Archive for May, 2016

Market Inefficiencies Give Black-Eyes to Classic Economists

Markets are efficient. Individuals behave rationally. All information is reflected in prices. Huh…are you kidding me? These are the beliefs held by traditional free market economists (“rationalists”) like Eugene Fama (Economist at the University of Chicago and a.k.a. the “Father of the Efficient Market Hypothesis”). Striking blows to the rationalists are being thrown by “behavioralists” like Richard Thaler (Professor of Behavioral Science and Economics at the University of Chicago), who believes emotions often lead to suboptimal decisions and also thinks efficient market economics is a bunch of hogwash.

Individual investors, pensions, endowments, institutional investors, governments, were left sifting through the rubble in the aftermath of the 2008-2009 financial crisis because common beliefs were thrown out the window. Experts and non-experts are still attempting to figure out how this mass destruction occurred and how it can be prevented in the future. Economists, as always, are happy to throw in their two cents. Right now traditional free market economists like Fama have received a black eye and are on the defensive – forced to explain to the behavioral finance economists (Thaler et. al.) how efficient markets could lead to such a disastrous outcome.

Religion and Economics

Like religious debates, economic rhetoric can get heated too. Religion can be divided up in into various categories (e.g., Christianity, Islam, Judaism, Hinduism, Buddhism, and other), or more simply, religion can be divided into those who believe in a god (theism) and those who do not (atheism). There are multiple economic categorizations or schools as well (e.g., Keynsians, monetarists, libertarians, behavioral finance economists, etc.). Debates and disagreements across the rainbow of religions and economic schools have been going on for centuries, and the arrival and departure of the 2008-09 financial crisis further ignited the battle between the “behavioralists” (behavioral finance economists) and the “rationalists” (traditional free market economists).

Behavioral Finance on the Offensive

In the efficient market world of the “rationalists,” market prices reflect all available information and cannot be wrong at any moment in time. Effectively, individuals are considered human calculators that optimize everything from interest rates and costs to benefits and inflation expectations in every decision. What classic economists fail to account for are the emotional and behavioral flaws made by individuals.

Claiming financial market decisions are not impacted by emotions becomes more challenging to defend, if you consider the countless irrational anomalies occurring throughout history. Consider the following:

- Tulip Mania: Bubbles are nothing new – they have persisted for hundreds of years. Let’s reflect on the tulip bulb mania of the 1600s. For starters, I’m not sure how classic economists can explain the irrational exchanging of homes or a thousand pounds of cheese for a tulip bulb? Or how peak prices of $60,000+ in inflation-adjusted dollars were paid for a bulb at the time (C-Cynical)? These are tough questions to answer for the rationalists.

- Flash Crash: Seeing multiple stocks and Exchange Traded Funds (ETFs) temporarily plummet -99% in minutes is not exactly the sign of an efficient market. Stalwarts like Procter & Gamble also collapsed -37%, only to rebound minutes later near pre-collapse levels. All this volatility doesn’t exactly ooze with efficiency (see Making Millions in Minutes).

- Negative Interest Rates: Plenty of so-called pundits are arguing that equity markets are expensive, but what about the $8 trillion in negative interest rate bonds? Prices for many of these bonds are astronomical. Paying someone to take my money doesn’t make a lot of sense, but trillions in speculative investments are still being made today.

- Technology and Real Estate Bubbles: Both of these asset classes were considered “can’t lose” investments in the late 1990s and mid-2000s, respectively. Many tech stocks were trading at unfathomable values (more than 100 x’s annual profits) and homebuyers were inflating real estate prices because little-to-no money was required for the purchases.

- ’87 Crash: October 19, 1987 became infamously known as “Black Monday” since the Dow Jones Industrial Average plunged over -22% in one day (-508 points), the largest one-day percentage decline ever.

The ever-growing list of nonsensical anomalies only makes the rationalists’ jobs that much tougher in refuting the illogical behavior. Risk aversion has been alive and well in the post financial crisis environment as wild swings have resulted from a wide range of concerns, including: the U.S. debt downgrade; Arab Spring; potential Greek exit from the EU; Sequestration; Fed Taper Tantrum; Obamacare implementation; Russian invasion of Ukraine; Gaza conflict; Fukashima disaster; Ebola outbreak; Ferguson tensions; Paris/San Bernardino/Brussels terrorist attacks; China recessionary fears; oil price volatility; Mideast turmoil – ISIS expansion; Federal Reserve rate increases; and many other worries. Often, the human lizard brain is what leads to sub-optimal decision making. Maybe the rationalists can use the same efficient market framework to help explain to my wife why I ate a whole box of Twinkies in one sitting?

Rationalist Rebuttal

The growing list of market inefficiencies has given the rationalists a black eye, but they are not going down without a fight. Here are some quotes from Fama and fellow Chicago rationalist pals:

On the Crash-Related Attacks from Behavioralists: Behavioralists say traditional economics has failed in explaining the irrational decisions and actions leading up to the 2008-09 crash. Fama states, “I don’t see this as a failure of economics, but we need a whipping boy, and economists have always, kind of, been whipping boys, so they’re used to it. It’s fine.”

Rationalist Explanation of Behavioral Finance: Fama doesn’t deny the existence of irrational behavior, but rather believes rational and irrational behaviors can coexist. “Efficient markets can exist side by side with irrational behavior, as long as you have enough rational people to keep prices in line,” notes Fama. John Cochrane treats behavioral finance as a pseudo-science by replying, “The observation that people feel emotions means nothing. And if you’re going to just say markets went up because there was a wave of emotion, you’ve got nothing. That doesn’t tell us what circumstances are likely to make markets go up or down. That would not be a scientific theory.”

Description of Panics: “Panic” is not a term included in the dictionary of traditional economists. Fama retorts, “You can give it the charged word ‘panic,’ if you’d like, but in my view it’s just a change in tastes.” Calling these anomalous historic collapses a “change in tastes” is like calling American Idol judge Simon Cowell, “diplomatic.” More likely, what’s really happening is these severe panics are driving investors’ changes in preferences.

Throwing in White Towel Regarding Crash: Not all classic economists are completely digging in their heels like Fama and Cochrane. Gary Becker, a rationalist disciple, acknowledged the blind-siding of the 2008-2009 financial crisis when he admitted, “Economists as a whole didn’t see it coming. So that’s a black mark on economics, and it’s not a very good mark for markets.”

Settling Dispute with Lab Rats

The boxing match continues, and the way the behavioralists would like to settle the score is through laboratory tests. In the documentary Mind Over Money, numerous laboratory experiments are run using human subjects to tease out emotional behaviors. Here are a few examples used by behavioralists to bolster their arguments:

- The $20 Bill Auction: Zach Burns, a professor at the University of Chicago, conducted an auction among his students for a $20 bill. Under the rules of the game, as expected, the highest bidder wins the $20 bill, but as an added wrinkle, Burns added the stipulation that the second highest bidder receives nothing but must still pay the amount of the losing bid. Traditional economists would conclude nobody would bid higher than $20. See the not-so rational auction results here at minute 1:45.

- $100 Today or $102 Tomorrow? This was the question posed to a group of shoppers in Chicago, but under two different scenarios. Under the first scenario, the individuals were asked whether they would prefer receiving $100 in a year from now (day 366) or $102 in a year and one additional day (day 367)? Under the second scenario, the individuals were asked whether they would prefer receiving $100 today or $102 tomorrow? The rational response to both scenarios would be to select $102 under both scenarios. See how the participants responded to the questions here at minute 4:30.

Rationalist John Cochrane is not fully convinced. “These experiments are very interesting, and I find them interesting, too. The next question is, to what extent does what we find in the lab translate into how people…understanding how people behave in the real world…and then make that transition to, ‘Does this explain market-wide phenomenon?,’” he asks.

As I alluded to earlier, religion, politics, and economics will never fall under one universal consensus view. The classic rationalist economists, like Eugene Fama, have in aggregate been on the defensive and taken a left-hook in the eye for failing to predict and cohesively explain recurring market inefficiencies, including the financial crash of 2008-09. On the other hand, Richard Thaler and his behavioral finance buds will continue on the offensive, consistently swinging at the classic economists over this key economic mind versus money dispute.

See Complete Mind Over Money Program

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in PG and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Pulling the Band-Aid Off Slowly

Federal Reserve monetary policy once again came to the forefront as the Fed released its April minutes this week. After living through years of a ZIRP (Zero Interest Rate Policy) coupled with QE (Quantitative Easing), many market participants and commentators are begging for a swifter move back to “normalization” (a Federal Funds Rate target set closer to historical averages). The economic wounds from the financial crisis may be healing, as seen in the improving employment data, but rather than ripping off the interest rate Band-Aid quickly and putting the pain behind investors, the dovish Fed Chair Janet Yellen has been signaling for months the Fed will increase rates at a “gradual” pace.

Despite the more hawkish tone regarding the possibility of an additional rate hike in June, Fed interest rate futures are currently still only factoring in about a 26% probability of a rate increase in June. As I have been saying for years (see “Fed Fatigue”), there has, and will likely continue to be, an overly, hyper-sensitive focus on monetary policy and language disseminated by members of the Feral Reserve Open Market Committee.

For example, in 1994, despite the Fed increasing target rates by +2.5% in a single year (from 3.0% to 5.5%), stock prices finished roughly flat for the year, and the market resumed its decade-long bull market run the subsequent year. Today, the higher bound of Fed Funds sits at a mere 0.5%, and the Fed has announced only one target increase this cycle (equaling a fraction of the ’94 pace). Even if investors are panicking over another potential quarter point in June or July, can you say, “overkill?”

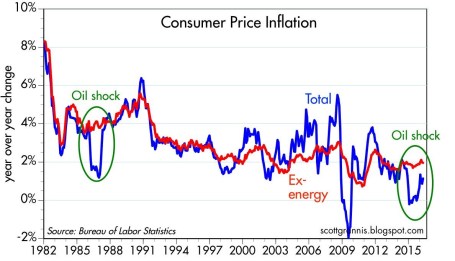

While the Fed is approaching the lower-end of the range for its employment mandate (unemployment currently sitting at 5%), despite the recent bounce in oil prices, core inflation remains in check (see Calafia Pundit chart below). This long-term benign pricing trend gives the Fed a longer leash as it relates to the pace of future rate hikes.

Source: Calafia Beach Pundit

Sure, ripping off the Fed Band-Aid with a small handful of +0.5% (50 bps) hikes might appease hawkish investors, but Janet Yellen, the “Fed Fairy Godmother,” has made it abundantly clear she is in no hurry to raise rates. Whether there is zero, one, or two additional rate hikes this year is much less important than other fundamental factors. Adding fuel to the Fed-speak fire in the short-run will be Yellen speeches on May 27th at Harvard University and on June 6th at the World Affairs Council of Philadelphia. And then following that, we will have the “Brexit” referendum (i.e., the vote on whether Britain should exit the EU); a steady stream of election noise; and many other unanticipated economic/geopolitical headlines.

As I continually state, the key factors driving the direction of long-term stock prices are profits, interest rates, valuations, and sentiment (see Follow the Stool). Profits (ex-energy) are growing near record levels; interest rates are near record lows (even with potential 2016 hikes); valuations remain near historical averages; and sentiment regarding stock ownership is firing strongly as a positive contrarian indicator.

While many pundits have been calling for and predicting the Fed to rip the Band-Aid off with a swift string of rate increases, persistently low inflation, coupled with a consistently dovish Fed Chair are likely to lead to a slow peeling of the monetary policy Band-Aid. Unfortunately, the endless flow of irrelevant monetary policy guesswork regarding the timing of future rate hikes will be more painful than the actual hikes themselves. In the end, any future hikes should be justified with a stronger economic foundation, which should represent future strength, rather than future weakness.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Yield Starving Foreigners Go Muni Hunting

In the current cold, barren, negative interest rate environment, foreign investors are getting hungry and desperate as they hunt for yield. In the hopes of kick-starting economic activity around the globe, central bankers are taking the drastic measure of establishing negative interest rate policies. This unusual endeavor is pressing international investors to chase yield, no matter how small, wherever they can find it.

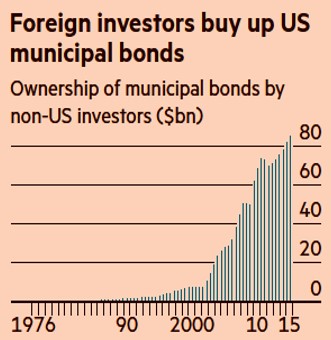

One of those areas in which foreigners are hunting for yield is the U.S. municipal bond market (see FT article). On the surface, this sounds ludicrous. Why would an outsider living in Germany or Japan invest in a U.S. municipal bond that yields a paltry rate that’s less than 1.7%, especially considering those investors will not benefit from the tax-free income advantages offered to Americans?

As strange as it sounds, Natalie Cohen, Wells Fargo’s head of municipal research correctly pointed out this pursuit for municipal bond yield across continents boils down to simple math. “Even if [foreign investors] are not subject to the US tax code, a plus two is better than a minus one,” Cohen notes.

Although foreign investment in the $3.7 trillion municipal bond market is relatively small, the rapidly rising appetite for munis is clearly evident, as shown in the chart below.

Source: The Financial Times

With our country’s crumbling roads and bridges, these ever-increasing piles of foreign cash pouring into our municipal bonds are helping fund a broad array of U.S. infrastructure projects. Given the election season is upon us, this issue may gain heightened attention. Both likely-presidential candidates are highlighting the need for infrastructure investment as part of their platforms, and the NIRP (negative interest rate policies) agenda of international central banks may make these municipal infrastructure dreams a reality.

We Americans are no stranger to the idea of borrowing money from foreigners. In fact, the Chinese own about $1.3 trillion of our Treasury bonds. This is all fine and dandy as long as the international appetite for lending us money remains healthy. If our city, state, and federal governments become too addicted to the Chinese, Europeans, and Japanese loans, financial risks can/will grow to unmanageable levels. Guess what happens once our borrowings swell to a level that forces foreigners to question our ability of repaying their debt? Interest rates will accelerate upwards, our interest payments will balloon, and our deficits will widen. The consequences of these unfavorable outcomes will be devastating budget cuts and/or tax increases.

For the time being, we will gladly accept the charitable donations of foreign investors to help lower funding costs for our sorely needed infrastructure projects. Fortunately, for now fiscal sanity is prevailing. The post financial crisis political environment has scared municipalities from borrowing too much, as explained here by the FT:

“For local and state politicians grappling with pension reforms, new healthcare programs and — in Alaska, Texas and Oklahoma — a drag on finances from lower energy prices, the looming presidential election is also diminishing the appeal of [municipal debt] issuance.”

In a near-zero/negative rate environment, there certainly will be incentives for irresponsible governments and corporations to extend themselves too far with cheap debt. However, in the short-run, as starving foreigners hunt for yield in the U.S. municipal bond market, Americans have the opportunity of exploiting this foreign generosity for the benefit our country’s long-term infrastructure.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Flat Pancakes & Dividends

Over the last 18 months, stock prices have been flat as a pancake. Absent a few brief China and recessionary scares, the Dow Jones Industrial Average index has spent most of 2015 and 2016 trading between the relatively tight levels of 17,000 – 18,000. Record corporate profits and faster growth than other developed and developing markets have created a tug-of-war with countervailing factors. A strong dollar, reversal in monetary policy, geopolitical turmoil, and volatile commodity markets have produced a neutralizing struggle among corporate executives with deep financial pockets and short arms. In this environment, share buybacks, stable profit margins, and growing dividends have taken precedence over accelerated capital investments and expensive new-hires.

With flat stock prices and interest rates at unprecedented low levels, it’s during times like these that stock investors really appreciate the appetizing flavor of stable, growing dividends. To this day, I still find it almost impossible to fathom how investors are burning money by irrationally speculating in $7 trillion in negative interest rate bonds (see Retire at Age 90).

Historically there are very few periods in which stock dividend yields have exceeded bond yields (2.1% S&P yield vs. 1.8% 10-Year Treasury yield). As I showed in my Dividend Floodgates article, for roughly 50 years (1960 – 2010), the yield on the 10-Year Treasury Notes have exceeded the dividend yield on stocks (S&P 500) – that longstanding trend does not hold today.

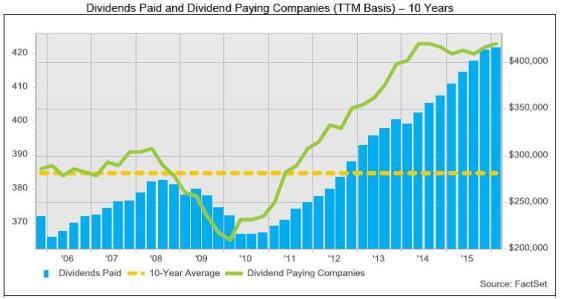

In the face of the competitive stock market, several trends are contributing to the upward trajectory in dividend payments (see chart below).

#1.) Corporate profits (ex-Energy) are growing and at/near record levels. Earnings are critical in providing fertile ground for dividend growth.

#2.) Demographics, plain and simple. As 76 million Baby Boomers transition into retirement, their income needs escalate. These shareholders whine and complain to corporate executives to share the spoils and increase dividends.

#3.) Low interest rates and disinflation are shrinking the available pool of income generating assets. As I pointed out above, when trillions of dollars are getting thrown into negative yielding investments, many investors are flocking to alternative income-generating assets…like dividend paying stocks.

Source: FactSet

The Power of Dividends (Case Studies)

Most people don’t realize it, but over the last 100 years, dividends have accounted for approximately 40% of stocks’ total return as measured by the S&P 500. In other words, using history as a guide, if you initially invested in a stock XYZ at $100 that appreciated in value to $160 (+60%) 10 years later, that stock on average would have supplied an incremental $40 in dividends (40%) over that period, creating a total return of 100%.

Rather than using a hypothetical example, here are a few stock specific illustrations that highlight the amazing power of compounding dividend growth rates. Here are two “Dividend Aristocrats” (stocks that have increased dividends for at least 25 consecutive years):

- PepsiCo Inc (PEP): PepsiCo has increased its dividend for an astonishing 44 consecutive years. Today, the dividend yield is 2.9% based on the current share price. But had you purchased the stock in June 1972 for $1.60 per share (split-adjusted), you would currently be earning a +188% dividend yield ($3.01 dividend / $1.60 purchase price), which doesn’t even account for the +6,460% increase in the share price ($104.96 per share today from $1.60 in 1972). Over that 44 year period, the split-adjusted dividend has increased from about $0.02 per share to an annualized $3.01 dividend per share today, which equates to a mind-blowing +16,153% increase. On top of the $103 price appreciation, assuming a conservative 5% dividend reinvestment rate, my estimates show investors would have received more than $60 in reinvested dividends, making the total return that much more gargantuan.

- Emerson Electric Co (EMR): Emerson Electric too has had an even more incredible streak of dividend increases, which has now extended for 59 consecutive years. Emerson currently yields a respectable 3.6% rate, but if you purchased the stock in June 1972 for $3.73 per share (split-adjusted), you would currently be earning a +51% dividend yield ($1.92 dividend / $3.73 purchase price), which doesn’t even consider the +1,423% increase in the share price ($53.31 per share today from $3.73 in 1972).

There is never a shortage of FUD (Fear, Uncertainty, and Doubt), which has kept stock prices flat as a pancake over the last couple of years, but market leading franchise companies with stable/increasing dividends do not disappear during challenging times. Record profits (ex-energy), demographics, and a scarcity of income-generating investment alternatives are all contributing factors to the increased appetite for dividends. If you want to sweeten those flat pancakes, do yourself a favor and pour some quality dividend syrup over your investment portfolio.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and PEP, but at the time of publishing had no direct position in EMR or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Energizer Market… Keeps Going and Going

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (May 2, 2016). Subscribe on the right side of the page for the complete text.

Boom, boom, boom…it keeps going…and going…and going…

You’ve seen the commercials: A device operating on inferior batteries dies just as a drum-beating, battery operated Energizer bunny comes speeding and spiraling across the television screen. Onlookers waiting for the battery operated toy to run out of juice, instead gaze in amazement as they watch the energized bunny keep going and going. The same phenomenon is occurring in the stock market, as many observers eagerly await for stock prices to die. The obituary of the stock market has been written many times over the last eight years (see Series of Unfortunate Events). Mark Twain summed up this sentiment well, when after a premature obituary was written about him, he quipped, “The reports of my death are greatly exaggerated.”

With fears abound, stocks added to their annual gains by finishing their third consecutive positive month with the S&P 500 indexes and Dow Jones Industrial Average advancing +0.5% and +0.3%, respectively. Skeptics and worry-warts have been concerned about stocks plummeting ever since the Financial Crisis of 2008-2009. We experienced a 100 year flood then, and as a consequence, scarred investors now expect the 100 year flood to repeat every 100 days (see also 100 Year Flood). Given the damage created in the wake of the “Great Recession,” many individuals have become afraid of their own shadow. The shadows currently scaring investors include the following:

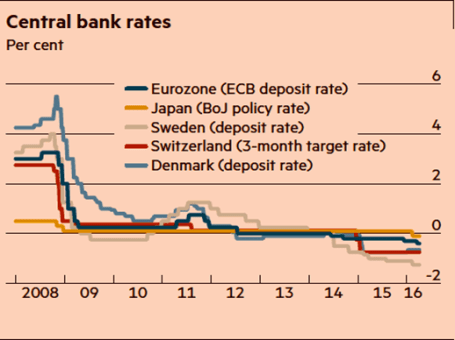

- Negative Interest Rates: The unknown consequences of negative interest rate policies by central banks (see chart below).

- U.S. Monetary Policy: The potential continuation of the Federal Reserve hiking interest rates.

- Sluggish Economic Growth: With a GDP growth figure up only +0.5% during the first quarter many people are worried about the vulnerability of slipping into recession.

- Brexit Fears: Risk of Britain exiting the European Union (a.k.a. “Brexit”) will blanket the airwaves as the referendum approaches next month

For these reasons, and others, the U.S. central bank is likely to remain accommodative in its stance (i.e., Fed Chairwoman Janet Yellen is expected to be slow in hitting the economic brakes via interest rate hikes).

Source: Financial Times. Central banks continue with attempts to stimulate with zero/negative rates.

Climbing the Wall of Worry

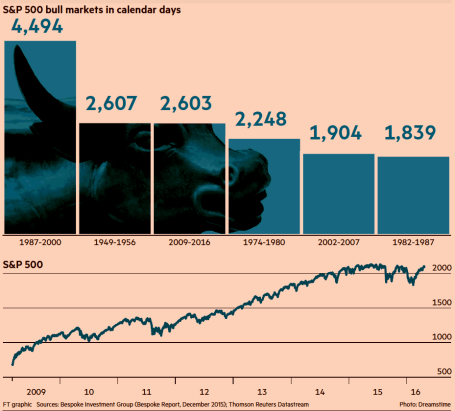

Despite all these concerns, stock prices continue climbing the proverbial “wall of worry” while approaching record levels. As famed investor Sir John Templeton stated on multiple occasions, “Bull markets are born on pessimism, and they grow on skepticism, mature on optimism, and die on euphoria.” It’s obvious to me there currently is no euphoria in the overall market, if you consider investors have withdrawn $2 trillion in stock investments since 2007. The phenomenon of stocks moving higher in the face of bad news is nothing new. A recent study conducted by the Financial Times newspaper shows the current buoyant bull market entering the second longest advancing period since World War II (see chart below).

Source: Financial Times

There will never be a shortage of concerns or bad things occurring in a world of 7.4 billion people, but the Energizer bunny U.S. economy has proven resilient. Our economy is entering its seventh consecutive year of expansion, and as I recently pointed out the job market keeps plodding along in the right direction – unemployment claims are at a 43-year low (see Spring Has Sprung). Over the last few years, these job gains have come despite corporate profits being challenged by the headwinds of a stronger U.S. dollar (hurts our country’s exports) and tumbling energy profits. Fortunately, the negative factors of the dollar and oil prices have stabilized lately, and these dynamics are in the process of shifting into tailwinds for company earnings. The -5.7% year-to-date decline in the Dollar Index coupled with the recent rebound in oil prices are proof that the economic laws of supply-demand eventually respond to large currency and commodity swings. With the number of rigs drilling for oil down by approximately -80% over the last two years, it comes as no surprise to me that a drop in oil supply has steadied prices.

The volatility in oil prices has been amazing. Energy companies have been reeling as oil prices dropped -76% from a 2014-high of $108 per barrel to a 2016-low of $26 per barrel. Since then, the picture has improved significantly. Crude oil prices are now hovering around $46 per barrel, up +76%.

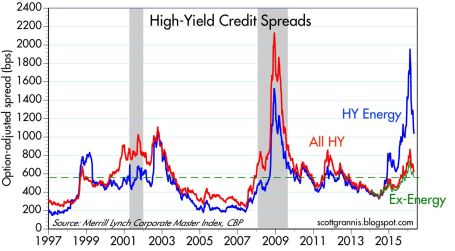

Energy Bankruptcy & Recessionary Fears Abate

If you take a look at the borrowing costs of high-yield companies in the chart below (Calafia Beach Pundit), you can see that prior spikes in the red line (all high-yield borrowing costs) were correlated with recessions – represented by the gray periods occurring in 2001 and 2008-09. During 2016, you can see from the soaring blue line, investors were factoring in a recession for high-yield energy companies (until the oil price recovery), but the non-energy companies (red-green lines) were not anticipating a recession for the other sectors of the economy. Bottom-line, this chart is telling you the knee-jerk panic of recessionary fears during the January-February period of this year has quickly abated, which helps explain the sharp rebound in stock prices.

After a jittery start to 2016 when economic expectations were for a dying halt, investors have watched stocks recharge their batteries in March and April. There are bound to be more fits and starts in the future, as there always are, but for the time being this Energizer bunny stock market and economy keeps going…and going…and going…

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}