Posts tagged ‘Treasury yields’

What Do You Worry About Next?

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (November 1, 2016). Subscribe on the right side of the page for the complete text.

Boo! Halloween has just passed and frightened investors have still survived to tell the tale in 2016. While most people have gotten spooked by the presidential election, other factors like record-high corporate profits, record-low interest rates, and reasonable valuations have led to annual stock market gains. More specifically, values have risen in 2016 by approximately +4% (or +6% including dividend payments). Despite last week’s accelerating 3rd quarter GDP economic growth figure of +2.9%, which was the highest rate in two years and more than doubled the rate of the previous quarter (up +1.4%), there were still more tricks than treats during October. Recently, scary politics have shocked many Halloween participants into a zombie-like state, as evidenced by stock values declining around -1.7% during October.

This recent volatility is nothing new. Even though financial markets are significantly higher in recent years, that has not prevented repeated corrections over the year(s) as shown below in the 2009 – 2015 chart.

In order to earn higher long-term returns, investors have to accept a certain amount of short-term price movements (upwards and downwards). With a couple months remaining in the year, stock investors have achieved gains through a tremendous amount of economic and geopolitical uncertainty, including the following scares:

- China: A significant fallout from a Chinese slowdown at the beginning of the year (stocks fell about -14%).

- Brexit: A 48-hour Brexit vote scare in June (stocks fell -6%).

- Fed Fears: Threatening comments in September from the Federal Reserve about potentially hiking increasing interest rates (stocks fell -4%).

With the elections just a week away, political anxiety has jolted Americans’ adrenaline levels. The polls continue to move up and down, but as I have repeatedly pointed out, the only certain winner in Washington DC is gridlock. Sure, in a Utopian world, politicians should join hands and compromise to solve all our country’s serious problems. Unfortunately, this is not the case (see Congress’s approval rating). However, there is a silver lining to this dysfunction…gridlock can lead to fiscal discipline.

Our country’s debt/deficit financial situation has been spiraling out of control, in large measure due to rapidly rising entitlement spending, including Medicare, and Social Security. Witnessing all the political rhetoric and in-fighting is very difficult, but as I highlighted in last month’s newsletter, gridlock has flattened the spending curve significantly since 2009 – a positive development.

And although the economic recovery has been one of the slowest since World War II and global growth remains anemic, the U.S. remains a better house in a bad global neighborhood (e.g., Europe and Japan continue to suck wind), as evidenced by a number of these following positive economic indicators:

- Employment Improvement: Unemployment has fallen from 10% to 5% since 2009, and more than 15 million jobs have been added over that period.

- Housing Recovery Continues: Home sales and prices continue their multi-year rise; housing inventories remain tight; and affordability remains strong, given generationally low interest rates.

- Record Auto Sales: Car sales remain near record levels, hovering around 17 million units per year.

- Consumer Confidence on the Rise: Ever since the financial crisis, consumer sentiment figures have rebounded by about 50%.

-

Record Consumer Sales: Consumer spending accounts for approximately 70% of our economy, and as you can see from the chart below, despite consumers saving more, stronger employment and wages are fueling more spending.

Source:Calculated Risk

Source:Calculated Risk

Absent a clean sweep of control by the Democrat or Republican Presidential-Congressional candidates, our democratic system will retain its healthy status of checks and balances. Based on all the current polling data, a split between the White House, Senate, and House of Representatives remains a very high likelihood scenario.

The political process has been especially exhausting during the current cycle, but regardless of whether your candidate wins or loses, much of the current uncertainty will likely dissipate. As the saying goes, at least it is “Better the devil you know than the devil you don’t know.”

After the November 8th elections are completed, there will be one less election to worry about. Thankfully, after 25 years in the industry, I’m not naïve enough to believe there will be nothing else to worry about. When the financial media and blogosphere get bored, at a minimum, you can guarantee yourself plenty of useless coverage regarding the next monetary policy move by the Federal Reserve (see also Fed Fatigue).

Whatever the next set of worries become, U.K. Prime Minister Winston Churchill said it best as it relates to American politics and economics, “You can always count on Americans to do the right thing – after they’ve tried everything else.” If Churchill’s words don’t provide comfort and you had fun getting spooked over the elections on Halloween, feel free to keep wearing your costume. Behind any constructive economic data, the prolific media machine will continue doing their best in manufacturing plenty of fear, uncertainty, and doubt to keep you worried.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Fall is Here: Change is Near

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (October 1, 2016). Subscribe on the right side of the page for the complete text.

Although the fall season is here and the leaf colors are changing, there are a number of other transforming dynamics occurring this economic season as well. The S&P 500 index may not have changed much this past month (down -0.1%), but the technology-laden NASDAQ index catapulted higher (+1.9% for the month and +6.0% for 2016).

With three quarters of the year now behind us, beyond experiencing a shift in seasonal weather, a number of other changes are also coming. For starters, there’s no ignoring the elephant in the room, and that is the presidential election, which is only weeks away from determining our country’s new Commander in Chief. Besides religion, there are very few topics more emotionally charged than politics – whether you are a Republican, Democrat, Independent, Libertarian, or some combination thereof. Even though the first presidential debate is behind us, a majority of voters are already set on their candidate choice. In other words, open-minded debate on this topic can be challenging.

Hearing critical comments regarding your favorite candidate are often interpreted in the same manner as receiving critical comments about a personal family member – people often become defensive. The good news, despite the massive political divide currently occurring in the country and near-record low politician approval ratings in Congress , politics mean almost nothing when it comes to your money and retirement (see also Politics & Your Money). Regardless of what politicians might accomplish (not much), individuals actually have much more control over their personal financial future than politicians.

While inaction may rule the day currently, more action generally occurs during a crisis – we witnessed this firsthand during the 2008-2009 financial meltdown. As Winston Churchill famously stated,

“You can always count on Americans to do the right thing – after they’ve tried everything else.”

Political discourse and gridlock are frustrating to almost everyone from a practical standpoint (i.e., “Why can’t these idiots get something done in Washington?!”), however from an economic standpoint, gridlock is good (see also Who Said Gridlock is Bad?) because it can keep a responsible lid on frivolous spending. Educated individuals can debate about the proper priorities of government spending, but most voters agree, maintaining a sensible level of spending and debt should be a bipartisan issue.

From roughly 2009 – 2014, you can see how political gridlock has led to a massive narrowing in our government’s deficit levels (chart below) – back to more historical levels.This occurred just as rising frustration with Washington has been on the rise.

The Fed: Rate Revolution or Evolution?

Besides the changing season of politics, the other major area of change is Federal Reserve monetary policy. Even though the Fed has only increased interest rates once over the last 10 years, and interest rates are at near-generational lows, investors remain fearful. There is bound to be some short-term volatility if interest rates rise to 0.50% – 0.75% in December, as currently expected. However, if the Fed continues at its current snail’s pace, it won’t be until 2032 before they complete their rate hike cycles.

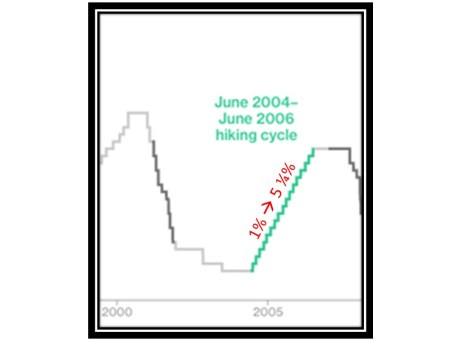

We can put the next rate increase into perspective by studying history. More specifically, the Fed raised interest rates 17 times from 2004 – 2006 (see chart below). Fortunately over this same time period, the world didn’t end as the Fed increased interest rates from 1.00% to 5.25% (stocks prices actually rose around +11%). The same can be said today – the world won’t likely end, if interest rates rise from 0.50% to 0.75% in a few months.

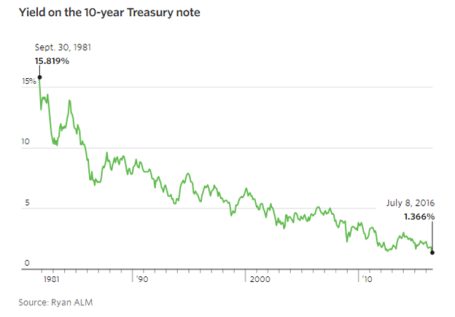

The next question becomes, why are interest rates so low? There are many reasons and theories, but a few of the key drivers behind low rates include, slower global economic growth, low inflation, high demand for low-risk assets, technology, and demographics. I could devote a whole article to each of these factors, and indeed in many cases I have, but suffice it to say that there are many reasons beyond the oversimplified explanation that artificial central bank intervention has led to a 35 year decline in interest rates (see chart below).

Change is a constant, and with fall arriving, some changes are more predictable than others. The timing of the U.S. presidential election outcome is very predictable but the same cannot be said for the timing of future interest rate increases. Irrespective of the coming changes and the related timing, history reminds us that concerns over politics and interest rates often are overblown. Many individuals remain overly-pessimistic due to excessive, daily attention to gloomy and irrelevant news headlines. Thankfully, stock prices are paying attention to more important factors (see Don’t Be a Fool) and long-term investors are being rewarded with record high stock prices in recent weeks. That’s the type of change I love.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

March Madness – Dividend Grandness & Volatility Blandness

March Madness has arrived once again. This NCAA basketball event, which has been around since 1939, begins with a selection committee choosing the top 68 teams in the country. These teams are matched up against each other through a single-elimination tournament until a national champion is throned. The stock market does not have a selection committee that picks teams from conferences like the SEC, Big East, Pac-12, and ACC, but rather millions of investors select the best investments from asset classes like stocks, bonds, real estate, commodities, venture capital, and private equity.

In the investment world, there are no win-loss records, but rather there are risk-return profiles. Investors generally migrate towards the asset classes where they find the optimal trade-off between risk and return. Speculators, day-traders, and momentum traders may define risk differently, but regardless, over the long-run, capital goes where it is treated best. And over the last six years, the U.S. stock market hasn’t been a bad place to be (the S&P 500 has about tripled).

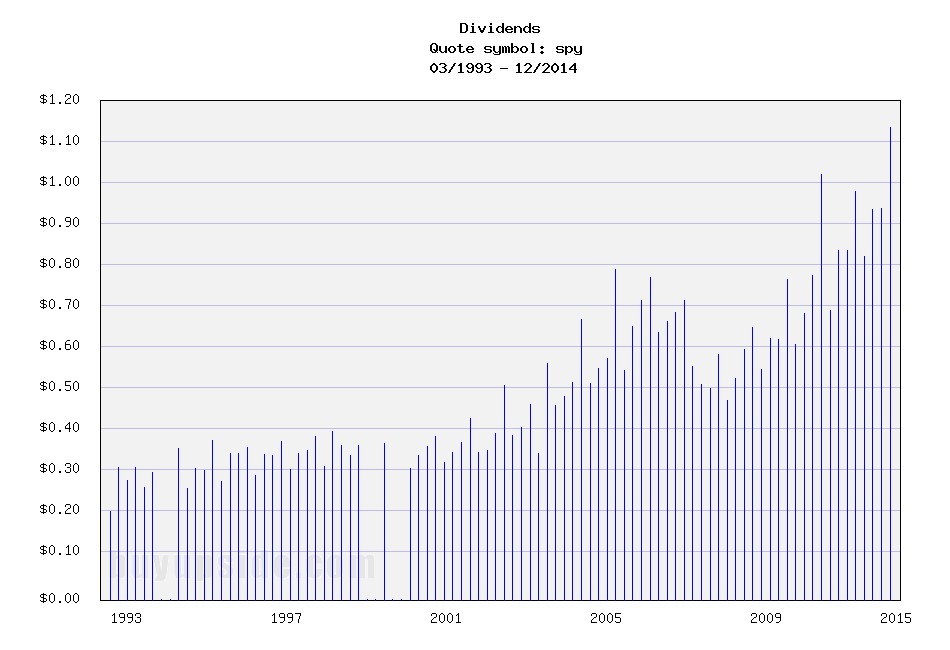

Why such outperformance in stocks? Besides a dynamic earnings recovery from the 2008-2009 financial crisis, another major factor has been the near-0% interest rate environment. When investors are earning near nothing in their bank and savings accounts, it is perfectly rational for savers to look for riskier options, if they are compensated for that risk. In addition to loose central bank and quantitative easing policies fueling demand for stocks, rising dividends have increased the attractiveness of the stock market. In fact, as you can see from the chart below, dividends have about doubled from 2008-2009 and about tripled from the year 2000.

Source: Buy Upside

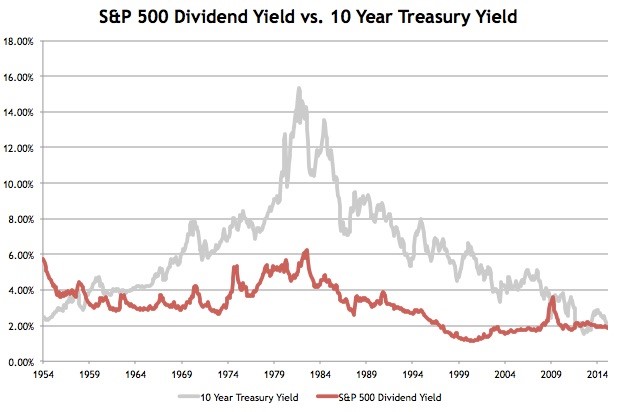

Stock prices have moved higher in concert with rising dividends, which, as you can see from the chart below, has kept the dividend yield flat at around 2% over the last few years. Treasury bond yields, on the other hand, have been on steady declining trend for the last 35 years. So, while coupons on newly issued bonds have been declining for virtually the last three and a half decades, stock dividends have been on a steadily upward moving rampage, excluding recessions (up +13% in the most recent reported period).

Source: Avondale Asset Management

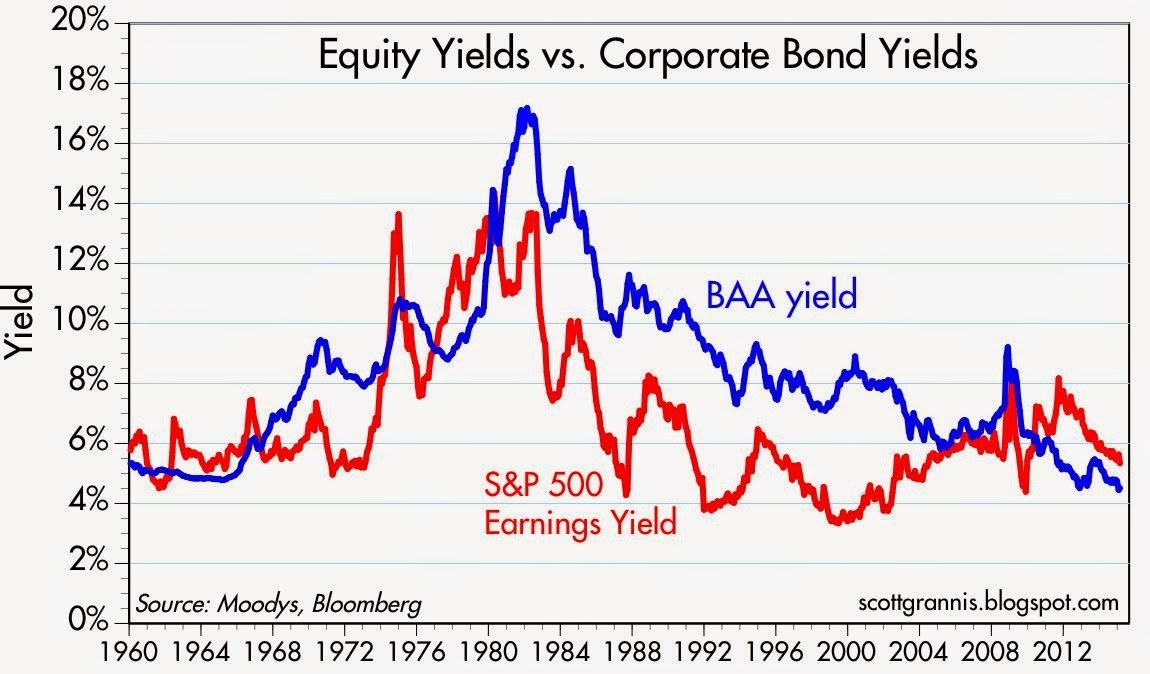

Declining interest rates have made stocks look attractive relative to investment grade corporate bonds too as evidenced by the chart below. As you can see, over the last half-century, corporate bond yields have predominantly offered higher income yields than the earnings yield on stocks – that is not the case today.

Source: Calafia Beach Pundit

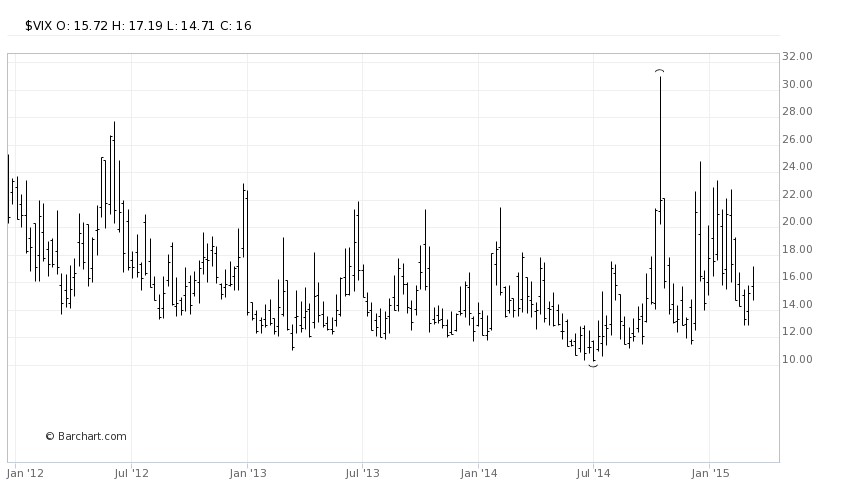

What does all this stock dividend, earnings yield stuff mean? In the grand scheme of things, income starving Baby Boomers and retirees are slowly realizing that stocks in general stack up favorably in an environment in which interest payments are going down and dividend payments are going up. One of the areas highlighting the underlying demand for stocks is the Volatility Index (VIX) – a.k.a., the “Fear Gauge.” Despite Greece, Russia, ISIS, the Fed, and the Dollar dominating the headlines, the hunger for yield and growth in a declining interest rate environment is cushioning the blow during these heightened periods of volatility (see also A Series of Unfortunate Events).

Since the end of 2011, the monthly close of the VIX has stayed above its historical average of approximately 20 only two times (see chart below). In other words, over that timeframe, the VIX has remained below average about 95% of the time. When the VIX has spiked above 20, generally it has only been for brief periods, until cooler heads prevail and bargain hunters come in to buy depressed stock bargains.

Source: Barchart

I’m not naïve enough to believe the bull market in stocks will last forever, but as long as interest rates don’t spike up and/or corporate earnings crater, underlying demand for yield should provide a floor for stocks during heightened periods of volatility. We may be in the midst of March Madness but volatility blandness is showing us that investors are paying attention to dividend grandness.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and SPY, but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}