Posts tagged ‘401k’

Can You Retire? Getting to Your Number

What’s “your number?” The catchy phrase has been tried on 30-second television commercials before, but the fact remains, most Americans have no clue how much they need to save for retirement. The ever-shifting and imprecise variables needed to compute the size of your needed nest egg can seem overwhelming: lifespan; career span; inflation; college tuition; healthcare expenses; rising insurance costs; social security; employer benefits; inheritance; child support; parental support; etc. The list goes on and with near-zero interest rates, and stock prices at record highs, the retirement challenge has only gotten riskier and more difficult.

I understand this task may not be easy and could eat into your House of Cards viewing, Candy Crush playing, or football watching. However, if you can spend two weeks planning a family vacation, you certainly can afford devoting a few hours to scribbling down some numbers as it relates to the lifeblood of your financial future. The project is definitely doable.

Here are some key steps to finding “your number.” If you’re not single, then calculate the figures for your household:

1). Calculate Your Budget: Where to start? A good place to begin is with is a boring budget (or your monthly expenses). The budget does not need to be down to the penny, but you should be able to estimate your monthly spend with the help of your bank and credit card statements. Make sure to include estimates for periodic unforeseen potential expenses like annual auto repairs, home repairs, or emergency hospital visits. Once you determine your monthly spend, extrapolating your annual spend shouldn’t be too difficult.

2). Compute Your Income: Your sources of income should be fairly straightforward. For most people this includes your salary and potential bonus. Some people will also generate income from investments, a business, and/or real estate. Before getting too excited about all the income you are raking in, don’t forget to subtract out taxes collected by Uncle Sam, and include a possible scenario of rising tax rates during your working years. Obviously, the economy can also have a positive or negative impact on your income projections, nevertheless, if you conservatively plan for some potential future setbacks, you will be in a much better position in forecasting the amount of savings needed to reach “your number.”

3). Planned Retirement Date: The date you pick may or may not be realistic, but by choosing a specific date, you can now evaluate how much savings will be necessary to reach your required nest egg number. The difference between your annual income (#2) and annual budget (#1) is your annual savings, which you can multiply by the number of years you plan to work until retirement. For example, assume you wanted to retire 15 years from now and were able to save/invest $20,000 each year while earning a 6% annualized return. By the year 2030 these savings would equate to about $465,000 and could be added to any other savings and other retirement income (pension, 401(k), Social Security, inheritance, etc.) to meet your retirement needs.

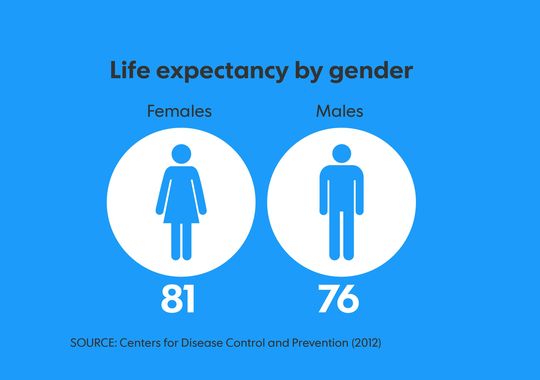

4). Life Expectancy: After you have determined when you want to retire, now comes the tricky part. How long are you going to live? Assuming you are currently healthy, you can use actuarial tables for life expectancy. According to a new report on American mortality from the Centers for Disease Control and Prevention’s National Center for Health Statistics, the average life expectancy is 81 for females and 76 for males (see graphic below). The estimates are a little rosier, if you have lived to age 65, in which case females are expected to live past 85 years old and males to about 83 years. You can adjust these figures higher or lower based on personal information and family history, but if you consider yourself “average,” then you better plan to have at least 15 years of fire power in your savings nest egg (see example at bottom of article).

Source: USA Today

Empty Retirement Wallets & Purses

The harsh realities are Americans are not saving enough. It‘s true, you can survive off a smaller nest egg, if you plan to live off of cat food and vacation in Tijuana, but most Americans and retirees have become accustomed to a higher standard of living. A New York Times article highlighted that 75% percent of Americans nearing retirement age had less than $30,000 in their retirement accounts – that’s not going to buy you that winter home on Maui or leave enough to cover your golf dues at the local country club.

Control the things that make a difference.

- Save. Pay yourself first by tucking money away each month. If you haven’t established an IRA (Individual Retirement Account) or savings account, make sure you contribute to your employer’s matching 401(k) plan to the fullest extent possible, if available. This is free money your employer is offering you and by not participation you are shooting yourself in the foot.

- Spend prudently. Review your monthly / annual budgets and determine where there is room to cut expenses. Every budget has fat in it, so it’s just a matter of cutting excessive and less important items, without sacrificing dramatic changes to your standard of living.

- Manage your career. Invest in yourself with education, apply for that promotion, or look for other employment alternatives if you are unhappy or not being paid your proper value.

- Push Retirement Out: If you are healthy and enjoy your work, extending your working years can have profoundly positive benefits to your retirement. Not only will you have more money saved up for retirement, but you will also receive higher Social Security benefits by delaying retirement (see Social Security benefit estimator).

The bottom-line is if you are like most working Americans, you will need to save more and invest more prudently (e.g., in a low-cost, tax-efficient manner like strategies offered by Sidoxia).

Use Your Thumb to Get Started

Rules of thumb are never perfect, but are not a bad place to start before fine-tuning your estimates. Some retirement pundits begin by using an 80% “income replacement ratio” rule as a retirement guide. In other words, you should not need 100% of your pre-retirement income during retirement because a number of your major living expenses should be reduced. For example, during retirement your tax expenses should decrease (because you are not working); your mortgage payment should be lower (i.e., house is paid off); your kids should be independent and off the family payroll; and you may be in the position to downsize your home (e.g., empty-nesters often decide to move to a lower square footage residence).

Another rule of thumb is the “15x Rule,” which says you will need an investment account equivalent to at least 15-times your pre-retirement income. Therefore, if your after-tax income is $100,000 before retirement and you need to replace $80,000 during retirement (80% replacement ratio), this means you actually only need to replace about $60,000 per year. We arrive at the lower $60,000 figure by further assuming the $80,000 can be reduced by about $20,000 flowing in annually from Social Security. Through the mighty powers of division, we can then apply the 4% Sustainable Withdrawal Rate rule (SWR) to reverse engineer the estimate of “our number.” In this example, our ultimate nest egg needed is $1,500,000 (equal to $60,000 / 4% or $60,000 x 25 years), which is estimated to last for 25 years of retirement. As you can see, there are quite a few assumptions baked into this scenario, including a retirement investment portfolio that beats inflation by 4%, but nevertheless this line of thinking creates an understandable framework to operate under.

Of course, for all the non-math Investing Caffeine readers, life could have been made easier by simply multiplying the $100,000 pre-retirement income by 15x to arrive at our $1.5 million nest egg. More elegant, but less fun for this nerdy math author.

We’ve covered a lot of ground, but I’m absolutely confident if you have read this far, you can definitely come up with “your number.” If this all seems too overwhelming, there is no need to worry, just find an experienced investment advisor or financial planner…I’m sure I could help you find one 🙂 .

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Retirement Epidemic: Poison Now or Later?

We live in an instant gratification society. The house, the car, and annual vacation take precedence over contributions to retirement and savings accounts. It therefore comes as no surprise to me that Americans spend more time on planning for vacation than they do on planning for retirement.

Given the choice of spending or saving, Americans in large part choose, “spend now, save later.” Or in other words, Americans choose to drink $10 margaritas now (spend) and swallow the more expensive poison (save) later. Spending now and saving later sounds good in theory until you reach your mid-60s and realize you’re going to have to work as a Wal-Mart Stores (WMT) greeter into your 80s while eating cat food in your tent.

To make matters worse, you don’t have to be a genius to see irresponsible government spending and globalization has compromised the health of our countries entitlements (Social Security and Medicare). Benefits are likely to be reduced over time and age eligibility requirements are likely to increase. If you fold in the dynamic of exploding healthcare costs and broad-based inflationary pressures, one can quickly realize savings habits need to change. The traditional model of working for 40 years and then relying on a pension and Social Security payments to cover a blissful multi-decade retirement just doesn’t apply to current reality. On top of the disappearance of plump pensions, life expectancy is rising (around 80 years in the U.S.), so the realistic risk of outliving your savings has a larger probability of occurring.

Surely I am overly dramatizing the situation by sounding the investing alarm bells out of self-interest…right? Wrong. As a geeky, financial numbers guy, I can objectively rely on numbers, and the statistics aren’t pretty.

Here’s a sampling:

- Empty Savings Cupboard: A 2013 study by the Employee Benefit Research Institute found that nearly half of workers had less than $10,000 saved, and according to Blackrock Inc (BLK), CEO, Larry Fink, the average American has saved only $25,000 for retirement

- Food Stamp Living: Almost half of middle-class workers, will be forced into a poor retirement lifestyle, living on a food budget of about $5 a day.

- 401(k) Will Not Save the Day: Compared to other forms of savings, the average 401(k) balance reached $89,300 at the end of 2013 – that’s the good news. The bad news is that only about half of all companies offer their employees 401(k) benefits, and for the approximately 60 million people that participate, about a fourth withdraw these 401(k) funds before retirement – out of necessity or for frivolous reasons. Even if you cheerily accept the size of the average balance, sadly this dollar amount is still massively deficient in meeting retirement needs. It’s believed that your savings should approximate 15-20 times your annual retirement expenses that aren’t covered by outside sources of income, such as social security or a pension.

If these figures aren’t scary enough to get you saving more, then just use common sense and understand the future is very uncertain. A 2012 New York Times article sarcastically captured how easy it is to plan for retirement:

First, figure out when you and your spouse will be laid off or be too sick to work. Second, figure out when you will die. Third, understand that you need to save 7 percent of every dollar you earn. (30 percent of every dollar [if you are 55 now].) Fourth, earn at least 3 percent above inflation on your investments, every year. (Easy. Just find the best funds for the lowest price and have them optimally allocated.) Fifth, do not withdraw any funds when you lose your job, have a health problem, get divorced, buy a house or send a kid to college. Sixth, time your retirement account withdrawals so the last cent is spent the day you die.

What to Do?

The short answer is save! Simplistically, this can be achieved in one of two ways: cut expenses or raise income. I won’t go into the infinite ways of doing this, but adjusting your mindset to live within your means is probably the first necessary step for most.

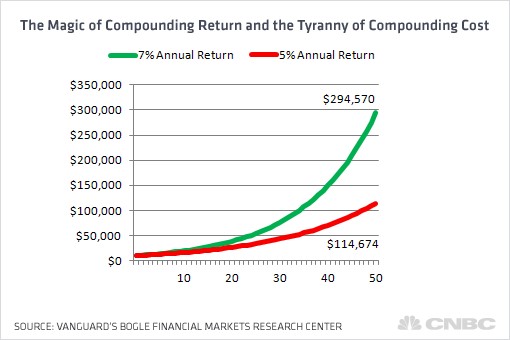

As it relates to your investments, fees should be your other major area of focus. The godfather of passive investing, Jack Bogle, highlighted the dramatic impact of fees on retirement savings. As you can see from the chart below, the difference between making 7% vs. 5% over an investing career by reducing fees can equate to hundreds of thousands of dollars, and prevent your nest egg from collapsing 2/3rd in value.

Source: CNBC

Lastly, if you are going to use an investment advisor, make sure to ask the advisor whether they are a “fiduciary” who legally is required to place your interests first. Sidoxia Capital Management is certainly not the only fiduciary firm in the industry, but less than 10% of advisors operate under this gold standard.

Investing and saving is a lot like dieting…easy to understand the concept but difficult to execute. The numbers speak for themselves. Rather than dealing with a crisis in your 70s and 80s, it’s better to take your poison now by investing, and reap the rewards of your hard work during your golden years.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds (ETFs), and WMT, but at the time of publishing SCM had no direct discretionary position in BLK, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Stock Market: Shrewd Bet or Stupid Gamble?

Trillions of dollars have been lost and gained over the last five years. The extreme volatility strangled investment portfolios, and as a result millions of investors capitulated by throwing in the towel and locking in losses. Melted 401ks, shrunken IRAs, and beat-up retirement accounts bruised the overarching psyche of Americans to the point they questioned whether the stock market is a shrewd bet or stupid gamble?

The warmth and safety of bonds provided some temporary relief in subsequent years, but the explosive rebound in stock prices to new record highs in 2013 coupled with the worst year in a decade for bonds still have many on the sidelines asking whether they should get back in?

As I’ve written many times in the past (see Timing Treadmill), timing the market is a fruitless effort. Elementary statistics, including the “Law of Large Numbers” will demonstrate that blind squirrels can and will beat the market on occasion, but very few can consistently beat the stock market indices for sustained periods (see Dart-Throwing Chimps).

However, there have been some gun-slinging hedge fund managers who have accumulated some impressive track records. Because of insanely high management fees, many overpaid hedge fund managers will swing for the fences by using a combination of excessive leverage and/or concentration. If the hedge funds connect with lucky returns, the managers can take the money and run. If they swing and miss…no problem. Close shop, hang out a shingle across the street, change the hedge fund’s name, and try again. Of course there are those successful hedge fund managers who have learned how to manipulate the system and exploit information to their advantage, but many of those managers like Raj Rajaratnam and Steven Cohen are either behind bars or dealing with the Feds (see fantastic Frontline piece on Cohen).

But not everyone cheats. There actually are a minority of managers who consistently beat the market by taking a long-term approach like Warren Buffett. Long-term outperforming managers are like lifetime .300 hitters in Major League Baseball – the outperformers exist, but they are rare. In 2007, AssociatedContent.com did a study that showed there were only 12 active career .300 hitters in Major League Baseball.

Another legend in the investment industry is John Bogle, the founder of the Vanguard Group, a firm primarily focused on passive, index-based investment strategies. Although it is counter-intuitive to most, just matching the market (or index) will put you in the top-quartile over the long-run (see Darts, Monkeys & Pros). There’s a reason Vanguard manages more than $2,000,000,000,000+ (yes…trillion) of investors’ money. Even at this gargantuan size, Vanguard remains a fraction of the overall industry. Regardless, the gospel of low-cost, tax-efficient, long-term horizons is slowly leaking out to the masses (Disclosure: Sidoxia is a devoted user of Vanguard and other providers’ low-cost Exchange Traded Funds [ETFs]).

Rolling the Dice?

Unlike Las Vegas, where the odds are stacked against you, in the stock market the odds are stacked in your favor if you stay in the game long enough and don’t chase performance. Dr. Ed Yardeni has a great chart (below) summarizing stock market returns over the last 85 years, and what the data highlights is that the market is up (or flat) 69% of the time (59/86 years). The probabilities are so favorable that if I got comparable odds in Vegas, I’d probably live there!

Source: Dr. Ed’s Blog

Unfortunately, rather than using this time arbitrage in conjunction with the incredible power of compounding (see A Penny Saved is Billions Earned), many individuals look at the stock market like a casino – similarly to betting on black or red at a roulette wheel. Speculating about the direction of the market can be fun, and I’ve been known to guess on occasion, but it’s a complete waste of time. Creating a long-term plan of reaching or maintaining your retirement goals through a diversified portfolio is the way to go – not bobbing in out of the market with cash and bonds.

At Sidoxia, we don’t actively trade and time individual stocks either. For the majority of our client portfolios, we follow a growth philosophy similar to the late T. Rowe Price:

“The growth stock theory of investing requires patience, but is less stressful than trading, generally has less risk, and reduces brokerage commissions and income taxes.”

Nobody knows the direction of the stocks with certainty, and irrespective of whether the market goes down this year or not, history has proven the stock market has been a shrewd, long-term bet.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Avoid Chasing Your 401k Tail

David Laibson, a professor of economics at Harvard University, has done extensive research on the savings habits of Americans in their 401k retirement accounts. What he discovers is that workers, like a dog chasing their tail, allocate more of their investments to the areas that have done well and sell the underperforming segments. In short, workers attempt to “time the market.”

Professor Laibson demonstrates this pyramiding strategy has not worked out so well and provides the following advice:

“We know that individual investors are terrible in terms of their market timing. They tend to buy at the tops, they tend to sell at the bottoms. So don’t try to time the market. Don’t think about recouping – just think about a long term strategy.”

That long term strategy he advocates entails a diversified allocation of stocks and bonds that reduces exposure to equities as a person gets older. In short, he says, “Hold a diversified portfolio appropriate for your age.”

He advises those aged in their 20s and 30s to allocate nearly 100% of their portfolio to equities, or investments with commensurate risk. Alternatively, if investors don’t want to adjust the allocation themselves, people should consider life-cycle funds or Self Directed 401k options (Read story here). For those in retirement, he recommends a portfolio with the following characteristics:

“30, 40, 50% should be equities, more as you’re younger…simply hold a long term portfolio with less and less allocation to equities as you age.”

Jason Zweig, a journalist at The Wall Street Journal, recently chimed in with similar thoughts on performance chasing:

“…to buy more of what has gone up, precisely because it has gone up, is to fall for the belief that stocks become safer as their prices rise. That is the same fallacy that led investors straight into disaster in 1929, 1972, 1999, 2007 and every other market bubble in history.”

There are many different strategies for making money in the market, but a plan based solely on emotion is doomed for failure – Professor Laibson’s data supports that assertion. So the next time you are considering re-allocating the mix of investments in your 401k, implement a disciplined, systematic approach. That approach should include the following:

1) Invest Your Age in Fixed Income Securities. John Bogle, Chairman at Vanguard Group, has long made this argument, with the balance placed in equities. For example a sixty year old should have 60% of their assets in bonds and 40% in stocks. This rule of thumb is a good starting point, but the picture becomes cloudier once you account for other assets such as real estate, convertible bonds, and income generated from private businesses.

2) Periodically Rebalance. Rather than investing more into outperforming areas, harvest your gains and redeploy into underperforming segments of your asset allocation. There obviously is an art to knowing “when to hold them and when to fold them,” nonetheless I concur with Professor Laibson that chasing winners is not the proper strategy.

3) Diversify. Spread your assets across multiple asset classes, segments, and styles, including equities, fixed income, commodities, real estate, inflation protection, growth, value, etc. Too much concentration in any one category can really come back to haunt you.

The key to successful retirement planning is to implement an unemotional systematic approach, so you don’t end up chasing your 401k tail.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: At the time of publishing, Sidoxia Capital Management and some of its clients owned certain exchange traded funds, but had no direct positions in any other security referenced.

Mountains of Cash Starting to Trickle Back

The month of July was an interesting month because investors opened their 401k and investment statements for the first time in a long while to notice an unfamiliar trend… account values were actually up. Like a child that has burnt their hand on a stove, the wounds and memories are still too fresh – more time must pass before investors decide to get back into the market in full force.

As you can see from the charts below, as investors globally panicked throughout 2008 and early 2009, money earning next to nothing in CDs and Money Market accounts was stuffed under the mattress in droves. The fear factor of last fall has caused current liquid assets to stand near 10 year highs at a level near 120% of the S&P 500 total market capitalization (Thomson Reuters) and at more extreme levels last fall if you just look at Money Market assets (bottom chart) . Now that the Armageddon scenario has been temporarily put to rest, we’re starting to see some of that cash to trickle back into the market. The silver lining is that there is still plenty of dry powder left to drive the market higher – not overnight, but once sustained confidence returns. If the earnings outlook continues to improve, come the beginning of October when 3rd quarter statements arrive in the mail, the pain of not being in the market will overwhelm the fear of burning another hand on the stove like in 2008.

It is funny how the sentiment pendulum can swing from the grips of despair a year ago. There is still headroom for the market to climb higher before the pendulum swings too far in the bullish direction – if you don’t believe me just look on the horizon at the mountain of cash.

Source: SentimenTrader.com (Fall 2008)

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

You and Your 401K are Not Alone

You have choices when it comes to managing your 401k.

A large majority of individual investors watched their 401k retirement accounts crater throughout 2008 and the beginning of 2009. For some, prudently managing these accounts, while attempting to decipher historic, unimaginable events, proved to be a difficult challenge. Fortunately for investors there are alternatives beyond managing a narrow 401k menu of options by yourself.

One option to consider is the establishment of a Self Directed 401k account, sometimes called a Self Directed Brokerage Account (SDBA). This is an option offered by a minority of plan sponsors (employers) to their employees, so make sure to ask your human resources department if you are interested in exploring this selection. By opening a separate Self Directed 401k account at a third party brokerage firm the investor should have access to a broader set of investment options relative to traditional 401k offerings. The retirement plan documents may however limit investment choices to certain investment products, in part due to litigation concerns created by potentially poor plan participant decisions. Increased trading and administrative charges are other potential costs to mull over.

Opening up one of these self directed accounts also avails a 401k investor to work with an outside advisor who can assist with managing the external brokerage account. Of course, nothing in life comes for free, so the individual will be paying the advisor for these services rather than managing the account solo.

Instead of creating a whole new external Self Directed account, 401k investors can also hire companies for personal 401k management advice in their existing accounts. One such firm, Financial Engines, made famous by its academic all-star founder Bill Sharpe, provides advice to investing participants for a fee, based on the dollar value of the account.

Financial Engines claims to work with more than 750 large employers (including 112 of the FORTUNE 500 and 8 of the FORTUNE 20) and 8 of the largest retirement plan providers serving the retirement market. The problem with services like these (including Guided Choice, also a brainchild of a finance guru – Harry Markowitz) is that no matter how great the advice may be, the investor is stuck with the limited investment options provided by the employer on the 401k company menu.

Other players in the financial industry are swirling around to advise participants on a piece of this $3 trillion 401k U.S. retirement asset market (ICI 2007 estimate), including some brokerage and mutual fund companies, and even independent financial planners. Also, don’t forget if you ever leave an employer, you have the ability to roll over your 401k account into a personal IRA (Individual Retirement Account) – an account you fully control with a buffet of options.

Regardless of the money you may have lost or the amount of confusion you feel, realize that you are not alone (if you choose not to be). Make sure to contact the appropriate human resource professional in charge of retirement benefits, and discover your 401k options.

{kind=link}