Posts tagged ‘Peter Lynch’

You Can’t Kiss All the Beauties

When I was in high school and college, kissing all the pretty girls was not a realistic goal. The same principle applies to stock picking – you can’t buy all the outperforming stocks. As far as I’m concerned, there will always be some people who are smarter, better looking, and wealthier than I am, but that has little to do with whether I can continue to outperform, if I stick to my systematic, disciplined process. In fact, many smart people are horrible investors because they overthink the investing process or suffer from “paralysis by analysis.” When it comes to investing, the behavioral ability to maintain independence is more important than being a genius. If you don’t believe me, just listen to arguably the smartest investor of all-time, Warren Buffett:

“Success in investing doesn’t correlate with I.Q. once you’re above the level of 125. Once you have ordinary intelligence, what you need is the temperament to control the urges that get other people into trouble in investing.”

Even the best investors and stock pickers of all-time are consistently wrong. When selecting stocks, a worthy objective is to correctly pick three outperforming stocks out of five stocks. And out of the three winning stocks, the rationale behind the outperformance should be correct in two out of those three stocks. In other words, you can be right for the wrong reason in one out of three outperforming stocks. The legendary investor Peter Lynch summed it up when he stated, “If you’re terrific in this business you’re right six times out of 10.”

Yes, it’s true, luck does play a role in stock selection. You just don’t want luck being the major driving force behind your success because luck cannot be replicated consistently over the long-run. There are so many unpredictable variables that in the short-run can work for or against the performance of your stock. Consider factors like politics, monetary policy, weather, interest rates, terrorist attacks, regulations, tax policy, and many other influences that are challenging or impossible to forecast. Over the long-run, these uncontrollable and unpredictable factors should balance out, thereby allowing your investing edge to shine.

Although I have missed some supermodel stocks, I have kissed some pretty stocks in my career too. I wish I could have invested in more stocks like Amazon.com Inc. (AMZN) that have increased more than 10x-fold, but other beauties like Apple Inc. (AAPL), Alphabet Inc. (GOOG), and Facebook Inc. (FB), haven’t hurt my long-term performance either. As is the case for most successful long-term investors, winning stocks generally more than compensate for the stinkers, if you can have the wherewithal to hold onto the multi-baggers (i.e., stocks that more than double), which admittedly is much easier said than done. Peter Lynch emphasized this point by stressing a focus on the long-term:

“You don’t need a lot of good hits every day. All you need is two to three goods stocks a decade.”

Sticking to a process of identifying and investing in well-managed companies at attractive valuations is a much better approach to investing than chasing every beauty you see or read about. If you stick to this simple formula, you can experience lovely, long-term results.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AAPL, FB, GOOG, AMZN, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Stocks: Be My Long-Term Valentine

With Valentine’s Day just around the corner, stock bulls remain in love as the major indexes once again hit another new, all-time record high this week (Dow 20,269). Unfortunately, however, there are many other investors afraid of going through another 2008-2009-like break-up, so they remain single as they watch from the sidelines. In a recent post, I point out, as repeated record highs continue to be broken, the skeptics remain fearful of divorcing their cash. While it is indeed true that since the end of the 2016 presidential election, some investors are beginning to date stocks again, there are still wide swaths of conflicted observers very afraid of potential rejection.

As I’ve documented on numerous occasions, the skepticism is evident in the depressing long-term trends found in the weekly fund flows data and the disheartening record-low stock ownership statistics.

Long-Term Relationships

For some, casually dating can be fun and exciting. The same principle applies to short-term traders and speculators. In the short-run, the freedom to make free-wheeling, non-committal stock purchases can be exhilarating. Unfortunately, the fiscal and emotional costs of short-term dating/trading often outweigh the fleeting benefits.

How can you avoid the relationship blues? In short…focus on the long-term. Like any relationship, investing takes work, and there will always be highs, lows, and bumps in the road. It is better to think in terms of a marathon, rather than a sprint. The important lesson is to maintain a systematic, disciplined approach that you can apply irrespective of the changing investment environment. In other words, that means not loosely reacting (buying or selling) to presidential tweets of the day.

Famed investor Peter Lynch spoke about long-term stock fund investing in this manner

“If you invest in mutual funds and make mutual funds investment changes in less than 10 years…you’re really just ‘dating.’ Investing in mutual funds should be marital – for richer, for poorer, and so on; mutual fund decisions should be entered into soberly and advisedly and for the truly long term.”

No relationship survives without experiencing wild swings, and stocks are no exception. Establishing deep roots to your investments via intensive fundamental analysis provides stability, especially if you are managing your portfolio personally. Even if you are outsourcing your investment management to an advisor like Sidoxia Capital Management, it is still important to understand your advisor’s investment process and philosophy. That way, when the economic and political winds are blowing fiercely, you won’t overreact emotionally and see your gains fly away.

Investing legend Warren Buffett has discussed the importance of intensive research on long-term investment performance through his “20-Hole Punch Card” rule:

“I could improve your ultimate financial welfare by giving you a ticket with only twenty slots in it so that you had twenty punches – representing all the investments that you got to make in a lifetime. And once you’d punched through the card, you couldn’t make any more investments at all. Under those rules, you’d really think carefully about what you did, and you’d be forced to load up on what you’d really thought about. So you’d do so much better.”

Patience is a Virtue

In the instant gratification society we live in, patience is difficult to come by, and for many people ignoring the constant chatter of fear is challenging. Pundits spend every waking hour trying to explain each blip in the market, but in the short-run, prices often move up or down regardless of the daily headlines.

Explaining this randomness, Peter Lynch said the following:

“Often, there is no correlation between the success of a company’s operations and the success of its stock over a few months or even a few years. In the long term, there is a 100% correlation between the success of a company and the success of its stock. It pays to be patient, and to own successful companies.”

Long-term investing, like long-term relationships, is not a new concept. Investment time horizons have been shortening for decades, so talking about the long-term is generally considered heresy. Rather than casually dating your investments, perhaps you should commit to a long-term relationship and divorce your bad short-term centric habits. Now that sounds like a sweet Valentine’s Day kiss your investment portfolio would enjoy.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AAPL, T, FB and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Dow 20,000 – Braking News or Breaking News?

Investors from around the globe excitedly witnessed the Dow Jones Industrial Average index break the much-anticipated 20,000 level and set a new all-time record high this week. The question now becomes, is this new threshold braking news (time to be concerned) or breaking news (time to be enthused)? The true answer is neither. While the record 20,000 achievement is a beautifully round number and is responsible for a bevy of headlines splashing around the world, the reality is this artificial 20,000 level is completely arbitrary.

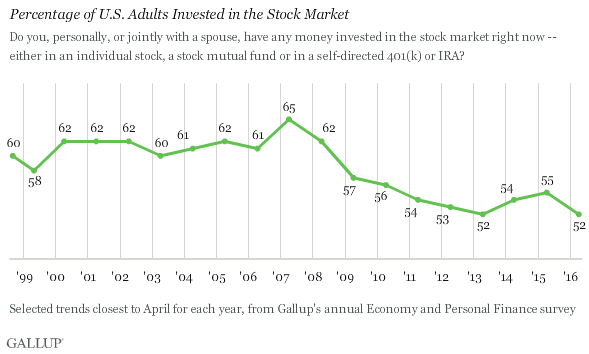

Time will tell whether this random numeric value will trigger the animal spirits of dispirited investors, but given all the attention, it is likely to jolt the attention span of distracted, ill-prepared savers. Unfortunately, the median family has only saved a meager $5,000 for retirement. For some years now, I have highlighted that this is the most hated bull market (see The Most Hated Bull Market Ever), and Gallup’s 2016 survey shows record low stock ownership, which also supports my view (chart below). Trillions of dollars coming out of stock funds is additional evidence of investors’ sour mood (see fund outflow data).

While investors have been selling stocks for years, record corporate profits, trillions in share buybacks, and trillions of mergers and acquisitions (in the face of a weak IPO market) have continually grinded stock prices to new record highs.

Pessimism Sells

The maligned press (deservedly so in many instances) has been quick to highlight a perpetual list of dread du jour. The daily panic-related topics do however actually change. Some days it’s geopolitical concerns in the Middle East, Russia, South China Sea, North Korea, and Iran and other days there are economic cries of demise in China, Brazil, Venezuela, or collapse in the Euro. And even when the economy is doing fine (unemployment rate chopped in half from 10%, near full employment), the media and talking heads often supply plenty of airtime to impending spikes of crippling inflation or Fed-induced string of choking interest rate increases.

I fondly look back on my articles from 2009, and 2010 when I profiled schlocks like Peter Schiff (see Emperor Schiff Has No Clothes) who recklessly peddled catastrophe to the masses. I guess Schiff didn’t do so well when he called for the NASDAQ to collapse to 500 (5,660 today) and the Dow to reach 2,000 (20,000 today).

Or how about the great forecaster John Mauldin who also piled onto death and destruction near the bottom in 2009 (see The Man Who Cries Wolf ). Here’s what Mauldin had to say:

“All in all, the next few years are going to be a very difficult environment for corporate earnings. To think we are headed back to the halcyon years of 2004-06 is not very realistic. And if you expect a major bull market to develop in this climate, you are not paying attention.” … “We are going to pay for that with a likely dip back into a recession.”

At S&P 856 (2,295 today) Mauldin added:

“This rally has all the earmarks of a major short squeeze…When the short squeeze is over, the buying will stop and the market will drop. Remember, it takes buying and lot of it to move a market up but only a lack of buying to create a bear market.”

Nouriel Roubini a.k.a. “Dr Doom” was another talking head who plastered the airwaves with negativity after the 2008-2009 financial crisis that I also profiled (see Pinning Down Roubini). For example, in early 2009, here’s what Roubini said:

“We are still only in the early stages of this crisis. My predictions for the coming year, unfortunately, are even more dire: The bubbles, and there were many, have only begun to burst.”

For long-term investors, they understand the never-ending doom and gloom headlines are meaningless noise. Legendary investor Peter Lynch pointed on on numerous occasions:

“If you spend more than 13 minutes analyzing economic and market forecasts, you’ve wasted 10 minutes.”

(see also Peter Lynch video)

The good news is all the media pessimism and investor skepticism creates opportunities for shrewd investors focusing on key drivers of stock price appreciation (corporate earnings, interest rates, valuations, and sentiment).

While the eternally, half-glass full media is quick to highlight the negatives, it’s interesting that it takes an irrelevant, arbitrary level to finally create a positive headline for a new all-time record high of Dow 20,000. Frustratingly, the new all-time record highs reached by the Dow in 2013, 2014, 2015, and 2016 were almost completely ignored (see chart below):

Source: Barchart.com

What happens next? Nobody knows for certain. What is certain however is that using the breaking news headlines of Dow 20,000 to make critical investment decisions is not an intelligent long-term strategy. If you, like many investors, have difficulty in sticking to a long-term strategy, then find a trusted professional to help you create a systematic, disciplined investment strategy. Now, that is some real breaking news.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Sweating Your Way to Investment Success

There are many ways to make money in the financial markets, but if this was such an easy endeavor, then everybody would be trading while drinking umbrella drinks on their private islands. I mean with all the bright blinking lights, talking baby day traders, and software bells and whistles, how difficult could it actually be?

Unfortunately, financial markets have a way of driving grown men (and women) to tears, usually when confidence is at or near a peak. The best investors leave their emotions at the door and follow a systematic disciplined process. Investing can be a meat grinder, but the good news is one does not need to have a 90% success rate to make it lucrative. Take it from Peter Lynch, who averaged a +29% return per year while managing the Magellan Fund at Fidelity Investments from 1977-1990. “If you’re terrific in this business you’re right six times out of 10,” says Lynch.

Sweating Way to Success

If investing is so tough, then what is the recipe for investment success? As the saying goes, money management requires 10% inspiration and 90% perspiration. Or as strategist and long-time investor Don Hays notes, “You are only right on your stock purchases and sales when you are sweating.” Buying what’s working and selling what’s not, doesn’t require a lot of thinking or sweating (see Riding the Wave), just basic pattern recognition. Universally loved stocks may enjoy the inertia of upward momentum, but when the music stops for the Wall Street darlings, investors rarely can hit the escape button fast enough. Cutting corners and taking short-cuts may work in the short-run, but usually ends badly.

Real profits are made through unique insights that have not been fully discovered by market participants, or in other words, distancing oneself from the herd. Typically this means investing in reasonably priced companies with significant growth prospects, or cheap out-of-favor investments. Like dieting, this is easy to understand, but difficult to execute. Pulling the trigger on unanimously hated investments or purchasing seemingly expensive growth stocks requires a lot of blood, sweat, and tears. Eating doughnuts won’t generate the conviction necessary to justify the valuation and excess expected return for analyzed securities.

Times Have Changed

Investing in stocks is difficult enough with equity fund flows hemorrhaging out of investor accounts like the asset class is going out of style. Stocks’ popularity haven’t been helped by the heightened volatility, as evidenced by the multi-year trend in the schizophrenic volatility index (VIX) – escalated by the international geopolitics and presidential elections. Globalization, which has been accelerated by technology, has only increased correlations between domestic market and international markets. In decades past, concerns over economic activity in Iceland, Dubai, and Greece may not even make the back pages of The Wall Street Journal. Today, news travels at the speed of a “Tweet” and eventually results in a sprawling front page headline.

The equity investing game may be more difficult today, but investing for retirement has never been more important. Stuffing money under the mattress in Treasuries, money market accounts, CDs, or other conservative investments may feel good in the short run, but will likely not cover inflation associated with rising fuel, food, healthcare, and leisure costs. Regardless of your investment strategy, if your goal is to earn excess returns, you may want to check the moistness of your armpits – successful long-term investing requires a lot of sweat.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in ETFC, VXX, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Growth Stocks – Cheaper by the Day

Are you a value investor? If you said “yes,” how would you feel about buying an $18 stock with a P/E (Price/Earnings) ratio of greater than 100x and a Price/Sales ratio of 14x for a company that three years earlier was started in a garage? This may not sound like a value stock, but had you bought this stock at the initial public offering (IPO), it would have been a screaming bargain – priced at less than 1x P/E ratio, based on this year’s earnings estimates.

You may be surprised to know, this company with a meager $18 IPO share price is now worth $9,192 per share today (if you adjust for three stock splits)! Yes, that’s correct, a +50,900% return. If you are wondering to which stock I’m referring, I am talking about Amazon.com Inc. (AMZN). Incredibly, ever since Amazon went public in 1997, the CEO Jeff Bezos has managed to command the start-up e-commerce company from $31 million in revenues to $121 billion (with a “b”) on an annual basis in 2016 (a +389,000% increase).

Discovering the next IPO that turns into a $363 billion behemoth is easier said than done, and unfortunately these types of companies are a rare breed. Even if you are lucky enough to identify these diamonds-in-the-rough, early in their growth cycle, very few investors have the fortitude and discipline to continually own the stocks through the perpetual volatility (i.e., peaks and valleys).

The good news is, although you may be unable to find every unicorn out there, you can still apply the same principles and characteristics to any growth stock you invest in. In order to prudently achieve outsized returns, one must identify innovative market leaders that have gained some type of sustainable competitive advantage, which will serve as the profit and cash flow growth engine for the stock over the long-term.

If a company does not have a unique advantage over industry competitors, they will likely be unable to compound earnings growth – the key to becoming a big winner. Albert Einstein, Nobel Prize winner is credited with identifying compounding as the “eighth wonder of the world,” and without compounding there will be no gigantic results.

Amazon may be a rare breed, but there are plenty of other examples of so-called “expensive” stocks that get dismissed or fall through the cracks as they explode in value to the stratosphere. Consider Starbucks Corp. (SBUX), which at the time of its IPO in 1992 was priced at a very rich P/E of 52x. Sound expensive? Actually, this was a greatest offer in a generation. Adjusted for stock splits, the IPO shares were valued at $0.27 – in the most recent trading session Starbucks shares closed at $55.90, a +20,600% increase. Similar to Amazon, had you purchased Starbucks shares at the IPO price, you would have been paying less than a measly, eye-popping 1x P/E ratio based on 2016 earnings.

Alphabet Inc. (GOOGL), formerly Google Inc., is another case of growth stock appearing pricey on the outside, but really a value of a lifetime on the inside. The hype surrounding the Google IPO was so palpable in 2004, the stock priced at a relatively nose-bleed level of 60x P/E level, approximately. The unconventional auction bidding method to buy the initial shares made investors even more skeptical. Suffice it to say, the greater than +1,600% gain has once again shown that investors can reap handsome rewards, if they do thorough enough due diligence and ignore the illusory big ticket IPO prices.

What most investors fail to realize is that P/E ratios are temporary. By purchasing a growth stock, the numerator of the P/E ratio (price) becomes static or fixed. As earnings of a growth company expand, the stock becomes cheaper by the day. More specifically, the numerator of the P/E (price) is flat, while the denominator (earnings) grows, thereby making the P/E ratio smaller (cheaper). And as you can see from the few previous examples I have provided, if you are able to identify winners, and hold them long enough, you will eventually realize the initial hefty price tag at purchase will be considered almost free after all the earnings compounding.

Legendary growth investor Peter Lynch summed it up concisely when he noted, “People concentrate too much on the P, but the E really makes the difference.” Lynch goes on to highlight the importance of patience in growth investing because stocks often go down or move sideways for long periods of time before dramatic increases occur:

“My best stocks performed in the 3rd year, 4th year, 5th year, not in the 3rd week or 4th week.”

I’ve illustrated a few successful examples of meteoric growth stocks, but more importantly the misconception many investors place on the current P/E ratio. There still is no substitute for hard-nosed, detailed fundamental research for finding big growth winners, because true growth stocks bought and held for a long enough period, will become cheaper by the day. If you don’t have the time, discipline, or patience to execute this winning strategy, find and hire an experienced investment manager who understands these concepts.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), AMZN, and GOOGL, but at the time of publishing had no direct position in SBUX, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Brexit-Schmexit

Do you remember the panic-inducing headlines related to PIIGS, Crimea, Ebola, Cyprus, and the Flash Crash? Probably not. But if you do remember, these false alarms have likely been relegated to the financial memory graveyard, along with the many other sensationalist news events that have been killed off in the post-financial crisis era. Time will tell whether Brexit dies off or becomes a resurrected concern, like the repeating fears of a China slowdown or Greek collapse. Regardless, as the S&P 500 stock index reaches new all-time record highs, investors are currently shrug off the noise while muttering, “Brexit-Schmexit.”

Individuals have tried to use scary headlines as a timing tool to consistently time market corrections for all of recorded history. Unfortunately, emotional, knee-jerk reactions to alarming news stories rarely is the best strategy. Famed fund manager Peter Lynch said it best when he noted,

“Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.”

Having invested for some 25 years, experience has taught me not only is conventional wisdom often wrong, but it also is frequently an accurate contrarian indicator. In other words, frightening news often should be an indicator to buy…not sell. Case in point is the U.K. European Union referendum. The Brexit referendum “Leave” vote caught virtually everyone by surprise, but the rebound in stock prices to new record highs may be even more surprising to most observers. However, for investors following the key factors of interest rates, profits, valuation, and sentiment (see also Don’t Be a Fool, Follow the Stool), may not be shocked by the positive price action.

- Interest Rates: For starters, you don’t have to be a genius to realize that stocks become more attractive when there is a scarcity of investment alternatives. When there are an estimated $13 trillion of negative interest rate bonds, a layman can quickly understand a 2%, 3%, or 4% dividend yield offered on certain stocks (and funds) can represent a much more attractive opportunity. With interest rates at record lows (see chart below), the overall dividend yield of stocks has provided a floor for stock prices and has limited the depth and duration of sell-offs and corrections.

Source: Calafia Beach Pundit

- Profits: Corporate profits are near record highs but have been sluggish due to several factors, including the negative impact of the strong dollar on multinational exports; the depressing effect of declining interest rates on the banking sector’s net interest profit margins; the general decline in oil and commodity prices; and general lethargic economic growth overall in international markets (emerging and developed economies). Encouragingly, a stabilization in the value of the U.S. dollar, along with a rebound in energy prices augurs well for a potential shift back to earnings growth in the coming quarters.

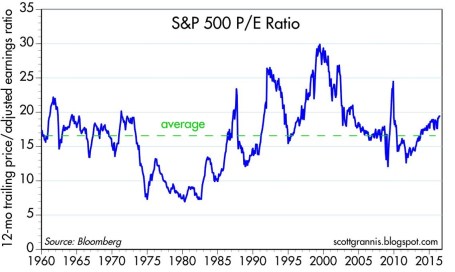

- Valuation: On a valuation basis, the Price/Earnings ratio of the stock market is about 10-15% above historical averages (see chart below). The average S&P 500 stock price trades around 19x’s the value of trailing twelve-month earnings. However, in the context of all-time record low-interest rates, a premium valuation is well deserved, especially for those companies paying a dividend and growing their bottom line.

Source: Calafia Beach Pundit

- Sentiment: Since the Great Financial Crisis / Recession, there has been about $1.5 trillion in equity investments that have been pulled out of U.S. equity mutual funds. This statistic is a clear sign of the extreme risk aversion and pervasive pessimism. Despite money flowing out of equity funds, corporations have bolstered the upward trajectory in stock prices with hundreds of billions in corporate stock buybacks and trillions in mergers & acquisition transactions. With all the universal jitteriness, I like to remind investors of Warren Buffett’s credo, “Buy fear, and sell greed.”

Brexit-Schmexit NOT Brexit-Panic

Despite the risk aversion in the marketplace, stock prices in the U.S. continue to grind higher to record levels. The stock market is currently communicating interest rates, profits, valuation, and sentiment are more important factors to price direction than are Brexit and other geopolitical concerns.

The silver lining behind severe investor skepticism is the creation of additional investment opportunities. As famous investor Sir John Templeton stated regarding stock market cycles, “Bull markets are born on pessimism and they grow on skepticism, mature on optimism, and die on euphoria.” Even the most objective observers have difficulty pointing to a broad set of indicators signaling euphoria, and the recent Turkish military coup attempt and domestic gun violence incidents will not squash out the negativity. Until optimism and elation rule the day, there’s no need to worry-schworry.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds , but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Avoiding Cigarette Butts

Too many investors hang their hat on investments that seem “cheap”. Unfortunately, too often something that looks like a bargain turns out to be a cigarette butt from which investors are hoping to take a last puff. As the old adage states, “you get what you pay for,” and that certainly applies to the world of investments. There are endless examples of cheap stocks getting cheaper, or in other words, stocks with low price/earnings ratios going lower. Stocks that appear cheap today, in many cases turn out to be expensive tomorrow because of deteriorating or collapsing profitability.

For instance, take Haliburton Company (HAL), an energy services company. Wall Street analysts are forecasting the Houston, Texas based oil services company to achieve 2016 EPS (earnings per share) of $0.32, down -79%. The share price currently stands at $37, so this translates into an eye-popping valuation of 128x P/E ratio, based on 2016 earnings estimates. What has effectively occurred in the HAL example is earnings have declined faster than the share price, which has caused the P/E to go higher. If you were to look at the energy sector overall, the same phenomenon is occurring with the P/E ratio standing at a whopping 97x (at the end of Q1).

These inflated P/E ratios are obviously not sustainable, so two scenarios are likely to occur:

- The price of the P/E (numerator) will decline faster than earnings (denominator)

- AND/OR

- The earnings of the P/E (denominator) will rise faster than the price (numerator)

Under either scenario, the current nose-bleed P/E ratio should moderate. Energy companies are doing their best to preserve profitability by cutting expenses as fast as possible, but when the product you are selling plummets about -70% in 18 months (from $100 per barrel to $30), producing profits can be challenging.

The Importance of Price (or Lack Thereof)

Similarly to the variables an investor would consider in purchasing an apartment building, “price” is supreme. With that said, “price” is not the only important variable. As famed investor Warren Buffett shrewdly notes, the quality of a company can be even more important than the price paid, especially if you are a long-term investor.

“It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.”

The advantage of identifying and owning a “wonderful company” is the long-term stream of growing earnings. The trajectory of future earnings growth, more than current price, is the key driver of long-term stock performance.

Growth investor extraordinaire Peter Lynch summed it up well when he stated,

“People Concentrate too much on the P, but the E really makes the difference.”

Albert Einstein identified the power of “compounding” as the 8th Wonder of the World, which when applied to earnings growth of a stock can create phenomenal outperformance – if held long enough. Warren Buffett emphasized the point here:

“If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes. Put together a portfolio of companies whose aggregate earnings march upward over the years, and so also will the portfolio’s market value.”

Throw Away Cigarette Butts

I have acknowledged the importance of aforementioned price, but your investment portfolio will perform much better, if you throw away the cigarette butts and focus on identifying market leading franchise that can sustain earnings growth. The lower the growth potential, the more important price becomes in the investment question. (see also Magic Quadrant)

Here are the key factors in identifying wining stocks:

- Market Share Leaders: If you pay peanuts, you usually get monkeys. Paying a premium for the #1 or #2 player in an industry is usually the way to go. Certainly, there is plenty of money to be made by smaller innovative companies that disrupt an industry, so for these exceptions, focus should be placed on share gains – not absolute market share numbers.

- Proven Management Team: It’s nice to own a great horse (i.e., company), but you need a good jockey as well. There have been plenty of great companies that have been run into the ground by inept managers. Evaluating management’s financial track record along with a history of their strategic decisions will give you an idea what you’re working with. Performance doesn’t happen in a vacuum, so results should be judged relative to the industry and their competitors. There are plenty of incredible managers in the energy sector, even if the falling tide is sinking all ships.

- Large and/or Growing Markets: Spotting great companies in niche markets may be a fun hobby, but with limited potential for growth, playing in small market sandboxes can be hazardous for your investment health. On the other hand, priority #1, #2, and #3 should be finding market leaders in growth markets or locating disruptive share gainers in large markets. Finding fertile ground on long runways of growth is how investors benefit from the power of compound earnings.

- Capital Allocation Prowess: Learning the capital allocation skillset can be demanding for executives who climb the corporate ladder from areas like marketing, operations, or engineering. Regrettably, these experiences don’t prepare them for the ultimate responsibility of distributing millions/billions of dollars. In the current low/negative interest rate environment, allocating capital to the highest return areas is more imperative than ever. Cash sitting on the balance sheet earning 0% and losing value to inflation is pure financial destruction. Conservatism is prudent, however, excessive piles of cash and overpaying for acquisitions are big red flags. Managers with a track record of organically investing in their businesses by creating moats for long-term competitive advantage are the leaders we invest in.

Many so-called “value” investors solely use price as a crutch. Anyone can print out a list of cheap stocks based on Price-to-Earnings, Enterprise Value/EBITDA, or Price/Cash Flow, but much of the heavy lifting occurs in determining the future trajectory of earnings and cash flows. Taking that last puff from that cheap, value stock cigarette butt may seem temporarily satisfying, but investing into too many value traps may lead you gasping for air and force you to change your stock analysis habits.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in HAL or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Chasing Headlines

It’s been an amazing start to the year. First the market cratered on slowing China economic concerns, domestic recessionary fears, deteriorating oil prices, and negative interest rates abroad. In response to all these worries (and others), stocks dove more than -11% (S&P 500 Index) in January, before settling down. Subsequently, the market has made a screaming recovery, in part due to dovish monetary policy comments (i.e., reduction in forecasted interest rate hikes) and diminished anxiety over a potential global collapse. Month-to-date stocks are up an impressive +5.4%, and year-to-date equities are flattish, or down less than -1%.

With an endless amount of information flowing across our smart phones and computers, it becomes quite easy and tempting to chase news headlines, just like a hyper dog chasing a car. But even once an investor catches up (or reacts) to a headline, there’s confusion around how to profit from the fleeting information. First of all, every plugged-in hedge fund and institutional investor has likely already traded on the stale information you received. Second of all, rarely is the data relevant to the long-term cash generating capabilities of the company or economy. And lastly, the news is more often than not, instantly factored into the stock price. Chasing news headlines only eaves individual investors holding the bag of performance-shattering transactions costs, taxes, and worn-out pricing.

The heightened volatility in late 2015 and early 2016 hasn’t however prevented investors and so-called pundits from attempting to time the market. Any battle-tested investment veteran knows it’s virtually impossible to consistently time the market (see also Market Timing Treadmill), but this fact hasn’t prevented speculators from attempting the feat nonetheless. Famed investment guru, Peter Lynch, who earned an average +29% annual return from 1977-1990, summed it up well when he stated the following:

“Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.”

The Important Factors

As I’ve written many times in the past, the keys to long-term stock performance are not knee-jerk reactions to headlines, but rather these following crucial factors (see also Don’t Be a Fool, Follow the Stool):

- Profits

- Interest Rates

- Sentiment

- Valuations

On the profit growth front, corporate income has been pressured by numerous headwinds over the last few years, including an export-shattering increase in the value of the U.S. dollar and a profit-squeezing collapse in energy sector earnings. As you can see from the chart below, the value of the U.S. dollar increased by about 25% from mid-2014 to early-2015, in part because of diverging global central bank policies (more hawkish U.S. Fed vs. more dovish ECB/international central banks). Since that spike, the dollar has settled into a broad range (95 – 100), and the former forceful headwind have now turned into modest tailwinds. This trend is important because an estimated 35-40% of corporate profits are derived from international operations.

Adding insult to injury, the roughly greater than -70% decline in forward energy earnings over the last 18 months has caused a significant hit to overall S&P 500 profits. The tide appears to be finally turning (or at least stabilizing) however, as we’ve seen oil prices rebound by about +30% this year from the lows in January. If these aforementioned trends persist, profit pressures in 2016 are likely to abate significantly, and may actually become additive to growth.

Source: Barchart.com

Profits are important, but so are interest rates. While incessant talk about the path of future Fed policy continues to blanket the airwaves (see also Fed Fatigue), absent a rapid increase in interest rates (say 300-400 basis points), interest rates remain unambiguously positive for equity markets, providing a floor for the oft-repeated volatility in financial markets. As long as stocks are providing higher yields than many bonds, and depositors are earning 0% (or negative rates) on their checking accounts, stocks may remain unloved, but not forgotten.

And speaking of unloved, the sentiment for stocks remains sour. One need look no further than the quarter-billion dollars in hemorrhaging outflows out of U.S. equity funds (see ICI Long-Term Mutual Fund Flows) since 2014. This deep underlying skepticism serves as a positive contrarian indicator for future equity prices. Right now, very few individual investors are swimming in the pool – the time to get out of the stock market pool is when everyone is jumping in.

And lastly, valuations remain very much in line with historical averages (approximatqely 17x 2016 projected earnings), especially considering the generational low in interest rates. Bears continue to point to the elevated CAPE ratio, which has been a disastrous indicator the last seven years (and longer), as a reason to remain cautious. The ironic part is that valuations are virtually guaranteed to improve a few years from now as we roll off the artificially depressed years of 2008-2010.

When you add it all up, zero (or negative) interest rates, combined with the other key factors of profits, sentiment, and valuations, equities remain an important and attractive part of a diversified long-term portfolio. Your objectives, time horizon, and risk tolerance will always drive the proportion of your equity allocation. Nevertheless, some bond exposure is essential to smooth out volatility. Regardless of your investment strategy, chasing headlines, like a dog chasing a car, serves no purpose other than leaving you with a tired, unproductive investment portfolio.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Invest with a Telescope…Not a Microscope

It was another bloody week in the stock market (S&P 500 index dropped -3.1%), and any half-glass full data was interpreted as half-empty. The week was epitomized by a Citigroup report entitled “World Economy Trapped in a Death Spiral.” A sluggish monthly jobs report on Friday, which registered a less than anticipated addition of 151,000 jobs, painted a weakening employment picture. Professional social media site LinkedIn Corp. (LNKD) added fuel to the fire with a soft profit forecast, which resulted in the stock getting almost chopped in half (-44%)…in a single day (ouch).

It’s funny how quickly the headlines can change – just one week ago, the Dow Jones Industrial index catapulted higher by almost +400 points in a single day and we were reading about soaring stocks.

Coherently digesting the avalanche of diverging and schizophrenic headlines is like attempting to analyze a windstorm through a microscope. A microscope is perfect for looking at a single static item up close, but a telescope is much better suited for analyzing a broader set of data. With a telescope, you are better equipped to look farther out on the horizon, to anticipate what trends are coming next. The same principle applies to investing. Short-term traders and speculators are great at using a short-term microscope to evaluate one shiny, attention-grabbing sample every day. The investment conclusion, however, changes the following day, when a different attention-grabbing headline is analyzed to a different conclusion. As Mark Twain noted, “If you don’t read the newspaper, you are uninformed. If you do read the newspaper, you are misinformed.”

Short-termism is an insidious disease that will slowly erode short-run performance and if not controlled will destroy long-run results as well. This is not a heretic concept. Some very successful investors have preached this idea in many ways. Here are a few of them:

‘‘We will continue to ignore political and economic forecasts which are an expensive distraction for many investors and businessmen.” –Warren Buffett (Annual Newsletter 1994)

‘‘If you spend more than 14 minutes a year worrying about the market, you’ve wasted 12 minutes’’ –Peter Lynch

“Excessive short-termism results in permanent destruction of wealth, or at least permanent transfer of wealth” -Jack Gray Grantham

On the flip side, those resilient investors who have succeeded through investment cycles understand the importance of taking a long-term view.

“Whatever method you use to pick stocks or stock mutual funds, your ultimate success or failure will depend on your ability to ignore the worries of the world long enough to allow your investments to succeed.” –Peter Lynch

“The farther you can lengthen your time horizon in the investment process, the better off you will be.” – David Nelson (Legg Mason)

“Long term owners are more relaxed, more informed, more patient, less emotional.” –John Templeton

“If you are really a long-term investor, you will view a bear market as an opportunity to make money.” –John Templeton

“Long term is not a popular time-horizon for today’s hedge fund short-term mentality. Every wiggle is interpreted as a new secular trend.” –Don Hays

“In the long run, one of the greatest risk to your net worth is not owning stocks. Bonds do not grow. They can only return their face value at maturity…Inflation is a silent, insidious tax that erodes your net worth…Fortunately, there is an easy way to keep pace with and even beat inflation, and this is stocks.” – John Spears

“In the short-term, the stock market is a voting machine; in the long-term a weighing machine.” -Benjamin Graham

There has been a lot of pain experienced so far in 2016, and there may be more to come. However, trying to time the market and call a bottom is a fruitless effort. Great companies and investments do not disappear in a bear market. At times like these, it is important to stick to a systematic, disciplined approach that integrates valuation and risk controls based on where we are in an economic cycle. Despite all the recent volatility, as I’ve repeated many times, the key factors driving the direction of the stock market are the following: 1) Corporate profits; 2) Interest rates; 3) Valuations; and 4) Sentiment (see also Don’t Be a Fool, Follow the Stool). Doom and gloom “Death Spiral” headlines may currently rule the day, but the four key stock-driving factors on balance remain skewed towards the positive…if you have the ability to put away your microscope and take out your telescope.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in LNKD or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Don’t Do Something…Just Stand There!

Like a full plane hitting a rough patch of turbulence, investors have been shaken by the recent price volatility in the stock market over concerns of a slowing Chinese economy, plummeting oil prices, and a host of other alarming headlines. As a result, investors are left picking up the pieces of the S&P 500 decline, which currently sits off -11% from its 2015 highs (down -15% at the 1/20/16 low). The picture looks even uglier if you consider the Russell 2000 small cap index, which has collapsed -21% from its 2015 highs (-26% at the 1/20/16 low).

What now, and what does this mean? There has been all kinds of crazy technical trading activity occurring around heavy options expirations, stop-loss selling, and short cover buying. With all the frenetic gyrations in the stock market (e.g., 2,000 point swing in the Dow Jones over the last month), there have been no shortage of opinions on TV, on the internet or at the watercooler. However, the best sage advice probably came from 86-year-old investor legend, John “Jack” Bogle (founder of Vanguard Group – $3.4 trillion in assets under management at 12/31/15), who emphatically told investors to “Don’t do something…just stand there!”

The advice to “stay the course” can be very counter-intuitive to human nature. In periods of stress, our brains tend to revert back to our ancestors’ Darwinian survival instincts, which tell us to flee from the ferocious lion (see also Controlling the Investment Lizard Brain). The fact is these periods of turbulence are normal – no different than a bumpy flight into San Francisco. In fact, we’ve hit quite a few choppy air pockets in recent years:

- Debt Downgrade/Debt Ceiling Debate/European PIIGS Crisis (-22% in 2011)

- Arab Spring/Grexit Fears (-11% in 2012)

- Fed Taper Tantrum (-8% in 2013)

- Ebola Outbreak (-10% in 2014)

- China Slowdown Fears (-13% in 2015)

Through all of this mayhem, including the current 2016 dip, the stock market has still managed to rise an impressive +77% since the 2011 pullback, which sure beats the sub-1% yield earned on bank CDs.

Inevitably, with the recent price breakdown, speculation has begun to swirl around the dreaded “R”-word (aka, recession) again. In general, this is a fruitless effort. When the smartest Nobel Prize winning economists fail miserably at predicting recessions, it’s hard to believe you or I will have a much better success rate. The great investor Peter Lynch astutely summed up recession forecasting as follows:

“It’s lovely to know when there’s recession. I don’t remember anybody predicting 1982 we’re going to have 14 percent inflation, 12 percent unemployment, a 20 percent prime rate, you know, the worst recession since the Depression. I don’t remember any of that being predicted. It just happened. It was there. It was ugly. And I don’t remember anybody telling me about it. So I don’t worry about any of that stuff. I’ve always said if you spend 13 minutes a year on economics, you’ve wasted 10 minutes.”

The noted Nobel Prize winning economist Paul Samuelson offered this shrewd observation on recessions as well:

“The stock market has called nine of the last five recessions.”

In other words, the stock market can predict recessions, but often times it is a horrible indicator for the health of the economy (e.g., see 2011-2015 above).

While I am definitely not a Nobel Prize winning economist, I can objectively point to supporting evidence showing we currently are not on the edge of a new recession. It is certainly true that a strong U.S. dollar and a Q4 energy earnings deterioration has been a drag on earnings, but these factors only paint a small part of the picture. Without going into gory economic detail, you do not need to be an expert to understand basic macro trends like employment, housing, auto sales, gasoline prices, and interest rates are providing a buttress to the economy.

As you can see from the chart below, the -73% cut in Q4 energy sector earnings, along with challenged exports from multinational corporations, has pressured profitability in the S&P 500. However, if you strip out the energy sector, earnings continue to grow. And although it’s early in the 2016 earnings reporting season, so far 73% of companies are beating estimates by 3% on average.

The economic winds are definitely spinning, and we may not be completely through the turbulence, but rather than panicking, you’re probably best served by following the advice of Jack Bogle by standing through the turmoil and look for opportunities when the volatility settles.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}

{kind=link}