Posts tagged ‘William O’Neil’

The Art & Science of Successful Investing

As I described in my book, How I Managed $20,000,000,000.00 by Age 32, I believe successful investing is achieved by integrating aspects of both art and science. The science aspect of investing is fairly straightforward – most of the accounting and valuation math involved could be solved by a 7th grader. The more challenging aspect to successful investing is controlling the vacillating emotions of fear and greed when searching for attractive investments.

When people ask me about my investment philosophy, I do not like to be pigeon-holed into one style box because normally my portfolios hold investments that outsiders would deem both value and growth oriented. Since I am an absolute return investor, I am more concerned about how I can maximize upside returns while minimizing downside risk for my investors.

Because valuation is such an important factor in my process (price always matters), the most accurate description of my style would likely be “high octane GARP” (Growth At a Reasonable Price). While many GARP investors limit themselves to current or historical valuation metrics, my process has allowed me to take a more long-term, forward looking analysis of valuations, which has directed me to participate in some large winners, like Amazon (AMZN), Apple (AAPL), and Google/Alphabet (GOOGL), to name a few. To many observers, positions like these have traditionally been falsely considered “expensive” growth stocks.

Case in point is Google/Alphabet, which went public at $85 per share in 2004. At the time, the broad Wall Street consensus was the IPO (Initial Public Offering) price was way overheated. As it turned out, the stock has reached $1,000 per share and the Price-Earnings ratio (P/E) was a steal at less than 3x had you bought Google at the IPO price. ($85 2004 price/$33.98 2017 EPS estimate). Google is a perfect example of a dominant market leader that has been able to grow earnings dramatically for many years. In short order after going public, Google’s earnings ended up more than quintupling in less than three years and the stock price quintupled as well, proving that ill-advised focus on stale, traditional valuation metrics can lead you to wrong conclusions. Certainly, finding stocks that can increase in value by more than 11x fold is easier said than done, however, applying longer-term valuation metrics to dominant growth leading franchises will allow you to occasionally find monster winners like Google.

The greatest long-term winners don’t start off as the largest weightings, but due to the compounding of returns, position sizes can explode over time. As Peter Lynch states,

“You don’t need a lot of good hits every day. All you need is two to three good stocks a decade.”

Google/Alphabet proves what can appear expensive in the short-run is, in many cases, wildly cheap based on future earnings growth. Earnings tomorrow may be significantly larger than earnings today. Lynch emphasizes the importance of earnings over current prices,

“People concentrate too much on the ‘P’ (Price), but the ‘E’ (Earnings) really makes the difference.”

“Just because a stock is cheaper than before is no reason to buy it, and just because it’s more expensive is no reason to sell.”

The Google/Alphabet chart below shows the incredible price appreciation that can be realized from compounding earnings growth.

The Google example also underscores the importance of patience. Although the stock has been a massive home-run since its IPO, the stock barely budged from late 2006 through 2011. Accurately picking the perfect timing to make an investment is nearly impossible. I concur with Bill Miller when he stated,

“We expect the stocks we buy today to contribute to our performance several years hence. While it’s nice if they contribute to this year’s performance, this year’s performance should be driven by decisions we made in previous years. If we keep doing this, we hope that we will provide adequate returns in the future.”

Regarding timing, Miller adds,

“Nobody buys at lows and sells at highs except liars.”

The Sidoxia Philosophy

Over time, as I have fine-tuned my investment philosophy, I have not been bashful in borrowing winning ideas from growth gurus like Peter Lynch, Phil Fisher, William O’Neil, and Ron Baron, to name a few. By the same token, I am not shy about stealing ideas from value veterans like Warren Buffett, Seth Klarman, and Bill Miller as well.

While I don’t agree with Warren Buffett’s “forever” time horizon, I do believe in the power of compounding he espouses, which requires a longer-term investment horizon. The power of compounding is accelerated not only by committing to a long-term horizon, but also by the benefits accrued from lower trading costs and taxes. What’s more, taking a long view lowers your blood pressure and creates fewer ulcers. Legendary growth manager, T. Rowe Price, captures the essence of this idea here:

“The growth stock theory of investing requires patience, but is less stressful than trading, generally has less risk, and reduces brokerage commissions and income taxes.”

The Science of Investing

As discussed earlier, successful investing is an endeavor that involves the practices of both art and science – too much of either approach can be detrimental to your financial health. Quantitative screening can be an excellent tool for identifying new securities for research along with streamlining the fundamental analysis process. However, many investment funds rely too heavily on the quantitative science. The adage that “correlation does not equal causation” is an important credo to follow when reviewing various quantitative models (see Butter in Bangladesh).

The collapse of the infamous, multi-billion Long Term Capital Management hedge fund should also be a lesson to everyone (see When Genius Failed ). If world renowned Nobel Prize winners, Robert Merton and Myron Scholes, can single-handedly bring the global market to its knees as a result of using inconsistent and unreliable quantitative models, then I feel validated for my fundamentally-based investment approach.

While there are some artistic facets to valuation techniques, in large part, the valuation science is a fairly straightforward mathematical exercise. Unfortunately, the market consists of emotional and unpredictable individuals who continually change their opinions. Eventually the financial markets prod prices in the right direction, but over shorter time intervals, proper investment analysis requires some imperfect estimation.

Emotions regularly result in individuals overpaying for stocks, and this tendency is a risky strategy for any investment. In many cases investors chase darling stocks highlighted in news headlines, but regrettably these pricy investments often end up performing poorly. When it comes to hot stocks, I’m on the same page as famed value investor Bill Miller,

“If it’s in the papers, it’s in the price. One needs to anticipate, not react.”

Usually a news event that makes headlines is already factored into the stock price. The financial markets are generally forward looking mechanisms, not backward looking.

The Art of Investing

“It’s tough to make predictions, especially about the future.”

-Yogi Berra

Investing is undoubtedly a challenging undertaking, but like almost any profession, the more experience one has, the better results generally achieved. Experience alone does not guarantee extraordinary performance, in large part due to emotional pressures. Investing would be much easier for everyone, if you didn’t have to worry about controlling those pesky emotions of fear and greed. The best investment decisions, and frankly any decision, are rarely made under these heightened emotions.

The most successful set of investors I have studied and modeled my investment process after are professionals who have married the quantitative science with the fundamental art of investing. At Sidoxia, we use a disciplined cash flow based valuation approach, along with thorough fundamental analysis to identify attractively valued, market leading franchises that can sustain above average growth. It sounds like a mouthful, but over time, it has worked well for the benefit of my clients and me.

The market leading franchises we invest in tend to have a competitive advantage, whether in the form of superior research and development, low-cost manufacturing, leading marketing, and/or other exceptional functions in the company that allow the entity to consistently garner more growth and more market share from its competitors. Quality franchises tend to also employ first-class management teams that have a proven track record, along with thoughtful, systematic processes in place to maintain their competitive edge. These competitive advantages are what allow companies to produce exceptional earnings growth for extended periods of time, thereby producing outstanding long-term performance for shareholders.

Finding sustainable growth in competitive niche markets is nearly impossible, and that is why I center my attention on large or emerging sectors of the economy that can support long runways of growth. When analyzing companies with durable, long runways of earnings growth, I concentrate on those developing, share-taking companies and dominant market leaders. In other words, disruptive companies that are entering new markets with vast potential and established companies that are gaining significant share in large markets. Well-known growth authority, Phil Fisher summarized the objective,

“The greatest investment rewards come to those who by good luck or good sense find the occasional company that over the years can grow in sales and profits far more than industry as a whole.”

I am privileged and honored to manage the hard earned investments of my clients. If this was a simple profession, everyone would do it, and I would not be employed as an investment manager. I have developed what I believe is a superior way of managing money, but I realize my investment process is not the only way to make money. If you were to assemble 10 different investment managers in the same room, and ask them, “What is the best way to invest money?,” you are likely to get 10 different answers. Having been in the investment industry and managed money for over 25 years, my experience has shown me that the vast majority of professional managers have underperformed the passive benchmarks. However, there are investment managers who have survived the test of time. For those veterans incorporating a disciplined, systematic approach that integrates the artistic and scientific aspects of investing, exceptional long-term returns can be achieved and have been achieved.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, AMZN, GOOG/GOOGL, and AAPL, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Airbag Protection from Pundit Backseat Drivers

Giving advice to a driver from the backseat of a car is quite easy and enjoyable for some, but whether that individual is actually qualified to give advice is another subject. In the financial blogosphere and media there is an unending mass of backseat drivers recklessly directing investors off cliffs and into walls, but unfortunately there are no consequences for these blabbers. It’s the investors who are driving their personal portfolios that ultimately suffer from crashed financial dreams.

Unlike drivers who mandatorily require a license to drive to the local grocery store, bloggers, journalists, economists, analysts, strategists (aka “pundits”), and any other charismatic or articulate individual can emphatically counsel investors without any credentials, education, or licenses. More importantly than a piece of paper or letters on a business card, many of these self-proclaimed experts have little or no experience of investing real money…the exact topic the pundits are using to direct peoples’ precious and indispensable lifesavings.

It’s easy for bearish pundits like Peter Schiff, Nouriel Roubini, John Mauldin, and David Rosenberg (see also The Fed Ate My Homework) to throw economic hand grenades with their outlandishly gloomy predictions and fear mongering. However, more important than selling valuable advice, the pundit’s #1 priority is selling a convincing story, whether the story is grounded in reality or not. The pundit’s story is usually constructed by looking into the rearview mirror by creatively connecting current event dots in a way that may seem reasonable on the surface.

Crusty investors who have invested through various investment cycles know better than to pay attention to these opinions. As the saying goes, “Opinions are like ***holes. Everybody has one.” Stated differently, the great growth investor William O’Neil said the following:

“I would say 95% of all these people you hear on TV shows are giving you their personal opinion. And personal opinions are almost always worthless … facts and markets are far more reliable.”

Successful long-time investors like Warren Buffett rarely make predictions about the short-term directions of the market. Long-term investors know the only certainty in the market is uncertainty. At the core, investing is a game of probabilities. The objective of the game is to place your bets on those investments that establish the odds in your favor. As in many professions, however, the right process can have a negative outcome in the short-run. Those talented investors who have experience consistently applying a probabilistic approach generally do quite well in the long-run.

There is an endless multitude of investing advice, regardless of whether you choose to consume it over the TV, in newspapers, or through blogs. That’s why it’s so important to be discerning in your financial media consumption by focusing on experience…experience is the key. If you were to undergo a heart surgery, would you want a nurse or experienced doctor who had performed 2,000 successful heart surgeries? When you fly cross-country, do you want a flight attendant to fly the plane or a 20-year veteran pilot? I think you get the point.

The other factor to consider when comparing advice from a media pundit vs. experienced investor is skin in the game. Investment advisers who have their personal dollars at stake typically have spent a significantly larger amount of time formulating an investment thesis or strategy as compared to a loose-cannon TV journalist or inexperienced, maverick blogger.

There is a lot to consider as you maneuver your investment portfolio through volatile markets. With all the dangerous advice out there from backseat drivers, make sure you have experienced investment advice installed as protective airbags because listening to inexperienced air bags (pundits) could crash your portfolio into a wall.

Related Content: Financial Blogging Interview on Charlie Rose w/ Joe Weisenthal, Josh Brown, Felix Salmon, and Megan Murphy

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own a range of positions in certain exchange traded fund positions, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Controlling the Investment Lizard Brain

“Normal fear protects us; abnormal fear paralyses us.”

– Martin Luther King, Jr.

Investing is challenging enough without bringing emotions into the equation. Unfortunately, humans are emotional, and as a result investors often place too much reliance on their feelings, rather than using objective information to drive rational decision making.

What causes investors to make irrational decisions? The short answer: our “amygdala.” Author and marketer Seth Godin calls this almond-shaped tissue in the middle of our head, at the end of the brain stem, the “lizard brain” (video below). Evolution created the amygdala’s instinctual survival flight response for lizards to avoid hungry hawks and humans to flee ferocious lions.

Over time, the threat of lions eating people in our modern lives has dramatically declined, but the human’s “lizard brain” is still running in full gear, worrying about other fear-inducing warnings like Iran, Syria, Obamacare, government shutdowns, taxes, Cyprus, sequestration, etc. (see Series of Unfortunate Events)

When the brain in functioning properly, the prefrontal cortex (the front part of the brain in charge of reasoning) is actively communicating with the amygdala. Sadly, for many people, and investors, the emotional response from the amygdala dominates the rational reasoning portion of the prefrontal cortex. The best investors and traders have developed the ability of separating emotions from rational decision making, by keeping the amygdala in check.

With this genetically programmed tendency of constantly fearing the next lion or stock market crash, how does one control their lizard brain from making sub-optimal, rash investment decisions? Well, the first thing you should do is turn off the TV. And by turning off the TV, I mean stop listening to talking head commentators, economists, strategists, analysts, neighbors, co-workers, blogger hacks, newsletter writers, journalists, and other investing “wannabes”. Sure, you could throw my name into the list of people to ignore if you wanted to, but the difference is, at least I have actually invested real money for over 20 years (see How I Managed $20,000,000,000.00), whereas the vast majority of those I listed have not. But don’t take my word for it…listen or read the words of other experienced investors Warren Buffett, Peter Lynch, Ron Baron, John Bogle, Phil Fisher, and other investment titans (see also Sidoxia Hall of Fame). These investment legends have successful long-term investment track records and they lived through wars, recessions, financial crises, and other calamities…and still managed to generate incredible returns.

Another famed investor, William O’Neil, summed this idea nicely by adding the following:

“Since the market tends to go in the opposite direction of what the majority of people think, I would say 95% of all these people you hear on TV shows are giving you their personal opinion. And personal opinions are almost always worthless … facts and markets are far more reliable.”

The Harmful Consequence of Brain on Pain

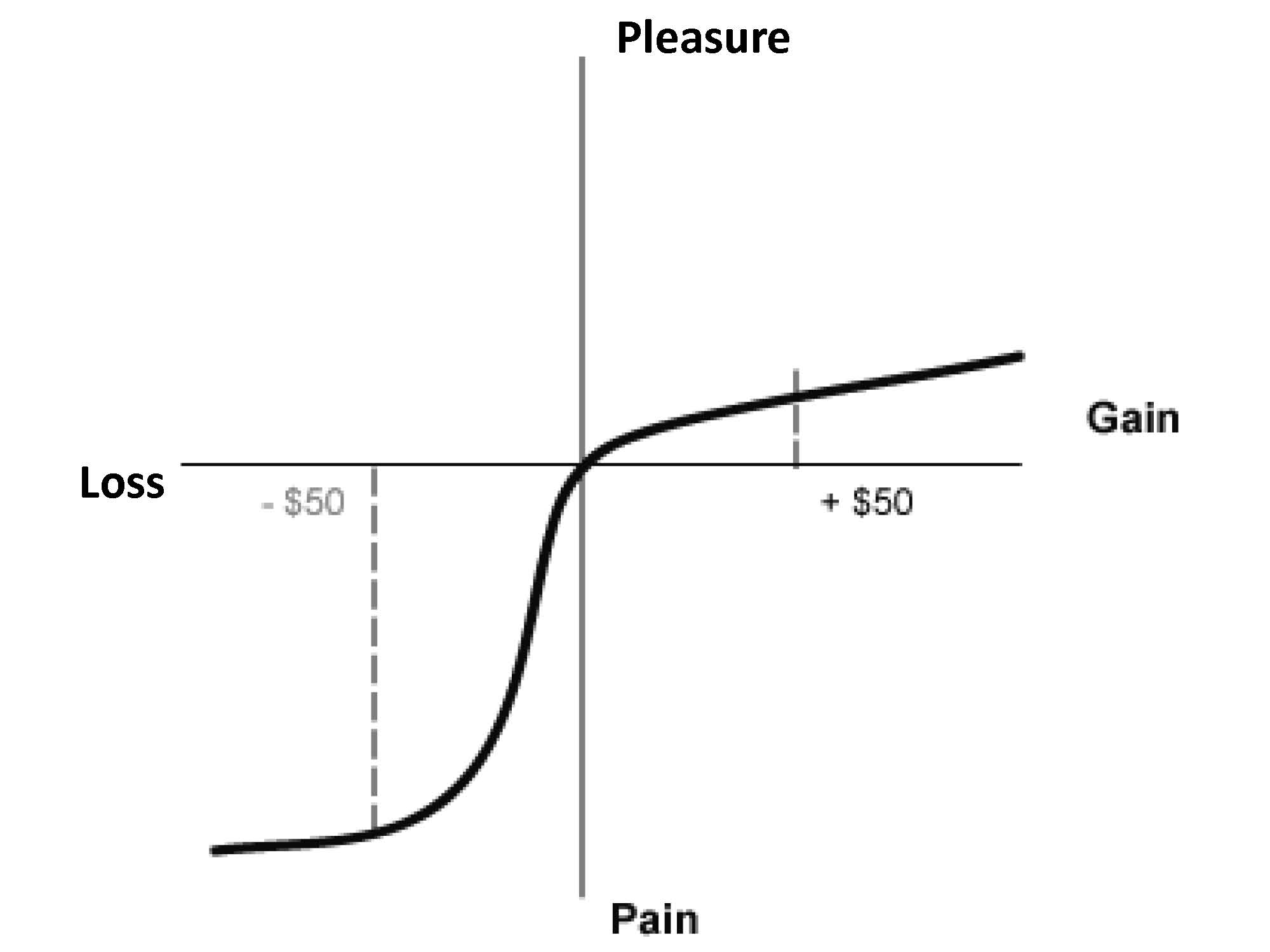

Besides forcing damaging decisions, another consequence of our lizard brain is its ability to distort reality. Behavioral economists Daniel Kahneman (Nobel Prize winner) and Amos Tversky through their research demonstrated the pain of $50 loss is more than twice as painful as the pleasure from $50 gain (see Pleasure/Pain Principle). Common sense would dictate our brains would treat equivalent scenarios in a proportional manner, but as the chart below shows, that is not the case:

Source: Investopedia

Kahneman adds to the decision-making relationship of the amygdala and prefrontal cortex by describing the concepts of instinctual and deliberative choices in his most recent book, Thinking Fast and Slow (see Decision Making on Freeways).

Optimizing Risk

Taking excessive risks in technology stocks in the 1990s or in housing in the mid-2000s was very damaging to many investors, but as we have seen, our lizard brains can cause investors to become overly risk averse. Over the last five years, many people have personally experienced the ill effects of unwarranted conservatism. Investment great Sir John Templeton summed up this risk by stating, “The only way to avoid mistakes is not to invest – which is the biggest mistake of all.”

Every person has a different perception and appetite for risk. The optimal amount of risk taken by any one investor should be driven by their unique liquidity needs and time horizon…not a perceived risk appetite. Typically risk appetites go up as markets peak, and conservatism reaches a fearful apex near market bottoms – the opposite tendency of rational decision making. Besides liquidity and time horizon, a focus on valuation coupled with diversification across asset class (stocks/bonds), geography (domestic/international), size (small/large), style (value/growth) is critical in controlling risk. If you can’t determine your personal, optimal risk profile, then find an experienced and knowledgeable investment advisor to assist you.

With the advent of the internet and mobile communication, our brains and amygdala continually get bombarded with fearful stimuli, leading to disastrous decision-making and damaging portfolio outcomes. Turning off the TV and selectively choosing the proper investment advice is paramount in keeping your amygdala in check. Your lizard brain may protect you from getting eaten by a lion, but falling prey to this structural brain flaw may eat your investment portfolio alive.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Sidoxia’s Investor Hall of Fame

Investing Caffeine has profiled many great investors over the months and years, so I thought now would be a great time to compile a “Hall of Fame” summarizing some of the greatest of all-time. Nothing can replace experience, but learning from the greats can only improve your investing results – I’ve benefitted firsthand and so have Sidoxia’s clients. Here is a partial list from the Pantheon of investing greats along with links to the complete articles (special thanks to Kevin Weaver for helping compile):

Phillip Fisher – Author of the must-read classic Common Stocks and Uncommon Profits, he enrolled in college at age 15 and started graduate school at Stanford a few years later, before he dropped out and started his own investment firm in 1931. “If the job has been correctly done when a common stock is purchased, the time to sell it is – almost never.” Not every investment idea made the cut, however he is known to have bought Motorola (MOT) stock in 1955 and held it until his death in 2004 for a massive gain. (READ COMPLETE ARTICLE)

Phillip Fisher – Author of the must-read classic Common Stocks and Uncommon Profits, he enrolled in college at age 15 and started graduate school at Stanford a few years later, before he dropped out and started his own investment firm in 1931. “If the job has been correctly done when a common stock is purchased, the time to sell it is – almost never.” Not every investment idea made the cut, however he is known to have bought Motorola (MOT) stock in 1955 and held it until his death in 2004 for a massive gain. (READ COMPLETE ARTICLE)

Peter Lynch – Lynch graduated from Boston College in 1965 and earned a Master of Business Administration from the Wharton School of the University of Pennsylvania in 1968. Lynch’s Magellan fund averaged +29% per year from 1977 – 1990 (almost doubling the return of the S&P 500). In 1977, the obscure Magellan Fund started with about $20 million, and by his retirement the fund grew to approximately $14 billion (700x’s larger). Magellan outperformed 99.5% of all other funds, according to Barron’s. (READ COMPLETE ARTICLE)

Peter Lynch – Lynch graduated from Boston College in 1965 and earned a Master of Business Administration from the Wharton School of the University of Pennsylvania in 1968. Lynch’s Magellan fund averaged +29% per year from 1977 – 1990 (almost doubling the return of the S&P 500). In 1977, the obscure Magellan Fund started with about $20 million, and by his retirement the fund grew to approximately $14 billion (700x’s larger). Magellan outperformed 99.5% of all other funds, according to Barron’s. (READ COMPLETE ARTICLE)

William O’Neil – After graduating from Southern Methodist University, O’Neil started his career as a stock broker. Soon thereafter, at the ripe young age of 30, O’Neil purchased a seat on the New York Stock Exchange and started his own company, William O’Neil + Co. Incorporated. Following the creation of his firm, O’Neil went on to pioneer the field of computerized investment databases. He used his unique proprietary data as a foundation to unveil his next entrepreneurial baby, Investor’s Business Daily, in 1984. (READ COMPLETE ARTICLE)

Sir John Templeton – After Yale and Oxford, Templeton moved onto Wall Street, borrowed $10,000 to purchase more than 100 stocks trading at less than $1 per share (34 of the companies were in bankruptcy). Only four of the investments became worthless and Templeton made a boatload of money. Templeton bought an investment firm in 1940, leading to the Templeton Growth Fund in 1954. A $10,000 investment made at the fund’s 1954 inception would have compounded into $2 million in 1992 (translating into a +14.5% annual return). (READ COMPLETE ARTICLE)

Charles Ellis – He has authored 12 books, founded institutional consulting firm Greenwich Associates, a degree from Yale, an MBA from Harvard, and a PhD from New York University. A director at the Vanguard Group and Investment Committee chair at Yale, Ellis details that many more investors and speculators lose than win. Following his philosophy will not only help increase the odds of your portfolio winning, but will also limit your losses in sleep hours. (READ COMPLETE ARTICLE)

Charles Ellis – He has authored 12 books, founded institutional consulting firm Greenwich Associates, a degree from Yale, an MBA from Harvard, and a PhD from New York University. A director at the Vanguard Group and Investment Committee chair at Yale, Ellis details that many more investors and speculators lose than win. Following his philosophy will not only help increase the odds of your portfolio winning, but will also limit your losses in sleep hours. (READ COMPLETE ARTICLE)

Seth Klarman – President of The Baupost Group, which manages about $22 billion, he worked for famed value investors Max Heine and Michael Price of the Mutual Shares. Klarman published a classic book on investing, Margin of Safety, Risk Averse Investing Strategies for the Thoughtful Investor, which is now out of print and has fetched upwards of $1,000-2,000 per copy in used markets. From it’s 1983 inception through 2008 his Limited partnership averaged 16.5% net annually, vs. 10.1% for the S&P 500. During the “lost decade” he crushed the S&P, returning 14.8% and 15.9% for the 5 and 10-year periods vs. -2.2% and -1.4%. (READ COMPLETE ARTICLE)

Seth Klarman – President of The Baupost Group, which manages about $22 billion, he worked for famed value investors Max Heine and Michael Price of the Mutual Shares. Klarman published a classic book on investing, Margin of Safety, Risk Averse Investing Strategies for the Thoughtful Investor, which is now out of print and has fetched upwards of $1,000-2,000 per copy in used markets. From it’s 1983 inception through 2008 his Limited partnership averaged 16.5% net annually, vs. 10.1% for the S&P 500. During the “lost decade” he crushed the S&P, returning 14.8% and 15.9% for the 5 and 10-year periods vs. -2.2% and -1.4%. (READ COMPLETE ARTICLE)

George Soros – Escaping Hungary in 1947, Soros immigrated to the U.S. in 1956 and held analyst and management positions for the next 20 years. Known as the “The man who broke the Bank of England,” he risked $10 billion against the British pound in 1992 in a risky trade and won. Soros also gained notoriety for running the Quantum Fund, which generated an average annual return of more than 30%. (READ COMPLETE ARTICLE)

George Soros – Escaping Hungary in 1947, Soros immigrated to the U.S. in 1956 and held analyst and management positions for the next 20 years. Known as the “The man who broke the Bank of England,” he risked $10 billion against the British pound in 1992 in a risky trade and won. Soros also gained notoriety for running the Quantum Fund, which generated an average annual return of more than 30%. (READ COMPLETE ARTICLE)

Bruce Berkowitz -Bruce Berkowitz has not exactly been a household name. With his boyish looks, nasally voice, and slicked-back hair, one might mistake him for a grad student. However, his results are more than academic, which explains why this invisible giant was recently named the equity fund manager of the decade by Morningstar. The Fairholme Fund (FAIRX) fund earned a 13% annualized return over the ten-year period ending in 2009, beating the S&P 500 by an impressive 14%. (READ COMPLETE ARTICLE)

Thomas Rowe Price, Jr. – Known as the “Father of Growth Investing,” in 1937 he founded T. Rowe Price Associates (TROW) and successfully ramped up the company before the launch of the T. Rowe Price Growth Stock Fund in 1950. Expansion ensued until he made a timely sale of his company in the late 1960s. His Buy and Hold strategy proved successful. For example, in the early 1970s, Price had accumulated gains of +6,184% in Xerox (XRX), which he held for 12 years, and gains of +23,666% in Merck (MRK), which he held for 31 years. (READ COMPLETE ARTICLE)

There you have it. Keep investing and continue reading about investing legends at Investing Caffeine, and who knows, maybe you too can join Sidoxia’s Hall of Fame?!

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and WMT, but at the time of publishing SCM had no direct position in MOT, TROW, XRX, MRK, FAIRX, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

O’Neil Swings for the Fences

Approaches used in baseball strategy are just as varied as they are in investing. Some teams use a “small ball” approach to baseball, in which a premium is placed on methodically advancing runners around the bases with the help of bunts, bases on ball, stolen bases, sacrifice flies, and hit-and- run plays. Other teams stack their line-up with power-hitters, with the sole aim of achieving extra base hits and home runs.

Investing is no different than baseball. Some investors take a conservative, diversified value-approach and seek to earn small returns on a repeated basis. Others, like William J. O’Neil, look for the opportunities to knock an investment out of the park. O’Neil has no problem of concentrating a portfolio in four or five stocks. Warren Buffett talks about how Ted Williams patiently waited for fat pitches–O’Neil is very choosy too, when it comes to taking investment swings.

The Making of a Growth Guru

Born in Oklahoma and raised in Texas, William O’Neil has accomplished a lot over his 53-year professional career. After graduating from Southern Methodist University, O’Neil started his career as a stock broker in the late-1950s. Soon thereafter in 1963, at the ripe young age of 30, O’Neil purchased a seat on the New York Stock Exchange (NYX) and started his own company, William O’Neil + Co. Incorporated. Ambition has never been in short supply for O’Neil – following the creation of his firm, O’Neil the investment guru put on his computer science hat and went onto pioneer the field of computerized investment databases. He used his unique proprietary data as a foundation to unveil his next entrepreneurial baby, Investor’s Business Daily, in 1984.

O’Neil’s Secret Sauce

The secret sauce behind O’Neil’s system is called CAN SLIM®. O’Neil isn’t a huge believer in stock diversification, so he primarily focuses on the cream of the crop stocks in upward trending markets. Here are the components of CAN SLIM® that he searches for in winning stocks:

C Current Quarterly Earnings per Share

A Annual Earnings Increases

N New Products, New Management, New Highs

S Supply and Demand

L Leader or Laggard

I Institutional Sponsorship

M Market Direction

Rebel without a Conventional Cause

In hunting for the preeminent stocks in the market, the CAN SLIM® method uses a blend of fundamental and technical factors to weed out the best of the best. I may not agree with everything O’Neil says in his book, How to Make Money in Stocks, but what I love about the O’Neil doctrine is his maverick disregard of the accepted modern finance status quo. Here is a list of O’Neil’s non-conforming quotes:

- Valuation Doesn’t Matter: “The most successful stocks from 1880 to the present show that, contrary to most investors’ beliefs, P/E ratios were not a relevant factor in price movement and have very little to do with whether a stock should be bought or sold.” (see also The Fallacy of High P/Es)

- Diversification is Bad: “Broad diversification is plainly and simply a hedge for ignorance… The best results are usually achieved through concentration, by putting your eggs in a few baskets that you know well and watching them very carefully.”

- Buy High then Buy Higher: “[Buy more] only after the stock has risen from your purchase price, not after it has fallen below it.”

- Dollar-Cost Averaging a Mistake: “If you buy a stock at $40, then buy more at $30 and average out your cost at $35, you are following up your losers and throwing good money after bad. This amateur strategy can produce serious losses and weigh down your portfolio with a few big losers.”

- Technical Analysis Matters: “Learn to read charts and recognize proper bases and exact buy points. Use daily and weekly charts to materially improve your stock selection and timing.”

- Ignore TV & So-Called Experts: “Stop listening to and being influenced by friends, associates, and the continuous array of experts’ personal opinions on daily TV shows.”

- Stay Away from Dividends: “Most people should not buy common stocks for their dividends or income, yet many people do.”

Managing Momentum Risk

Although O’Neil’s CAN SLIM® investment strategy does not rely on a full-fledged, risky style of momentum investing (see Riding the Momentum Wave), O’Neil’s investment approach utilizes very structured rules designed to limit downside risk. Since true O’Neil disciples understand they are dealing with flammable and volatile hyper-growth companies, O’Neil always keeps a safety apparatus close by – I like to call it the 8% financial fire extinguisher rule. O’Neil simply states, “Investors should definitely set firm rules limiting the loss on the initial capital they have invested in each to an absolute maximum of 7% or 8%.” If a trade is not working, O’Neil wants you to quickly cut your losses. As the “M” in CAN SLIM® indicates, downward trending markets make long position gains very challenging to come by. Raising cash and cutting margin is the default strategy for O’Neil until the next bull cycle begins.

While some components of William O’Neil’s “cup and handle” teachings (see link)are considered heresy among various traditional financial textbooks, O’Neil’s lessons and CAN SLIM® method shared in How to Make Money in Stocks provide a wealth of practical information for all investors. If you want to add a power-hitting element to your investing game and hit a few balls out of the park, it behooves you to invest some time in better familiarizing yourself with the CAN SLIM® teachings of William O’Neil.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Wade Slome, President of Sidoxia Capital Management (SCM), worked at William O’Neil + Co. Incorporated in 1993-1996. SCM and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in NYX or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

The Fallacy of High P/E’s

Would you pay a P/E ratio (Price-Earnings) of 1x’s future earnings for a dominant market share leading franchise that is revolutionizing the digital industry and growing earnings at an +83% compounded annual growth rate? Or how about shelling out 3x’s future profits for a company with ambitions of taking over the global internet advertising and commerce industries while expanding earnings at an explosive +51% clip? If you were capable of identifying Apple Inc. (AAPL) and Google Inc. (GOOG) as investment ideas in 2004, you would have made approximately +2,000% and +600%, respectively, over the following six years. I know looking out years into the future can be a lot to ask for in a world of high frequency traders and stock renters, but rather than focusing on daily jobless claims and natural gas inventory numbers, there are actual ways to accumulate massive gains on stocks without fixating on traditional trailing P/E ratios.

At the time in 2004, Apple and Google were trading at what seemed like very expensive mid-30s P/E ratios (currently the S&P 500 index is trading around 15x’s trailing profits) before these stocks made their explosive, multi-hundred-percent upward price moves. What seemingly appeared like expensive rip-offs back then – Apple traded at a 37x P/E ($15/$0.41) and Google 34x P/E ($85/$2.51) – were actually bargains of a lifetime. The fact that Apple’s share price appreciated from $15 to $347 and Google’s $85 to $538, hammers home the point that analyzing trailing P/E ratios alone can be hazardous to your stock-picking health.

Why P/Es Don’t Matter

In William O’Neil’s book, How to Make Money in Stocks he comes to the conclusion that analyzing P/E ratios is worthless:

“Our ongoing analysis of the most successful stocks from 1880 to the present show that, contrary to most investors beliefs, P/E ratios were not a relevant factor in price movement and have very little to do with whether a stock should be bought or sold. Much more crucial, we found, was the percentage increase in earnings per share.”

Here is what O’Neil’s data shows:

- From 1953 – 1985 the best performing stocks traded at a P/E ratio of 20x at the early stages of price appreciation versus an average P/E ratio of 15x for the Dow Jones Industrial Average over the same period. The largest winners saw their P/E multiples expand by 125% to 45x.

- From 1990 – 1995, the leading stocks saw their P/E ratios more than double from an average of 36 to the 80s. Once again, O’Neil explains why you need to pay a premium to play with the market leading stocks.

You Get What You Pay For

When something is dirt cheap, many times that’s because what you are buying is dirt. Or as William O’Neil says,

“You can’t buy a Mercedes for the price of a Chevrolet, and you can’t buy oceanfront property for the same price you’d pay for land a couple of miles inland. Everything sells for about what it’s worth at the time based on the law of supply and demand…The very best stocks, like the very best art, usually command a higher price.”

Any serious investor has “value trap” scars and horror stories to share about apparently cheap stocks that seemed like bargains, only to later plummet lower in price. O’Neil uses the example of when he purchased Northrop Grumman Corp (NOC) many years ago when it traded at 4x’s earnings, and subsequently watched it fall to a P/E ratio of 2x’s earnings.

Is Your Stock a Teen or a Senior?

A mistake people often make is valuing a teen-ager company like it’s an adult company (see also the Equity Life Cycle article). If you were offered the proposition to pay somebody else an upfront lump-sum payment in exchange for a stream of their lifetime earnings, how would you analyze this proposal? Would you make a higher lump-sum payment for a 21-year-old, Phi Beta Kappa graduate from Harvard University with a 4.0 GPA, or would you pay more for an 85 year old retiree generating a few thousand dollars in monthly Social Security income? As you can imagine, the vast majority of investors would pay more for the youngster’s income because the stream of income over 65-70 years would statistically be expected to be much larger than the stream from the octogenarian. This same net present value profit stream principle applies to stocks – you will pay a higher price or P/E for the investment opportunity that has the best growth prospects.

Price Follows Earnings

At the end of the day, stock prices follow the long-term growth of earnings and cash flows, whether a stock is considered a growth stock, a value stock, or a core stock. Too often investors are myopically focused on the price action of a stock rather than the earnings profile of a company. Or as investment guru Peter Lynch states:

”People may bet on hourly wiggles of the market but it’s the earnings that waggle the wiggle long term.”

“People Concentrate too much on the P (Price), but the E (Earnings) really makes the difference.”

Correctly determining how a company can grow earnings is a more crucial factor than a trailing P/E ratio when evaluating the attractiveness of a stock’s share price.

Valuations Matter

Even if you buy into the premise that trailing P/E ratios do not matter, valuation based on future earnings and cash flows is critical. When calculating the value of a company via a discounted cash flow or net present value analysis, one does not use historical numbers, but rather future earnings and cash flow figures. So when analyzing companies with apparently sky-high valuations based on trailing twelve month P/E ratios, do yourself a favor and take a deep breath before hyperventilating, because if you want to invest in unique growth stocks it will require implementing a unique approach to evaluating P/E ratios.

See also Evaluating Stocks Vegas Style

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, AAPL, and GOOG, but at the time of publishing SCM had no direct position in NOC, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Fees, Exploitation and Confusion Hammer Investors

The financial industry is out to hammer you. If you haven’t figured that out, then it’s time to wake up to the cruel realities of the industry. Let’s see what it takes to become the hammer rather than receiving the brunt of the pounding, like the nail.

Fees, Fees, Fees

I interface with investors of all stripes and overwhelmingly the vast majority of them have no idea what they are paying in fees. When I ask investors what fees, commissions, and transactions costs are being siphoned from their wallets, I get the proverbial deer looking into the headlight response. And who can blame them? Buried in the deluge of pages and hiding in the fine print is a list of load fees, management fees, 12b-1 fees, administrative fees, surrender charges, transaction costs, commissions, and more. One practically is required to obtain a law degree in order to translate this foreign language.

Wolf in Sheep’s Clothing

These wolves don’t look like wolves. These amicable individuals have infiltrated your country clubs, groups, volunteer organizations, and churches. The following response is what I usually get: “Johnny, my financial consultant, is such a nice man – we have known him for so long.” Yeah, well maybe the reason why Johnny is so nice and happy is because of the hefty fees and commissions you are paying him. Rather than paying for an expensive friend, maybe what you need is someone who can accelerate your time to retirement or improve your quality of life. If you prefer eating mac and cheese over filet mignon, or are looking to secure a position at Wal-Mart as a greeter in your 80s, then don’t pay any attention to the fees you may be getting gouged on.

I don’t want to demonize all practitioners and aspects of the financial industry, but like Las Vegas, there is a reason the industry makes so much money. The odds and business practices are stacked in their favor, so focus on protecting yourself.

Confusion

Investors face a very challenging environment these days, needing to decipher everything from Dubai debt defaults and PIIGS sovereign risk (Portugal-Ireland-Italy-Greece-Spain) to proposed new banking regulation and massive swings in the U.S. dollar. If our brightest economists and government officials can’t decipher these issues and “time the market,” then how in the heck are aggressive financial salesmen and casual investors supposed to digest all this ever-changing data? Making matters worse, the media continuously pours gasoline on fear-inducing uncertainties and shovels piles of greed-motivating fodder, which only serves to make matters more confusing for investors. Do yourself a favor and turn off the television. There are better ways of staying informed, without succumbing to sensationalized media stories, like reading Investing Caffeine!

Pushy financial salespeople complicate the situation by attempting to “wow” clients with fancy acronyms and industry jargon in hopes of impressing a prospect or client. In some situations, this superficial strategy may confuse an investor into thinking the consultant is knowledgeable, but in more instances than not, if the salesperson doesn’t know how to explain the investment concept in terms you understand, then there’s a good chance they are just blowing a lot of hot air.

Here’s what famous growth investor William O’Neil has to say about advice:

“Since the market tends to go in the opposite direction of what the majority of people think, I would say 95% of all these people you hear on TV shows are giving you their personal opinion. And personal opinions are almost always worthless … facts and markets are far more reliable.”

Amen.

Mistake of Trying to Time Market

My best advice to you is not to try and time the market. Even for the speculators with correct timing on one trade rarely get the move right the next time. As previously mentioned, even the smartest people on our planet have failed miserably, so I don’t recommend you trying it ether.

Here are a few examples of timing gone awry:

- Nobel Prize winners Robert Merton and Myron Scholes incorrectly predicted the direction of various economic variables in 1998, while investing client money at Long Term Capital Management. As a result of their poor timing, they single-handedly almost brought the global financial markets to their knees.

- Former Federal Reserve Chairman, Alan Greenspan, is famously quoted for his “irrational exuberance” speech in 1996 when the NASDAQ index was trading around 1,300. Needless to say, the index went on to climb above 5,000 in the coming years. Not such great timing Al.

- More recently, Ben Bernanke assumed the Federal Reserve Chairman role (arguably the most powerful financial position in our Universe) in February 2006. Unfortunately even he could not identify the credit and housing bubble that soon burst right under his nose.

Some of the best advice I have come across comes from Peter Lynch, former Fidelity manager of the Magellan Fund. From 1977-1990 his fund’s investment return averaged +29% PER YEAR. Here’s what he has to say about investment timing in the market:

“Worrying about the stock market 14 minutes per year is 12 minutes too many.”

“Anyone can do well in a good market, assume the market is going nowhere and invest accordingly.”

Rather than attempting to time the market, I would encourage you to focus on discovering a disciplined, systematic investment approach that can work in various market environments (see also, One Size Does Not Fit All).

Financial Carnage

The long-term result for investors playing the game, with rules stacked against them, is financial carnage.

If you don’t believe me, then just ask John Bogle, chairman of one of the fastest growing and most successful large financial firms in the industry. His 1984-2002 study shows how badly the average investor gets slammed, thanks to aggressive fees peddled by forceful financial salesmen and the urging into destructive emotional decisions. Specifically, the study shows the battered average fund investor earning a meager 2.7% per year while the overall stock market earned +12.9% annually over the period.

Source: Bogle Financial Center

It’s Your Investment Future

Given the economic times we are experiencing now, there is more confusion than ever in the marketplace. Insistent financial salespeople are using aggressive smoke and mirror tactics, which in many cases leads to unfortunate and damaging investment outcomes. Do your best to prepare and educate yourself, so you can become the hammer and not the nail.

It’s your investment future – invest it wisely.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including Vanguard ETFs and funds), but at time of publishing had no direct positions in securities mentioned in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}