Posts filed under ‘Behavioral Finance’

Confusing Fear Bubbles with Stock Bubbles

With the Dow Jones Industrial Average approaching and now breaking the 16,000 level, there has been a lot of discussion about whether the stock market is an inflating bubble about to burst due to excessive price appreciation? The reality is a fear bubble exists…not a valuation bubble. This fear phenomenon became abundantly clear from 2008 – 2012 when $100s of billions flowed out of stocks into bonds and trillions in cash got stuffed under the mattress earning near 0% (see Take Me Out to the Stock Game). The tide has modestly turned in 2013 but as I’ve written over the last six months, investor skepticism has reigned supreme (see Most Hated Bull Market Ever & Investors Snore).

Volatility in stocks will always exist, but standard ups-and-downs don’t equate to a bubble. The fact of the matter is if you are reading about bubble headlines in prominent newspapers and magazines, or listening to bubble talk on the TV or radio, then those particular bubbles likely do not exist. Or as strategist and investor Jim Stack has stated, “Bubbles, for the most part, are invisible to those trapped inside the bubble.”

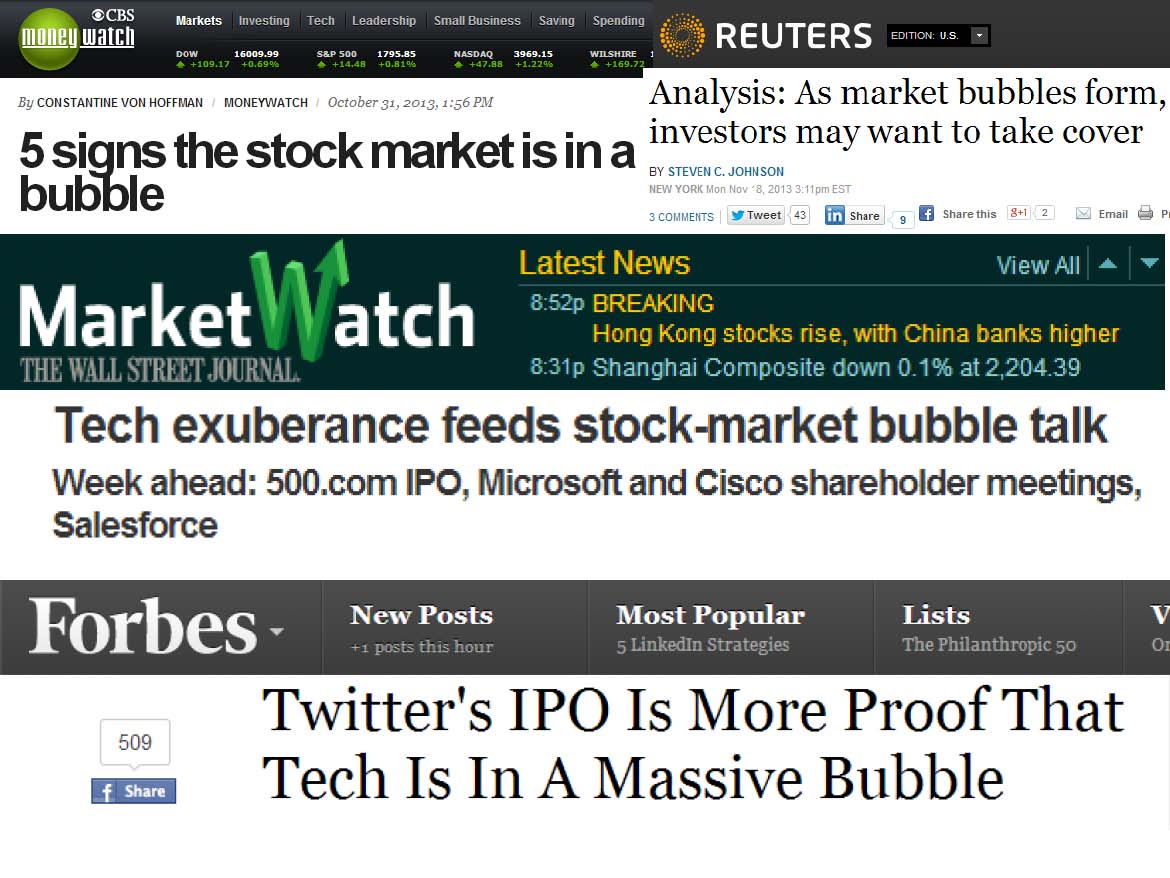

All the recent bubble talk scattered over all the media outlets only bolsters my fear case more. If we actually were in a stock bubble, you wouldn’t be reading headlines like these:

From 1,300 Bubble to 5,000

If you think identifying financial bubbles is easy, then you should buy former Federal Reserve Chairman Alan Greenspan a drink and ask him how easy it is? During his chairmanship in late-1996, he successfully managed to identify the existence of an expanding technology bubble when he delivered his infamous “irrational exuberance” speech. The only problem was he failed miserably on his timing. From the timing of his alarming speech to the ultimate pricking of the bubble in 2000, the NASDAQ index proceeded to more than triple in value (from about 1,300 to over 5,000).

Current Fed Chairman Ben Bernanke was no better in identifying the housing bubble. In his remarks made before the Federal Reserve Board of Chicago in May 2007, Bernanke had this to say:

“…We believe the effect of the troubles in the subprime sector on the broader housing market will likely be limited, and we do not expect significant spillovers from the subprime market to the rest of the economy or to the financial system. The vast majority of mortgages, including even subprime mortgages, continue to perform well.”

If the most powerful people in finance are horrible at timing financial market bubbles, then perhaps you shouldn’t stake your life’s savings on that endeavor either.

Bubbles History 101

Each bubble is unique in its own way, but analyzing previous historic bubbles can help understand future ones (see Sleeping Through Bubbles):

• Dutch Tulip-Mania: About 400 years ago in the 1630s, rather than buying a new house, Dutch natives were paying over $60,000 for tulip bulbs.

• British Railroad Mania: The overbuilding of railways in Britain during the 1840s.

• Roaring 20s: Preceding the Wall Street Crash of 1929 (-90% plunge in the Dow Jones Industrial average) and Great Depression, the U.S. economy experienced an extraordinary boom during the 1920s.

• Nifty Fifty: During the early 1970s, investors and traders piled into a set of glamour stocks or “Blue Chips” that eventually came crashing down about -90%.

• Japan’s Nikkei: The value of the Nikkei index increased over 450% in the eight years leading up to the peak of 38,957 in December 1989. Today, almost 25 years later, the index stands at about 15,382.

• Tech Bubble: Near the peak of the technology bubble in 2000, stocks like JDS Uniphase Corp (JDSU) and Yahoo! Inc (YHOO) traded for over 600x’s earnings. Needless to say, things ended pretty badly once the bubble burst.

As long as humans breathe, and fear and greed exist (i.e., forever), then we will continue to encounter bubbles. Unfortunately, we are unlikely to be notified of future bubbles in mainstream headlines. The objective way to unearth true economic bubbles is by focusing on excessive valuations. While stock prices are nowhere near the towering valuations of the technology and Japanese bubbles of the late 20th century, the bubble of fear originating from the 2008-2009 financial crisis has pushed many long-term bond prices to ridiculously high levels. As a result, these and other bonds are particularly vulnerable to spikes in interest rates (see Confessions of a Bond Hater).

Rather than chasing bubbles and nervously fretting over sensationalistic headlines, you will be better served by devoting your attention to the creation of a globally diversified investment portfolio. Own a portfolio that integrates a wide range of asset classes, and steers clear of popularly overpriced investments that the masses are talking about. When fear disappears and everyone is clamoring to buy stocks, you can be confident the stock bubble is ready to burst.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in TWTR, JDSU, YHOO or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Sitting on the Sidelines: Fear & Selective Memory

Fear is a motivating (or demotivating) emotion that can force individuals into suboptimal actions. The two main crashes of the 2000s (technology & housing bubbles) coupled with the mini-crises (e.g., flash crash, European crisis, debt ceiling, sequestration, fiscal cliff, etc.) have scared millions of investors and trillions of dollars to sit on the sidelines. Financial paralysis may be great in the short-run for bruised psyches and egos, but for the passive onlookers, the damage to retirement accounts can be crippling.

Selective memory is a great coping mechanism for those investors sitting on the sidelines as well. Purposely forgetting your wallet at a group dinner may be beneficial in the near-term, but repeated incidents will result in lost friends over the long-run. Similarly, most gamblers frequenting casinos tend to pound their chests when bragging about their wins, however they tend to conveniently forget about all the losses. These same reality avoidance principles apply to investing.

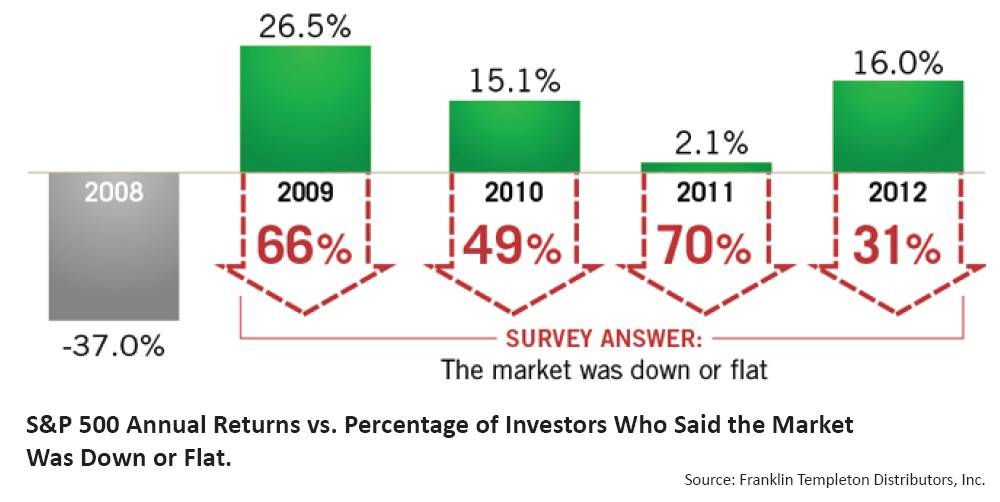

A recent piece written by CEO Bill Koehler at Tower Wealth Managers, entitled The Fear Bubble highlights a survey conducted by Franklin Templeton. In the study, investors were asked how the stock market performed in 2009-2012. As you can see from the chart below, perception is the polar opposite of reality (actual gains far exceeded perceived losses):

Source: Franklin Templeton via Tower Wealth Managers

With so many investors sitting on the sidelines in cash or concentrated in low-yielding bonds and gold, I suppose the results shouldn’t be too surprising. Once again, selective memory serves as a wonderful tool to bury the regrets of missing out on a financial market recovery of a lifetime.

Humans also have a predisposition to seek out people who share similar views, even though accumulating different viewpoints ultimately leads to better decisions. Morgan Housel at The Motley Fool just wrote an article, Putting a Gap Between You and Stupid, explaining how individuals should seek out others who can help protect them from harmful biases. A scientific study referenced in the article showed how the functioning of biased brains literally shuts down:

“During the 2004 presidential election, psychologist Drew Westen of Emory University and his colleagues studied the brains of 15 “committed” Democrats and 15 “committed” Republicans with an MRI scanner. Each group was shown a collection of contradictory statements made by George W. Bush and John Kerry. Not surprisingly, the partisans were quick to call out contradictions made by the opposing party, and made up all kinds of justifications to rationalize quotes made by their own side’s candidate. But here’s what’s scary: The participants weren’t just being stubborn. Westen found that areas of their brains that control reasoning and logic virtually shut down when confronted with a conflicting view of their preferred candidate.”

Rather than letting emotions rule the day, the proper approach is to stick to unbiased numbers like valuations, yields, fees, and volatility. If you continually make mistakes; you aren’t disciplined enough; or you don’t like investing; then find a trusted advisor who uses an objective financial approach. Opportunistically taking advantage of volatility, instead of knee-jerk reactions is the preferred approach. For those people sitting on the sidelines and using selective memory, you may feel better now, but you will eventually have to get in the game, if you don’t want to lose the retirement account game.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is the information to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Investing: Coin Flip or Skill?

The Sidoxia Monthly Newsletter will be released in a few days (subscribe on right side of the page), so here is an Investing Caffeine classic to tide you over until then:

Everyone believes they are above-average drivers and most investors believe successful investing can be attributed to skill. Michael Mauboussin, author and Chief Investment Strategist at Legg Mason Capital Management, tackles the issue of how important a role luck plays in various professional activities, including investing (read previous IC article on Mauboussin) in his meaty 42-page thought piece, Untangling Skill and Luck.

Skill Litmus Test

Whenever someone becomes successful or a sports team wins, doubters often respond with the response, “Well, they are just lucky.” For some, the intangible factor of luck can be difficult to measure, but for Mauboussin, he has a simple litmus test to evaluate the level of skill and luck credited to a professional activity:

“There’s a simple and elegant test of whether there is skill in an activity: ask whether you can lose on purpose. If you can’t lose on purpose, or if it’s really hard, luck likely dominates that activity. If it’s easy to lose on purpose, skill is more important.”

Mauboussin uses various sports and games as tools to explain the relative importance that skill (or lack thereof) plays in determining an outcome. At one extreme end of the spectrum you have a brain game like chess, in which a skillful chess pro could beat an amateur 1,000 times in a 1,000 matches. In the field of professional sports, at the other end of the spectrum, Mauboussin hammers home the relative significance luck contributes in professional baseball:

“In major league baseball the worst team will beat the best team in a best-of-five series about 15 percent of the time.“

Here is a skill-luck continuum provided by Mauboussin:

Source: Legg Mason Capital Management

Streaks vs. Mean Reversion

Mr. Mauboussin spends a great deal of time exploring the implications of skill and luck in relation to streaks and mean reversion. In the streak department, Mauboussin uses Joe DiMaggio’s record 56-consecutive game hitting stretch. He acknowledges the presence of luck, but skill is a prerequisite:

“Not all skillful performers have streaks, but all long streaks of success are held by skillful performers.”

When detailing streaks, Mauboussin may also be defending his fellow Legg Mason colleague Bill Miller (see Revenge of the Dunce), who had an incredible 15 consecutive year of besting the S&P 500 index before mean reverting back to lousy human-like returns.

This is a nice transition into his discussion about mean reversion because Mauboussin basically states this reversion concept dominates activities laden with luck (as shown in the Skill-Luck Continuum chart above). Time will tell whether Miller’s streak was due to skill, if he can put together another streak, or whether his streak was merely a lucky fluke. Unlike the judicial world, investment managers are often treated as guilty until proven innocent. For now, Miller’s 1991-2005 streak is being treated as luck by many in the investment community, rather than skill.

Nobel-prize winner Paul Samuelson may believe differently since he concedes the existence of skillful investing:

“It is not ordained in heaven, or by the second law of thermodynamics, that a small group of intelligent and informed investors cannot systematically achieve higher mean portfolio gains with lower average variabilities. People differ in their heights, pulchritude, and acidity. Why not their P.Q. or performance quotient?”

Peter Lynch’s +29% annual return from 1977-1990 is another streak on which historians can chew (read more on Lynch). I, like Samuelson, will give Lynch the benefit of the doubt.

Creating a Skillful Analytical Edge

Unlike the process of mowing lawns, in which more applied work time generally equates to more lawns cut (i.e., more profits), the investment world doesn’t quite work that way. Many people could work all day, stare at their screen for 23 hours, trade off of useless information, and still earn lousy returns. When it comes to investing, more work does not necessarily produce better results. Mauboussin’s prescription is to create an analytical edge. Here is how he describes it:

“At the core of an analytical edge is an ability to systematically distinguish between fundamentals and expectations.”

Thinking like a handicapper is imperative to win in this competitive game, and I specifically addressed this in my previous Vegas-Wall Street article. Steven Crist sums up this indispensable concept beautifully:

“There are no “good” or “bad” horses, just correctly or incorrectly priced ones.”

A disciplined, systematic approach will incorporate these ideas, however all good investors understand the good processes can lead to bad outcomes in the short-run. By continually learning from mistakes, and refining the process with a constant feedback loop, the investment process can only get better. On the other hand, schizophrenically reacting to an endless flood of ever-changing information, or fearfully chasing the leadership du jour will only lead to pain and sorrow. Fortunately for you, you have skillfully completed this article, meaning financial luck should now be on your side.

Read full Mauboussin article (Untangling Skill and Luck) here

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. Radio interviews included opinions of Wade Slome – not advice. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is the information to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Most Hated Bull Market Ever

Life has been challenging for the bears over the last four years. For the first few years of the recovery (2009-2010) when stocks vaulted +50%, supposedly we were still in a secular bear market. Back then the rally was merely dismissed as a dead-cat bounce or a short-term cyclical rally, within a longer-term secular bear market. Then, after an additional +50% move the commentary switched to, “Well, we’re just in a long-term trading range. The stock market hasn’t done a thing in a decade.” With major indexes now hitting all-time record highs, the pessimists are backpedaling in full gear. Watching the gargantuan returns has made it more difficult for the bears to rationalize a tripling +225% move in the S&P 600 index (Small-Cap); a +214% move in the S&P 400 index (Mid-Cap); and a +154% in the S&P 500 index (Large-Cap) from the 2009 lows.

For the unfortunate souls who bunkered themselves into cash for an extended period, the return-destroying carnage has been crippling. Making matters worse, some of these same individuals chased a frothy over-priced gold market, which has recently plunged -30% from the peak.

Bonds have generally been an OK place to be as Europe imploded and domestic political gridlock both helped push interest rates to record-lows (e.g., tough to go lower than 0% on the Fed-Funds rate). But now, those fears have subsided, and the recent rate spike from Ben Bernanke’s “taper tantrum” has caused bond bulls to reassess their portfolios (see Fed Fatigue). Staring at the greater than -90% underperformance of bonds, relative to stocks over the last four years, has been a bitter pill to swallow for fervent bond believers. The record -$9.9 billion outflow from Mr. New Normal’s (Bill Gross) Pimco Total Return Fund in June (a 26-year record) is proof of this anxiety. But rather than chase an unrelenting stock market rally, stock haters and skeptics remain stubborn, choosing to place their bond sale proceeds into their favorite inflation-depreciating asset…cash.

Crash Diet at the Buffet

I’ve seen and studied many markets in my career, but the behavioral reactions to this most-hated bull market in my lifetime have been fascinating to watch. In many respects this reminds me of an investing buffet, where those participating in the nourishing market are enjoying the spoils of healthy returns, while the skeptical observers on the sidelines are on a crash diet, selecting from a stingy menu of bread and water. Sure, there is some over-eating, heartburn, and food coma experienced by those at the stock market table, but one can only live on bread and water for so long. The fear of losses has caused many to lose their investing appetite, especially with news of sequestration, slowing China, Middle East turmoil, rising interest rates, etc. Nevertheless, investors must realize a successful financial future is much more like an eating marathon than an eating sprint. Too many retirees, or those approaching retirement, are not responsibly handling their savings. As legendary basketball player and coach John Wooden stated, “Failing to prepare is preparing to fail.”

20 Years…NOT 20 Days

I will be the first to admit the market is ripe for a correction. You don’t have to believe me, just take a look at the S&P 500 index over the last four years. Despite the explosion to record-high stock prices, investors have had to endure two corrections averaging -20% and two other drops approximating -10%. Hindsight is 20-20, but at each of those fall-off periods, there were plenty of credible arguments being made on why we should go much lower. That didn’t happen – it actually was the opposite outcome.

For the vast majority of investing Americans, your investing time horizon should be closer to 20 years…not 20 days. People that understand this reality realize they are not smart enough to consistently outwit the market (see Market Timing Treadmill). If you were that successful at this endeavor, you would be sitting on your private, personal island with a coconut, umbrella drink.

Successful long-term investors like Warren Buffett recognize investors should “buy fear, and sell greed.” So while this most hated bull market remains fully in place, I will follow Buffett’s advice comfortably sit at the stock market buffet, enjoying the superior long-term returns put on my plate. Crash dieters are welcome to join the buffet, but by the time they finally sit down at the stock market table, I will probably have left to the restroom.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), including IJR, and IJH, but at the time of publishing, SCM had no direct position in BRKA/B, Pimco Total Return Fund, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Information Choking Your Money & Mood to Misery

Source: Photobucket

On a daily basis, I make my way into the office before the market opening bell, preparing myself to gorge on a massive heaping of news stories and headlines. But scarfing down tons of tweets and hundreds of headlines is not enough. Magazines, newspapers, conference calls, blogs, presentations, conferences, interviews, television clips, and software lists are but just a few additional aspects to my steady diet of information. Like shopping down each and every aisle of the grocery store, an annoying tendency I admittedly commit, there are plenty of healthy and unhealthy items to choose from. The key is identifying the items that are the best for your financial health. After carrying out this gluttonous information-stuffing business for more than twenty years, I’ve gotten much better at separating the data wheat from information chaff. This is critical in avoiding heartburn for my Sidoxia clients and me.

One might ask, “What harmless headline or innocent anecdote could possibly cause harmful financial indigestion?” I don’t know about you, but in recent months, gobbling down these following headlines without discretion can lead to a serious case of acid reflux:

- “Stocks Tumble as Bernanke Discusses Tapering” – USA Today

- “China’s Economy is Freezing Up. How Freaked Out Should We Be?” – Washington Post

- ” ‘Suffocating in the Streets’: Chemical Weapons Attack Reported in Syria” – NBC News

- “Europe’s Zombie Banks – Blight of the Living Dead” – The Economist

- “Threats from Extremists as Egypt Slides into Turmoil” – The Times

- “Japan Market Plunge Sparks Global Sell-Off” – Los Angeles Times

I think you get the idea. No wonder investors collectively are acting like a deer in headlights, resulting in declining stock market participation – a 15-year low (see Investing Caffeine’s DMV Economy)

In the world of competitive eating, the execution of improper consumption technique can lead to a so-called “reversal of fortune,” as can be experienced by the last video on my Investing Caffeine article, Baseball and Hot Dogs. Disciplined processes are needed to prevent such an event when devouring excessive amounts of information. This is a timely topic as Joey Chestnut recently set a new world record by eating 69 hot dogs in 10 minutes.

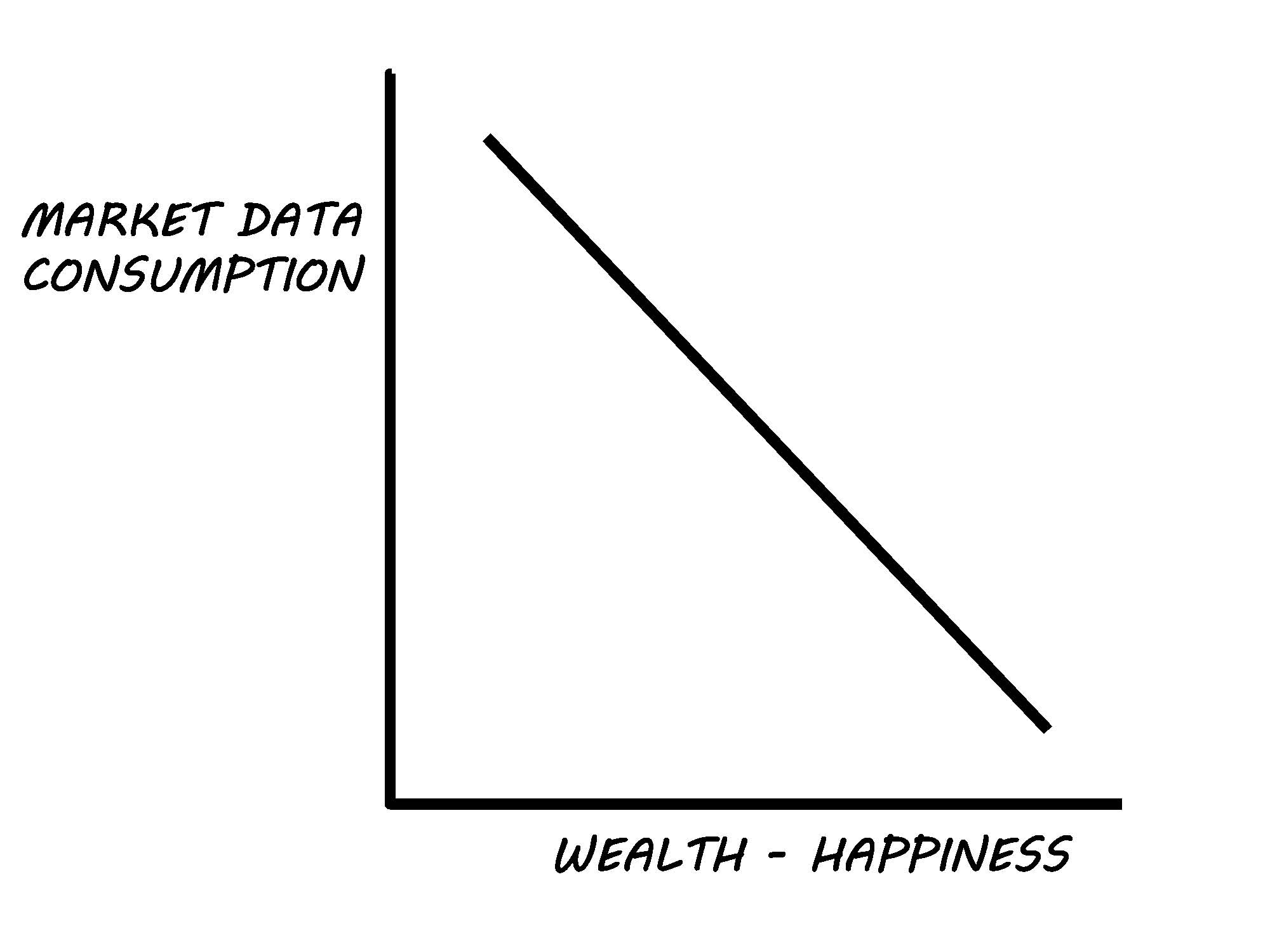

While digesting the avalanche of daily data is quite complex, understanding the harmful consequences of doing so is quite simple. Carl Richards, a contributor writer to the The New York Times and Morningstar Advisor does a great job of outlining the detrimental impact of information consumption on investors’ wealth and happiness through minimalist charts found at BehaviorGap.com.

Here is my co-mingled version of Richards’ work:

As Mark Twain said, “If you don’t read the newspaper, you are uninformed. If you do read the newspaper, you are misinformed.” It’s perfectly fine to remain current with major economic, political, and worldly events, but the consequences to overreacting to the ever-changing news flow can be disastrous to your financial and personal well-being. Managing your life savings can be stressful and if not managed correctly will damage your financial goals.

If you do not have the time, interest, or self-control to digest the massive buffet of endless information, do yourself a favor and find an experienced and trusted advisor that can assist you with the Heimlich maneuver, so you don’t choke on the infinite amount of data.

See also (Investing Caffeine: Age of Information Overload)

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and CMCSA, but at the time of publishing, SCM had no direct position in GCI, WPO, NYT, MORN or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

What’s Going on with This Crazy Market?!

The massive rally of the stock market since March 2009 has been perplexing for many, but the state of confusion has reached new heights as the stock market has surged another +2.0% in May, surpassing the Dow 15,000 index milestone and hovering near all-time record highs. Over the last few weeks, the volume of questions and tone of disbelief emanating from my social circles has become deafening. Here are some of the questions and comments I’ve received lately:

“Wade, why in the heck is the market up so much?”; “This market makes absolutely no sense!”; “Why should I buy at the peak when I can buy at the bottom?”; “With all this bad news, when is the stock market going to go down?”; “You must be shorting (betting against) this market, right?”

If all the concerns about the Benghazi tragedy, IRS conservative targeting, and Federal Reserve bond “tapering” are warranted, then it begs the question, “How can the Dow Jones and other indexes be setting new all-time highs?” In short, here are a few reasons:

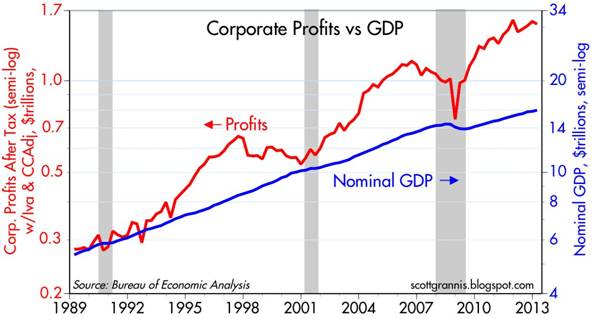

You hear a lot of noise on TV and read a lot of blathering in newspapers/blogs, but what you don’t hear much about is how corporate profits have about tripled since the year 2000 (see red line in chart above), and how the profit recovery from the recent recession has been the strongest in 55 years (Scott Grannis). The profit collapse during the Great Recession was closely chronicled in nail-biting detail, but a boring profit recovery story sells a lot less media advertising, and therefore gets swept under the rug.

II.) Reasonable Prices (Comparing Apples & Oranges):

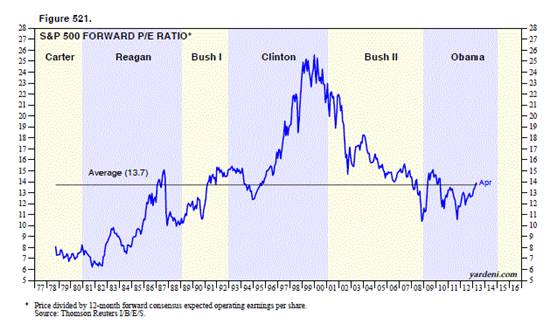

Source: Dr. Ed’s Blog

The Price-Earnings ratio (P/E) is a general barometer of stock price levels, and as you can see from the chart above (Ed Yardeni), current stock price levels are near the historical average of 13.7x – not at frothy levels experienced during the late-1990s and early 2000s.

Comparing Apples & Oranges:

At the most basic level of analysis, investors are like farmers who choose between apples (stocks) and oranges (bonds). On the investment farm, growers are generally going to pick the fruit that generates the largest harvest and provide the best return. Stocks (apples) have historically offered the best prices and yielded the best harvests over longer periods of time, but unfortunately stocks (apples) also have wild swings in annual production compared to the historically steady crop of bonds (oranges). The disastrous apple crop of 2008-2009 led a massive group of farmers to flood into buying a stable supply of oranges (bonds). Unfortunately the price of growing oranges (i.e., buying bonds) has grown to the highest levels in a generation, with crop yields (interest rates) also at a generational low. Even though I strongly believe apples (stocks) currently offer a better long-term profit potential, I continue to remind every farmer (investor) that their own personal situation is unique, and therefore they should not be overly concentrated in either apples (stocks) or oranges (bonds).

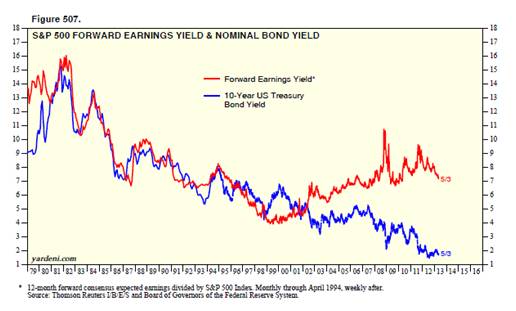

Source: Dr. Ed’s Blog

Regardless, you can see from the chart above (Dr. Ed’s Blog), the red line (stocks) is yielding substantially more than the blue line (bonds) – around 7% vs. 2%. The key for every investor is to discover an optimal balance of apples (stocks) and oranges (bonds) that meets personal objectives and constraints.

III.) Skepticism (Market Climbs a Wall of Worry):

Source: Calafia Beach Pundit

Although corporate profits are strong, and equity prices are reasonably priced, investors have been withdrawing hundreds of billions of dollars from equity funds (negative blue lines in chart above – Calafia Beach Pundit). While the panic of 2008-2009 has been extinguished from average investors’ psyches, the Recession in Europe, slowing growth in China, Washington gridlock, and the fresh memories of the U.S. financial crisis have created a palpable, nervous skepticism. Most recently, investors were bombarded with the mantra of “Selling in May, and Going Away” – so far that advice hasn’t worked so well. To buttress my point about this underlying skepticism, one need not look any further than a recent CNBC segment titled, “The Most Confusing Market Ever” (see video below):

Source: CNBC

It’s clear that investors remain skittish, but as legendary investor Sir John Templeton so aptly stated, “Bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria.” The sentiment pendulum has been swinging in the right direction (see previous Investing Caffeine article), but when money flows sustainably into equities and optimism/euphoria rules the day, then I will become much more fearful.

Being a successful investor or a farmer is a tough job. I’ll stop growing apples when my overly optimistic customers beg for more apples, and yields on oranges also improve. In the meantime, investors need to remember that no matter how confusing the market is, don’t put all your oranges (bonds) or apples (stocks) in one basket (portfolio) because the financial markets do not need to get any crazier than they are already.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Fence-Sitting: The Elusive Art of More Data and Pullbacks

The world of financial markets is full of fence-sitters, especially in the professional realm. Why? Well, for starters, fence-sitting provides the luxury of never being wrong. If fence-squatting observers do nothing and provide no opinions, then they cannot by definition be wrong or mistaken. Why should a professional put their neck out for an economic, sector, or investment specific forecast, if there is a potential of looking stupid or losing a job?

For many, the consequences of possibly being wrong feel so horrendous that participants choose instead to sit on the non-committal fence. In most cases, the fence posts on any financial issue or investment align along the comfort of consensus thinking. Unfortunately, consensus thinking has a limited shelf life, because the views held by the majority are constantly changing. Repeatedly modifying personal opinions to match consensus views may prevent the bruising of egos, however, this naïve strategy can be destructive to long-term returns. Here are a few examples:

2000

Consensus View: New Normal tech stocks will continue explosive growth; Consensus Outcome: Wrong; Investor Net Result: Losses and/or Lost Profits.

2006

Consensus View: Home prices will rise forever and leverage is beautiful; Consensus Outcome: Wrong; Investor Net Result: Losses and/or Lost Profits.

2010

Consensus View: Greece and European collapse to cause a double-dip global recession; Consensus Outcome: Wrong; Investor Net Result: Losses and/or Lost Profits.

2011

Consensus View: U.S. credit downgrade will be bad for Treasuries and rates; Consensus Outcome: Wrong; Investor Net Result: Losses and/or Lost Profits.

2012

Consensus View: Uncertainty surrounding election bad for equities; Consensus Outcome: Wrong; Investor Net Result: Losses and/or Lost Profits.

2012

Consensus View: China’s slowing growth and real estate bubble expected to cause a global double-dip recession; Consensus Outcome: Wrong; Investor Net Result: Losses and/or Lost Profits.

2012

Consensus View: Impending fiscal cliff bad for equities; Consensus Outcome: Wrong; Investor Net Result: Losses and/or Lost Profits.

2013

Consensus View: Debt ceiling debate bad for equities; Consensus Outcome: ???; Investor Net Result: ???.

2013

Consensus View: Looming sequestration bad for equities; Consensus Outcome: ???; Investor Net Result: ???.

In recent years the market has continued to climb a wall of worry, but will this year be different? We shall soon see.

Placing the concern du jour aside, if consensus fears coalesce around a specific upcoming event, chances are that particular issue is already factored into existing expectations and price structures. Therefore, rather than wasting personal “worry” bandwidth on those fears, investor anxiety should be dedicated to less prevalent but potentially more impactful unknown concerns. Or if you need clarification about the unknowns to worry about, perhaps Donald Rumsfeld can clarify the situation by highlighting the risk of “unknown unknowns”:

I Love Data and Pullbacks!

When faced with apprehension or uncertainty, many fence-sitting investors revert to wanting more data or waiting for a better price. For example, I often hear, “I love stock XYZ, but I want to wait for the earnings to come out,” or analyst day, or share buyback announcement, or merger closing, or restructuring, etc., etc., etc. For strategists and economists, they are famished for the next critically irrelevant weekly jobless claims number, Federal Reserve policy minutes, ISM monthly manufacturing data, or latest consumer confidence figure.

More data for fence sitters is not sufficient. I often listen to stock-pickers say, “I love XYZ stock, but not at the current $52.50 price, but I’ll back up the truck at $51.50!” Okay, so you’re telling me that you think the stock is worth +40% more, but you want to litigate the purchase price over $1?!

Sadly, there is a cost for all this fence-sitting: a) if good news comes out, investment prices catapult higher and the investor is stuck with a pricier investment; b) if bad news comes out, that long-awaited price pullback is usually not acted upon because fundamentals have now deteriorated; or c) in many cases the price grinds higher before the long-awaited jewel of information is disseminated. The net result is further fence-sitting paralysis, which paradoxically is not helped by more information or a price pullback.

The other reason fence-sitters say or do nothing is because articulating a gloomy thesis simply sounds smarter. For instance, saying “The reason I’m on the sidelines is because we are in a secular bear market due to the debasement of our currency as a result of inflationary Fed monetary policies,” sounds smarter and more compelling than “Stocks are cheap and are already factoring in a lot of negativity.”

Investing is an unbelievably challenging endeavor, but for those fence-sitters with an insatiable appetite for more data and elusive pullbacks, I humbly point out, there is an infinite amount of information that regenerates itself daily. In addition, there is nothing wrong with having a disciplined valuation process in place, but if your best investment ideas are predicated on a minor pullback, then enjoy watching your returns wither away…as you sit on your cozy fence.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Uncertainty: Love It or Hate It?

Source: Photobucket

Uncertainty is like a fin you see cutting through the water – many people are uncertain whether the fin sticking out of the water is a great white shark or a dolphin? Uncertainty generates fear, and fear often produces paralysis. This financially unproductive phenomenon has also reared its ugly fin in the investment world, which has led to low-yield apathy, and desensitization to both interest rate and inflation risks.

The mass exodus out of stocks into bonds worked well for the very few that timed an early 2008 exit out of equities, but since early 2009, the performance of stocks has handily trounced bonds (the S&P has outperformed the bond market (BND) by almost 100% since the beginning of March 2009, if you exclude dividends and interest). While the cozy comfort of bonds has suited investors over the last five years, a rude awakening awaits the bond-heavy masses when the uncertain economic clouds surrounding us eventually lift.

The Certainty of Uncertainty

What do we know about uncertainty? Well for starters, we know that uncertainty cannot be avoided. Or as former Secretary of the Treasury Robert Rubin stated so aptly, “Nothing is certain – except uncertainty.”

Why in the world would one of the world’s richest and most successful investors like Warren Buffett embrace uncertainty by imploring investors to “buy fear, and sell greed?” How can Buffett’s statement be valid when the mantra we continually hear spewed over the airwaves is that “investors hate uncertainty and love clarity?” The short answer is that clarity is costly (i.e., investors are forced to pay a cherry price for certainty). Dean Witter, the founder of his namesake brokerage firm in 1924, addressed the issue of certainty in these shrewd comments he made some 78 years ago, right before the end of worst bear market in history:

“Some people say they want to wait for a clearer view of the future. But when the future is again clear, the present bargains will have vanished.”

Undoubtedly, some investors hate uncertainty, but I think there needs to be a distinction between good investors and bad investors. Don Hays, the strategist at Hays Advisory, straightforwardly notes, “Good investors love uncertainty.”

When everything is clear to everyone, including the novice investing cab driver and hairdresser, like in the late 1990s technology bubble, the actual risk is in fact far greater than the perceived risk. Or as Morgan Housel from Motley Fool sarcastically points out, “Someone remind me when economic uncertainty didn’t exist. 2000? 2007?”

What’s There to Worry About?

I’ve heard financial bears argue a lot of things, but I haven’t heard any make the case there is little uncertainty currently. I’ll let you be the judge by listing these following issues I read and listen to on a daily basis:

- Fiscal cliff induced recession risks

- Syria’s potential use of chemical weapons

- Iran’s destabilizing nuclear program

- North Korean missile tests by questionable new regime

- Potential Greek debt default and exit from the eurozone

- QE3 (Quantitative Easing) and looming inflation and asset bubble(s)

- Higher taxes

- Lower entitlements

- Fear of the collapse in the U.S. dollar’s value

- Rigged Wall Street game

- Excessive Dodd-Frank financial regulation

- Obamacare

- High Frequency Trading / Flash Crash

- Unsustainably growing healthcare costs

- Exploding college tuition rates

- Global warming and superstorms

- Etc.

- Etc.

- Etc.

I could go on for another page or two, but I think you get the gist. While I freely admit there is much less uncertainty than we experienced in the 2008-2009 timeframe, investors’ still remain very cautious. The trillions of dollars hemorrhaging out of stocks into bonds helps make my case fairly clear.

As investors plan for a future entitlement-light world, nobody can confidently count on Social Security and Medicare to help fund our umbrella-drink-filled vacations and senior tour golf outings. Today, the risk of parking your life savings in low-rate wealth destroying investment vehicles should be a major concern for all long-term investors. As I continually remind Investing Caffeine readers, bonds have a place in all portfolios, especially for income dependent retirees. However, any truly diversified portfolio will have exposure to equities, as long as the allocation in the investment plan meshes with the individual’s risk tolerance and liquidity needs.

Given all the uncertain floating fins lurking in the economic background, what would I tell investors to do with their hard-earned money? I simply defer to my pal (figuratively speaking), Warren Buffett, who recently said in a Charlie Rose interview, “Overwhelmingly, for people that can invest over time, equities are the best place to put their money.” For the vast majority of investors who should have an investment time horizon of more than 10 years, that is a question I can answer with certainty.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) including BND, but at the time of publishing SCM had no direct positions in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Decision Making on Freeways and in Parking Lots

Many drivers here in California adhere to the common freeway speed limit of 65 miles per hour, while some do not (I’ll take the 5th). In the vast majority of cases, racing to your destination at these faster speeds makes perfect sense. However, driving 65 mph through the shopping mall parking lot could get you killed, so slower driving is preferred in this instance. Ultimately, the specific environment and situation will dictate the rational and prudent driving speed. Decision making works in much the same way, and Daniel Kahneman, a Nobel Prize winner, has encapsulated his decades of research in psychology and economics in his most recent book, Thinking, Fast and Slow.

Much of Kahneman’s big ideas are analyzed through the lenses of “System 1” and “System 2” – the fast and slow decision-making processes persistently used by our brains. System 1 thinking is our intuition in the fast lane, continually making judgments in real-time. Our System 1 hunches are often correct, but because of speedy, inherent biases and periodic errors this process can cause us to miss an off-ramp or even cause a conclusion collision. System 2, on the other hand, is the slower, methodical decision-making process in our brains that keeps our hasty System 1 process in check. Although little mental energy is exerted by using System 1, a great deal of cerebral horsepower is required to use System 2.

Summarizing 512 pages of Kahneman’s book in a single article may be challenging, nevertheless I will do my best to summarize some of the interesting highlights and anecdotes. A multitude of Kahneman’s research is reviewed, but a key goal of the book is designed to help individuals identify errors in judgment and biases, in order to lower the prevalence of mental mistakes in the future.

Over Kahneman’s 50+ year academic career, he has uncovered an endless string of flaws in the human thought process. To bring those mistakes to life, he uses several mind experiments to illustrate them. Here are a few:

Buying Baseball: We’ll start off with a simple Kahneman problem. If a baseball bat and a ball cost a total of $1.10, and the bat costs $1 more than the ball, then how much does the ball cost? The answer is $0.10, right? WRONG! Intuition and the rash System 1 forces most people to answer $0.10 cents for the ball, but after going through the math it becomes clear that this gut answer is wrong. If the ball is $0.10 and the bat is $1 more, then that would mean the bat costs $1.10, making the total $1.20…WRONG! This is clearly a System 2 problem, which requires the brain to see a $0.05 ball plus $1.05 bat equals $1.10…CORRECT!

The Invisible Gorilla: As Kahneman points out, humans can be blind to the obvious and blind to our blindness. To make this point he references an experiment and book titled Invisible Gorilla, created by Chritopher Chabris and Daniel Simons. In the experiment, three players wearing white outfits pass a basketball around at the same time that a group of players wearing black outfits pass around a separate basketball. The anomaly in the experiment occurs when someone in a full-sized gorilla outfit goes prancing through the scene for nine full seconds. To the surprise of many, about half of the experiment observers do not see the gorilla. In addition, the gorilla-blind observers deny the existence of the large, furry animal when confronted with recorded evidence (see video below).

Green & Red Dice: In this thought experiment, Kahneman describes a group presented with a regular six-sided die with four green sides (G) and two red sides (R), meaning the probability of the die landing on green (G) is is much higher than the probability of landing on red (R). To make the experiment more interesting, the group is provided a cash prize for picking the highest probability scenario out of the following three sequences: 1) R-G-R-R-R; 2) G-R-G-R-R-R; and 3) G-R-R-R-R-R. Although most participants pick sequence #2 because it has the most greens (G) in it, if one looks more closely, sequence #2 is the same as #1 except for sequence #2 has an additional green (G). Therefore, the highest probability winning answer should be sequence #1 because sequence #2 adds an uncertain roll that may or may not land on green (G).

While the previous experiments described some notable human decision-making flaws, here are some more human flaws:

Anchoring Effect: Was Gandhi 114 when he died, or was Gandhi 35 when he died? Depending how the question is asked, asking the initial question first will skew the respondents answer to a higher age, because the respondents answer will be somewhat anchored to the number “114”. Similarly, the price a homebuyer would pay for a house will be influenced or anchored to the asking price. Another word used by some for anchoring is “suggestion”. If a subliminal suggestion is planted, people’s responses can become anchored to that idea.

Overconfidence: We encounter overconfidence in several forms, especially from what Kahneman calls the “Illusion of Pundits,” which is the confidence that comes with 20-20 hindsight experienced in our 24/7 media world. Or as Kahneman states in a different way, “The illusion that we understand the past fosters overconfidence in our ability to predict the future.” Driving is another example of overconfidence – very few people believe they are poor drivers. In fact, a well-known study shows that “90% of drivers believe they are better than average,” despite defying the laws of mathematics.

Risk Aversion: In Kahneman’s book, he also references risk aversion studies by Mathew Rabin and Richard Thaler. What the researchers discovered is that people appear to be irrational in the way they respond to certain risk scenarios. For example, people will turn down the following gambles:

A 50% chance to lose $100 and a 50% chance to win $200;

OR

A 50% chance to lose $200 and a 50% chance to win $20,000 .

Although rational math would indicate these are smart bets to take, however most people decline the game because humans on average weigh losses twice as much as gains (see also the Pleasure/Pain Principle). To get a better understanding of predictive human behavior, the real emotional costs of disappointment and regret need to be accounted for.

Truth Illusions: A reliable way to make people believe in falsehoods is through repetition. More exposure will breed more liking. In addition to normal conversations, these repetitive truth illusions can be witnessed in propaganda or advertising. Minimizing cognitive strain also reinforces points. Using bold, colored, and contrasted language is more convincing. Simpler language rather than more complex language is also more credible.

Narrative Fallacies: We humans have an innate desire to continually explain the causation of an event due to skill or stupidity – even if randomness is the best explanation.People try to make sense of the world, even though many outcomes have no straightforward explanation. Often times, a statistical phenomenon like “regression to the mean” can explain the results (i.e., outliers revert directionally toward averages). The “Sports Illustrated Jinx,” or the claim that a heralded cover story athlete will be subsequently cursed with bad performance, is used as a case in point. Actually, there is no jinx or curse, but often fickle luck disappears and athletic performance reverts to norms.

Kahneman on Stocks

Many of the principles in Kahneman’s book can be applied to the world of stocks and investing too. According to Kahneman, the investing industry has been built on an “illusion of skill,” or the belief that one person has better information than the other person. To make his point, Kahneman references research by Terry Odean, a finance professor at UC Berkely, who studied the records of 10,000 brokerage accounts of individual investors spanning a seven-year period and covering almost 163,000 trades. The net result showed dramatic underperformance by the individual traders and confirmed that stocks sold by the traders consistently did better than the stocks purchased.“Taking a shower and doing nothing” would have been better than the value destroying trading activity. In fact, the most active traders did much worse than those who traded the least. For professional managers the conclusions are not a whole lot different. “For a large majority of fund managers, the selection of stocks is more like rolling dice than like playing poker. Typically at least two out of every three mutual funds underperform the overall market in any given year,” says Kahneman. I don’t disagree, but I do believe, like .300 hitters in baseball, there are a few managers that can consistently outperform.

There are a lot of lessons to be learned from Daniel Kahneman’s book Thinking, Fast and Slow and I apply many of his conclusions to my investment practice at Sidoxia. We all race through decisions every day, but as he repeatedly points out, familiarizing ourselves with these common mental pitfalls, and also utilizing our more methodical and accurate System 2 thought process regularly, can create better decisions. Better decisions not only for our regular lives, but also for our investing lives. It’s perfectly OK to race down the mental freeway at 65 mph (or faster), but don’t forget to slow down occasionally, in order to avoid mental collisions.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Experts vs. Dart-Throwing Chimps

Daniel Kahneman, a professor of psychology at Princeton University, knows a few things about human behavior and decision making, and he has a Nobel Prize in Economics to prove it. We live in a complex world and our brains will often try to compensate by using shortcuts (or what Kahneman calls “heuristics” and “biases”), in hopes of simplifying complicated situations and problems.

When our brains become lazy, or we are not informed in a certain area, people tend to also listen to so-called experts or pundits to clarify uncertainties. In the process of their work, Kahneman and other researchers have discovered something – experts should be listened to as much as monkeys. Frequent readers of Investing Caffeine understand my shared skepticism of the talking heads parading around on TV (read first entry of 10 Ways to Destroy Your Portfolio)

Here is how Kahneman describes the reliability of professional forecasts and predictions in his recently published bestseller, Thinking, Fast and Slow:

“People who spend their time, and earn their living, studying a particular topic produce poorer predictions than dart-throwing monkeys who would have distributed their choices evenly over the options.”

Most people fall prey to this illusion of predictability created by experts, or this idea that more knowledge equates to better predictions and forecasts. One of the factors perpetuating this myth is the rearview mirror. In other words, human’s ability to concoct a credible story of past events creates a false confidence in peoples’ ability to accurately predict the future.

Here’s how Kahneman describes the phenomenon:

“The idea that the future is unpredictable is undermined every day by the ease with which the past is explained…Our tendency to construct and believe coherent narratives of the past makes it difficult for us to accept the limits of our forecasting ability. Everything makes sense in hindsight, a fact financial pundits exploit every evening as they offer convincing accounts of the day’s events. And we cannot suppress the powerful intuition that what makes sense in hindsight today was predictable yesterday. The illusion that we understand the past fosters overconfidence in our ability to predict the future.”

Even when experts are wrong about their predictions, they tend to not accept accountability. Rather than take responsibility for a bad prediction, Philip Tetlock says the errors are often attributed to “bad timing” or an “unforeseeable event.” Philip Tetlock, a psychologist at the University of Pennsylvania did a landmark twenty-year study, which was published in his book Expert Political Judgment: How Good Is It? How Can We Know? (read excellent review in The New Yorker). In the study Tetlock interviewed 284 economic and political professionals and collected more than 80,000 predictions from them. The results? The experts did worse than blind guessing.

Based on the extensive training and knowledge of these experts, many of them develop a false sense of confidence in their predictions. Or as Tetlock explains it, “They [experts] are just human in the end. They are dazzled by their own brilliance and hate to be wrong. Experts are led astray not by what they believe, but by how they think.”

Brain Blunders and Stock Picking

The buyer of a stock thinks the price will go up and the seller of a stock thinks the price will go down. Both participants engage in the transaction because they believe the current stock price is wrong. The financial services industry is built largely on this phenomenon that Kahneman calls an “illusion of skill,” or ability to exploit inefficient market pricing. Relentless advertisements and marketing pitches continually make the case that professionals can outperform the markets, but this is what Kahneman found:

“Although professionals are able to extract a considerable amount of wealth from amateurs, few stock pickers, if any, have the skill needed to beat the market consistently, year after year. Professional investors, including fund managers, fail a basic test of skill: persistent achievement…Skill in evaluating the business prospects of a firm is not sufficient for successful stock trading, where the key question is whether the information about the firm is already incorporated in the price of its stock. Traders apparently lack the skill to answer this crucial question, but they appear ignorant of their ignorance.”

For the few managers that actually do outperform, Kahneman assigns luck to the outcome, not skill:

“For a large majority of fund managers, the selection of stocks is more like rolling dice than like playing poker. Typically at least two out of three mutual funds underperform the overall market in any given year…The successful funds in any given year are mostly lucky; they have a good roll of the dice.”

The picture for individual investors isn’t any prettier. Evidence from Terry Odeam, a finance professor at UC Berkeley, who studied 100,000 individual brokerage account statements and about 163,000 trades over a seven-year period, was not encouraging. He discovered that stocks sold actually did +3.2% better than the replacement stocks purchased. And this detrimental impact on performance excludes the significant expenses related to trading.

In response to Odean’s work, Kahneman states:

“It is clear that for the large majority of individual investors, taking a shower and doing nothing would have been a better policy than implementing the ideas that came to their minds….Many individual investors lose consistently by trading, an achievement that a dart-throwing chimp could not match.”

In a future Odean paper titled, “Trading is Hazardous to your Wealth,” Odean and his colleague Brad Barber also proved that “less is more.” The results showed the most active traders had the weakest performance, and those traders who traded the least had the best returns. Interestingly, women were shown to have better investment results than men.

Regardless of whether someone is listening to an expert, fund manager, or individual investor, what Daniel Kahneman has discovered in his long, illustrious career is that humans consistently make errors. If you are wise, you will heed Kahneman’s advice by stealing the expert’s darts and handing them over to the chimp.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}