Posts tagged ‘healthcare’

Can You Retire? Getting to Your Number

What’s “your number?” The catchy phrase has been tried on 30-second television commercials before, but the fact remains, most Americans have no clue how much they need to save for retirement. The ever-shifting and imprecise variables needed to compute the size of your needed nest egg can seem overwhelming: lifespan; career span; inflation; college tuition; healthcare expenses; rising insurance costs; social security; employer benefits; inheritance; child support; parental support; etc. The list goes on and with near-zero interest rates, and stock prices at record highs, the retirement challenge has only gotten riskier and more difficult.

I understand this task may not be easy and could eat into your House of Cards viewing, Candy Crush playing, or football watching. However, if you can spend two weeks planning a family vacation, you certainly can afford devoting a few hours to scribbling down some numbers as it relates to the lifeblood of your financial future. The project is definitely doable.

Here are some key steps to finding “your number.” If you’re not single, then calculate the figures for your household:

1). Calculate Your Budget: Where to start? A good place to begin is with is a boring budget (or your monthly expenses). The budget does not need to be down to the penny, but you should be able to estimate your monthly spend with the help of your bank and credit card statements. Make sure to include estimates for periodic unforeseen potential expenses like annual auto repairs, home repairs, or emergency hospital visits. Once you determine your monthly spend, extrapolating your annual spend shouldn’t be too difficult.

2). Compute Your Income: Your sources of income should be fairly straightforward. For most people this includes your salary and potential bonus. Some people will also generate income from investments, a business, and/or real estate. Before getting too excited about all the income you are raking in, don’t forget to subtract out taxes collected by Uncle Sam, and include a possible scenario of rising tax rates during your working years. Obviously, the economy can also have a positive or negative impact on your income projections, nevertheless, if you conservatively plan for some potential future setbacks, you will be in a much better position in forecasting the amount of savings needed to reach “your number.”

3). Planned Retirement Date: The date you pick may or may not be realistic, but by choosing a specific date, you can now evaluate how much savings will be necessary to reach your required nest egg number. The difference between your annual income (#2) and annual budget (#1) is your annual savings, which you can multiply by the number of years you plan to work until retirement. For example, assume you wanted to retire 15 years from now and were able to save/invest $20,000 each year while earning a 6% annualized return. By the year 2030 these savings would equate to about $465,000 and could be added to any other savings and other retirement income (pension, 401(k), Social Security, inheritance, etc.) to meet your retirement needs.

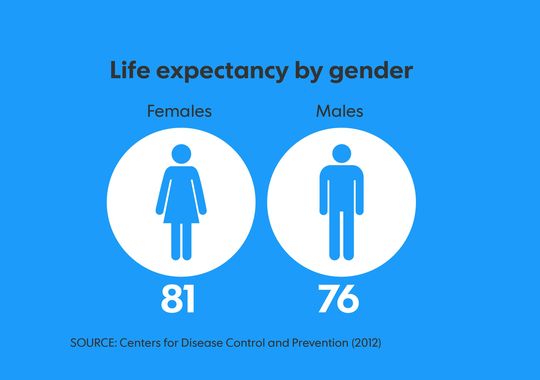

4). Life Expectancy: After you have determined when you want to retire, now comes the tricky part. How long are you going to live? Assuming you are currently healthy, you can use actuarial tables for life expectancy. According to a new report on American mortality from the Centers for Disease Control and Prevention’s National Center for Health Statistics, the average life expectancy is 81 for females and 76 for males (see graphic below). The estimates are a little rosier, if you have lived to age 65, in which case females are expected to live past 85 years old and males to about 83 years. You can adjust these figures higher or lower based on personal information and family history, but if you consider yourself “average,” then you better plan to have at least 15 years of fire power in your savings nest egg (see example at bottom of article).

Source: USA Today

Empty Retirement Wallets & Purses

The harsh realities are Americans are not saving enough. It‘s true, you can survive off a smaller nest egg, if you plan to live off of cat food and vacation in Tijuana, but most Americans and retirees have become accustomed to a higher standard of living. A New York Times article highlighted that 75% percent of Americans nearing retirement age had less than $30,000 in their retirement accounts – that’s not going to buy you that winter home on Maui or leave enough to cover your golf dues at the local country club.

Control the things that make a difference.

- Save. Pay yourself first by tucking money away each month. If you haven’t established an IRA (Individual Retirement Account) or savings account, make sure you contribute to your employer’s matching 401(k) plan to the fullest extent possible, if available. This is free money your employer is offering you and by not participation you are shooting yourself in the foot.

- Spend prudently. Review your monthly / annual budgets and determine where there is room to cut expenses. Every budget has fat in it, so it’s just a matter of cutting excessive and less important items, without sacrificing dramatic changes to your standard of living.

- Manage your career. Invest in yourself with education, apply for that promotion, or look for other employment alternatives if you are unhappy or not being paid your proper value.

- Push Retirement Out: If you are healthy and enjoy your work, extending your working years can have profoundly positive benefits to your retirement. Not only will you have more money saved up for retirement, but you will also receive higher Social Security benefits by delaying retirement (see Social Security benefit estimator).

The bottom-line is if you are like most working Americans, you will need to save more and invest more prudently (e.g., in a low-cost, tax-efficient manner like strategies offered by Sidoxia).

Use Your Thumb to Get Started

Rules of thumb are never perfect, but are not a bad place to start before fine-tuning your estimates. Some retirement pundits begin by using an 80% “income replacement ratio” rule as a retirement guide. In other words, you should not need 100% of your pre-retirement income during retirement because a number of your major living expenses should be reduced. For example, during retirement your tax expenses should decrease (because you are not working); your mortgage payment should be lower (i.e., house is paid off); your kids should be independent and off the family payroll; and you may be in the position to downsize your home (e.g., empty-nesters often decide to move to a lower square footage residence).

Another rule of thumb is the “15x Rule,” which says you will need an investment account equivalent to at least 15-times your pre-retirement income. Therefore, if your after-tax income is $100,000 before retirement and you need to replace $80,000 during retirement (80% replacement ratio), this means you actually only need to replace about $60,000 per year. We arrive at the lower $60,000 figure by further assuming the $80,000 can be reduced by about $20,000 flowing in annually from Social Security. Through the mighty powers of division, we can then apply the 4% Sustainable Withdrawal Rate rule (SWR) to reverse engineer the estimate of “our number.” In this example, our ultimate nest egg needed is $1,500,000 (equal to $60,000 / 4% or $60,000 x 25 years), which is estimated to last for 25 years of retirement. As you can see, there are quite a few assumptions baked into this scenario, including a retirement investment portfolio that beats inflation by 4%, but nevertheless this line of thinking creates an understandable framework to operate under.

Of course, for all the non-math Investing Caffeine readers, life could have been made easier by simply multiplying the $100,000 pre-retirement income by 15x to arrive at our $1.5 million nest egg. More elegant, but less fun for this nerdy math author.

We’ve covered a lot of ground, but I’m absolutely confident if you have read this far, you can definitely come up with “your number.” If this all seems too overwhelming, there is no need to worry, just find an experienced investment advisor or financial planner…I’m sure I could help you find one 🙂 .

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Digesting the Anchovy Pizza Market

Source: Photobucket

Article is an excerpt from previously released Sidoxia Capital Management’s complementary July 2012 newsletter. Subscribe on right side of page.

I love pizza, and most fellow connoisseurs have difficulty refusing a hot, fresh slice of heaven too. Pizza is so universally appreciated that people consider pizza like ice cream – it’s good even when it’s bad (I agree). However, even the biggest, diehard pizza-lover will sheepishly admit their fondness for the flat and circular cheesy delight changes when you integrate anchovies into the mix. Not many people enjoy salty, slimy, marine creatures layered onto their doughy mozzarella and marinara pizza paradise.

With all the turmoil and uncertainty going on in the global financial markets, prudently investing in a widely diversified portfolio, including a broad range of equity securities, is viewed as palatable as participating in an all-you-can-eat anchovy pizza contest. Why are investors’ appetites so salty now? Hmmm, let me think. Oh yes, here are a few things that come to mind:

- Presidential Election Uncertainty

- European Financial Crisis

- Impending Fiscal Cliff (tax cut expirations, automatic spending cuts, termination of stimulus, etc.)

- Unsustainable Fiscal Debt & Deficits

- Slowing Subpar Domestic Economic Growth

- Partisan Politics and Gridlock in Washington

- High Unemployment

- Fears of a Hard Economic Landing in China

Doesn’t sound too appealing, does it? So, what are most investors doing in this unclear market? Rather than feasting on a pungent pie of anchovies, investors are flocking to the perceived safety of low yielding asset classes, no matter the price. In other words, the short-term warmth and comfort of CDs, money market, checking, and fixed income assets are being gobbled up like nicotine-laced pepperoni pizzas selling for $29.95/each + tax. The anchovy alternative, like stocks, is much more attractively priced now. After accounting for dividends, earnings, and cash flows, the anchovy/stock option is currently offering a 2-for-1 special with breadsticks and a salad…quite the bargain!

Nonetheless, the plain and expensive pepperoni/bond option remains the choice du jour and there are no immediate signs of a pepperoni hangover just quite yet. However, this risk aversion addiction cannot last forever. The bond gorging buffet has gone on relatively unabated for the last three decades, as you can see from the chart below. In spite of this, the bond binging game is quickly approaching a mathematical terminal end-game, as interest rates cannot logically go below zero.

Source: Calafia Beach Pundit with Sidoxia comments

Since my firm (Sidoxia Capital Management) is based in Newport Beach, next to PIMCO’s global headquarters, we get to follow the progression of the bond binging game firsthand. I’ve personally learned that if I manage close to $2 trillion in assets under management, I too can construct a 23-story Taj Mahal-esque headquarters that overlooks the Pacific Ocean from a stones-throw away.

Beyond glorified headquarters, there is evidence of other low-risk appetite examples. Here are some reinforcing pictures:

The Bond Binge

Source (The Financial Times): Bond purchases have exploded in the last three years.

Cash Hoarding

Source (Calafia Beach Pundit): Stuffing money under the mattress has accelerated in recent years as fear, uncertainty, and doubt have reigned supreme.

The Anchovy Special

Even though anchovy pizza, or a broadly diversified portfolio across asset class, size, geography, and style may not sound appealing, there are plenty of reasons to fight the urges of caving to fear and skepticism. Here are a few:

1) Growth Rolls On: Despite the aforementioned challenges occurring domestically and abroad, growth has continued unabated for 11 consecutive quarters, albeit at a rate less than desired. We are not immune to global recessionary forces, but regardless of European forces, the U.S. has been resilient in its expansion.

Source: Calafia Beach Pundit

2) Jobs and Housing on the Upswing: Unemployment remains high, but our country has experienced 27 consecutive months of private creation, leading to more than 4 million new jobs being added to our workforce. As you can see from the clear longer-term downward trend in unemployment claims, we are moving in the right direction.

Source: Calafia Beach Pundit

3) Eurozone Slowly Healing its Wounds: The Greek political and fiscal soap opera is grabbing all the headlines, but quietly in the background there are signs that the eurozone is slowly healing the wounds of the financial crisis. If you look at the 2-year borrowing costs of Europe’s troubled countries (ex-Greece), there is an unambiguous and beneficial decline. There is no doubt that Spain and Italy play a larger role than Portugal and Ireland, but at least some seeds of change have been planted for optimism.

Source: Calafia Beach Pundit

4) Record Corporate Profits: Investors are not the only people reading uncertain newspaper headlines and watching CNBC business television. CEOs are reading the same gloomy sensationalistic stories, and as a result, corporations have been cautious about dipping their short arms into their deep pockets. Significant expense reductions and a reluctance to hire have led to record profits and cash hoards. As evidenced by the chart below, profits continue to rise, and these earnings are being applied to shareholder friendly uses like dividends, share buybacks, and accretive acquisitions.

Source: Yardeni.com

5) Attractive Valuations (Pricing): We have already explored the lofty prices surrounding bonds and $30 pepperoni pizzas, but counter-intuitively, stock prices are trading at a discount to historical norms, despite record low interest rates. All else equal, an investor should pay higher prices for stocks when interest rates are at a record low (and vice versa), but currently we are seeing the opposite dynamic occur.

Source: Calafia Beach Pundit

Even though the financial markets may look, smell, and taste like an anchovy pizza, the price, value, and return benefits may outweigh the fishy odor. And guess what…anchovies are versatile. If you don’t like them on your pizza, you can always take them off and put them on your Caesar salad or use them for bait the next time you go fishing. The gloom-filled headlines haven’t been spectacular, but if they were, the return opportunities would be drastically reduced. Therefore you are much better off by following investor legend Warren Buffett’s advice, which is to “buy fear and sell greed.”

Investing has never been more difficult with record low interest rates, and it has also never been more important. Excluding a small minority of late retirees and wealthy individuals, efficiently investing your retirement dollars has become even more critical. The safety nets of Social Security and Medicare are likely to be crippled, which will require better and more prudent investing by individuals. Inflation relating to food, energy, healthcare, gasoline, and entertainment is dramatically eroding peoples’ nest eggs.

Digesting a pepperoni pizza may sound like the most popular and best option given the gloomy headlines and uncertain outlook, but if you do not want financial heartburn you may consider alternative choices. Like the healthier and less loved anchovy pizza, a more attractively valued strategy based on a broadly diversified portfolio across asset class, size, geography, and style may be the best financial choice to satiate your long-term financial goals.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Ration or Tax: Eating Cake Not an Option

We live in an instant gratification society that would like everything for free ( like my pal Bill Maher), which explains why we want to have our healthcare cake and eat it too. I think George Will said it best when discussing universal healthcare coverage, “If you think health care is expensive now, just wait until it is free.” Look, I love free stuff too, like the rest of us, whether it’s free sausage sample at Costco (COST) or a breath mint at the Olive Garden (DRI). But regrettably, exploding deficits come at a price.

With midterm elections coming up, the issue of healthcare is once again front and center. The majority party feels like a checkbook is a solution to healthcare prosperity. Can you really look me in the eyes and say covering additional 32 million uninsured Americans is going to save us money. The government hasn’t exactly built a ton of credibility with the disastrous train-wreck we call Medicare, which is already carrying 45 million covered passengers.

The minority party hasn’t done a lot better with the layering of the 2006 unsustainable Medicare Part D drug plan. Conservatives are campaigning on “repeal and replace” and that is great, but where are the cuts?

There are only two solutions to our current healthcare problem: ration or tax (read Plucking Feathers of Taxpaying Geese). Is healthcare a right or privilege? I don’t know, but if we want to cover current obligations, or add 32 – 50 million more uninsured, then we will be required to cut expenses (ration) to pay for increased benefits and/or increase taxes to cover additional benefits. I would love to cover all Americans, along with the starving children in Africa too, but unfortunately we are limited by our resources. Writing checks with borrowed money will only last for so long.

How severe are the exploding healthcare costs, which are covering the graying of the 76 million baby boomers? Here’s how Forbes describes the unsustainable Medicare obligations:

The Medicare Trustees tell us that Medicare’s expected future obligations exceeded premiums and dedicated taxes by $89 trillion (measured in current dollars). No, that’s not a misprint. To put that number in perspective, Medicare’s liability is about 5 1/2 times the size of Social Security’s ($18 trillion) and about six times the size of the entire U.S. economy.

Not a pretty picture. These estimates look pretty far in the future, but even more bare bone figures arrive at a still frightening $33 trillion. Take a look at healthcare spending forecasts as a percentage of GDP – even the lowest estimates are depressing:

Source: National Center for Policy Analysis via Forbes

In our increasingly flat globalized world, competition between countries is becoming even more intense. We are in a marathon race for improved standards of living, and all these debts and deficits are dragging us down like an anchor tied to our legs. Even without considering other massive entitlements like Social Security, healthcare alone has the potential of grinding our economy to a halt. Politicians are great at promising more benefits and tax cuts in exchange for your votes, but true leadership requires delivering the sour medicine necessary for future prosperity. Before we eat the healthcare cake, let’s raise the money to buy the cake first.

Read more about the Medicare Explosion on Forbes

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in COST, DRI, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Debt Control: Turn Off Costly Sprinklers When Raining

By living in Southern California, I am acutely aware of the water shortage issues we face in this region of the country. We all have our pet peeves, and one that eats at me repeatedly occurs when I drive by a neighbor’s house and notice they are blasting the sprinklers in the pouring rain. I get the same sensation when I read about out-of control government spending confronting our current and future generations in light of the massive debt loads we presently carry.

I, like most people, love free stuff, whether it comes in the form of tooth-pick skewered, teriyaki meatball samples at Costco Wholesale Corp. (COST), or free government education from our school systems. But in times of torrential downpours, at a minimum, we need to be a little more cost conscious of our surroundings and turn off the spending sprinklers.

Certainly, when it comes to government spending, there’s no getting around the entitlement elephant in the room, which accounts for the majority of our non-discretionary government spending (see D-E-B-T: New Four Letter Word article). Unfortunately, layering on new entitlements on top of already unsustainable promises is not aiding our cause. For example, showering our Americans with free drugs as part of Medicare Part D program, and paying for tens of millions into a fantasy-based universal healthcare package (purported to save money…good luck) only serves to fatten up the elephant squeezed into our room.

Reform is absolutely necessary and affordable healthcare should be made available to all, but it is important to cut spending first. Then, subsequently, we will be in a better position to serve the needy with the associated savings. Instead, what we chose appears to have been a jamming of a massive, complex, divisive bill through Congress.

Slome’s Spending Rules

In an effort to guide ourselves back onto a path of sensibility, I urge our government legislators to follow these basic rules as a first step:

Rule #1 – Don’t Pay Dead People: I know we have an innate maternal/paternal instinct to help out others, but perhaps our government could stop doling out taxpayer dollars to buried individuals underground or those people incarcerated in jail? Over the last three years the government sent $180 million in benefit checks to 20,000 corpses, and also delivered $230 million to 14,000 convicted felons (read more).

Rule #2 – Pay for Our Own First: Before we start spending money on others outside our borders, I propose we tend to our flock first. For starters, our immigration policies are a disaster. As I wrote earlier (read Our Nation’s Keys to Success), I am a big proponent of legal immigration for productive, higher-educated individuals – not elitist, just practical. If you don’t believe me, just count the jobs created by the braniac immigrant founders at the likes of Google Inc. (GOOG), Intel Corp. (INTC), and Yahoo! Inc. (YHOO). These are the people who will create jobs and out-battle scrappy, resourceful international competitors that want to steal our jobs and our economic leadership position in the world. What I don’t support is illegal immigration – paying for the healthcare and education of foreign criminals with our country’s maxed-out credit cards. This is the equivalent of someone breaking into my house, and me making their bed and feeding them breakfast…ridiculous. I do not support the immigration law passed in Arizona, but this unfortunate chain of events thankfully puts a spotlight on the issue.

Rule #2a. – Stop Being the Globe’s Free Police: If we are going to comb the caves of Tora Bora as part of funding two wars and chasing terrorists all over the world, then we not only should be spending our defense budget more efficiently (non-Cold War mentality), but also charging freeloaders for our services (directly or indirectly). We are spending a whopping 20 cents of each federal tax dollar on defense, so let’s spend it wisely and charge those outside our borders benefiting from our monetary and physical sacrifices. And, oh by the way, sending $400 million to the territory controlled by Hamas (read more) doesn’t sound like the brightest decision given our fiscal and human challenges at home. I sure hope there are some tangible, accountable benefits accruing to the right people when we have 25 million people here in the U.S. unemployed, underemployed, or discouraged from finding a job.

Rule #3: Put the Obese Elephant on a Diet – As I alluded to above, our government doesn’t need to serve our overweight, entitlement-fed elephant more chocolate, pizza, and ice cream in the form of more entitlements we are not capable of funding. Let’s cut our spending first before we buy off the voters with new spending.

There are obviously a wide ranging set of economic, political, and even religious perspectives on the best ways of managing our hefty debt and deficits. I do not pretend to have all the answers, but what I do know is it is not wise to blast the sprinklers when it is pouring rain outside.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, and GOOG, but at the time of publishing SCM had no direct positions in COST, YHOO, INTC, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Plucking the Feathers of Taxpaying Geese

“The art of taxation consists in so plucking the goose as to get the most feathers with the least hissing.” ~Jean Baptist Colbert

With exploding deficits, multiple wars, healthcare reform, and a sluggish economy, there are two logical immediate choices on how to improve our current financial situation:

1) Cut spending. This is not a desirable option for politicians since benefit cuts to voters are not appreciated come re-election period.

2) Raise Taxes. Not desirable from a voter standpoint either, but the Obama administration has chosen to target the rich – the smaller voting population. This can of course backfire, when many of these wealthy individuals are campaign contributors or have ties to lobbyists who are backing the President’s agendas.

The tax-paying geese are getting fatter, but before the goose can be put in the oven, the feathers need plucking with the goal of minimizing hissing. Sure, I am an advocate for tax cuts like most taxpayers. I’m even a larger proponent, if Congress had the political gumption to cut spending to fund the tax drops. Unfortunately, politicians view expense reduction as suicide because cutting programs or benefits will only lead to fewer reelection votes. Congressmen are perfectly fine letting taxpayers live high on the hog for now, and just saddle future generations with our mounting debt problems.

What’s Fair?

The current strategy is based on taxing the wealthy to fund deficits, healthcare, wars, debt, etc. Since the rich represent a smaller proportion of voters, from the egotistical politician standpoint (reelection is paramount), this wealth distribution strategy appears more palatable to incumbent legislators. Democrats would rather focus on squeezing a narrower demographic footprint of voters versus an across the board tax increase, which would impact all taxpayers. Merely taxing the rich can certainly backfire however, especially if the wealthy demographic getting taxed is the exact population paying for the politicians’ reelection and lobbying agendas.

Source: Alan’s Money Blog (U.S. has high corporate tax rate)

But at what point is taxing the rich unfair and counterproductive? Currently the top 10% of the nation that earns more than $92,400 a year, pay about 72% of the country’s income taxes. Ari Fleischer, former G.W. Bush Press Secretary compares the current tax policy to an “inverted pyramid scheme” in a Wall street Journal Op-Ed earlier this year. Like an upside spinning top, the whirling pyramid is supported by a narrow, pointy pinnacle.

Fleischer goes onto add:

“According to the CBO, those who made less than $44,300 in 2001 — 60% of the country — paid a paltry 3.3% of all income taxes. By 2005, almost all of them were excused from paying any income tax. They paid less than 1% of the income tax burden. Their share shrank even when taking into account the payroll tax. In 2001, the bottom 60% paid 16.3% of all taxes; by 2005 their share was down to 14.3%. All the while, this large group of voters made 25.8% of the nation’s income. When you make almost 26% of the income and you pay only 0.6% of the income tax, that’s a good deal, courtesy of those who do pay income taxes.”

Cheaters Should Not Be Exempt (See Celebrity Tax Evader Article)

Certainly loopholes and undeserving credits for multinationals and the wealthy should be removed as well. The House of Representatives recently approved a $387 million boost for the IRS to fund a high-wealth unit focusing on trusts, real estate investments, privately held companies and other business entities controlled by rich individuals (read Reuters article). The IRS is also opening new criminal offices in Beijing, Panama City and Sydney to focus on international enforcement of tax cheaters. At the center of the IRS’ offshore effort is the legal cases against Swiss banking giant UBS (stands for Union Bank of Switzerland), which resulted in UBS agreeing to turn over almost 5,000 client names and pay $780 million to settle tax evasion charges.

Taxes in 2010 and Beyond

When it comes to future taxes, a lot of details remain up in the air. What we do know is that the 2001 Bush tax cuts are set to expire in 2010 and the Obama administration has indicated they want to raise taxes on the rich (those earning more than $250,000) and keep the cuts static for those in the lower paying tax brackets.

- Healthcare: If healthcare reform will indeed pass, those benefits won’t be free. The Obama administration is backing a House bill that creates a 5.4% surtax on income over $500,000 for single filers or $1 million for couples.

- Income Taxes: On the income tax front, Obama and some Democrats are pushing to have the two highest tax brackets revert back to the pre-2001 levels of 36% and 39.6%.

- Capital Gains: If the Obama administration gets its way, capital-gains tax rates would go back to 20% for wealthier individuals and qualified dividends would be taxed as ordinary income up to the top rate of 39.6%.

- Estate Taxes: The House passed a bill earlier this month that makes the 2009 estate tax provisions permanent (i.e., a 45% top marginal rate on estates larger than $3.5 million or $7 million for married couples). If the Senate were not to pass the bill, current law has the estate tax rate reverting to a 55% rate on estates worth more than $1 million after next year.

Given the exploding deficits and weary economy, which is recovering from a severe economic crisis, getting our tax policy situation back in order is critical. Having politicians make tough tax policy decisions runs contrary to their partisan reelection agendas, however our country needs to pluck more feathers from our taxpaying geese to face these monumental economic challenges…even if it requires listening to irritating hissing from our citizens.

Ari Fleischer WSJ Op-Ed From Earlier This Year

Article on Tax Policy Issues for 2010 and Beyond

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at time of publishing had no direct positions in an security referenced, including UBS. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Stewart Makes Skewered Beck-Kebabs

Since Fox news-host, Glenn Beck, has been peddling death and destruction, John Stewart, host of the The Daily Show, decided to dish out some devastation of his own to Mr. Beck by skewering him on several issues. Specifically, Stewart questions whether Beck’s Armageddon view on the economy may be influenced by an economic conflict of interest in gold (not just a political axe to grind)?

Beck on Gold

View The Daily Show Clip on Glenn Beck

As the third party mentions, “If you are worried about worrying, you go out and you buy gold.”

Is Glenn Beck a worried, gold lover? (see other IC articles: Gold #1 & Gold #2) Well, judging by the seven responses of Beck specifically spouting out “gold”, along with his panic-filled quotes, I would say “yes”:

- “America is burning down to the ground!”

- “Here are the three scenarios that we could be facing: recession, depression, or collapse.”

- “Here’s our second scenario: global civil unrest.”

- “You are the protector of liberty. You are the guardian of freedom.”

If these feelings were not enough, Beck also goes on to compare the country’s situation to Nazi Germany.

Do any of these issues worry you? Well if they do, then good for gold prices and good also for Glenn Beck, because he is a paid spokesman for Goldline.com, a site that sells gold.

This is how John Stewart boils down the incestuous relationship between Fox, Goldline.com, and Beck:

“This is a kinda nice feedback loop. Glenn Beck is paid by Goldline to drum up interest in gold, which increases in value during times of fear, an emotion reinforced nightly on Fox by Glenn Beck. Alright, I’m almost sold. Fox is vouching for Beck, and Beck is vouching for Goldmine.”

Gold Pricing & Demand

With gold prices setting new all-time highs earlier this month, one might expect gold demand to be sky-rocketing…actually not. Just last month, the World Gold Council said gold demand totaled 800.3 tons in Q3, down -34% year-over-year. What’s more, the supply of gold inventories is at record highs (Comex) and mining production rose +6% over the same time period. Generally speaking, economics would say the combination of these factors would be a bad formula for prices.

Beck and the CEO of Goldmine.com use inflation adjusted prices based on the last $850/oz. peak in 1980 to rationalize $2,000/oz+ targets for gold. If that’s the case then I guess NASDAQ targets of 10,000 (2x of the 5,000 year 2000 peak) shouldn’t be out of the question either (the index currently trades around 2,190)? In the meantime, I’ll let the speculative gold dust settle and comfortably watch from the sidelines.

Source: InvestmentTools.com

Hemorrhoid Hypocrisy on Healthcare

In an earlier The Daily Show episode, Stewart questions the consistency of Beck’s changing views on healthcare. So which one is it? Is it the best healthcare program in the world, or the one that doesn’t care for Glenn Beck and the “schlubs that are just average working stiffs?”

In creating a feeling of alarm regarding healthcare reform, here’s what Beck had to say in the middle of the healthcare reform debate:

- “You’re about to lose the best healthcare system in the world.”

- “America already has the best healthcare in the world. We do take care of our sick.”

Rewind 16 months earlier upon completion of Beck’s hemorrhoid surgery:

- “Getting well in this country, can almost kill you.”

- “No matter how much the health care system would try to keep me down, I’m back.”

See Daily Show Clip on Healthcare and Glenn Beck

All this bickering can upset your stomach, but after John Stewart’s skewering of Glenn Beck, I have this sudden urge for shish kebabs. Bon appétit until next time…

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (VFH) and RTP in client and personal portfolios at the time of publishing. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Maher Cheerleads No Profit Healthcare

Bill Maher, shock-comedian and host of Real Time with Bill Maher on HBO, has made up a new rule in a recent article, “Not Everything in America Has to Make a Profit.”

Hey Bill, that sounds intriguing. I’ve got an idea – how about you decide to work for no profit? If free healthcare is a right for every American, then why should people pay for your stupid jokes? If I have a right to free healthcare, then why not a right to free laughs?

Don’t get me wrong, our system is broke and needs to be fixed. The real question, is insuring an additional 50 million uninsured, by the same bureaucratic healthcare system leading the Medicare train-wreck, our best approach in solving our healthcare crisis? Sure, doing nothing should not be a fallback, but I’m not sure a trillion dollar healthcare plan with Washington bureaucrats is the best idea either? I’m not against government involvement, but before we dive headfirst into the deep-end with additional deficit exploding plans, why not wade in the shallow end and slowly roll-out success-based models that prove their superiority first.

I’m no medical expert, but let’s take the best structures, whether it’s the Mayo Clinic, Cleveland Clinic, or other leading structures and have the government manage a steady roll-out. If the government can prove a lower-cost, more efficient way of serving higher quality care, then by all means…let’s see it. Some argue we don’t have time to test new models, well unfortunately our disastrous system took decades to create and a pork-filled bill through Congress is not going to be an immediate silver-bullet for our dire healthcare problems.

Getting back to Mr. Maher’s profit objections on healthcare, I wonder if he’s ever complained or contemplated the innovations created by the profit-laden healthcare system. Whether it’s an MRI, hip replacement, cholesterol drug, cancer test, glaucoma treatment, ADHD medication or the hundreds of other beneficial advancements, maybe Mr. Maher should ask and understand where all these innovations came from? The answer: good old profits that were invested in critical research and development. Without those profits, there would be fewer and less impactful healthcare innovation for millions of Americans.

As for the firemen who do not “charge” or make a profit, I would like to remind Mr. Maher who is paying their fair share for those services consumed by hundreds of millions of Americans – it’s those same “soulless vampires making money off human pain” that you castigate. Profitable corporations are funding those essential government services with tax dollars derived from, you guessed it, profits. If we can find a lower-cost, more efficient way of serving the public services by the government, then as Phil Knight from Nike (NKE) says, “Just Do It!” Unfortunately, I prefer to see some tangible proof first, before spending hundreds of billions of tax dollars.

Healthy Incentives

From an early age, even as babies, we are incentivized for certain behavior. Whether it’s offering M&Ms to potty-train a two year old, or submitting six-figure bonuses to a fifty-two year old for hitting department profit targets, incentives always plays a central role in shaping behavior. Figure out the desired behavior and create incentives for your subjects (and penalties for non-compliance).

As the government comes up with a public solution, I have no problem with Washington pressuring insurance companies and the medical industry to become more efficient and provide a higher threshold of care. I’m confident that structures can be put in place that mitigate conflicts of interest (i.e., pure profit motive), while increasing the standard of care and efficiency. Rewarding the healthcare industry with incentives, rather than just simply beating them over the head with lower reimbursements under a single-payer system, may produce longer-lasting, sustainable benefits.

In certain areas of society, such as policemen/women, firefighters, national defense, and doctors there has always been a view that government is better suited for handling certain services. However, sometimes government does not implement the proper incentive plans, which then leads to bureaucracy, inefficiency, and excessive costs. Eventually, these negative trends overwhelm the system into failure, much like sand grinding engine gears to a halt.

Bill, I appreciate your viewpoint, and I like you would love if everything was free. For starters, I’ll look for your press release announcing the cancellation of your multi-million contract with HBO, closely followed by the revelation of your pro-bono comedy work. Here’s to profitless prosperity.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in NKE, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}