Archive for April, 2017

Managing the Chaos – Investing vs. Gambling

How does one invest amid the slew of palm sweating, teeth grinding headlines of Syria, North Korea, Brexit, expanding populism, Trumpcare, French candidate Marine Le Pen, and a potential government shutdown? Facing a persistent mountain of worries can seem daunting to many. With so many seemingly uncontrollable factors impacting short-term interest rates, foreign exchange rates, and equity markets, it begs the question of whether investing is a game of luck (gambling) or a game of skill?

The short answer is…it depends. Professional gambler Alvin “Titanic” Thompson captured the essence when someone asked him whether poker was a game of chance. Thompson responded by stating, “Not the way I play it.”

If you go to Las Vegas and gamble, most games are generally a zero sum-game, meaning there are an equal number of winners and losers with the house (casino) locking in a guaranteed spread (profit). For example, consider a game like roulette – there are 18 red slots, 18 black slots, and 2 green slots (0 & 00), so if you are betting on red vs. black, then the casino has a 5.26% advantage. If you bet long enough, the casino will get all your money – there’s a reason Lost Wages Las Vegas can build those extravagantly large casinos.

The same principles of money-losing bets apply to speculative short-term trading. Sure, there are examples of speculators hitting it big in the short-run, but most day traders lose money (see Day Trading Your House) because the odds are stacked against them. In order to make an accretive, profitable trade, not only does the trader have to be right on the security they’re selling (i.e. that security must underperform in the future), but they also have to be right on the security they are buying (i.e. that security must outperform in the future). But the odds for the speculator get worse once you also account for the trading fees, taxes, bid-ask spreads, impact costs (i.e., liquidity), and informational costs (i.e., front running, high frequency traders, algorithms, etc.).

The key to winning at investing is to have an edge, and the easiest way to have an investing edge is to invest for the long-run – renowned Professor Jeremy Siegel agrees (see Stocks for the Long Run). It’s common knowledge the stock market is up about two-thirds of the time, meaning the odds and wind are behind the backs of long-term investors. Short-term trading is the equivalent of going fishing, and then continually pulling your fishing line out of the water (you’re never going to catch anything). The fisherman is better off by researching a good location and then maintaining the lure in the water for a longer period until success is achieved.

Although most casino games are based on pure luck, there are some games of skill, like poker, that can produce consistent long-term positive results, if you are a patient professional with an advantage or edge (see Dan Harrington article ). Having an edge in investing is crucial, but an edge is not the only aspect of successful investing. How you structure a portfolio to control risk (i.e., money management), and reducing your personal behavioral biases are additional components to a winning investment strategy. Professional poker player Walter Clyde “Puggy” Pearson summed it up best when he described the three critical components to winning:

“Knowing the 60-40 end of a proposition, money management, and knowing yourself.”

At Sidoxia Capital Management, we have also achieved long-term success by following a systematic, disciplined process. A large portion of our investment strategy is focused on identifying market leading franchises with a long runway of growth, and combining those dynamics with positions trading at attractive or fair values. As part of this process, we rank our stocks based on multiple factors, primarily using data from our proprietary SHGR ranking (see Investing Holy Grail) and free cash flow yield analysis, among other important considerations. Based on the risk-reward profiles of our existing holdings and the pool of targeted investments, we can appropriately size our positions accordingly (i.e., money management). As valuations rise, or risk profiles deteriorate, we can make the corresponding portfolio positions cuts, especially if we find more attractive alternative investments. Having a proven, systematic, unbiased process has helped us tremendously in minimizing behavioral pitfalls (i.e., knowing yourself) when we construct client portfolios.

The world is under assault…but that has always been the case. Throughout investment history, there have been wars, assassinations, unexpected election outcomes, banking crises, currency crises, natural disasters, health epidemics, and more. Unfortunately, millions have gambled and bet their money away based on these frivolous, ever-changing, short-term headlines. On the other hand, those investors who understand the 60-40 end of a proposition, coupled with the importance of money management and controlling personal biases, will be the skillful winners to prosper over the long-run.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Investing in a World of Black Swans

In the world of modern finance, there has always been the search for the Holy Grail. Ever since the advent of computers, practitioners have looked to harness the power of computing and direct it towards the goal of producing endless profits. Today the buzz words being used across industries include, “AI – Artificial Intelligence,” “Machine Learning,” “Neural Networks,” and “Deep Learning.” Regrettably, nobody has found a silver bullet, but that hasn’t slowed down people from trying. Wall Street has an innate desire to try to turn the ultra-complex field of finance into a science, just as they do in the field of physics. Even banking stalwart JPMorgan Chase (JPM) and its renowned CEO/Chairman Jamie Dimon suffered billions in losses in the quest for infinite income, due in large part to their over-reliance on pseudo-science trading models.

Preceding JPM’s losses, James Montier of Grantham Mayo van Otterloo’s asset allocation team gave a keynote speech at a CFA Institute Annual Conference in Chicago, where he gave a prescient talk explaining why bad models were the root cause of the financial crisis. Montier noted these computer algorithms essentially underappreciate the number and severity of Black Swan events (low probability negative outcomes) and the models’ inability to accurately identify predictable surprises.

What are predictable surprises? Here’s what Montier had to say on the topic:

“Predictable surprises are really about situations where some people are aware of the problem. The problem gets worse over time and eventually explodes into crisis.”

When Dimon was made aware of the 2012 rogue trading activities, he strenuously denied the problem before reversing course and admitting to the dilemma. Unfortunately, many of these Wall Street firms and financial institutions use value-at-risk (VaR) models that are falsely based on the belief that past results will repeat themselves, and financial market returns are normally distributed. Those suppositions are not always true.

Another perfect example of a Black Swan created by a bad financial model is Long Term Capital Management (LTCM) – see also When Genius Failed. Robert Merton and Myron Scholes were world renowned Nobel Prize winners who single-handedly brought the global financial market to its knees in 1998 when LTCM lost $500 million in one day and required a $3.6 billion bailout from a consortium of banks. Their mathematical models worked for a while but did not fully account for trading environments with low liquidity (i.e., traders fleeing in panic) and outcomes that defied the historical correlations embedded in their computer algorithms. The “Flash Crash” of 2010, in which liquidity evaporated due to high-frequency traders temporarily jumping ship, is another illustration of computers wreaking havoc on the financial markets.

The problem with many of these models, even for the ones that work in the short-run, is that behavior and correlations are constantly changing. Therefore any strategy successfully reaping outsized profits in the near-term will eventually be discovered by other financial vultures and exploited away.

Another pundit with a firm hold on Wall Street financial models is David Leinweber, author of Nerds on Wall Street. As Leinweber points out, financial models become meaningless if the data is sliced and diced to form manipulated and nonsensical relationships. The data coming out can only be as good as the data going in – “garbage in, garbage out.”

In searching for the most absurd data possible to explain the returns of the S&P 500 index, Leinweiber discovered that butter production in Bangladesh was an excellent predictor of stock market returns, explaining 75% of the variation of historical returns. By tossing in U.S. cheese production and the total population of sheep in Bangladesh, Leinweber was able to mathematically “predict” past U.S. stock returns with 99% accuracy. To read more about other financial modeling absurdities, check out a previous Investing Caffeine article, Butter in Bangladesh.

Generally, investors want precision through math, but as famed investor Benjamin Graham noted more than 50 years ago, “Mathematics is ordinarily considered as producing precise, dependable results. But in the stock market, the more elaborate and obtuse the mathematics, the more uncertain and speculative the conclusions we draw therefrom. Whenever calculus is brought in, or higher algebra, you can take it as a warning signal that the operator is trying to substitute theory for experience.”

If these models are so bad, then why do so many people use them? Montier points to “intentional blindness,” the tendency to see what one expects to see, and “distorted incentives” (i.e., compensation structures rewarding improper or risky behavior).

Montier’s solution to dealing with these models is not to completely eradicate them, but rather recognize the numerous shortcomings of them and instead focus on the robustness of these models. Or in other words, be skeptical, know the limits of the models, and build portfolios to survive multiple different environments.

Investors seem to be discovering more financial Black Swans over the last few years in the form of events like the Lehman Brothers bankruptcy, Flash Crash, and Greek sovereign debt default. Rather than putting too much faith or dependence on bad financial models to identify or exploit Black Swan events, the over-reliance on these models may turn this rare breed of swans into a large bevy.

See Full Article on Montier: Failures of Modern Finance

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own JPM and certain exchange traded funds, but at the time of publishing SCM had no direct position in Lehman Brothers, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

You Can’t Kiss All the Beauties

When I was in high school and college, kissing all the pretty girls was not a realistic goal. The same principle applies to stock picking – you can’t buy all the outperforming stocks. As far as I’m concerned, there will always be some people who are smarter, better looking, and wealthier than I am, but that has little to do with whether I can continue to outperform, if I stick to my systematic, disciplined process. In fact, many smart people are horrible investors because they overthink the investing process or suffer from “paralysis by analysis.” When it comes to investing, the behavioral ability to maintain independence is more important than being a genius. If you don’t believe me, just listen to arguably the smartest investor of all-time, Warren Buffett:

“Success in investing doesn’t correlate with I.Q. once you’re above the level of 125. Once you have ordinary intelligence, what you need is the temperament to control the urges that get other people into trouble in investing.”

Even the best investors and stock pickers of all-time are consistently wrong. When selecting stocks, a worthy objective is to correctly pick three outperforming stocks out of five stocks. And out of the three winning stocks, the rationale behind the outperformance should be correct in two out of those three stocks. In other words, you can be right for the wrong reason in one out of three outperforming stocks. The legendary investor Peter Lynch summed it up when he stated, “If you’re terrific in this business you’re right six times out of 10.”

Yes, it’s true, luck does play a role in stock selection. You just don’t want luck being the major driving force behind your success because luck cannot be replicated consistently over the long-run. There are so many unpredictable variables that in the short-run can work for or against the performance of your stock. Consider factors like politics, monetary policy, weather, interest rates, terrorist attacks, regulations, tax policy, and many other influences that are challenging or impossible to forecast. Over the long-run, these uncontrollable and unpredictable factors should balance out, thereby allowing your investing edge to shine.

Although I have missed some supermodel stocks, I have kissed some pretty stocks in my career too. I wish I could have invested in more stocks like Amazon.com Inc. (AMZN) that have increased more than 10x-fold, but other beauties like Apple Inc. (AAPL), Alphabet Inc. (GOOG), and Facebook Inc. (FB), haven’t hurt my long-term performance either. As is the case for most successful long-term investors, winning stocks generally more than compensate for the stinkers, if you can have the wherewithal to hold onto the multi-baggers (i.e., stocks that more than double), which admittedly is much easier said than done. Peter Lynch emphasized this point by stressing a focus on the long-term:

“You don’t need a lot of good hits every day. All you need is two to three goods stocks a decade.”

Sticking to a process of identifying and investing in well-managed companies at attractive valuations is a much better approach to investing than chasing every beauty you see or read about. If you stick to this simple formula, you can experience lovely, long-term results.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AAPL, FB, GOOG, AMZN, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

No April Fool’s Joke – Another Record

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (April 3, 2017). Subscribe on the right side of the page for the complete text.

Having children is great, but a disadvantage to having younger kids are the April Fool’s jokes they like to play on parents. Fortunately, this year was fairly benign as I only suffered a nail-polish covered bar of soap in the shower. However, what has not been a joke has been the serious series of new record highs achieved in the stock market. While it is true the S&P 500 index finished roughly flat for the month (-0.0%) after hitting new highs earlier in March, the technology-laden NASDAQ index continued its dominating run, advancing +1.5% in March contributing to the impressive +10% jump in the first quarter. For 2017, the NASDAQ supremacy has been aided by the stalwart gains realized by leaders like Apple Inc. (up +24%), Facebook Inc. (up +23%), and Amazon.com Inc. (up +18%). The surprising fact to many is that these records have come in the face of immense political turmoil – most recently President Trump’s failure to deliver on a campaign promise to repeal and replace the Obamacare healthcare system.

Like a broken record, I’ve repeated there are much more important factors impacting investment portfolios and the stock market other than politics (see also Politics Schmolitics). In fact, many casual observers of the stock market don’t realize we have been in the midst of a synchronized, global economic expansion, helped in part by the stabilization in the value of the U.S. dollar over the last couple of years.

Source: Investing.com

As you can see above, there was an approximate +25% appreciation in the value of the dollar in late-2014, early-2015. This spike in the value of the dollar suddenly made U.S. goods sold abroad +25% more expensive, resulting in U.S. multinational companies experiencing a dramatic profitability squeeze over a short period of time. The good news is that over the last two years the dollar has stabilized around an index value of 100. What does this mean? In short, this has provided U.S. multinational companies time to adjust operations, thereby neutralizing the currency headwinds and allowing the companies to return to profitability growth.

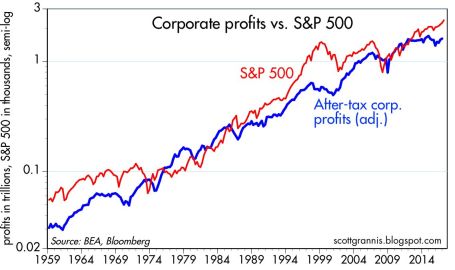

Source: Calafia Beach Pundit

And profits are back on the rise indeed. The six decade long chart above shows there is a significant correlation between the stock market (red line – S&P 500) and corporate profits (blue line). The skeptics and naysayers have been out in full force ever since the 2008-2009 financial crisis – I profiled these so-called “sideliners” in Get out of Stocks!.

As the stock market continues to hit new record highs, the doubters continue to scream danger. There will always be volatility, but when the richest investor of all-time, Warren Buffett, continues to say that stocks are still attractively priced, given the current interest rate environment, that goes a long way to assuage investor concerns.

Politically, a lot could still go wrong as it relates to healthcare, tax reform, and infrastructure spending, to name a few issues. However, it’s still early, and it’s possible positive surprises could also occur. More importantly, as I’ve noted before, corporate profits, interest rates, valuations, and investor sentiment are much more important factors than politics, and on balance these factors are on the favorable side of the ledger. These factors will have a larger impact on the long-term direction of stock prices.

With approval ratings of Congress and the President at low levels, investors have had trouble finding humor in politics, even on April Fool’s Day. Another significant factor more important than politics is the issue of retirement savings by Americans, which is no joke. As you finalize your tax returns in the coming weeks, it behooves you to revisit your retirement plan and investment portfolio. Inefficiently investing your money or outliving your savings is no laughing matter. I’ll continue with my disciplined financial plan and leave the laughing to my kids, as they enjoy planning their next April Fool’s Day prank.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AAPL, FB, AMZN, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}