Posts tagged ‘volatility’

Searching for the Market Boogeyman

With the stock market reaching all-time record highs (S&P 500: 1900), you would think there would be a lot of cheers, high-fiving, and back slapping. Instead, investors are ignoring the sunny, blue skies and taking off their rose-colored glasses. Rather than securely sleeping like a baby (or relaxing during a three-day weekend) with their investment accounts, people are biting their fingernails with clenched teeth, while searching for a market boogeyman in their closets or under their beds.

If you don’t believe me, all you have to do is pick up the paper, turn on the TV, or walk over to the office water cooler. An avalanche of scary headlines that are spooking investors include geopolitical concerns in Ukraine & Thailand, slowing housing statistics, bearish hedge fund managers (i.e., Tepper Einhorn, Cooperman), declining interest rates, and collapsing internet stocks. In other words, investors are looking for things to worry about, despite record corporate profits and stock prices. Peter Lynch, the manager of the Magellan Fund that posted +2,700% in gains from 1977-1990, put short-term stock price volatility into perspective:

“You shouldn’t worry about it. You should worry what are stocks going to be 10 years from now, 20 years from now, 30 years from now.”

Rather than focusing on immediate stock market volatility and other factors out of your control, why not prioritize your time on things you can control. What investors can control is their asset allocation and spending levels (budget), subject to their personal time horizons and risk tolerances. Circumstances always change, but if people spent half the time on investing that they devoted to planning holiday vacations, purchasing a car, or choosing a school for their child, then retirement would be a lot less stressful. After realizing 99% of all the short-term news is nonsensical noise, the next important realization is stocks are volatile securities, which frequently go down -10 to -20%. As much as amateurs and professionals say or think they can profitably predict these corrections, they very rarely can. If your stomach can’t handle the roller-coaster swings, then you shouldn’t be investing in the stock market.

Bear-markets generally coincide with recessions, and since World War II, Americans experience about two economic contractions every decade. And as I pointed out earlier in A Series of Unfortunate Events, even during the current massive bull market, a recession has not been required to suffer significant short-term losses (e.g., Flash Crash, Greece, Arab Spring, Obamacare, Cyprus, etc.). Seasoned veterans understand these volatile periods provide incredible investment opportunities. As Warren Buffett states, “Be fearful when others are greedy, and be greedy when others are fearful.” Fear and panic may be behind us, but skepticism is still firmly in place. Buying during current skepticism is still not a bad thing, as long as greed hasn’t permeated the masses, which remains the case today.

Overly emotional people that make investment decisions with their gut do more damage to their savings accounts than conservative, emotional investors who understand their emotional shortcomings. On the other hand, the problem with investing too conservatively, for those that have longer-term time horizons (10+ years), is multi-pronged. For starters, overly conservative investments made while interest rate levels hover near historical lows lead to inflationary pressures gobbling up savings accounts. Secondly, the low total returns associated with excessively conservative investments will result in a later retirement (e.g., part-time Wal-Mart greeter in your 80s), or lower quality standard of living (e.g., macaroni & cheese dinners vs. filet mignon).

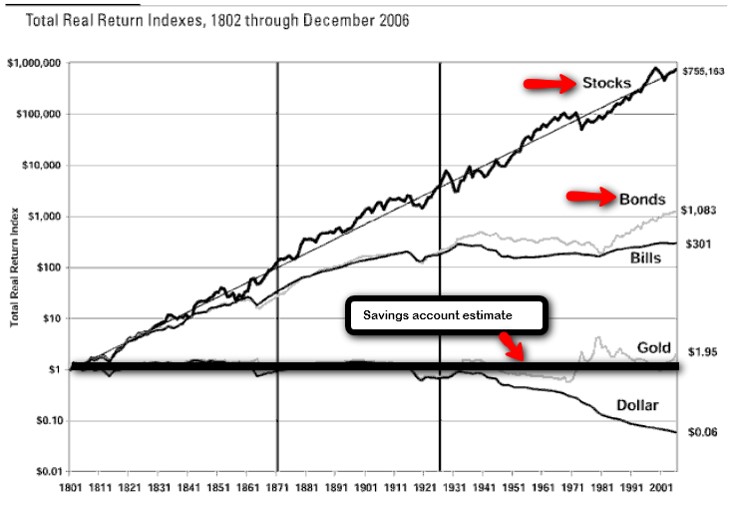

Most people say they understand the trade-offs of risk and return. Over the long-run, low-risk investments result in lower returns than high risk investments (i.e., bonds vs. stocks). If you look at the following chart and ask anyone what their preferred path would be over the long-run, almost everyone would select the steep, upward-sloping equity return line.

Source: Betterment.com / Stocks for the Long Run

Yet, stock ownership and attitudes towards stocks remain at relatively low and skeptical levels (see Gallup survey in Markets Soar and Investors Snore). It’s true that attitudes are changing at a glacial pace and bond outflows accelerated in 2013, but more recently stock inflows remain sporadic and scared money is returning to bonds. Even though it has been over five years, the emotional scars from 2008-2009 apparently still need some time to heal.

Investing in stocks can be very scary and hazardous to your health. For those millions of investors who realize they do not hold the emotional fortitude to withstand the ups and downs, leave the worrying responsibilities to the experienced advisors and investment managers like me. That way you can focus on your job and retirement, while the pros can remain responsible for hunting and slaying the boogeyman.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds and WMT, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Confessions of a Bond Hater

Source: stock.xchng

Hi my name is Wade, and I’m a bond hater. Generally, the first step in addressing any type of personal problem is admitting you actually have a problem. While I am not proud of being a bond hater, I have been called many worse things during my life. But as we have learned from the George Zimmerman / Trayvon Martin case, not every situation is clear-cut, whether we are talking about social issues or bond investing. For starters, let me be clear to everyone, including all my detractors, that I do not hate all bonds. In fact, my Sidoxia clients own many types of fixed income securities. What I do hate however are low yielding, long duration bonds.

Duration…huh? Most people understand what “low yielding” means, when it comes to bonds (i.e., low interest, low coupon, low return, etc.), but when the word duration is uttered, the conversation is usually accompanied by a blank stare. The word “duration” may sound like a fancy word, but in reality it is a fairly simple concept. Essentially, high-duration bonds are those fixed income securities with the highest sensitivity to changes in interest rates, meaning these bonds will go down most in price as interest rates rise.

When it comes to equity markets, many investors understand the concept of high beta stocks, which can be used to further explain duration. There are many complicated definitions for beta, but the basic principle explains why high-beta stock prices generally go up the most during bull markets, and go down the most during bear markets. In plain terms, high beta equals high octane.

If we switch the subject back to bonds, long duration equals high octane too. Or stated differently, long duration bond prices generally go down the most during bear markets and go up the most during bull markets. For years, grasping the risk of a bond bear market caused by rising rates has been difficult for many investors to comprehend, especially after witnessing a three-decade long Federal Funds tailwind taking the rates from about 20% to about 0% (see Fed Fatigue Setting In).

The recent interest rate spike that coincided with the Federal Reserve’s Ben Bernanke’s comments on QE3 bond purchase tapering has caught the attention of bond addicts. Nobody knows for certain whether this short-term bond price decline is the start of an extended bear market in bonds, but mathematics would dictate that there is only really one direction for interest rates to go…and that is up. It is true that rates could remain low for an indefinite period of time, but neither scenario of flat to down rates is a great outcome for bond holders.

Fixes to Fixed-Income Failings

Even though I may be a “bond hater” of low yield, high duration bonds, currently I still understand the critical importance and necessity of a fixed income portfolio for not only retirees, but also for the diversification benefits needed by a broader set of investors. So how does a bond hater reconcile investing in bonds? Easy. Rather than focusing on lower yielding, longer duration bonds, I invest more client assets in shorter duration and/or higher yielding bonds. If you harbor similar beliefs as I do, and believe there will be an upward bias to the trajectory of long-term interest rates, then there are two routes to go. Investors can either get compensated with a higher yield to counter the increased interest rate risk, and/or they can shorten duration of bond holdings to minimize capital losses.

Worth noting, there is an alternative strategy for low yielding, long duration bond lovers. In order to minimize interest rate risk, these bond lovers may accept sub-optimal yields and hold bonds to maturity. This strategy may be associated with short-term price volatility, but if the bond issuer does not default, at least the bond investor will get the full principal at maturity to help relieve the pain of meager yields.

Now that you’ve survived all this bond babbling, let me cut to the chase and explain a few ways Sidoxia is taking advantage of the recent interest rate volatility for our clients:

Floating Rate Bonds: Duration of these bonds is by definition low, or near zero, because as interest rates rise, coupons/interest payments are advantageously reset for investors at higher rates. So if interest rates jump from 2% to 3%, the investor will receive +50% higher periodic payments.

Inflation Protection Bonds: These bonds come in long and short duration flavors, but if interest rates/inflation rise higher than expected, investors will be compensated with higher periodic coupons and principal payments.

Shorter Duration: One definition of duration is the weighted average of time until a bond’s fixed cash flows are received. A way of shortening the duration of your bond portfolio is through the purchase of shorter maturity bonds (e.g., buying 3-year bonds rather than 30-year bonds).

High Yield Bonds: Investing in the high yield bond category is not limited to domestic junk bond purchases, but higher yields can also be earned by investing in international and/or emerging market bonds.

Investment Grade Corporate Bonds: Similar to high yield bonds, investment grade bonds offer the potential of capital appreciation via credit improvement. For instance, credit rating upgrades can provide gains to help offset price declines caused by rising interest rates.

Despite my bond hater status, the recent taper tantrum and interest rate spike, highlight some advantages bonds have over stocks. Even though prices declined, bonds by and large still have lower volatility than stocks; provide a steady stream of income; and provide diversification benefits.

To the extent investors have, or should have, a longer-term time horizon, I still am advocating a stock bias to client portfolios, subject to each investor’s risk tolerance. For example, an older retired couple with a conservative target allocation of 20%/80% (equity/fixed income) may consider a 25% – 30% allocation. A shift in this direction may still meet the retirees’ income needs (especially if dividend-paying stocks are incorporated), while simultaneously acknowledging the inflation and interest rate risks impacting bond positions. It’s important to realize one size doesn’t fit all.

Higher Volatility, Higher Reward

Frequent readers of Investing Caffeine have known about my bond hating tendencies for quite some time (see my 2009 article Treasury Bubble has not Burst…Yet), but the bond baby shouldn’t be thrown out with the bath water. For those investors who thought bonds were as safe as CDs, the recent -6% drop in the iShares Aggregate Bond Index (AGG) didn’t feel comfortable for most. Although I am still an enthusiastic stock cheerleader (less so as valuation multiples expand), there has been a cost for the gargantuan outperformance of stocks since March of ’09. While stocks have outperformed bonds (S&P vs. AGG) by more than +140%, equity investors have had to endure two -10% corrections and two -20% corrections (e.g.,Flash Crash, Debt Ceiling Debate, European Financial Crisis, and Sequestration/Elections). If investors want to earn higher long-term equity returns, this desire will translate into more volatility than bonds…and more Tums.

I may still be a bond hater, and the general public remains firm stock haters, but at some point in the multi-year future, I will not be surprised to hear myself say, “Hi my name is Wade, and I am addicted to bonds.” In the mean time, Sidoxia will continue to optimize its client bond portfolios for a rising interest rate environment, while also investing in attractive equity securities and ETFs. There’s nothing to hate about that.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), including floating rate bonds/loan funds, inflation-protection funds, corporate bond ETF, high-yield bond ETFs, and other bond ETFs, but at the time of publishing, SCM had no direct position in AGG or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Time Arbitrage: Investing vs. Speculation

The clock is ticking, and for many investors that makes the allure of short-term speculation more appealing than long-term investing. Of course the definition of “long-term” is open for interpretation. For some traders, long-term can mean a week, a day, or an hour. Fortunately, for those that understand the benefits of time arbitrage, the existence of short-term speculators creates volatility, and with volatility comes opportunity for long-term investors.

What is time arbitrage? The concept is not new and has been addressed by the likes of Louis Lowenstein, Ralph Wanger, Bill Miller, and Christopher Mayer. Essentially, time arbitrage is exploiting the benefits of moving against the herd and buying assets that are temporarily out of favor because of short-term fears, despite healthy long-term fundamentals. The reverse holds true as well. Short-term euphoria never lasts forever, and experienced investors understand that continually following the herd will eventually lead you to the slaughterhouse. Thinking independently, and going against the grain is ultimately what leads to long-term profits.

Successfully executing time arbitrage is easier said than done, but if you have a systematic, disciplined process in place that assists you in identifying panic and euphoria points, then you are well on your way to a lucrative investment career.

Winning via Long-Term Investing

Legg Mason has a great graphical representation of time arbitrage:

Source: Legg Mason Funds Management

The first key point to realize from the chart is that in the short-run it is very difficult to distinguish between gambling/speculating and true investing. In the short-run, speculators can make money just as well as anybody, and in some cases, even make more profits than long-term investors. As famed long-term investor Benjamin Graham so astutely states, “In the short run the market is a voting machine. In the long run it’s a weighing machine.” Or in other words, speculative strategies can periodically outperform in the short run (above the horizontal mean return line), while thoughtful long-term investing can underperform.

Financial Institutions are notorious for throwing up strategies on the wall like strands of spaghetti. If some short-term outperforming products spontaneously stick, then the financial institutions often market the bejesus out of them to unsuspecting investors, until the strategies eventually fall off the wall.

Beware o’ Short-Termism

I believe Jack Gray of Grantham, Mayo, Van Otterloo got it right when he said, “Excessive short-termism results in permanent destruction of wealth, or at least permanent transfer of wealth.” What’s led to the excessive short-termism in the financial markets (see Short-Termism article)? For starters, technology and information are spreading faster than ever with the proliferation of the internet, creating a sense of urgency (often a false sense) to react or trade on that information. With more than 2 billion people online and 5 billion people operating mobile phones, no wonder investors are getting overwhelmed with a massive amount of short-term data. Next, trading costs have declined dramatically in recent decades, to the point that brokerage firms are offering free trades on various products. Lower trading costs mean less friction, which often leads to excessive and pointless, profit-reducing trading in reaction to meaningless news (i.e., “noise”). Lastly, the genesis of ETFs (exchange traded funds) has induced a speculative fervor, among those investors dreaming to participate in the latest hot trend. Usually, by the time an ETF has been created, the cat is already out of the bag, and the low hanging profit fruits have already been picked, making long-term excess returns tougher to achieve.

There is never a shortage of short-term fears, and today the 2008-09 financial crisis; “Flash Crash”; debt downgrade; European calamity; upcoming presidential elections; expiring tax cuts; and structural debts/deficits are but a few of the fear issues du jour in investors’ minds. Markets may be overbought in the short-run, and a current or unforeseen issue may derail the massive bounce from early 2009. For investors who can put on their long-term thinking caps and understand the concept of time arbitrage, buying oversold ideas and selling over-hyped ones will lead to profitable usage of investment time.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Sweating Your Way to Investment Success

Source: StopSweatyArmpits.com

There are many ways to make money in the financial markets, but if this was such an easy endeavor, then everybody would be trading while drinking umbrella drinks on their private islands. I mean with all the bright blinking lights, talking baby day traders, and software bells and whistles, how difficult could it actually be?

Unfortunately, financial markets have a way of driving grown men (and women) to tears, usually when confidence is at or near a peak. The best investors leave their emotions at the door and follow a systematic disciplined process. Investing can be a meat grinder, but the good news is one does not need to have a 90% success rate to make it lucrative. Take it from Peter Lynch, who averaged a +29% return per year while managing the Magellan Fund at Fidelity Investments from 1977-1990. “If you’re terrific in this business you’re right six times out of 10,” says Lynch.

Sweating Way to Success

If investing is so tough, then what is the recipe for investment success? As the saying goes, money management requires 10% inspiration and 90% perspiration. Or as strategist and long-time investor Don Hays notes, “You are only right on your stock purchases and sales when you are sweating.” Buying what’s working and selling what’s not, doesn’t require a lot of thinking or sweating (see Riding the Wave), just basic pattern recognition. Universally loved stocks may enjoy the inertia of upward momentum, but when the music stops for the Wall Street darlings, investors rarely can hit the escape button fast enough. Cutting corners and taking short-cuts may work in the short-run, but usually ends badly.

Real profits are made through unique insights that have not been fully discovered by market participants, or in other words, distancing oneself from the herd. Typically this means investing in reasonably priced companies with significant growth prospects, or cheap out-of-favor investments. Like dieting, this is easy to understand, but difficult to execute. Pulling the trigger on unanimously hated investments or purchasing seemingly expensive growth stocks requires a lot of blood, sweat, and tears. Eating doughnuts won’t generate the conviction necessary to justify the valuation and excess expected return for analyzed securities.

Times Have Changed

Investing in stocks is difficult enough with equity fund flows hemorrhaging out of investor accounts like the asset class is going out of style (See ICI data via The Reformed Broker). Stocks’ popularity haven’t been helped by the heightened volatility, as evidenced by the multi-year trend in the schizophrenic volatility index (VIX) – escalated by the “Flash Crash,” U.S. debt ceiling debate, and European financial crisis. Globalization, which has been accelerated by technology, has only increased correlations between domestic market and international markets. As we have recently experienced, the European tail can wag the U.S. dog for long periods of time. In decades past, concerns over economic activity in Iceland, Dubai, and Greece may not even make the back pages of The Wall Street Journal. Today, news travels at the speed of a “Tweet” for every Angela Merkel – Nicolas Sarkozy breakfast meeting or Chinese currency adjustment, and eventually results in a sprawling front page headline.

The equity investing game may be more difficult today, but investing for retirement has never been more important. Stuffing money under the mattress in Treasuries, money market accounts, CDs, or other conservative investments may feel good in the short run, but will likely not cover inflation associated with rising fuel, food, healthcare, and leisure costs. Regardless of your investment strategy, if your goal is to earn excess returns, you may want to check the moistness of your armpits – successful long-term investing requires a lot of sweat.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in ETFC, VXX, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

August Shakes, Rattles, and Swirls

Shake, Rattle, & Swirl: Category 3 hurricane Irene pounded the eastern seaboard with winds reaching 110 miles per hour, knocking out power in an estimated 8 million homes and businesses. Some analysts estimate the damage to be somewhere between $7 billion and $10 billion. If that wasn’t enough, earlier in the same week, a 5.8-magnitude earthquake rippled from its Virginia epicenter up to Maine rattling both buildings and people’s nerves.

Shake, Rattle, & Swirl: Category 3 hurricane Irene pounded the eastern seaboard with winds reaching 110 miles per hour, knocking out power in an estimated 8 million homes and businesses. Some analysts estimate the damage to be somewhere between $7 billion and $10 billion. If that wasn’t enough, earlier in the same week, a 5.8-magnitude earthquake rippled from its Virginia epicenter up to Maine rattling both buildings and people’s nerves.

Volatility Spikes in August: Volatility, as measured by the Volatility Index (VIX – a.k.a. “Fear Gauge”), reared its ugly head again in August, reaching a level exceeding 44 (Source: Hays Advisory). This reading has only been experienced nine times in the last 25 years. Historically, on average, these have been excellent buying points for long-term investors.

Volatility Spikes in August: Volatility, as measured by the Volatility Index (VIX – a.k.a. “Fear Gauge”), reared its ugly head again in August, reaching a level exceeding 44 (Source: Hays Advisory). This reading has only been experienced nine times in the last 25 years. Historically, on average, these have been excellent buying points for long-term investors.

![]() Steve Jobs Lets Go of Reins: After being Chief Executive Officer of Apple Inc. (AAPL – formerly Apple Computers) for more than 20 years, Steve Jobs passed the CEO reins over to Tim Cook, who has been with the company for 13 years (including interim CEO). Jobs will remain on board as Chairman of Apple and still provide assistance in a more limited capacity.

Steve Jobs Lets Go of Reins: After being Chief Executive Officer of Apple Inc. (AAPL – formerly Apple Computers) for more than 20 years, Steve Jobs passed the CEO reins over to Tim Cook, who has been with the company for 13 years (including interim CEO). Jobs will remain on board as Chairman of Apple and still provide assistance in a more limited capacity.

Buffett Puts Dry Powder to Work: Billionaire Warren Buffett is putting his money where his mouth is. Although he is one of a few wealthy individuals griping about too LOW income taxes (NYT OpEd), at least he is using some of his extra bucks to support the country’s financial system. More specifically, Buffet’s Berkshire Hathaway Inc. (BRKA) is investing $5 billion in troubled banking giant Bank of America Corp.’s (BAC) preferred stock (paying a 6% dividend), with warrants to buy additional stock in the future at a mutually prearranged price.

Buffett Puts Dry Powder to Work: Billionaire Warren Buffett is putting his money where his mouth is. Although he is one of a few wealthy individuals griping about too LOW income taxes (NYT OpEd), at least he is using some of his extra bucks to support the country’s financial system. More specifically, Buffet’s Berkshire Hathaway Inc. (BRKA) is investing $5 billion in troubled banking giant Bank of America Corp.’s (BAC) preferred stock (paying a 6% dividend), with warrants to buy additional stock in the future at a mutually prearranged price.

Google Buys Motorola Mobility: Google Inc. (GOOG) agreed to pay $12.5 billion to buy cellphone maker Motorola Mobility Holdings (MMI) in a move designed to protect the internet giant, and its partners, against patent litigation as it pertains to the Google Android mobile phone operating system. that could shake up the balance of power among among tech rivals. Time will tell whether Motorola’s assets will providing valuable resources for Google’s partners (i.e., HTC, LG Electronics and Samsung Electronics) or whether the acquisition will create competitive conflicts.

Google Buys Motorola Mobility: Google Inc. (GOOG) agreed to pay $12.5 billion to buy cellphone maker Motorola Mobility Holdings (MMI) in a move designed to protect the internet giant, and its partners, against patent litigation as it pertains to the Google Android mobile phone operating system. that could shake up the balance of power among among tech rivals. Time will tell whether Motorola’s assets will providing valuable resources for Google’s partners (i.e., HTC, LG Electronics and Samsung Electronics) or whether the acquisition will create competitive conflicts.

ECB Buys some Bonds:The European Central Bank (ECB), Europe’s equivalent of the U.S. Federal Reserve Bank, began buying up billions of dollars in Spanish and Italian bonds last month. The goal of the bond buying program is to stem any potential contagion effect arising from debt crises occurring in countries like Greece, Portugal, and Ireland.

ECB Buys some Bonds:The European Central Bank (ECB), Europe’s equivalent of the U.S. Federal Reserve Bank, began buying up billions of dollars in Spanish and Italian bonds last month. The goal of the bond buying program is to stem any potential contagion effect arising from debt crises occurring in countries like Greece, Portugal, and Ireland.

Quote of the Month

On Volatility:

“Worry gives a small thing a big shadow.”

– Swedish Proverb

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: For those taking this article seriously, please look up “parody” in the dictionary. Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, GOOG, and AAPL, but at the time of publishing SCM had no direct position in BRKA, MMI, HTC,

LG Electronics and Samsung Electronics, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page

Shoot First and Ask Later?

The financial markets have been hit by a tsunami on the heels of idiotic debt negotiations, a head-scratching credit downgrade, and slowing economic data after a wallet-emptying spending binge by the government. These chain of events have forced many investors and speculators alike to shoot first, and ask questions later. Is this the right strategy? Well, if you think the world is going to end and we are in a global secular bear market stifled by a choking pile of sovereign debt, then the answer is a resounding “yes.” If however, you believe the blood curdling screams from an angered electorate will eventually influence existing or soon-to-be elected politicians in dealing with the obvious, then the answer is probably “no.”

Plug Your Ears

Anybody that says they confidently know what is really going to happen over the next six months is a moron. You can ask those same so-called talking head experts seen over the airwaves if they predicted the raging +35% upward surge last summer, right after the market tanked -17% on “double-dip” concerns and Fed Chairman Ben Bernanke gave his noted quantitative easing speech in Jackson Hole, Wyoming. I’m still flicking through the channels looking for the professionals who perfectly envisaged the panicked buying of the same downgraded Treasuries Standard and Poor’s pooped on. Oh sure, it makes perfect sense that trillions of dollars would flock to the warmth and coziness of sub-2% yielding debt in a country exploding with unsustainable obligations and deficits, fueled by a Congress that can barely blows its nose to a successful negotiation.

The moral of the story is that nobody knows the future with certainty – no matter how much CNBC producers would like you to believe the opposite is true. Some of the arguably smartest people in the world have single handedly triggered financial market implosions. Consider Robert Merton and Myron Scholes, both renowned Nobel Prize winners, who brought global financial markets to its knees in 1998 when Merton and Scholes’s firm (Long Term Capital Management) lost $500 million in one day and required a $3.6 billion bailout from a consortium of banks. Or ask yourself how well Fed Chairmen Alan Greenspan and Ben Bernanke did in predicting the credit crisis and housing bubble.

If the strategist or trader du jour squawking on the boob-tube was really honest, he or she would steal the sage words of wisdom from the television series secret agent Angus MacGyver who articulated, “Only a fool is sure of anything, a wise man keeps on guessing.”

Listen to the “E”-Word

If you can’t trust all the squawkers, then whom can you trust (besides me of course…cough, cough)? The answer is no different than the person you would look for in other life-important decisions. If you needed a serious heart by-pass surgery, would you get advice from a nurse or medical professor, or would you listen more closely to the top cardiologist at the Mayo Clinic who performed over 2,000 successful surgeries? If you were looking for a pilot to fly your plane, would you prefer a 25-year-old flight attendant, or a 55-year old steely veteran who has 10 million miles of flight experience? OK, I think you get the point…legitimate experience with a track record is key.

Unfortunately, most of the slick, articulate people we see on television may look experienced and have some gray hair, but the only thing they are experienced at is giving opinions. As my great, great grandmother once told me, “Opinions are a dime a dozen, but experience is much more valuable” (embellished for dramatic effect). You are better off listening to experienced professionals like Warren Buffett (listen to his recent Charlie Rose interview), who have lived through dozens of crises and profited from them – Buffett becoming the richest person on the planet doesn’t just come from dumb luck.

If you are having trouble sleeping, you either are taking too much risk, or do not understand the nature of the risk you are taking (see Sleeping like a Baby). Things can always get worse, and the risk of a self-fulfilling further decline is a possibility (read about Soros and Reflexivity). If you are determined to make changes to your portfolio, use a scalpel, and not an axe. The recent extreme volatility makes times like these ideal for reviewing your financial position, goals, and risk tolerance. But before you shoot your portfolio first, and ask questions later, prevent a prison sentence of panic, or your financial situation may end up behind bars.

[tweetmeme source=”WadeSlome” only_single=false https://investingcaffeine.com/2011/08/20/shoot-first-and-ask-later/%5D

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in MHP, CMCSA, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Sleeping like a Baby with Your Investment Dollars

Amidst the recent, historically high volatility in the financial markets, there have been a large percentage of investors who have been sleeping like a baby – a baby that stays up all night crying! For some, the dream-like doubling of equity returns achieved from the first half of 2009 through the first half of 2011 quickly turned into a nightmare over the last few weeks. We live in an inter-connected, globalized world where news travels instantaneously and fear spreads like a damn-bursting flood. Despite the positive returns earned in recent years, the wounds of 2008-2009 (and 2000 to a lesser extent) remain fresh in investors’ minds. Now, the hundred year flood is expected every minute. Every European debt negotiation, S&P downgrade, or word floating from Federal Reserve Chairman Ben Bernanke’s lips, is expected to trigger the next Lehman Brothers-esque event that will topple the global economy like a chain of dominoes.

Volatility Victims

The few hours of trading that followed the release of the Federal Reserve’s August policy statement is living proof of investors’ edginess. After initially falling approximately -400 points in a 30 minute period late in the day, the Dow Jones Industrial Average then climbed over +600 points in the final hour of trading, before experiencing another -400 point drop in the first hour of trading the next day. Many of the day traders and speculators playing with the explosively leveraged exchange traded funds (e.g., TNA, TZA, FAS, FAZ), suffered the consequences related to the panic selling and buying that comes with a VIX (Volatility Index) that climbed about +175% in 17 days. A VIX reading of 44 or higher has only been reached nine times in the last 25 years (source: Don Hays), and is normally associated with significant bounce-backs from these extreme levels of pessimism. Worth noting is the fact that the 2008-2009 period significantly deteriorated more before improving to a more normalized level.

Keys to a Good Night’s Sleep

The nature of the latest debt ceiling negotiations and associated Standard & Poor’s downgrade of the United States hurt investor psyches and did little to boost confidence in an already tepid economic recovery. Investors may have had some difficulty catching some shut-eye during the recent market turmoil, but here are some tips on how to sleep comfortably.

• Panic is Not a Strategy: Panic selling (and buying) is not a sustainable strategy, yet we saw both strategies in full force last week. Emotional decisions are never the right ones, because if they were, investing would be quite easy and everyone would live on their own personal island. Rather than panic-sell, investments should be looked at like goods in a grocery store – successful long-term investors train themselves to understand it is better to buy goods when they are on sale. As famed growth investor Peter Lynch said, “I’m always more depressed by an overpriced market in which many stocks are hitting new highs every day than by a beaten-down market in a recession.”

• Long-Term is Right-Term: Everybody would like to retire at a young age, and once retired, live like royalty. Admirable goals, but both require bookoo bucks. Unless you plan on inheriting a bunch of money, or working until you reach the grave, it behooves investors to pull that money out from under the mattress and invest it wisely. Let’s face it, entitlements are going to be reduced in the future, just as inflation for food, energy, medical, leisure and other critical expenses continue eroding the value of your savings. One reason active traders justify their knee-jerk actions and derogatory description of long-term investors is based on the stagnant performance of U.S. equity markets over the last decade. Nonetheless, the vast number of these speculators fail to recognize a more than tripling in average values in markets like Brazil, India, China, and Russia over similar timeframes. Investing is a global game. If you do not have a disciplined, systematic long-term investment strategy in place, you better pray you don’t lose your job before age 70 and be prepared to eat Mac & Cheese while working as a Wal-Mart (WMT) greeter in your 80s.

• Diversification: Speaking of sleep, the boring topic of diversification often puts investors to sleep, but in periods like these, the power of diversification becomes more evident than ever. Cash, metals, and certain fixed income instruments were among the investments that cushioned the investment blow during the 2008-2009 time period. Maintaining a balanced diversified portfolio across asset classes, styles, size, and geographies is crucial for investment survival. Rebalancing your portfolio periodically will ensure this goal is achieved without taking disproportionate sized risks.

• Tailored Plan Matching Risk Tolerance: An 85 year-old wouldn’t go mountain biking on a tricycle, and a 10 year-old shouldn’t drive a bus to his fifth grade class. Sadly, in volatile times like these, many investors figure out they have an investment portfolio mismatched with their goals and risk tolerance. The average investor loves to take risk in up-markets and shed risk in down-markets (risk in this case defined as equity exposure). Regrettably, this strategy is designed exactly backwards for long-term investors. Historically, actual risk, the probability of permanent losses, is much lower during downturns; however, the perceived risk by average investors is viewed much worse. Indeed, recessions have been the absolute best times to purchase risky assets, given our 11-for-11 successful track record of escaping post World War II downturns. Could this slowdown or downturn last longer than expected and lead to more losses? Absolutely, but if you are planning for 10, 20, or 30 years, in many cases that issue is completely irrelevant – especially if you are still adding funds to your investment portfolio (i.e., dollar-cost averaging). On the flip side, if an investor is retired and entirely dependent upon an investment portfolio for income, then much less attention should be placed on risky assets like equities.

If you are having trouble sleeping, then one of two things is wrong: 1.) You are taking on too much risk and should cut your equity exposure; and/or 2.) You do not understand the risk you are taking. Volatile times like these are great for reevaluating your situation to make sure you are properly positioned to meet your financial goals. Talking heads on TV will tell you this time is different, but the truth is we have been through worse times (see History Never Repeats, but Rhymes), and lived to tell the tale. All this volatility and gloom may create anxiety and cause insomnia, but if you want to quietly sleep through the noise like a content baby, make yourself a long-term financial bed that you can comfortably sleep in during good times and bad. Focusing on the despondent headline of the day, and building a portfolio lacking diversification will only lead to panic selling/buying and results that would keep a baby up all night crying.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including emerging market ETFs) and WMT, but at the time of publishing SCM had no direct position in TNA, TZA, FAS, FAZ, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Getting Paid to Eat Bon-Bons and Sell Options

I have a diverse set of interests, and two of my passions include eating assorted bon bons, and buying stocks low (selling them high). The only thing better than that is to also get paid for doing those same activities. Until I get paid for competing on the national bon bon competitive eating circuit, I’ll stick to getting paid for selling (“writing”) options.

The Mechanics of Option Writing

There are many places to learn about the basics of options, but for simplicity purposes think of options as tools for speculating, hedging, and generating income. Unfortunately, most people trading options lose money because of speculation and numerous shortcomings. Like guns, knives, or any other weapon, if properly used, these self-defense option tools can provide owners with significant benefits. If however the weapons are used irresponsibly, the consequences can be deadly. The same principles apply to options investing – beneficial in the right hands, disastrous in the wrong hands (see also Butter Knife or Cleaver article).

A Pricey Option Illustration

In order to illustrate the mechanics of option writing, let’s use Priceline.com Inc. (PCLN) as an example:

Suppose I did my in-depth fundamental research on Priceline and upon completion of my due diligence I realized that the stock is fairly valued at its current share price of $529. However, upon further consideration I realize I would love to buy 100 shares at a discount price of $500 if Priceline shares pulled back. In mirror-like fashion my fundamental valuation process may also indicate an adequate selling valuation level at a $560 premium.

Based on these previous assumptions, I could profitably sell (“write”) one naked put option with a strike price of $500 and an expiration date in October (approximately five months from today), in exchange for $3,560 in upfront cash less comissions.* That’s right, someone is going to pay me thousands of dollars to buy something I am openly willing to purchase at lower prices anyway. In bon bon terminology, speculators are paying me to eat bon bons, an activity I love even without upfront cash payments from others. In the case of an escalating Priceline share price, I prefer to sell covered calls (i.e. own underlying stock position plus simultaneously selling a call option), consistent with my valuation sell price targets (strik price of $560 per share).

Selling Insurance

Since writing options is effectively like selling insurance, it intuitively follows the best time to sell insurance is when people (investors) are the most nervous. If you were a fire insurance carrier and wanted to maximize collections, setting prices a week after a large fire in the hot, dry summer season around the firework-laden 4th of July may not be a bad choice. In the equity markets, the VIX (Volatility Index) is often referred to as the “fear gauge,” which can be used as an indicator to optimize premium collections from options sales.

Options, which are part of the derivatives family, get lumped into these wide set of financial instruments that billionaire investor Warren Buffett called “weapons of mass destruction.” The ironic part of that whole situation is that despite the evil titling of these instruments, Buffett has used these “weapons of mass destruction” extensively, more recently with his strategies related to selling index options – see Insurance Weapons of Mass Destruction. For those who followed the financial crisis of 2008-2009, observers fully realize that American International Group (AIG) was selling insurance on credit defaults (Credit Default Swaps). Regrettably, the CDS market was not regulated to a similar extent as the more sophisticated options and futures market.

Eating bon bons for pay can be satisfying, and so can trading stocks for cash, when buying them low and selling them high. On the other hand, these same activities can prove to be harmful if abused or misused. If you eat bon bons in moderation, and receive premiums from thoroughly researched naked puts and covered calls, then you have nothing to worry about.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: *Based on 5-9-11 closing trade data from Yahoo Finance. Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in PCLN, AIG, VXX or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Ray Allen, the VIX, and the Rule of 16

Photo Source: Babble.com

Ray Allen gets paid a lot of money for running into people and bouncing an orange ball around a wooden floor, but even his game can appreciate the importance volatility can play in a high stakes game. First, Allen set an NBA Final’s basketball record of eight three-pointers made (including seven in a row) in Game 2, and then followed up in the next game with an astonishingly dismal “O” for thirteen performance – the second worst shooting performance during a Final’s game in 32 years. The emotional rollercoaster ride for the Celtics fans resembles a volatility chart of the VIX (Volatility Index) in recent weeks.

Chart Source: Yahoo! Finance

In the last 40 trading days the VIX has moved more than +/- 5% on 30 different trading sessions (75% of the time), including seventeen +/- 10% trading days. The +32% spike in the VIX on the day of the “Flash Crash” (May 6, 2010) would have even generated a smirk on the face of Ray Allen, not to mention the face changing impact of the other three +/- 30% move days that occurred within a month of the Flash Crash trading debacle. Even though the VIX has settled down from a short-term peak last month (48.20 on May 21st) to a lower level (28.79), the fear gauge still stands at almost double the rate of the multi-year low just a few months ago (15.23 on April 12th).

The VIX and the Rule of 16

No, this VIX is not the same as the Vicks vapor rub medication placed on your chest to relieve cough symptoms, rather this VIX indicator calculates inputs from various call and put options to create an approximation of the S&P 500 index implied volatility for the next 30 days. Put simply, when fear is high, the price of insurance catapults upwards as measured by the VIX – just like we saw when the VIX spiked above 80 during the 2008 financial crisis and above 40 during the more fresh Greek debt disaster. I’m not in the position to bust out some differential calculus to explain the nuances of a complex VIX formula, but what I can do is regurgitate a helpful formula relating to the VIX, called the Rule of 16. What the Rule of 16 allows laymans to do is understand the relationship between the VIX and daily volatility.

This is how Jeff Luby of Green Faucet describes the Rule of 16:

• VIX of 16 – 1/3 of the time the SPX will have a daily change of at least 1%

• VIX of 32 – 1/3 of the time the SPX will have a daily change of at least 2%

• VIX of 48 – 1/3 of the time the SPX will have a daily change of at least 3%

To put these VIX numbers in perspective, industry citations put the long-term VIX average around a level of 20. With a VIX hovering around 30 now, we are approaching the 2nd bucket of expectations (2%+ moves in the market 1/3 of the time). The price moves don’t correlate directly with the Dow Jones Industrial Average index, but I think about the current VIX levels equating to about a +/- 200 point move in the Dow one or two times per week…uggh.

Generally, I would prefer lower volatility, but I continually remind myself volatility is not necessarily a bad thing – volatility creates opportunities. I’m not sure if I can apply the Rule of 16 to Ray Allen’s scoring output, however based on last night’s 5-10 shooting performance, perhaps volatility in the market and Ray Allen’s shooting game will begin to normalize toward historical ranges.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including S&P 500-like positions), but at the time of publishing SCM had no direct positions in SPX, VIX-related securities, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Seesawing Through Organized Chaos

Still fresh in the minds of investors are the open wounds created by the incredible volatility that peaked just a little over a year ago, when the price of insurance sky-rocketed as measured by the Volatility Index (VIX). Even though equity markets troughed in March of 2009, earlier the VIX reached a climax over 80 in November 2008. With financial institutions falling like flies and toxic assets clogging up the lending pipelines, virtually all asset classes moved downwards in unison during the frefall of 2008 and early 2009. The traditional teeter-totter phenomenon of some asset classes rising simultaneously while others were falling did not hold. With the recent turmoil in Greece coupled with the “Flash Crash” (read making $$$ trading article) and spooky headline du jour, the markets have temporarily reverted back to organized chaos. What I mean by that is even though the market recently dove about +8% in 8 days, we saw the teeter-totter benefits of diversification kick in over the last month.

Seesaw Success

While the S&P fell about -4.5% over the studied period below, the alternate highlighted asset classes managed to grind out positive returns.

While traditional volatility has returned after a meteoric bounce in 2009, there should be more investment opportunities to invest around. With the VIX hovering in the mid-30s after a brief stay above 40 a few weeks ago, I would not be surprised to see a reversion to a more normalized fear gauge in the 20s – although my game plan is not dependent on this occurring.

VIX Chart Source: Yahoo! Finance

Regardless of the direction of volatility, I’m encouraged that even during periods of mini-panics, there are hopeful signs that investors are able to seesaw through periods of organized chaos with the assistance of good old diversification.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including AGG, BND, VNQ, IJR and TIP), but at the time of publishing SCM had no direct positions in VXX, GLD, or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}