE2, QE3, and Operation Twist). The QE narrative implied the bull advance was temporary due to the non-stop, artificial printing presses of the Fed. Now that the Fed has not only ended QE but reversed it (the Fed is actually contracting its balance sheet) and hiked interest rates (no longer cutting), outsiders are once again at a loss. Now, the bears are left clinging to the flawed CAPE metric I wrote about three years ago (see CAPE Smells Like BS), and using political headlines as a theory for record prices (i.e., record stock prices stem from inflated tax cut and infrastructure spending expectations).

It’s unfortunate for the bears that all the conspiracy theory headlines and F.U.D. (fear, uncertainty, and doubt) over the last 10 years have failed miserably as predictors for stock prices. The truth is that stock prices don’t care about headlines – stock prices care about economics. More specifically, stock prices care about profits, interest rates, and supply & demand.

Profits

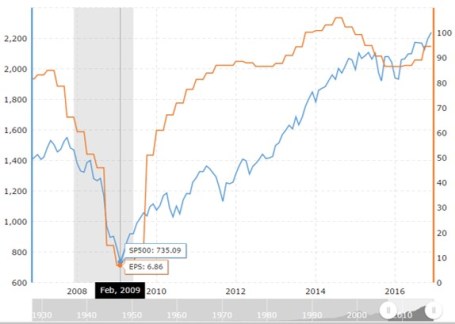

It’s quite simple. Stock prices have more than tripled since early 2009 because profits have more than tripled since 2009. As you can see from the Macrotrends chart below, 2009 – 2016 profits for the S&P 500 index rose from $6.86 to $94.54, or +1,287%. It’s no surprise either that stock prices stalled for 18 months from 2015 to mid-2016 when profits slowed. After profits returned to growth, stock price appreciation also resumed.

Source: Macrotrends

Interest Rates

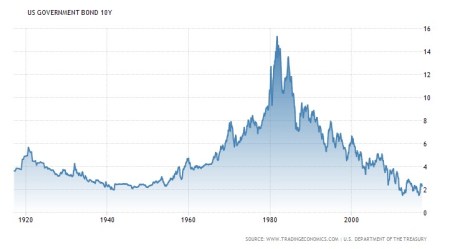

When you could earn a +16% on a guaranteed CD bank rate in the early 1980s, do you think stocks were a more or less attractive asset class? If you can sense the rhetorical nature of my question, then you can probably understand why stocks were about as attractive as rotten milk or moldy bread. Back then, stocks traded for about 8x’s earnings vs. the 18x-20x multiples today. The difference is, today interest rates are near generational lows (see chart below), and CDs pay near +0%, thereby making stocks much more attractive. If you think this type of talk is heresy, ignore me and listen to the greatest investor of all-time, Warren Buffett who recently stated:

“Measured against interest rates, stocks are actually on the cheap side.”

Source: Trading Economics

Supply & Demand

Another massively ignored area, as it relates to the health of stock prices, is the relationship of new stock supply entering the market (e.g., new dilutive shares via IPOs and follow-on offerings), versus stock exiting the market through corporate actions. While there has been some coverage placed on the corporate action of share buybacks – about a half trillion dollars of stock being sucked up like a vacuum cleaner by cash heavy companies like Apple Inc. (AAPL) – little attention has been paid to the trillions of dollars of stock vanishing from mergers and acquisition activities. Yes, Snap Inc. (SNAP) has garnered a disproportionate amount of attention for its $3 billion IPO (Initial Public Offering), this is a drop in the bucket compared to the exodus of stock from M&A activity. Consider the trivial amount of SNAP supply entering the market ($3 billion) vs. $100s of billions in major deals announced in 2016 – 2017:

- Time Warner Inc. merger offer by AT&T Inc. (T) for $85 billion

- Monsanto Co. merger offer by Bayer AG (BAYRY) for $66 billion

- Reynolds American Inc. merger offer by British American Tobacco (BTI) for $47 billion

- NXP Semiconductors merger offer by Qualcomm Inc. (QCOM) for $39 billion

- LinkedIn merger offer by Microsoft Corp. (MSFT) for $28 billion

- Jude Medical, Inc. merger offer by Abbott Laboratories (ABT) for $25 billion

- Mead Johnson Nutrition merger offer by Reckitt Benckiser Group for $18 billion

- Mobileye merger offer by Intel Corp. (INTC) for $15 billion

- Netsuite merger offer by Oracle Corp. (ORCL) for $9 billion

- Kate Spade & Co. merger offer by Coach Inc. (COH) for $2 billion

While these few handfuls of deals represent over $300 billion in disappearing stock, as long as corporate profits remain strong, interest rates low, and valuations reasonable, there will likely continue to be trillions of dollars in stocks being purchased by corporations. This continued vigorous M&A activity should provide further healthy support to stock prices.

Admittedly, there will come a time when profits will collapse, interest rates will spike, valuations will get stretched, sentiment will become euphoric, and/or supply of stock will flood the market (see Don’t be a Fool, Follow the Stool). When the balance of these factors turn negative, the risk profile for stock prices will obviously become less desirable. Until then, I will let the skeptics and bears ignore the healthy economic vital signs and call for the death of a healthy patient (stock market). In the meantime, I will continue focus on the basics of math and offer my economics textbook to the doubters.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own AAPL, ABT, INTC, MSFT, T, and certain exchange traded funds, but at the time of publishing SCM had no direct position in SNAP, TWX, MON, KATE, N, MBLY, MJN, STJ, LNKD, NXPI, BAYRY, BTI, QCOM, ORCL, COH, RAI, Reckitt Benckiser Group, any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

The Fallacy Behind Populism and Automation Fears

The rise of global populism and anti-immigration sentiments, coupled with the perpetual rising trend of automation and robotics has stoked the fear fires of job security. Many stories perpetuate erroneous stereotypes and falsehoods. The news reports and blog articles come in various flavors, but in a nutshell the stories state the U.S. is hemorrhaging jobs due to the thieves of illegal immigration and heartless robotics. The job displacement theory is built upon the idea that these two sources of labor (immigrants & robots) are cheaper and more productive than traditional blue collar and white collar American workers.

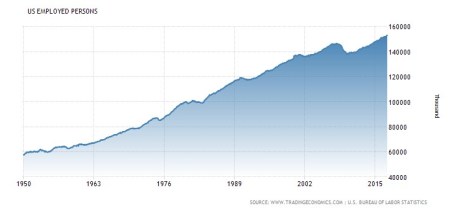

Although these logical beliefs make for great soundbites, and may sell subscriptions and advertising, unfortunately the substance behind the assertions holds little water. Let’s take a look at the facts. In the most recent April jobs report, nonfarm payrolls employment increased by 211,000 jobs, according to the U.S. Bureau of Labor Statistics. Since early 2009 the unemployment rate has plummeted from 10.0% down to a historically low level of 4.4%. Over the similar timeframe, the economy has added over 15,000,000 new jobs. Does this sound like an environment in which immigrants and robots are killing all American jobs?

Sounds like a bunch of phoney-baloney, if you ask me. Just look at the employed person chart below, which shows a rising employment trend over the last seven decades, with the exception of some brief recessionary periods.

As I point out in a previous article (see Rise of the Robots), from the beginning of the United States, the share of the largest segment of the economy (agriculture) dropped by more than 98%, yet the standard of living and output in the agriculture sector have still exploded. There may not have been robots two and a half centuries ago, but technology and automation were alive and well, just as they are today. Although there were no self-driving cars, no internet, no biotech drugs, and no mobile phones, there were technological advances like the cotton gin, plow, scythe, chemical fertilizers, tractors, combine harvesters, and genetically engineered seeds over time.

Source: Carpe Diem

And while there most certainly were farmers who regrettably were displaced by these technologies, there were massive new industries fostered by the industrial revolution, which redeployed labor to new burgeoning industries like manufacturing, aerospace, transportation, semiconductors, medicine, and many more.

While it may be difficult to fathom what industries will replace the workers displaced by self-service kiosks at restaurants, airports, and retail stores, famed economist Milton Friedman summed it up best when he stated:

“Human wants & needs are infinite, and so there will always be new industries, there will always be new professions.”

As globalization and technology continue permeating through society, it is true, the importance of education becomes more critical. Billions of people around the globe in developing markets, along with automation technology, will be stealing lower-paying American jobs that require repetitive processes. Educating our workforce up the value-add food chain is imperative.

The bottom-line is that integration of technology and automation will improve the standard of living for the masses. Sure, immigration will displace some workers, but if legislative policy can be designed to cherry-pick (attract) the cream of the skilled foreign crop (and retrain displaced workers), skilled immigrants will keep on innovating and creating higher valued jobs. Just consider a recent study that shows 51% of U.S. billion-dollar startups were founded by immigrants.

The populist drum may continue to pound against immigration, and horror stories of job-stealing robots may abound, however the truth cannot be erased. Over the long-run, the fallacies behind populism and automation will be uncovered. The benefits and truths surrounding highly skilled immigrants and robots will be realized, as these dynamics dramatically improve the standard of living and productivity of our great economy.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Glass Half Full or Half Empty?

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (May 1, 2017). Subscribe on the right side of the page for the complete text.

We live in a time of confusing dichotomies, which makes deciphering the flood of daily data quite challenging. In that context, determining whether the current economic fundamentals should be viewed from a glass half empty of glass half full perspective can be daunting.

More specifically, stock markets have again recently hit new all-time record highs, yet if you read the newspaper headlines, you might think we’re in the midst of Armageddon. Last month, the Dow Jones Industrial Average stock index eclipsed 21,000 and the technology-heavy NASDAQ index surpassed the psychologically important 6,000 threshold. In spite of the records, here’s a sampling of the steady stream of gloomy feature stories jamming the airwaves:

- French Elections – Danger of European Union Breakup

- Heightened Saber Rattling by U.S. Towards North Korea

- Threat of U.S. Government Shutdown

- First 100 Days – Obamacare repeal failure, tax reform delays, no significant legislation

- NAFTA Trade Disputes

- Russian Faceoff Over Syrian Civil War & Terrorism

- Federal Reserve Interest Rate Hikes Could Derail Stock Market

- Slowing GDP / Economic Data

Given all this doom, how is it then that stock markets continue to defy gravity and continually set new record highs? Followers of my writings understand the crucial, driving dynamics of financial markets are not newspaper, television, magazine, and internet headlines. The most important factors are corporate profits, interest rates, valuations, and investor sentiment. All four of these elements will bounce around, month-to-month, and quarter-to-quarter, but for the time being, these elements remain constructive on balance, despite the barrage of negative, gut-wrenching headlines.

Countering the perpetual flow of gloomy, cringe-worthy headlines, we have seen a number of positive developments:

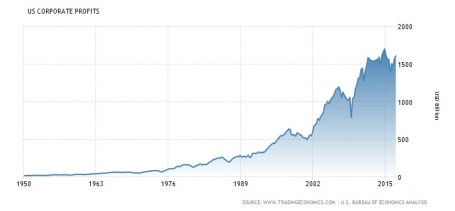

- Record Breaking Corporate Profits: Profits are the chief propellant for higher stock prices, and so far, for the 1st quarter, S&P 500 company profits are estimated to have risen +12.4% – the highest rate since 2011, according to Thomson Reuters I/B/E/S. As I like to remind my readers, stock prices follow profits over the long-run, which is evidenced by the chart below.

Source: Trading Economics

- Interest Rates Low: With interest rate levels still near generational lows (10-Year Treasury @ 2.28%), and inflation relatively stable around 2%, this augurs well for most asset prices. For U.S. consumers there are many stimulative effects to lower interest rates, whether you are buying a house, purchasing a car, paying off a school loan, and/or reducing credit card debt. Lower rates equal lower payments.

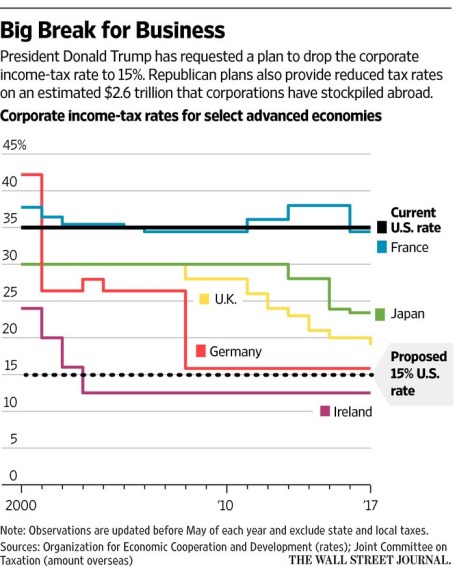

- Potential Tax Reform: There are numerous stimulative components to the largest planned tax-cut in history. First of all, cutting the tax rate from 35% to 15% for corporations and small businesses (i.e. pass-through entities like LLCs and S-Corps) would place a lot of dollars back in the pockets of taxpayers and should stimulate economic growth. Other components of the White House proposal include the termination of the estate tax, the elimination of the AMT (Alternative Minimum Tax) targeted at wealthier households, and the doubling of the standard deduction to help middle-income families. All of this sounds great on paper, but not a lot of details have been provided yet on how these benefits will be paid for – removing state tax deductions alone is unlikely to fully offset revenue declines. The chart below highlights how high U.S. corporate income tax rates are relative to other foreign counterparts.

Source: The Wall Street Journal

- Business Spending & Confidence on the Rise: Ever since the 2008-09 Great Recession, the U.S. has been a better house in a bad neighborhood relative to other global developed economies. However, the recovery has been gradual and muted due to tight-fisted companies being slow to hire and invest. Although recent Q1 GDP economic data came in at a sluggish +0.7% growth rate, the bright spot embedded in the data was a +12% annualized increase in private fixed investment. This is consistent with the spike we’ve seen in recent business and consumer confidence surveys (see chart below). Although this confidence has yet to translate into an acceleration in broader economic data, the ramp in capital spending and positive business sentiment could be a leading indicator for faster economic growth to come. Stimulative legislation enacted by Congress (i.e., tax reform, infrastructure spending, foreign repatriation, etc.) could add further fuel to the economic growth engine.

Source: Trading Economics

- Economy Keeps Chugging Along: As the wealthiest country on the planet, we Americans can become a little spoiled with success, which helps explain the media’s insatiable appetite for growth. Nevertheless, the broader economic data show a continuing trend of improvement. Simply consider the trend occurring in these major areas of the economy:

- Unemployment – The jobless rate has been chopped by more than half from a 10.0% cycle peak to 4.5% today.

- Housing – The number of annual existing home sales has increased by more than +60% from the cycle low to 5.7 million units, which still leaves plenty of headroom for growth before 2006 peak sales levels are reached.

- Consumer Spending – This segment accounts for roughly 70% of our country’s economic activity. Although we experienced a soft patch in Q1 of 2017, as you can see from the chart below, we Americans have had no problem spending more to keep our economy functioning.

Source: Trading Economics

While key economic statistics remain broadly constructive, there will come a time when prudence will dictate the pursuit of a more defensive investment strategy. When will that be? In short, the time to become more cautious will be when we see a combination of the following occur:

- Sharp increase in interest rates

- Signs of a significant decline in corporate profits

- Indications of an economic recession (e.g., an inverted yield curve)

- Spike in stock prices to a point where valuation (prices) are at extreme levels and skeptical investor sentiment becomes euphoric

To date, there is no objective evidence indicating these dynamics are in place, so until then, I will remain thirsty and grab my half glass full of water.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}