Archive for February, 2015

Can You Retire? Getting to Your Number

What’s “your number?” The catchy phrase has been tried on 30-second television commercials before, but the fact remains, most Americans have no clue how much they need to save for retirement. The ever-shifting and imprecise variables needed to compute the size of your needed nest egg can seem overwhelming: lifespan; career span; inflation; college tuition; healthcare expenses; rising insurance costs; social security; employer benefits; inheritance; child support; parental support; etc. The list goes on and with near-zero interest rates, and stock prices at record highs, the retirement challenge has only gotten riskier and more difficult.

I understand this task may not be easy and could eat into your House of Cards viewing, Candy Crush playing, or football watching. However, if you can spend two weeks planning a family vacation, you certainly can afford devoting a few hours to scribbling down some numbers as it relates to the lifeblood of your financial future. The project is definitely doable.

Here are some key steps to finding “your number.” If you’re not single, then calculate the figures for your household:

1). Calculate Your Budget: Where to start? A good place to begin is with is a boring budget (or your monthly expenses). The budget does not need to be down to the penny, but you should be able to estimate your monthly spend with the help of your bank and credit card statements. Make sure to include estimates for periodic unforeseen potential expenses like annual auto repairs, home repairs, or emergency hospital visits. Once you determine your monthly spend, extrapolating your annual spend shouldn’t be too difficult.

2). Compute Your Income: Your sources of income should be fairly straightforward. For most people this includes your salary and potential bonus. Some people will also generate income from investments, a business, and/or real estate. Before getting too excited about all the income you are raking in, don’t forget to subtract out taxes collected by Uncle Sam, and include a possible scenario of rising tax rates during your working years. Obviously, the economy can also have a positive or negative impact on your income projections, nevertheless, if you conservatively plan for some potential future setbacks, you will be in a much better position in forecasting the amount of savings needed to reach “your number.”

3). Planned Retirement Date: The date you pick may or may not be realistic, but by choosing a specific date, you can now evaluate how much savings will be necessary to reach your required nest egg number. The difference between your annual income (#2) and annual budget (#1) is your annual savings, which you can multiply by the number of years you plan to work until retirement. For example, assume you wanted to retire 15 years from now and were able to save/invest $20,000 each year while earning a 6% annualized return. By the year 2030 these savings would equate to about $465,000 and could be added to any other savings and other retirement income (pension, 401(k), Social Security, inheritance, etc.) to meet your retirement needs.

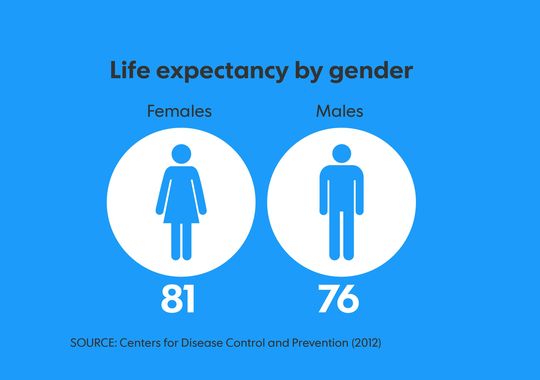

4). Life Expectancy: After you have determined when you want to retire, now comes the tricky part. How long are you going to live? Assuming you are currently healthy, you can use actuarial tables for life expectancy. According to a new report on American mortality from the Centers for Disease Control and Prevention’s National Center for Health Statistics, the average life expectancy is 81 for females and 76 for males (see graphic below). The estimates are a little rosier, if you have lived to age 65, in which case females are expected to live past 85 years old and males to about 83 years. You can adjust these figures higher or lower based on personal information and family history, but if you consider yourself “average,” then you better plan to have at least 15 years of fire power in your savings nest egg (see example at bottom of article).

Source: USA Today

Empty Retirement Wallets & Purses

The harsh realities are Americans are not saving enough. It‘s true, you can survive off a smaller nest egg, if you plan to live off of cat food and vacation in Tijuana, but most Americans and retirees have become accustomed to a higher standard of living. A New York Times article highlighted that 75% percent of Americans nearing retirement age had less than $30,000 in their retirement accounts – that’s not going to buy you that winter home on Maui or leave enough to cover your golf dues at the local country club.

Control the things that make a difference.

- Save. Pay yourself first by tucking money away each month. If you haven’t established an IRA (Individual Retirement Account) or savings account, make sure you contribute to your employer’s matching 401(k) plan to the fullest extent possible, if available. This is free money your employer is offering you and by not participation you are shooting yourself in the foot.

- Spend prudently. Review your monthly / annual budgets and determine where there is room to cut expenses. Every budget has fat in it, so it’s just a matter of cutting excessive and less important items, without sacrificing dramatic changes to your standard of living.

- Manage your career. Invest in yourself with education, apply for that promotion, or look for other employment alternatives if you are unhappy or not being paid your proper value.

- Push Retirement Out: If you are healthy and enjoy your work, extending your working years can have profoundly positive benefits to your retirement. Not only will you have more money saved up for retirement, but you will also receive higher Social Security benefits by delaying retirement (see Social Security benefit estimator).

The bottom-line is if you are like most working Americans, you will need to save more and invest more prudently (e.g., in a low-cost, tax-efficient manner like strategies offered by Sidoxia).

Use Your Thumb to Get Started

Rules of thumb are never perfect, but are not a bad place to start before fine-tuning your estimates. Some retirement pundits begin by using an 80% “income replacement ratio” rule as a retirement guide. In other words, you should not need 100% of your pre-retirement income during retirement because a number of your major living expenses should be reduced. For example, during retirement your tax expenses should decrease (because you are not working); your mortgage payment should be lower (i.e., house is paid off); your kids should be independent and off the family payroll; and you may be in the position to downsize your home (e.g., empty-nesters often decide to move to a lower square footage residence).

Another rule of thumb is the “15x Rule,” which says you will need an investment account equivalent to at least 15-times your pre-retirement income. Therefore, if your after-tax income is $100,000 before retirement and you need to replace $80,000 during retirement (80% replacement ratio), this means you actually only need to replace about $60,000 per year. We arrive at the lower $60,000 figure by further assuming the $80,000 can be reduced by about $20,000 flowing in annually from Social Security. Through the mighty powers of division, we can then apply the 4% Sustainable Withdrawal Rate rule (SWR) to reverse engineer the estimate of “our number.” In this example, our ultimate nest egg needed is $1,500,000 (equal to $60,000 / 4% or $60,000 x 25 years), which is estimated to last for 25 years of retirement. As you can see, there are quite a few assumptions baked into this scenario, including a retirement investment portfolio that beats inflation by 4%, but nevertheless this line of thinking creates an understandable framework to operate under.

Of course, for all the non-math Investing Caffeine readers, life could have been made easier by simply multiplying the $100,000 pre-retirement income by 15x to arrive at our $1.5 million nest egg. More elegant, but less fun for this nerdy math author.

We’ve covered a lot of ground, but I’m absolutely confident if you have read this far, you can definitely come up with “your number.” If this all seems too overwhelming, there is no need to worry, just find an experienced investment advisor or financial planner…I’m sure I could help you find one 🙂 .

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Here Comes the Great Rotation…Finally?

For decades interest rates have continually gravitated to zero like flies attracted to stink. For a split second in 2013, as long-term U.S. Treasury rates about doubled from 1.5% to 3.0% before reversing, it appeared the declining rate cycle could finally be broken. At the time, pundits of all types were calling for the “great rotation” out of bonds into stocks. Half of this forecast came to fruition as stocks grinded to record highs in 2014, but even I the big stock bull admittedly did not expect interest rates on 10-year Switzerland bonds to turn negative (see also Draghi QE Beer Goggles), especially after U.S. quantitative easing (QE) came to an end.

With rates already at a generational low, how could anyone be expected to accept a measly 0.3% annual return for a whole decade? Well, that’s exactly what’s happening in massive developed markets like Germany and Japan. While investors and retirees are painted into a corner by being forced to accept near-0% interest payments, savvy corporate borrowers are taking advantage of this once in a lifetime opportunity. Take for example the recently unprecedented $1.35 billion Switzerland bond issuance by Apple Inc. (AAPL), which included a tranche of bonds maturing in 2024 that yielded a paltry 0.25%.

With bonds offering lower and lower yield possibilities for investors of all stripes, at Sidoxia we are still finding plenty of opportunities in stocks, especially in high dividend-paying equity investments. In the U.S., the average S&P 500 stock is yielding approximately the same as the 10-Year Treasury Note (2.0%), but in other parts of the world, equity markets such as the following are offering significantly higher yields:

- iShares MSCI Australia (Yield 5.0% – EWA)

- Europe FTSE Europe (Yield: 4.6% – VGK)

- Market Vectors Russia (Yield 4.6% – RSX)

- iShares MSCI Brazil (Yield 4.0% – EWZ)

- iShares MSCI Sweden (Yield 3.8% – EWD)

- iShares MSCI Malaysia (Yield 3.8% – EWM)

- iShares MSCI Singapore (Yield 3.4% – EWS)

- iShares China (Yield 2.5% – FXI)

A New “Great Rotation” in 2015?

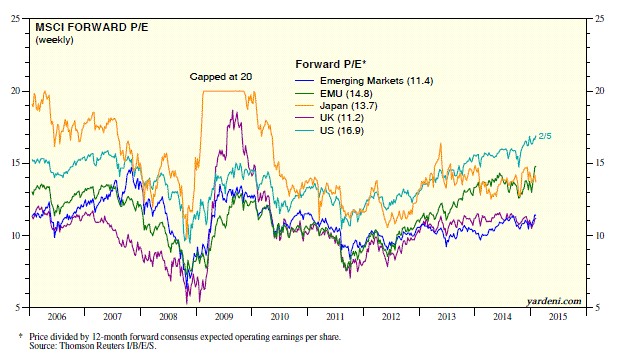

If you look at the 2014 ICI (Investment Company Institute) fund flow data, it becomes clear the great rotation out of bonds into U.S. stocks has not occurred. More specifically, despite the S&P 500 index reaching new record highs, -$60 billion flowed out of U.S. stock funds last year, and about +$44 billion flowed into all bond funds. Could the “great rotation” out of bonds into stocks finally happen in 2015? Certainly, this scenario is a possibility, but given the barren bond yield environment, perhaps the new “great rotation” in 2015 will be out of domestic equities into higher yielding international equity markets. In addition to the higher international market yields listed above, many of these foreign markets are priced more attractively (i.e., lower Price-Earnings (P/E) ratios) as you can see from the chart below created by strategist Dr. Ed Yardeni.

Source: Ed Yardeni – Dr. Ed’s Blog

Obviously, any asset shifting scenario is not mutually exclusive, and there could be a combination of investor reallocations made in 2015. It’s possible that previously unloved emerging markets and international developed markets could receive new investor capital from several areas.

With defensive sectors like utilities (up +25%) and healthcare (up +24%) leading the U.S. sector higher last year, it’s evident to me that “skepticism” remains the operative word in investors’ minds and there is no clear evidence of widespread euphoria hitting the U.S. stock market. Valuations as measured by trailing P/E ratios have objectively moved above historical averages, however this has occurred within the context of all-time record low interest rates and inflation. If you take into account the near-0% interest rate environment into your calculus, current stock prices (P/E ratios) are well within historical norms (see also The Rule of 20 Can Make You Plenty), which still leaves room for expansion.

If some of the half-glass full economic waters spill into the half-glass empty emerging markets/international markets, conceivably the eagerly anticipated “great rotation” out of bonds into U.S. stocks may also flow into even more attractively valued foreign equity opportunities.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AAPL and certain exchange traded funds (ETFs) including VGK, EWZ, FXI, but at the time of publishing SCM had no direct position in EWA, RSX, EWD, EWM, EWS, and any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Is Good News, Bad News?

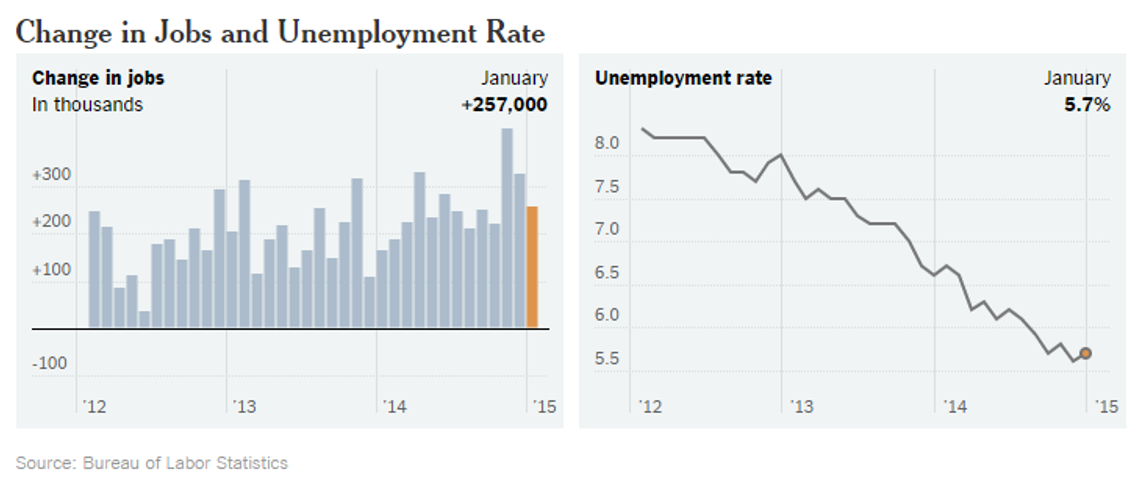

The tug-of-war is officially on as investors try to decipher whether good news is good or bad for the stock market? On the surface, the monthly January jobs report released by the Bureau of Labor Statistics (BLS) appeared to be welcomed, positive data. Total jobs added for the month tallied +257,000 (above the Bloomberg consensus of +230,000) and the unemployment rate registered 5.7% thanks to the labor participation rate swelling during the month (see chart below). More specifically, the number of people looking for a job exceeded one million, which is the largest pool of job seekers since 2000.

Source: BLS via New York Times

Initially the reception by stocks to the jobs numbers was perceived positively as the Dow Jones Industrial index climbed more than 70 points on Friday. Upon further digestion, investors began to fear an overheated employment market could lead to an earlier than anticipated interest rate hike by the Federal Reserve, which explains the sell-off in bonds. The yield on the 10-Year Treasury proceeded to spike by +0.13% before settling around 1.94% – that yield compares to a recent low of 1.65% reached last week. The initial euphoric stock leap eventually changed direction with the Dow producing a -180 point downward reversal, before the Dow ended the day down -62 points for the session.

Crude Confidence?

The same confusion circling the good jobs numbers has also been circulating around lower oil prices, which on the surface should be extremely positive for the economy, considering consumer spending accounts for roughly 70% of our country’s economic output. Lower gasoline prices and heating bills means more discretionary spending in the pockets of consumers, which should translate into more economic activity. Furthermore, it comes as no surprise to me that oil is both figuratively and literally the lubricant for moving goods around our country and abroad, as evidenced by the Dow Jones Transportation index that has handily outperformed the S&P 500 index over the last 18 months. While this may truly be the case, many journalists, strategists, economists, and analysts are nevertheless talking about the harmful deflationary impacts of declining oil prices. Rather than being viewed as a stimulative lubricant to the economy, many of these so-called pundits point to low oil prices as a sign of weak global activity and an omen of worse things to come.

This begs the question, as I previously explored a few years ago (see Good News=Good News?), is it possible that good news can actually be good news? Is it possible that lower energy costs for oil importing countries could really be stimulative for the global economy, especially in regions like Europe and Japan, which have been in a decade-long funk? Is it possible that healthier economies benefiting from substantial job creation can cause a stingy, nervous, and scarred corporate boardrooms to finally open up their wallets to invest more significantly?

Interest Rate Doom May Be Boom?

Quite frankly, all the incessant, never-ending discussions about an impending financial market Armageddon due to a potential single 0.25% basis point rate hike seem a little hyperbolic. Could I be naively whistling past the graveyard? From my perspective, although it is a foregone conclusion the Fed will have to increase interest rates above 0%, this is nothing new (I’m really putting my neck out there on this projection). Could this cause some volatility when it finally happens…of course. Just look at what happened to financial markets when former Federal Reserve Chairman Ben Bernanke merely threatened investors with a wind-down of quantitative easing (QE) in 2013 and investors had a taper tantrum. Sure, stocks got hit by about -5% at the time, but now the S&P 500 index has catapulted higher by more than +25%.

Looking at how stocks react in previous rate hike cycles is another constructive exercise. The aggressive +2.50% in rate hikes by former Fed Chair Alan Greenspan in 1995 may prove to be a good proxy (see also 1994 Bond Repeat?). After suffering about a -10% correction early in 1994, stocks rallied in the back-half to end the year at roughly flat.

And before we officially declare the end of the world over a single 0.25% hike, let’s not forget that the last rate hike cycle (2004 – 2006) took two and a half years and 17 increases in the targeted Federal Funds rate (1.00% to 5.25%). Before the rate increases finally broke the stock market’s back, the bull market moved about another +40% higher…not too shabby.

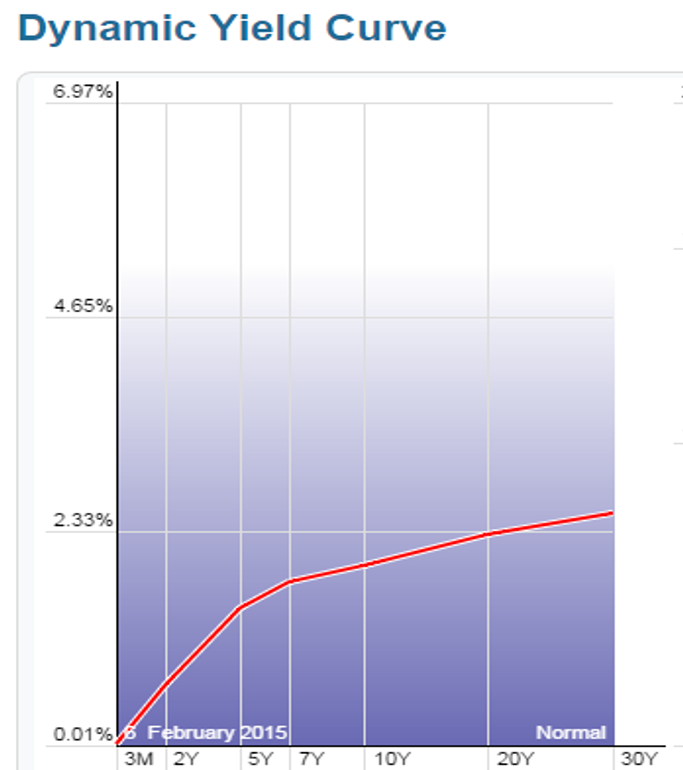

Lastly, before writing the obituary of this bull market, it’s worth noting the yield curve has been an incredible leading indicator and currently this gauge is showing zero warnings of any dark clouds approaching on the horizon (see chart below). As a matter of fact, over the last 50 years or so, the yield curve has turned negative (or near 0%) before every recession.

Source: StockCharts.com

As the chart above shows, the yield curve remains very sloped despite modest flattening in recent quarters.

While many skeptics are having difficulty accepting the jobs data and declining oil prices as good news because of rate hike fears, history shows us this position could be very misguided. Perhaps, once again, this time around good news may actually be good news.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Inflating Dollars & Deflating Footballs

This article is an excerpt from a previously released Sidoxia Capital Management complementary newsletter (February 2, 2015). Subscribe on the right side of the page for the complete text.

In the weeks building up to Super Bowl XLIX (New England Patriots vs. Seattle Seahawks) much of the media hype was focused on the controversial alleged “Deflategate”, or the discovery of deflated Patriot footballs, which theoretically could have been used for an unfair advantage by New England’s quarterback Tom Brady. While Brady ended up winning his record-tying 4th Super Bowl ring for the Patriots by defeating the Seahawks 28-24, the stock market deflated during the first month of 2015 as well. Similar to last year, the stock market has temporarily declined last January before surging ahead +11.4% for the full year of 2014. It’s early in 2015, and investors chose to lock-in a small portion of the hefty, multi-year bull market gains. The S&P 500 was sacked for a loss of -3.1% and the Dow Jones Industrial index by -3.7%.

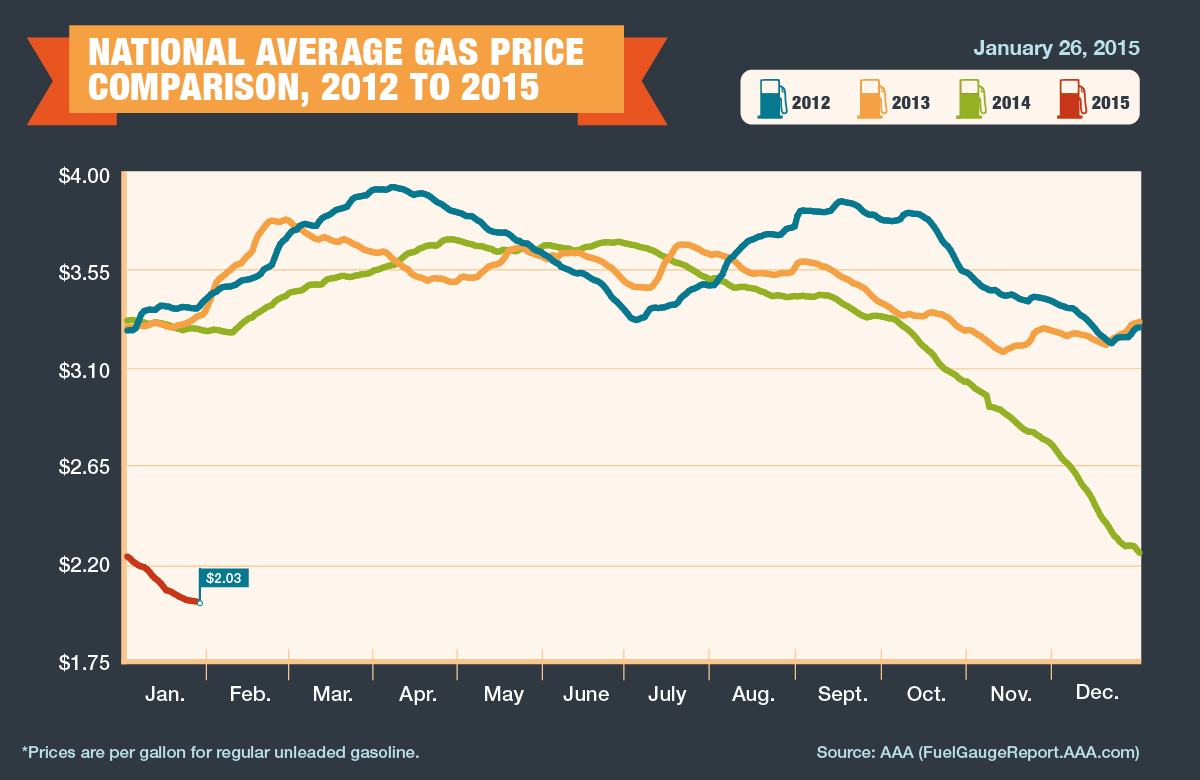

Despite some early performance headwinds, the U.S. economy kicked off the year with the wind behind its back in the form of deflating oil prices. Specifically, West Texas Intermediate (WTI) crude oil prices declined -9.4% last month to $48.24, and over -51.0% over the last six months. Like a fresh set of substitute legs coming off the bench to support the team, the oil price decline represents an effective $125 billion tax cut for consumers in the form of lower gasoline prices (average $2.03 per gallon nationally) – see chart below. The gasoline relief will allow consumers more discretionary spending money, so football fans, for example, can buy more hot dogs, beer, and souvenirs at the Super Bowl. The cause for the recent price bust? The primary reasons are three-fold: 1) Sluggish oil demand from developed markets like Europe and Japan coupled with slowing consumption growth in some emerging markets like China; 2) Growing supply in various U.S. fracking regions has created a temporary global oil glut; and 3) Uncertainty surrounding OPEC (Organization of Petroleum Exporting Countries) supply/production policies, which became even more unclear with the recent announced death of Saudi Arabia’s King Abdullah.

Source: AAA

More deflating than the NFL football’s “Deflategate” is the approximate -17% collapse in the value of the euro currency (see chart below). Euro currency matters were made worse in response to European Central Bank’s (ECB) President Mario Draghi’s announcement that the eurozone would commence its own $67 billion monthly Quantitative Easing (QE) program (very similar to the QE program that Federal Reserve Chairwoman Janet Yellen halted last year). In total, if carried out to its full design, the euro QE version should amount to about $1.3 trillion. The depreciating effect on the euro (and appreciating value of the euro) should help stimulate European exports, while lowering the cost of U.S. imports – you may now be able to afford that new Rolls-Royce purchase you’ve been putting off. What’s more, the rising dollar is beneficial for Americans who are planning to vacation abroad…Paris here we come!

Source: XE.com

Another fumble suffered by the global currency markets was introduced with the unexpected announcement by the Swiss National Bank (SNB) that decided to remove its artificial currency peg to the euro. Effectively, the SNB had been purchased and accumulated a $490 billion war-chest reserve (Supply & Demand Lessons) to artificially depress the value of the Swiss franc, thereby allowing the country to sell more Swiss army knives and watches abroad. When the SNB could no longer afford to prop up the value of the franc, the currency value spiked +20% against the euro in a single day…ouch! In addition to making its exports more expensive for foreigners, the central bank’s move also pushed long-term Swiss Treasury bond yields negative. No, you don’t need to check your vision – investors are indeed paying Switzerland to hold investor money (i.e., interest rates are at an unprecedented negative level).

In addition to some of the previously mentioned setbacks, financial markets suffered another penalty flag. Last month, multiple deadly terrorist acts were carried out at a satirical magazine headquarters and a Jewish supermarket – both in Paris. Combined, there were 16 people who lost their lives in these senseless acts of violence. Unfortunately, we don’t live in a Utopian world, so with seven billion people in this world there will continue to be pointless incidences like these. However, the good news is the economic game always goes on in spite of terrorism.

As is always the case, there will always be concerns in the marketplace, whether it is worries about inflation, geopolitics, the economy, Federal Reserve policy, or other factors like a potential exit of Greece out of the eurozone. These concerns have remained in place over the last six years and the stock market has about tripled. The fact remains that interest rates are at a generational low (see also Stretching the High Yield Rubber Band), thereby supplying a scarcity of opportunities in the fixed income space. Diversification remains important, but regardless of your time horizon and risk tolerance, attractively valued equities, including high-quality, dividend-paying stocks should account for a certain portion of your portfolio. Any winning retirement playbook understands a low-cost, globally diversified portfolio, integrating a broad set of asset classes is the best way of preventing a “deflating” outcome in your long-term finances.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}