Posts tagged ‘unemployment’

The COVID Comeback

Rocky Balboa (“The Italian Stallion”) the underdog boxer from the movie, Rocky, was down and out until he was given the opportunity to fight World Heavyweight Champion, Apollo Creed. Like the stock market during early 2020, Rocky was up against the ropes and got knocked down, but eventually he picked himself up and rebounded to victory in his rematch with Creed.

The stock market comeback also persisted last month as the COVID-19 pandemic health situation continued to stabilize and the broader economy accelerated business re-openings. For the month, the Dow Jones Industrial Average increased +4.3% (+1,037 points to 25,383), while the S&P 500 index bounced+5.3%, and the NASDAQ catapulted the most by +6.8%.

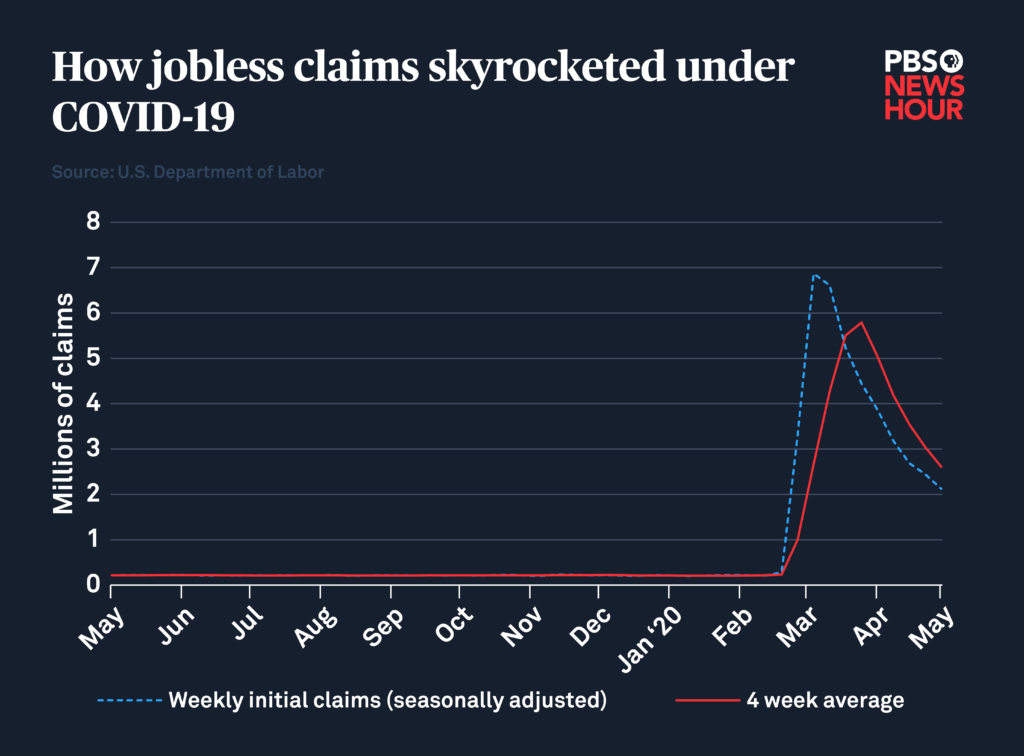

How can the stock market (i.e., the Dow) rebound +39%, or more than 7,100 points, from the March 2020 lows? The large move is even more surprising once you consider 41 million people have lost their jobs since the epidemic hit American soil (see chart below), and COVID-19 related deaths have climbed to over 100,000 people.

Getting Back to Fighting Shape

By the time we reached Rocky VI, Rocky Balboa was retired and recovered from brain damage. But Rocky is no quitter, and he trained himself into championship fighting condition and got back into the boxing ring. With unemployment rates approaching Great Depression levels, the U.S. economy has been experiencing challenging circumstances as well – a self-induced coma (shutdown). Fortunately, our country has been slowly recovering day-by-day, and week-by-week. The economy may not be back to peak fighting shape, but activity is slowly and consistently getting better.

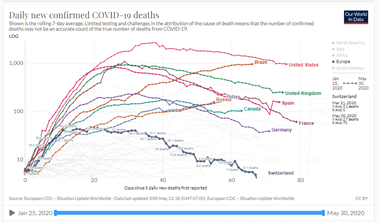

There are many different perspectives in looking at this extremely complex, unprecedented coronavirus pandemic. The speed and pace of selling stocks during February and March reached radically-high panic levels, as measured by objective indicators like the Volatility Index (i.e., the VIX – or Fear Gauge). However, like a coiled spring, the stock market sprung back up during April and May as stay-at-home orders and quarantine measures around the world significantly bent the curve of COVID-19 infections and deaths (see chart below). As you can see, with the exception of a few countries globally (e.g., Brazil and Russia), the number of daily confirmed deaths has been broadly declining for many weeks.

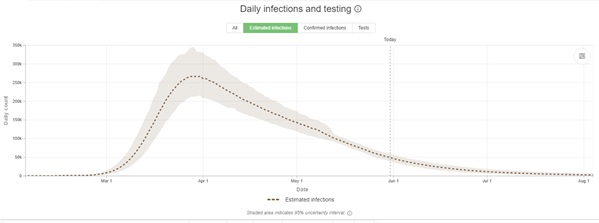

Estimated infections have been coming down as well, according to the Institute for Health Metrics and Evaluation (IMHE). IMHE estimates also show the number of daily infections has consistently been coming down over the last couple months.

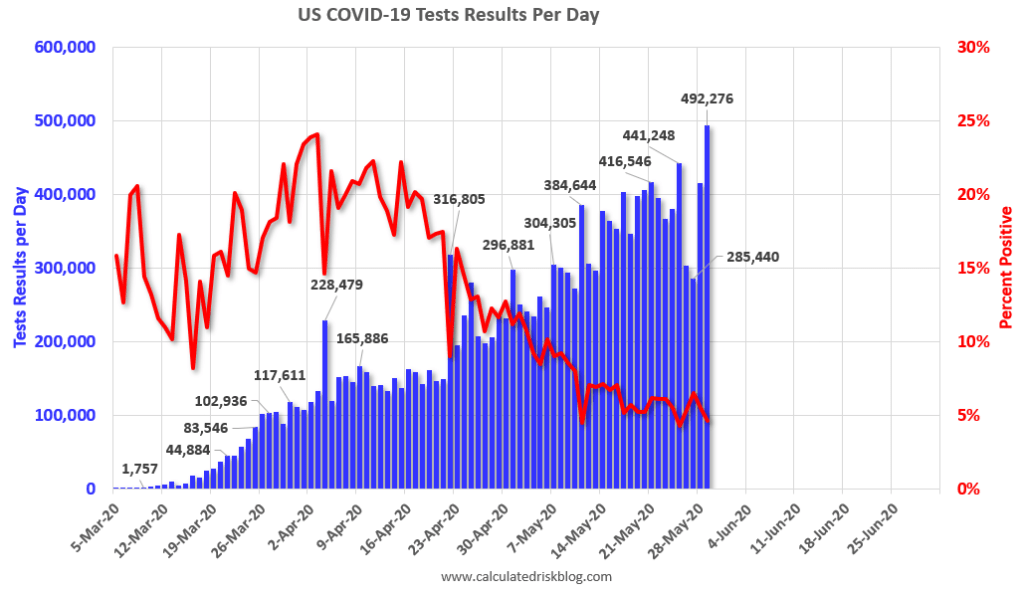

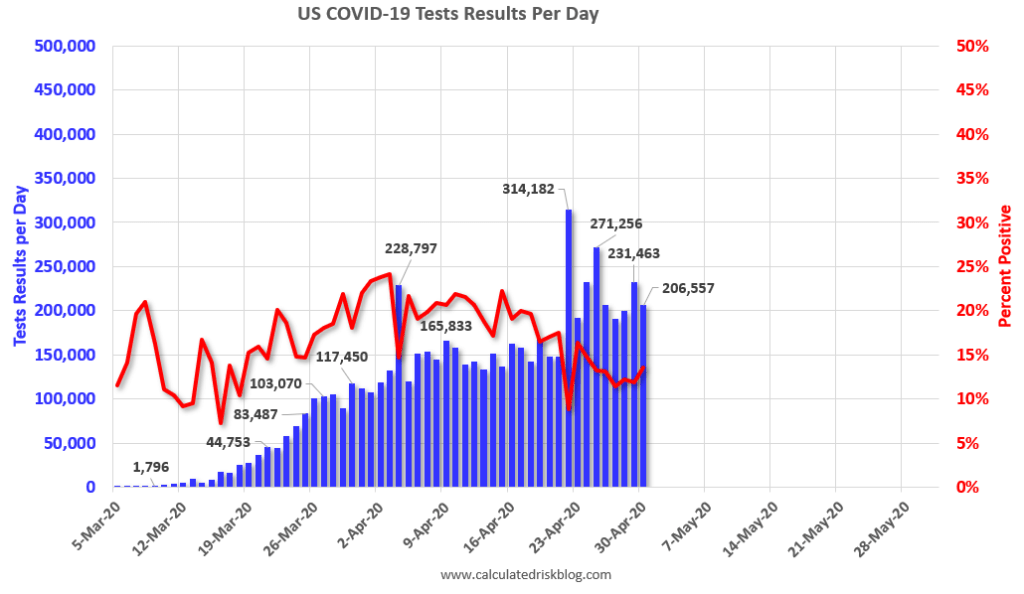

In addition to the stay-at-home orders and social distancing protocols, what has also contributed to the declines in COVID-19 deaths and infections? Two words…”increased testing.” Although, arguably COVID-19 testing got off to a rough start, as seen in the chart below, nevertheless daily tests have risen dramatically over the last couple months from about 100,000 per day to roughly 500,000 per day (see chart below). Increased testing capacity has and will continue to help better control the spread (or lack thereof) of the virus.

Not only has the spread of the coronavirus been substantially mitigated, but the fighting economy has also received an adrenaline shot in the form of trillions of dollars of fiscal and monetary support as I described in my previous article ( see also Recovering from the Coma).

Investors Need to Keep Guard Up

Like Rocky Balboa, the U.S. is a strong, respected fighter but even though strength is being regained, the economy and stock market is susceptible to a surprise upper-cut punch or hook. What could potentially hurt the financial comeback?

- Flare Ups & Second Wave: As cities, counties, and states carry on with expanded business openings, we could experience “flare ups” of COVID-19 infections or a “second wave.” But the good news is, we should be in much better shape to handle these scenarios thanks to expanded stockpiles of ventilators; larger supplies of PPE (Personal Protective Equipment) for frontline workers; increased production of therapeutic drugs like remdesivir from Gilead Sciences Inc. (GILD); and improved contact tracing from the magnified number of tests. And this analysis doesn’t even contemplate the more than 100 vaccines being developed (i.e., a potential cure) for COVID-19, which could be available in limited quantities as early as the end of this year.

- Social Unrest: The death of George Floyd, an African-American man who died after a Minneapolis police officer forcefully restrained George by keeping his knee on his neck, which triggered lethal complications to the victim. As a result, nationwide racial injustice protests and disruptive violence have erupted, thereby forcing government intervention with the hope of limiting violence and damage caused by non-peaceful protesters.

- Strained Relations with China Due to Actions in Hong Kong: Recent political actions mandated by the Chinese government to strip autonomy from Hong Kong has strained relations with the United States, and progress made with the previous U.S. – China trade deal could erode.

- Inflation: Despite no near-term evidence of rising prices, the unparalleled increase of trillions of dollars in fiscal debt and deficits has the credible long-term potential of creating incendiary inflation that could burn through consumers’ buying power.

Rocky Balboa faced many formidable foes in the boxing ring, including Clubber Lang (Mr. T) and Russian Ivan Drago, but Rocky survived and persevered. The stock market is bound to face future punches from unforeseen challengers in the form of impending known and unknown threats, but the alarmist calls for a COVID knockout appear to be overstated.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (June 1, 2020). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in GILD and certain exchange traded funds (ETFS), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

What the Heck & What Now?

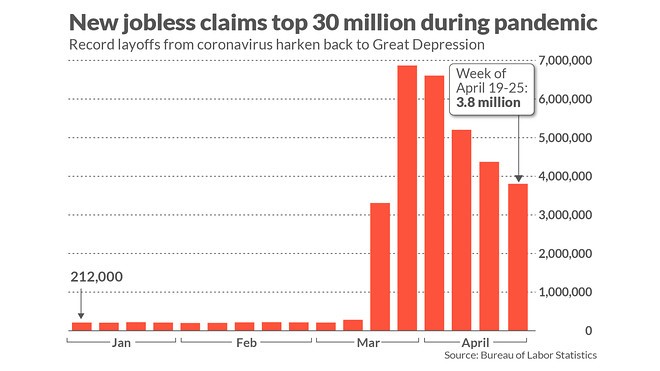

The Covid-19 viral pandemic that hit our shores in early 2020 shut down the economy to a virtual halt, and unemployment has skyrocketed to an estimated 19%, as 30 million people have now filed for unemployment benefits over the last six weeks (see chart below). Shockingly, we have not seen joblessness levels this high since the Great Depression. All this destruction has investors asking themselves, “What the heck, and what now?

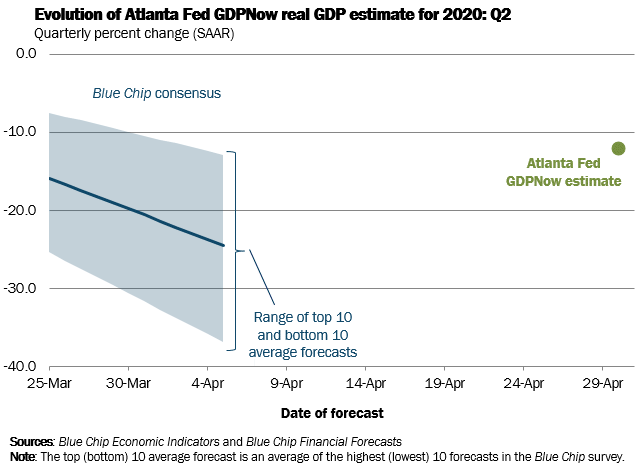

Forecasts for 2nd quarter economic activity (Gross Domestic Product) are estimating an unprecedented decline of -12% (see chart below) with some projections plummeting as low as -34%. Despite the dreadful freefall in the stock market during March, along with the pessimistic economic outlook, the major stock indexes came back with a vengeance during April. More specifically, the Dow Jones Industrial Average soared +2,428 points, or +11% for the month. The other major indexes, S&P 500 and NASDAQ, catapulted higher over the same period by +13% and +15%, respectively.

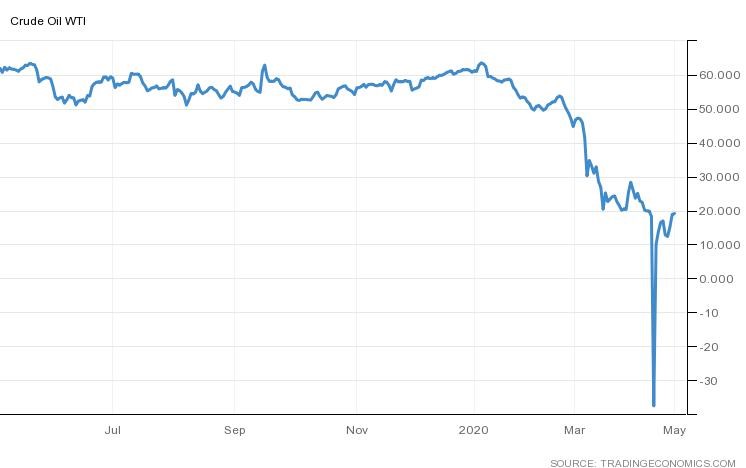

Certainly, there have been some industries hurt by Covid-19 more than others. At the top of the misery list are travel related industries such as airlines, cruise lines, and hotels. Retailers like Neiman Marcus, Pier 1, and JCPenney are filing for bankruptcy or on the verge of closing. Restaurants have also been pummeled (partially offset by the ability to offer pickup and delivery services), and entertainment industries such as sporting arenas, concert venues, movie theaters, and theme parks have all painfully come to a screeching halt as well. Let’s not forget energy and oil companies, which are battling for their survival life in an environment that has witnessed oil prices plunge from $61 per barrel at the beginning of the year to $19 per barrel today (with a brief period at negative -$37…yes negative!) – click here for an explanation and see the chart below.

What the Heck?!

With all this horrifying economic data financially crippling millions of businesses and families coupled with an epidemic that has resulted in a U.S. death count surpassing 60,000, how in the heck can the stock market be up approximately +34% from the epidemic lows experienced just five short weeks ago?

I was optimistic in my Investing Caffeine post last month, but here are some more specific explanations that have contributed to the recent significant rebound in the stock market.

- Virus Curve Flattening: The wave of Covid-19 started in China and crashed all over Europe before landing in the U.S. Fortunately, as you can see from the chart below (U.S. = red line), social distancing and stay-at-home orders have slowed the growth in coronavirus deaths.

- Fiscal Stimulus: The government fire trucks are coming to the rescue and looking to extinguish the Covid fire by spraying trillions of stimulus and aid dollars to individuals, businesses, and governments. Most recently, Congress passed a $484 billion bill in stimulus funding, including $320 billion in additional funding for the wildly popular Payroll Protection Program (PPP), which is designed to quickly get money in the hands of small businesses, so employers can retain employees rather than fire them. This half trillion program adds to the $2 trillion package Congress approved last month (see also Recovering from the Coma).

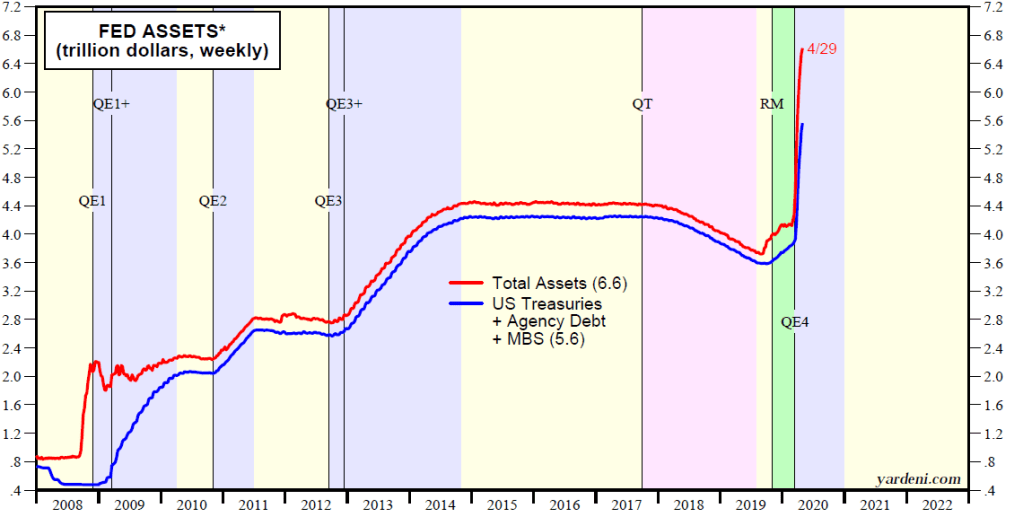

- Monetary Stimulus: The Federal Reserve has pulled out another monetary bazooka with the announcement of $2.3 trillion dollars in additional lending to small businesses . This action, coupled with the long menu of actions announced last month brings the total amount of stimulus dollars to well above $6 trillion (see also Recovering from the Coma for a list of Fed actions). You can see in the chart below how the Fed’s balance sheet has ballooned by approximately $3 trillion in recent months. The central bank is attempting to stimulate commerce by injecting dollars into the economy through financial asset purchases.

- Improving Healthcare System: Treatments for sick Covid patients has only gotten better, including new therapeutics like the drug remdesivir from Gilead Sciences Inc. (GILD). Dr. Anthony Fauci, the NIAID Director (National Institute of Allergy and Infectious Diseases) stated remdesivir “will be the standard of care.” With 76 vaccine candidates under development, there is also a strong probability researchers could discover a cure for Covid by 2021. With the help of the Defense Production Act (DPA), the government is also slowly relieving critical manufacturing bottlenecks in areas such as ventilators, PPE (Personal Protective Equipment) and Covid test kits. Making testing progress is crucial because this process is a vital component to reopening the economy (see chart below).

- Economy Reopening: After I have completed all of Netflix, participated in dozens of Zoom Happy Hours, and stocked up on a year’s supply of toilet paper, I have become a little stir crazy like many Americans who are itching to return to normalcy. The government is doing its part by attempting a three-phase reopening of the economy as you can see from the table below. You can’t fall off the floor, so a rebound is almost guaranteed as states slowly reopen in phases.

What Now?!

In the short run, it appears the worst is behind us. Why do I say that? Covid deaths are declining; Congress is spending trillions of dollars to support the economy; the Federal Reserve has effectively cut interest rates to 0% and provided trillions of dollars to provide the economy a backstop; our healthcare preparedness has improved; and global economies (including ours) are in the process of reopening. What’s not to like?!

However, it’s not all rainbows, flowers, and unicorns. We are in the middle of a severe recession with tens of millions unemployed. The Covid-19 epidemic has created a generation of germaphobes who will be hesitant to dive back into old routines. And until a vaccine is found, fears of a resurgence of the virus during the fall is a possibility, even if the masses and our healthcare system are much more prepared for that possibility.

As the world adjusts to a post-Covid 2.0 reality, I’m confident consumer spending will rebound, and pent-up demand will trigger a steady rise of economic demand. However, I am not whistling past the graveyard. I fully understand behavior and protocols will significantly change in a post-Covid 2.0 world, if not permanently, at least for a long period of time. Before the 9/11 terrorist attacks, nobody suspected air travelers would be required to remove shoes, take off belts, place laptops in bins, and carry tiny bottles of mouthwash and shampoo. Nevertheless, a much broader list of social distancing and safety codes of behaviors will be established, which could slow down the pace of the economic recovery.

Regardless of the recovery pace, over just a few short months, we have already placed our hands around the throat of the virus. There are bound to be future setbacks related to the pandemic. Physical and economic wounds will take time to heal. Turbulence will remain commonplace during these uncertain times, but volatility will create opportunities as the recovery continues to gain stronger footing. Although Covid-19 has produced significant damage, don’t let fear and panic infect your long-term investment future.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (May 1, 2020). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in GILD, Zoom, Netflix , and certain exchange traded funds (ETFS), but at the time of publishing had no direct position in Neiman Marcus, Pier 1, and JCPenney or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Recovering from the Coma

The patient, the U.S. economy, is sick and remains in a coma. Although the patient was never healthier six weeks ago, now the economy has fallen victim to a worldwide pandemic that has knocked the global economy on its back. On the surface, the physical impact of coronavirus on the health of the 330 million Americans seems relatively modest statistically (4,394 deaths vs. 45,000 estimated common flu deaths this season). However, in order to kill this insidious novel coronavirus, which has spread like wildfire across 200 countries, governments have been forced to induce the economy into a coma, by closing schools, halting sporting events, creating social distancing guidelines, instituting quarantines/lockdowns, and by shutting down large non-essential swaths of the economy (e.g., restaurants, retail, airlines, cruises, hotels, etc.). We have faced and survived other epidemics like SARS (2003-04), H1N1 (2009-10), MERS (2012), and Ebola (2014-16), but the pace of COVID-19 spreading has been extraordinarily rapid and has created dramatic resource drains on healthcare systems around the world (including New York with approximately 75,000 cases alone). The need for test kits, personal protective equipment, and ventilators, among other demands has hit the U.S. caregiving system especially hard.

Given the unique characteristics of this sweeping virus, U.S. investors were not immune from the economic impact. The swift unprecedented downdraft from all-time record highs has not been seen since the October 1987 crash. And although the major indexes experienced an illness this month (Dow Jones Industrial Average -13.7%; S&P 500 -12.5%; NASDAQ -10.1%), the nausea was limited in large part thanks to trillions of dollars in unparalleled government intervention announced in the form of monetary and fiscal stimulus.

Healing the Patient

While the proliferation of the viral outbreak has been painful in many ways from a human and financial perspective, the beneficial impact of the medicine provided to the economic patient by the Federal Reserve and federal government through the Coronavirus Aid, Relief, and Economic Security (CARES) act cannot be overstated. The measures taken will provide a temporary safety net for not only millions of businesses, but also millions of workers and investors. Although last month many investors felt like vomiting when they looked at their investment account balances, gratefully the period ended on an upbeat note with the Dow bouncing +20% from last week’s lows.

Fed Financial Fixes

Here is a partial summary of the extensive multi-trillion dollar emergency measures taken by the Federal Reserve to keep the financial markets and economy afloat:

- Cut interest rates on the benchmark Federal Funds target to 0% – 0.25% from 1% – 1.25%.

- Make $1 trillion available in 14-day loans it is offering every week.

- Make $1 trillion of overnight loans a day available.

- Purchase an unlimited amount of Treasury securities after initially committing to $500 billion.

- Purchase an unlimited amount of mortgage-backed securities after initially committing to at least $200 billion.

- Provide $300 billion of financing to employers, consumers, and businesses. The Department of the Treasury will provide $30 billion in equity to this financing via the Exchange Stabilization Fund (ESF).

- Establish two lending facilities to support credit to large employers – the Primary Market Corporate Credit Facility (PMCCF) for new bond and loan issuance and the Secondary Market Corporate Credit Facility (SMCCF) to provide liquidity for outstanding corporate bonds.

- Create the Term Asset-Backed Securities Loan Facility (TALF), to support the flow of credit to consumers and businesses, including student loans, auto loans, credit card loans, loans guaranteed by the Small Business Administration (SBA).

- Expand the Money Market Mutual Fund Liquidity Facility (MMLF) and the Commercial Paper Funding Facility (CPFF) to include a wider range of securities.

Corona CARE to Country

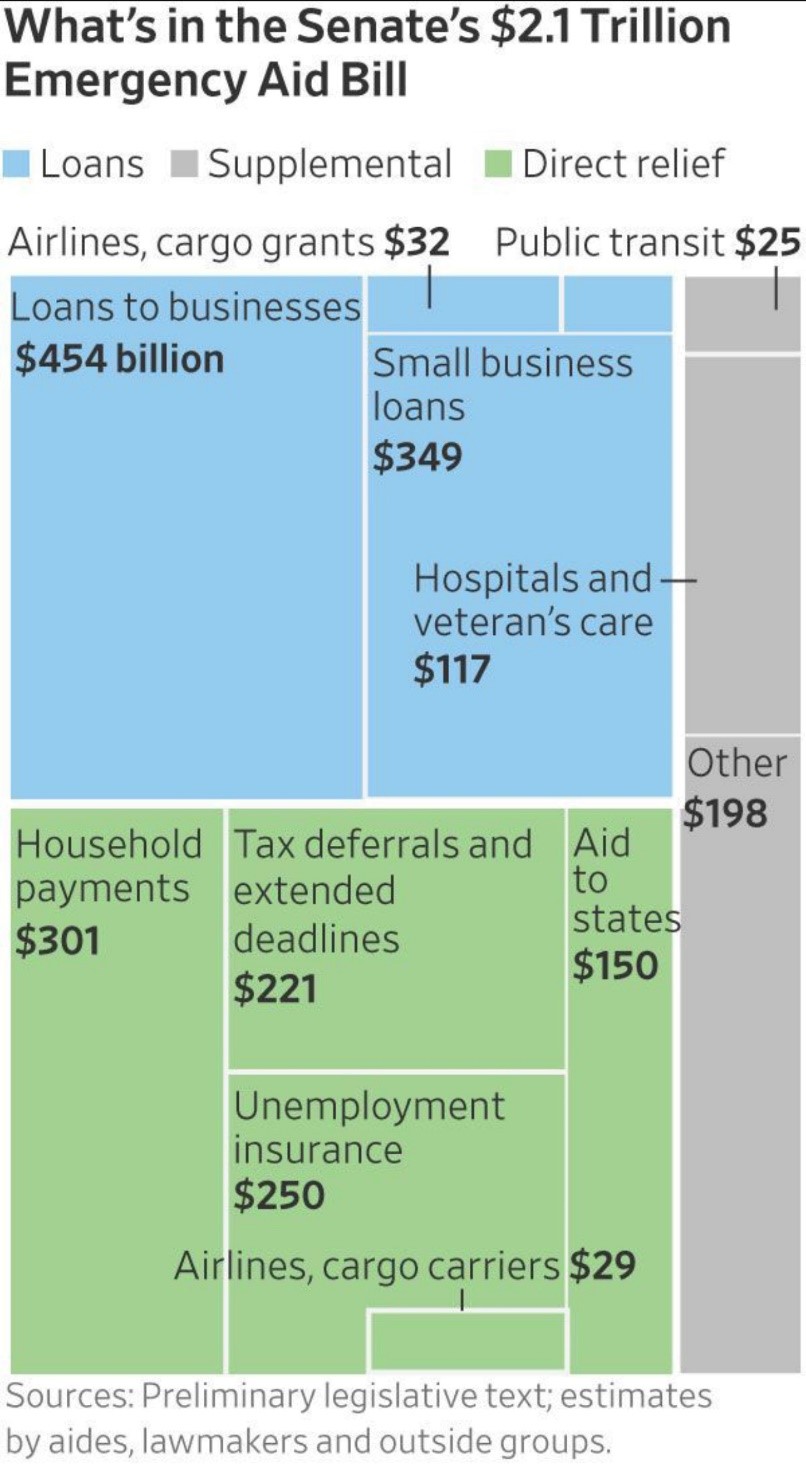

Here is a limited summary of the sprawling $2.1 trillion bipartisan stimulus legislation that was recently passed by Congress (see summary and table below):

- Direct Payments: Americans who pay taxes will receive a one-time direct deposit of up to $1,200, and married couples will receive $2,400, plus an additional $500 per child. The payments will be available for incomes up to $75,000 for individuals and $150,000 for married couples, and phase out completely at $99,000 and $198,000, respectively.

- Unemployment: The program provides $250 billion for an extended unemployment insurance program and expands eligibility and offers workers an additional $600 per week for four months, on top of what state programs pay. It also extends UI benefits through Dec. 31 for eligible workers. The deal also applies to the self-employed, independent contractors and gig economy workers.

- Payroll Taxes: The measure allows employers to delay the payment of their portion of 2020 payroll taxes until 2021 and 2022.

- Use of Retirement Funds: The bill waives the 10% early withdrawal penalty for distributions up to $100,000 for coronavirus-related purposes, retroactive to Jan. 1. Withdrawals are still taxed, but taxes are spread over three years, or the taxpayer has the three-year period to roll it back in.

- Small Business Relief: $350 billion is being earmarked to preventing layoffs and business closures while workers need to stay home during the outbreak. Companies with 500 employees or fewer that maintain their payroll during coronavirus can receive up to 8 weeks of financial assistance. If employers maintain payroll, the portion of the loans used for covered payroll costs, interest on mortgage obligations, rent, and utilities would be forgiven.

- Large Corporations: $500 billion will be allotted to provide loans, loan guarantees, and other investments, these will be overseen by a Treasury Department inspector general. These loans will not exceed five years and cannot be forgiven. Airlines will receive $50 billion (of the $500 billion) for passenger air carriers, and $8 billion for cargo air carriers.

- Hospitals and Health Care: The deal provides over $140 billion in appropriations to support the U.S. health system, $100 billion of which will be injected directly into hospitals. The rest will be dedicated to providing personal and protective equipment for health care workers, testing supplies, increased workforce and training, accelerated Medicare payments, and supporting the CDC, among other health investments.

- Coronavirus Testing: All testing and potential vaccines for COVID-19 will be covered at no cost to patients.

- States and Local Governments: State, local and tribal governments will receive $150 billion. $30 billion is set aside for states, and educational institutions. $45 billion is for disaster relief, and $25 billion for transit programs.

- Agriculture: The deal would increase the amount the Agriculture Department can spend on its bailout program from $30 billion to $50 billion.

Source: The Wall Street Journal

Patient Requires Patience

As we enter the new 30-day extension of social distancing guidelines until April 30th, there is good news and bad news for the patient as the economy recovers from its self-induced coma. On the good news front, their appears to be a light at the end of the tunnel with respect to the spread of the virus. Enough data has been collected from countries like China, S. Korea, Italy, and our own, such that statisticians appear to have a better handle on the trajectory of the virus.

More specifically, here are some positive developments:

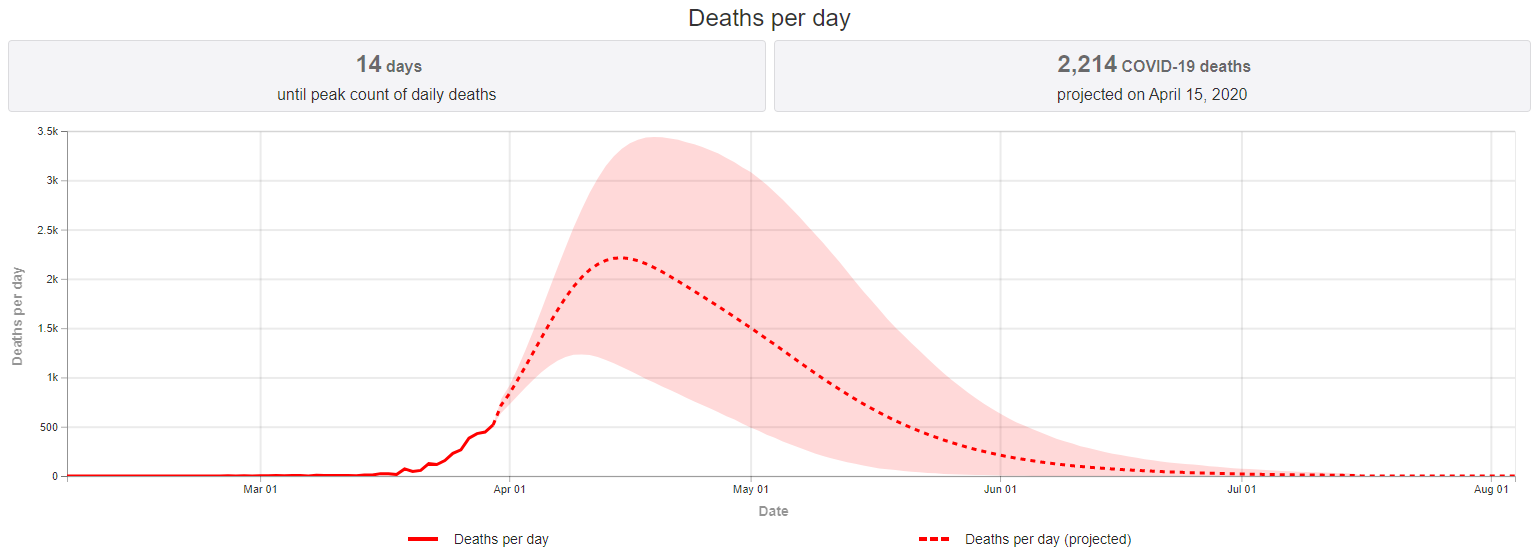

- Peak Seen on April 14th: According to the IMHE model that the White House is closely following, the number of COVID-19 deaths is projected to peak in two weeks.

Source: IHME

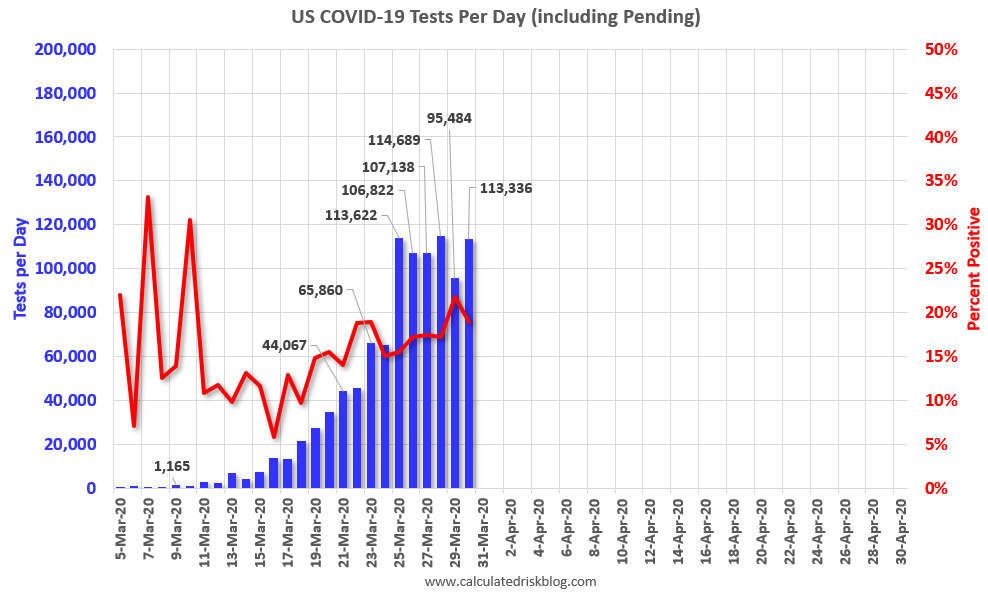

- Testing Ramping: The United States definitely got off to a slow start in the virus testing department, but as you can see from the chart below, COVID-19 tests are ramping significantly. Nevertheless, the number of tests still needs to increase dramatically until the percent of “positive” test results declines to a level of 5% or lower, based on data collected from South Korea. In another promising development, Abbott Laboratories (ABT) received emergency approval from the FDA for a rapid point-of-care test that produces results in just five minutes.

Source: Calculated Risk

- Closer to a COVID Cure: There are no Food and Drug Administration (FDA)-approved therapies or vaccines yet, but the FDA has granted emergency use authorization to anti-malarial drugs chloroquine phosphate and hydroxychloroquine sulfate to treat coronavirus patients. Patients are currently using these drugs in conjunction with the antibiotic azithromycin in hopes of achieving even better results. Remdesivir is a promising anti-viral treatment (also used in treating the Ebola virus) manufactured by Gilead Sciences Inc. (GILD), which is in Phase 3 clinical trial testing of the drug. If proven effective, broad distribution of remdesivir could be administered to COVID-19 patients in the not-too-distant future. Another company, Regeneron Pharmaceuticals (REGN), is working on clinical trials of its rheumatoid arthritis antibody drug Kevzara as a hopeful treatment. In addition, there are multiple companies, including Moderna Inc. (MRNA) and Johnson & Johnson (JNJ) that are making progress on coronavirus vaccines, that could have limited availability as soon as early-2021.

Darkest Before the Dawn

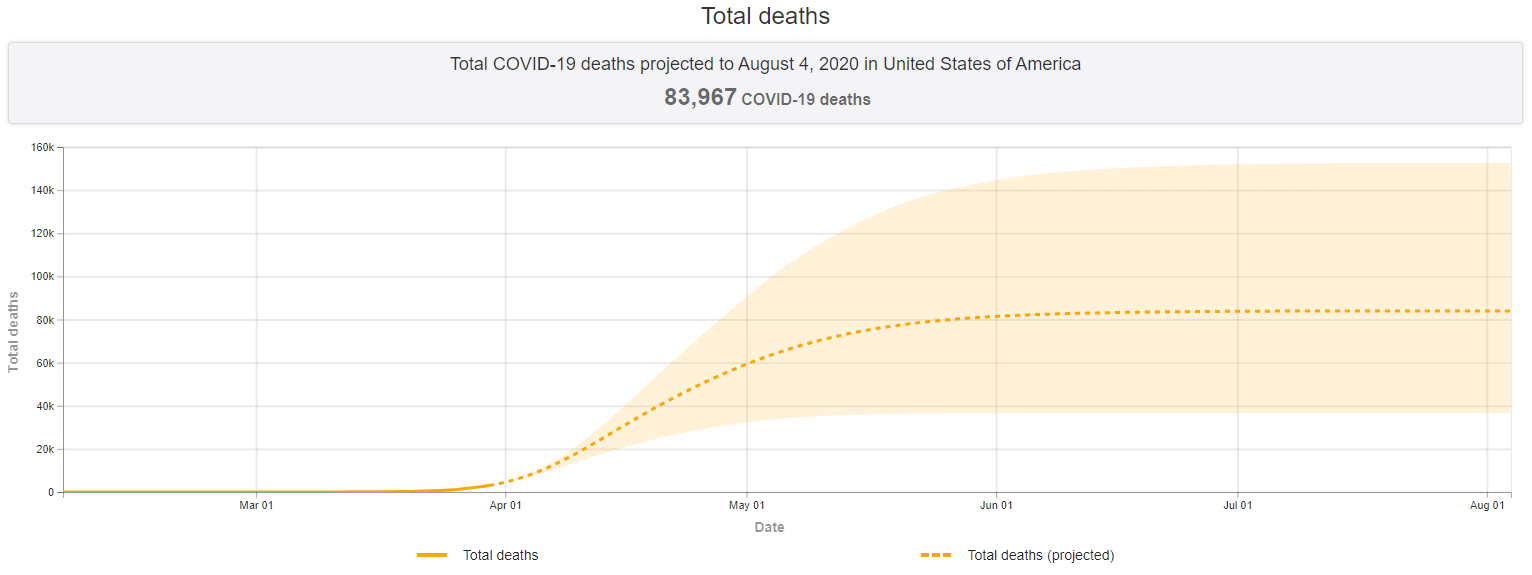

It is always darkest before the dawn, and the same principle applies to this coronavirus epidemic. Despite providing the patient’s medicine in the form of monetary and fiscal stimulus, time and patience is necessary for the prescription to take effect. As you can see from the chart below, the median total deaths projected is expected to rise to over 80,000 deaths by June 1st from roughly 4,000 today.

Source: IHME

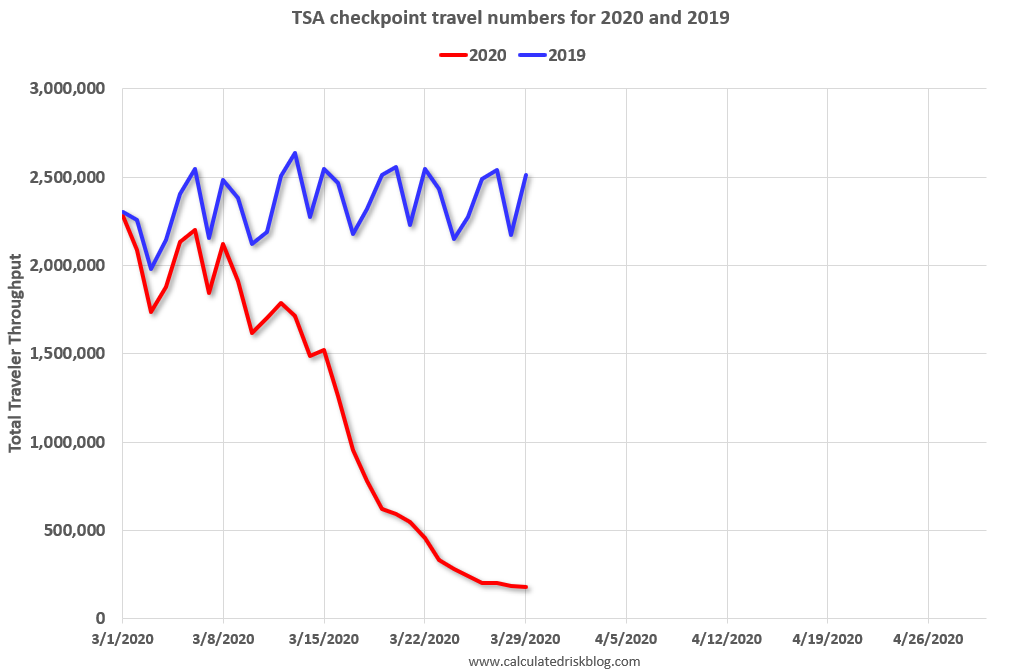

The physical toll will exceedingly become difficult over the next month, and the same can be said economically, especially for the hardest hit industries such as leisure, hospitality, and transportation. Just take a look at the -93% decline in airport travel versus a year ago (see chart below).

Source: Calculated Risk

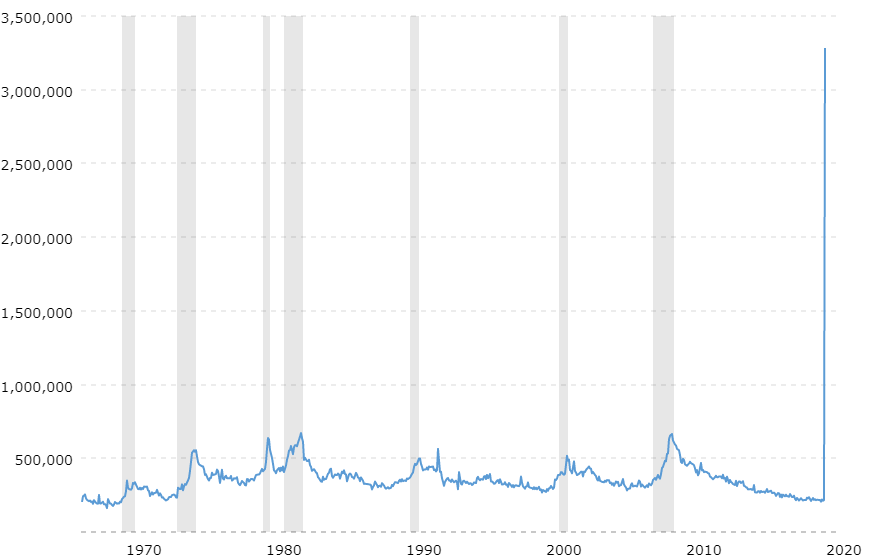

The closure of restaurants, retail stores, and hotels, coupled with a cratering of travel has resulted in a more than a 1,000% increase in Americans filing for unemployment payments (see chart below – gray shaded regions correspond to recessions), and the unemployment rate is expected to increase from a near record-low 3.5% unemployment to a staggering 10% – 30% unemployment rate.

Source: Macrotrends

The spread of the incredibly debilitating COVID-19 virus has placed the economic patient into a self-induced coma. The financial and physical pain felt by the epidemic will worsen in the coming weeks, but fortunately the monetary stimulus, fiscal emergency relief, and social distancing guidelines are pointing to a predictable recovery in the not-too-distant future. Financial markets have survived wars, assassinations, recessions, impeachments, banking crises, currency crises, housing collapses, and yes, even pandemics. Each and every time, we have emerged stronger than ever…and I’m confident we will achieve the same result once COVID-19 is defeated.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (April 1, 2020). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in GILD, MRNA, JNJ, and certain exchange traded funds (ETFS), but at the time of publishing had no direct position in ABT, REGN or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Missing the Financial Forest for the Political Trees

In the never-ending, 24/7, polarizing political news cycle, headlines of Ukraine phone calls, China trade negotiations, impeachment hearings, presidential elections, Federal Reserve monetary policy, and other Washington based stories have traders and news junkies glued to their phones, Twitter feeds, news accounts, blog subscriptions, and Facebook stories. However, through the incessant, deafening noise, many investors are missing the overall financial forest as they get lost in the irrelevant D.C. details.

Meanwhile, as many investors fall prey to the mesmerizing, but inconsequential headlines, financial markets have not fallen asleep or gotten distracted. The S&P 500 stock market index rose another +1.7% last month, and for the year, the index has registered a +18.7% return. As we enter the volatile fourth quarter, many stock market participants remain shell-shocked from last year’s roughly -20% temporary collapse, even though the S&P 500 subsequently rallied +29% from the 2018 trough to the 2019 peak.

Why are many people missing the financial forest? A big key to the significant rally in 2019 stock prices can be attributed to two words…interest rates. Unlike last year’s fourth quarter, when the Federal Reserve was increasing interest rates (i.e., tapping the economic brakes), this year the Fed is cutting rates (i.e., hitting the economic accelerator). Interest rates are a key leg to Sidoxia’s financial four-legged stool (see Don’t Be a Fool, Follow the Stool). Interest rates are at or near generational lows, depending where on the geographic map you reside. For example, interest rates on 10-year German government bonds are -0.55%. Yes, it’s true. If you were to invest $10,000 in a negative yielding -0.55% German bond for 10-years starting in 2019, if you held the bond until maturity (2029), the investor would get back less than the original $10,000 invested. In other words, many bond investors are choosing to pay bond issuers for the privilege of giving the issuers money for the unpalatable right of receiving less money in the future.

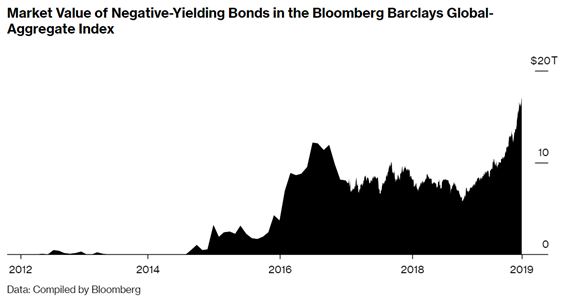

The unprecedented negative-yielding bond market is reaching epic proportions, having eclipsed $17 trillion globally (see chart below). This gargantuan and growing dollar figure of negative-yielding bonds defies common sense and feels very reminiscent of the panic buying of technology stocks in the late 1990s.

Source: Bloomberg

At Sidoxia Capital Management, we are implementing proprietary fixed income strategies to navigate this negative interest rate environment. However, the plummeting interest rates and skyrocketing bond prices only make our bond investing job tougher. On the other hand, declining rates, all else equal, also make my stock-picking job easier. Nevertheless, many market participants have gotten lost in the financial trees. More specifically, investors are losing sight of the key tenet that money goes where it is treated best (go where yields are highest and valuations lowest). With many bonds yielding low or negative interest rates, bond investors are being treated like criminals forced to serve jail time and pay large fines because future returns will become much tougher to accrue. In my Investing Caffeine blog, I have been writing about how the stock market’s earnings yield (current approximating +5.5%) and the S&P dividend yield of about +1.9% are handily outstripping the +1.7% yield on the 10-Year Treasury Note (see Going Shopping: Chicken vs. Beef ).

Unless our economy falls into a prolonged recession, interest rates spike substantially higher, or stock prices catapult appreciably, then any decline in stock prices will likely be temporary. Fortunately, the economy appears to be chugging along, albeit at a slower rate. For instance, 3rd quarter GDP (Gross Domestic Product) estimates are hovering around +2.0%.

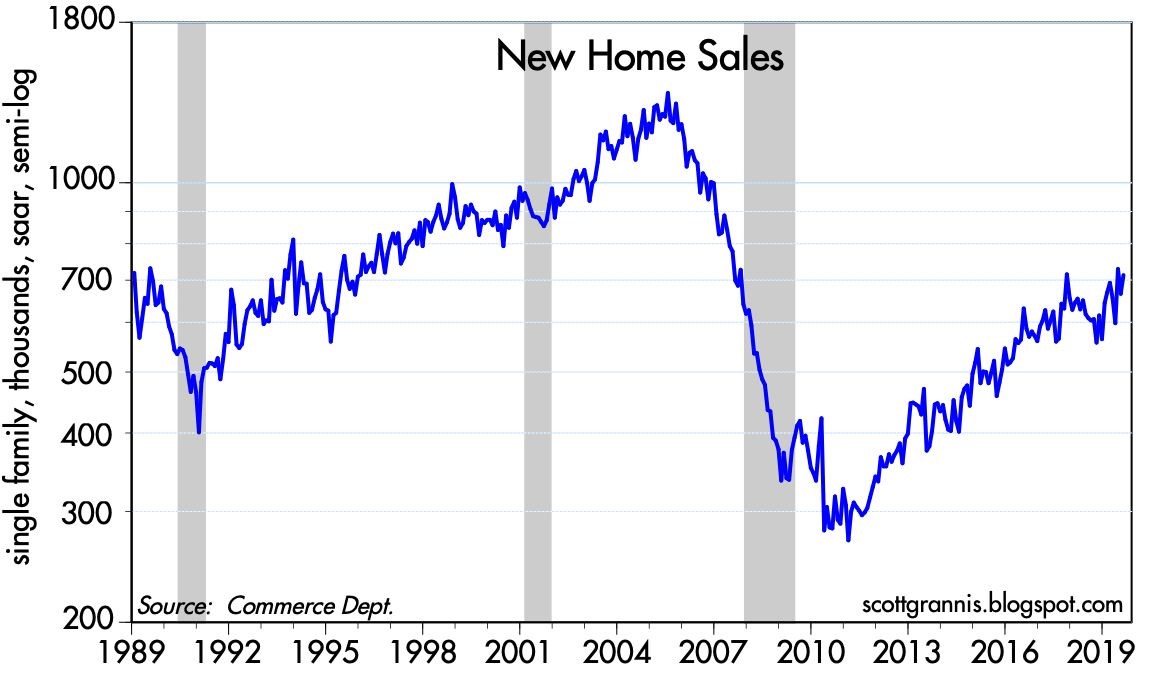

Low Rates Aid Housing Market

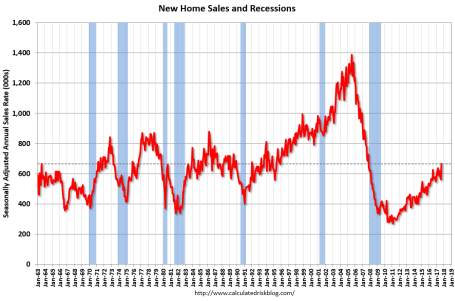

Thanks to low interest rates, the housing markets remain strong. As you can see from the chart below, new home sales continue to ratchet higher over the last eight years, and lower mortgage rates are only helping this cause.

Source: Calafia Beach Pundit

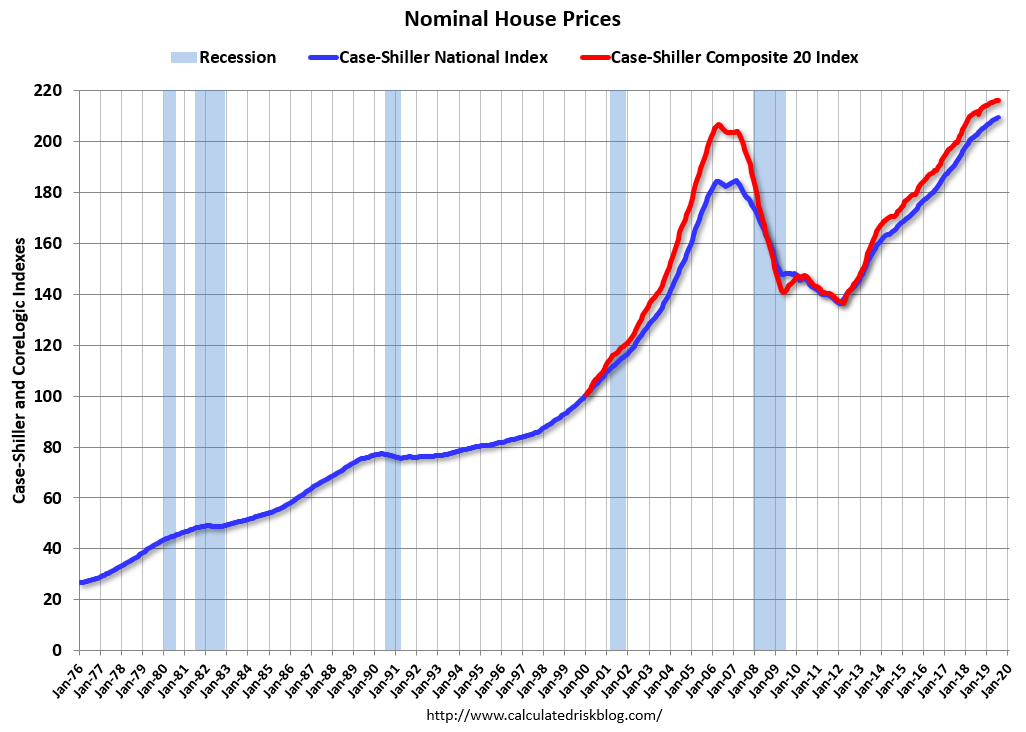

The same tailwind of lower interest rates can be seen below with rising home prices.

Source: Calculated Risk

Consumer Flexes Muscles

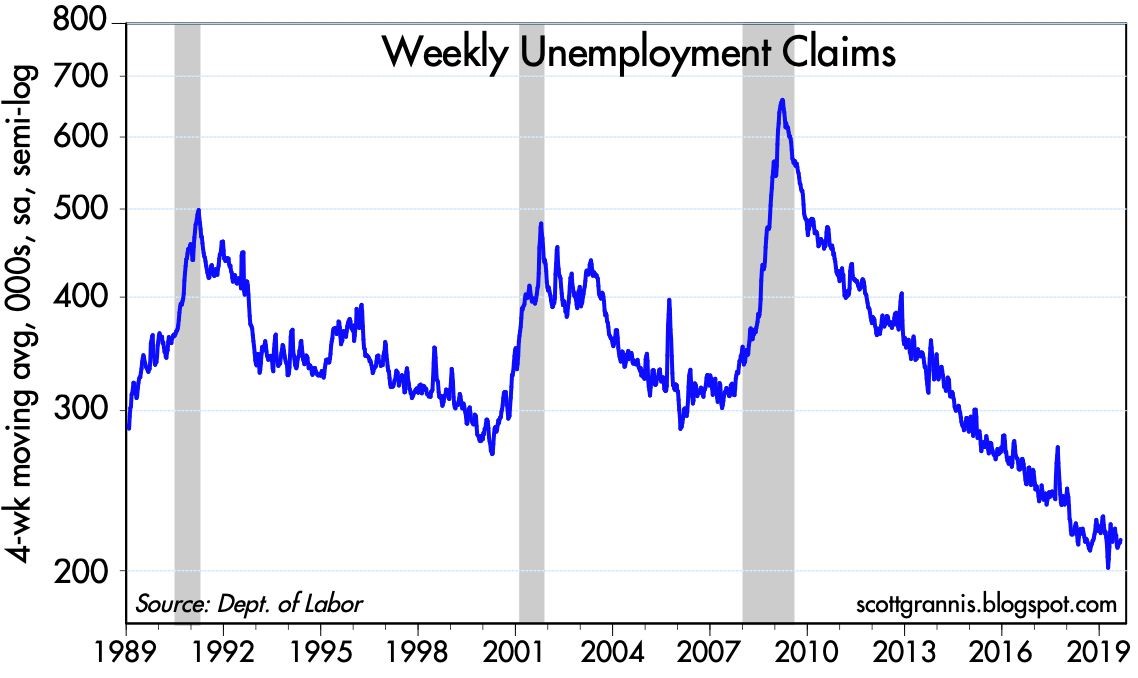

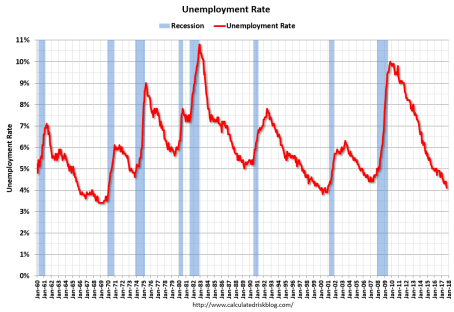

At 3.7%, the unemployment rate remains low and the number of workers collecting unemployment is near multi-decade lows (see chart below).

Source: Calafia Beach Pundit

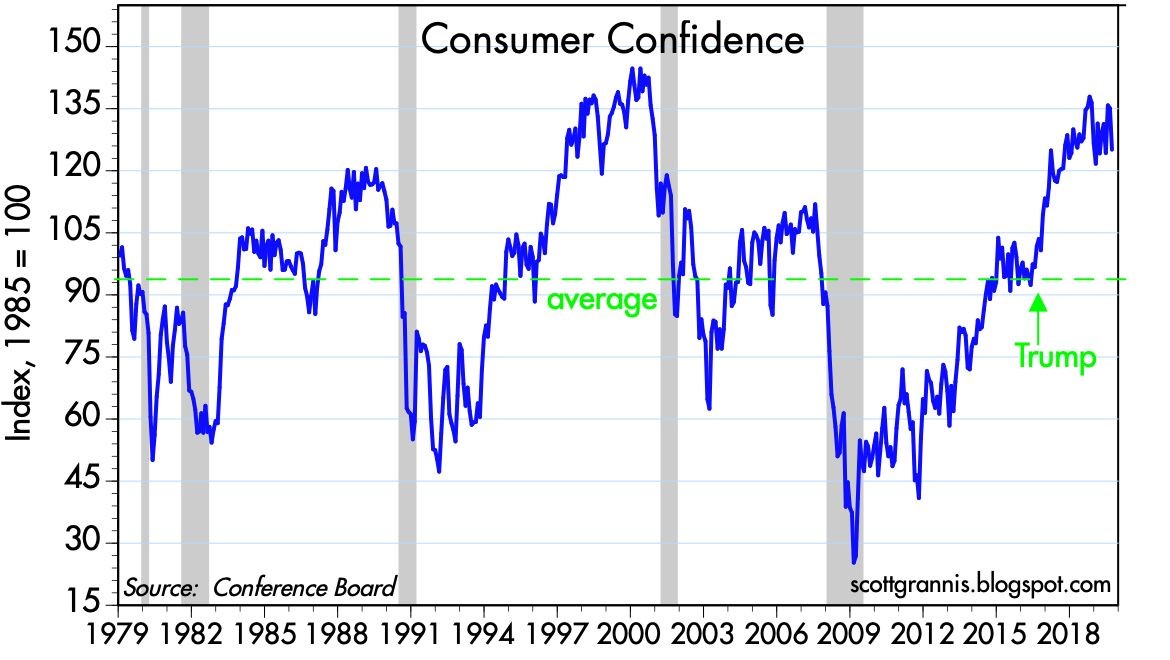

It should come as no surprise that the more employed workers there are collecting paychecks, the more consumer confidence will rise (see chart below). As you can see, consumer confidence is near multi-decade record highs.

Source: Calafia Beach Pundit

Although politics continue to dominate headlines and grab attention, many investors are missing the financial forest because the political noise is distracting the irrefutable, positive effect that low interest rates is contributing to the positive direction of the stock market and the economy. Do your best to not miss the forest – you don’t want your portfolio to suffer by you getting lost in the trees.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (October 1, 2019). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Will Santa Leave a Lump of Coal?

As we enter the last month of the year, the holiday season is kicking into full gear, decorations are popping up everywhere, and the burning question arises, “Will Santa Claus bring gifts for stock market investors, or will he leave a lump of coal in their stockings?”

It was a bumpy sleigh ride last month, but we ultimately entered December in a festive mood with joyful monthly gains of +1.7% in the Dow Jones Industrial Average, and +1.8% in the S&P 500. There have been some naughty and nice factors leading to some turbulent but modest gains in 2018. For the first 11 months of the year, the Dow has rejoiced with a +3.3% advance, and the S&P 500 has celebrated a rise of +3.2% – and these results exclude additional dividends of approximately 2%.

Despite the monthly gains, not everything has been sugar plums. President Trump has been repeatedly sparring with the Federal Reserve Chairman, Jerome Powell, treating him more like the Grinch due to his stingy interest rate increases than Santa. As stockholders have contemplated the future path of interest rates, the major stock indexes temporarily slipped into negative territory for the year, until Mr. Powell gave stock and bond investors an early Christmas present last week by signaling interest rates are “just below” the nebulous neutral target. The dovish comment implied we are closer to the end of the economy-slowing rate-hike cycle than we are to the beginning.

Trade has also contributed to the recent spike in stock market volatility, despite the fresh establishment of the trade agreement reached between the U.S., Mexico, and Canada (USMCA – U.S.-Mexico-Canada Agreement), a.k.a., NAFTA 2.0. Despite the positive progress with our Mexican and Canadian neighbors, uncertainty surrounding our country’s trade relations with China has been challenging due to multiple factors including, Chinese theft of American intellectual property, cyber-attacks, forced technology transfer, agricultural trade, and other crucial issues. Fortunately, optimism for a substantive agreement between the world’s two super-powers advanced this weekend at the summit of the Group of 20 nations in Argentina, when a truce was reached to delay an additional $200 billion in tariffs for 90 days, while the two countries further negotiate in an attempt to finalize a comprehensive trade pact.

Source: Financial Times

Economic Tailwinds

Besides positive developments on the interest rate and trade fronts, the economy has benefited from tailwinds in some other important areas, such as the following:

Low Unemployment: The economy keeps adding jobs at a healthy clip with the unemployment rate reaching a 48-year low of 3.7%.

Source: Calculated Risk

Rising Consumer Confidence: Although there was a slight downtick in the November Consumer Confidence reading, you can see the rising long-term, 10-year trend has been on a clear upward trajectory.

Source: Chad Moutray

Solid Economic Growth: As the chart below indicates, the last two quarters of economic growth, measured by GDP (Gross Domestic Product), have been running at multi-year highs. Forecasts for the 4th quarter currently stand at a respectable mid-2% range.

Source: BEA

Uncertain Weather Forecast

Although the majority of economic data may have observers presently singing “Joy to the World,” the uncertain political weather forecast could require Rudolph’s red-nose assistance to navigate the foggy climate. The mid-term elections have created a split Congress with the Republicans holding a majority in the Senate, and the Democrats gaining control of the House of Representatives. As we learned in the last presidential term, gridlock is not necessarily a bad thing (see also, Who Said Gridlock is Bad?). For instance, a lack of government control can place more power in the hands of the private sector. Political ambiguity also surrounds the timing and outcome of Robert Mueller’s Special Counsel investigation into potential Russian interference and collusion, however as I have continually reminded followers, there are more important factors than politics as it relates to the performance of the stock market (see also, Markets Fly as Media Noise Goes By).

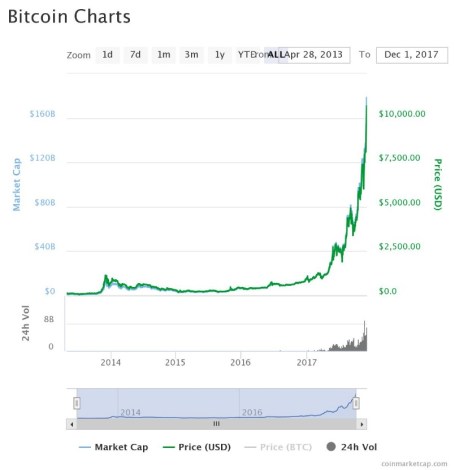

From an economic standpoint, some speculative areas have been pricked – for example the decline in FAANG stocks or the burst of the Bitcoin bubble as the price has declined from roughly $19,000 from its peak to roughly $4000 today (see chart below).

Source: Coindesk

On the housing front, unit sales of new and existing homes have not been immune to the rising interest rate policies of the Federal Reserve. Nevertheless, as you can witness below, housing prices remain at all-time record high prices, according to the recent Case-Shiller data.

Source: Calculated Risk

I like to point out to my investors there is never a shortage of things to worry about. Even when the economy is Jingle Bell Rocking, the issues of inflation and Fed policy inevitably begin to creep into investor psyches. While prognosticators and talking heads will continue trying to forecast whether Santa Claus will place presents or coal into investors’ stockings this season, at Sidoxia we understand predictions are a fool’s errand. Regardless of Santa’s generosity (or lack thereof), we continue to find attractive opportunities for our investors, as we look to balance the risk and rewards presented to us during both stable and volatile periods.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (December 3, 2018). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Arm Wrestling the Economy & Tariffs

Financial markets have been battling back and forth like a championship arm-wrestling match as economic and political forces continue to collide. Despite these clashing dynamics, capitalism won the arm wrestling match this month as investors saw the winning results of the Dow Jones Industrial Average adding +4.7% and the S&P 500 index advancing +3.6%.

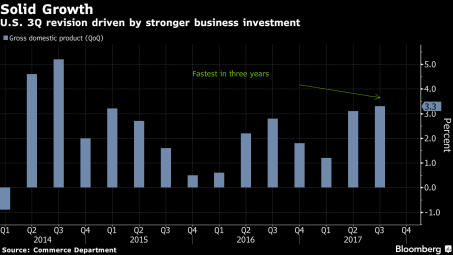

Fueling the strength this month was U.S. economic activity, which registered robust 2nd quarter growth of +4.1% – the highest rate of growth achieved in four years (see below).

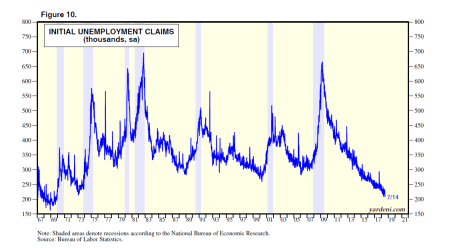

The job market is on fire too with U.S. jobless claims hitting their lowest level in 48 years (see chart below). This chart shows the lowest number of people in a generation are waiting in line to collect unemployment checks.

Source: Dr. Ed’s Blog

If that isn’t enough, so far, the record corporate profits being reported for Q2 are up a jaw-dropping +23.5% from a year ago. What can possibly be wrong?

Excess Supply of Concern

While the economic backdrop is largely positive, there is never a shortage of things to worry about – even during decade-long bull market of appreciation. More specifically, investors have witnessed the S&P 500 index more than quadruple from a March 2009 low of 666 to 2,816 today (+322%). Despite the massive gains achieved over the last decade, there have been plenty of volatility and geopolitics to worry about. Have you already forgotten about the Flash Crash, Arab Spring, Occupy Wall Street, Government Shutdowns, Sequestration, Taper Tantrum, Ebola, Iranian nuclear threat, plunging oil prices, skyrocketing oil prices, Brexit, China scares, Elections, and now tariffs, trade, and the Federal Reserve monetary policy?

Today, tariffs, trade, Federal Reserve monetary policy, and inflation are top-of-mind investor concerns, but history insures there will be new issues to worry about tomorrow. Ever since the bull market began a decade ago, there have been numerous perma-bears incorrectly calling for a deathly market collapse, and I have written a substantial amount about these prognosticators’ foggy crystal balls (see Emperor Schiff Has No Clothes [2009] & Clashing Views with Dr. Roubin [2009]. While these doomsdayers get a lot less attention today, similar bears like John Hussman, who like a broken record, has erroneously called for a market crash every year for the last seven years (click chart link).

Although many investment accounts are up over the last 10 years, many people quickly forget it has not been all rainbows and unicorns. While the stock market has more than quadrupled in value since 2009, we have lived through about a dozen alarming corrections, including the worrisome -12% pullback we experienced in February. If we encounter another -5 -10% correction this year, this is perfectly healthy, normal, and should not be surprising. More often than not, these temporary drops provide opportunistic openings to scoop up valued bargains.

Longtime readers and followers of Sidoxia’s investment philosophy and Investing Caffeine understand the majority of these economic predictions and political headlines are useless noise. Social media, addiction to smart phones, and the 24/7 news cycle create imaginary, scary mountains out of harmless molehills. As I have preached for years, the stock market does not care about politics and opinions – the stock market cares about 1) corporate profits (at record levels) – see chart below; 2) interest rates (rising, but still near historically low levels); 3) the price of the stock market/valuation (which is getting cheaper as profits soar from tax cuts); and 4) sentiment (a favorable contrarian indicator until euphoria kicks in).

Source: Dr. Ed’s Blog

Famed investor manager, Peter Lynch, who earned +29% annually from 1977-1990 also urged investors to ignore attempts of predicting the direction of the economy. Lynch stated, “I’ve always said if you spend 13 minutes a year on economics, you’ve wasted 10 minutes.”

I pay more attention to successful long-term investors, like Warren Buffett (the greatest investor of all-time), who remains optimistic about the stock market. As I’ve noted before, although we remain constructive on the markets over the intermediate to long-term periods, nobody has been able to consistently prophesize about the short-term direction of financial markets.

At Sidoxia, rather than hopelessly try to predict every twist and turn in the market, or react to every meaningless molehill, we objectively analyze the available data without getting emotional, and then take advantage of the opportunities presented to us in the marketplace. Certain asset classes, stocks, and bonds, will constantly move in and out of favor, which allows us to continually find new opportunities. A contentious arm wrestling struggle between uncertain tariffs/rising interest rates and stimulative tax cuts/strong economy is presently transpiring. As always, we will continually monitor the evolving data, but for the time being, the economy is flexing its muscle and winning the battle.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (August 1, 2018). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

‘Tis the Season for Giving

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (December 1, 2017). Subscribe on the right side of the page for the complete text.

Holiday season is in full swing, and that means it’s the primetime period for giving. The stock market has provided its fair share of giving to investors in the form of a +2.7% monthly return in the S&P 500 index (up +18% in 2017). For long-term investors, stocks have been the gift that keeps on giving. As we approach the 10-year anniversary of the 2008 Financial Crisis, stocks have returned +68% from the October 2007 peak and roughly +297% from the March 2009 low. If you include the contributions of dividends over the last decade, these numbers look even more charitable.

Compared to stocks, however, bonds have acted more like a stingy Ebenezer Scrooge than a generous Mother Theresa. For the year, the iShares Core Aggregate bond ETF (AGG) has returned a meager +1%, excluding dividends. Contributing to the lackluster bond results has been the Federal Reserve’s miserly monetary policy, which will soon be managed under new leadership. In fact, earlier this week, Jerome Powell began Congressional confirmation hearings as part of the process to replace the current Fed chair, Janet Yellen. As the Dow Jones Industrial Average rose for the 8th consecutive month to 24,272 (the longest winning streak for the stock index in 20 years), investors managed to take comfort in Powell’s commentary because he communicated a steady continuation of Yellen’s plan to slowly reverse stimulative policies (i.e., raise interest rate targets and bleed off assets from the Fed’s balance sheet).

Because the pace of the Federal Funds interest rate hikes have occurred glacially from unprecedented low levels (0%), the resulting change in bond prices has been relatively meager thus far in 2017. In that same deliberate vein, the Fed is meeting in just a few weeks, with the expectation of inching the Federal Funds rate higher by 0.25% to a target level of 1.5%. If confirmed, Powell plans to also chip away at the Fed’s gigantic $4.5 trillion balance sheet over time, which will slowly suck asset-supporting liquidity out of financial markets.

Economy Driving Stocks and Interest Rates Higher

Presents don’t grow on trees and stock prices also don’t generally grow without some fundamental underpinnings. With the holidays here, consumers need money to fulfill the demanding requests of gift-receiving individuals, and a healthy economy is the perfect prescription to cure consumers’ empty wallet and purse sickness.

Besides the Federal Reserve signaling strength by increasing interest rates, how do we know the economy is on firm footing? While economic growth may not be expanding at a barn-burning rate, there still are plenty of indications the economy keeps chugging along. Here are a few economic bright spots to highlight:

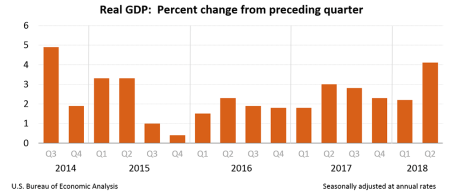

- Accelerating GDP Growth: As you can see from the chart below, broad economic growth, as measured by Gross Domestic Product (GDP), accelerated to a very respectable +3.3% growth rate during the third quarter of 2017 (the fastest percentage gain in three years). These GDP calculations are notoriously volatile figures, nevertheless, the recent results are encouraging, especially considering these third quarter statistics include the dampening effects of Hurricane Harvey and Irma.

Source: Bloomberg

- Recovering Housing Market: The housing market may not have rebounded as quickly and sharply as the U.S. stock market since the Financial Crisis, but as the chart below shows, new home sales have been on a steady climb since 2011. What’s more, a historically low level of housing inventory should support the continued growth in home prices and home sales for the foreseeable future. The confidence instilled from rising home equity values should also further encourage consumers’ cash and credit card spending habits.

Source: Calculated Risk

- Healthy Employment Gains: Growth in the U.S. coupled with global synchronous economic expansion in Europe, Asia, and South America have given rise to stronger corporate profits and increased job hiring. The graph highlighted below confirms the 4.1% unemployment rate is the lowest in 17 years, and puts the current rate more than 50% below the last peak of 10.0% hit in 2009.

Source: Calculated Risk

Turbo Tax Time

Adding fuel to the confidence fire is the prospect of the president signing the TCJA (Tax Cuts and Jobs Act). At the time this article went to press, Congress was still feverishly attempting to vote on the most significant tax-code changes since 1986. Republicans by-and-large all want tax reform and tax cut legislation, but the party’s narrow majority in the House and Senate leaves little wiggle room for disagreement. Whether compromises can be met in the coming days/weeks will determine whether a surprise holiday package will be delivered this year or postponed by the Grinch.

Unresolved components of the tax legislation include, the feasibility of cutting the corporate tax rate from 35% to 20%; the deductibility of state and local income taxes (SALT); the potential implementation of a tax cut limit “trigger”, if forecasted economic growth is not achieved; the potential repeal of the estate tax (a.k.a., “death tax”); mortgage interest deductibility; potential repeal of the Obamacare individual mandate; the palatability of legislation expanding deficits by $1 trillion+; debates over the distribution of tax cuts across various taxpayer income brackets; and other exciting proposals that will heighten accountants’ job security, if the TCJA is instituted.

Bitcoin Bubble?

If you have recently spent any time at the watercooler or at a cocktail party, you probably have not been able to escape the question of whether the digital blockchain currency, Bitcoin, is an opportunity of a lifetime or a vehicle to crush your financial dreams to pieces (see Bitcoin primer).

Let’s start with the facts: Bitcoin’s value traded below $1,000 at the beginning of this year and hit $11,000 this week before settling around $10,000 at month’s end (see chart below). In addition, blogger Josh Brown points out the scary reality that “Bitcoin has already crashed by -80% on five separate occasions over the last few years.” Suffice it to say, transacting in a currency that repeatedly loses 80% of its value can pose some challenges.

Source: CoinMarketCap.com

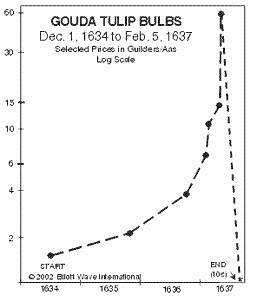

Bubbles are not a new phenomenon. Not only have I lived through numerous bubbles, but I have also written on the topic (see also Sleeping and Napping through Bubbles). I find the Dutch Tulip Bulb Mania that lasted from 1634 – 1637 to be the most fascinating financial bubble of all (see chart below). At the peak of the euphoria, individual Dutch tulip bulbs were selling for the same prices as homes ($61,700 on an inflation-adjusted basis), and one historical account states 12 acres of land were offered for a single tulip bulb.

Forecasting the next peak of any speculative bubble is a fool’s errand in my mind, so I choose to sit on the sidelines instead. While I may be highly skeptical of the ethereal value placed on Bitcoin and other speculative markets (i.e. ICOs – Initial Coin Offerings), I fully accept the benefits of the digital blockchain payment technology and also acknowledge Bitcoin’s value could more than double from here. However, without any tangible or intellectual process of valuing the asset, history may eventually place Bitcoin in the same garbage heap as the 1630 tulips.

For some of you out there, if you are anything like me, your digestion system is still recovering from the massive quantities of food consumed over the Thanksgiving holiday. However, when it comes to your personal finances, digesting record-breaking stock performance, shifting Federal Reserve monetary policy, tax legislation, and volatile digital currencies can cause just as much heartburn. In the spirit of “giving”, if you are having difficulty in chewing through all the cryptic economic and political noise, “give” yourself a break by contacting an experienced, independent, professional advisor. That’s definitely a gift you deserve!

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

A Recipe for Disaster

Justice does not always get served in the stock market because financial markets are not always efficient in the short-run (see Black-Eyes to Classic Economists). However, over the long-run, financial markets usually get it right. And when the laws of economics and physics are functioning properly, I must admit it, I do find it especially refreshing.

There can be numerous reasons for stocks to plummet in price, but common attributes to stock price declines often include profit losses and/or disproportionately high valuations (a.k.a. “bubbles”). Normally, your garden variety, recipe for disaster consists of one part highly valued company and one part money-losing operation (or deteriorating financials). The reverse holds true for a winning stock recipe. Flavorful results usually involve cheaply valued stocks paired with improving financial results.

Unfortunately, just because you have the proper recipe of investment ingredients, doesn’t mean you will immediately get to enjoy a satisfying feast. In other words, there isn’t a dinner bell rung to signal the timing of a crash or spike – sometimes there is a conspicuous catalyst and sometimes there is not. Frequently, investments require a longer expected bake time before the anticipated output is produced.

As I alluded to at the beginning of my post, justice is not always served immediately, but for some high profile IPOs, low-quality ingredients have indeed produced low-quality results.

Snap Inc. (SNAP): Let’s first start with the high-flying social media darling Snap, which priced its IPO at $17 per share in March, earlier this year. How can a beloved social media company that generates $515 million in annual revenue (up +286% in the recent quarter) see its stock plummet -48% from its high of $29.44 to $15.27 in just four short months? Well, one way of achieving these dismal results is to burn through more cash than you’re generating in revenue. Snap actually scorched through more than -$745 million dollars over the last year, as the company reported accounting losses of -$618 million (excluding -$2 billion of stock-based compensation expenses). We’ll find out if the financial bleeding will eventually stop, but even after this year’s stock price crash, investors are still giving the company the benefit of the doubt by valuing the company at $18 billion today.

Source: Barchart.com

Blue Apron Holdings Inc. (APRN): Online meal delivery favorite, Blue Apron, is another company suffering from the post-IPO blues. After initially targeting an opening IPO price of $15-$17 per share a few weeks ago, tepid demand forced Blue Apron executives to cut the price to $10. Fast forward to today, and the stock closed at $7.36, down -26% from the IPO price, and -57% below the high-end of the originally planned range. Although the company isn’t hemorrhaging losses at the same absolute level of Snap, it’s not a pretty picture. Blue Apron has still managed to burn -$83 million of cash on $795 million in annual sales. Unlike Snap (high margin advertising revenues), Blue Apron will become a low-profit margin business, even if the company has the fortune of reaching high volume scale. Even after considering Blue Apron’s $1 billion annual revenue run rate, which is 50% greater than Snap’s $600 million run-rate, Blue Apron’s $1.4 billion market value is sadly less than 10% of Snap’s market value.

Source: Barchart.com

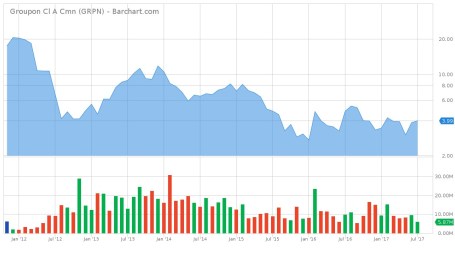

Groupon Inc. (GRPN): Unlike Snap and Blue Apron, Groupon also has the flattering distinction of reporting an accounting profit, albeit a small one. However, on a cash-based analysis, Groupon looks a little better than the previous two companies mentioned, if you consider an annual -$7 million cash burn “better”. Competition in the online discounting space has been fierce, and as such, Groupon has experienced a competitive haircut in its share price. Groupon’s original IPO price was $20 in January 2011 before briefly spiking to $31. Today, the stock has languished to $4 (-87% from the 2011 peak).

Source: Barchart.com

Stock Market Recipe?

Similar ingredients (i.e., valuations and profit trajectory) that apply to stock performance also apply to stock market performance. Despite record corporate profits (growing double digits), low unemployment, low inflation, low-interest rates, and a recovering global economy, bears and even rational observers have been worried about a looming market crash. Not only have the broader masses been worried today, yesterday, last week, last month, and last year, but they have also been worried for the last nine years. As I have documented repeatedly (see also Market Champagne Sits on Ice), the market has more than tripled to new record highs since early 2009, despite the strong under-current of endless cynicism.

Historically market tops have been marked by a period of excesses, including excessive emotions (i.e., euphoria). It has been a long time since the last recession, but economic downturns are also often marked with excessive leverage (e.g., housing in the mid-2000s), excessive capital (e.g., technology IPOs [Initial Public Offerings] in the late-1990s), and excessive investment (e.g., construction / manufacturing in early-1990s).

To date, we have seen little evidence of these markers. Certainly there have been pockets of excesses, including overpriced billion dollar tech unicorns (see Dying Unicorns), exorbitant commercial real estate prices, and a bubble in global sovereign debt, but on a broad basis, I have consistently said stocks are reasonably priced in light of record-low interest rates, a view also held by Warren Buffett.

The key lessons to learn, whether you are investing in individual stocks or the stock market more broadly, are that prices will follow the direction of earnings over the long-run. This helps explain why stock prices always go down in recessions (and are volatile in anticipation of recessions).

If you are looking for a recipe for disaster, just find an overpriced investment with money-losing (or deteriorating) characteristics. Avoiding these investments and identifying investments with cheap growth qualities is much easier said than done. However, by mixing an objective, quantitative framework with more artistic fundamental analysis, you will be in a position of enjoying tastier returns.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in SNAP, APRN, GRPN, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is the information to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Keeping the Economy Afloat

There have been plenty of concerns about rising interest rates, flattening yield curves, and potential recessions, but we all know that consumer spending accounts for roughly two-thirds of our country’s economy. Well, I certainly met my personal economic duty this summer by putting my consumer spending responsibilities to work. Not only did my family vacation involve approximately 5,700 miles of cross-country flying, but also 1,400 miles of driving all over the East Coast. By placing my credit card charging limits to the test on hotels, Airbnb, restaurants, gasoline, and overpriced tourist activities, I may have single-handedly kept the economy afloat for the rest of 2017.

Here’s a synopsis of the Slome family adventure and my spending spree binge.

Bon Jour Montreal!

View of the city from Mount Royal.

Montréal is the cultural, French-speaking crown jewel of Canada. Unbeknownst to me, the largest city in Canada’s province of Québec is actually a floating island on the Saint Lawrence River. The city name, Montreal, is actually derived from the prominent and picturesque hill at the heart of the city, Mount Royal.

Port of Montreal – Cirque de Soleil tents in the background.

Finger Lakes Fun

Ithaca, New York is located at the base of the Finger Lakes (Cayuga Lake) in upstate New York. With a population of around 30,000, this college town is home to my business school alma mater (Cornell University), which was founded in 1865 and home to a total of more than 20,000 students.

Taughannock Falls, which is Native American for “great fall in the woods,” is a 215-foot waterfall making it the highest single-drop waterfall east of the Rocky Mountains.

My drone shot of Cayuga Lake and a small portion of the Cornell University campus.

Niagara Falls

We chose to check out the 176-foot Niagara Falls from the Canadian side of the U.S.-Canada border. About 34 million gallons per minute flows during the summer time, and our drenched extremities were proof positive of this fact.

Panoramic view of Niagara Falls from Journey Behind the Falls.

View of Horseshoe Falls from 520 feet in the air while on the rotating restaurant in the Skylon Tower.

Rockin’ It in Cleveland

Cleveland is the second-largest city in Ohio, located on Lake Eerie. Even though the Cleveland Cavaliers may have lost in the NBA Finals to the Golden State Warriors, the city still rocks. The “Forest City” is home to the famous Rock and Roll Hall of Fame designed by renowned architect I. M. Pei and the well-known West Side Market.

The iconic pyramid-shaped Rock and Roll Hall of Fame located on the beautiful Lake Eerie waterfront.

It’s a little known fact that Cleveland is home to the original Christmas Story movie house. The movie was set in the early-1940s but released in 1983. Nostalgic items such as the infamous leg lamp, Red Ryder Carbine Action 200-shot Range Model BB gun, and photos of Ralphie can be found in the adjacent museum.

Slomes Seize Steel City

We discovered the vibrant city of Pittsburgh, also known as the “Steel City” and “City of Bridges” (446 bridges), at the intersection of the Allegheny, Monongahela, and Ohio Rivers “Three Rivers”. This sports-driven city is home to the World Champion Penguins (hockey), Steelers (football), and Pirates (baseball) professional teams. My dad grew up here and attended the University of Pittsburgh (“Pitt”) for both his undergraduate and medical school degrees. The rolling hills landscape provides some breathtaking views of the city, especially from Mount Washington.

Downtown Pittsburgh from Mount Washington.

The 42-story Gothic Cathedral of Learning located at the center of the Pitt campus – the second tallest university building in the world.

Gettysburg – Civil War Galore

As we began our eastward trek, Gettysburg, Pennsylvania offered a beneficial dual purpose in providing both a valuable history lesson and also a pit-stop on the way to our next vacation location. It was dumb luck rather than strategic planning that landed us at Gettysburg on the 154th anniversary of the greatest but bloodiest Civil War battle in July 1863 (half way through the Civil War 1861 – 1865). The United States of America may have looked a lot different if the 75,000 Confederate troops led by General Robert E. Lee would have defeated the 97,000 Union troops commanded by General George Meade. However, when all was said and done, the anti-slavery Union troops defeated the Confederates over a three-day battle, which resulted in more than 6,000 deaths and greater than 50,000 casualties. President Abraham Lincoln honored the fallen Union soldiers in his famous two-minute Gettysburg address four months after the battle (November 1963). In the speech, Lincoln provided an important historical context of the battle, which ultimately turned the tide of the Civil War in the Union’s favor as they fought for human equality.

A view from the Gettysburg battlefield on the 154thanniversary of the famous Confederate-Union clash.

Looking for enlightenment as I sit next to Abe outside the Gettysburg Museum.

Wade Watches Washington

Stopping at the nation’s capital was a logical progression, as we continued our East Coast adventure. Whether you are a political junky or not, it’s difficult to not get sucked into the grandeur of this majestic city of roughly one million (including commuters) on the Potomac River. The District of Columbia borders the states of Virginia and Maryland and is named after President George Washington, a man who shares the same birthday with me. Between the memorials, monuments, museums, entertainment options, and restaurants, there is no shortage of activities to choose from in this spectacular city.

The Lincoln Memorial had new meaning after our Gettysburg visit.

We stopped to say hello to President Trump, then the president and I both decided to send out a tweet.

Beach Blast

Completing our journey at Virginia Beach was no accident. All of our speed vacationing required a little R&R, and turned out to be a blast in more than one way. Not only did we enjoy soaking in the miles of beaches and hundreds of hotels and restaurants along the oceanfront, but we also appreciated the 4th of July fireworks blasting right outside our beach resort.

Nice view outside our oceanfront room.

A little relaxing cruise time down the strand.

Like any vacation, the 2017 summer family adventure eventually came to an end. No matter what I believe or say, the debate about the timing of the next recession and/or bear market will rage on for eternity. But the fact remains, despite an unemployment rate of 4.4% near cyclically low levels, there is still a record high of six million job openings available, which means there is still plenty of slack in the economy to sustain economic expansion. Although I will continue to save and strive to maintain positive investment performance figures, I will also do my best to keep the economy afloat with my consumer spending and travel binging habits.

P.S. If you spend more time vacation planning than investment planning, give us a call…we can help!

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is the information to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Coast is Clear Until 2019

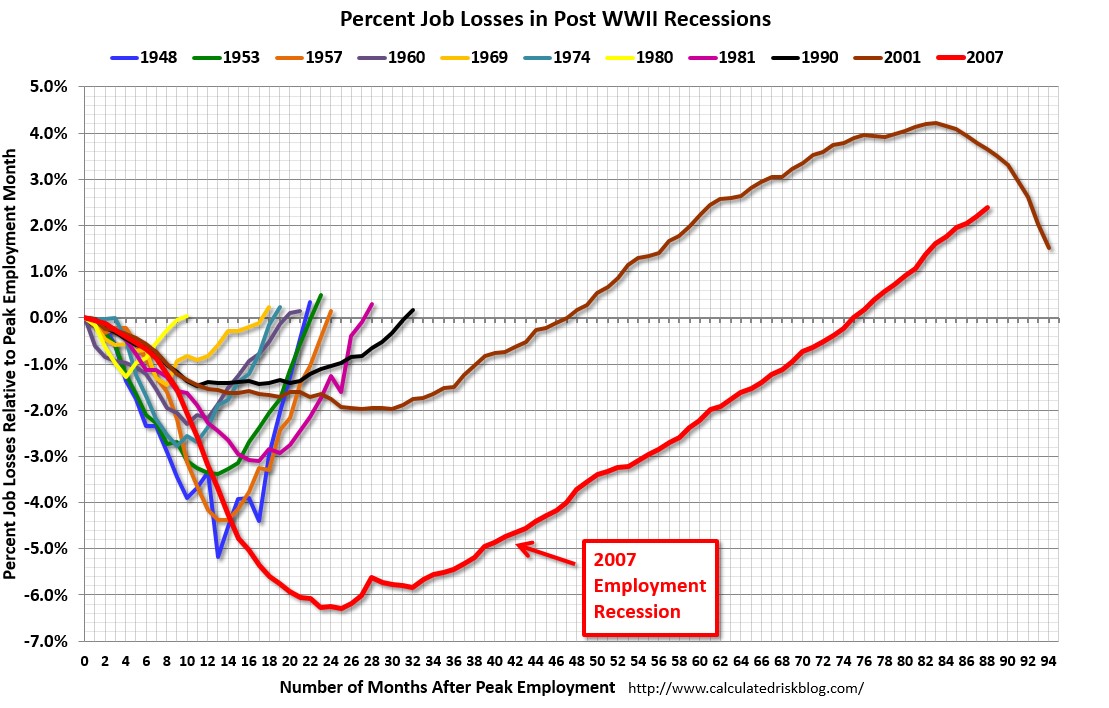

The economic recovery since the Great Financial Crisis of 2008-09 has been widely interpreted as the slowest recovery since World War II. Bill McBride of Calculated Risk captures this phenomenon incredibly well in his historical job loss chart (see red line in chart below):

Source: Calculated Risk

History tells us that the economy traditionally suffers from an economic recession twice per decade, but we are closing in on seven years since the last recession with little evidence of impending economic doom.

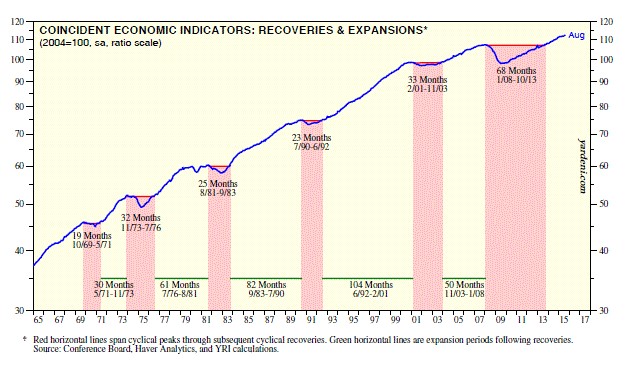

So, are we due for another recession? Logic would dictate that since this recovery has been the slowest in a generation, the duration of this recovery should also be the longest. Strategist Ed Yardeni of Dr. Ed’s Blog uses data from historical economic cycles and CEI statistics (Coincident Economic Indicators) to make the same case. Based on his analysis, Yardeni does not see the next recession arriving until March 2019 (see chart below). If you take a look at the last five previous cycle peaks, recoveries generally last for an additional five and a half years (roughly 65 months). Since the last rebound to a cyclical peak occurred in October 2013, 65 months from then would imply the next downturn would begin in March 2019.

Source: Dr. Ed’s Blog

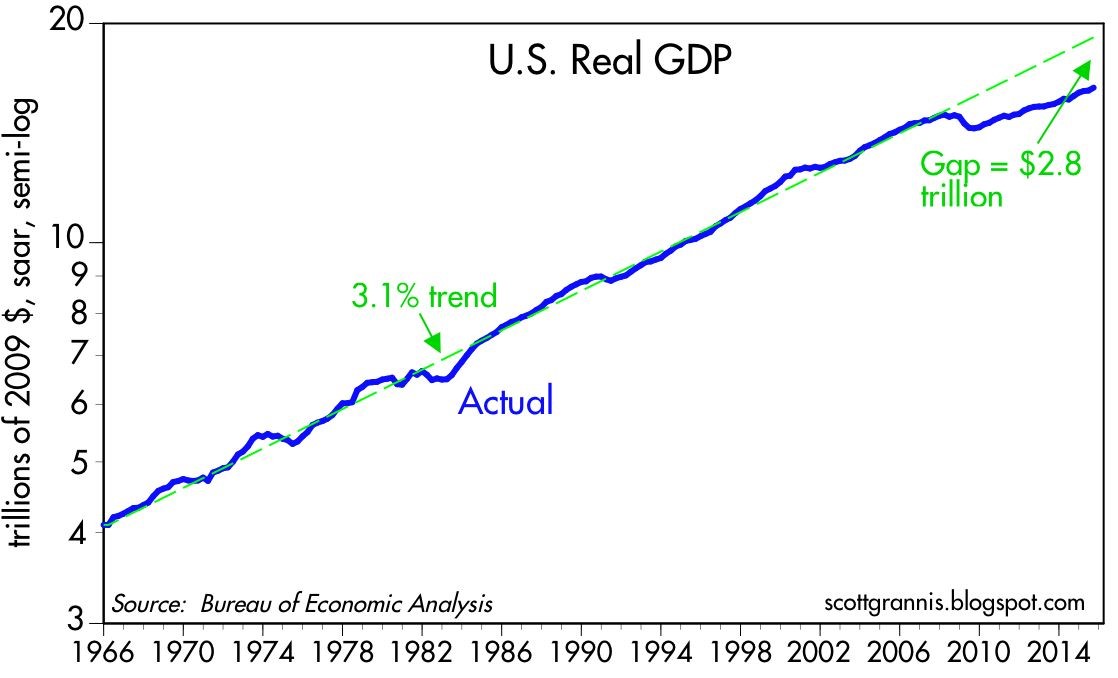

Typically, an economy loses steam and enters a recession after a phase of over-investment, tight labor conditions, and an extended period of tight central bank monetary policies. Over the last seven years, we have experienced quite the opposite. Corporations have been very slow to invest or hire new employees. For those employees hired, many of them are “under-employed” (i.e., working part-time), or in other words, these workers want more work hours. Our country’s slower-than-expected growth has created an output gap. Scott Grannis at Calafia Beach Pundit estimates this gap to approximate $2.8 trillion (see chart below). The CBO expects a smaller gap estimate of about $580 billion to narrow over the next few years. By Grannis’s calculations, there is a reservoir of 5 – 10 million jobs that could be tapped if the economy was operating more efficiently.

Source: Calafia Beach Pundit

Bolstering his argument, Grannis points out that the risk of a recession rises when there are significant capacity constraints and tight money. He sees the opposite happening – an enormous supply of unused capacity remains underutilized as he describes here:

“Today, money is abundant and resources are abundant. Even energy is abundant, because its price has fallen by over 50% in the past year or so. Corporate profits are near record highs, the supply of labor is virtually unconstrained, energy is suddenly cheap, and productive capacity is relatively abundant.”

While new uncertainties have been introduced (e.g., slowing China, potential government shutdown/sequestration, emerging market weakness), the reality remains there is always uncertainty. Even if you truly believe there is more uncertainty today relative to yesterday, the economy has some relatively strong shock absorbers to ride out the volatility.

There are plenty of potentially bad things to worry about, but if it’s a cyclical recession that you are worried about, then why don’t you grab a seat, order a coconut drink with an umbrella, and wait another three and a half years until you reach the circled date of March 2019 on your calendar.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) , but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}