Posts tagged ‘Wall Street’

Market Drops as GameStop Pops

The stock market started with a bang this year with the S&P 500 index at first climbing +3% in January before ending with a whimper and a monthly decline of -1%. This performance followed a strong finish to a wild 2020 presidential election year (the S&P 500 rose +16%). There has been plenty of focus on the coronavirus health crisis and vaccine distribution (100 million doses in 100 days), along with debates over a $1.9 trillion proposed relief package by newly elected President Joe Biden, but there has been another story stealing attention in the financial market headlines…GameStop.

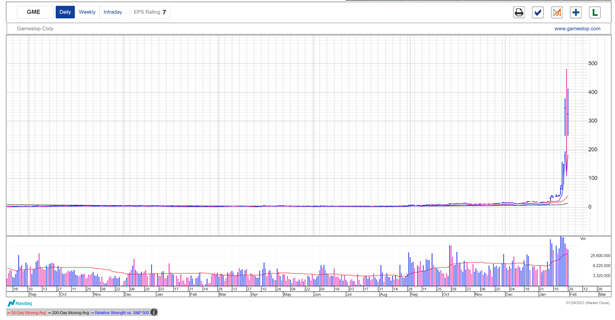

If a global pandemic and a populist attack on the Capitol were not enough for investors, the Reddit (WallStreetBets) and Robinhood revolution coordinated a mass attack on privileged hedge funds and short sellers by squeezing out-of-favor stocks like GameStop (Ticker: GME) to stratospheric levels (up +1,625% to $325/share in January alone) causing an estimated $20 billion of losses for many wealthy elites. To put the meteoric rise into perspective, before GameStop shares reached $325, the stock was valued below $20/share last month and has climbed more than 100x-fold from a low $2.57/share nine months ago (see chart below).

What Exactly Happened?

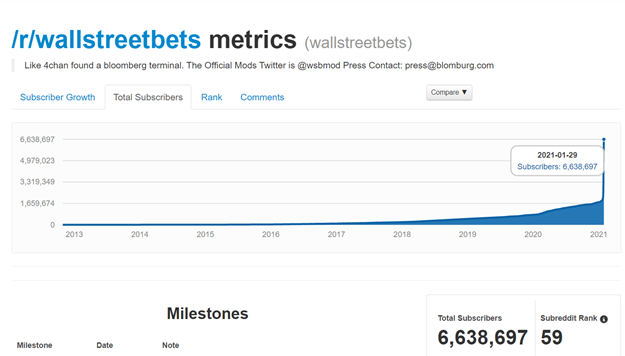

Well, millions of users on the social media platform Reddit banded together on a forum called “wallstreetbets” (see graphic below). WallStreetBets was established in 2012 and had approximately 1 million subscribers at the beginning of 2021 – today it has more than 7 million subscribers. Millions of these anti-establishment WallStreetBets followers effectively colluded together to inflate the share price of GameStop by ganging up on the many short sellers who were betting that GameStop share price would drop. In other words, Reddit-Robinhood buyer gains led to short seller losses. One hedge fund in particular, Melvin Capital, lost billions of dollars on its GameStop short bet and saw its fund performance decline by a whopping -53% in one month…ouch!

The Reddit WallStreetBets forum may have served as the match in this wildfire, but in order to trigger an inferno, a brokerage account is needed. A trading platform allows individual traders on Reddit to level the playing field against the hedge fund professionals and short sellers. The fuel for the GameStop detonation was Robinhood, a fintech (Financial Technology) brokerage firm founded in Silicon Valley in 2013 by two Stanford University graduates. The mission of the company is to “democratize finance for all.” But let’s not forget what Thomas Jefferson noted, “A democracy is nothing more than mob rule, where fifty-one percent of the people may take away the rights of the other forty-nine.” The Reddit-Robinhood mob certainly proved this point.

Although Robinhood was initially seen as a saint in the free trading revolution, eventually many of the brokerage company’s disciples became disenfranchised. Many users subsequently turned on the company and considered Robinhood a villain that was rigging the system when CEO Vlad Tenev halted the ability of its 13+ million users to buy GameStop shares.

Many traders came to the conclusion that Robinhood was working to save the perceived hedge fund bad guys by the firm temporarily terminating user purchases in GameStop stock. Mr. Tenev blamed regulatory capital requirements as a reason for disallowing Robinhood-ers to buy GameStop last week, which was a major contributing factor to why the stock price plummeted by -44% on January 28th. The following day, Robinhood partially reversed its stance and subsequently allowed minimal daily purchases of one share.

How Does Short Selling Work?

In the stock market, you can make gains by buying shares that go up in price, or you can make profits by short selling shares that go down in price. If you buy a stock, the most money you could lose is -100% of your original investment. For example, if you invest $1,000 into GameStop stock by buying 50 shares at $20 each, if the stock price goes to $0, the most the investor/trader could lose is 100% of their $1,000 original investment.

On the flip side, if you short a stock, the potential losses are limitless. For example, if you (or a hedge fund manager) shorts $1,000 of GameStop stock by selling 50 shares short at $20 each, if the stock price goes to $60, the short seller just loss -200% of their original investment [($20/shr – $60/shr) X 50 shares] = -$2,000. If GameStop goes to $100, the short seller loses -400%, and if GameStop price goes to $220, the short seller loses -1,000%. As you can see, the higher the price goes, there are infinite potential losses of the investor, trader, or hedge fund manager.

If a stock price continues to move higher, the only way for a short seller to stop the bleeding (i.e., close their short position or “bet”) is to buy shares. As a reminder, a buyer of stock closes their position by selling shares after they originally buy shares. A short seller closes their position by buying shares after they initially sell shares short. So again, if GameStop share price continues to move higher, the only way for GameStop short sellers to stop their losses is to buy more GameStop shares. This is the equivalent of pouring gasoline on a blazing fire because as millions of Reddit/Robinhood-ers are pushing GameStop’s share price higher almost every day, short selling hedge fund managers are left scrambling for the exits and forced to close their positions at even higher prices (i.e., larger losses).

What Does This All Mean?

Whether you are talking about speculation in Bitcoin, the rise of SPACs (Special Purpose Acquisition Companies), the increase in the number of IPOs (Initial Public Offerings), or the Reddit-Robinhood Revolution, risk appetite has been on the rise and long-term investors should proceed very cautiously. Just as many have experienced on trips to Las Vegas, big winnings can quickly turn to huge losses. Although it’s certainly fun to watch the individual Davids take down the hedge fund/short selling Goliaths, if the Reddit-Robinhood community gets too aggressive in its speculation, history shows us they will end up being the ones swimming in their tears or stoned to death.

If you need assistance navigating through all these land mines, please give us a call at Sidoxia Capital Management (949-258-4322) for a complimentary portfolio review.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (February 1, 2021). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in GME, AMC, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Women & Bosoms on Wall Street According to Jones

Billionaire hedge fund manager of Tudor Investment Corporation, Paul Tudor Jones, recently suffered from a case of foot-in-mouth disease when he addressed a sensitive subject – the lack of female traders and investors on Wall Street. Rather than provide a diplomatic response to the mixed audience at a recent University of Virginia symposium, Tudor Jones went on an unambiguous rant. Here’s an excerpt:

“You will never see as many great women investors or traders as men. Period, end of story….As soon as that baby’s lips touch that girl’s bosom, forget it. Every single investment idea, every desire to understand what’s going to make this go up or gonna go down is going to be overwhelmed by the most beautiful experience, which a man will never share of that emotive connection between that mother and baby.”

A more complete review of his unfiltered response can be found in this video:

Clearly there is a massive minority of females on Wall Street, but why such an under-representation in this field relative to other female-heavy professional industries such as advertising, nursing, and teaching? I addressed this controversial subject in an earlier article (see Females in Finance)

If there are 155.8 million females in the United States and 151.8 million males (Census Bureau: October 2009), then how come only 6% of hedge fund managers (BusinessWeek), 8% of venture capitalists, and 15% of investment bankers are female (Harvard Magazine)? Is the finance field just an ol’ boys network of chauvinist pig-headed males who only hire their own? Maybe cultural factors such as upbringing and education are other factors that make math-related jobs more appealing to men? Or do the severe time-demands of the field force females to opt-out of the industry due to family priorities?

Although I’m sure family choices and quality of life are factors that play into the decision of entering the demanding finance industry, from my experience I would argue women are notoriously underrepresented even at younger ages. For example, anecdotal evidence coming from my investment management firm (Sidoxia Capital Management – www.Sidoxia.com) clearly shows a preponderance of internship applications coming from males, even though it is premature for these students to fully contemplate family considerations at this young age.

If under-representation in the finance field is not caused by female choice, then perhaps the male dominated industry is merely a function of more men opting into the field (i.e., men are better suited for the industry)? More specifically, perhaps male brains are just wired differently? Some make the argument that all the testosterone permeating through male bodies leads them to positions involving more risk. If you look at other risk related fields like gambling, women too are dramatic minorities, making up about 1/3 of total compulsive gamblers.

Women Better than Men?

The funny part about the under-representation of females in finance is that one study actually shows female hedge fund managers outperforming their male counterparts. Here’s what a BusinessWeek article had to say about female hedge fund managers:

A new study by Hedge Fund Research found that, from January 2000 through May 31, 2009, hedge funds run by women delivered nearly double the investment performance of those managed by men. Female managers produced average annual returns of 9%, versus 5.82% for men and, in 2008, when financial markets were cratering, funds run by women were down 9.6%, compared with a 19% decline for men.

The article goes onto to theorize that women may not be afraid of risk, but actually are better able to manage risk. A UC Davis study found that male managers traded 45% more than female managers, thereby reducing returns by -2.65% (about 1% more than females).

Regardless of the theories or studies used to explain gender risk appetite, the relative under-representation of females in finance is a fact. Many theories exist but further thought and research need to be conducted on the subject.

However, before Paul Tudor Jones is completely demonized or sent to the guillotine, let’s not forget Tudor Jones is obviously not your ordinary, heartless, cold-blooded Wall Street type, as evidenced by his recent philanthropic profile on 60 Minutes. Thanks to his generous efforts, Tudor Jones and his Robin Hood Foundation charity have raised more than $400 million for worthy causes since 1988.

While Paul Tudor Jones may not have harbored any malicious intent with regards to his comments, it may make sense for Tudor Jones to take a course on gender sensitivity. Bosoms and women may be an interesting subject for many, however he might consider filtering his commentary the next time he speaks to a large symposium recorded on the internet.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

See also:

BusinessWeek article on female fund managers

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Ping Pong Vet Blasts Goldman

Source: Photobucket

In a recent New York Times op-ed, Greg Smith, former Goldman Sachs Group Inc. (GS) employee and ping pong medalist at the Jewish Olympics, came out with an earth-shattering revelation… he discovered and revealed that Goldman Sachs was not looking out for the best interests of its clients. I was floored to discover that a Wall Street bank valued at $60 billion would value profits more than clients’ needs.

Hmmm, I wonder what new eye-opening breakthrough he will unveil next? Perhaps Smith will get a job at Las Vegas Sands Corp. (LVS) for 12 years and then enlighten the public that casinos are in the business of making money at the expense of their customers. I can’t wait to learn about that breaking news.

But really, with all sarcasm aside, any objective observer understands that Goldman Sachs and any other Wall Street firm are simply middlemen operating at the center of capitalism – matching buyers and sellers (lenders and borrowers) and providing advice on both sides of a transaction. As a supposed trusted intermediary, these financial institutions often hold privileged information that can be used to the firms’ (not clients) benefit.

Most industry veterans like me understand how rife with conflicts the industry operates under, but very few insiders publicly speak out about these “dirty little secrets.” Readers of Investing Caffeine know I am not bashful about speaking my mind. In fact, I have tackled this subject in numerous articles, including Wall Street Meets Greed Street written a few months ago. Here’s an excerpt**:

“Wall Street and large financial institutions, however, are driven by one single mode…and that is greed. This is nothing new and has been going on for generations. Over the last few decades, cheap money, loose regulation, and a relatively healthy economy have given Wall Street and financial institutions free rein to take advantage of the system.”

As with any investment, clients and investors should understand the risks and inherent conflicts of interest associated with a financial relationship before engaging into business. While certain disclosures are sorely lacking, it behooves investors and clients to ask tough questions of bankers and advisors – questions apparently Mr. Smith did not ask his employer over his 12 year professional career at Goldman Sachs.

Reputational Risk Playing Larger Role

Even though Goldman called some clients “muppets,” Smith states there was no illegal activity going on. Regardless of whether the banks have gotten caught conducting explicit law-breaking behavior, the public and politicians love scapegoats, and what better target than the “fat-cat” bankers. With a financial crisis behind us, along with a multi-decade banking bull market of declining interest rates, the culture, profitability-model, and regulations in the financial industry are all in the midst of massive changes. As client awareness and frustration continue to rise, reputational risk will slowly become a larger concern for Wall Street banks.

Could the Goldman glow as the leading Wall Street investment bank finally be getting tarnished? Well, besides their earnings collapsing by about 2/3rds in 2011, the selection of Morgan Stanley (MS) and JPMorgan Chase (JPM) ahead of Goldman Sachs as the lead underwriters in the Facebook (FB) initial public offering (IPO) could be a sign that reputational risk is playing a larger role in investment banking market share shifts.

The public and corporate America may be slow in recognizing the shady behavior practiced on Wall Street, but eventually, the excesses become noticed. Congress eventually implements new regulations (Dodd-Frank) and customers vote with their dollars by moving to banks and institutions they trust more.

I commend Mr. Smith for speaking out about the corrupt conflicts of interest and lack of fiduciary duty at Goldman Sachs, but let’s call a spade a spade and not mischaracterize a situation as suddenly shifting when the practices have been going on forever. Either he is naïve or dishonest (I hope the former rather than the latter), but regardless, finding a new job on Wall Street may be challenging for him. Fortunately for Mr. Smith, he has something to fall back on…the professional ping-pong circuit.

***Other Relevant Articles and Video:

- Goldman Gambling Prosperity at Client Expense

- Goldman Cheat? Really?

- Stephen Colbert: Breaking the Sacred Trust

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in FB, GS, MS, JPM, LVS, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Cramer Pulls Apple from Romney Tree

Republican Presidential primary candidate Mitt Romney has taken a lot of heat for his lack of conviction on various issues, whether they be on immigration, universal healthcare, or abortion. Jim Cramer, former hedge fund manager and host of TV show Mad Money, has also been known to do a bit of his own John Kerry-esque waffling. One of Cramer’s most recent high profile flip-flops is highflying Apple Inc. (AAPL). If Mitt Romney had his own stock show in his free time like Jim Cramer, there’s a high probability that Romney and Cramer could both agree that they were “for Apple, before they were against it, and now for it again.”

Some might think that picking on Jim Cramer is like clubbing a defenseless seal; wrestling a first grader; or stealing candy from a baby. Suffice it to say, I am not the first person to point out the dangers, inconsistencies, and irresponsible behavior associated with Jim Cramer’s recommendations. Here are some of the highest profile critiques of Jim Cramer in recent years past:

I. Daily Show Destruction

Vodpod videos no longer available.

Daily Show Skewering PART II Daily Show Skewering PART III

II. The Barron’s Bashing

This 2007 Barron’s article not only dissected all of Jim Cramer’s picks over a multi-year period and outlined how much money was lost relative to the major stock market indices, but also a subsequent Barron’s article highlighted research showing a strategy that could yield 25% per month by betting against Cramer’s picks.

This 2007 Barron’s article not only dissected all of Jim Cramer’s picks over a multi-year period and outlined how much money was lost relative to the major stock market indices, but also a subsequent Barron’s article highlighted research showing a strategy that could yield 25% per month by betting against Cramer’s picks.

III. New York Times Expose

Last year, this article highlighted the good, bad, and ugly, but the sentiment noted by famed Yale University endowment fund manager David Swensen echoes the sentiment of many investment professionals:

“Cramer induces his viewers to do things that are bad for them. He’s smart enough to know what he’s doing. ‘Mad Money’ delivers a very dangerous message — that individual investors can beat the market with momentum-driven, high-octane trading strategies. There are individuals who do beat the market, but their number is vanishingly small. Cramer is a master manipulator. He has absolutely no accountability. This is serious business; people’s retirements are at stake.”

Spoiled Apple Turns Sweet Again

Apple stock has historically been a favorite of Jim Cramer. Because why? Well, like many short-term traders, it’s a stock that has been going up! A few short months ago, however, Apple’s stock stopped going up, and was actually going down. Jim Cramer’s long love affair with Apple was on the rocks – this is what he had to say about Apple on November 9th (AAPL price – $395.28):

“Times Have Changed for Apple. I’m hearing about weak tablet sales, about iPhone 4S sales not up to snuff, along with worries about holiday sales for iPods.” In the past Jim would brush these worries aside, but in the past, the visionary Steve Jobs was still breathing. “These days though, every nuance, every little bit of worry about Apple, as we heard today from a brokerage firm talking about lighter tablet sales seaps into my ears, and I actually listen, and I agonize over it – I don’t want to…But I can’t dismiss these minute Apple data points as irrelevant any more. These days it would just be too glib…Apple is no longer a given. We are not going to re-recommend endlessly right here. We are waiting. I think actually better prices are coming. No reason to pull the trigger [buy]. No reason until then [lower prices].”

Oh my, what a difference 90 days makes! Has Steve Jobs been resurrected from the dead? Last I checked, the answer is no. Anxiety of whether new CEO Tim Cook was about to drive Apple off a cliff to obsolescence, like Research in Motion Ltd. (RIMM), has apparently been put on hold. Previous deep-rooted concerns about iPad and iPhone 4S sales from Jim Cramer’s in-depth analysis turned out to be completely off base. As a matter of fact, two months after Cramer went on his anti-Apple rant, the company reported blowout quarterly results of record proportions. Not only did earnings results explode +116% from a year ago (+37% higher than Wall Street forecasts), but iPad unit sales grew by +111% (15.4 million iPads) and iPhone unit sales grew +128% (37.0 million iPhones). To make matters worse, during Cramer’s temporary Apple break-up, he told his followers to buy Google Inc. (GOOG) instead of Apple. Oops…since that short time ago, Apple has only outperformed Google by a massive +28% or so.

Well, no reason to fret now because any worries about a dead Steve jobs, collapsing iPad/iPhone sales, and a RIMM-like train wreck have been quickly forgotten by Cramer over the last few months. Apple gloom has turned to champagne cheers. Here’s what Jim has to say now:

“This stock (Apple) has gripped the imagination like no other I’ve seen in my career. A stock going to $500 in a straight line.”

When Wall Street analysts recently weren’t bullish enough for Cramer (despite 50 “Buy” ratings, 3 “Hold” ratings, 2 “Sell” ratings), he had this to say:

“I want to grab them by the throat and say, ‘Will you give me a break?’ Apple sells at 10 times earnings; the average stock sells at 15 times earnings; Apple is a lot better than the average stock. Don’t you understand this stock is galloping to where it has to go, simply to catch up with the rest of the market? Don’t you see that happening? Don’t you understand that apple has to go higher?!

If these whipsaw stock recommendation reversals are not fast enough for you, no need to worry. Apparently flip-flopping on the overall market only takes 24 hours. Last week, Cramer could hardly control his excitement during his show’s opening, given another up-day in the market. To bolster his bullish case, Cramer proceeded to chastise Wall Street analysts for being so negative. With one rotation of the Earth, the following day, Cramer turned negative and nervous once again as the Dow Jones Industrials index fell 0.69%. Who knows what Cramer’s ever-changing mood will be next, but I can give you a hint – if you look at the daily direction of the Dow, your mood guessing batting average will be higher than Ty Cobb’s career average.

Selective Consumption at the Investment Supermarket

Despite all the criticisms, one should not shed a tear for this multi-mega-millionaire, Harvard grad, and Goldman Sachs Group Inc. alum (GS). Mad Money is highly entertaining for short-term traders, and in upward trending momentum markets, Cramer followers might do OK. Unfortunately, the lucrative, straight-upward market that Cramer made his fortunes in during the 1990s hasn’t been in existence over the last 12 years. For the untrained, investing masses who are looking to preserve and grow their retirement nest eggs, the schizophrenic recommendations that Jim Cramer provides can prove extremely damaging. We have seen this destructive dynamic especially at key inflection points in the market, whether it was at the 2000 peak of the market when his 10-stock “Winners of the New World” portfolio that collapsed by over -90%, or in late 2008/early 2009, near the market bottom, when Cramer told all investors to sell stocks unless you can wait five years.

Jim Cramer is not an evil person and he his very entertaining and sharp individual. I fully admit that I occasionally watch Mad Money for a chuckle and to also gain perspective of the speculative sentiment in the market. Although I would like to see better programming on the network, CNBC is not to be fully blamed. CNBC is like a supermarket that sells both healthy and unhealthy goods. While long-time Investing Caffeine readers know, I have been known to take numerous cavalier economists and strategists to task, many of my investing philosophies and strategies have been built off of long-time, successful investors that CNBC has interviewed or profiled. CNCB guests whom I have written about include, Warren Buffett, Ron Baron, Bill Gross, Ken Heebner, Wilbur Ross, Joel Greenblatt, Laszlo Birinyi, Jimmy Rogers, and others.

While Jim Cramer can be consumed in small doses by professionals and short-term traders, average investors should tread lightly. Investors will be better served by reading the labels of television commentators’ advice, and instead listen to those advisors or managers that have a time horizon consistent with your long-term financial goals.

Jim Cramer has been picked apart by many, but his screaming “Booyahs!,” singing “hallelujah” choirs, and flying bulls, make for compelling television. Although Jim Cramer and I are on the same page as Apple currently (I’ve owned for a long time), I have yet to come to a definitive decision on the 2012 presidential elections. If Cramer changes his view on Apple again in the coming days and weeks, I hope he invites his friend Mitt Romney on as a guest. That way I can kill two birds with one stone, and if one flip-flopper is entertaining to watch, having two should certainly be twice as amusing.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, AAPL, and GOOG but at the time of publishing SCM had no direct position in RIMM, GS, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Wall Street Meets Greed Street

For investors, the emotional pendulum swings back and forth between fear and greed. Wall Street and large financial institutions, however, are driven by one single mode…and that is greed. This is nothing new and has been going on for generations. Over the last few decades, cheap money, loose regulation, and a relatively healthy economy have given Wall Street and financial institutions free rein to take advantage of the system.

Not only did the financial industry explode, but the large got much larger. The FCIC (Financial Crisis Inquiry Commission), a government appointed commission, highlighted the following:

“By 2005, the 10 largest U.S. commercial banks held 55% of the industry’s assets, more than double the level held in 1990. On the eve of the crisis in 2006, financial sector profits constituted 27% of all corporate profits in the United States, up from 15% in 1980.”

What’s more, the obscene profits were achieved with obscene amounts of debt:

“From 1978 to 2007, the amount of debt held by the financial sector soared from $3 trillion to $36 trillion, more than doubling as a share of gross domestic product.”

Times have changed, and financial institutions have gone from victors to villains. Sluggish economic growth in developed countries and choking levels of debt have transitioned political policies from stimulus to austerity. This in turn has created social unrest. Who’s to blame for all of this? Well if you watch the evening news and Occupy Wall Street movement, it becomes very easy to blame Wall Street. Certainly, fat cat bankers deserve a portion of the blame. As one can see from the following list, over the last few years, the financial industry has paid for its sins with the help of a checkbook:

CLICK TO ENLARGE

The disgusting amount of inequitable excess is smeared across the whole industry in this tiny, partial list. Billions of dollars in penalties and disgorged assets isn’t insignificant, but besides Bernie Madoff and Raj Rajaratnam, very little time has been scheduled behind bars for the perpetrators.

Whom Else to Blame?

Are the greedy bankers and financial institution operators the only ones to blame? Without doubt, lack of government enforcement and adequate regulation, coupled with a complacent, debt-loving public, contributed to the creation of this financial crisis monster. When the economy was rolling along, there was no problem in turning a blind-eye to subversive activity. Now, the greed cannot be ignored.

At the end of the day, voters have to correct this ugly situation. The general public and Occupy Wall Street-ers need to boycott corrupt institutions and vote in politicians who will institute fair and productive regulations (NOT more regulations). Sure corporate financial lobbyists will try to tip the scales to their advantage, but a vote from a lobbyist attending a $10,000 black-tie dinner carries the same weight as a vote coming from a Occupy Wall Street-er paying $5 for a foot-long sandwich at Subway. As Thomas Jefferson stated, “A democracy is nothing more than mob rule, where fifty-one percent of the people may take away the rights of the other forty-nine.”

Investor Protocol

Besides boycotting greedy institutions and using the voting booth, what else should individuals do with their investments in this structurally flawed system? First of all, find independent firms with a fiduciary duty to act in your best interest, like an RIA firm (Registered Investment Advisor). Brokers, financial consultants, financial advisors, or whatever euphemism-of-the-day is being used for an investment product pusher, may not be evil, but their incentives typically are not aligned to protect and grow your financial future (see Fees, Exploitation, and Confusion and Letter Shell Game).

There is a lot of blame to be spread around for the financial crisis, and the intersection of Wall Street and Greed Street is a major contributing factor. However, investors and voters need to wake up to the brutal realities of our structurally flawed system and take matters into their own hands. Only then can Main Street and Wall Street peacefully coexist.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in MS, UBS, C, JPM, WFC, SCHW, AMTD, BAC, GS, STT, Galleon, RBC, Subway, Amer Home, Brookside Captl, Morgan Keegan, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Opening the Broker Departure Floodgates

Even though the equity markets have rebounded massively, investors remain in a sour mood in light of sluggish domestic economic headlines. Technology, for example High Frequency Trading (HFT – read more), along with the harsh realities of financial regulatory reform is creating profit growth challenges for the global financial gargantuans. More specifically, the floodgates have sprung open with respect to broker departures from the big four brokerage firms.

According to Bloomberg, more than 7,300 brokers have left the four largest full-service brokerage firms (Merrill Lynch [BAC], Morgan Stanley Smith Barney [MS], UBS Wealth Management [UBS], and Wells Fargo Advisors [WFC]) since the beginning of 2009. But the brokers have not floated away quietly – more than $1 trillion in assets have fled these major brokerage firms and followed the brokers to their new employers.

Several factors have led to the deluge of departures of bodies and bucks:

1) Mergers: The financial crisis triggered an all-out economic assault on the brokerage firm industry. A subsequent game of musical chairs resulted in the marriage of disparate cultures (e.g., B of A-Merrill; Morgan Stanley-Smith Barney; Wells Fargo-Wachovia). Not only did the clashing cultures rub brokers the wrong way, but the surviving executives were left with redundant and unproductive brokers to cut.

2) Heightened Recruiting: With a shrinking pie and less growth comes more fierce competition. The discount brokerage firms have realized the Darwinian challenges and reacted to them accordingly. Take TD Ameritrade (AMTD) for example. In the first seven months of 2010, the discount brokerage firm added 212 independent advisers to its network, a +44% increase over the previous year. Charles Schwab Corp. (SCHW) with its network of 6,000 independent advisers is also ratcheting up its efforts to poach brokers away from the large brokerage firms.

3) Economics: Would you like 40-50% of profits generated from new clients, or 80-100%? In many instances, the broker from the large branded institution funnels the majority of the commissions to the mother-ship. Sure, the broker receives back-office, marketing, and branding support, but some brokers are now asking themselves is the brand an asset or liability? Wall Street has gotten a large black eye and it will take time to heal their corporate images…if they ever manage to succeed at all.

4) Customer Choice: Lastly, and most importantly, customers are voting with their dollars. As I have indicated in the past, I strongly believe the current system is structurally flawed (see Financial Sharks article). Financial institutions craft incentives designed to line the pockets of brokers (salespeople) and prioritize corporate profits over client wealth creation and preservation. The existing failed industry structure is based upon smoke, mirrors, opacity, and small print. Many independent, fee-only advisors are structuring financial relationships that align with portfolio performance and make transparency a top priority. Customers appreciate these benefits and are shifting dollars away from the brokerage firms.

LPL Loving IPO Life

If you are having a difficult time processing the magnitude of this investment advice shift, then consider the $4.4 billion estimated value being placed on the planned IPO (Initial Public Offering) of LPL Financial, the independent brokerage firm of 12,000+ financial advisors. LPL serves as a conduit for legacy brokers to become independent, and still allow them to benefit from an array of ala carte support services. Growth has been strong too – over the last decade the advisor count at LPL has more than tripled and assets under their umbrella now exceed $250 billion.

The Wall Street broker floodgates have opened, so unless regulatory changes are enacted, the old flawed way of doing things will require a life support raft. If not, independent, fee-only advisors like Sidoxia Capital Management will benefit from the current sinking migration of brokers.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in BAC, MS, UBS, WFC, AMTD, SCHW, LPL Financial or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

King of Controversy Reveals Maverick Solution

Mark Cuban, provocative and brash owner of the Dallas Mavericks basketball team and #400 wealthiest person in the world ($2.4 billion net worth), according to Forbes, has never been shy about sharing his opinion. In fact, this multi-billionaire’s opinions have been discouraged on multiple occasions, as evidenced by the NBA (National Basketball Association) slapping Cuban with more than $1.6 million in fines for his outbursts.

Cuban doesn’t only provide his views on basketball, as a serial entrepreneur who cashed in his former company Broadcast.com to Yahoo! (YHOO) for $5.9 billion, he also is providing his thoughts on Wall Street and the 1,000 point “fat finger” trading meltdown from last week. What does Cuban say is the answer to the rampant speculation conducted by idiot financial engineers? “Tax the Hell Out of Wall Street,” says Cuban in his recent blog flagged by TRB’s Josh Brown.

A Taxing Solution

Specifically, Cuban wants to tax investors 25 cents per share (and 5 cents per share for stocks trading at $5 per share or less) in hopes of encouraging myopic speculating traders to become longer-term shareholders. Cuban believes this approach will weed out the day traders and investment renters who in reality “don’t add anything to the markets.” Seems like a reasonable belief to me.

According to Cuban’s math, here are some of the benefits the tax would bring to the financial system:

“If the NYSE, Nasdaq, Amex and OTC are trading 2 Billion shares a day or more, like today, thats $ 500 Million Dollars PER DAY. If there are 260 trading days a year. Thats about 130 Billion dollars a year. If volumes drop because of the tax. It is still 10s of Billions of dollars per year. Thats real money for the US Treasury. Thats also an annual payment towards the next time Wall Street screws up and we have a black swan event that no one planned on.”

Practically speaking, a flat rate 25 cent tax per share is probably not the best way to go if you were to introduce a transaction tax, but the crux of Cuban’s argument essentially would not change. Creating a flat percentage tax (e.g., 1%) would likely make more sense, even if complexity may increase relative to the 25 cent tax. Take for example Citigroup (C) and Berkshire Hathaway Class A (BRKA). Cuban’s plan would result in paying 1.2% tax on a $4.17 share of Citigroup versus only 0.00022% tax for a $116,000.00 share of Berkshire Hathaway. Simple accounting maneuvers such as reverse stock splits and slowing of stock dividends, along with reducing company dilution through share and option issuance, may be methods of circumventing some of the tax burden created under Cuban’s described proposal.

Politically, adding any tax to investing voters could be re-election suicide, so rather than calling it a trading tax, I suppose the politicians would have to come up with some other euphemism, such as “charitable administrative fee for speculative trading.” The financial industry has already become experts in taxing investors with fees (read Fees, Exploitation and Confusion), so maybe Congress could give the banks and fund companies a call for some marketing ideas.

Step 1: Transparency

The murkiness and lack of transparency across derivatives markets is becoming more and more evident by the day. Some recent events that bolster the argument include: a) New CDO (Collateralized Debt Obligation) derivative allegations surfacing against Morgan Stanley (MS); b) The SEC (Securities and Exchange Commission) charges against Goldman Sachs (GS) in the Abacus synthetic CDO deal (see Goldman Sachs article); c) The collapse of AIG’s Credit Default Swap (CDS) department and subsequent push to transfer trading to open exchanges; and d) Now we’re dealing with last week’s cascading collapse of the equity markets within minutes. The brief cratering of multiple indexes points to a potential order entry blunder and/or absence of adequate and consistent circuit breakers across a web of disparate exchanges and ECNs (Electronic Communication Networks).

The mere fact we stand here five days later with no substantive explanation for the absurd trading anomalies (see Making Megabucks 13 Minutes at a Time) is proof positive changes in derivative and exchange transparency are absolutely essential.

Step 2: Incentives

In Freakonomics, the best-selling book authored by Steven Levitt, we learn that “Incentives are the cornerstone of modern life,” and “Economics is, at root, the study of incentives.” Incentives are crucial in that they permeate virtually all aspects of financial markets, not only in assisting economic growth, but also the negative aspects of bursting financial bubbles.

Michael Mauboussin, the Chief Investment Strategist at Legg Mason (read more on Mauboussin), also expands on the role incentives played in the housing collapse:

“Many, if not most, of the parties involved in the mortgage meltdown were doing what makes sense for them—even if it wasn’t good for the system overall. Homeowners got to live in fancier homes, mortgage brokers earned fees on the mortgages they originated without having to worry about the quality of the loans, investment banks earned tidy fees buying, packaging, and selling these loans, rating agencies made money, and investors earned extra yield on so-called AAA securities. So it’s a big deal to watch and unpack incentives.”

Regulation, penalties, and fines are means of creating preventative incentives against improper or unfair behavior. Just as people have no incentive to wash a rental car, nor do high frequency traders have an incentive to invest in equity securities for any extended period of time. Adding a Cuban tax may not be a cure-all for all our country’s financial woes, but as the regulatory reform debate matures in Congress, this taxing idea emanating from the King of Controversy may be a good place to start.

Read full blog article written by Mark Cuban

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and an AIG subsidary structured security, but at the time of publishing SCM had no direct positions in YHOO, C, AIG, LM, GS, BRKA, or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Gekko & Greed – Friedman & Freedom

Gordon Gekko and Milton Friedman

As the old saying goes, the more things change, the more things stay the same. The topic of greed, fat cat bankers, and political self-preservation is just as prevalent and relevant today as it was three decades ago, as evidenced by Milton Friedman’s past television interview (see video below). Milton Friedman and Gordon Gekko, the conniving financier from Oliver Stone’s movie Wall Street played by Michael Douglas, both may not philosophically agree on all aspects of life and politics but Friedman would likely buy into much of Gekko’s view on greed:

“Greed, for lack of a better word, is good. Greed is right, greed works. Greed clarifies, cuts through, and captures the essence of the evolutionary spirit. Greed, in all of its forms; greed for life, for money, for love, knowledge has marked the upward surge of mankind. And greed, you mark my words, will not only save Teldar Paper, but that other malfunctioning corporation called the USA.”

Although Friedman held some extreme views on certain issues, fundamentally underlying all his principles was his convicted belief in freedom – political, individual, and economic freedom.

Some things never change – Milton Friedman talks about greed and capitalism with Phil Donahue.

Background

Milton Friedman (1912-2006), one of the greatest economists of the 20th Century was a Nobel Prize winner in economics, Professor at the University of Chicago (1946-1977), and an economic advisor to President Ronald Reagan. Friedman’s laissez-faire economic views coupled with his belief that government should be severely restricted, not only had a significant influence on the field of economics in the United States, but also globally. His body of work was expansive, but some major areas of contribution include his impact on Federal Reserve monetary policy; his written work on consumption and the natural rate of unemployment; and his rejection of the Phillips curve (the inverse relation of inflation relative to unemployment), to name a few.

Political & Economic Firestorm on the Horizon

Although Friedman is tightly associated with his Republican advisor work (including Ronald Reagan), he strictly considered himself a Libertarian at the core. As much as politically left leaning Americans are blaming the 2008-2009 financial crisis on Friedman-backed deregulation and a lack of government oversight, Conservatives and Libertarians are screaming bloody murder at the Democratic controlled Congress when it comes to all the bailouts, stimulus, and entitlement legislation. If Milton Friedman is looking down upon us now, my guess is that his vote is to flush all the proposed government spending down the toilet, let the failing financial institutions drown, and for Gordon Gekko’s sake, let the greedy, fat cat bankers thrive.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at time of publishing had no direct position on any security referenced. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Too Big to Fail (Review)

Some call Andrew Ross Sorkin’s new behind-the-scenes book about the financial crisis of 2008-2009 “Too Big to Read” due to its meaty page count at 624 pages (a tad more than my book). But actually, once you crack the first chapter of Too Big to Fail you become immediately sucked in. In creating the “fly on the wall” perspective covering the elite power brokers of Wall Street and Washington, Sorkin utilizes 500 hours of interviews with more than 200 individuals.

Through the detailed and vivid conversations, you get the keen sense of overwhelming desperation and self-preservation that overtakes the executives of the sinking financial system. Some of the chief participants failed, some were triumphant, and some were pathetically bailed out. History will ultimately be the arbiter of whether government and Wall Street averted, mitigated, postponed, or contributed to the financial collapse. Regardless, Sorkin brilliantly encapsulates this emotionally panicked period in our history that will never be erased from our memories.

Here are a few passages that capture the feeling and mood of the book:

Merger Musical Chairs

The terror-induced insanity of merger musical chairs is best depicted through the notepad of Timothy Geithner, then the president of the New York Federal Reserve Bank:

“On a pad that morning, Geithner started writing out various merger permutations: Morgan Stanley and Citigroup. Morgan Stanley and JP Morgan Chase. Morgan Stanley and Mitsubishi. Morgan Stanley and CIC. Morgan Stanley and Outside Investor. Goldman Sachs and Citigroup. Goldman Sachs and Wachovia. Goldman Sachs and Outside Investor. Fortress Goldman. Fortress Morgan Stanley. It was the ultimate Wall Street chessboard.”

AIG Bombshell

The book is also laced with financial nuggets to put the scope of the crisis in perspective. Here Sorkin examines the distressed call of assistance from AIG CEO, Bob Willumstad, to Timothy Geithner:

“A bombshell that Willumstad was confident would draw Geithner’s attention-was a report on AIG’s counterparty exposure around the world, which included ‘$2.7 trillion of notional derivative exposures, with 12,000 individual contracts.” About halfway down the page, in bold, was the detail that Willumstad hoped would strike Geithner as startling: “$1 trillion of exposures concentrated with 12 major financial institutions.’”

Bernanke’s Bumbled Spelling Bee

In setting the stage for the drama that unfolds, Sorkin also provides a background on the key players in the book. For example in describing Ben Bernanke you learn he was

“born in 1953 and grew up in Dillon South Carolina, a small town permeated by the stench of tobacco warehouses. As an eleven-year-old, he traveled to Washington to compete in the national spelling championship in 1965, falling in the second round, when he misspelled ‘Edelweiss.’”

TARP Tidbits

On how the precise $700 billion TARP (Troubled Asset Relief Program) figure was created, Sorkin describes the scattered thought process of the program designer Neel Kashkari:

“They knew they could count on Kashkari to perform some sort of mathematical voodoo to justify it: ‘There’s around $11 trillion of residential mortgages, there’s around $3 trillion of commercial mortgages, that leads to $14 trillion, roughly five percent of that is $700 billion.’ As he plucked numbers from thin air even Kashkari laughed at the absurdity of it all.”

Mercedes Moment

Mixed in with the facts and downbeat conversations are a series of humorous anecdotes and one-liners. Here is one exchange between Goldman Sachs CEO, Lloyd Blankfein, and his Chief of Staff Russell Horwitz:

“’I don’t think I can take another day of this,’ Horowitz said wearily. Blankfein laughed. ‘You’re getting out of a Mercedes to go to the New York Federal Reserve – you’re not getting out of a Higgins boat* on Omaha Beach! Keep things in perspective.’”

*Blankfein’s quote: A reference to the bloody D-Day battle.

Too Big to Fail is an incredible time capsule for the history books. Let’s hope we do not have to relive a period like this in our lifetimes. I wouldn’t mind reading another Andrew Ross Sorkin book…just not another one about a future financial crisis.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but did not have any direct positions in any stock mentioned in this article at time of publication (including GS, AIG, WFC, MS, and C). No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

China Executes Wall Street Solution

China is taking an innovative approach to white collar crime…execution. Yang Yanming, a rogue securities trader, completed his death sentence this week for embezzling $9.52 million (a daily rounding error for Goldman Sachs, I might add). Not exactly a cheery topic for the holiday season, but nonetheless, apparently an effective technique for cracking down on illegal behavior. Last I heard, there has been no mention of a $65 billion Chinese version of the Madoff Ponzi scheme? I wonder what kind of risks the financial division of AIG would have undertaken, if involuntary death sentences were considered as viable options in the back of their minds? China in fact carries out more annual executions (via lethal injection and gun) than any other country in the world.

Part of the recent financial crisis can be attributed to the culture of Wall Street and the investment industry, which centers on exploiting “OPM,” an acronym I use to describe “other people’s money.” Often, industry professionals (I use the term loosely) assume undue amounts of risk in hopes of securing additional income, no matter the potential impact on the client. The thought process generally follows: “Why should I risk my own capital to make a mega-bonus, when I can swing for the fences using someone else’s?” And if OPM cannot be secured from individuals, perhaps the capital can be borrowed from the banks – at least before the bailouts occurred.

OPM does come with some caveats, however. Say for example the OPM comes from the government. When TARP (Troubled Asset Relief Program) funds got crammed down the throats of the banking industry, the auspice of reduced bonuses didn’t sit very well with many of the fat-cat Wall Street executives. Financial institutions prefer their OPM with few strings and little to no accountability. Goldman Sachs (GS), JP Morgan (JPM), and Morgan Stanley (MS) weren’t big fans of the government’s pay scale, so these banks paid back the TARP funds at mid-year. Citigroup (C) is still negotiating with the U.S. Treasury and regulators to remove the scarlet phrase of “exceptional assistance” from their chests.

This subject of accountability brings up additional doses of blame to distribute. Not only are the gun-slinging bankers and advisers the ones to blame, but in many cases the clients themselves shoulder some of the responsibility. Either the clients’ start drinking the speculative “Kool-Aid” of their advisor or they neglect to ask a few basic questions for accountability. Just as Ronald Reagan stressed in his conversations with the Soviets, it is also imperative for clients to “trust but verify” the relationship with their advisor (read how to get your financial house in order).

One thing we learned from the crisis of 2008-2009 is that trust is a scarce resource. Investors can “luck” into a trustworthy relationship, but more often than not, just like anything else, it takes time and effort to build a worthy partnership.

The suppliers of OPM have gotten smarter and more skeptical after the crisis, however the managers of OPM haven’t discarded risk from their toolboxes. In addition to the general rebound in domestic equities, we have seen emerging markets, commodities, high-yield bonds, and foreign currencies (to name a few areas), also vault higher.

Regulatory reform for the financial industry is a hot topic for discussion, although virtually nothing substantive has been implemented yet. Incentives, accountability, and adequate capital requirements need to be put in place, so excessive risk-taking (like we saw at the AIG division handling Credit Default Swaps) doesn’t compromise the safety of our financial system. Also, traders need to be incentivized for making responsible decisions and punished adequately for participating in illegal activities. I know the President has a lot on his plate right now, but perhaps the Obama administration could set up a brief meeting with the capital punishment committee in Beijing. I’m confident the Chinese could assist us in “executing” a financial regulatory system solution.

Read Full Reuters Article on Rogue Chinese Trader

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (VFH) and BAC, but at time of publishing had no direct positions in GS, AIG, JPM, MS and C. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}