Archive for March, 2016

Chasing Headlines

It’s been an amazing start to the year. First the market cratered on slowing China economic concerns, domestic recessionary fears, deteriorating oil prices, and negative interest rates abroad. In response to all these worries (and others), stocks dove more than -11% (S&P 500 Index) in January, before settling down. Subsequently, the market has made a screaming recovery, in part due to dovish monetary policy comments (i.e., reduction in forecasted interest rate hikes) and diminished anxiety over a potential global collapse. Month-to-date stocks are up an impressive +5.4%, and year-to-date equities are flattish, or down less than -1%.

With an endless amount of information flowing across our smart phones and computers, it becomes quite easy and tempting to chase news headlines, just like a hyper dog chasing a car. But even once an investor catches up (or reacts) to a headline, there’s confusion around how to profit from the fleeting information. First of all, every plugged-in hedge fund and institutional investor has likely already traded on the stale information you received. Second of all, rarely is the data relevant to the long-term cash generating capabilities of the company or economy. And lastly, the news is more often than not, instantly factored into the stock price. Chasing news headlines only eaves individual investors holding the bag of performance-shattering transactions costs, taxes, and worn-out pricing.

The heightened volatility in late 2015 and early 2016 hasn’t however prevented investors and so-called pundits from attempting to time the market. Any battle-tested investment veteran knows it’s virtually impossible to consistently time the market (see also Market Timing Treadmill), but this fact hasn’t prevented speculators from attempting the feat nonetheless. Famed investment guru, Peter Lynch, who earned an average +29% annual return from 1977-1990, summed it up well when he stated the following:

“Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.”

The Important Factors

As I’ve written many times in the past, the keys to long-term stock performance are not knee-jerk reactions to headlines, but rather these following crucial factors (see also Don’t Be a Fool, Follow the Stool):

- Profits

- Interest Rates

- Sentiment

- Valuations

On the profit growth front, corporate income has been pressured by numerous headwinds over the last few years, including an export-shattering increase in the value of the U.S. dollar and a profit-squeezing collapse in energy sector earnings. As you can see from the chart below, the value of the U.S. dollar increased by about 25% from mid-2014 to early-2015, in part because of diverging global central bank policies (more hawkish U.S. Fed vs. more dovish ECB/international central banks). Since that spike, the dollar has settled into a broad range (95 – 100), and the former forceful headwind have now turned into modest tailwinds. This trend is important because an estimated 35-40% of corporate profits are derived from international operations.

Adding insult to injury, the roughly greater than -70% decline in forward energy earnings over the last 18 months has caused a significant hit to overall S&P 500 profits. The tide appears to be finally turning (or at least stabilizing) however, as we’ve seen oil prices rebound by about +30% this year from the lows in January. If these aforementioned trends persist, profit pressures in 2016 are likely to abate significantly, and may actually become additive to growth.

Source: Barchart.com

Profits are important, but so are interest rates. While incessant talk about the path of future Fed policy continues to blanket the airwaves (see also Fed Fatigue), absent a rapid increase in interest rates (say 300-400 basis points), interest rates remain unambiguously positive for equity markets, providing a floor for the oft-repeated volatility in financial markets. As long as stocks are providing higher yields than many bonds, and depositors are earning 0% (or negative rates) on their checking accounts, stocks may remain unloved, but not forgotten.

And speaking of unloved, the sentiment for stocks remains sour. One need look no further than the quarter-billion dollars in hemorrhaging outflows out of U.S. equity funds (see ICI Long-Term Mutual Fund Flows) since 2014. This deep underlying skepticism serves as a positive contrarian indicator for future equity prices. Right now, very few individual investors are swimming in the pool – the time to get out of the stock market pool is when everyone is jumping in.

And lastly, valuations remain very much in line with historical averages (approximatqely 17x 2016 projected earnings), especially considering the generational low in interest rates. Bears continue to point to the elevated CAPE ratio, which has been a disastrous indicator the last seven years (and longer), as a reason to remain cautious. The ironic part is that valuations are virtually guaranteed to improve a few years from now as we roll off the artificially depressed years of 2008-2010.

When you add it all up, zero (or negative) interest rates, combined with the other key factors of profits, sentiment, and valuations, equities remain an important and attractive part of a diversified long-term portfolio. Your objectives, time horizon, and risk tolerance will always drive the proportion of your equity allocation. Nevertheless, some bond exposure is essential to smooth out volatility. Regardless of your investment strategy, chasing headlines, like a dog chasing a car, serves no purpose other than leaving you with a tired, unproductive investment portfolio.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Cutting Losses with Fisher’s 3 Golden Sell Rules

Returning readers to Investing Caffeine understand this is a location to cover a wide assortment of investing topics, ranging from electric cars and professional poker to taxes and globalization. Investing Caffeine is also a location that profiles great investors and their associated investment lessons.

Today we are going to revisit investing giant Phil Fisher, but rather than rehashing his accomplishments and overall philosophy, we will dig deeper into his selling discipline. For most investors, selling securities is much more difficult than buying them. The average investor often lacks emotional self-control and is unable to be honest with himself. Since most investors hate being wrong, their egos prevent taking losses on positions, even if it is the proper, rational decision. Often the end result is an inability to sell deteriorating stocks until capitulating near price bottoms.

Selling may be more difficult for most, but Fisher actually has a simpler and crisper number of sell rules as compared to his buy rules (3 vs. 15). Here are Fisher’s three sell rules:

1) Wrong Facts: There are times after a security is purchased that the investor realizes the facts do not support the supposed rosy reasons of the original purchase. If the purchase thesis was initially built on a shaky foundation, then the shares should be sold.

2) Changing Facts: The facts of the original purchase may have been deemed correct, but facts can change negatively over the passage of time. Management deterioration and/or the exhaustion of growth opportunities are a few reasons why a security should be sold according to Fisher.

3) Scarcity of Cash: If there is a shortage of cash available, and if a unique opportunity presents itself, then Fisher advises the sale of other securities to fund the purchase.

Reasons Not to Sell

Prognostications or gut feelings about a potential market decline are not reasons to sell in Fisher’s eyes. Selling out of fear generally is a poor and costly idea. Fisher explains:

“When a bear market has come, I have not seen one time in ten when the investor actually got back into the same shares before they had gone up above his selling price.”

In Fisher’s mind, another reason not to sell stocks is solely based on valuation. Longer-term earnings power and comparable company ratios should be considered before spontaneous sales. What appears expensive today may look cheap tomorrow.

There are many reasons to buy and sell a stock, but like most good long –term investors, Fisher has managed to explain his three-point sale plan in simplistic terms the masses can understand. If you are committed to cutting investment losses, I advise you to follow investment legend Phil Fisher – cutting losses will actually help prevent your portfolio from splitting apart.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

The Traitorous 8 and Birth of Silicon Valley

Over my 25 year investment career, I’ve made quite a few technology investments and visited dozens of Silicon Valley companies. I heard bits and pieces about the story of the Traitorous 8, but I never fully comprehended the technology revolution they started. Out of intellectual curiosity, I decided to delve a little deeper into the topic.

At the heart of this topic is a small device about the size of a fingernail. This object has several different names and can be quite confusing. The official name is an integrated circuit or IC, but usually it’s referred to as a chip, microchip, or semiconductor. These chips have become ubiquitous, scattered invisibly throughout our daily lives in our cars, computers, TVs, cell phones, appliances, and remote controls (an average household is home to about 1,000 of these semiconductors). Despite most people taking the microchip for granted, this diminutive piece of silicon created from our beach’s sand has contributed the largest burst of wealth creation in human history.

Before gaining a true understanding into the birth of Silicon Valley, we have to better understand the historical context in which the global technology capital was created – this takes us back to the early twentieth century when the vacuum tube was invented in 1904. Before Al Gore invented the Internet, we needed computers, and before we had personal computers, we needed integrated circuits, and before we had integrated circuits we had vacuum tubes (see chart below). Vacuum tubes were the electronic circuitry components required to make telephones, radios and televisions work in the early 1900s.

Tech History & the Vacuum Tube

The vacuum tube was invented in 1904 by an English physicist named John Ambrose Fleming. Like semiconductors, the main function of a vacuum tube is to control the flow of electric current. More specifically, a vacuum tube controls the current transferred between cathode and anode to make a circuit. Vacuum tubes were used for amazing applications, but in modern society this technology has been largely replaced by semiconductors, primarily because of cost, scalability and reliability factors.

The first all-electronic digital computer title is usually awarded to the ENIAC computer, which stood for Electronic Numerical Integrator and Calculator. ENIAC was built at the University of Pennsylvania between 1943 and 1945 by two professors, John Mauchly and J. Presper Eckert. World War II, the Soviet Union Cold War, and the space race kicked off by the Sputnik launch all pushed the vacuum tube technology to its limits. To give you an idea of how costly and inefficient vacuum tubes were relative to today’s microchips consider some of the ENIAC statistics. ENIAC filled a 20 x 40 foot room; weighed 30 tons; used more than 18,000 vacuum tubes; and only operated 50% of the time because operators were continuously replacing burned out vacuum tubes. In fact, the ENIAC vacuum tubes generated so much heat, the temperature in the computer room often reached 120 degrees.

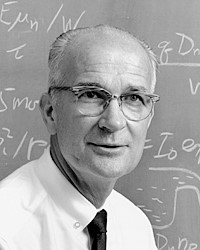

Shockley – The Godfather of the Transistor

Something had to change to improve vacuum tube technology, and it did…thanks in large part to a physicist named William Shockley, the so-called “Godfather of the Transistor.” Shockley received his Bachelor of Science degree from Caltech in 1932 and earned his Ph.D. degree from MIT in 1936. After graduation, Shockley left the famous Bell Labs research center, which was a research division of AT&T at the time (now owned by Nokia). As part of Shockley’s work at Bell Labs in the late 1940s, he contributed to the invention of the transistor with experimentalist Walter Brattain and quantum theorist John Bardeen. Fundamentally, the transistor is a switch, which over time has shrunk down to the size of a virus. The transistor is what ultimately replaced the vacuum tubes because it is smaller, more efficient, more reliable, more durable, and cheaper than vacuum tubes. Transistors switch and amplify the flow of electronic signals to create digital ones and zeros that instruct electronic applications. Without the benefits of shrinking transistors, today’s computer servers would be three stories high.

How small have transistors become? Take the iPhone 6 for example – it uses the A8 chip, which is made up of a whopping two billion transistors. To accomplish this feat, engineers are now creating transistors at the atomic level. Large semiconductor manufacturers like Intel Corp (INTC) are now developing transistors at the 10 nanometer level. To put this scale into perspective, consider a sheet of paper is approximately 100,000 nanometers thick. So in order to create a 10 nanometer sheet of paper, one would have to slice a single sheet 10,000 times thinner to reach 10 nanometers…mind-boggling.

Building atomic sized transistor technology is very cool, but also very expensive. Only a handful of semiconductor manufacturers have enough capital to build these new state-of-the art facilities. Case in point is Intel’s D1X fabrication facility in Hillsboro, Oregon, which is estimated to have cost $6 billion. Like seeing the pyramids – it’s difficult to understand the enormity of the structure without visiting it, which I was fortunate to do in 2014. It’s very ironic that in order to build these microscopic transistors and integrated circuits, multi-billion dollar manufacturing facilities the size of 38 football fields (~2.2 million square feet) are required. Another example of a next-generation manufacturing facility is Taiwan Semiconductor’s – Fab 15 (TSM), which was estimated to cost $9.3 billion.

These mega-transistor manufacturing facilities would not have been possible without Shockley’s contributions. Having helped invent the transistor largely replace the dominant computing technology of the last half century (i.e., vacuum tube), Shockley mustered up the courage to leave Bell Labs and start his own company, but he needed some cash to make it happen. He contacted Arnold Beckman, CEO of Beckman Coulter and his old professor at Caltech. Over a boat ride in Newport Beach, California, Shockley asked Beckman for $1 million to start his own lab. Silicon Valley potentially could have started in Southern California, but Shockley explained his aging mother lived in Palo Alto and convinced Beckman to start Shockley Semiconductor Laboratory in Mountain View, California during 1956.

After Shockley Semiconductor began operations, everything appeared to be going according to plan. Shortly after opening shop and recruiting the best and brightest engineers across the country, Shockley and his former Bell Labs colleagues Walter Brattain and John Bardeen were notified they all had won the Nobel Prize in physics (see photo below).

After the Nobel Prize celebrations, everything went downhill quickly. Shockley was known as a brilliant engineer but a horrific manager. He put his employees through a battery of tests including psychological tests, intelligence tests, and even lie detector tests. Shockley also posted employee salaries publicly and recorded phone calls. He was a paranoid individual who believed his workers were stealing trade secrets and sabotaging projects, so therefore he wouldn’t share findings with his research staff. Adding insult to injury, Shockley was a racist, who believed blacks were genetically inferior with subpar IQs, so they shouldn’t have kids.

Here is a video link summarizing William Shockley’s leadership:

The Traitorous 8 Surface

In 1957, the year after Shockley Semiconductor Labs started up, the division reached 30 employees. Eight of the employees, Sheldon Roberts, Eugene Kleiner, Victor Grinich, Jay Last, Julius Blank, Jean Hoerni, Robert Noyce, and Gordon Moore finally said, enough-is-enough and decided mutiny was their best option.

The disgruntled group ended up contacting a 30-year-old, snot-nosed, Harvard MBA graduate named Arthur Rock, the individual who eventually coined the phrase “venture capitalist.” In 1957, Rock was a New York banker working at Hayden Stone & Co. Rock believed the group of eight engineers (six of which had Ph.Ds) deserved attention, given their experience working with a Nobel Prize winner. The Traitorous 8 simply wanted to find an employer that would hire them as a group, but Rock advised them to start their own company – a novel idea during the 1950s.

After making a list and calling about 40 blue chip companies from the Wall Street Journal for funding, Rock almost gave up until they received a lead to contact Sherman Fairchild. Fairchild was a wealthy entrepreneur and playboy who hung out at the El Morocco in New York with Howard Hughes. Rock convinced Fairchild, the CEO of Fairchild Camera & Instrument, to invest $1.5 million into a Traitorous 8 startup.

The rest is history. The Traitorous 8 set up shop as Fairchild Semiconductor (FCS) in Mountain View, about twelve blocks from Shockley’s operations. Over the next 10 years, Fairchild Semiconductor grew from twelve employees to twelve thousand employees, and raked in some $130 million in annual revenues. Of the original Traitorous 8, two have become historical figures – Robert “Bob” Noyce and Gordon Moore. All good things come to an end, and Noyce and Moore increasingly got frustrated with Fairchild’s mismanagement of the semiconductor division.

After Fairchild passed over Noyce for a CEO promotion in 1968, Noyce told Moore, “I’m going to leave, are you interested?” Moore agreed, so he and Noyce contacted Arthur Rock again for his assistance. Rock quickly helped them raise $2.5 million, and Intel Corporation (short for “Integrated Electronics”) was born. Three years later in 1971, Intel launched its IPO at $23.50 per share ($.02 split-adjusted). An investment of $10,000 back then would be worth about $12,000,000 today –about a +120,000% return.

Here’s a video summarizing the creation of Intel:

Thomas Edison of Silicon Valley

Nowadays, Noyce is hailed by many as the “Thomas Edison of Silicon Valley.” Noyce received his Ph.D. from MIT and is most known for his invention of the integrated circuit. During the late 1950s, other engineers also worked on the IC, including Jack Kilby at Texas Instruments, but Noyce received the first patent in 1961. Unlike Kilby, who created his IC from germanium, Noyce created his IC from silicon, the semiconductor of choice still today. After a decade of litigation, Noyce and Kilby settled their differences and decided to cross-license their patents. Unfortunately, the Nobel Foundation doesn’t issue Nobel Prizes posthumously, so when the Nobel Prize was issued for the invention of the integrated circuit in the year 2000 (10 years after Noyce’s death), only Kilby was recognized. To Kilby’s credit, he acknowledged the contributions of Noyce and others in his Nobel speech with a story of a rabbit and beaver looking up at the Hoover Dam, “No, I didn’t build it myself. But it’s based on an idea of mine!”

Moore’s Law Established

Arguably, Moore was just as influential as Noyce, but due to his quiet leadership style, Moore is often overlooked. Moore was a year younger than Noyce and earned his chemistry degree from Berkeley and Ph.D. from Caltech. Unlike Noyce, who grew up in the Midwest (Iowa), Moore was raised near Palo Alto, which made recruiting Moore by William Shockley quite easy. Moore’s largest contribution is considered to “Moore’s Law,” which generally states the number of transistors (i.e., a chip’s computing power) will double every 1-2 years. During the 1980s, Noyce described the implications of Moore’s Law by comparing Moore’s Law to the airline industry. If the airline industry progressed at the trajectory of the semiconductor industry over the last 20 years, then the 767 airplane would cost $500 and travel around the world in 20 minutes on five gallons of gas. Regrettably, not many industries advance at the pace of semiconductors.

Moore came up with “Moore’s Law” when her wrote a seminal article for Electronics magazine in 1965 and in the article he properly predicted that the number of transistors that could be squeezed onto a microchip (around 60 at the time) would increase 1,000-fold to 60,000 transistors by 1975. It would take decades for his projections to come true, but Moore very presciently predicted the explosion of home computers, cell phones (which he called “portable communications equipment”), electronic wrist-watches, digital cars, and a host of other electronic devices and applications. A half century later, Moore’s Law holds true, but the pace of transistor growth admittedly is slowing. The physics behind semiconductor manufacturing is running into serious limitations of quantum mechanics, cost, and heat. Microchips are becoming so dense and fast that the internal components in many cases are melting the chips in research labs.

Here is a video link summarizing Moore’s Law:

While Moore’s Law is approaching diminishing returns, the costs of microchips keep declining, power keeps increasing, and efficiency keeps improving. Despite the slowing in Moore’s Law, as you can see below, the adoption of transistors via microchips is not plateauing. According to Intel, we are now consuming an estimated sextillion transistors!

Source: Intel Corporation

Politics, economics, terrorism, and social issues may dominate the daily headlines, but behind the scenes there are daily miracles occurring due to technology advancements. Driving much of that innovation is the microchip, and without the Traitorous 8, the world would look a lot different and there would be no Silicon Valley as we know it today. Had Robert Noyce and Gordon Moore miserably resigned themselves to remain at Shockley Semiconductor, perhaps mankind would not have achieved the giant strides in global standards of living (see chart below). Thankfully, their contributions live on today and ensure a bright future for our kids, grandchildren, and the world at large.

Source: FRED

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and in INTC (non-discretionary), TXN (non-discretionary), T (non-discretionary), but at the time of publishing had no direct position in TSM, NOK, FCS, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Dolphin or Shark…Time for Concern?

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (March 1, 2016). Subscribe on the right side of the page for the complete text.

Through the choppy stock market waters of February, investors nervously tried to stay afloat as they noticed a fin cutting through the water. The only problem is determining whether the fin approaching is coming from a harmless dolphin or a ferocious shark? The volatility in 2016 has been disconcerting for many, but a life preserver was provided during the month with the Dow Jones Industrial Average up a modest 50 points (+0.30%).

Remaining calm can be challenging when facing a countless number of ever-changing concerns. Stock investors have caught lots of fish since early 2009 (prices have about tripled), but here are some of the scary headlines (fins) floating out in the financial markets:

- Recession? Overall corporate profits have slowed in the face of plummeting energy prices and the headwind of a strong dollar. However, corporate profit margins remain near record levels and if you exclude the decline in the troubled oil patch, core profits keep chugging along. If an imminent recession were actually on the horizon, you wouldn’t expect to see a 4.9% unemployment rate (8-year low); record auto sales; an improving housing market; and stimulative national gasoline prices at $1.75/gallon (recent recessions have been caused by high energy prices).

- Negative Interest Rates: Would you like to get paid to borrow money? With $6 trillion dollars of negative interest rate bonds in the market (see chart below), that’s exactly what is happening. Just imagine walking into your local Best Buy, and asking the salesman, “Can I borrow $2,000 to buy that big screen TV there…and oh by the way, can you pay me interest every month after you give me the money?” Scary to think many people are panicked over the stock market when they should be more alarmed over negative interest rates. Would you rather earn 6.4% on the average stock (S&P 500 earnings yield) and a 2.2% dividend yield vs negative interest rate bonds? As I always caution investors, even though interest rates are at/near a generational low, diversified portfolios still need exposure to bonds, even if you’re at/near retirement because of the stability they provide. Bonds act like expensive pillows – they are necessary to sleep at night. Although some observers point to negative rates as a sign of a global collapse, low inflation, aggressive foreign central bank monetary policies, and a lingering risk aversion hangover from the 2008-09 financial crisis probably have more to do with the current strange status of interest rates.

Source: Financial Times

- Political Turbulence: Uncertainty abounds in another election year, just as is the case every other four years. As we head into Super Tuesday, the day in the presidential primary season when the largest number of states hold primary elections, the Republicans are set to battle for approximately half of the delegates necessary to secure the party nomination. The Democrats will be competing for about one-third of the delegates. While many individuals are placing paramount importance on the outcomes of the presidential elections, history teaches us otherwise. The ultimate person elected as president will certainly have a significant impact on the direction of the country, but there are other contributing factors as important (or more important) to economic growth, including the Federal Reserve, and the two houses of Congress. On numerous occasions, I have pointed out the irrelevance of presidential politics (see also Who Said Gridlock is Bad?). As the chart shows below, the past confirms there is no consistency to stock market performance based on political party affiliations. Stocks have performed strongly (and poorly) under both party affiliations.

- Brexit? After lengthy negotiations with EU leaders in Brussels, Britain’s Prime Minister David Cameron set June 23rd as the referendum date for voters to determine whether Britain stays in the European Union. Opinions remain divided (see chart below), but we have seen this movie before with Greece’s threat to leave the EU. As we experienced with the Greece exit (“Grexit”) drama, calmer heads are likely to prevail again. Nevertheless, until the end of June, regrettably we will be forced to listen to continued Brexit fears (see also Brexit article in the Economist for a more thorough review).

- Collapsing Oil Prices: The violent decline in oil prices over the last few years has been swift from about $100/barrel to $34/barrel today. However, the economic slowdown in China, coupled with a stronger U.S. dollar, has led to a broad downfall in commodity prices over the last five years as well. As much as declining demand has hurt commodities and been stimulative for buyers, over-building and excess supply has pressured prices equally. Fortunately, there are signs commodity prices could be in the process of bottoming (see CRB Index).

Financial market volatility in early 2016 has frayed some nerves, and the appearance of swirling fins has many investors wondering whether now’s the time to swim for shore or remain calm and catch the next growth wave. Despite the concerns over a potential recession, negative interest rates, bitter politics, Brexit fears, and depressed oil prices, our economy keeps slowly-but-surely powering forward. While U.S. corporations have been negatively impacted by a strong currency, compressed banking profits (i.e., lower interest rates), and a weak energy sector, S&P 500 companies are rewarding investors by returning a record $1 trillion in dividends and share buybacks (up from $500 million in 2005). When swimming in the current financial markets, you will be better served by swimming with the harmless dolphins rather than panicking over imaginary sharks.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in BBY or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}

{kind=link}

{kind=link}

{kind=link}