Posts tagged ‘interest rates’

Goldilocks Meets the Fragile 5 and the 3 Bears

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (February 3, 2014). Subscribe on the right side of the page for the complete text.

The porridge for stock market investors was hot in 2013, with the S&P 500 index skyrocketing +30%, while the porridge for bond investors was too cold, losing -4% last year (AGG). Like Goldilocks, investors are waiting to get more aggressive with their investment portfolios once everything feels “just right.” Dragging one’s feet too long is not the right strategy. Counterintuitively, and as I pointed out in “Here Comes the Dumb Money,” the investing masses have been very bashful in committing large sums of money out of cash/bonds into stocks, despite the Herculean returns experienced in the stock market over the last five years.

Once the party begins to get crowded is the period you should plan your exit. As experienced investors know, when the porridge, chair, and bed feel just right, is usually around the time the unhappy bears arrive. The same principle applies to the investing. In the late 1990s (i.e., technology bubble) and in the mid-2000s (i.e., housing bubble) everyone binged on tech stocks and McMansions with the help of loose credit. Well, we all know how those stories ended…the bears eventually arrived and left a bunch of carnage after tearing apart investors.

Fragile 5 Bed Too Hard

After enjoying some nice porridge at a perfect temperature in 2013, Goldilocks and investors are now searching for a comfortable bed. The recent volatility in the emerging markets has caused some lost sleep for investors. At the center of this sleeplessness are the financially stressed countries of Argentina and the so-called “Fragile Five” (Brazil, India, Indonesia, Turkey and South Africa) – still not sure why they don’t combine to call the “Sick Six” (see chart below).

|

| Source: Financial Times |

Why are these countries faced with the dilemma of watching their currencies plummet in value? One cannot overly generalize for each country, but these dysfunctional countries share a combination of factors, including excessive external debt (loans denominated in U.S. dollars), large current account deficits (trade deficits), and small or shrinking foreign currency reserves. This explanation may sound like a bunch of economic mumbo-jumbo, but at a basic level, all this means is these deadbeat countries are having difficulty paying their lenders and trading partners back with weaker currencies and depleted foreign currency reserves.

Many pundits, TV commentators, and bloggers like to paint a simplistic picture of the current situation by solely blaming the Federal Reserve’s tapering (reduction) of monetary stimulus as the main reason for the recent emerging markets sell-off. It’s true that yield chasing investors hunted for higher returns in in emerging market bonds, since U.S. interest rates have bounced around near record lows. But the fact of the matter is that many of these debt-laden countries were already financially irresponsible basket cases. What’s more, these emerging market currencies were dropping in value even before the Federal Reserve implemented their stimulative zero interest rate and quantitative easing policies. Slowing growth in China and other developed countries has made the situation more abysmal because weaker commodity prices negatively impact the core economic engines of these countries.

Argentina’s Adversity

In reviewing the struggles of some emerging markets, let’s take a closer look at Argentina, which has seen its currency (peso) decline for years due to imprudent and inflationary actions taken by their government and central bank. More specifically, Argentina tried to maintain a synchronized peg of their peso with the U.S. dollar by manipulating its foreign currency rate (i.e., Argentina propped up their currency by selling U.S. dollars and buying Argentinean pesos). That worked for a little while, but now that their foreign currency reserves are down -45% from their 2011 peak (Source: Scott Grannis), Argentina can no longer realistically and sustainably purchase pesos. Investors and hedge funds have figured this out and as a result put a bulls-eye on the South American country’s currency by selling aggressively.

Furthermore, Argentina’s central bank has made a bad situation worse by launching the money printing presses. Artificially printing additional money may help in paying off excessive debts, but the consequence of this policy is a rampant case of inflation, which now appears to be running at a crippling 25-30% annual pace. Since the beginning of last year, pesos in the black market are worth about -50% less relative to the U.S. dollar. This is a scary developing trend, but Argentina is no stranger to currency problems. In fact, during 2002 the value of the Argentina peso declined by -75% almost overnight compared to the dollar.

Each country has unique nuances regarding their specific financial currency pickles, but at the core, each of these countries share a mixture of these debt, deficit, and currency reserve problems. As I have stated numerous times in the past, money ultimately moves to the place(s) it is treated best, and right now that includes the United States. In the short-run, this state of affairs has strengthened the value of the U.S. dollar and increased the appetite for U.S. Treasury bonds, thereby pushing up our bond prices and lowering our longer-term interest rates.

Their Cold is Our Warm

Overall, besides the benefits of lower U.S. interest rates, weaker foreign currencies lead to a stronger dollar, and a stronger U.S. currency means greater purchasing power for Americans. A stronger dollar may not support our exports of goods and services (i.e., exports become more expensive) to our trading partners, however a healthy dollar also means individuals can buy imported goods at cheaper prices. In other words, a strong dollar should help control inflation on imported goods like oil, gasoline, food, cars, technology, etc.

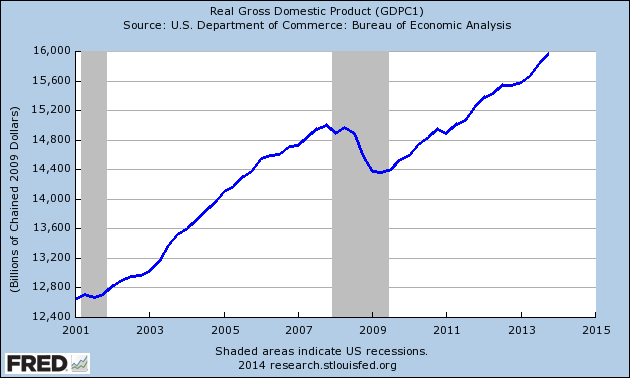

While emerging markets have cooled off fairly quickly, the temperature of our economic porridge in the U.S. has been quite nice. Most recently, the broadest barometer of economic growth (Real GDP) showed a healthy +3.2% acceleration in the 4th quarter to a record of approximately $16 trillion (see chart below).

|

| Source: Crossing Wall Street |

Moreover, corporate profits continue to come in at decent, record-setting levels and employment trends remain healthy as well. Although job numbers have been volatile in recent weeks and discouraged workers have shrunk the overall labor pool, nevertheless the unemployment rate hit a respectable 6.7% level last month and the positive initial jobless claims trend remains at a healthy level (see chart below).

Skeptics of the economy and stock market assert the Fed’s continued retrenchment from quantitative easing will only exacerbate the recent volatility experienced in emerging market currencies and ultimately lead to a crash. If history is any guide, the growl from this emerging market bear may be worse than the bite. The last broad-based, major currency crisis occurred in Asia during 1997-1998, yet the S&P 500 was up +31% in 1997 and +27% in 1998. If history serves as a guide, the past may prove to be a profitable prologue. So rather than running and screaming in panic from the three bears, investors still have some time to enjoy the nice warm porridge and take a nap. The Goldilocks economy and stock market won’t last forever though, so once the masses are dying to jump in the comfy investment bed, then that will be the time to run for the hills and leave the latecomers to deal with the bears.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in AGG, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Bernanke: Santa Claus or Grinch?

I’ve written plenty about my thoughts on the Fed (see Fed Fatigue) and all the blathering from the media talking heads. Debates about the timing and probability of a Fed “taper” decision came to a crescendo in the recent week. As is often the case, the exact opposite of what the pundits expected actually happened. It was not a huge surprise the Federal Reserve initiated a $10 billion tapering of its $85 billion monthly bond buying program, but going into this week’s announcement, the betting money was putting their dollars on the status quo.

With the holiday season upon us, investors must determine whether the tapered QE1/QE2/QE3 gifts delivered by Bernanke are a cause for concern. So the key question is, will this Santa Claus rally prance into 2014, or will the Grinch use the taper as an excuse to steal this multi-year bull market gift away?

Regardless of your viewpoint, what we did learn from this week’s Fed announcement is that this initial move by the Fed will be a baby step, reducing mortgage-backed and Treasury security purchases by a measly $5 billion each. I say that tongue in cheek because the total global bond market has been estimated at about $80,000,000,000,000 (that’s $80 trillion).

As I’ve pointed out in the past, the Fed gets way too much credit (blame) for their impact on interest rates (see Interest Rates: Perception vs Reality). Interest rates even before this announcement were as high/higher than when QE1 was instituted. What’s more, if the Fed has such artificial influence over interest rates, then why do Austria, Belgium, Canada, Denmark, Finland, France, Germany, Japan, Netherlands, Sweden, and Switzerland all have lower 10-year yields than the U.S.? Maybe their central banks are just more powerful than our Fed? Unlikely.

Dow 128,000 in 2053

Readers of Investing Caffeine know I have followed the lead of investing greats like Warren Buffett and Peter Lynch, who believe trying to time the markets is a waste of your time. In a recent Lynch interview, earlier this month, Charlie Rose asked for Lynch’s opinion regarding the stock market, given the current record high levels. Here’s what he had to say:

“I think the market is fairly priced on what is happening right now. You have to say to yourself, is five years from now, 10 years from now, corporate profits are growing about 7 or 8% a year. That means they double, including dividends, about every 10 years, quadruple every 20, go up 8-fold every 40. That’s the kind of numbers you are interested in. The 10-year bond today is a little over 2%. So I think the stock market is the best place to be for the next 10, 20, 30 years. The next two years? No idea. I’ve never known what the next two years are going to bring.”

READ MORE ABOUT PETER LYNCH HERE

Guessing is Fun but Fruitless

I freely admit it. I’m a stock-a-holic and member of S.A. (Stock-a-holic’s Anonymous). I enjoy debating the future direction of the economy and financial markets, not only because it is fun, but also because without these topics my blog would likely go extinct. The reality of the situation is that my hobby of thinking and writing about the financial markets has no direct impact on my investment decisions for me or my clients.

There is no question that stocks go down during recessions, and an average investor will likely live through at least another half-dozen recessions in their lifetime. Unfortunately, speculators have learned firsthand about the dangers of trading based on economic and/or political headlines during volatile cycles. That doesn’t mean everyone should buy and do nothing. If done properly, it can be quite advantageous to periodically rebalance your portfolio through the use of various valuation and macro metrics as a means to objectively protect/enhance your portfolio’s performance. For example, cutting exposure to cyclical and debt-laden companies going into an economic downturn is probably wise. Reducing long-term Treasury positions during a period of near-record low interest rates (see Confessions of a Bond Hater) as the economy strengthens is also likely a shrewd move.

As we have seen over the last five years, the net result of investor portfolio shuffling has been a lot of pain. The acts of panic-selling caused damaging losses for numerous reasons, including a combination of agonizing transactions costs; increased inflation-decaying cash positions; burdensome taxes; and a mass migration into low-yielding bonds. After major indexes have virtually tripled from the 2009 lows, many investors are now left with the gut-wrenching decision of whether to get back into stocks as the markets reach new highs.

As the bulls continue to point to the scores of gifts still lying under the Christmas tree, the bears are left hoping that new Fed Grinch Yellen will come and steal all the presents, trees, and food from the planned 2014 economic feast. There are still six trading days left in the year, so Santa Bernanke cannot finish wrapping up his +30% S&P 500 total return gift quite yet. Nevertheless, ever since the initial taper announcement, stocks have moved higher and Bernanke has equity investors singing “Joy to the World!”

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Perception vs. Reality: Interest Rates & the Economy

There is a difference between perception and reality, especially as it relates to the Federal Reserve, the economy, and interest rates.

Perception: The common perception reflects a belief that Quantitative Easing (QE) – the Federal Reserve’s bond buying program – has artificially stimulated the economy and financial markets through lower interest rates. The widespread thinking follows that an end to tapering of QE will lead to a crash in the economy and financial markets.

Reality: As the chart below indicates, interest rates have risen during each round of QE (i.e., QE1/QE2/QE3) and fallen after the completion of each series of bond buying (currently at a pace of $85 billion per month in purchases). That’s right, the Federal Reserve has actually failed on its intent to lower interest rates. In fact, the yield on the 10-year Treasury Note stands at 2.94% today, while at the time QE1 started five years ago, on December 16, 2008, the 10-year rate was dramatically lower (~2.13%). Sure, the argument can be made that rates declined in anticipation of the program’s initiation, but if that is indeed the case, the recent rate spike of the 10-year Treasury Note to the 3.0% level should reverse itself once tapering begins (i.e., interest rates should decline). Wow, I can hardly wait for the stimulative effects of tapering to start!

Source: Calafia Beach Pundit

Fact or Fiction? QE Helps Economy

Taken from a slightly different angle, if you consider the impact of the Federal Reserve’s actions on the actual economy, arguably there are only loose connections. More specifically, if you look at the jobs picture, there is virtually NO correlation between QE activity and job creation (see unemployment claims chart below). There have been small upward blips along the QE1/QE2/QE3 path, but since the beginning of 2009, the declining trend in unemployment claims looks like a black diamond ski slope.

Source: Calafia Beach Pundit

Moreover, if you look at a broad spectrum of economic charts since QE1 began, including data on capital spending, bank loans, corporate profits, vehicle sales, and other key figures related to the economy, the conclusion is the same – there is no discernible connection between the economic recovery and the Federal Reserve’s quantitative easing initiatives.

I know many investors are highly skeptical of the stock market’s rebound, but is it possible that fundamental economic laws of supply and demand, in concert with efficient capital markets, could have something to do with the economic recovery? Booms and busts throughout history have come as a result of excesses and scarcities – in many cases assisted by undue amounts of fear and greed. We experienced these phenomena most recently with the tech and housing bubbles in the early and middle parts of last decade. Given the natural adjustments of supply and demand, coupled with the psychological scars and wounds from the last financial crisis, there is no clear evidence of a new bubble about to burst.

While it’s my personal view that many government initiatives, including QE, have had little impact on the economy, the Federal Reserve does have the ability to indirectly increase business and consumer confidence. Ben Bernanke clearly made this positive impact during the financial crisis through his creative implementation of unprecedented programs (TARP, TALF, QE, Twist, etc.). The imminent tapering and eventual conclusion of QE may result in a short-term hit to confidence, but the economy is standing on a much stronger economic foundation today. Making Ben Bernanke a scapegoat for rising interest rates is easy to do, but in actuality, an improving economy on stronger footing will likely have a larger bearing on the future direction of interest rates relative to any upcoming Fed actions.

Doubters remain plentiful, but the show still goes on. Not only are banks and individuals sitting on much sturdier and healthier balance sheets, but corporations are running lean operations that are reporting record profit margins while sitting on trillions of dollars in cash. In addition, with jobs on a slow but steady path to recovery, confidence at the CEO and consumer levels is also on the rise.

Despite all the negative perceptions surrounding the Fed’s pending tapering, reality dictates the impact from QE’s wind-down will likely to be more muted than anticipated. The mitigation of monetary easing is more a sign of sustainable economic strength than a sign of looming economic collapse. If this reality becomes the common perception, markets are likely to move higher.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is the information to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Fed Fatigue Setting In

Uncle…uncle! There you have it – I have finally cried “uncle” because I cannot take it anymore. I don’t think I can listen to another panel or read another story debating about the timing of Fed “tapering”, or heaven forbid the Fed actually “tighten” the Federal Funds rate (i.e., increasing the targeted rate for inter-bank lending). Type in the words “Bernanke” and “tapering” into Google and you will get back more than 41,000,000 results. The build up to the 600-word FOMC (Federal Open Market Committee) statement was almost deafening, so much so that live coverage of Federal Reserve Chairman Ben Bernanke was available at your fingertips:

Source: Yahoo! Finance

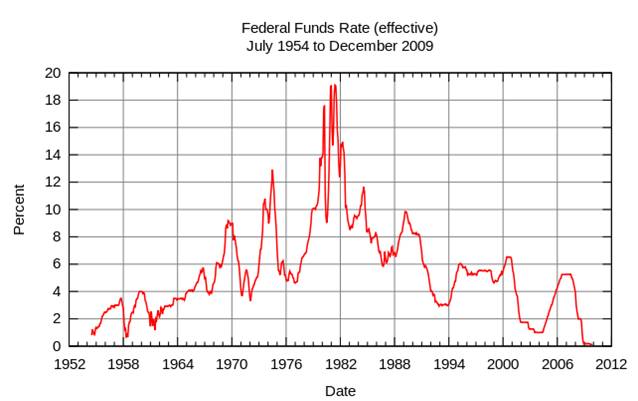

Like a toddler (or a California-based, investment blog writer) going to the doctor’s office to receive an inoculation, the anxiety and mental anguish caused in anticipation of the event is often more painful than the actual injection. As I highlighted in a previous Investing Caffeine article, the 1994 interest rate cycle wasn’t Armageddon for equity markets, and the same can be said for the rate hikes from 1.0% to 5.25% in the 2004-20006 period (see chart below). Even if QE3 ends in mid-2014 and the new Federal Reserve Chairman (thank you President Obama) raises rates in 2015, this scenario would not be the first (or last) time the Federal Reserve has tightened monetary policy.

Source: Wikipedia

Short Memories – What Have You Done for Me Lately?

People are quick to point out the one-day -350 Dow point loss earlier this week, but many of them forget about the +3,000 point moon shot in the Dow Jones Industrial index that occurred in six short months (November 2012 – May 2013). The same foggy recollection principle applies to interest rates. The recent rout in 10-year Treasury prices is easily recalled as rates have jumped from 1.5% to 2.5% over the last year, however amnesia often sets in for others if you ask them where rates were a few years ago. It’s easy to forget that 30-year fixed rate mortgages exceeded 5% and the 10-year reached 4% just three short years ago.

Bernanke: The Center of the Universe?

Does Ben Bernanke deserve credit for implementing extraordinary measures during extraordinary times during the 2008-09 financial crisis? Absolutely. But should every man, women, and child wait with bated breath to see if a word change or tonal adjustment is made in the eight annual FOMC meetings?

Like the public judging Ben Bernanke, my Sidoxia clients probably give me too much credit when things go well and too much blame when things don’t. I love how Bernanke gets blamed/credited for the generational low interest rates caused by his money printing ways and QE punch bowl tactics. Last I checked, the interest rate downtrend has been firmly in place over the last three decades, well before Bernanke came into the Fed and worked his monetary magic. How much credit/blame are we forgetting to give former Federal Reserve Chairmen Paul Volcker, Alan Greenspan, and other government policy-makers? Regardless of what happens economically for the remainder of 2013, Bernanke will do whatever he can to solidify his legacy in the waning sunset months of his term.

Another forgotten fact I like to point out: There is more than one central banker living on this planet. If you haven’t been asleep over the last few decades, our financial markets have increasingly become globally interconnected with the assistance of technology. I know our 10-year Treasury rates are hovering around 2.50%, and our egotistical patriotism leads us to hail Bernanke as a monetary god, but don’t any other central bankers or government officials around the world deserve any recognition for achieving yields even lower than ours? Here’s a partial list (June 22, 2013 – Financial Times):

- Japan – 0.86%

- Germany – 1.67%

- Canada – 2.33%

- U.K. – 2.31%

- France – 2.27%

- Sweden – 2.15%

- Austria – 2.09%

- Switzerland – 0.92%

- Netherlands – 2.07%

Although it may be fun to look at Ben Bernanke as our country’s financial Superman who is there to save the day, there are a lot more important factors to consider than the 47 words added and 19 subtracted from the latest FOMC statement. If investing was as easy as following central bank monetary policy, everyone would be continually jet setting to their private islands. Rather than wasting your time listening to speculative blathering about direction of Fed monetary policy, why not focus on finding solid investment ideas and putting a long-term investment plan in place. Now please excuse me – Fed fatigue has set in and I need to take a nap.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and GOOG, but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Helicopter Ben to QE3 Rescue

Faster than a speedy credit default swap, more powerful than a federal funds interest rate cut, and able to leap a tall Mario Draghi in a single bound, look…it’s Helicopter Ben! How did Federal Reserve Chairman Ben Bernanke become a monetary superhero with such a cool nickname as Helicopter Ben (a.k.a. “HB”)? Bernanke, a former Princeton University professor, has widely been known to be a diligent student of the Great Depression, and his aviation nickname stems from a 2002 speech in which he referenced dropping money from a helicopter to combat deflation. While investors may worry about HB’s ability to fight the inflation thugs, there should be no questions about his willingness to implement accommodative, deflation-fighting monetary policies.

Chairman Bernanke may not epitomize your ideal superhero, however this slightly past middle-aged bearded and balding man has helped mastermind some of the most creative and aggressive monetary rescue efforts our country and globe has seen in the history of man (and woman). This week’s money-printing QE3 announcement solidified Bernanke’s historic capital saturating ranking.

Since Helicopter Ben’s heroic appointment as Federal Reserve Chairman in 2006 by George W. Bush, Bernanke has instituted numerous monetary gadgets in hopes of meeting the Federal Reserve’s dual mandate, which is i) to achieve low inflation and ii) to strive for maximum employment. Arguably, given the anemic growth here in the U.S.; the recession in Europe; and slowing growth in the emerging markets (i.e., China, Brazil, India, etc.), slack in the economy and static labor wages have largely kept inflation in check. With the first part of the dual mandate met, Bernanke has had no problem putting his monetary superpowers to work.

As referenced earlier, Bernanke’s bazooka launch of QE3, an open ended MBS (Mortgage Back Securities) bond binging program, will add $40 billion of newly purchased assets to the Fed’s balance sheet on a monthly basis until the labor market improves “substantially” (whatever that means). What’s more, in addition to the indefinite QE3, Bernanke has promised to keep the federal funds rate near zero “at least through mid-2015,” even for a “considerable time after the economic recovery strengthens.”

HB’s Track Record

Throughout superhero history, Superman, Spider-man, and Batman have used a wide-array of superhuman powers, extraordinary gadgets, and superior intellect to conquer evil-doers and injustices across the globe. Bernanke has also forcefully put his unrivaled money-printing talents to work in an attempt to cure the financial ills of the world. Here’s a quick multi-year overview of how Bernanke has put his unique talents to print trillions of dollars and keep interest rates suppressed:

Rate Cuts (September 2007 – December 2008): Before “quantitative easing” was a part of our common vernacular, the Fed relied on more traditional monetary policies, such as federal funds rate targeting, conducted through purchases and sales of open market securities. Few investors recall, but before HB’s fed funds rate cut rampage of 10 consecutive reductions in 2007 and 2008 (the fed funds rate went from 5.25% to effectively 0%), Bernanke actually increased rates three times in 2006.

Crisis Actions (2007 – 2009): Love him or hate him, Bernanke has been a brave and busy soul in dealing with the massive proportions of the global financial crisis. If you don’t believe me, just check out the Financial Crisis Timeline listed at the St. Louis Federal Reserve. Many investors don’t remember, but Bernanke helped orchestrate some of the largest and most unprecedented corporate actions in our history, including the $30 billion loan to JPMorgan Chase (JPM) in the Bear Stearns takeover; the $182 billion bailout of AIG; the conversion of Morgan Stanley (MS) and Goldman Sachs Group Inc. (GS) into bank holding companies; and the loan/asset-purchase support to Fannie Mae (FNMA) and Freddie Mac (FMCC). These actions represented just the tip of the iceberg, if you also consider the deluge of liquidity actions taken by the Fed Chairman.

HB Creates Acronym Soup

In order to provide a flavor of the vastness in emergency programs launched since the crisis, here is an alphabet soup of program acronyms into which the Fed poured hundreds of billions of dollars:

- Term Asset-Backed Securities Loan Facility (TALF)

- Term Auction Facility (TAF)

- Money Market Investor Funding Facility (MMIFF)

- Commercial Paper Funding Facility (CPFF)

- Primary Dealer Credit Facility (PDCF)

- Asset-Backed Commercial Paper Money Market Fund Liquidity Facility (AMLF)

- Temporary Reciprocal Currency Arrangements (Swap lines)

- Term Securities Lending Facility (TSLF)

Plenty of acronyms to go around, but these juicy programs have garnered most of investors’ attention:

QE1 (November 2008 – March 2010): In hopes of lowering interest rates for borrowers and stimulating the economy, HB spearheaded the Fed’s multi-step, $1 trillion+ buying program of MBS (mortgage backed securities) and Treasuries.

QE2 (November 2010 – June 2011): Since the Fed felt QE1 didn’t pack enough monetary punch to keep the economy growing at a fast enough clip, the FOMC (Federal Open Market committee) announced its decision to expand its holdings of securities in November 2010. The Committee maintained its existing policy of reinvesting principal payments from its securities holdings and to also purchase a further $600 billion of longer-term Treasury securities by the end of the second quarter of 2011 (an equivalent pace of about $75 billion per month).

Operation Twist (September 2011 – December 2012): What started out as a $400 billion short-term debt for longer-term debt swap program in September 2011, expanded to a $667 billion program in June 2012. With short-term rates excessively low, Bernanke came up with this Operation Twist scheme previously used in the early 1960s. Designed to flatten the yield curve (bring down long-term interest rates) to stimulate economic activity, Bernanke thought this program was worth another go-around. Unlike quantitative easing, Operation Twist does not expand the Fed’s balance sheet – the program merely swaps short-term securities for long-term securities. Currently, the program is forecasted to conclude at the end of this year.

The Verdict on HB

So what’s my verdict on the continuous number of unprecedented actions that Helicopter Ben and the Fed have taken? Well for starters, I have to give Mr. Bernanke an “A-” on his overall handling of the financial crisis. Had his extreme actions not been taken, the pain and agony experienced by all would likely be significantly worse, and the financial hole a lot deeper.

With that said, am I happy about the announcement of QE3 and the explosion in the Fed’s money printing activities? The short answer is “NO”. It’s difficult to support a program with questionable short-run interest rate benefits, when the menacing inflationary pressures are likely to outweigh the advantages. The larger problem in my mind is the massive fiscal problem we are experiencing (over $16 trillion in debt and endless trillion dollar deficits). More importantly, this bloated fiscal position is creating an overarching, nagging crisis of confidence. A resolution to the so-called “fiscal cliff,” or the automated $600 billion in tax increases and spending cuts, is likely to have a more positive impact on confidence than a 0.05% – 0.25% reduction in mortgage rates from QE3. Once adequate and sustained growth returns, and inflation rears its ugly head, how quickly Helicopter Ben tightens policy will be his key test.

Until then, Bernanke will probably continue flying around while gloating in his QE3 cape, hoping his quantitative easing program will raise general confidence. Unfortunately, his more recent monetary policies appear to be creating diminishing returns. Even before QE3’s implementation, Helicopter Ben has witnessed his policies expand the Fed’s balance sheet from less than $900 billion at the beginning of the recession to almost $3 trillion today. Despite these gargantuan efforts, growth and confidence have been crawling forward at only a modest pace.

No matter the outcome of QE3, as long as Ben Bernanke remains Federal Reserve Chairman, and growth remains sluggish, you can stay confident this financial man of steel will continue dumping money into the system from his helicopter. If Bernanke wants to create a true legendary superhero ending to this story, the kryptonite-like effects of inflation need to be avoided. This means, less money-printing and more convincing of Congress to take action on our out-of-control debt and deficits. Now, that’s a comic book I’d pay to read.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct positions in JPM, AIG, MS, GS, FNMA, FMCC, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Rates Dance their Way to a Floor

The globe is awash in debt, deficits are exploding, and the Euro is about to collapse…right? Well, then why in the heck are six countries out of the G-7 seeing their 10-year sovereign debt trade at 2.5% or lower on a consistent downward long-term trajectory? What’s more, three of the six countries witnessing their rates plummet are from Europe, despite pundits continually calling for the demise of the eurozone.

Here is a snapshot of 10-year sovereign debt yields for the majority of the G-7 countries over the last few decades:

Source: TradingEconomics.com

The sole G-7 member missing from the bond yield charts above? Italy. Although Italy’s deficits are not massive (Italy actually has a smaller deficit than U.S. as % of GDP: 3.9% in 2011), its Debt/GDP ratio has been large and rising (see chart below):

Source: TradingEconomics.com

As the globe has plodded through the financial crisis of 2008-2009, investors have flocked to the perceived stability of these larger developed countries’ bonds, even if they are merely better homes in a bad neighborhood right now. PIMCO likes to call these popular sovereign bonds, “cleaner dirty shirts.” Buying sovereign debt from these less dirty shirt countries, without sensitivity to price or yield, has been a lucrative trade that has worked consistently for quite some time. Now, however, with sovereign bond yields rapidly approaching 0%, it becomes mathematically impossible to fall lower than the bottom rate floor that developed countries are standing on.

Bond bears have been wrong about the timing of the inevitable bond price reversal, myself included, but the bulls are skating on thinner and thinner ice as rates continue moving lower. The bears may prolong their bragging rights if interest rates continue downward, or persist at these lower levels for extended periods of time. Eventually the “buy the dips” mentality dies, as we so poignantly experienced in 2000 when the technology dips turned into outright collapse.

The Flies in the Bond Binging Ointment

As long as equities remain in a trading range, the “risk-off” bond binging arguments will continue holding water. If corporate earnings remain elevated and stock buybacks carry on, the pain of deflating real returns will eventually become too unbearable for investors. As the insidious rising prices of energy, healthcare, food, leisure, and general costs keep eating away everyone’s purchasing power, even the skeptics will become more impatient with the paltry returns they are currently earning. Earning negative real returns in Treasuries, CDs, money market accounts, and other conservative investments, is not going to help millions of Americans meet their future financial goals. Due to the laundry list of global economic concerns, large swaths of investors are still running and hiding, but this is not a sustainable strategy longer term. The danger from these so-called “safe,” low-yielding asset classes is actually riskier than the perceived risk, in my view.

With that said, I’ve consistently held there are a subset of investors, including a significant number of my Sidoxia Capital Management clients, who are in the later stage of retirement and have a rational need for capital preservation and income generating assets (albeit low yielding). For this investor segment, portfolio construction is not executed due to an opportunistic urge of chasing potential outsized rates of return, but more-so out of necessity. Shorter time horizons eliminate the prudence of additional equity exposure because of the extra associated volatility. Unfortunately, many of the 76 million Baby Boomers will statistically live another 20 – 30 years based on actuarial life expectations and under-save, so the risks of being too conservative can dramatically outweigh the risks of increasing equity exposure. This is all stated in the context of stocks paying a higher yield than long-term Treasuries – the first time in a generation.

Short-term risks and uncertainties remain high, with Greek election outcomes unknown; a U.S. Presidential election in flux; and an impending domestic fiscal cliff that needs to be addressed. But with interest rates accelerating towards 0% and investors’ fright-filled buying of pricey, low-yielding asset classes, many of these risks are already factored into current valuations. As it turns out, the pain of panic can be more detrimental than being stuck in over-priced assets, driven by rates dancing near an absolute floor.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Mr. Market Bullying Investors

Source: Photobucket

There’s been a bully pushing investor’s around and his name is “Mr. Market.” Volatility is Mr. Market’s partner in crime, and over the last 10 trading days Mr. M has used volatility to school equity investors to the tune of 1,600+ point swings, which has contributed to equity investors’ failing grade over the last few months. Who is Mr. Market? Charles Ellis, author of Winning the Loser’s Game (1998) described him best:

“Mr. Market is a mischievous but captivating fellow who persistently teases investors with gimmicks and tricks such as surprising earnings reports, startling dividend announcements, sudden surges of inflation, inspiring presidential announcements, grim reports of commodities prices, announcements of amazing new technologies, ugly bankruptcies, and even threats of war.”

How has Mr. Market been stealing investors’ lunch money? The process really hasn’t been that difficult for him, once you consider how many times investors have been heaved into the garbage can over the last decade, forced to deal with these messy events:

• 2001 technology bubble beating

• 2006 real estate collapse

• 2008 – 2009 financial crisis and recession

• 2010 “flash crash” and soft patch

• 2011 debt ceiling debate and credit rating downgrade

With this backdrop, investors are dropping like flies due to extreme bully fatigue. Over the last four months alone, approximately $75 billion in equities been liquidated, according to data from the Investment Company Institute – this is even more money withdrawn than the outflows occurring during the peak panic months after the Lehman Brothers collapse.

The Atomic Wedgie

Exhibit I (Source: Photobucket)

Mr. Market understands the severity of these prior economic scars, which have been even more painful than atomic wedgies (reference Exhibit I above), so he opportunistically is taking advantage of fragile nerves. Introducing the following scary scenarios makes collecting lunch money from panicked investors much easier for Mr. Market. What is he using to frighten investors?

- A potential Greek sovereign debt default that will trigger a collapse of the Euro.

- Slowing growth in China due to slowing developed market economic activity.

- Possible double-dip recession in the U.S. coupled with an austerity driven downturn in Europe.

- Lack of political policy response to short and long-term economic problems in Washington and abroad.

- Impending deflation caused by decelerating global growth or likely inflation brought about by central banks’ easy monetary policies (i.e., printing money).

- End of the world.

Bully Victim Protection

Of course, not all of these events are likely to occur. As a matter of fact, there are some positive forming trends, besides just improving valuations, that provide protection to bully victims:

- Not only is the earnings yield (E/P – 12-month trailing EPS/share price) trouncing the yield on the 10-year Treasury note (~8% vs. ~2%, respectively), but the dividend yield on the S&P 500 index is also higher than the 10-year Treasury note yield (source: MarketWatch). Historically, this has been an excellent time to invest in equities with the S&P 500 index up an average of 20% in the ensuing 12 months.

- Jobs data may be poor, but it is improving relative to a few years ago as depicted here:

Source: Calafia Beach Pundit

Source: Calafia Beach Pundit

- Record low interest rates and mortgage rates provide a stimulative backdrop for businesses and consumers. Appetite for risk taking remains low, but as history teaches us, the pendulum of fear will eventually swing back towards greed.

Source: Calafia Beach Pundit

As I say in my James Carville peace from earlier this year, It’s the Earnings Stupid, long term prices of stocks follow the path of earnings. Recent equity price market declines have factored in slowing in corporate profits. How severely the European debt crisis, and austerity have (and will) spread to the U.S. and emerging markets will become apparent in the coming weeks as companies give us a fresh look at the profit outlook. So far, we have gotten a mixed bag of data. Alpha Natural Resources (ANR) acknowledged slowing coal demand in Asia and FedEx Corp. (FDX) shave its fiscal year outlook by less than 2% due to international deceleration. Other bellwethers like Oracle Corp. (ORCL) and Nike Inc. (NKE) reported strong growth and outlooks. In the short-run Mr. Market is doing everything in his power to bully investors from their money, and lack of international policy response to mitigate the European financial crisis and contagion will only sap confidence and drag 2011-2012 earnings lower.

Punching Mr. Market

The warmth of negative real returns in cash, bonds, and CDs may feel pleasant and prudent, but for many investors the lasting effects of inflation erosion will inflict more pain than the alternatives. For retirees with adequate savings, these issues are less important and focus on equities should be deemphasized. For the majority of others, long-term investors need to reject the overwhelming sense of fear.

As I frequently remind others, I have no clue about the short-term direction of the market, and Greece could be the domino that causes the end of the world. But what I do know is that history teaches us the probabilities of higher long-term equity returns are only improving. Mr. Market is currently using some pretty effective scare tactics to bully investors. For those investors with a multi-year time horizon, who are willing to punch Mr. Market in the nose, the benefits are significant. The reward of better long-term returns is preferable to an atomic wedgie or a head-flush in the toilet received from Mr. Market.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, and FDX, but at the time of publishing SCM had no direct position in ANR, ORCL, NKE, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Stretching Rubber Band Creating More Value

Concerns over debt ceiling negotiations, European financial challenges, and overall economic malaise has reached a feverish pitch in the U.S., yet in the background, a valuation rubber band has quietly been stretching to ever more attractive levels. Regardless of whether seniors might not receive Social Security checks, troops not obtain ammunition, and investors not collect credit rating agency love, corporations keep churning profits out like they are going out of style (17%+ growth in 2011 estimated earnings). We have barely scratched the surface on earnings season, and I’m sure better than expected earnings from the likes of Google Inc. (GOOG), JPMorgan Chase & Co. (JPM), FedEx Corp. (FDX), Nike Inc. (NKE), and Bed Bath & Beyond Inc. (BBBY) will not sway the bears, but in the meantime profits keep chugging along. Although profits have more than doubled in the last 12 years, not to mention a halving in interest rates (10-year Treasury yield cut from 6% to about 3%), yet the S&P 500 is still down approximately -4% (June 1999 – June 2011).

What Gives?

Could the valuation stretching continue as earnings continue to grind higher? Absolutely. Just because prices have been chopped in half, doesn’t mean they can’t go lower. From 1966 – 1982 the Dow Jones Industrial index traded at around 800 and P/E multiples contracted to single digits. That rubber band eventually snapped and the index catapulted 17-fold from 800 to almost 14,000 in 25 years. Even though equities have struggled in the 21st century, a few things have changed from the low-point reached about 30 years ago. For starters, we have not hit an inflation rate of 15% or a Federal Funds rate of 20% (4% and 0% today, respectively), so we have a tad bit more headroom before the single digit P/E apocalypse descends upon us. If you listen to Peter Lynch, investor extraordinaire, his “Rule of 20” states a market equilibrium P/E ratio should equal 20 minus the inflation rate. This rule would imply an equilibrium P/E ratio of 16-17 when the current 2011 P/E multiple implies a value slightly above 13 times earnings. The bears may claim victory if the earnings denominator collapses, but if earnings, on the contrary, continue coming in better than expected, then the sun might break through the clouds in the form of significant price appreciation.

Another change that has occurred since the days of Cabbage Patch dolls has been the opening floodgates of globalization. The technology revolution has accelerated the flattening of the globe, which has created numerous new opportunities and threats. Creating a company like Facebook with about 750 million users and an estimated value of $80 billion to $100 billion couldn’t happen 30 years ago, but on the flip side, our country is also competing with billions of motivated brains lurking in the far reaches of the world with a singular focus of sucking away our jobs, resources, and dollars. Winners recognize this threat and are currently adapting. Losers blind to this trend remain busy digging their own graves.

Future is Uncertain

As famous Jedi Master Yoda aptly identified, “Always in motion is the future.” The future is always uncertain, and if it wasn’t, I would be on my private island drinking umbrella drinks all day. With undecided debt ceiling negotiations occurring over the next few weeks, political rhetoric will be blaring and traders will be hyperventilating with defibrillator paddles close at hand. If history is a guide, stupid decisions may be made, but the almighty financial markets (and maybe a few Molotov cocktails at a local protest rally) will eventually slap politicians in the face to wake up to reality. Perhaps you recall the attention the markets earned from legislators when the Dow fell 777 points in a single September 2008 trading session. Blood on the streets forced Congress to approve the Troubled Asset Relief Program hot potato four days after the initial vote failed. And if that wasn’t a gentle enough reminder for Democrats and Republicans, then a few lessons can be learned from the interest rate sledgehammer that capital markets vigilantes have slammed on the Greeks (10-year Greek yields are hovering above 17%+).

Down but Not Out

The stories of debt collapse, hyperinflation, double-dip recessions, plunging dollar, secular bear markets, and government shutdowns are all plausible but remote scenarios. As Winston Churchill so eloquently stated, “You can always count on Americans to do the right thing – after they’ve tried everything else.” Voter moods are so venomous that if fiscal irresponsibility is not changed, politicians will be voted straight out of office – even hardcore, extremist elected officials understand this self-serving point.

Suffice it to say, as the political noise reaches a deafening pitch in the coming weeks and months, a quiet rubber band in the background keeps stretching. When the political noise dies down, you may just hear a noise snapping stock prices higher.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Performance data from Morningstar.com. Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, GOOG, and FDX, but at the time of publishing SCM had no direct position in JPM, NKE, BBBY, Facebook, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Shoring Up Your Investment Stool from Collapse

With March Madness just kicking into full gear, there’s a chance that your gluteal assets may be parked on a stool in the next two weeks. When leaning on a bar countertop, while seated on a stool, we often take for granted the vital support this device provides, so we can shovel our favorite beverage and pile of nachos into our pie holes. OK, maybe I speak for myself when it comes to my personal, gluttonous habits. But the fact remains, whether you are talking about your rump, or your investment portfolio, you require a firm foundation.

The main problem, when it comes to investments, is the lack of a tangible, visible stool to analyze. Sure, you are able to see the results of a portfolio collapse when there is no foundation to support it, or you may even be able to ignore the results when they remain above water. But many investors do not evenperform the basic due diligence to determine the quality of their investment stool. Before you place your life savings in the hands of some brokerage salesman, or in your personal investment account, you may want to make sure your stool has more than one or two legs.

In the money management world, investors typically choose to buy the stool, rather than build it, which makes perfect common sense. Many people do not have the time or emotional make-up to manage their finances. If left to do it themselves, more often than not, investors usually do a less than stellar job. Unfortunately, when many investors do outsource the management of their investments, they neglect to adequately research the investment stool they buy. Usually the wobbly industry stool operates on the two legs of performance chasing and commission generation (see Fees, Exploitation, and Confusion). For most average investors, it doesn’t take long before that investment strategy teeters and collapses.

If the average investor does not have time to critically evaluate managers that take a long-term, low-cost, tax-efficient strategy to investing, those individuals would be best served by following Warren Buffet’s advice about passive investments, “A very low-cost index is going to beat a majority of the amateur-managed money or professionally-managed money.”

The Four Legs of the Investment Stool

For DIY-ers (Do-It-Yourself-ers), you do not need to buy a stool – you can build it. There are many ways to build a stool, but these are the four crucial legs of investing that have saved my hide over my career, and can be added as support for your investment stool:

1.) Valuation: I love sustainable growth as much as anything, just as much as I would like a shiny new Ferrari. But there needs to be a reasonable price paid for growth, and paying an attractive or fair price for a marquis asset will improve your odds for long-term success.

“Valuations do matter in the stock market, just as good pitching matters in baseball.”

-Fred Hickey (High Tech Strategist)

2.) Cash Flows: Cash flows, and more importantly free cash flows (cash left over after money is spent on capital expenditures), should be investors’ metric of choice. Companies do not pay for dividends, share buybacks, and capital expenditures with pro forma earnings, or non-GAAP earnings. Companies pay for these important outlays with cash.

“In looking for stocks to buy, why do you put so much emphasis on free cash flow? Because it makes the most sense to me. My first job was at a little corner grocery store, and it seemed pretty simple. Cash goes into the register; cash comes out.”

-Bruce Berkowitz (The Fairholme Fund)

3.) Interest Rates: Money goes where it is treated best, so capital will look at the competing yields paid on bonds. Intuitively, interest factors also come into play when calculating the net present value of a stock. Just look at the low Price-Earnings ratios of stocks in the early 1980s when the Fed Funds reached about 20% (versus effectively 0% today). In the long run, higher interest rates (and higher inflation) are bad for stocks, but worse for bonds.

“I don’t know any company that has rewarded any bondholder by raising interest rates [payments] – unlike companies raising dividends.”

-Peter Lynch (Former manager of the Fidelity Magellan Fund)

4.) Quality: This is a subjective factor, but this artistic assessment is as important, if not more important than any of the previous listed factors. In searching for quality, it is best to focus on companies with market share leading positions, strong management teams, and durable competitive advantages.

“If you sleep with dogs, you’re bound to get fleas.”

-Old Proverb

These four legs of the investment stool are essential factors in building a strong investment portfolio, so during the next March Madness party you attend at the local sports bar, make sure to check the sturdiness of your bar stool – you want to make sure your assets are supported with a sturdy foundation.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in Fairholme, Ferrari, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Siegel & Co. See “Bubblicious” Bonds

Source: Wall Street Journal - March 14, 2000

Siegel compares 1999 stock prices with 2010 bonds

Unlike a lot of economists, Jeremy Siegel, Professor at the Wharton School of Business, is not bashful about making contrarian calls (see other Siegel article). Just days after the Nasdaq index peaked 10 years ago at a level above 5,000 (below 2,200 today), Siegel called the large capitalization technology market a “Sucker’s Bet” in a Wall Street Journal article dated March 14, 2000. Investors were smitten with large-cap technology stocks at the time, paying balloon-like P/E (Price-Earnings) ratios in excess of 100 times trailing earnings (see table above).

Bubblicious Boom

Today, Siegel has now switched his focus from overpriced tech-stock bubbles to “Bubblicious” bonds, which may burst at any moment. Bolstering his view of the current “Great American Bond Bubble” is the fact that average investors are wheelbarrowing money into bond funds. Siegel highlights recent Investment Company Institute data to make his point:

“From January 2008 through June 2010, outflows from equity funds totaled $232 billion while bond funds have seen a massive $559 billion of inflows.”

The professor goes on to make the stretch that some government bonds (i.e., 10-year Treasury Inflation-Protected Securities or TIPS) are priced so egregiously that the 1% TIPS yield (or 100 times the payout ratio) equates to the crazy tech stock valuations 10 years earlier. Conceptually the comparison of old stock and new bond bubbles may make some sense, but let’s not lose sight of the fact that tech stocks virtually had a 0% payout (no dividends). The risk of permanent investment loss is much lower with a bond as compared to a 100-plus multiple tech stock.

Making Rate History No Mystery

What makes Siegel so nervous about bonds? Well for one thing, take a look at what interest rates have done over the last 30 years, with the Federal Funds rate cresting over 20%+ in 1981 (View RED LINE & BLUE LINE or click to enlarge):

Source: dshort.com

As I have commented before, there is only one real direction for interest rates to go, since we currently sit watching rates at a generational low. Rates have a minute amount of wiggle room, but Siegel rightfully understands there is very little wiggle room for rates to go lower. How bad could the pain be? Siegel outlines the following scenario:

“If over the next year, 10-year interest rates, which are now 2.8%, rise to 3.15%, bondholders will suffer a capital loss equal to the current yield. If rates rise to 4% as they did last spring, the capital loss will be more than three times the current yield.”

Siegel is not the only observer who sees relatively less value in bonds (especially government bonds) versus stocks. Scott Grannis, author of the Calafia Report artfully shows the comparisons of the 10-Year Treasury Note yield relative to the earnings yield on the S&P 500 index:

Source: Calafia Report (Scott Grannis)

As you can see, rarely have there been periods over the last five decades where bonds were so poorly attractive relative to equities.

Grannis mirrors Siegel’s view on government bond prices through his chart on TIPS pricing:

Source: Calafia Report (Scott Grannis)

Pricey Treasuries is not a new unearthed theme, however, Siegel and Grannis make compelling points to highlight bond risks. Certainly, the economy could soften further, and trying to time the bottom to a multi-decade bond bubble can be hazardous to your investing health. Having said that, effectively everyone should desire some exposure to fixed income securities, depending on their objectives and constraints (retirees obviously more). The key is managing duration and the risk of inflation in a prudent fashion. If you believe Siegel is correct about an impending bond bubble bursting, you may consider lightening your Treasury bond load. Otherwise, don’t be surprised if you do not collect on another “sucker’s bet.”

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including TIP and other fixed income ETFs), but at the time of publishing SCM had no direct position in any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}