Posts tagged ‘sequestration’

Ignoring Economics and Vital Signs

As stock prices sit near all-time record highs, and as we enter year nine of the current bull market, I remain amazed and amused at the brazen disregard for important basic economic concepts like supply & demand, interest rates, and rising profits.

If the stock market was a doctor’s patient, over the last decade, bloggers, pundits, talking heads, and pontificators have been ignoring the improving, healthy patient’s vital signs, while endlessly predicting the death of the resilient stock market.

However, let’s be clear – it has not been all hearts and flowers for stocks – there have been numerous -10%, -15%, and -20% corrections since the Financial Crisis nine years ago. Those corrections included the Flash Crash, debt downgrade, Arab Spring, sequestration, Taper Tantrum, Iranian Nuclear Threat, Ukrainian-Crimea annexation, Ebola, Paris/San Bernardino Terrorist Attacks, multiple European & Chinese slowdowns and more.

Despite the avalanche of headlines and volatility, we all know the net result of these events – a more than tripling of stock prices (+259%) from March 2009 to new all-time record highs. With the incessant stream of negative news, how could prices appreciate so dramatically?

Over the years, the explanations by outside observers have changed. First, the recovery was explained as a “dead cat bounce” or a short-term cyclical bull market within a long-term secular bear market. Then, when stock prices broke to new records, the focus shifted to Quantitative Easing (QE1, QE2, QE3, and Operation Twist). The QE narrative implied the bull advance was temporary due to the non-stop, artificial printing presses of the Fed. Now that the Fed has not only ended QE but reversed it (the Fed is actually contracting its balance sheet) and hiked interest rates (no longer cutting), outsiders are once again at a loss. Now, the bears are left clinging to the flawed CAPE metric I wrote about three years ago (see CAPE Smells Like BS), and using political headlines as a theory for record prices (i.e., record stock prices stem from inflated tax cut and infrastructure spending expectations).

It’s unfortunate for the bears that all the conspiracy theory headlines and F.U.D. (fear, uncertainty, and doubt) over the last 10 years have failed miserably as predictors for stock prices. The truth is that stock prices don’t care about headlines – stock prices care about economics. More specifically, stock prices care about profits, interest rates, and supply & demand.

Profits

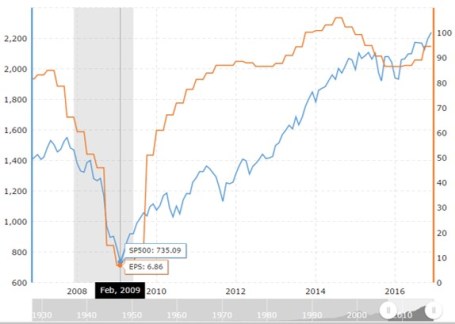

It’s quite simple. Stock prices have more than tripled since early 2009 because profits have more than tripled since 2009. As you can see from the Macrotrends chart below, 2009 – 2016 profits for the S&P 500 index rose from $6.86 to $94.54, or +1,287%. It’s no surprise either that stock prices stalled for 18 months from 2015 to mid-2016 when profits slowed. After profits returned to growth, stock price appreciation also resumed.

Source: Macrotrends

Interest Rates

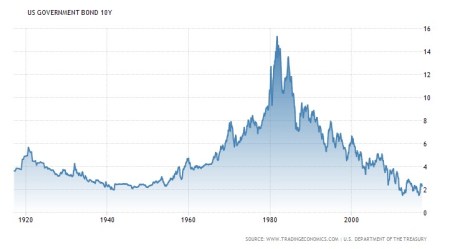

When you could earn a +16% on a guaranteed CD bank rate in the early 1980s, do you think stocks were a more or less attractive asset class? If you can sense the rhetorical nature of my question, then you can probably understand why stocks were about as attractive as rotten milk or moldy bread. Back then, stocks traded for about 8x’s earnings vs. the 18x-20x multiples today. The difference is, today interest rates are near generational lows (see chart below), and CDs pay near +0%, thereby making stocks much more attractive. If you think this type of talk is heresy, ignore me and listen to the greatest investor of all-time, Warren Buffett who recently stated:

“Measured against interest rates, stocks are actually on the cheap side.”

Source: Trading Economics

Supply & Demand

Another massively ignored area, as it relates to the health of stock prices, is the relationship of new stock supply entering the market (e.g., new dilutive shares via IPOs and follow-on offerings), versus stock exiting the market through corporate actions. While there has been some coverage placed on the corporate action of share buybacks – about a half trillion dollars of stock being sucked up like a vacuum cleaner by cash heavy companies like Apple Inc. (AAPL) – little attention has been paid to the trillions of dollars of stock vanishing from mergers and acquisition activities. Yes, Snap Inc. (SNAP) has garnered a disproportionate amount of attention for its $3 billion IPO (Initial Public Offering), this is a drop in the bucket compared to the exodus of stock from M&A activity. Consider the trivial amount of SNAP supply entering the market ($3 billion) vs. $100s of billions in major deals announced in 2016 – 2017:

- Time Warner Inc. merger offer by AT&T Inc. (T) for $85 billion

- Monsanto Co. merger offer by Bayer AG (BAYRY) for $66 billion

- Reynolds American Inc. merger offer by British American Tobacco (BTI) for $47 billion

- NXP Semiconductors merger offer by Qualcomm Inc. (QCOM) for $39 billion

- LinkedIn merger offer by Microsoft Corp. (MSFT) for $28 billion

- Jude Medical, Inc. merger offer by Abbott Laboratories (ABT) for $25 billion

- Mead Johnson Nutrition merger offer by Reckitt Benckiser Group for $18 billion

- Mobileye merger offer by Intel Corp. (INTC) for $15 billion

- Netsuite merger offer by Oracle Corp. (ORCL) for $9 billion

- Kate Spade & Co. merger offer by Coach Inc. (COH) for $2 billion

While these few handfuls of deals represent over $300 billion in disappearing stock, as long as corporate profits remain strong, interest rates low, and valuations reasonable, there will likely continue to be trillions of dollars in stocks being purchased by corporations. This continued vigorous M&A activity should provide further healthy support to stock prices.

Admittedly, there will come a time when profits will collapse, interest rates will spike, valuations will get stretched, sentiment will become euphoric, and/or supply of stock will flood the market (see Don’t be a Fool, Follow the Stool). When the balance of these factors turn negative, the risk profile for stock prices will obviously become less desirable. Until then, I will let the skeptics and bears ignore the healthy economic vital signs and call for the death of a healthy patient (stock market). In the meantime, I will continue focus on the basics of math and offer my economics textbook to the doubters.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own AAPL, ABT, INTC, MSFT, T, and certain exchange traded funds, but at the time of publishing SCM had no direct position in SNAP, TWX, MON, KATE, N, MBLY, MJN, STJ, LNKD, NXPI, BAYRY, BTI, QCOM, ORCL, COH, RAI, Reckitt Benckiser Group, any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Out of the Woods?

In the middle of the 24/7 news cycle, many investors get distracted by the headline du jour, much like a baby gets distracted by a shiny new object. While investor moods have been swinging violently back and forth, October’s performance has bounced back like a flying tennis ball. So far, the reversal in the S&P 500 performance has more than erased the -9% correction occurring in August and September. Could we finally be out of the woods, or will geopolitics and economic factors scare investors through Halloween and year-end?

Given recent catapulting stock prices, investor amnesia has erased the shear horror experienced over the last few months – this is nothing new for emotional stock market participants. As I wrote in Controlling the Lizard Brain, human brains have evolved the almond-shaped tissue in our brains (amygdala) that controlled our ancestors’ urge to flee ferocious lions. Today the urge is to flee scary geopolitical and economic headlines.

I expanded on the idea here:

“When the brain in functioning properly, the prefrontal cortex (the front part of the brain in charge of reasoning) is actively communicating with the amygdala. Sadly, for many people, and investors, the emotional response from the amygdala dominates the rational reasoning portion of the prefrontal cortex. The best investors and traders have developed the ability of separating emotions from rational decision making, by keeping the amygdala in check.”

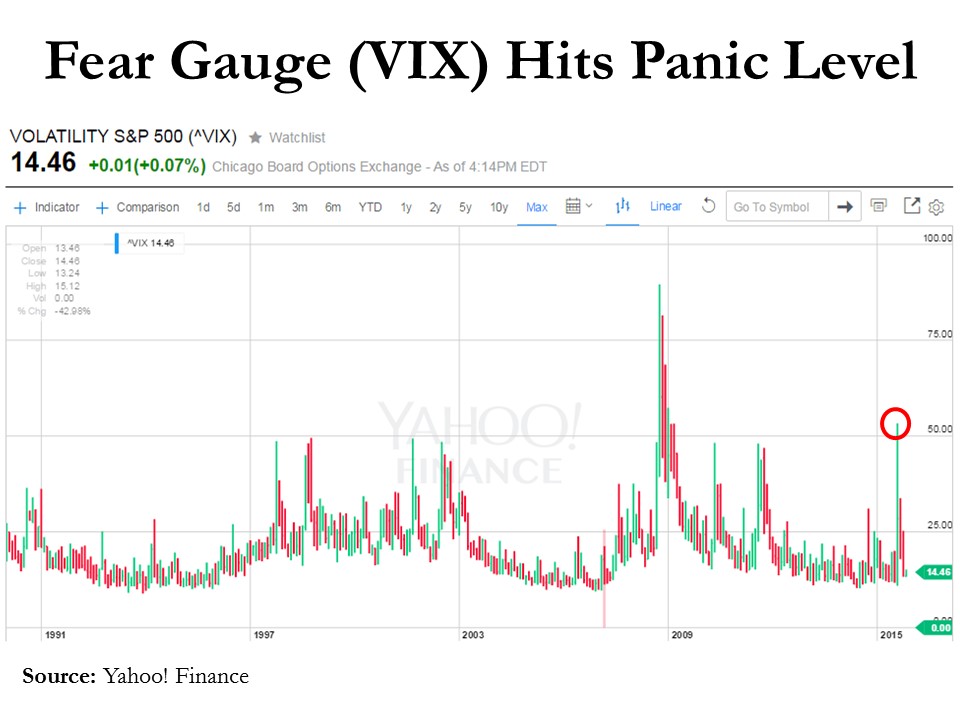

Evidence of lizard brains fear for flight happened just two months ago when the so-called “Fear Gauge” (VIX – Volatility Index) hit a stratospherically frightening level of 53 (see chart below), reached only once over the last few decades (2008-09 Financial Crisis).

Just as quickly as slowing China growth and a potential Fed interest rate hike caused investors to crawl underneath their desks during August (down –11% in four days), while biting their fingernails, investors have now sprung outside to the warm sunshine. The end result has been an impressive, mirror-like +11% increase in stock prices (S&P 500) over the last 18 trading days.

Has anything really changed over the last few weeks? Probably not. Economists, strategists, analysts, and other faux-soothsayers get paid millions of dollars in a fruitless attempt to explain day-to-day (or hour-by-hour) volatility in the stock markets. One Nobel Prize winner, Paul Samuelson, understood the random nature of stock prices when he observed, “The stock market has forecast nine of the last five recessions.” The pundits are no better at consistently forecasting stock prices.

As I have reiterated many times before, the vast majority of the pundits do not manage money professionally – the only people you should be paying attention to are successful long-term investors. Even listening to veteran professional investors can be dangerous because there is often such a wide dispersion of opinions based on varying time horizons, strategies, and risk tolerances.

Skepticism remains rampant regarding the sustainability of the bull market as demonstrated by the -$100 billion+ pulled out of domestic equity funds during 2015 (Source: ICI). The Volatility Index (VIX) shows us the low-hanging fruit of pessimism has been picked with the metric down -73% from August. With legislative debt ceiling and sequestration debates ahead in the coming weeks, we could hit some more choppy waters. Short-term volatility may resurrect itself, but the economy keeps chugging along, interest rates remain near all-time lows, and stock valuations, broadly speaking, remain reasonable. Investors may not be out of the woods yet, but one thing remains certain…an ever-changing stream of fearful headlines are likely to continue flooding in, which means we must all keep our lizard brains in check.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Marathon Market Gets a Cramp

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (October 1, 2015). Subscribe on the right side of the page for the complete text.

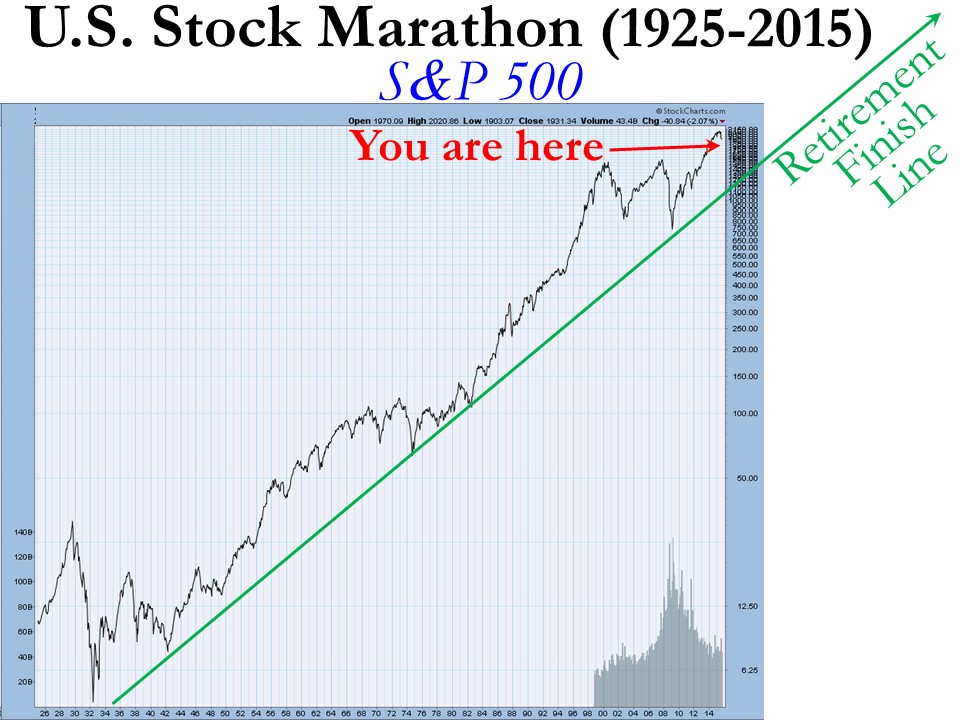

“Anyone can run a hundred meters, it’s the next forty-two thousand and two hundred that count.”

Investing is a lot like running a marathon…but it’s not a sprint to the retirement finish line. The satisfaction of achieving your long-term goal can be quite rewarding, but attaining ambitious objectives does not happen overnight. Along the hilly and winding course, there can be plenty of bumps and bruises mixed in with the elation of a runner’s high. While stocks have been running at a record pace in recent years, prices have cramped up recently as evidenced by the -2.6% decline of the S&P 500 stock index last month.

But the recent correction should be placed in the proper perspective as you approach and reach retirement. Since the end of the 2008 Financial Crisis the stock market has been racing ahead at a brisk rate, as you can see from the total return performance below (excluding 2015):

This performance is more indicative of a triumph than a catastrophe, but if you turned on the TV, listened to the radio, or surfed the web, you may come to a more frightening conclusion.

What’s behind the recent dip? These are some of the key concerns driving the recent price volatility:

- China: Slowing growth in China and collapse in Chinese stock market. China is suffering from a self-induced slowdown designed to mitigate corruption, prick the real estate bubble, and shift its export-driven economy to a more consumer-driven economy. These steps diminish short-term growth (albeit faster than U.S. growth), but nevertheless the measures should be constructive for longer-term growth.

- Interest Rates: Uncertainty surrounding the timing of a 0.25% target interest rate increase by the Federal Reserve. The move from 0% to 0.25% is like walking from the hardwood floor onto the rug…hardly noticeable. The inevitable move by the Fed has been widely communicated for months, and given where interest rates are today, the move will have a negligible impact on corporate borrowing costs. Like removing a Band-Aid, the initial action may cause some pain, but should be comfortably received shortly thereafter.

- Politics: Potential government shutdown / sequestration. The epic political saga will never end, however, as I highlighted in “Who Said Gridlock is Bad?,” political discourse in Washington has resulted in positive outcomes as it relates to our country’s fiscal situation (limited government spending and declining deficits). The government shutdown appears to have been averted for now, but it looks like we will be blanketed with brinkmanship nonsense again in a few months.

- Biotech/Pharmaceuticals: Politics over lofty drug prices and the potential impact of future regulation on the biotech sector. Given the current Congressional balance of power, any heavy-handed Democratic proposals is likely to face rigorous Republican opposition.

- Emerging Markets: Emerging market weakness, especially in Latin America (e.g., Brazil). These developments deserve close monitoring, but the growth in the three largest economic regions (U.S., Europe, and China) will have a much larger effect on the direction of global economic expansion.

- Middle East: Destabilized Middle East and Syria. Terrorist extremism and cultural animosity between various Middle East populations has existed for generations. There will be no silver bullet for a peaceful solution, so baby steps and containment are critical to maintain healthy global trade activity with minimal disruptions.

Worth noting, this current list of anxieties itemized above is completely different from six months ago (remember the Greece crisis?), and the list will change again six months into the future. Investing, like any competitive challenge, does not come easy…there is always something to worry about in the land of economics and geopolitics.

Here’s what the world’s top investor Warren Buffett said a few decades ago (1994) on the topic of politics and economics:

“We will continue to ignore political and economic forecasts which are an expensive distraction for investors and businessmen. Thirty years ago, no one could have foreseen the huge expansion of the Vietnam War, wage and price controls, two oil shocks, the resignation of a president, the dissolution of the Soviet Union, a one-day drop in the Dow of 508 points, or treasury bill yields fluctuating between 2.8% and 17.4%.”

In a world of 7.3 billion people and 196 countries there will never be a shortage of fear, uncertainty, and doubt (F.U.D.) – see events chart in The Bungee Market. In an ever-increasing, globally connected world, technology and the media continually amplify molehills into mountains, thereby making the next imagined Armageddon a simple click of a mouse or swipe of a smartphone away.

Today’s concerns are valid but in the vast majority of cases the issues are completely overblown, sensationalized and over-emphasized without context. Context is an integral part to investing, but unfortunately context usually cannot be explained in a short soundbite or headline. On the flip side, F.U.D. thrives in the realm of soundbites and headlines.

While investors may feel fatigued from a strong flow of headline headwinds, financial market race participants should take a break at the water stop to also replenish themselves with a steady tailwind of positive factors, including the following:

- Employment: The unemployment rate has been cut from a recession peak of 10.0% down to 5.1%, and the economy has been adding roughly +200,000 new monthly jobs on a fairly consistent basis. On top of that, there are a record 5.8 million job openings versus 3.7 million two years ago – a sign that the economy continues to hum along.

- Housing/Commercial Real Estate/Mortgage Rates: Housing prices have rebounded by about +30% from the 2012 lows; Housing starts have increased by +25% in the past year and 120% in the past four years; and 30-Year Fixed mortgage interest rates sit at 3.85% – a highly stimulative level within a spitting distance from record lows.

- Auto Sales: Surged to a post-recession record of 17.8 million units in August.

- Interest Rates: Massively stimulative and near generational lows, even if the Fed hikes its interest rate target by 0.25% in October, December or sometime in 2016.

- Capital Goods Orders: Up for three consecutive months.

- Rail Shipments/Truck Tonnage: Both these metrics are rising by about 3-4%.

- Retail Sales: Rising at a very respectable pace of 7% over the last six months.

- Low Energy & Commodity Prices: Inflation has remained largely in check thanks to plummeting commodity prices. Low oil and gas prices are benefiting consumers in numerous ways, including the contribution to car sales, home sales, and/or debt reduction.

While the -10% dip in stock prices from mid-August might feel like a torn knee ligament, long-term investors know -10% corrections historically occur about one-time per year, on average. So, even though you may be begging for a wheelchair, the best course of action is to take a deep breath, stick to your long-term investment plan, rebalance your portfolio if necessary, and continue staying on course towards your financial finish line.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) , but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

2014: Here Comes the Dumb Money!

Before this year’s gigantic rally, I wrote about the unexpected risk of a Double Rip. At that time, all the talk and concern was over the likelihood of a “Double Dip” recession due to the sequestration, tax increases, Obamacare, and an endless list of other politically charged worries.

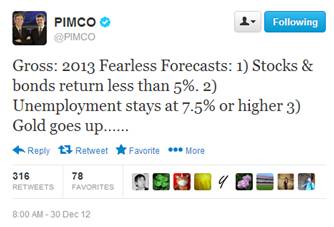

Perma-bear Nouriel Roubini has already incorrectly forecasted a double-dip in 2009, 2010, 2011, and 2012, and bond maven Bill Gross at PIMCO has fallen flat on his face with his “2013 Fearless Forecasts”: 1) Stocks & bonds return less than 5%. 2) Unemployment stays at 7.5% or higher 3) Gold goes up.

Well at least Bill was correct on 1 of his 4 predictions that bonds would suck wind, although achieving a 25% success rate would have earned him an “F” at Duke. The bears’ worst nightmares have come to reality in 2013 with the S&P up +25% and the NASDAQ climbing +33%, but there still are 11 trading days left in the year and a Hail Mary taper-driven collapse is in bears’ dreams.

Source: Scott Grannis

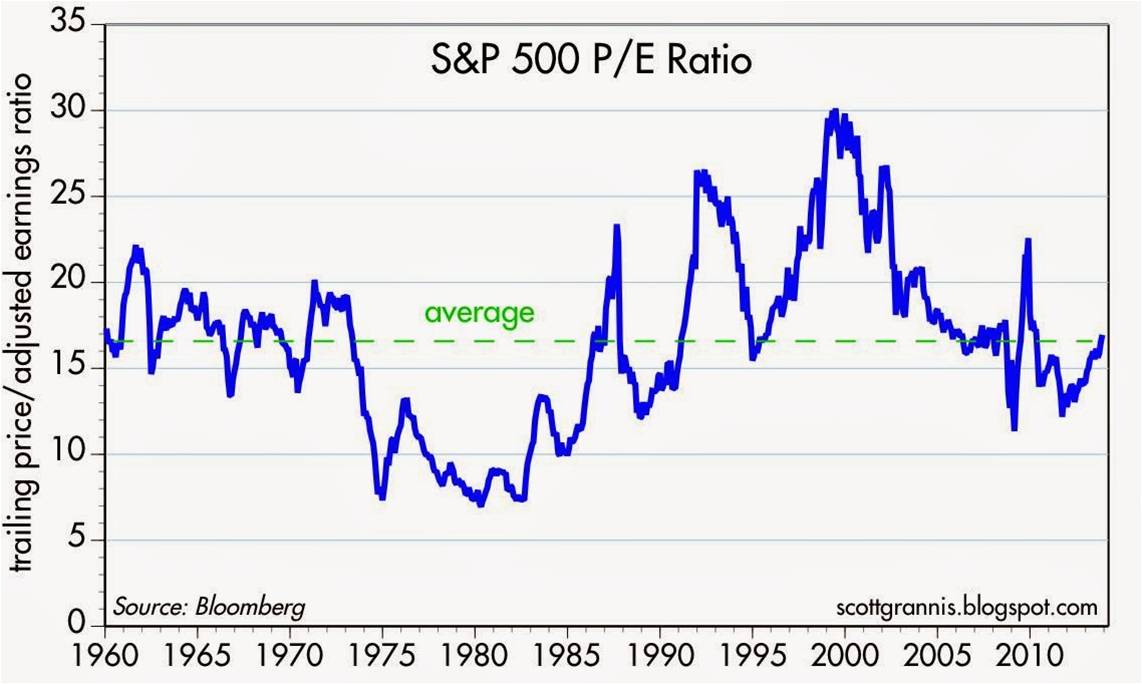

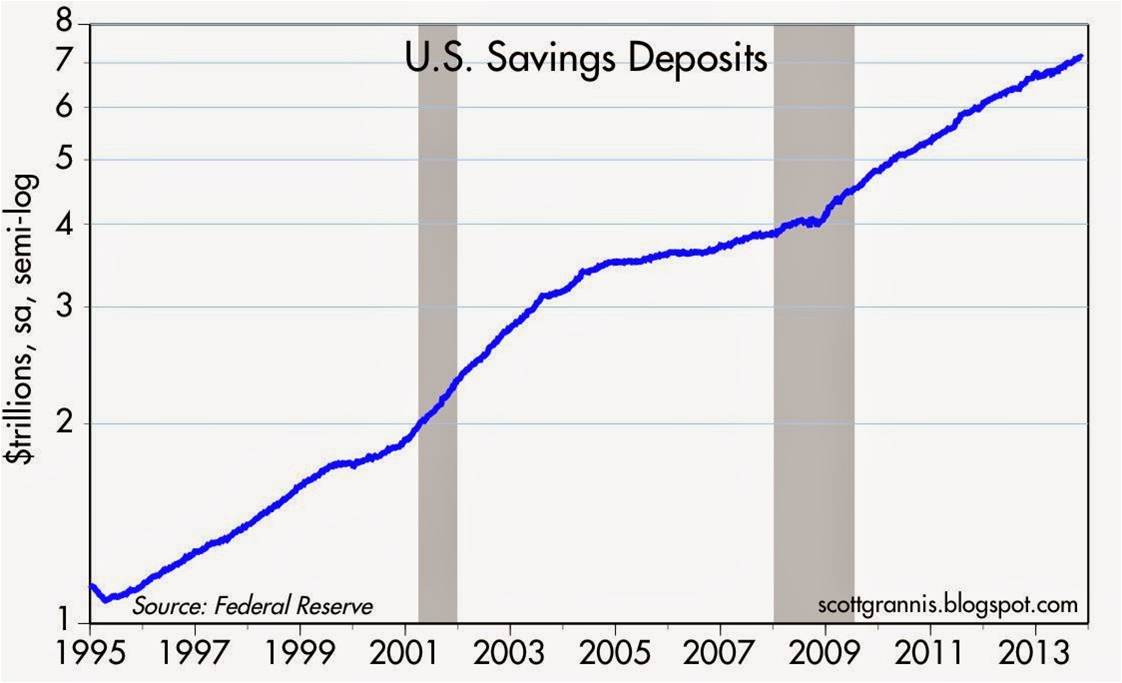

For bulls, the year has brought a double dosage of GDP and job expansion, topped with a cherry of multiple expansion on corporate profit growth. As we head into 2014, at historically reasonable price-earnings valuations (P/E of ~16x – see chart above), the new risk is no longer about Double-Dip/Rip, but rather the arrival of the “dumb money.” You know, the trillions of fear capital (see chart below) parked in low-yielding, inflation-losing accounts such as savings accounts, CDs, and Treasuries that has missed out on the more than doubling and tripling of the S&P and NASDAQ, respectively (from the 2009 lows).

Source: Scott Grannis

The fear money was emboldened in 2009-2012 because fixed income performed admirably under the umbrella of declining interest rates, albeit less robustly than stocks. The panic trade wasn’t rewarded in 2013, and the dumb money trade may prove challenging for the bears in 2014 as well.

Despite the call for the “great rotation” out of bonds into stocks earlier this year, the reality is it never happened. I will however concede, a “great toe-dip” did occur, as investor panic turned to merely investor skepticism. If you consider the domestic fund flows data from ICI (see chart below), the modest +$28 billion inflow this year is a drop in the bucket vis-à-vis the hemorrhaging of -$613 billion out of equities from 2007-2012.

Will I be talking about the multi-year great rotation finally coming to an end in 2018? Perhaps, but despite an impressive stock rally over the previous five years in the face of a wall of worry, I wonder what a half trillion dollar rotation out of bonds into stocks would mean for the major indexes? While a period of multi-year stock buying would likely be good for retirement portfolios, people always find it much easier to imagine potentially scary downside scenarios.

It’s true that once the taper begins, the economy gains more steam, and interest rates begin rising to a more sustainable level, the pace of this stock market recovery is likely to lose steam. The multiple expansion we’ve enjoyed over the last few years will eventually peak, and future market returns will be more reliant on the lifeblood of stock-price appreciation…earnings growth (a metric near and dear to my heart).

The smart money has enjoyed another year of strong returns, but the party may not quite be over in 2014 (see Missing the Pre-Party). Taper is the talk of the day, but investors might pull out the hats and horns this New Year, especially if the dumb money comes to join the fun.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Can Good News be Good News?

There has been a lot of hyper-taper sensitivity of late, ever since Fed Chairman Ben Bernanke broached the subject of reducing the monthly $85 billion bond buying stimulus program during the spring. With a better than expected ADP jobs report on Wednesday and a weekly jobless claims figure on Thursday, everyone (myself) included was nervously bracing for hot November jobs number on Friday. Why fret about potentially good economic numbers? Firstly, as a money manager my primary job is to fret, and secondarily, stronger than forecasted job additions in November would likely feed the fear monster with inflation and taper alarm, thus resulting in a triple digit Dow decline and a 20 basis point spike in 10-year Treasury rates. Right?

Well, the triple digit Dow move indeed came to fruition…but in the wrong direction. Rather than cratering, the Dow exploded higher by +200 points above 16,000 once again. Any worry of a potential bond market thrashing fizzled out to a flattish whimper in the 10-year Treasury yield (to approximately 2.86%). You certainly should not extrapolate one data point or one day of trading as a guaranteed indicator of future price directions. But, in the coming weeks and months, if the economic recovery gains steam I will be paying attention to how the market reacts to an inevitable Fed tapering and likely rise in interest rates.

The Expectations Game

Interpreting the correlation between the tone of news and stock direction is a challenging endeavor for most (see Circular Conversations & Tweet), but stock prices going up on bad news has not a been a new phenomenon. Many will argue the economy has been limp and the news flow extremely weak since stock prices bottomed in early 2009 (i.e., Europe, Iran, Syria, deficits, debt downgrade, unemployment, government shutdown, sequestration, taxes, etc.), yet actual stock prices have chugged higher, nearly tripling in value. There is one word that reconciles the counterintuitive link between ugly news and handsome gains…EXPECTATIONS. When expectations in 2009 were rapidly shifting towards a Great Depression and/or Armageddon scenario, it didn’t take much to move stock prices higher. In fact, sluggish growth coupled with historically low interest rates were enough to catapult equity indices upwards – even after factoring in a dysfunctional, ineffectual political backdrop.

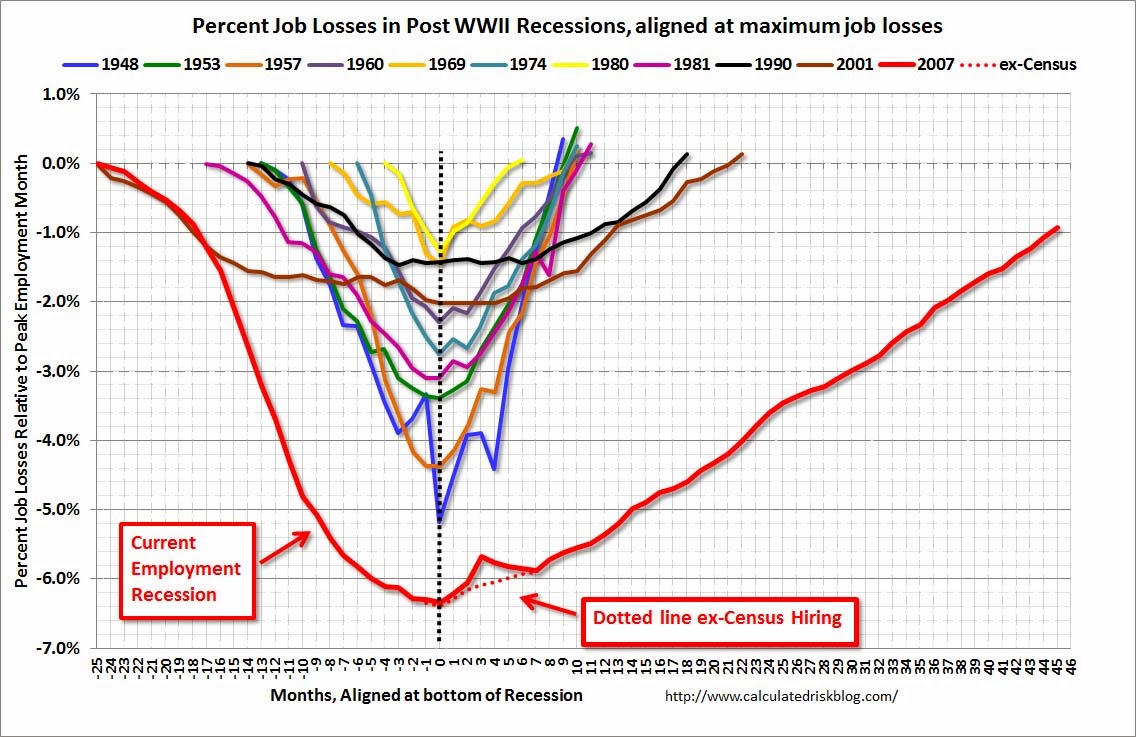

From a longer term economic cycle perspective, this recovery, as measured by job creation, has been the slowest since World War II (see Calculated Risk chart below). However, if you consider other major garden variety historical global banking crises, our crisis is not much different (see Oregon economic study).

While it’s true that stock prices can go up on bad news (and go down on good news), it is also possible for prices to go up on good news. Friday’s trading action after the jobs report is the proof of concept. As I’ve stated before, with the meteoric rise in stock prices, it’s my view the low hanging profitable fruit has been plucked, but there is still plenty of fruit on the trees (see Missing the Pre-Party). I am not the only person who shares this view.

Recently, legendary investor Warren Buffett had this to say about stocks (Source: Louis Navellier):

“I don’t have concerns about this market.” Buffet said stocks are “in a zone of reasonableness. Five years ago,” Buffett said, “I wrote an article for The New York Times that said they were very cheap. And every now and then, you can see that that they’re very overpriced or very underpriced.” Today, “they’re definitely not way overpriced. They’re definitely not underpriced.” “If you live long enough,” Buffett said, “you’ll see a lot higher prices. I don’t know what stocks will do next week or next month or next year, but five or 10 years from now, they are very likely to be higher.”

However, up cycles eventually run their course. As stocks continue to go up on good news, ultimately they begin to go down on good news. Expectations in time tend to get too lofty, and the market begins to anticipate a downturn. Stock prices are continually incorporating information that reflects the direction of future earnings and cash flow prospects. Looking into the rearview mirror at historical results may have some value, but gazing through the windshield and anticipating what’s around the corner is more important.

Rather than getting caught up with the daily mental somersault exercises of interpreting what the tone of news headlines means to the stock market (see Sentiment Pendulum), it’s better to take a longer-term cyclical sentiment gauge. As you can see from the chart below, waiting for the bad news to end can mean missing half of the upward cycle. And the same principle applies to good news.

Bad news can be good news for stock prices, and good news can be bad for stock prices. With the spate of recent positive results (i.e., accelerating purchasing manager data, robust auto sales, improving GDP, better job growth, and more new-home sales), perhaps good news will be good news for stock prices?

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Surviving a Series of Unfortunate Events

My children grew up reading a Series of Unfortunate Events by Lemony Snicket’s (the pseudonym for Daniel Handler). The award winning 13 book series began at the turn of the century (1999) with the Bad Beginning and seven years later, Handler ended the stories with The End (2006). The books chronicle the stories of three orphaned children (Violet, Klaus, and Sunny Baudelaire) who experience increasingly terrible events after the alleged death of their parents and burning of their house by a man named Count Olaf.

Crime, violence and hardships not only occur in novels, but also in real life. Stock market investors are no strangers to unfortunate events either. Within the last five years alone, investors have endured an endless stream of bad news, including the following:

- Flash Crash

- Debt Ceiling Debate

- U.S. Debt Downgrade

- European Recession

- Arab Spring

- Potential Greek Exit from EU

- Uncertain U.S. Presidential Elections

- Sequestration

- Cyprus Financial Crisis

- Tax Increases

- Fed Talks of Stimulus Tapering

- Syrian Civil War / Military Threat

- Gov. Shutdown

- Obamacare Rollout Glitches

- Iranian Nuclear Threat

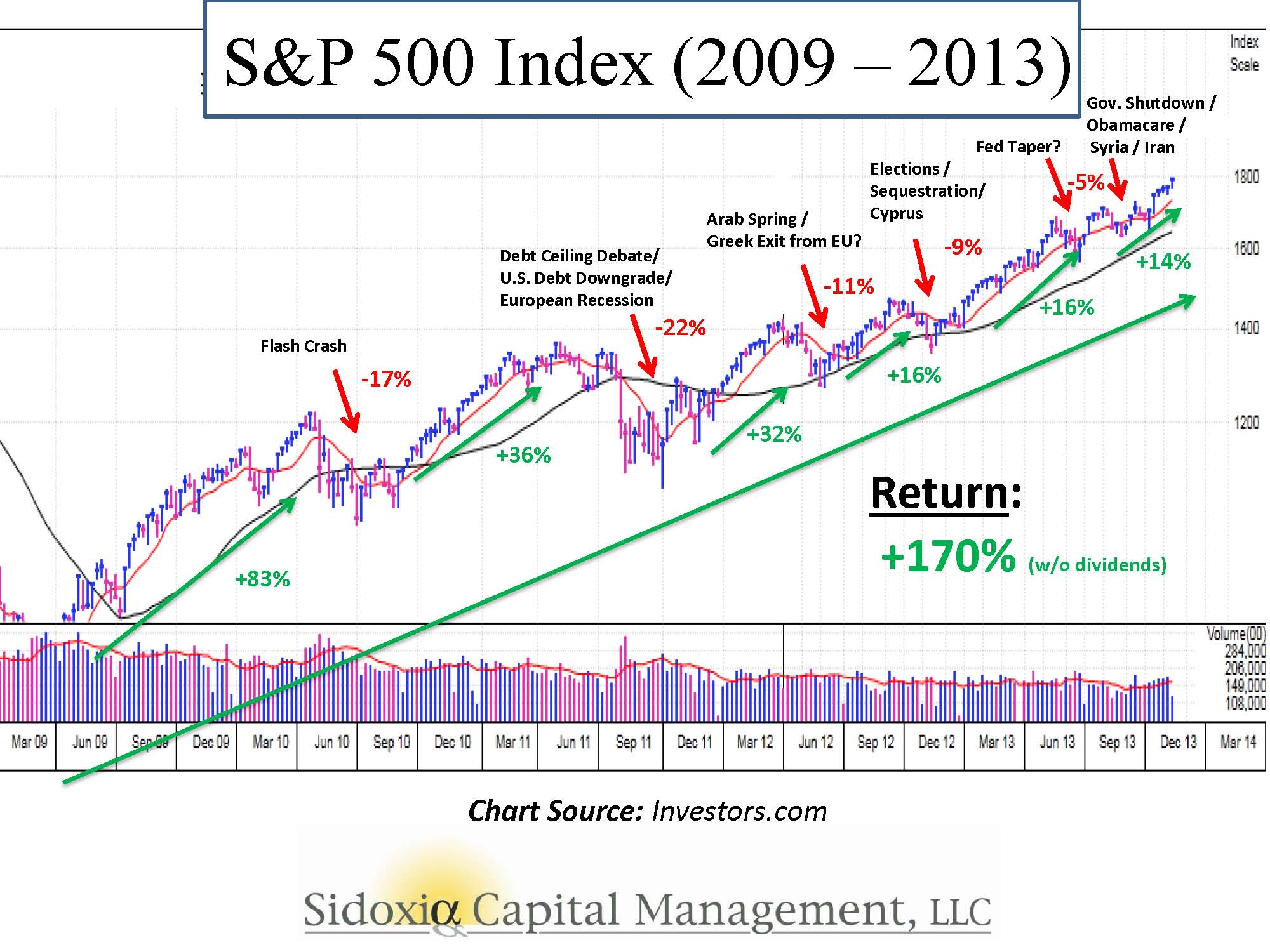

This is only a partial list, but wow, this never ending crises list sounds pretty ominous, right? I wonder how stocks have fared amidst this horrendous avalanche of negative headlines? The short answer is stocks are up a whopping +170% since the March 2009 lows as measured by the S&P 500 index, and would be significantly higher once accounting for reinvested dividends. A bit higher return than your CD, money market, or savings account rate.

As you can see from the chart above, the gargantuan returns achieved over this period have not occurred without some volatility. Investors have consumed massive quantities of Tums during the five highlighted corrections (averaging -13%) to counteract all the heartburn. As I’ve written in the past, with higher risk comes higher rewards. Those investors who cannot stomach the volatility shouldn’t go cold turkey on stocks though, but rather diversify their holdings and reduce the portfolio equity allocation to a more palatable level.

Doubting Thomases

Many people I bump into remain “Doubting Thomases” as it relates to the stock market recovery and they expect an imminent crash. Certainly, the rocket-like trajectory of the last year (and five years) is not sustainable, and historically stocks correct significantly twice a decade – equal to the number of recessions occurring each decade. There is no denying that this economic recovery has been the slowest since World War II, but could this be good news? From the half-full glass lens, a slower recovery may actually equate to a longer recovery.

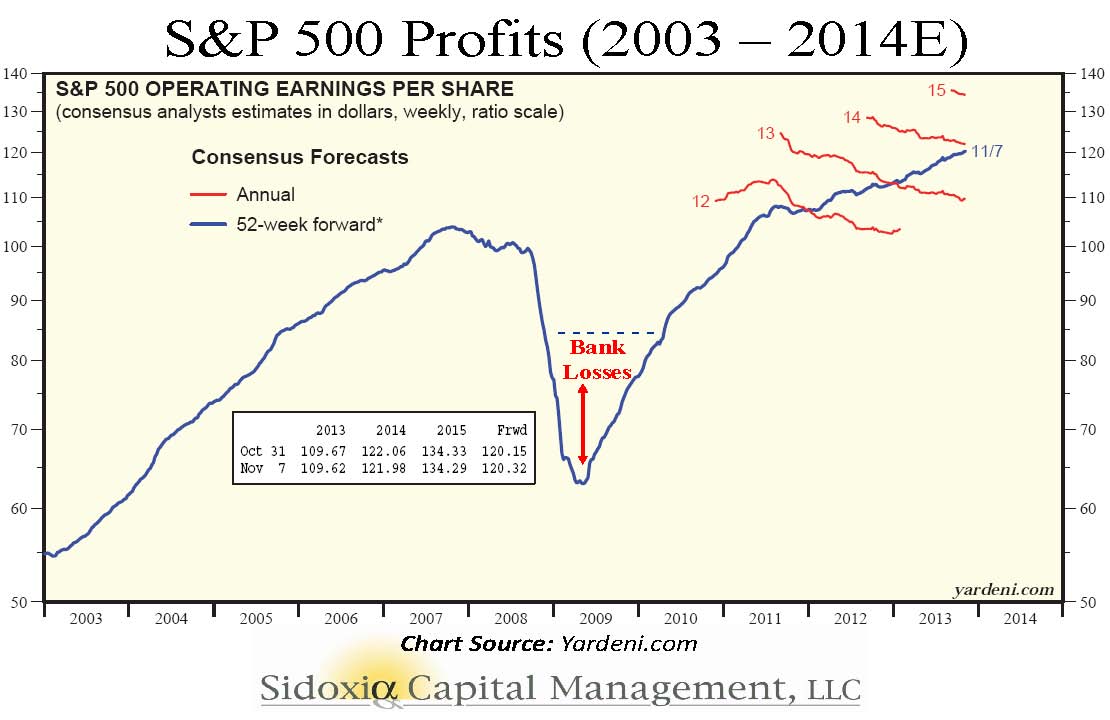

Just like skeptical investors, business executives have been slow to hire and slow to accelerate spending as well. Typically business cycles come to an end when overinvestment happens – recall the 2000 tech bubble and 2007 housing bubble. There may be pockets of investment bubbles (e.g., Twitter Inc [TWTR] and other money-losing speculative stocks), but as you can see from the chart below, corporate profits have skyrocketed and are at record highs. It should therefore come as no surprise that record profits have coincided with record stock prices (see also It’s the Earnings Stupid)

Over the period of 2003-2013 stock prices largely followed the slope of earnings, and excluding the enormous losses in the banking sector, non-financial stocks suffered much less.

History is on Your Side

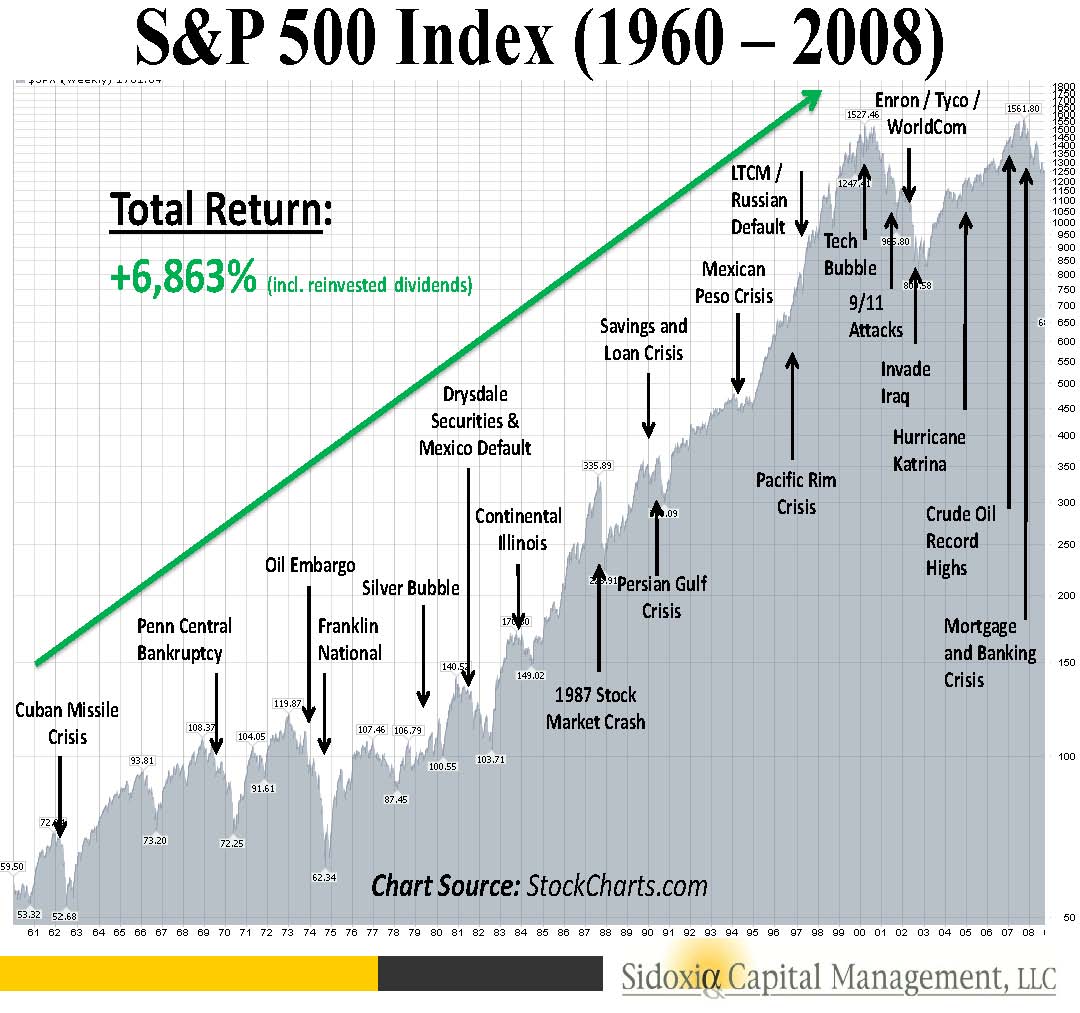

If you are in the camp that says this last five years has been an anomaly, history may beg to differ. Over the last 50 years we have experienced wars, assassinations, currency crises, banking crises, terrorist attacks, recessions, SARs, mad cow disease, military engagements, tax hikes, Fed rate hikes, and yes, even political gridlock. As the chart below shows, the stock market is volatile over the short-run, but quite resilient and lucrative over the long-run (+6,863% over 49 years). In fact, from January 1960 to October 2013 the S&P 500 index has catapulted +14,658%, including reinvested dividends (Source: DQYDJ.net).

Rather than getting caught up in the political or CNBC headline du jour, investors will be better served by creating a customized, long-term diversified portfolio that can meet long-standing goals and objectives. If you don’t have the discipline, interest, or time to properly create a personalized investment plan, then find an independent investment advisor like Sidoxia Capital Management (www.Sidoxia.com), so you can experience a series of fortunate (not unfortunate) events.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in TWTR, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page. Chart construction done by Kevin D. Weaver.

Sitting on the Sidelines: Fear & Selective Memory

Fear is a motivating (or demotivating) emotion that can force individuals into suboptimal actions. The two main crashes of the 2000s (technology & housing bubbles) coupled with the mini-crises (e.g., flash crash, European crisis, debt ceiling, sequestration, fiscal cliff, etc.) have scared millions of investors and trillions of dollars to sit on the sidelines. Financial paralysis may be great in the short-run for bruised psyches and egos, but for the passive onlookers, the damage to retirement accounts can be crippling.

Selective memory is a great coping mechanism for those investors sitting on the sidelines as well. Purposely forgetting your wallet at a group dinner may be beneficial in the near-term, but repeated incidents will result in lost friends over the long-run. Similarly, most gamblers frequenting casinos tend to pound their chests when bragging about their wins, however they tend to conveniently forget about all the losses. These same reality avoidance principles apply to investing.

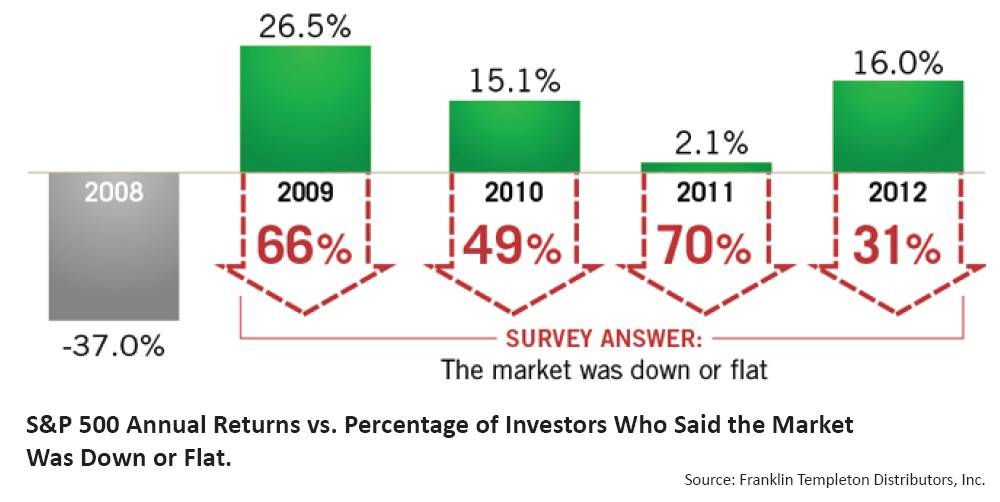

A recent piece written by CEO Bill Koehler at Tower Wealth Managers, entitled The Fear Bubble highlights a survey conducted by Franklin Templeton. In the study, investors were asked how the stock market performed in 2009-2012. As you can see from the chart below, perception is the polar opposite of reality (actual gains far exceeded perceived losses):

Source: Franklin Templeton via Tower Wealth Managers

With so many investors sitting on the sidelines in cash or concentrated in low-yielding bonds and gold, I suppose the results shouldn’t be too surprising. Once again, selective memory serves as a wonderful tool to bury the regrets of missing out on a financial market recovery of a lifetime.

Humans also have a predisposition to seek out people who share similar views, even though accumulating different viewpoints ultimately leads to better decisions. Morgan Housel at The Motley Fool just wrote an article, Putting a Gap Between You and Stupid, explaining how individuals should seek out others who can help protect them from harmful biases. A scientific study referenced in the article showed how the functioning of biased brains literally shuts down:

“During the 2004 presidential election, psychologist Drew Westen of Emory University and his colleagues studied the brains of 15 “committed” Democrats and 15 “committed” Republicans with an MRI scanner. Each group was shown a collection of contradictory statements made by George W. Bush and John Kerry. Not surprisingly, the partisans were quick to call out contradictions made by the opposing party, and made up all kinds of justifications to rationalize quotes made by their own side’s candidate. But here’s what’s scary: The participants weren’t just being stubborn. Westen found that areas of their brains that control reasoning and logic virtually shut down when confronted with a conflicting view of their preferred candidate.”

Rather than letting emotions rule the day, the proper approach is to stick to unbiased numbers like valuations, yields, fees, and volatility. If you continually make mistakes; you aren’t disciplined enough; or you don’t like investing; then find a trusted advisor who uses an objective financial approach. Opportunistically taking advantage of volatility, instead of knee-jerk reactions is the preferred approach. For those people sitting on the sidelines and using selective memory, you may feel better now, but you will eventually have to get in the game, if you don’t want to lose the retirement account game.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is the information to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Most Hated Bull Market Ever

Life has been challenging for the bears over the last four years. For the first few years of the recovery (2009-2010) when stocks vaulted +50%, supposedly we were still in a secular bear market. Back then the rally was merely dismissed as a dead-cat bounce or a short-term cyclical rally, within a longer-term secular bear market. Then, after an additional +50% move the commentary switched to, “Well, we’re just in a long-term trading range. The stock market hasn’t done a thing in a decade.” With major indexes now hitting all-time record highs, the pessimists are backpedaling in full gear. Watching the gargantuan returns has made it more difficult for the bears to rationalize a tripling +225% move in the S&P 600 index (Small-Cap); a +214% move in the S&P 400 index (Mid-Cap); and a +154% in the S&P 500 index (Large-Cap) from the 2009 lows.

For the unfortunate souls who bunkered themselves into cash for an extended period, the return-destroying carnage has been crippling. Making matters worse, some of these same individuals chased a frothy over-priced gold market, which has recently plunged -30% from the peak.

Bonds have generally been an OK place to be as Europe imploded and domestic political gridlock both helped push interest rates to record-lows (e.g., tough to go lower than 0% on the Fed-Funds rate). But now, those fears have subsided, and the recent rate spike from Ben Bernanke’s “taper tantrum” has caused bond bulls to reassess their portfolios (see Fed Fatigue). Staring at the greater than -90% underperformance of bonds, relative to stocks over the last four years, has been a bitter pill to swallow for fervent bond believers. The record -$9.9 billion outflow from Mr. New Normal’s (Bill Gross) Pimco Total Return Fund in June (a 26-year record) is proof of this anxiety. But rather than chase an unrelenting stock market rally, stock haters and skeptics remain stubborn, choosing to place their bond sale proceeds into their favorite inflation-depreciating asset…cash.

Crash Diet at the Buffet

I’ve seen and studied many markets in my career, but the behavioral reactions to this most-hated bull market in my lifetime have been fascinating to watch. In many respects this reminds me of an investing buffet, where those participating in the nourishing market are enjoying the spoils of healthy returns, while the skeptical observers on the sidelines are on a crash diet, selecting from a stingy menu of bread and water. Sure, there is some over-eating, heartburn, and food coma experienced by those at the stock market table, but one can only live on bread and water for so long. The fear of losses has caused many to lose their investing appetite, especially with news of sequestration, slowing China, Middle East turmoil, rising interest rates, etc. Nevertheless, investors must realize a successful financial future is much more like an eating marathon than an eating sprint. Too many retirees, or those approaching retirement, are not responsibly handling their savings. As legendary basketball player and coach John Wooden stated, “Failing to prepare is preparing to fail.”

20 Years…NOT 20 Days

I will be the first to admit the market is ripe for a correction. You don’t have to believe me, just take a look at the S&P 500 index over the last four years. Despite the explosion to record-high stock prices, investors have had to endure two corrections averaging -20% and two other drops approximating -10%. Hindsight is 20-20, but at each of those fall-off periods, there were plenty of credible arguments being made on why we should go much lower. That didn’t happen – it actually was the opposite outcome.

For the vast majority of investing Americans, your investing time horizon should be closer to 20 years…not 20 days. People that understand this reality realize they are not smart enough to consistently outwit the market (see Market Timing Treadmill). If you were that successful at this endeavor, you would be sitting on your private, personal island with a coconut, umbrella drink.

Successful long-term investors like Warren Buffett recognize investors should “buy fear, and sell greed.” So while this most hated bull market remains fully in place, I will follow Buffett’s advice comfortably sit at the stock market buffet, enjoying the superior long-term returns put on my plate. Crash dieters are welcome to join the buffet, but by the time they finally sit down at the stock market table, I will probably have left to the restroom.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), including IJR, and IJH, but at the time of publishing, SCM had no direct position in BRKA/B, Pimco Total Return Fund, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Confessions of a Bond Hater

Source: stock.xchng

Hi my name is Wade, and I’m a bond hater. Generally, the first step in addressing any type of personal problem is admitting you actually have a problem. While I am not proud of being a bond hater, I have been called many worse things during my life. But as we have learned from the George Zimmerman / Trayvon Martin case, not every situation is clear-cut, whether we are talking about social issues or bond investing. For starters, let me be clear to everyone, including all my detractors, that I do not hate all bonds. In fact, my Sidoxia clients own many types of fixed income securities. What I do hate however are low yielding, long duration bonds.

Duration…huh? Most people understand what “low yielding” means, when it comes to bonds (i.e., low interest, low coupon, low return, etc.), but when the word duration is uttered, the conversation is usually accompanied by a blank stare. The word “duration” may sound like a fancy word, but in reality it is a fairly simple concept. Essentially, high-duration bonds are those fixed income securities with the highest sensitivity to changes in interest rates, meaning these bonds will go down most in price as interest rates rise.

When it comes to equity markets, many investors understand the concept of high beta stocks, which can be used to further explain duration. There are many complicated definitions for beta, but the basic principle explains why high-beta stock prices generally go up the most during bull markets, and go down the most during bear markets. In plain terms, high beta equals high octane.

If we switch the subject back to bonds, long duration equals high octane too. Or stated differently, long duration bond prices generally go down the most during bear markets and go up the most during bull markets. For years, grasping the risk of a bond bear market caused by rising rates has been difficult for many investors to comprehend, especially after witnessing a three-decade long Federal Funds tailwind taking the rates from about 20% to about 0% (see Fed Fatigue Setting In).

The recent interest rate spike that coincided with the Federal Reserve’s Ben Bernanke’s comments on QE3 bond purchase tapering has caught the attention of bond addicts. Nobody knows for certain whether this short-term bond price decline is the start of an extended bear market in bonds, but mathematics would dictate that there is only really one direction for interest rates to go…and that is up. It is true that rates could remain low for an indefinite period of time, but neither scenario of flat to down rates is a great outcome for bond holders.

Fixes to Fixed-Income Failings

Even though I may be a “bond hater” of low yield, high duration bonds, currently I still understand the critical importance and necessity of a fixed income portfolio for not only retirees, but also for the diversification benefits needed by a broader set of investors. So how does a bond hater reconcile investing in bonds? Easy. Rather than focusing on lower yielding, longer duration bonds, I invest more client assets in shorter duration and/or higher yielding bonds. If you harbor similar beliefs as I do, and believe there will be an upward bias to the trajectory of long-term interest rates, then there are two routes to go. Investors can either get compensated with a higher yield to counter the increased interest rate risk, and/or they can shorten duration of bond holdings to minimize capital losses.

Worth noting, there is an alternative strategy for low yielding, long duration bond lovers. In order to minimize interest rate risk, these bond lovers may accept sub-optimal yields and hold bonds to maturity. This strategy may be associated with short-term price volatility, but if the bond issuer does not default, at least the bond investor will get the full principal at maturity to help relieve the pain of meager yields.

Now that you’ve survived all this bond babbling, let me cut to the chase and explain a few ways Sidoxia is taking advantage of the recent interest rate volatility for our clients:

Floating Rate Bonds: Duration of these bonds is by definition low, or near zero, because as interest rates rise, coupons/interest payments are advantageously reset for investors at higher rates. So if interest rates jump from 2% to 3%, the investor will receive +50% higher periodic payments.

Inflation Protection Bonds: These bonds come in long and short duration flavors, but if interest rates/inflation rise higher than expected, investors will be compensated with higher periodic coupons and principal payments.

Shorter Duration: One definition of duration is the weighted average of time until a bond’s fixed cash flows are received. A way of shortening the duration of your bond portfolio is through the purchase of shorter maturity bonds (e.g., buying 3-year bonds rather than 30-year bonds).

High Yield Bonds: Investing in the high yield bond category is not limited to domestic junk bond purchases, but higher yields can also be earned by investing in international and/or emerging market bonds.

Investment Grade Corporate Bonds: Similar to high yield bonds, investment grade bonds offer the potential of capital appreciation via credit improvement. For instance, credit rating upgrades can provide gains to help offset price declines caused by rising interest rates.

Despite my bond hater status, the recent taper tantrum and interest rate spike, highlight some advantages bonds have over stocks. Even though prices declined, bonds by and large still have lower volatility than stocks; provide a steady stream of income; and provide diversification benefits.

To the extent investors have, or should have, a longer-term time horizon, I still am advocating a stock bias to client portfolios, subject to each investor’s risk tolerance. For example, an older retired couple with a conservative target allocation of 20%/80% (equity/fixed income) may consider a 25% – 30% allocation. A shift in this direction may still meet the retirees’ income needs (especially if dividend-paying stocks are incorporated), while simultaneously acknowledging the inflation and interest rate risks impacting bond positions. It’s important to realize one size doesn’t fit all.

Higher Volatility, Higher Reward

Frequent readers of Investing Caffeine have known about my bond hating tendencies for quite some time (see my 2009 article Treasury Bubble has not Burst…Yet), but the bond baby shouldn’t be thrown out with the bath water. For those investors who thought bonds were as safe as CDs, the recent -6% drop in the iShares Aggregate Bond Index (AGG) didn’t feel comfortable for most. Although I am still an enthusiastic stock cheerleader (less so as valuation multiples expand), there has been a cost for the gargantuan outperformance of stocks since March of ’09. While stocks have outperformed bonds (S&P vs. AGG) by more than +140%, equity investors have had to endure two -10% corrections and two -20% corrections (e.g.,Flash Crash, Debt Ceiling Debate, European Financial Crisis, and Sequestration/Elections). If investors want to earn higher long-term equity returns, this desire will translate into more volatility than bonds…and more Tums.

I may still be a bond hater, and the general public remains firm stock haters, but at some point in the multi-year future, I will not be surprised to hear myself say, “Hi my name is Wade, and I am addicted to bonds.” In the mean time, Sidoxia will continue to optimize its client bond portfolios for a rising interest rate environment, while also investing in attractive equity securities and ETFs. There’s nothing to hate about that.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), including floating rate bonds/loan funds, inflation-protection funds, corporate bond ETF, high-yield bond ETFs, and other bond ETFs, but at the time of publishing, SCM had no direct position in AGG or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Time to Trade in the Investment Tricycle

This article is an excerpt from a previously released Sidoxia Capital Management’s complementary newsletter (May 1, 2013). Subscribe on the right side of the page for an entire monthly update.

As the stock market continues to set new, all-time record highs and the Dow Jones Industrial index nears another historic milestone (15,000 level), investors remain cautiously skeptical of the rebound – like a nervous toddler choosing to ride a tricycle instead of a bicycle. Investors have been moving slowly, but stock prices have not – the Dow has risen +13% in 2013 alone. What’s more, over the last four years the S&P 500 index (which represents large companies) has climbed +140%; the S&P 400 (mid-sized companies) +195%; and the S&P 600 (small-sized companies) +200%.

The gains have been staggering, but like the experience of riding a bicycle, the bumps, scrapes, and bruises suffered during the 2008-2009 financial crash have caused investors to abandon their investment bikes for a perceived safer vehicle…a tricycle. What do I mean by that? Well, over the last six years, investors have pulled out more than -$521,000,000,000 from stock funds and piled those proceeds into bonds (Calafia Beach Pundit chart below). For retirees and billionaires this strategy may make sense in certain instances. But for millions of others, interest rate risk, inflation risk, and the risk of outliving your money can be more hazardous to financial well-being, than the artificially perceived safety expected from bonds. The fact of the matter is investing inefficiently in cash, money markets, CDs, and low-yielding fixed income securities can be riskier in the long-run than a globally diversified portfolio invested across a broad set of asset classes (including equities). The latter should be the strategy of choice, unless of course you are someone who yearns to work at Wal-Mart (WMT) as a greeter in your 80s!

Investor Training Wheels

I don’t want to irresponsibly flog everyone, because investing attitudes have begun to change a little in 2013, as investors have added $66 billion to stock funds (data from ICI). Effectively, some investors have gone from riding their tricycle to hopping on a bike with training wheels. With this change in mindset, surely people have commenced selling bonds to buy stocks, right? Wrong! Investors have actually bought more bonds (+$69 billion) than stocks in the first three months of the year, which helps explain why interest rates on the 10-year Treasury are only yielding a paltry 1.67% (near last year’s record summer low) – remember, bond buying causes interest rates to go down. If you really want to do research, you could ask your parents when rates were ever this low, but some readers’ parents may not even had been born yet. The previous record low in interest rates, according to Bloomberg, at 1.95% was achieved in 1941.

I don’t want to irresponsibly flog everyone, because investing attitudes have begun to change a little in 2013, as investors have added $66 billion to stock funds (data from ICI). Effectively, some investors have gone from riding their tricycle to hopping on a bike with training wheels. With this change in mindset, surely people have commenced selling bonds to buy stocks, right? Wrong! Investors have actually bought more bonds (+$69 billion) than stocks in the first three months of the year, which helps explain why interest rates on the 10-year Treasury are only yielding a paltry 1.67% (near last year’s record summer low) – remember, bond buying causes interest rates to go down. If you really want to do research, you could ask your parents when rates were ever this low, but some readers’ parents may not even had been born yet. The previous record low in interest rates, according to Bloomberg, at 1.95% was achieved in 1941.

Over the last five years the news has been atrocious, and as we have proven, investing based off of current headlines is a horrible investment strategy. As we’ve seen firsthand, there can be very long, multi-year periods when stock performance has absolutely no correlation with the positive or negative nature of news reports. To better make my point, I ask you, what types of headlines have you been reading over the last four years? I can answer the question for you with a few examples. For starters, we’ve endured financial collapses in Iceland, Ireland, Dubai, Greece, and now Cyprus. At home domestically, we’ve experienced a “flash crash” that temporarily evaporated about $1 trillion dollars in value (and 1,000 Dow points) within a few minutes due to high frequency algorithmic traders. How about unemployment data? We’ve witnessed the slowest, jobless U.S. recovery in a generation (since World War II), and European countries have it much worse than we do (e.g., Spain just registered a 27% unemployment rate). What about political gridlock and brinksmanship? We’ve seen debt ceiling stand-offs lead to a historic loss of our country’s AAA debt status; a partisan presidential election; a deafening fiscal cliff debate; and now mindless sequestration. Nevertheless, large cap stocks and small cap stocks have more than doubled and tripled, respectively.

Fear sells advertising, and sounds smarter than “everything is rosy,” but the fact remains, things are not as bad as many bears claim. Corporations are earning record profits, and hold trillions in cash (e.g., Apple Inc.’s recent announcement of more than $50 billion in share repurchase and $11 billion in annual dividend payments are proof). Moreover, central banks around the globe are doing whatever it takes to stimulate growth – most recently the Bank of Japan promised to inject $1.4 trillion into its economy by the end of 2014, in order to kick-start expansion. Lastly, the U.S. employment picture continues to improve, albeit slowly (7.6% unemployment in March), allowing consumers to pay down debt, buy more homes, and spend money to spur economic growth.

Dangers of Being Informed

Hopefully this clarifies how useless and futile newspaper headlines are when it comes to effective investing. As Mark Twain astutely noted, “If you don’t read the newspaper, you are uninformed. If you do read the newspaper, you are misinformed.” It’s perfectly fine to remain in tune with current events, but shuffling around your life’s savings based on this information is a foolish plan.

Hopefully this clarifies how useless and futile newspaper headlines are when it comes to effective investing. As Mark Twain astutely noted, “If you don’t read the newspaper, you are uninformed. If you do read the newspaper, you are misinformed.” It’s perfectly fine to remain in tune with current events, but shuffling around your life’s savings based on this information is a foolish plan.

If the concerns and worries du jour have you nervously riding a tricycle, just realize that you may not reach your investment destination with this mode of transportation. I understand that it is not all hearts and flowers in the financial markets, and there are plenty of legitimate risks to consider. However, excessive exposure in low-rate asset classes may be riskier than many realize. If you’re still riding your investment tricycle, you’re probably better off by grabbing a helmet and pads (i.e., globally diversified portfolio) and jumping on a bike – you are more likely to reach your financial destination.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), WMT and AAPL, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}