Archive for November, 2013

Confusing Fear Bubbles with Stock Bubbles

With the Dow Jones Industrial Average approaching and now breaking the 16,000 level, there has been a lot of discussion about whether the stock market is an inflating bubble about to burst due to excessive price appreciation? The reality is a fear bubble exists…not a valuation bubble. This fear phenomenon became abundantly clear from 2008 – 2012 when $100s of billions flowed out of stocks into bonds and trillions in cash got stuffed under the mattress earning near 0% (see Take Me Out to the Stock Game). The tide has modestly turned in 2013 but as I’ve written over the last six months, investor skepticism has reigned supreme (see Most Hated Bull Market Ever & Investors Snore).

Volatility in stocks will always exist, but standard ups-and-downs don’t equate to a bubble. The fact of the matter is if you are reading about bubble headlines in prominent newspapers and magazines, or listening to bubble talk on the TV or radio, then those particular bubbles likely do not exist. Or as strategist and investor Jim Stack has stated, “Bubbles, for the most part, are invisible to those trapped inside the bubble.”

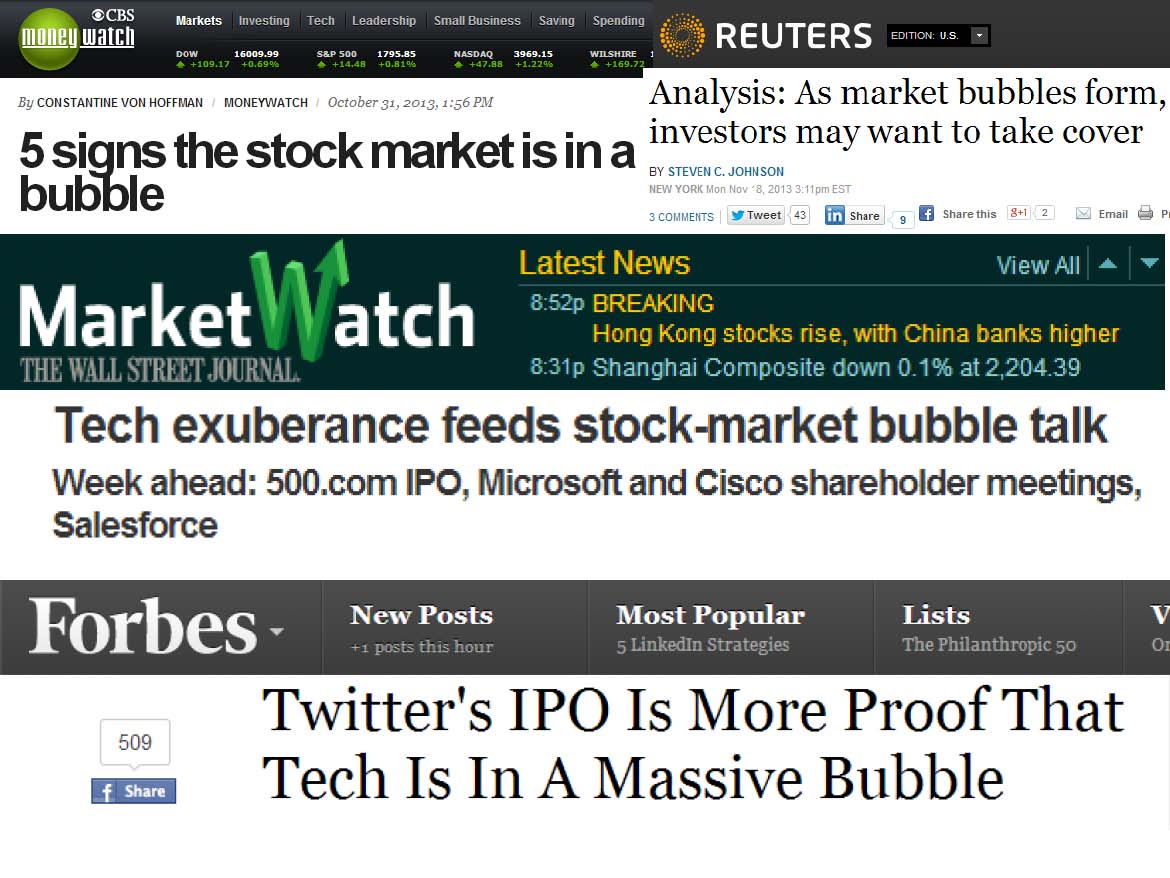

All the recent bubble talk scattered over all the media outlets only bolsters my fear case more. If we actually were in a stock bubble, you wouldn’t be reading headlines like these:

From 1,300 Bubble to 5,000

If you think identifying financial bubbles is easy, then you should buy former Federal Reserve Chairman Alan Greenspan a drink and ask him how easy it is? During his chairmanship in late-1996, he successfully managed to identify the existence of an expanding technology bubble when he delivered his infamous “irrational exuberance” speech. The only problem was he failed miserably on his timing. From the timing of his alarming speech to the ultimate pricking of the bubble in 2000, the NASDAQ index proceeded to more than triple in value (from about 1,300 to over 5,000).

Current Fed Chairman Ben Bernanke was no better in identifying the housing bubble. In his remarks made before the Federal Reserve Board of Chicago in May 2007, Bernanke had this to say:

“…We believe the effect of the troubles in the subprime sector on the broader housing market will likely be limited, and we do not expect significant spillovers from the subprime market to the rest of the economy or to the financial system. The vast majority of mortgages, including even subprime mortgages, continue to perform well.”

If the most powerful people in finance are horrible at timing financial market bubbles, then perhaps you shouldn’t stake your life’s savings on that endeavor either.

Bubbles History 101

Each bubble is unique in its own way, but analyzing previous historic bubbles can help understand future ones (see Sleeping Through Bubbles):

• Dutch Tulip-Mania: About 400 years ago in the 1630s, rather than buying a new house, Dutch natives were paying over $60,000 for tulip bulbs.

• British Railroad Mania: The overbuilding of railways in Britain during the 1840s.

• Roaring 20s: Preceding the Wall Street Crash of 1929 (-90% plunge in the Dow Jones Industrial average) and Great Depression, the U.S. economy experienced an extraordinary boom during the 1920s.

• Nifty Fifty: During the early 1970s, investors and traders piled into a set of glamour stocks or “Blue Chips” that eventually came crashing down about -90%.

• Japan’s Nikkei: The value of the Nikkei index increased over 450% in the eight years leading up to the peak of 38,957 in December 1989. Today, almost 25 years later, the index stands at about 15,382.

• Tech Bubble: Near the peak of the technology bubble in 2000, stocks like JDS Uniphase Corp (JDSU) and Yahoo! Inc (YHOO) traded for over 600x’s earnings. Needless to say, things ended pretty badly once the bubble burst.

As long as humans breathe, and fear and greed exist (i.e., forever), then we will continue to encounter bubbles. Unfortunately, we are unlikely to be notified of future bubbles in mainstream headlines. The objective way to unearth true economic bubbles is by focusing on excessive valuations. While stock prices are nowhere near the towering valuations of the technology and Japanese bubbles of the late 20th century, the bubble of fear originating from the 2008-2009 financial crisis has pushed many long-term bond prices to ridiculously high levels. As a result, these and other bonds are particularly vulnerable to spikes in interest rates (see Confessions of a Bond Hater).

Rather than chasing bubbles and nervously fretting over sensationalistic headlines, you will be better served by devoting your attention to the creation of a globally diversified investment portfolio. Own a portfolio that integrates a wide range of asset classes, and steers clear of popularly overpriced investments that the masses are talking about. When fear disappears and everyone is clamoring to buy stocks, you can be confident the stock bubble is ready to burst.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in TWTR, JDSU, YHOO or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Surviving a Series of Unfortunate Events

My children grew up reading a Series of Unfortunate Events by Lemony Snicket’s (the pseudonym for Daniel Handler). The award winning 13 book series began at the turn of the century (1999) with the Bad Beginning and seven years later, Handler ended the stories with The End (2006). The books chronicle the stories of three orphaned children (Violet, Klaus, and Sunny Baudelaire) who experience increasingly terrible events after the alleged death of their parents and burning of their house by a man named Count Olaf.

Crime, violence and hardships not only occur in novels, but also in real life. Stock market investors are no strangers to unfortunate events either. Within the last five years alone, investors have endured an endless stream of bad news, including the following:

- Flash Crash

- Debt Ceiling Debate

- U.S. Debt Downgrade

- European Recession

- Arab Spring

- Potential Greek Exit from EU

- Uncertain U.S. Presidential Elections

- Sequestration

- Cyprus Financial Crisis

- Tax Increases

- Fed Talks of Stimulus Tapering

- Syrian Civil War / Military Threat

- Gov. Shutdown

- Obamacare Rollout Glitches

- Iranian Nuclear Threat

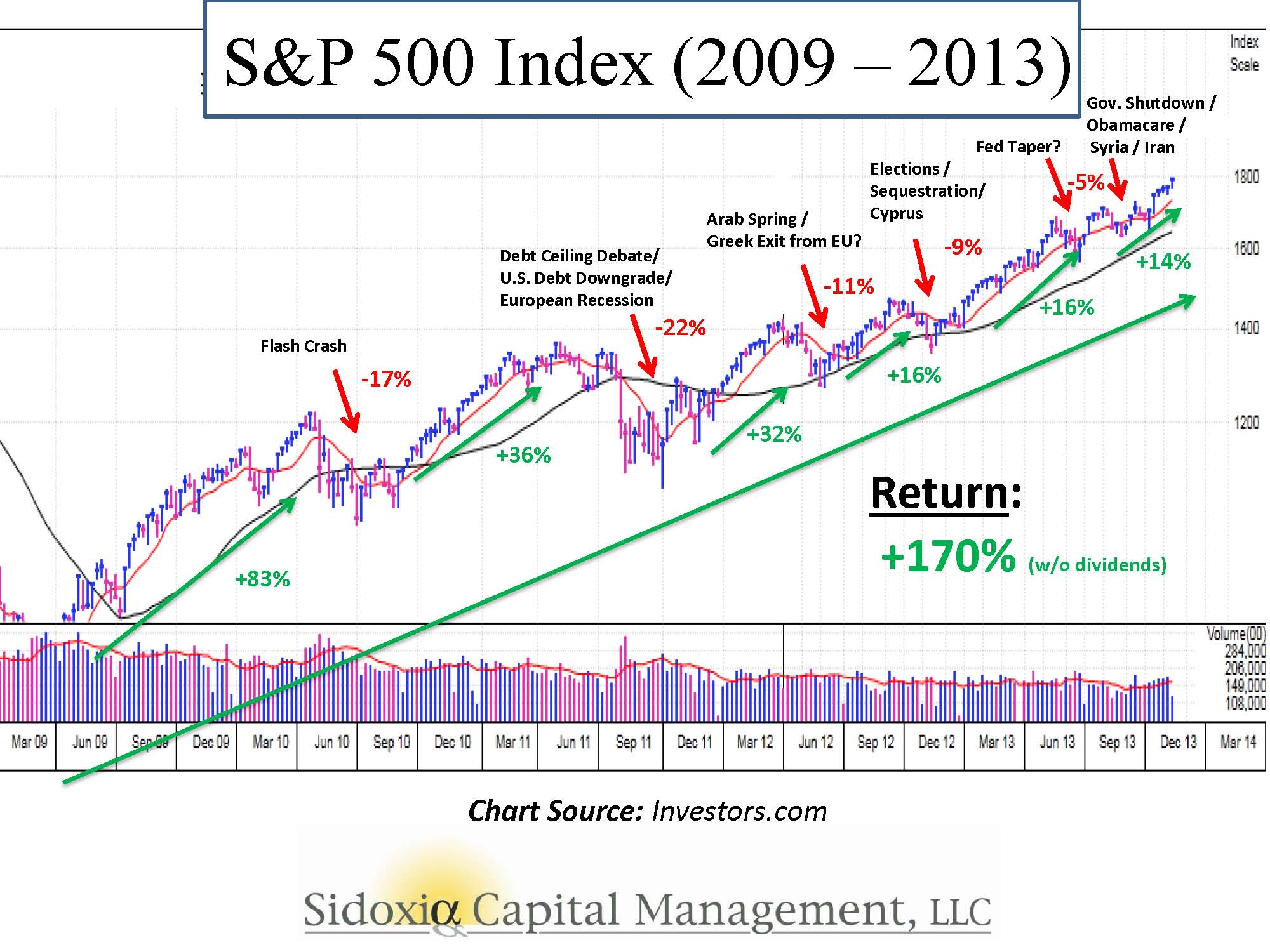

This is only a partial list, but wow, this never ending crises list sounds pretty ominous, right? I wonder how stocks have fared amidst this horrendous avalanche of negative headlines? The short answer is stocks are up a whopping +170% since the March 2009 lows as measured by the S&P 500 index, and would be significantly higher once accounting for reinvested dividends. A bit higher return than your CD, money market, or savings account rate.

As you can see from the chart above, the gargantuan returns achieved over this period have not occurred without some volatility. Investors have consumed massive quantities of Tums during the five highlighted corrections (averaging -13%) to counteract all the heartburn. As I’ve written in the past, with higher risk comes higher rewards. Those investors who cannot stomach the volatility shouldn’t go cold turkey on stocks though, but rather diversify their holdings and reduce the portfolio equity allocation to a more palatable level.

Doubting Thomases

Many people I bump into remain “Doubting Thomases” as it relates to the stock market recovery and they expect an imminent crash. Certainly, the rocket-like trajectory of the last year (and five years) is not sustainable, and historically stocks correct significantly twice a decade – equal to the number of recessions occurring each decade. There is no denying that this economic recovery has been the slowest since World War II, but could this be good news? From the half-full glass lens, a slower recovery may actually equate to a longer recovery.

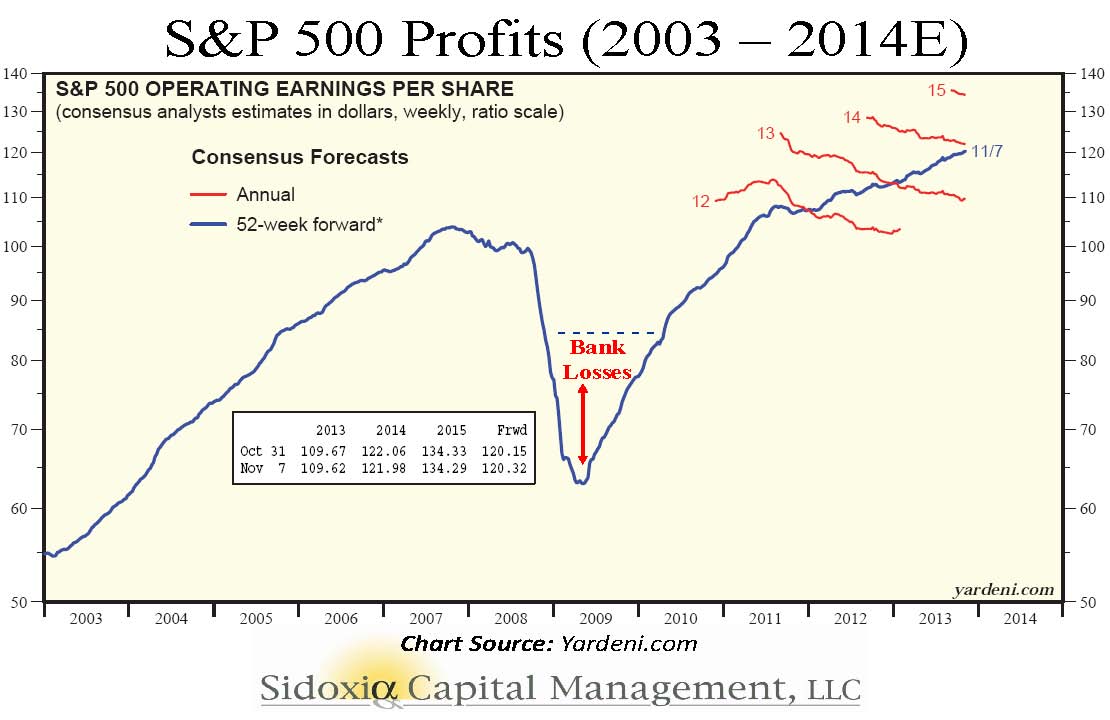

Just like skeptical investors, business executives have been slow to hire and slow to accelerate spending as well. Typically business cycles come to an end when overinvestment happens – recall the 2000 tech bubble and 2007 housing bubble. There may be pockets of investment bubbles (e.g., Twitter Inc [TWTR] and other money-losing speculative stocks), but as you can see from the chart below, corporate profits have skyrocketed and are at record highs. It should therefore come as no surprise that record profits have coincided with record stock prices (see also It’s the Earnings Stupid)

Over the period of 2003-2013 stock prices largely followed the slope of earnings, and excluding the enormous losses in the banking sector, non-financial stocks suffered much less.

History is on Your Side

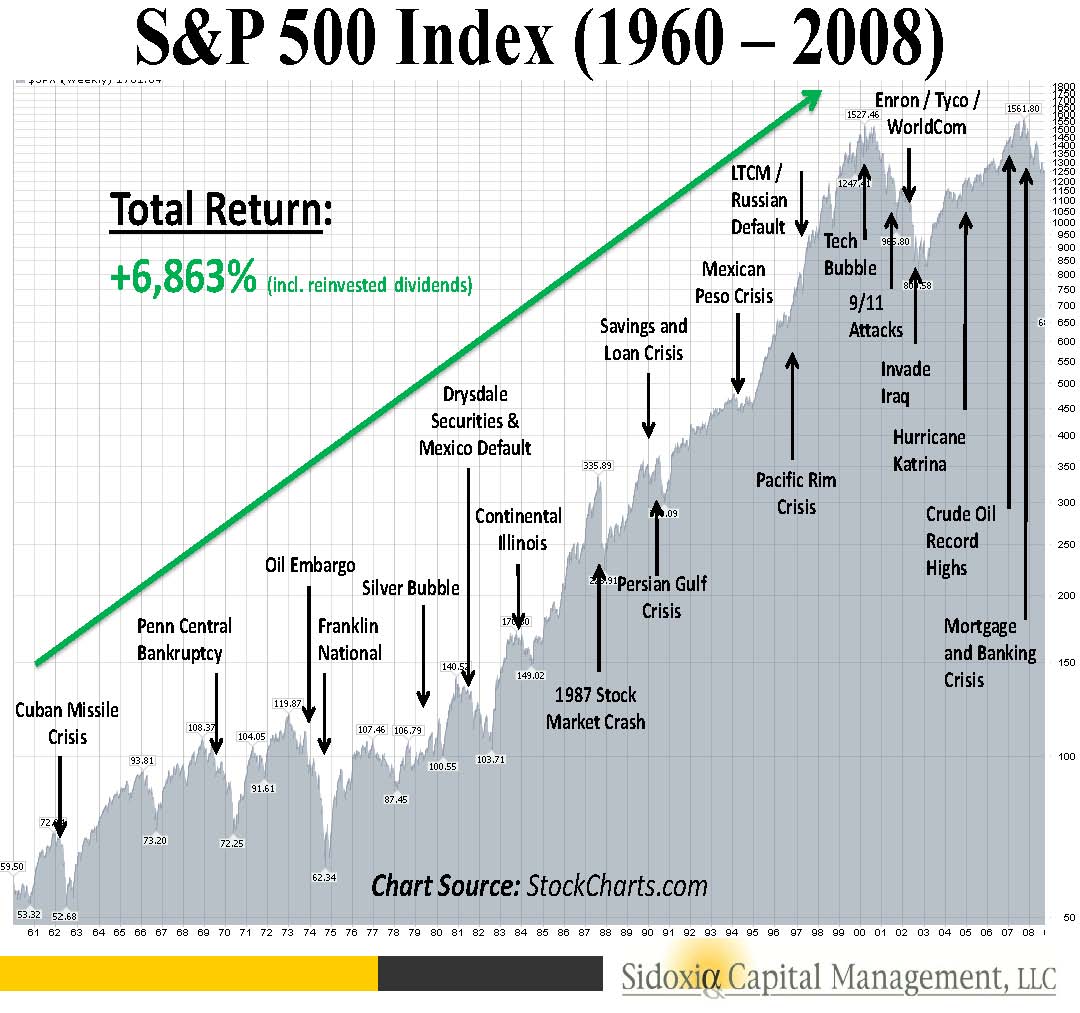

If you are in the camp that says this last five years has been an anomaly, history may beg to differ. Over the last 50 years we have experienced wars, assassinations, currency crises, banking crises, terrorist attacks, recessions, SARs, mad cow disease, military engagements, tax hikes, Fed rate hikes, and yes, even political gridlock. As the chart below shows, the stock market is volatile over the short-run, but quite resilient and lucrative over the long-run (+6,863% over 49 years). In fact, from January 1960 to October 2013 the S&P 500 index has catapulted +14,658%, including reinvested dividends (Source: DQYDJ.net).

Rather than getting caught up in the political or CNBC headline du jour, investors will be better served by creating a customized, long-term diversified portfolio that can meet long-standing goals and objectives. If you don’t have the discipline, interest, or time to properly create a personalized investment plan, then find an independent investment advisor like Sidoxia Capital Management (www.Sidoxia.com), so you can experience a series of fortunate (not unfortunate) events.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in TWTR, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page. Chart construction done by Kevin D. Weaver.

To Taper or Not to Taper…That is the Question?

It’s not Hamlet who is providing theatrical intrigue in the financial markets, but rather Federal Reserve Chairman Ben Bernanke. Watching Bernanke decide whether to taper or not to taper the $85 billion in monthly bond purchases (quantitative easing) is similar to viewing an emotionally volatile Shakespearean drama. The audience of investors is sitting at the edge of their seats waiting to see if incoming Fed Chief will be plagued with guilt like Lady Macbeth for her complicit money printing ways or will she score a heroic and triumphant victory for her hawkish stance on quantitative easing (QE). No need to purchase tickets at a theater box office near you, the performance is coming live to your living room as Yellen’s upcoming Senate confirmation hearings will be televised this upcoming week.

Bad News = Good News; Good News = Bad News?

In deciding whether to slowly kill QE, the Fed has been stricken with the usual stream of never-ending economic data (see current data from Barry Ritholtz). Most recently, investors have followed the script that says bad news is good news for stocks and good news is bad news. So-called pundits, strategists, and economists generally believe sluggish economic data will lead the Fed to further romance QE for a longer period, while robust data will force a poisonous death to QE via tapering.

Good News

Despite the recent, tragically-perceived government shutdown, here is the week’s positive news that may contribute to an accelerated QE stimulus tapering:

- Strong Jobs: The latest monthly employment report showed +204,000 jobs added in October, almost +100,000 more additions than economists expected. August and September job additions were also revised higher.

- GDP Surprise: 3rd quarter GDP registered in at +2.8% vs. expectations of 2%.

- IPO Dough: Twitter Inc (TWTR) achieved a lofty $25,000,000,000 initial public offering (IPO) value on its first day of trading.

- ECB Cuts Rates: The European Central Bank (ECB) lowered its key benchmark refinancing rate to a record low 0.25% level.

- Service Sector Surge: ISM non-manufacturing PMI data for October came in at 55.4 vs. 54.0 estimate.

Bad News

Here is the other side of the coin, which could assist in the delay of tapering:

- Mortgage Apps Decline: Last week the MBA mortgage application index fell -7%.

- Jobless # Revised Higher: Last week’s Initial jobless Claims were revised higher by 5,000 to 345,000.

- Investors Too Happy: The spread between Bulls & Bears is highest since April 2011 as measured by Investors Intelligence

Much Ado About Nothing

With the recent surge in the October jobs numbers, the tapering plot has thickened. But rather than a tragic death to the stock market, the inevitable taper and eventual tightening of the Fed Funds rate will likely be “Much Ado About Nothing.” How can that be?

As I have written in an article earlier this year (see 1994 Bond Repeat), the modest increase in 2013 yields (up +1.35% approximately) from the July 2012 lows pales in comparison to the +2.5% multi-period hike in the 1994 Federal Funds rate by then Fed Chairman Alan Greenspan. What’s more, inflation was a much greater risk in 1994 with GDP exceeding 4.0% and unemployment reaching a hot 5.5% level.

Given an overheated economy and job market in 1994, coupled with a hawkish Fed aggressively raising rates, the impact of these factors must have been disastrous for the stock market…right? WRONG. The S&P 500 actually finished the year essentially flat (~-1.5%) after experiencing some volatility earlier in the year, then subsequently stocks went on a tear to more than triple in value over the next five years.

To taper or not to taper may be the media question du jour, however the Fed’s ultimate decision regarding QE will most likely resemble a heroic Shakespearean finale or Much Ado About Nothing. Panicked portfolios may be in love with cash like Romeo & Juliet were with each other, but overreaction by investors to future tapering and rate hikes may result in poisonous or tragic returns.

Referenced article: 1994 Bond Repeat or 2013 Stock Defeat?

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in TWTR, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page. Some Shakespeare references were sourced from Kevin D. Weaver.

Hunt for Red October Turns Green

This article is an excerpt from a previously released Sidoxia Capital Management complementary newsletter (November 1, 2013). Subscribe on the right side of the page for the complete text.

In the movie the Hunt for Red October, Sean Connery plays Marko Ramius, a Soviet Union submarine commander, who wants to defect to the United States. Jack Ryan, played by Alec Baldwin, plays a CIA analyst who attempts to prevent Ramius’ stealthy submarine from attacking American soil.

October has historically been viewed as a bloody period in the stock market, given the multiple October crashes occurring in 1929, 1987, and 2008. However, the large number of bears and skeptics who were on a hunt for red (losing) October were rudely surprised last month. Rather than plunging in value, stocks ascended to new record green heights. Specifically, the S&P 500 index rose +4.5% in October, bringing 2013’s total climb to +23.2% (NASDAQ +29.8% for the year).

While the Soviet “Cold War” may have ended in the early 1990s, when it comes to retirement and financial assets, the emotional war for a prosperous future seems to never end for those without an investment plan.

How Can it Be?!

As the financial markets have recently grinded to new all-time record highs, I still stumble across a vast number of skeptics and doubters. These cynical cats make comments and ask questions like:

- “You’re shorting the market, right?” (i.e., betting prices will go down)

- “I’ll just get in and buy when the market goes down.”

- “How can the stock market keep setting new highs when the economy is so weak?”

- “This country is going to hell in a handbasket…what are these politicians in Washington thinking?!”

- “The only reason the market is up is due to the Federal Reserve’s money printing and artificial manipulation of the financial system.” (see also Greatest Thing Since Sliced Bread)

These are but a few of the widespread concerns, and understandably so because fear, uncertainty, and doubt are exactly what media outlets shovel in the faces of the masses. However, unlike humans, the financial markets do not watch TV or listen to the radio. As famed investor Benjamin Graham notes, “In the short run, the market is a voting machine but in the long run it is a weighing machine.” Or in other words, emotions can rule the short-term, but positive or negative fundamentals will rule the day over the long-term.

While the concerns listed above may have some validity, here are some alternative perspectives to help explain why patient investors have been rewarded:

Record Profits

|

| Source: Ed Yardeni (Dr. Ed’s Blog) |

This isn’t the first or last time I’ve focused on earnings data. At the end of the day, my investment philosophy that “prices follow earnings” aligns with legend Peter Lynch’s views:

“People may bet on hourly wiggles of the market but it’s the earnings that waggle the wiggle long term.”

Stocks are Cheap (Not Expensive)

Despite the massive run-up in prices, stocks are cheap. There are some metrics that show equity prices as fairly valued, but there is plenty of data to support why stocks have and continue to be loved.

|

| Source: Ed Yardeni (Dr. Ed’s Blog) |

Although the Federal Reserve’s economic model above shows how overvalued technology stocks were during the late-1990s bubble, eventually the speculative period burst. On the flip side, you can see how attractively priced (undervalued) stocks look today (prices are significantly below the historical average).

If that’s not enough evidence for you, take a peek at strategist Don Hays’s “Rule of Twenty” chart below (see also Investing Caffeine article). If you go back multiple decades, you can see a fairly tight correlation between the blue line (stock valuation/prices) and red line (Rule of 20), which creates an estimated fair value target that integrates inflation. So as you can see, when the blue line rises above the red line, stock prices are overvalued. Once again, you can see that stocks currently are relatively cheap historically (blue line below the red line), based on Hays’s analysis.

|

| Source: Hays Advisory |

Economy Keeps Chugging Along

The job market has improved dramatically, housing prices have rebounded, and families have lowered the debt on their balance sheets. The net result of these developments is evidenced by record consumer spending at retail (see chart below):

|

The 15 out of 16 quarters of economic growth as measured by Gross Domestic Product (GDP) have also been assisted by record exports (see chart below). Even though growth in the U.S. remains sluggish, innovative companies have found creative ways to export unique goods and services abroad.

Source: Calculated Risk

Even though Halloween is behind us, there are still bound to be some scary tricks ahead of us, including heated debates over government shutdowns, debt ceilings, and sequestrations. The key to a successful financial future is having a balanced, diversified portfolio that meets your long-term objectives, while helping you avoid investment torpedoes. Investing based on emotional, knee-jerk reactions to noisy mainstream media headlines is a sure way to sink your portfolio. That’s advice I’m sure Jack Ryan could agree on. If investors follow this guidance, their Hunt for Red October can turn into green portfolios.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}