Posts tagged ‘U.S. Economy’

Arm Wrestling the Economy & Tariffs

Financial markets have been battling back and forth like a championship arm-wrestling match as economic and political forces continue to collide. Despite these clashing dynamics, capitalism won the arm wrestling match this month as investors saw the winning results of the Dow Jones Industrial Average adding +4.7% and the S&P 500 index advancing +3.6%.

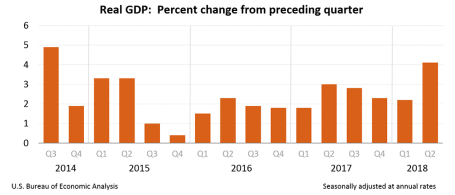

Fueling the strength this month was U.S. economic activity, which registered robust 2nd quarter growth of +4.1% – the highest rate of growth achieved in four years (see below).

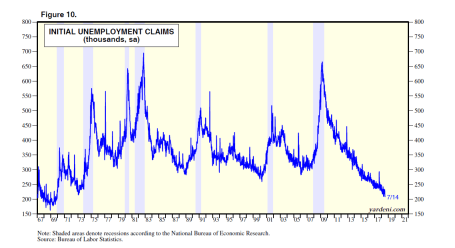

The job market is on fire too with U.S. jobless claims hitting their lowest level in 48 years (see chart below). This chart shows the lowest number of people in a generation are waiting in line to collect unemployment checks.

Source: Dr. Ed’s Blog

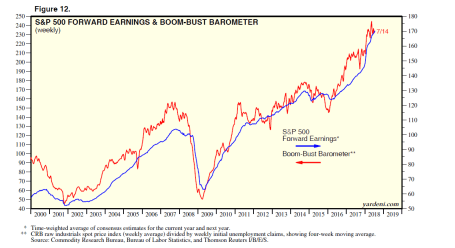

If that isn’t enough, so far, the record corporate profits being reported for Q2 are up a jaw-dropping +23.5% from a year ago. What can possibly be wrong?

Excess Supply of Concern

While the economic backdrop is largely positive, there is never a shortage of things to worry about – even during decade-long bull market of appreciation. More specifically, investors have witnessed the S&P 500 index more than quadruple from a March 2009 low of 666 to 2,816 today (+322%). Despite the massive gains achieved over the last decade, there have been plenty of volatility and geopolitics to worry about. Have you already forgotten about the Flash Crash, Arab Spring, Occupy Wall Street, Government Shutdowns, Sequestration, Taper Tantrum, Ebola, Iranian nuclear threat, plunging oil prices, skyrocketing oil prices, Brexit, China scares, Elections, and now tariffs, trade, and the Federal Reserve monetary policy?

Today, tariffs, trade, Federal Reserve monetary policy, and inflation are top-of-mind investor concerns, but history insures there will be new issues to worry about tomorrow. Ever since the bull market began a decade ago, there have been numerous perma-bears incorrectly calling for a deathly market collapse, and I have written a substantial amount about these prognosticators’ foggy crystal balls (see Emperor Schiff Has No Clothes [2009] & Clashing Views with Dr. Roubin [2009]. While these doomsdayers get a lot less attention today, similar bears like John Hussman, who like a broken record, has erroneously called for a market crash every year for the last seven years (click chart link).

Although many investment accounts are up over the last 10 years, many people quickly forget it has not been all rainbows and unicorns. While the stock market has more than quadrupled in value since 2009, we have lived through about a dozen alarming corrections, including the worrisome -12% pullback we experienced in February. If we encounter another -5 -10% correction this year, this is perfectly healthy, normal, and should not be surprising. More often than not, these temporary drops provide opportunistic openings to scoop up valued bargains.

Longtime readers and followers of Sidoxia’s investment philosophy and Investing Caffeine understand the majority of these economic predictions and political headlines are useless noise. Social media, addiction to smart phones, and the 24/7 news cycle create imaginary, scary mountains out of harmless molehills. As I have preached for years, the stock market does not care about politics and opinions – the stock market cares about 1) corporate profits (at record levels) – see chart below; 2) interest rates (rising, but still near historically low levels); 3) the price of the stock market/valuation (which is getting cheaper as profits soar from tax cuts); and 4) sentiment (a favorable contrarian indicator until euphoria kicks in).

Source: Dr. Ed’s Blog

Famed investor manager, Peter Lynch, who earned +29% annually from 1977-1990 also urged investors to ignore attempts of predicting the direction of the economy. Lynch stated, “I’ve always said if you spend 13 minutes a year on economics, you’ve wasted 10 minutes.”

I pay more attention to successful long-term investors, like Warren Buffett (the greatest investor of all-time), who remains optimistic about the stock market. As I’ve noted before, although we remain constructive on the markets over the intermediate to long-term periods, nobody has been able to consistently prophesize about the short-term direction of financial markets.

At Sidoxia, rather than hopelessly try to predict every twist and turn in the market, or react to every meaningless molehill, we objectively analyze the available data without getting emotional, and then take advantage of the opportunities presented to us in the marketplace. Certain asset classes, stocks, and bonds, will constantly move in and out of favor, which allows us to continually find new opportunities. A contentious arm wrestling struggle between uncertain tariffs/rising interest rates and stimulative tax cuts/strong economy is presently transpiring. As always, we will continually monitor the evolving data, but for the time being, the economy is flexing its muscle and winning the battle.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (August 1, 2018). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Trade War Bark: Hold Tight or Nasty Bite?

In recent weeks, President Trump has come out viciously barking about potential trade wars, not only with China, but also with other allies, including key trade collaborators in Europe, Canada, and Mexico. What does this all mean? Should you brace for a nasty financial bite in your portfolio, or should you remain calm and hold tight?

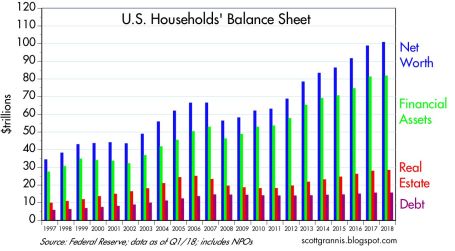

Let’s take a closer look. Recent talks of trade wars and tit-for-tat retaliations have produced mixed results for the stock market. For the month, the S&P 500 index advanced +0.5% (+1.7% year-to-date), while the Dow Jones Industrial Average modestly retreated -0.6% (-1.8% YTD). Despite trade war concerns and anxiety over a responsibly cautious Federal Reserve increasing interest rates, the economy remains strong. Not only is unemployment at an impressively low level of 3.8% (tying the lowest rate seen since 1969), but corporate profits are at record levels, thanks to a healthy economy and stimulative tax cuts. Consumers are feeling quite well regarding their financial situation too. For instance, household net worth has surpassed $100 trillion dollars, while debt ratios are declining (see chart below).

Source: Scott Grannis

Although trade is presently top-of-mind among many investors, a lot of the fiery rhetoric emanating from Washington should come as no surprise. The president heavily campaigned on the idea of reducing uniform unfair Chinese trade policies and leveling the trade playing field. It took about a year and a half before the president actually pulled out the tariff guns. The first $50 billion tariff salvo has been launched by the Trump administration against China, and an additional $200 billion in tariffs have been threatened. So far, Trump has enacted tariffs on imported steel, aluminum, solar panels, washing machines and other Chinese imports.

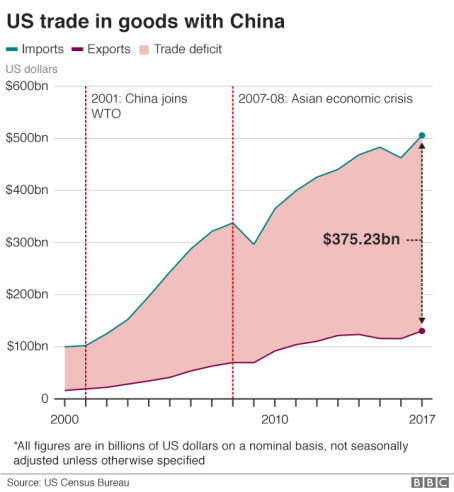

It’s important to understand, we are in the very early innings of tariff implementation and trade negotiations. Therefore, the scale and potential impact from tariffs and trade wars should be placed in the proper context relative to our $20 trillion U.S. economy (annual Gross Domestic Product) and the $16 trillion in annual global trade.

Stated differently, even if the president’s proposed $50 billion in Chinese tariffs quadruples in value to $200 billion, the impact on the overall economy will be minimal – less than 1% of the total. Even if you go further and consider our country’s $375 billion trade deficit with China for physical goods (see chart below), significant reductions in the Chinese trade deficit will still not dramatically change the trajectory of economic growth.

Source: BBC

The Tax Foundation adds support to the idea that current tariffs should have minimal influence:

“The tariffs enacted so far by the Trump administration would reduce long-run GDP by 0.06 percent ($15 billion) and wages by 0.04 percent and eliminate 48,585 full-time equivalent jobs.”

Of course, if the China trade skirmish explodes into an all-out global trade war into key regions like Europe, Mexico, Canada, and Japan, then all bets are off. Not only would inflationary pressures be a drag on the economy, but consumer and business confidence would dive and they would drastically cut back on spending and negatively pressure the economy.

Most investors, economists, and consumers recognize the significant benefits accrued from free trade in the form of lower-prices and a broadened selection. In the case of China, cheaper Chinese imports allow the American masses to buy bargain toys from Wal-Mart, big-screen televisions from Best Buy, and/or leading-edge iPhones from the Apple Store. Most reasonable people also understand these previously mentioned consumer benefits can be somewhat offset by the costs of intellectual property/trade secret theft and unfair business practices levied on current and future American businesses doing business in China.

Trump Playing Chicken

Right now, Trump is playing a game of chicken with our global trading partners, including our largest partner, China. If his threats of imposing stiffer tariffs and trade restrictions result in new and better bilateral trade agreements (see South Korean trade deal), then his tactics could prove beneficial. However, if the threat and imposition of new tariffs merely leads to retaliatory tariffs, higher prices (i.e., inflation), and no new deals, then this mutually destructive outcome will likely leave our economy worse off.

Critics of Trump’s tariff strategy point to the high profile announcement by Harley-Davidson to move manufacturing production from the United States to overseas plants. Harley made the decision because the tariffs are estimated to cost the company up to $100 million to move production overseas. As part of this strategy, Harley has also been forced to consider motorcycle price hikes of $2,200 each. On the other hand, proponents of Trump’s trade and economic policies (i.e., tariffs, reduced regulations, lower taxes) point to the recent announcement by Foxconn, China’s largest private employer. Foxconn works with technology companies like Apple, Amazon, and HP to help manufacture a wide array of products. Due to tax incentives, Foxconn is planning to build a $10 billion plant in Wisconsin that will create 13,000 – 15,000 high-paying jobs. Wherever you stand on the political or economic philosophy spectrum, ultimately Americans will vote for the candidates and policies that benefit their personal wallets/purses. So, if retaliatory measures by foreign countries introduces inflation and slowly grinds trade to a halt, voter backlash will likely result in politicians being voted out of office due to failed trade policies.

Source: Dr. Ed’s Blog

Time will tell whether the current trade policies and actions implemented by the current administration will lead to higher costs or greater benefits. Talk about China tariffs, NAFTA (North American Free Trade Agreement), TPP (Trans Pacific Partnership), and other reciprocal trade negotiations will persist, but these trading relationships are extremely complex and will take a long time to resolve. While I am explicitly against tariff policies in general, I am not an alarmist or doomsayer, at this point. Currently, the trade war bark is worse than the bite. If the situation worsens, the history of politics proves nothing is permanent. Circumstances and opinions are continually changing, which highlights why politics has a way of improving or changing policies through the power of the vote. While many news stories paint a picture of imminent, critical tariff pain, I believe it is way too early to come to that conclusion. The economy remains strong, corporate profits are at record levels (see chart above), interest rates remain low historically, and consumers overall are feeling better about their financial situation. It is by no means a certainty, but if improved trade agreements can be established with our key trading partners, fears of an undisciplined barking and biting trade dog could turn into a tame smooching puppy that loves trade.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (July 3, 2018). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AAPL, AMZN, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in WMT, HOG, HPQ, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

What Do You Worry About Next?

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (November 1, 2016). Subscribe on the right side of the page for the complete text.

Boo! Halloween has just passed and frightened investors have still survived to tell the tale in 2016. While most people have gotten spooked by the presidential election, other factors like record-high corporate profits, record-low interest rates, and reasonable valuations have led to annual stock market gains. More specifically, values have risen in 2016 by approximately +4% (or +6% including dividend payments). Despite last week’s accelerating 3rd quarter GDP economic growth figure of +2.9%, which was the highest rate in two years and more than doubled the rate of the previous quarter (up +1.4%), there were still more tricks than treats during October. Recently, scary politics have shocked many Halloween participants into a zombie-like state, as evidenced by stock values declining around -1.7% during October.

This recent volatility is nothing new. Even though financial markets are significantly higher in recent years, that has not prevented repeated corrections over the year(s) as shown below in the 2009 – 2015 chart.

In order to earn higher long-term returns, investors have to accept a certain amount of short-term price movements (upwards and downwards). With a couple months remaining in the year, stock investors have achieved gains through a tremendous amount of economic and geopolitical uncertainty, including the following scares:

- China: A significant fallout from a Chinese slowdown at the beginning of the year (stocks fell about -14%).

- Brexit: A 48-hour Brexit vote scare in June (stocks fell -6%).

- Fed Fears: Threatening comments in September from the Federal Reserve about potentially hiking increasing interest rates (stocks fell -4%).

With the elections just a week away, political anxiety has jolted Americans’ adrenaline levels. The polls continue to move up and down, but as I have repeatedly pointed out, the only certain winner in Washington DC is gridlock. Sure, in a Utopian world, politicians should join hands and compromise to solve all our country’s serious problems. Unfortunately, this is not the case (see Congress’s approval rating). However, there is a silver lining to this dysfunction…gridlock can lead to fiscal discipline.

Our country’s debt/deficit financial situation has been spiraling out of control, in large measure due to rapidly rising entitlement spending, including Medicare, and Social Security. Witnessing all the political rhetoric and in-fighting is very difficult, but as I highlighted in last month’s newsletter, gridlock has flattened the spending curve significantly since 2009 – a positive development.

And although the economic recovery has been one of the slowest since World War II and global growth remains anemic, the U.S. remains a better house in a bad global neighborhood (e.g., Europe and Japan continue to suck wind), as evidenced by a number of these following positive economic indicators:

- Employment Improvement: Unemployment has fallen from 10% to 5% since 2009, and more than 15 million jobs have been added over that period.

- Housing Recovery Continues: Home sales and prices continue their multi-year rise; housing inventories remain tight; and affordability remains strong, given generationally low interest rates.

- Record Auto Sales: Car sales remain near record levels, hovering around 17 million units per year.

- Consumer Confidence on the Rise: Ever since the financial crisis, consumer sentiment figures have rebounded by about 50%.

-

Record Consumer Sales: Consumer spending accounts for approximately 70% of our economy, and as you can see from the chart below, despite consumers saving more, stronger employment and wages are fueling more spending.

Source:Calculated Risk

Source:Calculated Risk

Absent a clean sweep of control by the Democrat or Republican Presidential-Congressional candidates, our democratic system will retain its healthy status of checks and balances. Based on all the current polling data, a split between the White House, Senate, and House of Representatives remains a very high likelihood scenario.

The political process has been especially exhausting during the current cycle, but regardless of whether your candidate wins or loses, much of the current uncertainty will likely dissipate. As the saying goes, at least it is “Better the devil you know than the devil you don’t know.”

After the November 8th elections are completed, there will be one less election to worry about. Thankfully, after 25 years in the industry, I’m not naïve enough to believe there will be nothing else to worry about. When the financial media and blogosphere get bored, at a minimum, you can guarantee yourself plenty of useless coverage regarding the next monetary policy move by the Federal Reserve (see also Fed Fatigue).

Whatever the next set of worries become, U.K. Prime Minister Winston Churchill said it best as it relates to American politics and economics, “You can always count on Americans to do the right thing – after they’ve tried everything else.” If Churchill’s words don’t provide comfort and you had fun getting spooked over the elections on Halloween, feel free to keep wearing your costume. Behind any constructive economic data, the prolific media machine will continue doing their best in manufacturing plenty of fear, uncertainty, and doubt to keep you worried.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Fall is Here: Change is Near

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (October 1, 2016). Subscribe on the right side of the page for the complete text.

Although the fall season is here and the leaf colors are changing, there are a number of other transforming dynamics occurring this economic season as well. The S&P 500 index may not have changed much this past month (down -0.1%), but the technology-laden NASDAQ index catapulted higher (+1.9% for the month and +6.0% for 2016).

With three quarters of the year now behind us, beyond experiencing a shift in seasonal weather, a number of other changes are also coming. For starters, there’s no ignoring the elephant in the room, and that is the presidential election, which is only weeks away from determining our country’s new Commander in Chief. Besides religion, there are very few topics more emotionally charged than politics – whether you are a Republican, Democrat, Independent, Libertarian, or some combination thereof. Even though the first presidential debate is behind us, a majority of voters are already set on their candidate choice. In other words, open-minded debate on this topic can be challenging.

Hearing critical comments regarding your favorite candidate are often interpreted in the same manner as receiving critical comments about a personal family member – people often become defensive. The good news, despite the massive political divide currently occurring in the country and near-record low politician approval ratings in Congress , politics mean almost nothing when it comes to your money and retirement (see also Politics & Your Money). Regardless of what politicians might accomplish (not much), individuals actually have much more control over their personal financial future than politicians.

While inaction may rule the day currently, more action generally occurs during a crisis – we witnessed this firsthand during the 2008-2009 financial meltdown. As Winston Churchill famously stated,

“You can always count on Americans to do the right thing – after they’ve tried everything else.”

Political discourse and gridlock are frustrating to almost everyone from a practical standpoint (i.e., “Why can’t these idiots get something done in Washington?!”), however from an economic standpoint, gridlock is good (see also Who Said Gridlock is Bad?) because it can keep a responsible lid on frivolous spending. Educated individuals can debate about the proper priorities of government spending, but most voters agree, maintaining a sensible level of spending and debt should be a bipartisan issue.

From roughly 2009 – 2014, you can see how political gridlock has led to a massive narrowing in our government’s deficit levels (chart below) – back to more historical levels.This occurred just as rising frustration with Washington has been on the rise.

The Fed: Rate Revolution or Evolution?

Besides the changing season of politics, the other major area of change is Federal Reserve monetary policy. Even though the Fed has only increased interest rates once over the last 10 years, and interest rates are at near-generational lows, investors remain fearful. There is bound to be some short-term volatility if interest rates rise to 0.50% – 0.75% in December, as currently expected. However, if the Fed continues at its current snail’s pace, it won’t be until 2032 before they complete their rate hike cycles.

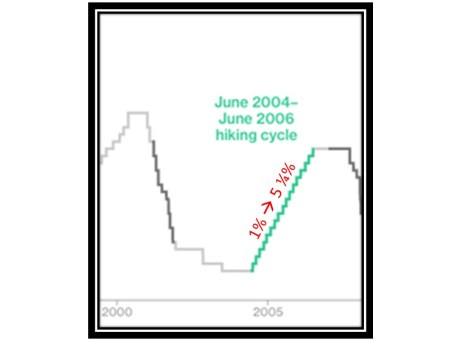

We can put the next rate increase into perspective by studying history. More specifically, the Fed raised interest rates 17 times from 2004 – 2006 (see chart below). Fortunately over this same time period, the world didn’t end as the Fed increased interest rates from 1.00% to 5.25% (stocks prices actually rose around +11%). The same can be said today – the world won’t likely end, if interest rates rise from 0.50% to 0.75% in a few months.

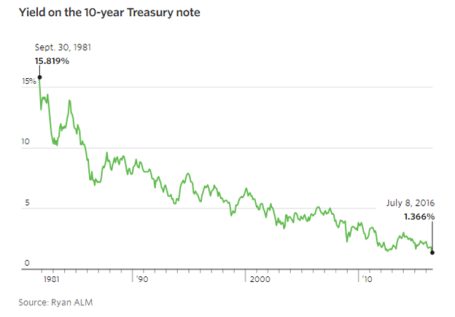

The next question becomes, why are interest rates so low? There are many reasons and theories, but a few of the key drivers behind low rates include, slower global economic growth, low inflation, high demand for low-risk assets, technology, and demographics. I could devote a whole article to each of these factors, and indeed in many cases I have, but suffice it to say that there are many reasons beyond the oversimplified explanation that artificial central bank intervention has led to a 35 year decline in interest rates (see chart below).

Change is a constant, and with fall arriving, some changes are more predictable than others. The timing of the U.S. presidential election outcome is very predictable but the same cannot be said for the timing of future interest rate increases. Irrespective of the coming changes and the related timing, history reminds us that concerns over politics and interest rates often are overblown. Many individuals remain overly-pessimistic due to excessive, daily attention to gloomy and irrelevant news headlines. Thankfully, stock prices are paying attention to more important factors (see Don’t Be a Fool) and long-term investors are being rewarded with record high stock prices in recent weeks. That’s the type of change I love.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Energizer Market… Keeps Going and Going

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (May 2, 2016). Subscribe on the right side of the page for the complete text.

Boom, boom, boom…it keeps going…and going…and going…

You’ve seen the commercials: A device operating on inferior batteries dies just as a drum-beating, battery operated Energizer bunny comes speeding and spiraling across the television screen. Onlookers waiting for the battery operated toy to run out of juice, instead gaze in amazement as they watch the energized bunny keep going and going. The same phenomenon is occurring in the stock market, as many observers eagerly await for stock prices to die. The obituary of the stock market has been written many times over the last eight years (see Series of Unfortunate Events). Mark Twain summed up this sentiment well, when after a premature obituary was written about him, he quipped, “The reports of my death are greatly exaggerated.”

With fears abound, stocks added to their annual gains by finishing their third consecutive positive month with the S&P 500 indexes and Dow Jones Industrial Average advancing +0.5% and +0.3%, respectively. Skeptics and worry-warts have been concerned about stocks plummeting ever since the Financial Crisis of 2008-2009. We experienced a 100 year flood then, and as a consequence, scarred investors now expect the 100 year flood to repeat every 100 days (see also 100 Year Flood). Given the damage created in the wake of the “Great Recession,” many individuals have become afraid of their own shadow. The shadows currently scaring investors include the following:

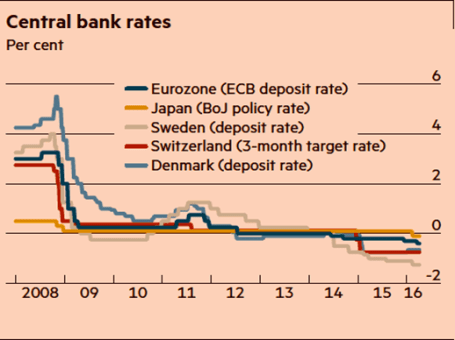

- Negative Interest Rates: The unknown consequences of negative interest rate policies by central banks (see chart below).

- U.S. Monetary Policy: The potential continuation of the Federal Reserve hiking interest rates.

- Sluggish Economic Growth: With a GDP growth figure up only +0.5% during the first quarter many people are worried about the vulnerability of slipping into recession.

- Brexit Fears: Risk of Britain exiting the European Union (a.k.a. “Brexit”) will blanket the airwaves as the referendum approaches next month

For these reasons, and others, the U.S. central bank is likely to remain accommodative in its stance (i.e., Fed Chairwoman Janet Yellen is expected to be slow in hitting the economic brakes via interest rate hikes).

Source: Financial Times. Central banks continue with attempts to stimulate with zero/negative rates.

Climbing the Wall of Worry

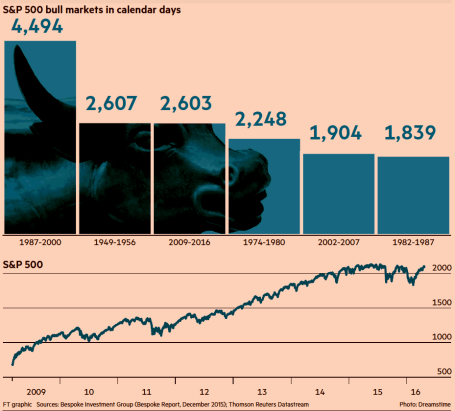

Despite all these concerns, stock prices continue climbing the proverbial “wall of worry” while approaching record levels. As famed investor Sir John Templeton stated on multiple occasions, “Bull markets are born on pessimism, and they grow on skepticism, mature on optimism, and die on euphoria.” It’s obvious to me there currently is no euphoria in the overall market, if you consider investors have withdrawn $2 trillion in stock investments since 2007. The phenomenon of stocks moving higher in the face of bad news is nothing new. A recent study conducted by the Financial Times newspaper shows the current buoyant bull market entering the second longest advancing period since World War II (see chart below).

Source: Financial Times

There will never be a shortage of concerns or bad things occurring in a world of 7.4 billion people, but the Energizer bunny U.S. economy has proven resilient. Our economy is entering its seventh consecutive year of expansion, and as I recently pointed out the job market keeps plodding along in the right direction – unemployment claims are at a 43-year low (see Spring Has Sprung). Over the last few years, these job gains have come despite corporate profits being challenged by the headwinds of a stronger U.S. dollar (hurts our country’s exports) and tumbling energy profits. Fortunately, the negative factors of the dollar and oil prices have stabilized lately, and these dynamics are in the process of shifting into tailwinds for company earnings. The -5.7% year-to-date decline in the Dollar Index coupled with the recent rebound in oil prices are proof that the economic laws of supply-demand eventually respond to large currency and commodity swings. With the number of rigs drilling for oil down by approximately -80% over the last two years, it comes as no surprise to me that a drop in oil supply has steadied prices.

The volatility in oil prices has been amazing. Energy companies have been reeling as oil prices dropped -76% from a 2014-high of $108 per barrel to a 2016-low of $26 per barrel. Since then, the picture has improved significantly. Crude oil prices are now hovering around $46 per barrel, up +76%.

Energy Bankruptcy & Recessionary Fears Abate

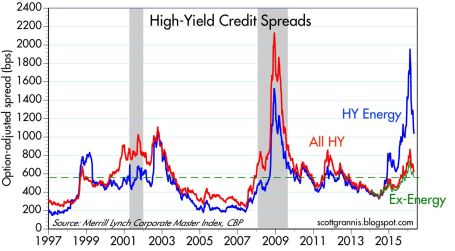

If you take a look at the borrowing costs of high-yield companies in the chart below (Calafia Beach Pundit), you can see that prior spikes in the red line (all high-yield borrowing costs) were correlated with recessions – represented by the gray periods occurring in 2001 and 2008-09. During 2016, you can see from the soaring blue line, investors were factoring in a recession for high-yield energy companies (until the oil price recovery), but the non-energy companies (red-green lines) were not anticipating a recession for the other sectors of the economy. Bottom-line, this chart is telling you the knee-jerk panic of recessionary fears during the January-February period of this year has quickly abated, which helps explain the sharp rebound in stock prices.

After a jittery start to 2016 when economic expectations were for a dying halt, investors have watched stocks recharge their batteries in March and April. There are bound to be more fits and starts in the future, as there always are, but for the time being this Energizer bunny stock market and economy keeps going…and going…and going…

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}