Archive for November, 2016

Sleeping and Napping Through Bubbles

We have lived through many investment bubbles in our history, and unfortunately, most investors sleep through the early wealth-creating inflation stages. Typically, the average investor wakes up later to a hot idea once every man, woman, and child have identified the clear trend…right as the bubble is about burst. Sadly, the masses do a great job of identifying financial bubbles at the end of a cycle, but have a tougher time realizing the catastrophic consequences of exiting a tired winner. Or as strategist Jim Stack states, “Bubbles, for the most part, are invisible to those trapped inside the bubble.” The challenge of recognizing bubbles explains why they are more easily classified as bubbles after a colossal collapse occurs. For those speculators chasing a precise exit point on a bubblicious investment, they may be better served by waiting for the prick of the bubble, then take a decade long nap before revisiting the fallen angel investment idea.

Even for the minority of pundits and investors who are able to accurately identify these financial bubbles in advance, a much smaller number of these professionals are actually able to pinpoint when the bubble will burst. Take for example Alan Greenspan, the ex-Federal Reserve Chairman from 1987 to 2006. He managed to correctly identify the technology bubble in late-1996 when he delivered his infamous “irrational exuberance” speech, which questioned the high valuation of the frothy, tech-driven stock market. The only problem with Greenspan’s speech was his timing was massively off. Stated differently, Greenspan was three years premature in calling out the pricking of the bubble, as the NASDAQ index subsequently proceeded to more than triple from early 1997 to early 2000 (the index exploded from about 1,300 to over 5,000).

One of the reasons bubbles are so difficult to time during their later stages is because the deflation period occurs so quickly. As renowned value investor Howard Marks fittingly notes, “The air always goes out a lot faster than it went in.”

Bubbles, Bubbles, Everywhere

Financial bubbles do not occur every day, but thanks to the psychological forces of investor greed and fear, bubbles do occur more often than one might think. As a matter of fact, famed investor Jeremy Grantham claims to have identified 28 bubbles in various global markets since 1920. Definitions vary, but Webster’s Dictionary defines a financial bubble as the following:

A state of booming economic activity (as in a stock market) that often ends in a sudden collapse.

Although there is no numerical definition of what defines a bubble or collapse, the financial crisis of 2008 – 2009, which was fueled by a housing and real estate bubble, is the freshest example in most people minds. However, bubbles go back much further in time – here are a few memorable ones:

Dutch Tulip-Mania: Fear and greed have been ubiquitous since the dawn of mankind, and those emotions even translate over to the buying and selling of tulips. Believe it or not, some 400 years ago in the 1630s, individual Dutch tulip bulbs were selling for the same prices as homes ($61,700 on an inflation-adjusted basis). This bubble ended like all bubbles, as you can see from the chart below.

Source: The Stock Market Crash.net

British Railroad Mania: In the mid-1840s, hundreds of companies applied to build railways in Britain. Like all bubbles, speculators entered the arena, and the majority of companies went under or got gobbled up by larger railway companies.

Roaring 20s: Here in the U.S., the Roaring 1920s eventually led to the great Wall Street Crash of 1929, which finally led to a nearly -90% plunge in the Dow Jones Industrial stock index over a relatively short timeframe. Leverage and speculation were contributors to this bust, which resulted in the Great Depression.

Nifty Fifty: The so-called Nifty Fifty stocks were a concentrated set of glamor stocks or “Blue Chips” that investors and traders piled into. The group of stocks included household names like Avon (AVP), McDonald’s (MCD), Polaroid, Xerox (XRX), IBM and Disney (DIS). At the time, the Nifty Fifty were considered “one-decision” stocks that investors could buy and hold forever. Regrettably, numerous of these hefty priced stocks (many above a 50 P/E) came crashing down about 90% during the 1973-74 period.

Japan’s Nikkei: The Japanese Nikkei 225 index traded at an eye popping Price-Earnings (P/E) ratio of about 60x right before the eventual collapse. The value of the Nikkei index increased over 450% in the eight years leading up to the peak in 1989 (from 6,850 in October 1982 to a peak of 38,957 in December 1989).

Source: Thechartstore.com

The Tech Bubble: We all know how the technology bubble of the late 1990s ended, and it wasn’t pretty. PE ratios above 100 for tech stocks was the norm (see table below), as compared to an overall PE of the S&P 500 index today of about 14x.

Source: Wall Street Journal – March 14, 2000

The Next Bubble

What is/are the next investment bubble(s)? Nobody knows for sure, but readers of Investing Caffeine know that long-term bonds are one fertile area. Given the generational low in yields and rates, and the 35-year bull run in bond prices, it can be difficult to justify heavy allocations of inflation losing bonds for long time-horizon investors. Commercial real estate and Silicon Valley unicorns could be other potential over-heated areas. However, as we discussed earlier, identifying and timing bubble bursts is extremely challenging. Nevertheless, the great thing about long-term investing is that probabilities and valuations ultimately do matter, and therefore a diversified portfolio skewed away from extreme valuations and speculative sectors will pay handsome dividends over the long-run.

Many traders continue to daydream as they chase performance through speculative investment bubbles, looking to squeeze the last ounce of an easily identifiable trend. As the lead investment manager at Sidoxia Capital Management, I spend less time sucking the last puff out of a cigarette, and spend more time opportunistically devoting resources to valuation-sensitive growth trends. As demonstrated with historical examples, following the popular trend du jour eventually leads to financial ruin and nightmares. Avoiding bubbles and pursuing fairly priced growth prospects is the way to achieve investment prosperity…and provide sweet dreams.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), MCD, DIS and are short TLT, but at the time of publishing SCM had no direct positions in AVP, XRX, IBM,or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

When Genius Failed

It has been a busy year between work, play, family, and of course the recent elections. My work responsibilities contain a wide-ranging number of facets, but in addition to research, client meetings, conference calls, conferences, trading, and other activities, I also attempt to squeeze in some leisure reading as well. While it’s sad but true that I find pleasure in reading SEC documents (10Ks and 10Qs), press releases, transcripts, corporate presentations, financial periodicals, and blogs, I finally did manage to also scratch When Genius Failed by Roger Lowenstein from my financial reading bucket list.

When Genius Failed chronicles the rise and fall of what was considered the best and largest global hedge fund, Long Term Capital Management (LTCM). The irony behind the collapse makes the story especially intriguing. Despite melding the brightest minds in finance, including two Nobel Prize winners, Robert Merton and Myron Scholes, the Greenwich, Connecticut hedge fund that started with $1.3 billion in early 1994 managed to peak at around $140 billion before eventually crumbling to ruin.

With the help of confidential internal memos, interviews with former partners and employees of LTCM, discussions with the Federal Reserve, and consultations with the six major banks involved in the rescue, Lowenstein provides the reader with a unique fly-on-the-wall perspective to this grand financial crisis.

There have certainly been plenty of well-written books recounting the 2008-2009 financial crisis (see my review on Too Big to Fail), but the sheer volume has burnt me out on the subject. With that in mind, I decided to go back in time to the period of 1993 – 1998, a point at the beginning of my professional career. Until LTCM’s walls began figuratively caving in and global markets declined by more than $1 trillion in value, LTCM was successful at maintaining a relatively low profile. The vast majority of Americans (99%) had never heard of the small group of bright individuals who started LTCM, until the fund’s ultimate collapse blanketed every newspaper headline and media outlet.

Key Characters

Meriwether: John W. Meriwether was a legendary trader at Salomon Brothers, where he started the Arbitrage Group in 1977 and built up a successful team during the 1980s. His illustrious career is profiled in Michael Lewis’s famed book, Liar’s Poker. Meriwether built his trading philosophy upon the idea that mispricings would eventually revert back to the mean or converge, and therefore shrewd opportunistic trading will result in gains, if patience is used. Another name for this strategy is called “arbitrage”. In sports terms, the traders of the LTCM fund were looking for inaccurate point spreads, which could then be exploited for profit opportunity. Prior to the launch of LTCM, in 1991 Meriwether was embroiled in the middle of a U.S. Treasury bid-rigging scheme when one of his traders Paul Mozer admitted to submitting false bids to gain unauthorized advantages in government-bond auctions. John Gutfreund, Salomon Brothers’ CEO was eventually forced to quit, and Salomon’s largest, famed shareholder Warren Buffett became interim CEO. Meriwether was slapped on the wrist with a suspension and fine, and although Buffett eventually took back Meriwether in a demoted role, ultimately the trader was viewed as tainted goods so he left to start LTCM in 1993.

LTCM Team: During 1993 Meriwether built his professional team at LTCM and he began this process by recruiting several key Salomon Brothers bond traders. Larry Hilibrand and Victor Haghani were two of the central players at the firm. Other important principals included Eric Rosenfeld, William Krasker, Greg Hawkins, Dick Leahy, Robert Shustak, James McEntee, and David W. Mullins Jr.

Nobel Prize Winners (Merton & Scholes): While Robert C. Merton was teaching at Harvard University and Myron S. Scholes at Stanford University, they decided to put their academic theory to the real-world test by instituting their financial equations with the other investing veterans at LTCM. Scholes and Merton were effectively godfathers of quantitative theory. If there ever were a Financial Engineering Hall of Fame, Merton and Scholes would be initial inductees. Author Lowenstein described the situation by saying, “Long-Term had the equivalent of Michael Jordan and Muhammad Ali on the same team.” Paradoxically, in 1997, right before the collapse of LTCM, Merton and Scholes would become Nobel Prize laureates in Economic Sciences for their work in developing the theory of how to price options.

The History:

Founded in 1993, Long-Term Management Capital was hailed as the most impressive hedge fund created in history. Near its peak, LTCM managed money for about 100 investors and employed 200 employees. LTCM’s primary strategy was to identify mispriced bonds and profit from a mean reversion strategy. In other words, as long as the overall security mispricings narrowed, rather than widened, then LTCM would stand to profit handsomely.

On an individual trade basis, profits from LTCM’s trades were relatively small, but the fund implemented thousands of trades and used vast amounts of leverage (borrowings) to expand the overall profits of the fund. Lowenstein ascribed the fund’s success to the following process:

“Leveraging its tiny margins like a high-volume grocer, sucking up nickel after nickel and multiplying the process a thousand times.”

Although LTCM implemented this strategy successfully in the early years of the fund, this premise finally collapsed like a house of falling cards in 1998. As is generally the case, hedge funds and other banking competitors came to understand and copy LTCM’s successful trading strategies. Towards the end of the fund’s life, Meriwether and the other fund partners were forced to experiment with less familiar strategies like merger arbitrage, pair trades, emerging markets, and equity investing. This diversification strategy was well intentioned, however by venturing into uncharted waters, the traders were taking on excessive risk (i.e., they were increasing the probability of permanent capital losses).

The Timeline

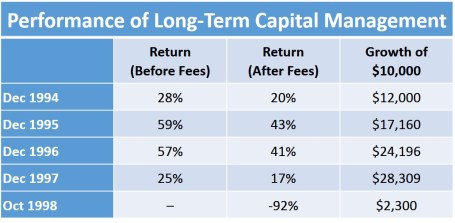

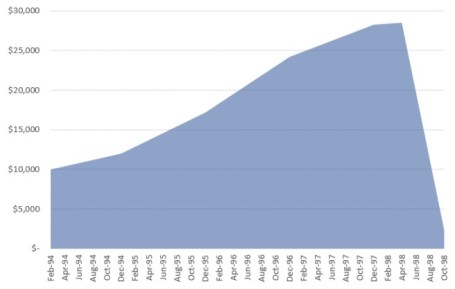

- 1994 (28% return, 20% after fees): After attempting to raise capital funding in 1993, LTCM opened its doors for business in February 1994 with $1.25 billion in equity. Financial markets were notably volatile during 1994 in part due to Federal Reserve Chairman Alan Greenspan leading the first interest rate hike in five years. The instability caused famed fund managers Michael Steinhardt and George Soros to lose -$800 million and $650 million, respectively, all within a timespan of less than a week. The so-called “Mexican Tequila Crisis” that occurred at the end of the year also resulted in a devaluation of the Mexican peso and crumbling of the Mexican stock market.

- 1995 (59% return, 43% after fees): By the end of 1995, the fund had tripled its equity capital and total assets had grown to $102 billion. Total leverage, or the ratio of debt to equity, stood around 28 to 1. LTCM’s derivative contract portfolio was like a powder keg, covering positions worth approximately $650 billion.

- 1996 (57% return, 41% after fees): By the spring of 1996, the fund was holding $140 billion in assets, making it two and a half times as big as Fidelity Magellan, the largest mutual fund on the planet. The fund also carried derivatives valued at more than $1 trillion, all financed off a relatively smaller $4 billion equity base. Investors were loving the returns and financial institutions were clamoring to gain some of LTCM’s business. During this period, as many as 55 banks were providing LTCM financing. The mega-returns earned in 1996 came in large part due to profitable leveraged spread trades on Japanese convertible bonds, Italian bonds, junk bonds, and interest rate swaps. Total profits for the year reached an extraordinary level of around $2.1 billion. To put that number in perspective, that figure was more money generated than the profits earned by McDonalds, Disney, American Express, Nike, Xerox, and many more Fortune 500 companies.

- 1997 (25% return, 17% after fees): The Asia Crisis came into full focus during October 1997. Thailand’s baht currency fell by -20% after the government decided to let the currency float freely. Currency weakness then spread to the Philippines, Malaysia, South Korea, and Singapore. As Russian bond spreads (prices) began to widen, massive trading losses for LTCM were beginning to compound. Returns remained positive for the year and the fund grew its equity capital to $5 billion. As the losses were mounting and the writing on the wall was revealing itself, professors Merton and Scholes were recognized with their Nobel Prize announcement. Ironically, LTCM was in the process of losing control. LTCM’s bloated number of 7,600 positions wasn’t making the fund any easier to manage. During 1997, the partners realized the fund’s foundation was shaky, so they returned $2.7 billion in capital to investors. Unfortunately, the risk profile of the fund worsened – not improved. More specifically, the fund’s leverage ratio skyrocketed from 18:1 to 28:1.

- 1998 (-92% return – loss): The Asian Crisis losses from the previous year began to bleed into added losses in 1998. In fact, losses during May and June alone ended up reducing LTCM’s capital by $461 million. As the losses racked up, LTCM was left in the unenviable position of unwinding a mind-boggling 60,000 individual positions. It goes almost without saying that selling is extraordinarily difficult during a panic. As Lowenstein put it, “Wall Street traders were running from Long-Term’s trades like rats from a sinking ship.” A few months later in September, LTCM’s capital shrunk to less than $1 billion, meaning about $100 billion in debt (leverage ratio greater than 100:1) was supporting the more than $100 billion in LTCM assets. It was just weeks later the fund collapsed abruptly. Russia defaulted on its ruble debt, and the collapsing currency contagion spread to global markets outside Russia, including Eastern Asia, and South America.

The End of LTCM

On September 23, 1998, after failed investment attempts by Warren Buffett and others to inject capital into LTCM, the heads of Bankers Trust, Bear Stearns, Chase Manhattan, Goldman Sachs, J.P. Morgan, Lehman Brothers, Merrill Lynch, Morgan Stanley Dean Witter, and Salomon Brothers all gathered at the Federal Reserve Bank of New York in the heart of Wall Street. Presiding over this historical get-together was Fed President, William J. McDonough. International markets were grinding to a halt during this period and the Fed was running out of time before an all-out meltdown was potentially about to occur. Ultimately, McDonough was able to get 14 banks to wire $3.65 billion in bailout funds to LTCM. While all LTCM partners were financially wiped out completely, initial investors managed to recoup a small portion of their original investment (23 cents on the dollar after factoring in fees), even though the tally of total losses reached approximately $4.6 billion. Once the bailout was complete, it took a few years for the fund to liquidate its gargantuan number of positions and for the banks to get their multi-billion dollar bailout paid back in full.

- 1999 – 2009 (Epilogue): Meriwether didn’t waste much time moping around after the LTCM collapse, so he started a new hedge fund, JWM Partners, with $250 million in seed capital primarily from legacy LTCM investors. Regrettably, the fund was hit with significant losses during the 2008-2009 Financial Crisis and was subsequently forced to close its doors in July 2009.

Source: The Personal Finance Engineer

Source: The Personal Finance Engineer

Lessons Learned:

- The Risks of Excessive Leverage: Although the fund grew to peak value of approximately $140 billion in assets, most of this growth was achieved with added debt. When all was said and done, LTCM borrowed more than 30 times the value of its equity. As Lowenstein put it, LTCM was “adding leverage to leverage, as if coating a flammable tinderbox with kerosene.” In home purchase terms, if LTCM wanted to buy a house using the same amount of debt as their fund, they would lose all of their investment, if the house value declined a mere 3-4%. The benefit of leverage is it multiplies gains. The downside to leverage is that it also multiplies losses. If you carry too much leverage in a declining market, the chance of bankruptcy rises…as the partners and investors of LTCM learned all too well. Adding fuel to the LTCM flames were the thousands of derivative contracts, valued at more than $1 trillion. Warren Buffett calls derivatives: “Weapons of Mass Destruction.”

- Past is Not Always Prologue for the Future: Just because a strategy works now or in the past, does not mean that same strategy will work in the future. As it relates to LTCM, Nobel Prize winning economist Merton Miller stated, “In a strict sense, there wasn’t any risk – if the world had behaved as it did in the past.” LTCM’s models worked for a while, then failed miserably. There is no Holy Grail investment strategy that works always. If an investment strategy sounds too good to be true, then it probably is too good to be true.

- Winning Strategies Eventually Get Competed Away: The spreads that LTCM looked to exploit became narrower over time. As the fund achieved significant excess returns, competitors copied the strategies. As spreads began to tighten even further, the only way LTCM could maintain their profits was by adding additional leverage (i.e., debt). High-frequency trading (HFT) is a modern example of this phenomenon, in which early players exploited a new technology-driven strategy, until copycats joined the fray to minimize the appeal by squeezing the pool of exploitable profits.

- Academics are Not Practitioners: Theory does not always translate into reality, and academics rarely perform as well as professional practitioners. Merton and Scholes figured this out the hard way. As Merton admitted after winning the Nobel Prize, “It’s a wrong perception to believe that you can eliminate risk just because you can measure it.”

- Size Matters: As new investors poured massive amounts of capital into the fund, the job of generating excess returns for LTCM managers became that much more difficult. I appreciate this lesson firsthand, given my professional experience in managing a $20 billion fund (see also Managing $20 Billion). Managing a massive fund is like maneuvering a supertanker – the larger a fund gets, the more difficult it becomes to react and anticipate market changes.

- Stick to Your Knitting: Because competitors caught onto their strategies, LTCM felt compelled to branch out. Meriwether and LTCM had an edge trading bonds but not in stocks. In the later innings of LTCM’s game, the firm became a big player in stocks. Not only did the firm place huge bets on merger arbitrage, but LTCM dabbled significantly in various long-short pair trades, including a $2.3 billion pair trade bet on Royal Dutch and Shell. Often the firm used derivative securities called equity swaps to make these trades without having to put up any significant capital. As LTCM experimented in the new world of equities, the firm was obviously playing in an area in which it had absolutely no expertise.

As philosopher George Santayana states, “Those who fail to learn from history are doomed to repeat it.” For those who take investing seriously, When Genius Failed is an important cautionary tale that provides many important lessons about financial markets and highlights the dangers of excessive leverage. You may not be a genius Nobel Prize winner in economics, but learning from Long-Term Capital Management’s failings will place you firmly on the path to becoming an investing genius.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), DIS, JPM, and MCD, but at the time of publishing had no direct position in AXP, NKE, XRX, RD, GS, MS, Shell, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page

Trump: Bark Worse Than the Bite?

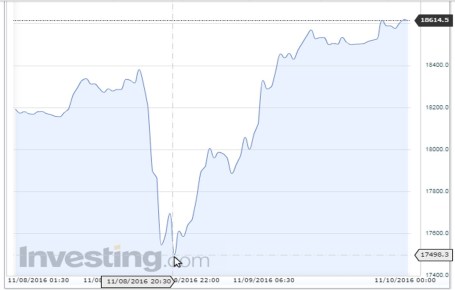

Unless you have been living in a cave this week, you are probably aware the country has elected a new president. Leading up to Election Day, the anxiety was palpable. A populist wave, much like the one experienced in the British Brexit vote earlier this year, resulted in economically disenfranchised voters coming out in full force to vote out the perceived establishment candidate, Hillary Clinton. Financial market pundits and media commentators predicted an immediate 11-13% decline in stock values if Donald Trump were to win. Could they have been more wrong? After a brief -5% decline in pre-trading Dow Jones Industrial Average future prices, the Dow subsequently skyrocketed more than 1,000 points higher to finish up +1.4% for the day (see chart below). For the week, the Dow amazingly rallied by +5.4%.

Source: Investing.com

As I have written on numerous occasions, politics have very little impact on the long-term direction of the financial markets. Yes, it is true that regulations and policies implemented by the president and Congress can influence specific industries or individual companies over the short-run. Hillary Clinton proved this assertion with her pharmaceutical industry tweet, which created a lasting hangover effect on the sector. But guess what? Regulations and politics have always changed throughout our country’s history, with various shifting policies impacting businesses asymmetrically – some positively and some negatively. The good news…in an ever-expanding global economy, accelerated through technology, capitalism forces businesses to adapt to political change.

Considering the amount of our nation’s political variation, what has been our country’s stock market and economic track record over the last 100 years under 17 different presidents (8 Democrats and 9 Republicans)? See chart below:

Source: Macrotrends

Not too shabby judging by the roughly 188x–fold increase in the Dow Jones Industrial Average (or > ~18,700%+ return) to a fresh all-time record high this week. While I am admittedly nervous about a full, Republican tri-power Trump administration (President/House/Senate), the reality is that Trump’s unconventional, unprecedented platform doesn’t fit squarely into the traditional Republican policy boxes. In fact, he has switched his party affiliation five times. President-elect Trump will therefore need to reach across the political aisle to Democrats, and work with Speaker of the House Paul Ryan to accomplish the platform agenda priorities he outlined during his presidential campaign.

While all this political election discussion has been stimulating and exhausting, fortunately, followers of my Investing Caffeine blog understand there are much more important factors than politics affecting the performance of the stock market and economy – namely corporate profits, interest rates, valuations, and sentiment (see Don’t Be a Fool, Follow the Stool).

As mentioned, the market’s returns are influenced by four key factors, but sentiment and stock market values are largely shaped by investor behavior. Trump has less control on investor behavior, but his policies can directly impact corporate profits and interest rates – two critical components of economic health. Part of the reason Trump won the election was due to campaign promises regarding many popular stimulative policies, including personal and corporate tax cuts; infrastructure spending; repatriation of foreign money; tax simplification and reform; Obamacare improvement; and immigration reform.

As it turns out, a good number of the issues relating to these policies happen to be bipartisan in nature. Given the Republican-controlled Congress, investors are perceiving these potential policy changes as positive for the market – at least for the first week of his presidential tenure.

For now, President-elect Trump has struck the proper conciliatory tone and made appropriate comments. In the coming days and weeks, investors are watching closely for tangible evidence and clues of his policy priorities, as he fills key political posts on his presidential team. Time will tell whether the early honeymoon will continue past Trump’s inauguration day, but currently, the consensus is his bark heard during Trump’s heated 18-month presidential campaign is worse than the actual bite of his election victory.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page

Uncertainty: A Love-Hate Relationship

An often over-quoted saying is “The stock market hates uncertainty.” However, the wealthiest investor of all-time has a different perspective about uncertainty:

“The future is never clear. You pay a very high price in the stock market for a cheery consensus. Uncertainty is the friend of the buyer of long-term values.”

-Warren Buffett

Buffett understands the benefits of long-term compounding and the beauty of buying fear and selling greed. Unfortunately, CNBC and every other media outlet do not carry the words “long-term” in their vernacular. Peddling F.U.D. (fear, uncertainty, doubt) equates to eyeballs and clicks, which equates to more advertising dollars. With the volatility index trading at fear-rich Brexit levels above 20, traders are certainly long on F.U.D. Time will tell whether the elections will increase or decrease F.U.D., but unless there is a contested election a la 2000 (Bush-Gore), there will be one less election to worry about and investors can then go back to normal worrying and political bashing.

As I have noted on multiple occasions, from a stock market standpoint, whomever wins (Republican or Democrat) should have no bearing on the performance of the stock market over the medium term as long as there remains gridlock in Washington (see also Fall is Here: Change is Near). Most Americans despise political inactivity, but if like many investors you believe in fiscal discipline, then you prefer fighting over spending, and generally, the more gridlock, the less spending.

In other words, fiscal discipline is likely to win IF there is a split Congress (House & Senate) or if the winning presidential party loses both the Senate and the House. For what it’s worth, Nate Silver, the guy who accurately predicted all 50 states in the 2012 presidential election is currently predicting gridlock (i.e., a split Congress), but the presidential and Congressional polls have been generally tightening across the board. For now, with just three days left before the election, investors have chosen to shoot now, and ask questions later, as evidenced by the 420 point decline in the Dow Jones Industrial Average during the first half of the 4th quarter.

My crystal ball is just as foggy as anybody else’s, and increased volatility in the short-run should come as no surprise to anyone. As in any volatile investment environment, during periods of turbulence, you should compile your shopping list to opportunistically purchase securities selling at a discount. There is no reason to be a hero, but you should prudently deploy cash or readjust your asset allocation, if there is a significant sell-off in risky assets. The same principle works in reverse. If for some unlikely reason, there is a post Brexit-like snapback, one should consider trimming or selling overbought positions.

The main point in periods like these is to let objective reasoning drive your decisions (or lack of decisions), rather than emotions. There has always been a love-hate relationship with uncertainty for traders and investors alike. If you are doing your job correctly, long-term investors should relish F.U.D. because as the saying goes, “This too shall pass.”

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page

What Do You Worry About Next?

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (November 1, 2016). Subscribe on the right side of the page for the complete text.

Boo! Halloween has just passed and frightened investors have still survived to tell the tale in 2016. While most people have gotten spooked by the presidential election, other factors like record-high corporate profits, record-low interest rates, and reasonable valuations have led to annual stock market gains. More specifically, values have risen in 2016 by approximately +4% (or +6% including dividend payments). Despite last week’s accelerating 3rd quarter GDP economic growth figure of +2.9%, which was the highest rate in two years and more than doubled the rate of the previous quarter (up +1.4%), there were still more tricks than treats during October. Recently, scary politics have shocked many Halloween participants into a zombie-like state, as evidenced by stock values declining around -1.7% during October.

This recent volatility is nothing new. Even though financial markets are significantly higher in recent years, that has not prevented repeated corrections over the year(s) as shown below in the 2009 – 2015 chart.

In order to earn higher long-term returns, investors have to accept a certain amount of short-term price movements (upwards and downwards). With a couple months remaining in the year, stock investors have achieved gains through a tremendous amount of economic and geopolitical uncertainty, including the following scares:

- China: A significant fallout from a Chinese slowdown at the beginning of the year (stocks fell about -14%).

- Brexit: A 48-hour Brexit vote scare in June (stocks fell -6%).

- Fed Fears: Threatening comments in September from the Federal Reserve about potentially hiking increasing interest rates (stocks fell -4%).

With the elections just a week away, political anxiety has jolted Americans’ adrenaline levels. The polls continue to move up and down, but as I have repeatedly pointed out, the only certain winner in Washington DC is gridlock. Sure, in a Utopian world, politicians should join hands and compromise to solve all our country’s serious problems. Unfortunately, this is not the case (see Congress’s approval rating). However, there is a silver lining to this dysfunction…gridlock can lead to fiscal discipline.

Our country’s debt/deficit financial situation has been spiraling out of control, in large measure due to rapidly rising entitlement spending, including Medicare, and Social Security. Witnessing all the political rhetoric and in-fighting is very difficult, but as I highlighted in last month’s newsletter, gridlock has flattened the spending curve significantly since 2009 – a positive development.

And although the economic recovery has been one of the slowest since World War II and global growth remains anemic, the U.S. remains a better house in a bad global neighborhood (e.g., Europe and Japan continue to suck wind), as evidenced by a number of these following positive economic indicators:

- Employment Improvement: Unemployment has fallen from 10% to 5% since 2009, and more than 15 million jobs have been added over that period.

- Housing Recovery Continues: Home sales and prices continue their multi-year rise; housing inventories remain tight; and affordability remains strong, given generationally low interest rates.

- Record Auto Sales: Car sales remain near record levels, hovering around 17 million units per year.

- Consumer Confidence on the Rise: Ever since the financial crisis, consumer sentiment figures have rebounded by about 50%.

-

Record Consumer Sales: Consumer spending accounts for approximately 70% of our economy, and as you can see from the chart below, despite consumers saving more, stronger employment and wages are fueling more spending.

Source:Calculated Risk

Source:Calculated Risk

Absent a clean sweep of control by the Democrat or Republican Presidential-Congressional candidates, our democratic system will retain its healthy status of checks and balances. Based on all the current polling data, a split between the White House, Senate, and House of Representatives remains a very high likelihood scenario.

The political process has been especially exhausting during the current cycle, but regardless of whether your candidate wins or loses, much of the current uncertainty will likely dissipate. As the saying goes, at least it is “Better the devil you know than the devil you don’t know.”

After the November 8th elections are completed, there will be one less election to worry about. Thankfully, after 25 years in the industry, I’m not naïve enough to believe there will be nothing else to worry about. When the financial media and blogosphere get bored, at a minimum, you can guarantee yourself plenty of useless coverage regarding the next monetary policy move by the Federal Reserve (see also Fed Fatigue).

Whatever the next set of worries become, U.K. Prime Minister Winston Churchill said it best as it relates to American politics and economics, “You can always count on Americans to do the right thing – after they’ve tried everything else.” If Churchill’s words don’t provide comfort and you had fun getting spooked over the elections on Halloween, feel free to keep wearing your costume. Behind any constructive economic data, the prolific media machine will continue doing their best in manufacturing plenty of fear, uncertainty, and doubt to keep you worried.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}