Posts tagged ‘U.S. dollar’

Chasing Headlines

It’s been an amazing start to the year. First the market cratered on slowing China economic concerns, domestic recessionary fears, deteriorating oil prices, and negative interest rates abroad. In response to all these worries (and others), stocks dove more than -11% (S&P 500 Index) in January, before settling down. Subsequently, the market has made a screaming recovery, in part due to dovish monetary policy comments (i.e., reduction in forecasted interest rate hikes) and diminished anxiety over a potential global collapse. Month-to-date stocks are up an impressive +5.4%, and year-to-date equities are flattish, or down less than -1%.

With an endless amount of information flowing across our smart phones and computers, it becomes quite easy and tempting to chase news headlines, just like a hyper dog chasing a car. But even once an investor catches up (or reacts) to a headline, there’s confusion around how to profit from the fleeting information. First of all, every plugged-in hedge fund and institutional investor has likely already traded on the stale information you received. Second of all, rarely is the data relevant to the long-term cash generating capabilities of the company or economy. And lastly, the news is more often than not, instantly factored into the stock price. Chasing news headlines only eaves individual investors holding the bag of performance-shattering transactions costs, taxes, and worn-out pricing.

The heightened volatility in late 2015 and early 2016 hasn’t however prevented investors and so-called pundits from attempting to time the market. Any battle-tested investment veteran knows it’s virtually impossible to consistently time the market (see also Market Timing Treadmill), but this fact hasn’t prevented speculators from attempting the feat nonetheless. Famed investment guru, Peter Lynch, who earned an average +29% annual return from 1977-1990, summed it up well when he stated the following:

“Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.”

The Important Factors

As I’ve written many times in the past, the keys to long-term stock performance are not knee-jerk reactions to headlines, but rather these following crucial factors (see also Don’t Be a Fool, Follow the Stool):

- Profits

- Interest Rates

- Sentiment

- Valuations

On the profit growth front, corporate income has been pressured by numerous headwinds over the last few years, including an export-shattering increase in the value of the U.S. dollar and a profit-squeezing collapse in energy sector earnings. As you can see from the chart below, the value of the U.S. dollar increased by about 25% from mid-2014 to early-2015, in part because of diverging global central bank policies (more hawkish U.S. Fed vs. more dovish ECB/international central banks). Since that spike, the dollar has settled into a broad range (95 – 100), and the former forceful headwind have now turned into modest tailwinds. This trend is important because an estimated 35-40% of corporate profits are derived from international operations.

Adding insult to injury, the roughly greater than -70% decline in forward energy earnings over the last 18 months has caused a significant hit to overall S&P 500 profits. The tide appears to be finally turning (or at least stabilizing) however, as we’ve seen oil prices rebound by about +30% this year from the lows in January. If these aforementioned trends persist, profit pressures in 2016 are likely to abate significantly, and may actually become additive to growth.

Source: Barchart.com

Profits are important, but so are interest rates. While incessant talk about the path of future Fed policy continues to blanket the airwaves (see also Fed Fatigue), absent a rapid increase in interest rates (say 300-400 basis points), interest rates remain unambiguously positive for equity markets, providing a floor for the oft-repeated volatility in financial markets. As long as stocks are providing higher yields than many bonds, and depositors are earning 0% (or negative rates) on their checking accounts, stocks may remain unloved, but not forgotten.

And speaking of unloved, the sentiment for stocks remains sour. One need look no further than the quarter-billion dollars in hemorrhaging outflows out of U.S. equity funds (see ICI Long-Term Mutual Fund Flows) since 2014. This deep underlying skepticism serves as a positive contrarian indicator for future equity prices. Right now, very few individual investors are swimming in the pool – the time to get out of the stock market pool is when everyone is jumping in.

And lastly, valuations remain very much in line with historical averages (approximatqely 17x 2016 projected earnings), especially considering the generational low in interest rates. Bears continue to point to the elevated CAPE ratio, which has been a disastrous indicator the last seven years (and longer), as a reason to remain cautious. The ironic part is that valuations are virtually guaranteed to improve a few years from now as we roll off the artificially depressed years of 2008-2010.

When you add it all up, zero (or negative) interest rates, combined with the other key factors of profits, sentiment, and valuations, equities remain an important and attractive part of a diversified long-term portfolio. Your objectives, time horizon, and risk tolerance will always drive the proportion of your equity allocation. Nevertheless, some bond exposure is essential to smooth out volatility. Regardless of your investment strategy, chasing headlines, like a dog chasing a car, serves no purpose other than leaving you with a tired, unproductive investment portfolio.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Shoot Now, Ask Later

![940614_83408820[1]](https://investingcaffeine.com/wp-content/uploads/2011/08/940614_834088201.jpg?w=311&h=230)

Since the start of 2016, investor sentiment has led to a shoot now, ask questions later mentality. In the court of economic justice, all stocks have been convicted guilty of recession despite the evidence and defense that proves the economy innocent. Even the Federal Reserve Chair Janet Yellen did not prove to be a great public defender of the economy with her comments that negative interest rates are on the table.

With large cap stocks down -13% and small cap stocks losing -25% from 2015, there are a mixture of indicators suggesting a looming recession could be coming. For example, banking stocks, the beating heart of the U.S. economy, saw prices collapse almost -30% from the 2015 highs this week. As CNBC pointed out, “American Airlines (AAL), United Continental (UAL), General Motors (GM) and Ford (F) all sell for five times 2016 earnings” – about a 70% discount to the average S&P 500 stock. As a group, these economically sensitive cyclical stocks grew earnings per share greater than 50%, while their stock prices are down by more than -30% from their 52-week highs. In general, the cyclicals are serving jail time, even though growth has been gangbusters and the current valuations massively discounted.

On the flip side, defensive stocks with little-to-no revenue growth like “Campbell Soup (CPB) trade at 20 times earnings, Kimberly-Clark (KMB) is at 21 times earnings, Procter & Gamble (PG) is at 22 times earnings and Clorox (CLX) is at 25 times earnings. All of these stocks are near 52-week highs.”

Confused? Well, if we are indeed going into recession, than this valuation dichotomy between cyclicals and staples makes sense. Stocks can be a leading indicator (i.e., predictor) of future recessions, but as the famed Nobel Prize winner in economics Paul Samuelson noted, “The stock market has forecast nine of the last five recessions.”

On the other hand, if this current correction is a false recession scare, then now would be a tremendous buying opportunity. In fact, over the last five years, there have been plenty of tremendous buying opportunities for those courageous long-term investors willing to put capital to work during these panic periods (see also Groundhog Day All Over Again):

- 2011: Debt Downgrade/Debt Ceiling Debate/European PIIGS Crisis (-22% correction)

- 2012:Arab Spring/Greek “Gr-Exit” Fears (-11% correction)

- 2013: Fed Taper Tantrum (-8% correction)

- 2014: Ebola Outbreak (-10% correction)

- 2015: China Slowdown Fears (-13% correction in August)

- 2016 (1st Six Weeks): Strong Dollar, Collapsing Oil, interest Rate Hikes/Negative Rates, Weakening China (-15% correction)

- 2016 (Next 46 Weeks): ??????????

Today’s threats rearing their ugly heads have definite recession credibility, but if you think about the strong dollar, collapsing oil prices, Fed monetary policies, weakening Chinese economy, and negative global interest rates, all of these threats existed well before stock prices nose-dived during the last six weeks. If the economic court is judging the current data for potential recession evidence, making a case and proving the economy guilty is challenging. It’s tough to find a recession when we witness a low unemployment rate (4.9%); record corporate profits (ex-energy); record car sales (17.5 million); an improving housing market; a positively sloped yield curve; healthy banking and consumer balance sheets; sub-$2/gallon gasoline; and a flattening U.S. dollar, among other factors.

Could stock prices be clairvoyantly predicting Armageddon? Sure, anything is possible…but this scenario is unlikely now. Even if the U.S. economy is headed towards a recession, the -20% plunge in stock prices is already factoring in most, if not all, of a mild-to-moderate recession. If the economic data does actually get worse, there is still room for stock prices to go down. Under a recession scenario, the tremendous buying opportunities will only get better. While weak hands may be shooting (selling) first and asking questions later, now is the time for you to use patience and discipline. These characteristics will serve as bullet proof vest for your investment portfolio and lead to economic justice over the long-term.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and non-discretionary positions in PG, and KMB, but at the time of publishing had no direct position in AAL, CLX, CPB, F, GM, UAL, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Groundhog Day All Over Again

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (February 1, 2016). Subscribe on the right side of the page for the complete text.

It’s that time of the year when the masses gather in eager anticipation of Groundhog Day to predict whether the furry rodent will see its shadow in 2016, thereby extending winter for an additional six weeks.

In the classic movie Groundhog Day, actor Bill Murray plays character Phil Connors, an arrogant, self-centered TV weatherman who, during an assignment covering the annual Groundhog Day event in Punxsutawney, Pennsylvania, finds himself stuck in a time loop, repeating the same day over and over. With a feeling of nothing to lose, Phil repeatedly decides to indulge in reckless hedonism and criminal behavior. After being resigned to perpetually reliving the same day forever, Phil begins to re-examine his life and falls in love with his co-worker Rita Hanson (see scene here). Ultimately, Phil’s pure focus on the important priorities of life allows himself to break the painful monotonous time loop and win Rita’s love.

Stock market investors are lining up in a similar fashion to predict whether the financial winter experienced in January will persist through the rest of the year. The groundhog, equipped with a thick fur coat, certainly would have been more optimally prepared for the icy January financial market conditions. More specifically, the S&P 500 index declined -5.1% for the month and the Dow Jones fell -5.5%.

Unfortunately for many investors, they too have been trapped in a never-ending news cycle, which painfully buries the public with a monotonous loop of daily pessimistic headlines. As a result of the eternally distorted media cycle, many investors have lost sight of important priorities like Phil Connors. Since the beginning of 2011, the investors who have endured the relentless wave of media gloom have been handsomely rewarded. From 2011-2016, the S&P 500 stock index has ascended approximately 54%, even after accounting for the significant January 2016 decline.

Unless you were burrowed in a hole like a groundhog, you will probably recognize a number of these ominous headlines spanning across the 2011 – 2015 headlines:

- 2011: Debt Downgrade/Debt Ceiling Debate/European PIIGS Crisis (-22% correction)

- 2012: Arab Spring/Greek “Gr-Exit” Fears (-11% correction)

- 2013: Fed Taper Tantrum (-8% correction)

- 2014: Ebola Outbreak (-10% correction)

- 2015: China Slowdown Fears (-13% correction)

Similar to the Groundhog Day movie, the headlines of 2016 match the tone and mood we’ve seen in recent years. Here’s an abbreviated list of the recurring worries-du-jour in January:

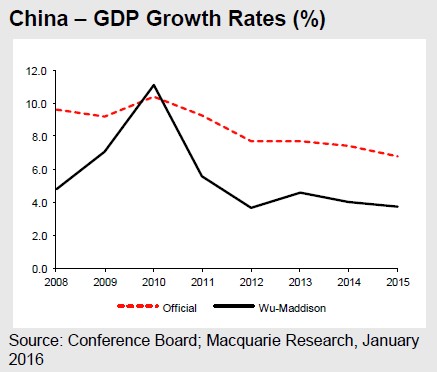

China Slowdown: Is this something new? As you can see from the chart below, China has been slowing since 2010. Due to the law of large numbers, and as the second largest economy on the globe, it is natural to see such an enormous economic engine eventually slow. Rather than panic over China’s slowing, observers should be applauding. China’s Q4 GDP growth recently came in at +6.8%, almost 10x the level recorded by the U.S. in Q4 (+0.7%). Even if you mistrust the official Chinese government’s reported data, our economy would kill for the still impressive independently reported growth statistics (see chart below). While the concerted effort of the political regime to migrate the country from an export-driven economy to a consumption-based one has caused some growing pains, nevertheless in recent months we have seen China report record automobile purchases, retail sales, oil consumption, and industrial production.

Rise of the U.S. Dollar: This is a legitimate concern that has had tangible negative impacts on the U.S. economy. As you can see from the chart below (blue line), in less than one year, the value of the U.S. dollar spiked by approximately +25%. If you are a multinational company exporting a product to Europe for $100, and consumers wake up a year later having to pay $125 for the same product, it should come as no surprise to anyone that this phenomenon is squeezing profits. The good news is that U.S. corporations have already absorbed the worst of this currency pain dating back to early 2015, so if the stabilizing foreign exchange trends remain near current levels, as they have over the last year, there should be no additional economic drag.

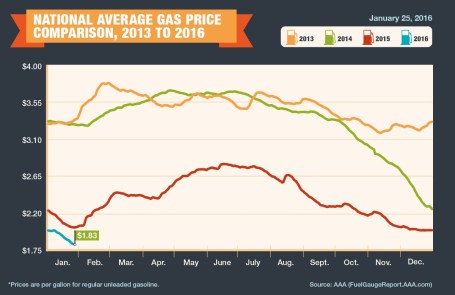

Oil Prices Down: Somehow the U.S. media is trying to convince the public that lower oil prices are bad for the economy. Yes, it is true, the financial restructurings and lost jobs associated with oil price declines will hurt the economy and the banks overall. However, the benefits of lower oil prices on the broader economy (i.e., more money in consumers’ pockets) is unambiguously positive and will overwhelm any indirect damage. Every penny decrease in gasoline prices (now roughly $1.83 per gallon nationally) equates to about a $1 billion tax cut for consumers (see chart below). Many people are worried about oil prices being a signal of weakness, but if you look at the last few recessions, they were all preceded by an oil price spike, not a price collapse.

Source: AAA

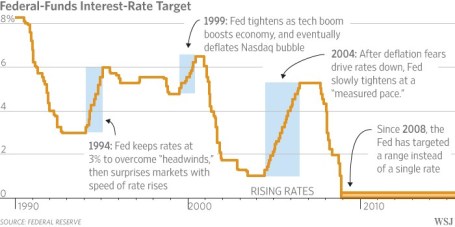

Federal Reserve Monetary Policy: The first interest rate hike in nine years took place in 2015, but that did not prevent investors from fretting about the timing of the next interest rate hike. As I’ve written many times (see Fed Fatigue Setting In), the Fed has barely budged its target rate to 0.375%, so this is much to do about nothing. Wake me up when we get to 2.00%, at which point we will still be far below the long-term average but at a more meaningful level (see chart below).

Source: The Wall Street Journal

Presidential Elections: Congress’s approval rating is abysmal, but like it or not, primary season is just starting and we are stuck in a presidential election cycle until the second Tuesday of November. Guess what? If you want to know the impact of the elections on the financial markets, then I will give you the short answer…it just does not matter who gets elected. History shows us that the markets go up and down under both Republican and Democratic parties. If you are comparing the track record on the political parties’ track record on debt creation, it is a mixed bag as well (see chart below). Arguably, in half the cases, the nomination of the Federal Reserve chairs will have as large (or larger) an impact than the elected president. If you were to factor in the inevitable splits in Congress to the equation, the result is gridlock. I have contended for some time that gridlock is a positive outcome because it structurally forces a lid on disciplined government spending (see Who Said Gridlock is Bad?). If this isn’t a good enough explanation, see Barry Ritholtz’s take on the subject of politics and the stock market…I couldn’t sum it up any better (click here)

Source: Calafia Beach Pundit

Fortunately for groundhogs, and long-term investors, dealing with challenging and volatile climates is nothing new. Both burrowing marmots and emotional investors need to adapt to ever-changing environments…sunny or overcast. In addition to a cold 2016 start, January was also a chilly month in 2014 and 2015, with the S&P 500 down -3.6% and -3.1%, respectively. Despite this seasonal sour sentiment, there is a silver lining. In both instances (2014 & 2015), the market rebounded significantly in subsequent months after the slow start at the beginning of the year. For the remainder of the year, the S&P advanced +15.5% in 2014, and +2.5% in 2015.

In Groundhog Day the movie, Bill Murray relived the same day over and over again, and repeated the same missteps until he learned from his mistakes. Long-term investors will be served best by applying this same philosophy to their investments. Like a groundhog, investors have a tendency to become scared of their own shadows. It’s easy to succumb to the infinite time loop of worrisome headlines, but rather than burrowing away in hibernation, creating a diversified, low-cost, tax-efficient portfolio customized for your specific time horizon, risk tolerance, and liquidity needs is a better way of celebrating this year’s Groundhog Day.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Who Gives a #*&$@%^?!

The stock market is just a big rigged casino, fueled by a reckless money printing Fed that is artificially inflating a global asset bubble, right? That seems to be the mentality of many investors as evidenced by the lack of meaningful domestic stock fund buying/inflows (see also Digesting Stock Gains). Underlying investor skepticism is a foundation of mistrust and detachment caused by the unprecedented 2008-09 financial crisis, when regulators fell asleep at the switch.

Making matters worse, the proliferation of the Internet, smart phones, and social media, has forced investors to digest a never-ending avalanche of breaking news headlines and fear mongering. Here is a partial list of the items currently frightening investors:

- Interest Rates: Will the Federal Reserve raise interest rates in June or September?

- Volatility: The Dow is up 200 points one day and then down 200 the next day. Keep me away.

- Greece: One day Greece is going to exit the eurozone and the next day it’s going to reach a deal with the IMF (International Monetary Fund) and European leaders.

- Terrorism / Middle East: ISIS is like a cancer taking over the Middle East, and it’s only a matter of time before they invade our home soil. And if ISIS doesn’t get us, then the Iranian boogeyman will attack us with their inevitable nuclear weapons.

- Inflation: The economy is slowing improving and as we approach full employment in the U.S., wage pressure is about to kick inflation into high gear. After falling significantly, oil prices are inching higher, which is also moving inflation in the wrong direction.

- Strong Dollar: Now that Europe is copying the U.S. by implementing quantitative easing, domestic exports are getting squeezed and revenue growth is slowing.

- Bubble? Stocks have had a monster run over the last six years, so we must be due for a crash…correct?

Seemingly, on a daily basis, some economist, strategist, analyst, or talking head pundit on TV articulately explains how the financial markets can fall off the face of the earth. Unfortunately, there is a problem with this type of analysis, if your evaluation is solely based upon listening to media outlets. Bottom line is you can always find a reason to sell your investments if you listen to the so-called experts. I made this precise point a few years ago when I highlighted the near tripling in stock prices despite the barrage of bad news (see also A Series of Unfortunate Events).

While I am certainly not asking anyone to blindly assume more risk, especially after such a large run-up in stock prices, I find it just as important to point out the following:

“Taking too much risk is as risky as not taking enough risk.”

In other words, driving 35 mph on the freeway may be more life threatening than driving 75 mph. In the world of investing, driving too slowly by putting all your savings in cash or low-yielding securities, as many Americans do, may feel safe. However this default strategy, which may feel comfortable for many, may actually make attaining your financial goals impossible.

At Sidoxia, we create customized Investment Policy Statements (IPS) for all our clients in an effort to optimize risk levels in a Goldilocks fashion…not too hot, and not too cold. Retirement is supposed to be relaxing and stress free. Do yourself a favor and create a disciplined and systematic investment plan. Being apathetic due to an infinite stream of worrisome sounding headlines may work in the short-run, but in the long-run it’s best to turn off the noise…unless of course you don’t give a &$#*@%^ and want to work as a greeter at Wal-Mart in your mid-80s.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and WMT, but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on ICContact page.

Inflating Dollars & Deflating Footballs

This article is an excerpt from a previously released Sidoxia Capital Management complementary newsletter (February 2, 2015). Subscribe on the right side of the page for the complete text.

In the weeks building up to Super Bowl XLIX (New England Patriots vs. Seattle Seahawks) much of the media hype was focused on the controversial alleged “Deflategate”, or the discovery of deflated Patriot footballs, which theoretically could have been used for an unfair advantage by New England’s quarterback Tom Brady. While Brady ended up winning his record-tying 4th Super Bowl ring for the Patriots by defeating the Seahawks 28-24, the stock market deflated during the first month of 2015 as well. Similar to last year, the stock market has temporarily declined last January before surging ahead +11.4% for the full year of 2014. It’s early in 2015, and investors chose to lock-in a small portion of the hefty, multi-year bull market gains. The S&P 500 was sacked for a loss of -3.1% and the Dow Jones Industrial index by -3.7%.

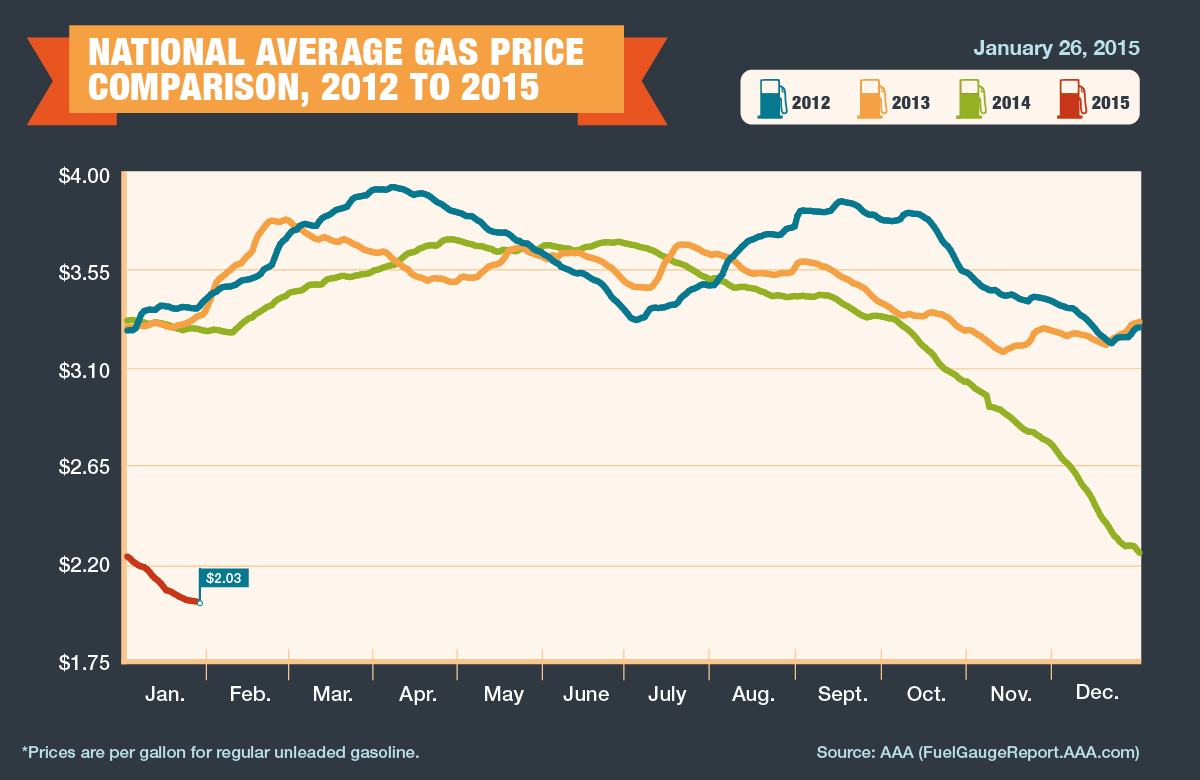

Despite some early performance headwinds, the U.S. economy kicked off the year with the wind behind its back in the form of deflating oil prices. Specifically, West Texas Intermediate (WTI) crude oil prices declined -9.4% last month to $48.24, and over -51.0% over the last six months. Like a fresh set of substitute legs coming off the bench to support the team, the oil price decline represents an effective $125 billion tax cut for consumers in the form of lower gasoline prices (average $2.03 per gallon nationally) – see chart below. The gasoline relief will allow consumers more discretionary spending money, so football fans, for example, can buy more hot dogs, beer, and souvenirs at the Super Bowl. The cause for the recent price bust? The primary reasons are three-fold: 1) Sluggish oil demand from developed markets like Europe and Japan coupled with slowing consumption growth in some emerging markets like China; 2) Growing supply in various U.S. fracking regions has created a temporary global oil glut; and 3) Uncertainty surrounding OPEC (Organization of Petroleum Exporting Countries) supply/production policies, which became even more unclear with the recent announced death of Saudi Arabia’s King Abdullah.

Source: AAA

More deflating than the NFL football’s “Deflategate” is the approximate -17% collapse in the value of the euro currency (see chart below). Euro currency matters were made worse in response to European Central Bank’s (ECB) President Mario Draghi’s announcement that the eurozone would commence its own $67 billion monthly Quantitative Easing (QE) program (very similar to the QE program that Federal Reserve Chairwoman Janet Yellen halted last year). In total, if carried out to its full design, the euro QE version should amount to about $1.3 trillion. The depreciating effect on the euro (and appreciating value of the euro) should help stimulate European exports, while lowering the cost of U.S. imports – you may now be able to afford that new Rolls-Royce purchase you’ve been putting off. What’s more, the rising dollar is beneficial for Americans who are planning to vacation abroad…Paris here we come!

Source: XE.com

Another fumble suffered by the global currency markets was introduced with the unexpected announcement by the Swiss National Bank (SNB) that decided to remove its artificial currency peg to the euro. Effectively, the SNB had been purchased and accumulated a $490 billion war-chest reserve (Supply & Demand Lessons) to artificially depress the value of the Swiss franc, thereby allowing the country to sell more Swiss army knives and watches abroad. When the SNB could no longer afford to prop up the value of the franc, the currency value spiked +20% against the euro in a single day…ouch! In addition to making its exports more expensive for foreigners, the central bank’s move also pushed long-term Swiss Treasury bond yields negative. No, you don’t need to check your vision – investors are indeed paying Switzerland to hold investor money (i.e., interest rates are at an unprecedented negative level).

In addition to some of the previously mentioned setbacks, financial markets suffered another penalty flag. Last month, multiple deadly terrorist acts were carried out at a satirical magazine headquarters and a Jewish supermarket – both in Paris. Combined, there were 16 people who lost their lives in these senseless acts of violence. Unfortunately, we don’t live in a Utopian world, so with seven billion people in this world there will continue to be pointless incidences like these. However, the good news is the economic game always goes on in spite of terrorism.

As is always the case, there will always be concerns in the marketplace, whether it is worries about inflation, geopolitics, the economy, Federal Reserve policy, or other factors like a potential exit of Greece out of the eurozone. These concerns have remained in place over the last six years and the stock market has about tripled. The fact remains that interest rates are at a generational low (see also Stretching the High Yield Rubber Band), thereby supplying a scarcity of opportunities in the fixed income space. Diversification remains important, but regardless of your time horizon and risk tolerance, attractively valued equities, including high-quality, dividend-paying stocks should account for a certain portion of your portfolio. Any winning retirement playbook understands a low-cost, globally diversified portfolio, integrating a broad set of asset classes is the best way of preventing a “deflating” outcome in your long-term finances.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Playing Whack-A-Mole with the Pros

Source: Flickr

Deciphering the ups and the downs of the financial markets is a lot like playing a game of Whack-A-Mole. First the market is up 300 points, then down 300 points. Next Greece and Europe are going down the drain, and then Germany and the ECB (European Central Bank) are here to save the day. The daily data points are a rapid moving target, and if history continues to serve as a guide (see History Often Rhymes with the Future), the bobbing consensus views of pundits will continue to get hammered by investors’ mallets.

Let’s take a look at recent history to see who has been the “whack-er” and whom has been the “whack-ee.” Whether it was the gloom and doom consensus view in the early 1980s (reference BusinessWeek’s 1979 front page “The Death of Equities”) or the euphoric championing of tech stocks in the 1990s (see Money magazine’s March 2000 cover, “The Hottest Market Ever”), the consensus view was wrong then, and is likely wrong again today.

Here are some of the fresher consensus views that have popped up and then gotten beaten down:

End of QE2 – The Consensus: If you rewind the clock back to June 2011 when the Federal Reserve’s $600 billion QE2 (Quantitative Easing Part II) monetary stimulus program was coming to an end, a majority of pundits expected bond prices to tank in the absence of the Fed’s Ben Bernanke’s checkbook support. Before the end of QE2, Reuters financial service surveyed 64 professionals, and a substantial majority predicted bond prices would tank and interest rates would catapult upwards. Actual Result: The pundits were wrong and rates did not go up, they in fact went down. As a result, bond prices screamed higher – bond values increased significantly as 10-year Treasury yields fell from 3.16% to a low of 1.72% last week.

Debt Ceiling Debate – The Consensus: Just one month later, Democrats and Republicans were playing a game of political “chicken” in the process of raising the debt ceiling to over $16 trillion. Bill Gross, bond guru and CEO of fixed income giant PIMCO, was one of the many pros who earlier this year sold Treasuries in droves because fears of bond vigilantes shredding prices of U.S. Treasury bonds .

Here was the prevalent thought process at the time: Profligate spending by irresponsible bureaucrats in Washington if not curtailed dramatically would cascade into a disaster, which would lead to higher default risk, cancerous inflation, and exploding interest rates ala Greece. Actual Result: Once again, the pundits were proved wrong in the deciphering of their cloudy crystal balls. Interest rates did not rise, they actually fell. As a result, bond prices screamed higher and 10-year Treasury yields dived from 2.74% to the recent low of 1.72%.

S&P Credit Downgrade – The Consensus: The S&P credit rating agency warned Washington that a failure to come to meaningful consensus on deficit and debt reduction would result in bitter consequences. Despite a $2 trillion error made by S&P, the agency kept its word and downgraded the U.S.’s long-term debt rating to AA+ from AAA. Research from JP Morgan (JPM) cautioned investors of the imminent punishment to be placed on $4 trillion in Treasury collateral, which could lead to a seizing in credit markets. Actual Result: Rather than becoming the ugly stepchild, U.S. Treasuries became a global safe-haven for investors around the world to pile into. Not only did bond prices steadily climb (and yields decline), but the value of our currency as measured by the Dollar Index (DXY) has risen significantly since then.

Dollar Index (DXY) Source: Bloomberg

What is next? Nobody knows for certain. In the meantime, grab some cotton candy, popcorn, and a rubber mallet. There is never a shortage of confident mole-like experts popping up on TV, newspapers, blogs, and radio. So when the deafening noise about the inevitable collapse of Europe and the global economy comes roaring in, make sure you are the one holding the mallet and not the mole getting whacked on the head.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in JPM, MHP, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Money Goes Where Treated Best

“The world is going to hell in a handbasket” seems to be a prevailing sentiment among many investors. Looking back, a lack of fiscal leadership in Washington, coupled with historically high unemployment, has only fanned the flames of restlessness. A day can hardly go by without hearing about some fiscal problem occurring somewhere around the globe. Geographies have ranged from Iceland to Dubai, and California to Greece. Regardless, eventually voters force politicians to take notice, as we recently experienced in the Massachusetts vote for Senator.

Time to Panic?

So is now the time to panic? Entitlement obligations such as Social Security and Medicare, when matched with a rising interest payment burden from our ballooning debt, stands to consume the vast majority of our country’s revenues in the coming decades (if changes are not made). It’s clear to most that the current debt trajectory is not sustainable – see also Debt: The New Four-Letter Word. With that said, historical debt levels have actually been at higher levels before. For example, during World War II, debt levels reached 122% of GDP (Gross Domestic Product). Since promises generally garner votes, politicians have traditionally found it easier to legislate new spending into law rather than cutting back existing spending and benefits.

Money Goes Where it’s Treated Best

If our government leaders choose to ignore the growing upswell in fiscal discontent, then the global financial markets will pay more attention and disapprove less diplomatically. As the globe’s reserve currency, the U.S. Dollar stands to collapse if a different direction is not forged, and interest costs could skyrocket to unpalatable levels. Fortunately, the flat world we live on has created some of these naturally occurring governors to forcibly direct sovereign entities to make better decisions…or suffer the consequences. Right now Greece is paying for the financial sins of its past, which includes widening deficits and untenable debt levels.

As new, growing powers such as China, Brazil, India, and other emerging countries fight for precious capital to feed the aspirational goals of their rising middle classes, money will migrate to where it is treated best. Speculative money will flow in and out of various capital markets in the short-run, but ultimately capital flows where it is treated best. Meaning, those countries with policies fostering fiscal conservatism, financial transparency, prudent regulations, pro-growth initiatives, tax incentives, order of law, and other capital-friendly guidelines will enjoy their fair share of the spoils. The New York Times editorial journalist Tom Friedman coined the term “golden straitjacket” in describing this naturally occurring restraint system as a result of globalization.

Push Comes to Shove

Push will eventually come to shove, but the real question is whether we will self-impose fiscal restraint on ourselves, or will the global capital markets shove us in that direction, like the markets are doing to Greece (and other financially strapped nations) today? I am hopeful it will be the former. Why am I optimistic? Although more government spending has typically lead to more votes for politicians, cracks in the support wall have surfaced through the Massachusetts Senatorial vote, and rising populist sentiment, as manifested through the “Tea Party” movement (previously considered a fringe group).

Political gridlock has traditionally been par for the course, but crisis usually leads to action, so I eventually expect change. I am banking on the poisonous and sour mood permeating through the country’s voter base, in conjunction with the collapse of foreign currencies, to act as a catalyst for financial reform. If not, resident capital and domestic jobs will exodus to other countries, where they will be treated best.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including emerging market-based ETFs), but at time of publishing had no direct positions in securities mentioned in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Timothy Geithner, the Eddie Haskell Dollar Czar

Treasury Secretary Timothy Geithner recently stated after a meeting of G-7 financial officials that “it is very important to the United States that we continue to have a strong dollar.”

With comments like this, why does Timothy Geithner remind me so much of Eddie Haskell (played by Ken Osmond) from the 1950s suburban sitcom Leave It to Beaver? Eddie Haskell plays the scheming trouble maker who is extremely polite on the exterior around adults, but reverts to a crafty conniver once the grown-ups leave the room.

I can just picture the conversations between Treasury Secretary Geithner and President Obama before a high powered meeting with Chinese administration officials:

Geithner: “Barack, the skyrocketing debt will be no problem, we can we shovel plenty of this paper on these Chinese.”

Barack: “Uh, oh…Hu is here for our meeting.”

Geithner: “Oh hello Mr. President Jintao – what a lovely trade surplus you have. We look forward to keeping a very fiscally responsible agenda here in the United States, so you can keep buying our valuable debt.”

Where did Timothy Haskell get his crafty dollar oration skills?

According to David Malpass, president of the research firm Encima Global and deputy assistant Treasury Secretary, Geithner training came from “using a code phrase, a carryover from the Bush administration. It means that the U.S. approves of a constantly weakening dollar but doesn’t want a disruptive collapse.”

These tactics and rhetoric can only work for so long. Exploding deficits and skyrocketing debt levels will eventually lead to a dumping of our debt, rising interest rates, crowding-out of private investments, and a damaging decline in the dollar. Sure, the weakening dollar helps us in the short-run with exports but eventually major U.S. debtholders will no longer buy our sweet talking.

With all the “U.S. dollar is going to collapse” talk, one would think a shift to an SDR (Special Drawing Rights) global currency structure is an inevitable outcome. Just six months ago the governor of China’s central bank argued the U.S. dollar’s role as the world’s reserve currency should be restructured. The SDR model has already been implemented by the IMF (International Monetary Fund), so if the Chinese wanted to create an SDR proxy, they could easily purchase euros, sterling, and yen in proper proportions. Would the Chinese want to make any sudden changes? Certainly not, because any quick adjustments would destroy the value of the Chinese’s existing dollar denominated portfolio. The logistics surrounding a legitimate SDR program would require the IMF or some other international agency to act as a global central bank, which would not only need to determine the appropriate mix of currencies in the SDR, but also decide future global liquidity actions. In order to legitimately run a new SDR program, countries like China would need to give up sovereignty – not a likely scenario.

Until a new SDR regime is agreed upon, dollar-reliant countries will continue to have barks bigger than their bites and Timothy Geithner Haskell will continue to sweet talk U.S. dollar owners.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

Hear Eddie (or Treasury Secretary) Speak Here:

{kind=link}