Blushing Pinocchio – The Half Trillion Lie

When in doubt, or when in debt by half a trillion dollars, why not just make some crazy stuff up? This is the exact strategy California pension administrators used when implementing +50% increases in union member benefits earlier this decade. The pension plans decided to take a break from reality and enter fantasyland when they projected the Dow Jones Industrial Average would hit 25,000 by the end of the decade and 28,000,000 by 2099, a forecast that would even make Pinocchio blush.

Dealing with the Problem

Governor Arnold Schwarzenegger and his economic advisors attempted to take on the unions. Unfortunately, not everyone got the message. On the day the Governor struck a deal with the unions, California Public Employees’ Retirement System (CalPERS) ordered a hike of $4 billion to the annual pension payments to its members.

The financial woes of California have been well documented as the state looks to lower its $19.1 billion deficit and an estimated one-half trillion dollars in unfunded pension liabilities – a level equal to about seven times the state’s total debt level. Even after multiple years of severe cuts, Schwarzenegger has had to resort to drastic measures, including his most recent desperate move to get some 200,000 state workers to accept slashes in pay to a $7.25/hour minimum wage.

Facing Reality

As I have discussed in the past, dealing with excessive debt requires a gut check. Cutting debt is similar to dieting – easy to understand, but difficult to execute (see my Debt Control article).

Whether Republican candidate Meg Whitman or Democratic candidate Jerry Brown wins the thankless position of California Governor, they will have to face the elephant in the room, but hopefully they will not resort to fuzzy accounting or predictions of Dow 28 million that would make even Pinocchio blush.

Read Full Related Article from Vincent Fernando at Business Insider

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct positions in any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Living Large – Technology Revolution Raises Tide

It’s hard to believe that my kids will never truly know what it is was like to live without a microwave, VCR, GPS device, internet connection or many of the other modern day inventions. In my elementary school days, when I had to write a report about Alfred Hitchcock, I was forced to drag my mom to the public library, chase down some librarians, and comb through floors of book shelves, only to find the book I needed was already checked-out. Today, it’s amazing to watch my kid, barely old enough to pull the milk container out of the fridge, scamper over to the computer, type in a few search words on Google (GOOG) and access an endless pool of information for a homework assignment. Fortunately for my wife and me, my daughter has not discovered Facebook yet.

Rising Tide Lifts All

In the uncertain times we live in, many people lose sight of the incredible advancements achieved over our generation, and ignore the difficult challenges and problems entrepreneurs are solving today. And many of these advancements have trickled down to wide swaths of the population. The minimum wage worker, cleaning dishes at the local restaurant, may not be able to afford the new $500 iPad from Apple Inc. (AAPL), but technology advancements have benefited the less privileged in different ways. For example, similar computing power used in the iPad has also been used in the logistics and sourcing departments of retail chains like Family Dollar (FDO), thereby making goods cheaper for lower-income consumers.

One person who has not lost sight of these advancements of productivity is Mark J. Perry of the Enterprise Blog. In a recent article, Perry compares what a consumer working 152 hours in 1964, earning an average wage, could purchase versus an average consumer today (46 years later) working the same 152 hours. Beyond the average wage of $2.50 per hour increasing to $19 per hour, Perry shows the unbelievable increase in the quality and number of products.

Perry places the continuing technological revolution in context by stating:

“Americans today can purchase low-priced electronics products that even a billionaire in the past wouldn’t have been able to buy.”

Another person that knows a little about technology, Sergey Brin (Co-Founder of Google Inc.), put recent technology advancements in perspective in the company’s 2008 annual report:

“Our first major purchase when we started Google was an array of disk drives that we spent a good fraction of our life savings on and took several car trips to carry. Today, I walked out of a store with a small box in my hand that stores more than all those drives and cost about $100. Similarly, the processors available today are about 100 times as powerful as those we used in 1998.”

Advancements in our standard of living are not only limited to electronic gadgets and internet searches, but also tangible benefits continue to be realized in the most important elements of our human survival. A picture says a thousand words, and these charts speak volumes about our standard of living:

Lives are Extending and Food More Affordable

Obviously, everything is not a bed of roses and some of these improvements have come at a cost. Our country has lost millions of jobs over the last few years, and globalization has significantly increased foreign competition in broad areas of our economy. But before you succumb to the devastation rhetoric of the nay-sayers, please do not forget about the almost imperceptible rising tide of technological innovations that are allowing us to live better lives, even in uncertain times.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, GOOG, and AAPL, but at the time of publishing SCM had no direct positions in RSH, FDO, Facebook, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Kass: Triple Lindy Redux

About a year ago, I wrote about Doug Kass (founder and president of Seabreeze Partners) and his attempt at pulling off the famous “Triple Lindy” dive, which was made famous in the classic movie Back to School starring Rodney Dangerfield. If I were a judge, I would say Kass’s landing wasn’t a perfect 10, but rather closer to a 6.5. After successfully nailing the bear market in 2008, and subsequently declaring the “generational low” of March 2009, Kass became cautious in June 2009. At the time, Kass pulled in his horns by pronouncing a consumer-led double dip in late 2009 or in the first half 2010 from a consumption binge hangover, while declaring his previous 1050 S&P 500 index target as overly ambitious. What actually transpired is the S&P 500 went from around 942 to 1220 over the next ten months, or up about +30%.

Today, Kass is trying to make another large splash, but now he is reversing course and once more calling for a rally…at least a mini one. Rather than speaking in terms of his previous generational low (S&P 666), Kass sees the recent lows around 1,010 being the “bottom for the year” and his new 2010 target is based on climbing to positive territory for the year, implying a +10% to +12% move from the beginning of July.

View Doug Kass Interview and Prediction

View Doug Kass Interview and Prediction

Kass is not your traditional investor, and he admits as much:

“I’m not a perma-bear, I’m not a perma-bull. I try to be flexible and eclectic in my view, and this is especially necessary in a market, which is so volatile as it’s been for the last several years.”

In explaining his upbeat rationale, Kass highlights nuanced aspects to employment data, payroll growth, moderate economic expansion, and an attractive valuation for the overall market:

“I’m not technically based, therefore I’m not sentiment based, I’m fundamental based….The markets are traveling on a path of fear and share prices have significantly disconnected from fundamentals.”

Even if Kass didn’t nail the “Triple Lindy,” he still deserves special attention as a practitioner, in addition to his side job as a market prognosticator. Additional recognition is warranted solely based on the potshots he aimed at rent-a-strategists like Nouriel Roubini, CNBC celebrity, (see Roubini articles #1 or #2) and Robert Prechter, long-running technician who is currently predicting Dow destruction to unfathomable level of 1,000. I’m not in the business of predicting short-term market gyrations, but I’ll enjoy watching Kass’s next dive to see whether he’ll make a splash or not.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct positions in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Jobs: The Gluttonous Cash Hog

Really? Do you think Steve Jobs actually needs to hoard $42 billion in cash reserves on the company’s balance sheet, when they are already adding to the gargantuan mountain of money at a $12 billion clip per year. Let’s not forget, this gaudy amount of money is being added after all operating expenses and capital expenditures have been paid for.

Perhaps Steve is just a little worried about the economy, and wants a little extra loose change around for a rainy day? I’d buy that argument, but Mr. Jobs and the rest of the executives just witnessed the worst financial crisis in a generation, and the company still managed to generate about $9 billion in free cash flow in both fiscal 2008 and 2009.

If Apple was not creating cash flow like those cascading chocolate fountains I see at wedding receptions, then perhaps a cash safety blanket is needed for acquisitions? Here’s what Steve had to say about Apple’s cash levels in February:

Steve Jobs (Source: Photobucket)

“We know if we need to acquire something – a piece of the puzzle to make something big and bold – we can write a check for it and not borrow a lot of money and put our whole company at risk…The cash in the bank gives us tremendous security and flexibility.”

Let’s explore that idea a little further. First of all, what type of experience does Apple have in doing large acquisitions? Not a lot, and just to humor myself I ran a screen on a universe of more than 10,000 stocks and I came up with 111 companies with a value (market capitalization) greater than $40 billion. Unless Apple plans on buying companies like Coca Cola (KO), Chevron Corp. (CVX), Pfizer (PFE), or United Parcel Service (UPS), I think Apple can part ways with some of their billions. Certainly, there are a handful of theoretical targets in the areas of technology and content, but for certain, (a) any large deal would face intense regulatory scrutiny, and (b) if truly there were grand synergies from doing a massive deal, then most definitely they would be able to issue stock (if Jobs hates debt) to help fund the deal. It is pure nonsense and laughable to believe any “big and bold” acquisition would put the company “at risk.” The only thing at risk for doing a large deal would be Apple’s stock price.

The truth of the matter is returning cash to shareholders would be a fantastic self-disciplining tool, like putting mayonnaise on a brownie to prevent excess calorie consumption. Steve should give current or former CEOs of AOL, Time Warner, Mercedes Benz, Chrysler, Sprint, and Nextel a call to see how those large deals worked out for them. Apple could use an acquisition security blanket, but they do not need a circus tent of cash.

Times of Change

Although times have changed, some executives have not. Many tech companies, including Apple, have nostalgic memories of the go-go tech bubble days of the 1990s when growth at any price was the main mantra and no attention was paid to prudent capital allocation. With a stagnant stock market over the last twelve years, and interest rates sitting sluggishly at record lows (effectively 0% on the Federal Funds rate), investors are demanding prudent decision-making when it comes to capital allocation. Mr. Jobs, it is time to expand your narrow views and show the stewardship of sensibly managing the cash of your loyal investors.

Believe it or not, there are still a few of us actual “investors” that still exist. I’m talking about investors who do not just speculatively rent a stock for a day, week, or month, but rather those who invest for the long-term because they believe in the vision and execution capabilities of management and believe the company’s capital will be invested in their best interest.

I do not mean to single Mr. Jobs out, because he is not the only gluttonous, cash-hog offender among CEOs. In many respects, Apple has the good fortune of becoming a cash-hoarding poster child. The company does indeed deserve credit for becoming a $225 billion technology-consumer-media-retail juggernaut that has spread its tentacles brilliantly across numerous massive markets, whether its PCs, cell phones, music, television, movies, games, advertising etc.…you get the picture. But just because you are an exceptionally gifted visionary doesn’t give you the right to destroy value of hopelessly idle cash, which is begging for a better home than a 0.25% T-Bill.

Solutions – Taming the Cash Hog:

1) Divvy Up Dividends: With $42 billion in cash on the balance sheet and additional annual free cash generation on pace for $12 billion per year, there is no reason Steve Jobs and the board couldn’t declare a dividend that would yield 3% today. If that feels like too much, then how about shave off a pittance of $5 billion or so to pay out a sustainable dividend, which would yield a market-matching 2% dividend yield to investors. This scenario would accommodate Apple with at least a few decades of a cash cushion to cover ALL the company’s operating expenses and capital expenditures. This meagerly, ultra-conservative dividend policy can actually persist (or grow) longer than expected, if Apple can sustainably grow profits – a good possibility.

2) Share Buyback: This solution is much less desirable from my perspective compared to the dividend route, since many of the large share repurchasers tend to also issue lots of new shares to employees and executives, thereby neutering the benefits of the share repurchases.

3) Bank of Apple – (B of A): Why doesn’t Jobs just create a new entity, plop $40 billion of cash from Apple Inc. into the venture, and then open it up as Bank of Apple. At least that way, as an investor in the bank, I could make more profitable lending spreads at B of A relative to the 0.25% yield earned on the mega-billions deteriorating on Apple’s corporate balance sheet.

The downside of instituting these cash reducing solutions:

- The company doesn’t have as much cash as it would like to do large stupid acquisitions.

- The company loses a bunch of day-traders and short-term stock renters that don’t even know what a dividend is.

The upside to efficiently allocating capital through a 2% dividend is Steve (and the other investors) will receive a nice fat quarterly check. In the case of Jobs, he’ll collect a handsome $27 million or so to his measly $1 annual salary. In the process, the company will also gain long term shareholders that buy into the strategic vision of the company.

Stubbornness has served Steve Jobs tremendously well in his career, and a successful CEO like Steve Jobs is not required to listen to my advice. However, I am hopeful that Mr. Jobs will see the hazards of choking on a rapidly growing $42 billion cash hoard and discover the benefits of slimming down a gluttonous cash hog.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and AAPL, but at the time of publishing SCM had no direct positions in KO, CVX, PFE, UPS, AOL, Time Warner, Mercedes Benz, Chrysler, Sprint, Nextel, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Baseball, Hot Dogs, and Fixed Income Securities

Having just celebrated another 4th of July holiday, I reflected on the historical importance of our country’s independence finalized 234 years ago, the defining birthday of our great country that permanently marked the separation of our nation from Great Britain. In honor of this revolutionary milestone, our culture has added a few American traditions over the centuries, including watching baseball, and gorging ourselves on hot dogs, and apple pie.There is no better symbol of the importance our culture places on overindulgence than Nathan’s International Hot Dog Eating Contest, held each year on July 4th in Coney Island, Brooklyn, New York. The 95th annual contest winner was Joey Chestnut with a total of 54 HDBs (Hot Dogs & Buns) consumed, but not without some controversy thanks to the arrest of former Nathan’s champ Takeru Kobayashi, who watched from the sidelines this year due to a contract dispute with event organizers. Chestnut holds the world record set in 2009 with 68 HDBs, equivalent to about 20,000 calories. In setting the unmatched record, the winner of wiener eating contest inhaled in 10 minutes what an average human should consume in 10 days.

Bond Binge

In the financial markets, Americans have been pigging out on something else over the last few decades, and that is bonds. The craving for bonds has not changed since the end of the financial crisis either. According to Morningstar, since the end of 2008, investors have placed a net $390 billion into taxable bond funds and withdrawn -$45 billion out of U.S. stock funds. A continuation of these trends can be seen in the latest ICI (Investment Company Institute) fund flow data, in which we saw a +$6.3 billion inflow into bonds and a -$1.3 billion abandonment of stocks from the hands of jittery stock investors.

Beyond the endless checklist of worries (Europe default, China slowing, twin deficits, elections, etc.), there has been a consistent exodus of capital from money market funds due to the ridiculously low yields – the seven-day yield on taxable money-market funds, as measured by IMoneyNet, has recently held steady around 0.04%. For yield-hungry investors, bondholders are not getting a lot of bang for their buck if you consider the 10-Year Treasury Note is trading at 2.98%. Nothing in life comes for free, so in the case of Treasuries, bond investors are predominantly swapping market risk for interest rate risk. As I have repeatedly stated in the past, bonds are not evil, however fixed income exposure in a portfolio should be customized for an individual in the context of a diversified portfolio that meets investors’ objectives and risk tolerance.

Although the inflation skies are sunny now, there are clouds on the horizon and the stimulative monetary policies conducted over the last few years do not augur well for a likely climb in future interest rates.

Reversal of Fortune

In the competitive eating world, there is a so-called “reversal of fortune” that disqualifies eaters. At some point, you can only consume so much before the forces of nature take over.

I don’t know when the day of regurgitation will come for many fixed income securities, but managing your consumption of bonds, and the associated duration, becomes crucial as bond bellies continue to bulge. Takeru Kobayashi discovered this first hand at the Nathan’s 2007 championship event.

Baseball, hot dogs, and apple pie have been essential components to the unique aspects of the great American culture. In the world of investing, we have witnessed an acceleration in investors’ appetite for bonds – I just hope for the sake of overzealous bond investors, they will not suffer a reversal of fortune.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including fixed income ETFs), but at the time of publishing SCM had no direct positions in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

LeBron James’s Stock: Buy, Sell, or Hold? (Ticker: LBJ)

The world is watching. With the National Basketball Association (NBA) free agency period officially kicking off on July 1st, frothing-mouthed NBA owners have been released to attack LeBron “King” James in hopes of dragging him back to their home teams. Don’t be surprised to see extensive media footage of paparazzi chasing around a Cadillac Escalade with tinted windows or LeBron’s custom logo’d Ferrari – at least until James officially announces his new team of choice (or reasserts his loyalty to his hometown Cleveland Cavaliers). Stalking one of the greatest professional basketball players of all-time may be fascinating to many, but in the high stakes business of professional sports, LeBron is nothing more than a financial asset being shopped around everywhere from Los Angeles and New Jersey to Miami and New York. So, if LeBron James was a stock, would he be a buy, sell, or hold? And if so, at what price? By the way, his bud, and fellow biased posse member, Warren Buffett, is not eligible to answer these important questions.

Hot IPO Season

Although LeBron is the talk of the town these days, there is a flood of other new contract issuances coming to market. Unlike the stock market, the IPO (Initial Public Offering) and Secondary Offering markets for NBA players is flaming hot this year, with some fresher faces mixing it up with some steely veterans. Beyond LeBron James, you have an incredibly talented cast of characters chasing big bucks, including Dwyane Wade, Chris Bosh, Amar’e Stoudemire, Joe Johnson, Paul Pierce, Ray Allen, Dirk Nowitzki, Yao Ming, Carlos Boozer, Manu Ginobili, Richard Jefferson, and Michael Redd.

Valuation

James is not an unknown commodity like a private start-up company with a limited track record, so valuing LeBron is much easier than sizing up a rookie. What is a 25 year old, two-time MVP phenom, who averages 27.8 points per game, 7.0 rebounds, and 7.0 assists worth?

Well, what kind of coin are other illustrious players making…for example Kobe Bryant of the Los Angeles Lakers? Even with Bryant’s slightly less dazzling stats (25.3 points per game, 5.3 rebounds, and 4.7 assists), in April he signed a three-year contract extension worth almost $90 million that will keep him in Los Angeles through the 2013-14 season. The comparison isn’t exactly fair, since Bryant, a 12-time All-Star, has been in the league twice as long as James (14 years vs. 7 years) and Bryant also just secured his fifth golden championship ring (versus zero for James).

To get an even better feel on LBJ stock’s comparable analysis, let’s look at the green that other premier players in the league pulled in last season:

1. Tracy McGrady (Houston Rockets): $23.4 million

2. Kobe Bryant (LA Lakers): $23.2 million

3. Jermaine O’Neal (Miami Heat): $22.8 million

4. Tim Duncan (San Antonio Spurs): $22.2 million

5. Shaquille O’Neal (Cleveland Cavaliers): $20 million

6. Dirk Nowitzki (Dallas Mavericks) $19.8 million

Paul Pierce (Boston Celtics): $19.8 million

8. Ray Allen (Boston Celtics): $19.75 million

9. Rashard Lewis (Orlando Magic): $18.9 million

10. Michael Redd (Milwaukee Bucks): $17 million

Big bucks all these players make, but so sad what they do with it (read Hidden Pro Athlete Train Wreck)

M & A Perspective

Another way of looking at the LBJ free agency circus is from a mergers and acquisition standpoint. Unfortunately, the vast majority of mergers fail (see CNET article). One major reason is the culture dynamics that need to align between the coach, LeBron, and the other supporting cast on the team. Golden state Warrior Latrell Sprewell’s choking of Coach P.J. Carlesimo in 1997 is proof positive of what can go wrong when cultures collide. Another aspect of deal-busters is the tendency for suitors to overpay for acquisition deals, and bake in too optimistic assumptions regarding the target’s capabilities to perform.

On the flip side, some obvious complementary skill-set synergies could mesh nicely if a multi-player deal could be constructed between Chris Bosh (Toronto Raptors), Dwyane Wade…cool name (Miami Heat), and resurrected Coach Pat Riley, also of the Heat.

The Buck Stops in ???

When all is said and done, LeBron’s choice is simple – join the team that offers the best hope of winning a championship. The dollars and cents component of the deal are pretty formulaic due to salary caps and league maximums mandated through the Collective Bargaining Agreement (CBA) between owners and players. As the Associated Press points out, the difference between staying in Cleveland and going elsewhere is around a measly $30 million (easy for me to say):

“James can get perhaps $125 million over six years by staying in Cleveland; $96 million over five years if he goes.”

My bottom line is that LBJ’s stock is pricey right now, but well worth the BUY if he ends up in Miami with Wade and Bosh. Unfortunately, a restructuring or 1-time charge in Cleveland will not get the job done (Shaq proved that point), so in the Cavs’ hands James is a sell. On the speculative BUY side, let us please forget I am a biased California native, and not fully dismiss the possibility of the Los Angeles Clippers landing LeBron. Billy Crystal is no iconic Laker fan like Jack Nicholson, but nonetheless with LBJ dressed up in red, white, and blue, Billy would have no trouble recruiting some of his celeb pals to hang courtside with him.

Given all the suitors and scenarios, determining a precise Buy, Sell, or Hold rating can be quite challenging. Information in this epic story is changing by the hour, but based on the current data, I am selling LeBron short in Cleveland, and buying him long in Los Angeles. Kobe, don’t confirm your 6th celebration parade next June just quite yet.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct positions in MSG, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

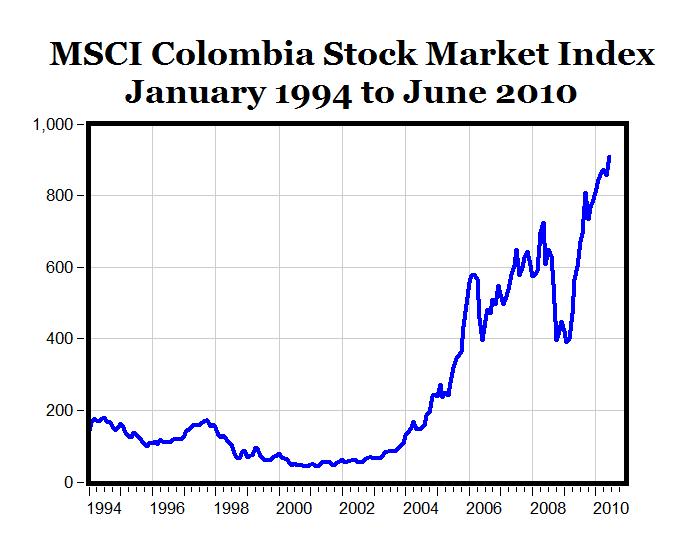

Colombia: The Hidden Latin American Gem

Judging by the all the volatility in the markets and the gloomy headlines blanketing business periodicals, one would think the global walls of capitalism and democracy were crumbling into oblivion. That’s why it’s a nice diversion to discover a diamond in the rough, shining through the darkness in the form of the Colombian stock market. How special is this South American gem? An +1,845% return over 10 years sounds pretty exceptional to me. Those are the results that Professor Dr. Mark J. Perry from the University of Michigan calculated in a posting he recently wrote about the MSCI Colombia stock market index in his blog, Carpe Diem.

Source: Carpe Diem

Fueling the surge in the equity markets has been a right-leaning, free market government with a hawkish defense stance, led by President Álvaro Uribe for the last eight years. The voters voted to continue Uribe’s mandate by voting in his former defense minister, Juan Manuel Santos, who promises to keep the disruptive guerilla forces operating under Revolutionary Armed Forces of Colombia (FARC) in check.

Colombia has been a close ally of the United States, thanks to their support of a joint crackdown on drug smuggling into the U.S. In return for their support, Colombia has received a nice fat $600 million check from the U.S. each year. What would even make our relationship tighter is an approval stamp placed on an awaiting U.S.-Colombia free trade agreement, which Congress has inexplicably kept on the backburner.

The U.S. and Colombia also agree on something else…their mutual disdain for Venezuelan leader, Hugo Chavez. Mr. Chavez poses a threat to the region, but Santos and the wave of free market leaders in the territory are more likely to wreak havoc on the Venezuelan leader according to Investor’s Business Daily:

“But Santos is probably most dangerous for Chavez, because Colombia’s rags-to-riches success story is so dramatic — showing that any beat-up nation can drag itself out of misery through markets — and because Venezuela and Colombia are such close neighbors. Word gets out about how well things are going in Colombia and it spreads fast in Venezuela. Santos need never fire a shot at Venezuela to slay Chavez’s revolution because the power of the markets will do it for him.”

Colombia’s Gross Domestic Product (GDP) is not overly large relative to some more developed neighbors, but the World Bank estimated the country’s 2008 GDP at $244 billion, almost triple the figure from five years earlier. The explosive economic growth explains how this market was the highest returning market in the world over the last decade, even eclipsing white hot markets like China, Russia, Brazil, Peru, India, and Turkey, among many others.

How does one invest in this Colombian gem? One way to gain exposure is through an exchange traded fund (ETF): Global X/InterBolsa FTSE Colombia 20 ETF (GXG). This particular ETF is concentrated into 20 positions, with heavy weightings in financial, energy, and industrial stocks. So, as you continue to read about the so-called inevitable “double-dip” recession and collapse of the U.S. dollar as the global reserve currency, please do not forget there are some brilliant free market economies, like Colombia, that are growing brilliantly and producing sparkling returns.

Read Professor Perry’s complete article on the Colombia market

Read the WSJ article written on the subject

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct positions in GXG, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Dividends: From Sapling to Abundant Fruit Tree

Dividends are like fruit and an investment in stock is much like purchasing a sapling. When purchasing a stock (sapling) the goal is two-fold: 1) Buy a sapling (tree) that is expected to bear a lot of fruit; and 2) Pay a cheap or fair price. If the right saplings are purchased at the right prices, then investors can enjoy a steady diet of fruit that has the potential of producing more fruit each year. Fruit can come in the form of future profits, but as we will see, the sweetness of a profitable company also paying dividends can prove much more fruitful over the long-term.

Investing in growth equities at reasonable prices seems like a pretty intelligent strategy, but of late the vast majority of fresh investor capital has been piling into bonds. This is not a flawed plan for retirees (and certain wealthy individuals) and should be a staple in all investment portfolios, to a degree (some of my client portfolios contain more than 80%+ in fixed income-like securities), but for many investors this overly narrow bond focus can lead to suboptimal outcomes. Right now, I like to think of bonds like a reliable bag of dried fruit, selling for a costly price. However, unlike stocks, bonds do not have the potential of raising periodic payments like a sapling with strong growth prospects. “Double-dippers” who are expecting the economy to spiral into a tailspin, along with nervous snakebit equity investors, prefer the reliability of the bagged dry fruit (bonds)… no matter how high the price.

How Sweet is the Fruit? How Does a +2,300% Yield Sound?

Not only do equities offer the potential of capital appreciation, but they also present the prospect of dividend hikes in the future – important characteristics, especially in inflationary environments. Bonds, on the other hand, offer static fixed payments (no hope of interest rate hikes) with declining purchasing power during periods of escalating general prices.

Given the possibility of a “double-dip” recession, one would expect corporate executives to be guarding their cash with extreme stinginess. On the contrary, so far in 2010, companies have shown their confidence in the recovery by increasing or initiating dividends at a +55% higher clip versus the same period last year. Underpinning these announcements, beyond a belief in an economic recovery, are large piles of cash growing on the balance sheets of nonfinancial companies. According to Standard & Poor’s (S&P), cash hit a record $837 billion at the end of March, up from $665 billion last year.

The S&P 500 dividend yield at 2.06% may not sound overwhelmingly high, but with CDs and money markets paying next to nothing, the Federal Funds rate at effectively 0%, and the 10-Year Treasury Note yielding an uninspiring 3.11%, the S&P yield looks a little more respectable in that light.

If the stock market yield doesn’t enthuse you, how does a +2,300% yield sound to you? That’s roughly what a $.05 (split adjusted) purchase of Wal-Mart (WMT) stock in 1972 would be earning you today based on the current $1.21 dividend per share paid today. That return alone is mind-blowing, but this analysis doesn’t even account for the near 1,000-fold increase in the stock price over the similar timeframe. That’s what happens if you can find a company that increases its dividend for 37 consecutive years.

Procter & Gamble (PG) is another example. After PG increased its dividend for 54 consecutive years, from a split-adjusted $.01 per share in 1970 to a $1.93 payout today, original shareholders are earning an approximate 245% yield on their initial investment (excluding again the massive capital appreciation over 40 years). There’s a reason investment greats like Warren Buffett have invested in great dividend franchises like WMT, PG, KO, BUD, WFC, and AXP.

Bad Apples do Exist

Dividend payment is not guaranteed by any means, as evidenced by the dividend cuts by financial institutions during the 2008-2009 crisis (e.g., BAC, WFC, C) or the discontinuation of BP PLC’s (BP) dividend after the Gulf of Mexico oil spill disaster. Bonds are not immune either. Although bonds are perceived as “safe” investments, the interest and principal payment streams are not fully insured – just ask bondholders of bankrupt companies like Lehman Brothers, Visteon, Tribune, or the countless other companies that have defaulted on their debt promises.

This is where doing your homework by analyzing a company’s competitive positioning, financial wherewithal, and corporate management team can lead you to those companies that have a durable competitive advantage with a corporate culture of returning excess capital to shareholders (see Investing Caffeine’s “Education” section). Certainly finding a WMT and/or PG that will increase dividends consistently for decades is no easy chore, but there are dozens of budding possibilities that S&P has identified as “Dividend Aristocrats” – companies with a multi-year track record of increasing dividends. And although there is uncertainty revolving around dividend taxation going into 2011, I believe it is fair to assume dividend payment treatment will be more favorable than bond income.

Apple Allocation

Growth companies that reinvest profits into new value-expanding projects and/or hoard cash on the balance sheet may make sense conceptually, but dividend paying cultures instill a self-disciplining credo that can better ensure proper capital stewardship by corporate boards. All too often excess capital is treated as funny money, only to be flushed away by overpaying for some high-profile acquisition, or meaningless share buybacks that merely offset generous equity grants to employees.

So, when looking at new and existing investments, consider the importance of dividend payments and dividend growth potential. Investing in an attractively priced sapling with appealing growth prospects can lead to incredibly fruitful returns.

Read the Whole WSJ Article on Dividends

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and WMT, but at the time of publishing SCM had no direct positions in BAC, WFC, C, BP, PG, KO, BUD, WFC, AXP, Lehman Brothers, Visteon, Tribune, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Forecasting Recipe: Trend Analysis & Sustainability

Forecasting financial performance of a company requires a fairly simple recipe: one part trend analysis and one part determining sustainability. On the surface, forecasting sounds pretty easy. While discovering certain financial trends can be straightforward, the ability to ascertain the durability of a trend can become endlessly complex.

Before you become Nostradamus and spreadsheet your way to the Wall Street Hall of Fame, an accurate forecaster must first build a firm understanding of a company and the underlying industry. Unfortunately for the predictor, not all companies and industries are created equally. Evaluating the profit dynamics of Cheesecake Factory Inc. (CAKE), an upscale casual chain of restaurants, is quite different from deciphering the financials of 3SBio (SSRX), a Chinese biotech company focused on recombinant products. Regardless of the thorniness of the company or industry, before you can truly look out into the future, the investor should learn the language of the company. For example, learning the importance of “comparable store sales” and “sales per square foot” for CAKE may be just as important as learning about the “Phase III FDA trial endpoint” and “pipeline” for SSRX.

Because you could spend a lifetime following just one company – for instance General Electric Co. (GE) or Microsoft Corp. (MSFT) – and never make an investment, you would probably be better served by applying a framework that allows you to research and analyze multiple industries and companies. There are various tools, whether you consider Harvard professor Michael Porter’s Five Forces or SWOT analysis (Strengths Weaknesses Opportunities Threats), and each provides a template or process to use when tearing apart specific companies and industries.

Nuts & Bolts of Forecasting

Before you can identify a trend, you first need to gather the data. For all companies I examine, I first compile a quarterly and annual income statement, balance sheet, and cash flow statement – those that have followed me know the extreme importance I place on the cash flows of a business. In general a good start is to create common size financial statements for the income statement and balance sheet. Basically, this exercise creates an income statement and balance sheet in percentage terms – usually expressed as a percentage of net sales (income statement) and as a percentage of total assets (balance sheet). Earnings forecasts are often used as a logical starting point for driving the shape of future results across the financials, but further insight can be gleaned by comparing year-over-year (this year vs. last) and sequential (this quarter vs. last quarter) growth rates for key figures.

These common statements will then serve as the foundation of identifying the trends, and force the forecaster to seek answers to random questions like these?

- Why is depreciation expense going down even though the company is expanding retail stores?

- Gross margins increased for seven consecutive quarters for a total of 250 basis points (2.5%), however in the recent quarter margins declined by 175 basis points…why?

- Long-term debt increased by $200 million in the current quarter, but if the company just issued $325 million in equity last quarter, then why do they need new capital?

Many of these types of questions may have logical explanations, but by getting answers the analyst will be in a position to better understand the business issues affecting financial performance and to better forecast future economic values.

Forecasting Your Way to Wrongness

A lot can go wrong with forecasting, principally in the assumptions used for the forecast. As the character Felix Unger from the Odd Couple stated, “You should never “assume.” You see, when you “assume,” you make an “ass”… out of “you”… and “me.”” Often assumptions do not consider the inclusion of important economic shocks or unexpected factors, such as recessions, currency fluctuations, management turnover, lawsuits, accounting changes, new products, restructurings, acquisitions, divestitures, flash crashes, Greek debt downgrades, regulatory reform…yada…yada…yada (you get the idea). To get a better sense for a range of outcomes, sensitivity analysis can be employed to determine a “base case” outcome in conjunction with a rosier “upside case” and more conservative “downside case.” Worth noting is the impact debt levels can have on the variance of outcomes – I think Bear Stearns and Lehman Brothers would concur with this point.

Pinpointing variable financial figures is quite difficult. Different companies and industries inherently have more or less predictable attributes. Predicting when the sun will rise and set is quite a bit more predictable than predicting what Intel Corp’s (INTC) gross margins will be on a quarterly basis. As mentioned earlier, layering on debt can increase the volatility of earnings forecasts as well.

Forecasting is essential in the investment world, but even if you were the best forecaster in the world, investors cannot disregard the importance of valuation skills. The art of valuation is just as important, if not more important than being right on your financial scenarios.

All in all, the recipe of forecasting sounds simple if you look at the basic ingredients of trend and sustainability analysis. However, before the ultimate forecast comes out of the oven, this straightforward recipe requires a lot of preparation, whether it is slicing and dicing cash flow figures, whipping up some margin trends, or measuring up sales growth. Any way you cut it, systematically following a recipe of trend and sustainability analysis is a non-negotiable requirement if you want to heat up superior financial results.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct positions in GE, MSFT, CAKE, SSRX, INTC, JPM/Bear Stearns, Lehman Brothers, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

The Accomplished Mole – Seth Klarman

I do quite a bit of reading and in my spare time I came across something very interesting. Here are some of the characteristics that describe this unique living mammal: 1) You will rarely see this creature in the open; 2) It roams freely and digs in deep, dark areas where many do not bother looking; and 3) This active being has challenged eyesight.

If you thought I was talking about a furry, burrowing mole (Soricomorpha Talpidae) you were on the right track, but what I actually was describing was legendary value investor Seth Klarman. He shares many of the same features as a mole, but has made a lot more money than his very distant evolutionary cousin.

The Making of a Legend

Photo source: SuperInvestorDigest.com

Before becoming the President of The Baupost Group, a Boston-based private investment partnership which manages about $22 billion in assets on behalf of wealthy private families and institutions, he worked for famed value investors Max Heine and Michael Price of the Mutual Shares (purchased by Franklin Templeton Investments). Klarman also published a classic book on investing, Margin of Safety, Risk Averse Investing Strategies for the Thoughtful Investor, which is now out of print and has fetched upwards of $1,000-2,000 per copy in used markets like Amazon.com (AMZN).

Klarman chooses to keep a low public profile, but recently his negative views on stock market and inflation risk have filtered out into the public domain. Nonetheless, he is still optimistic about certain distressed opportunities and believes the financial crisis has cultivated a more favorable, less competitive environment for investment managers due to the attrition of weaker investors.

Philosophy

Klarman despises narrow mandates – they are like shackles on potential returns. Opportunities do not lay dormant in one segment of the financial markets. Investors are fickle and fundamentals change. He believes superior results are achieved through a broadening of mandates. He prefers to invest in areas off the proverbial beaten path – the messier and more complicated the situation, the better. Currently his funds have significant investments in distressed debt instruments, many of which were capitulated forced sales by funds that are unable to hold non-investment grade debt.

In order to make his wide net point to investing, Klarman uses real estate as an illustration device. For example, investors do not need to limit themselves to publicly traded REITs (Real Estate Investment Trusts) – they can also invest in the debt of a REIT, convertible real estate debt, equity of property (such as own building), bank loan on a building, municipal bond that’s backed by real estate, or commercial/residential mortgage backed securities.

Klarman summarizes his thoughts by saying:

“If you have a broader mandate, they let you own all kinds of debt, all kinds of equity. Perhaps some private assets, like real estate. Perhaps hold cash when you can’t find anything great to do. You now have more weapons at your disposal to take advantage of conditions in the market.”

Klarman’s 3 Underlying Investment Pillars

Besides mentors Heine and Price, Klarman is quick to highlight his investment philosophy has been shaped by the likes of Warren Buffett and Benjamin Graham, among others. In addition to many of the basic tenets espoused by these investment greats, Klarman adds these three main investment pillars to his repertoire:

1) Focus on risk first (the probability of loss) before return. Determine how much capital you can lose and what the probability of that loss is. Also, do not confuse volatility with risk. Volatility creates opportunities.

2) Absolute performance, not relative performance, is paramount. The world is geared towards relative performance because of asset gathering incentives. Wealthy investors and institutions are more focused on absolute returns. Focus on benchmarks will insure mediocrity.

3) Concentrate on bottom-up research, not top down. Accurately forecasting macroeconomic trends and also profiting from those predictions is nearly impossible to do over longer periods of time.

These are great, but represent just a few of his instructional nuggets.

Performance

I did some digging regarding Klarman’s performance, and given the range of markets experienced over the last 25+ years, the results are nothing short of spectacular. Here is what I dug up from the Outstanding Investor Digest:

“Since its February 1, 1983 [2008] inception through December 31st, his Baupost Limited Partnership Class A-1 has provided its limited partners an average annual return of 16.5% net of fees and incentives, versus 10.1% for the S&P 500. During the “lost decade”, Baupost obliterated the averages, returning 14.8% and 15.9% for the 5 and 10-year periods ending December 31st versus -2.2% and -1.4%, respectively, for the S&P.”

Here is some additional color from Market Folly on Klarman’s incredible feats:

“Despite Klarman’s typically high levels of cash [sometimes in excess of 50%], Baupost has still generated astonishing performance. It was up 22% in 2006, 54% in 2007, and around 27% in 2009. During the crisis in 2008, Klarman’s funds lost “between 7% and the low teens.” Still though, he certainly outperformed the market indices and much of his investment management brethren in a time of panic.”

Although Seth Klarman has plowed over the competition and remained underground from the mass media, it’s still extremely difficult to ignore the long-term record of success of this accomplished mole. In the short-run, volatility may hurt his performance – especially if holding 20-30% cash. But as I was told at a young age by my grandmother, it is not prudent to make mountains out of molehills. Apparently, Klarman’s grandma taught her mole-like grandson how to make mountains of money from hills of opportunities. Klarman’s investors certainly stand to benefit as he continues to dig for value-based gems.

Watch interesting but lengthy presentation video given by Seth Klarman

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, and AMZN, but at the time of publishing SCM had no direct positions in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}

{kind=link}