Posts tagged ‘risk’

Avoiding Automobile and Portfolio Crashes

Personal opinions of oneself don’t always mirror reality. Self perceptions relating to both driving and investing can be inflated. For example, the National Highway Traffic Safety Administration (NHTSA) reports that 95% of crashes are caused by human error, but 75% of drivers say they are better drivers than most.

Contributing factors to crashes include: 1) Distractions; 2) Alcohol; 3) Unsafe behavior (i.e., speeding); 4) Time of day (fatality rate is 3x higher at night); 5) Lack of safety belt; 6) Weather; and 7) Time of week (weekends are worst crash days).

A spokesman for the Insurance Institute for Highway Safety is quick to point out that driving behind the wheel is the riskiest activity most people engage in on a daily basis – more than 40,000 driving related fatalities occur each year. Careful common sense helps while driving, but driving sober at 4 a.m. (very few drivers on the road) on a weekday with your seatbelt on won’t hurt either.

Avoiding a Portfolio Crash

Another dangerous activity frequently undertaken by Americans is investing, despite people’s inflated beliefs of their money management capabilities. Investing, however, does not have to be harmful if proper precautions are taken.

Here is some of the hazardous behaviors that should be avoided by those maneuvering an investment portfolio:

1) Trading Too Much: Excessive trading leads to undue commissions, transaction costs, bid-ask spread, impact costs. Many of these costs are opaque or invisible and won’t necessarily be evident right away. But like a leaky boat, direct and indirect trading costs have the potential of sinking your portfolio.

2) Worrying about the Economy Too Much: The country experiences about two recessions a decade, nonetheless our economy continues to grow. If macroeconomics still worry you, then look abroad for even healthier growth – considerable international exposure should aid the long-term success of your portfolio and assist you in sleeping better at night.

3) Emotionally Reacting – Not Objectively Planning: News is bad, so sell. News is good, so buy. This type of conduct is a recipe for portfolio disaster. Better to do as Warren Buffett says, “Be fearful when others are greedy, and be greedy when others are fearful.” The long-term fundamental prospects for any investment are much more important than the daily headlines that get the emotional juices flowing.

4) Hostage to Short-term Time Horizon: Rather than worry about the next 10 days, you should be focused on the next 10 years. The further out you can set your time horizon, the better off you will be. Patience is a virtue.

5) Incongruent Portfolio with Risk: Many retirees got caught flat-footed in the midst of the global financial crisis of 2008-09 with investment portfolios heavy in equities and real estate. Diversified portfolios including fixed-income, commodities, international exposure, cash, and alternative investments should be optimized to meet your specific objectives, constraints, risk tolerance, and time horizon.

6) Timing the Market: Attempting to time the market can be hazardous to your investment health (see Market Timing article). If you really want to make money, then avoid the masses – the grass is greener and the eating better away from the herd.

Driving and investing can both be dangerous activities that command responsible behavior. Do yourself a favor and protect yourself and your portfolio from crashing by taking the appropriate precautions and avoiding the common hazardous mistakes.

Read Full Forbes Article on Driving Dangers

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Controlling the Investment Lizard Brain

“Normal fear protects us; abnormal fear paralyses us.”

– Martin Luther King, Jr.

Investing is challenging enough without bringing emotions into the equation. Unfortunately, humans are emotional, and as a result investors often place too much reliance on their feelings, rather than using objective information to drive rational decision making.

What causes investors to make irrational decisions? The short answer: our “amygdala.” Author and marketer Seth Godin calls this almond-shaped tissue in the middle of our head, at the end of the brain stem, the “lizard brain” (video below). Evolution created the amygdala’s instinctual survival flight response for lizards to avoid hungry hawks and humans to flee ferocious lions.

Over time, the threat of lions eating people in our modern lives has dramatically declined, but the human’s “lizard brain” is still running in full gear, worrying about other fear-inducing warnings like Iran, Syria, Obamacare, government shutdowns, taxes, Cyprus, sequestration, etc. (see Series of Unfortunate Events)

When the brain in functioning properly, the prefrontal cortex (the front part of the brain in charge of reasoning) is actively communicating with the amygdala. Sadly, for many people, and investors, the emotional response from the amygdala dominates the rational reasoning portion of the prefrontal cortex. The best investors and traders have developed the ability of separating emotions from rational decision making, by keeping the amygdala in check.

With this genetically programmed tendency of constantly fearing the next lion or stock market crash, how does one control their lizard brain from making sub-optimal, rash investment decisions? Well, the first thing you should do is turn off the TV. And by turning off the TV, I mean stop listening to talking head commentators, economists, strategists, analysts, neighbors, co-workers, blogger hacks, newsletter writers, journalists, and other investing “wannabes”. Sure, you could throw my name into the list of people to ignore if you wanted to, but the difference is, at least I have actually invested real money for over 20 years (see How I Managed $20,000,000,000.00), whereas the vast majority of those I listed have not. But don’t take my word for it…listen or read the words of other experienced investors Warren Buffett, Peter Lynch, Ron Baron, John Bogle, Phil Fisher, and other investment titans (see also Sidoxia Hall of Fame). These investment legends have successful long-term investment track records and they lived through wars, recessions, financial crises, and other calamities…and still managed to generate incredible returns.

Another famed investor, William O’Neil, summed this idea nicely by adding the following:

“Since the market tends to go in the opposite direction of what the majority of people think, I would say 95% of all these people you hear on TV shows are giving you their personal opinion. And personal opinions are almost always worthless … facts and markets are far more reliable.”

The Harmful Consequence of Brain on Pain

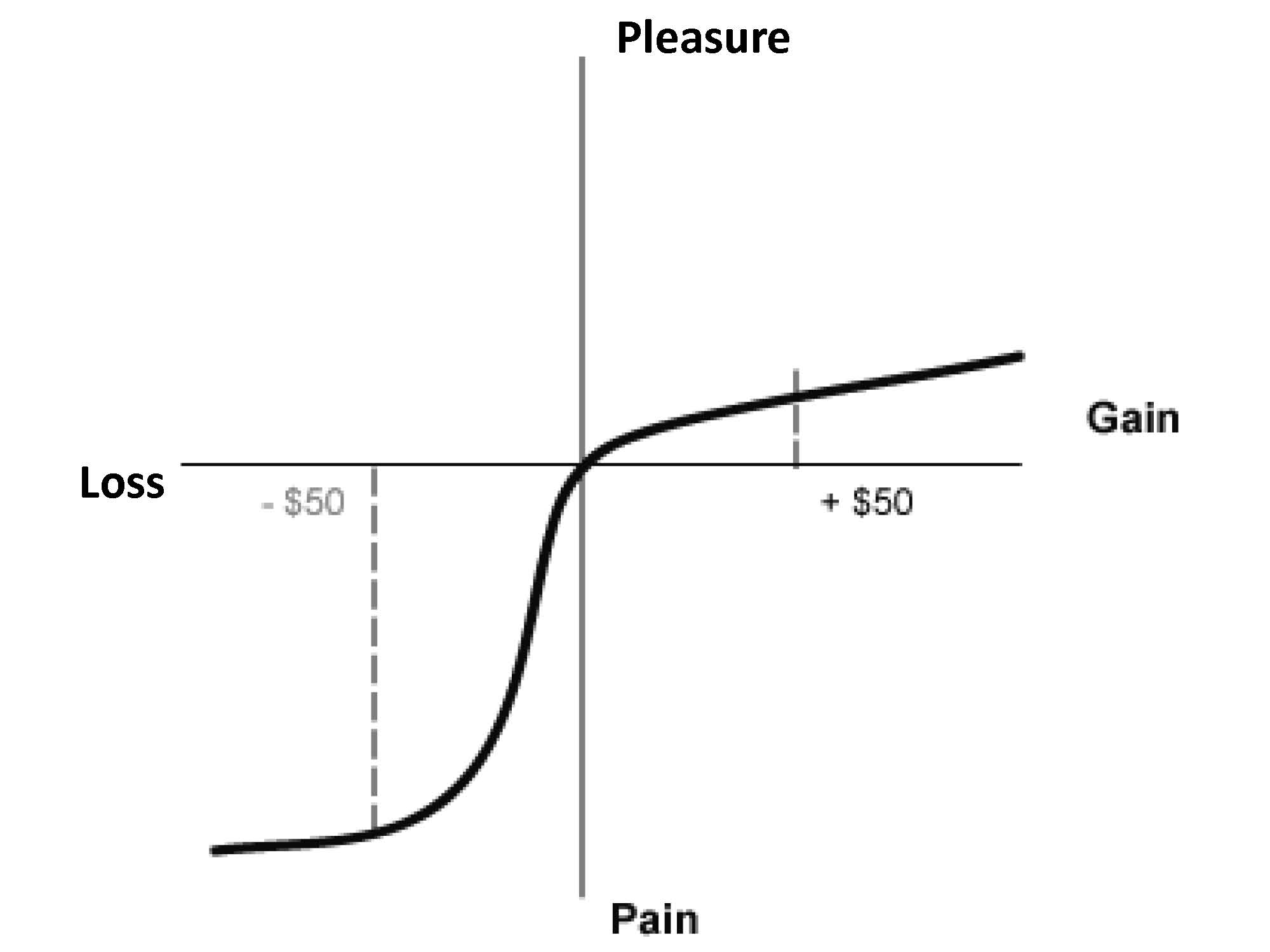

Besides forcing damaging decisions, another consequence of our lizard brain is its ability to distort reality. Behavioral economists Daniel Kahneman (Nobel Prize winner) and Amos Tversky through their research demonstrated the pain of $50 loss is more than twice as painful as the pleasure from $50 gain (see Pleasure/Pain Principle). Common sense would dictate our brains would treat equivalent scenarios in a proportional manner, but as the chart below shows, that is not the case:

Source: Investopedia

Kahneman adds to the decision-making relationship of the amygdala and prefrontal cortex by describing the concepts of instinctual and deliberative choices in his most recent book, Thinking Fast and Slow (see Decision Making on Freeways).

Optimizing Risk

Taking excessive risks in technology stocks in the 1990s or in housing in the mid-2000s was very damaging to many investors, but as we have seen, our lizard brains can cause investors to become overly risk averse. Over the last five years, many people have personally experienced the ill effects of unwarranted conservatism. Investment great Sir John Templeton summed up this risk by stating, “The only way to avoid mistakes is not to invest – which is the biggest mistake of all.”

Every person has a different perception and appetite for risk. The optimal amount of risk taken by any one investor should be driven by their unique liquidity needs and time horizon…not a perceived risk appetite. Typically risk appetites go up as markets peak, and conservatism reaches a fearful apex near market bottoms – the opposite tendency of rational decision making. Besides liquidity and time horizon, a focus on valuation coupled with diversification across asset class (stocks/bonds), geography (domestic/international), size (small/large), style (value/growth) is critical in controlling risk. If you can’t determine your personal, optimal risk profile, then find an experienced and knowledgeable investment advisor to assist you.

With the advent of the internet and mobile communication, our brains and amygdala continually get bombarded with fearful stimuli, leading to disastrous decision-making and damaging portfolio outcomes. Turning off the TV and selectively choosing the proper investment advice is paramount in keeping your amygdala in check. Your lizard brain may protect you from getting eaten by a lion, but falling prey to this structural brain flaw may eat your investment portfolio alive.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The European Dog Ate My Homework

I never thought my daily routine would be dominated by checking European markets before our domestic open, but these days it is appearing like the European tail is wagging the global dog. Tracking Spanish bond yields from the Tesoro Publico and the Italia Borsa index is currently having a larger bearing on my portfolio than U.S. fundamentals. When explaining short term performance to others, I feel a little like an elementary school student making an excuse that my dog ate my homework.

Although the multi-year European saga has gone on for years, this too shall pass. What’s more, despite the bailouts of Portugal, Ireland, and Greece in recent years, the resilient U.S. economy has recorded 11 consecutive quarters of GDP (Gross Domestic Product) growth and added more than 4 million jobs, albeit at a less than desirable pace.

Could it get worse? Certainly. Will it get worse before it gets better? Probably. Is worsening European fundamentals and a potential Greek eurozone exit already factored into current stock prices? Possibly. The truth of the matter is that nobody knows the answers to these questions with certainty. At this point, the probability of an unknown or unexpected event in a different geography is more likely to be the cause of our economic downfall than a worsening European crisis. As sage investor and strategist Don Hays aptly points out, “When everyone is concerned about a problem, that problem is solved.” That may be overstating the truth a bit, but I do believe the issues absent from current headlines are the matters we should be most concerned about.

The European financial crisis may drag on for a while longer, but nothing lasts forever. Years from now, worries about the PIIGS countries (Portugal, Ireland, Italy, Greece, Spain) will switch to others, like the BRICs (Brazil, Russia, India, China) or other worry geography du jour. The issues of greatest damage in 2008-2009, like Bear Stearns, Lehman Brothers, AIG, CDS (credit default swaps), and subprime mortgages, didn’t dominate the headlines for years like the European crisis stories of today. As compared to Europe’s problems, these prior pains felt like Band Aids being quickly ripped off.

Correlation Conundrum

Eventually European worries will be put on the backburner, but until some other boogeyman dominates the daily headlines, our financial markets will continue to correlate tightly with European security prices. How does one fight these tight correlations? For starters, the correlations will not stay tight forever. If an investor can survive through the valley of strong security association, then the benefits will eventually accrue.

Although the benefits from diversification may disappear in the short-run, they should not be fully forgotten. Bonds, cash, and precious metals (i.e., gold) proved to be great portfolio diversifiers in 2008 and early 2009. Commodities, inflation protection, floating rate bonds, real estate, and alternative investments, are a few asset classes that will help diversify portfolios. Risk is defined in many circles as volatility (i.e., standard deviation) and combining disparate asset classes can lower volatility. But risk, defined as the potential of experiencing permanent losses, can also be controlled by focusing on valuation. By in large, large cap dividend paying stocks have struggled for more than a decade, despite equity dividend yields for the S&P 500 exceeding 10-year Treasury yields (the first time in more than 50 years). Investing in large companies with strong balance sheets and attractive growth prospects is another strategy of lowering portfolio risk.

Politics & Winston Churchill

Some factors however are out of shareholders hands, such as politics. As we know from last year’s debt ceiling melee and credit downgrade debacle, getting things done in Washington is very challenging. If you think achieving consensus in one country is difficult, imagine what it’s like in herding 17 countries? That’s the facts of life we are dealing with in the eurozone right now.

Although I am optimistic something will eventually get done, I consider myself a frustrated optimist. I am frustrated because of the gridlock, but optimistic because these problems are not rocket science. Rather these challenges are concepts my first grade child could understand:

• Expenses are running higher than revenues. You must cut expenses, increase revenues, or a combination thereof.

• Adding debt can support growth, but can lead to inflation. Cutting debt can hinder growth, but leads to a more sustainable fiscal state of wellbeing.

Relieving all the excess global leverage is a long, tortuous process. We saw firsthand here in the U.S. what happened to the U.S. real estate market and associated financial institutions when irresponsible debt consumption took place. Fortunately, corporations and consumers adjusted their all-you-can-eat debt buffet habits by going on a diet. As a matter of fact, corporations today are holding records amounts of cash and debt service loads for consumers has been reduced to levels not seen in decades (see chart below). Unlike governments, luckily CEOs and individuals do not need Congressional approval to adapt to a world of reality – they can simply adjust spending habits.

Source: Calafia Beach Pundit (Scott Grannis)

Governments, on the other hand, generally do need legislative approval to adjust spending habits. Regrettably, cutting the benefits of your constituents is not a real popular political strategy for accumulating votes or brownie points. If you don’t believe me, see what voters are doing to their leaders in Europe. Nicolas Sarkozy is the latest European leader to be booted from office due to austerity backlash and economic frustration. No less than nine European leaders have been cast aside since the financial crisis began.

The fate for U.S. politicians is less clear as we enter into a heated presidential election over the next six months. We do however know how the mid-term Congressional elections fared for the incumbents…not all sunshine and roses. Until elections are completed, we are resigned to the continued mind-numbing political gridlock, with no tangible resolutions to the trillion dollar deficits and gargantuan debt load. Obviously, most citizens would prefer a forward looking strategic plan from politicians (rather than a reactive one), but there are no signs that this will happen anytime soon…in either party.

Realistically though, tough decisions made by politicians only occur during crises, and if this slow-motion train wreck continues along this same path, then at least we have something to look forward to – forced resolution. We are seeing this firsthand in Greece. The “bond vigilantes” (see Plumbers & Cops) and responsible parents (i.e., Germany) have given Greece two options:

1.) Fix your financial problems and receive assistance; or

2.) Leave the EU (return to the Drachma currency) and figure your problems out yourself.

Panic has a way of forcing action, and we are approaching that “when push comes to shove” moment very quickly. I believe the Europeans are currently taking a note from our strategic playbook, which basically is the spaghetti approach – throw lots of things up on the wall and see what sticks. Or as Winston Churchill stated, “You can always count on Americans to do the right thing – after they’ve tried everything else.”

There is no question, the European sovereign debt issue is a complete mess, and there are no clear paths to a quick solution. Until voters force politicians into making tough unpopular decisions, or leaders come together with forward looking answers, the default position will be to keep kicking the fiscal can issues down the road. In the absence of political leadership, eventually the crisis will naturally force tough decisions to be made. Until then, I will go on explaining to others how the European dog ate my homework.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including commodities, inflation protection, floating rate bonds, real estate, dividend, and alternative investment ETFs), but at the time of publishing SCM had no direct position in AIG, JNJ, Bear Stearns, Lehman Brothers, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Skiing Portfolios Down Bunny Slopes

Oh Nelly, take it easy…don’t get too crazy on that bunny slope. With fall officially kicking off and the crisp smell of leaves in the air, the new season also marks the beginning of the ski season. In many respects, investing is a lot like skiing. Unfortunately, many investors are financially skiing their investment portfolios down a bunny slope by stuffing their money in low yielding CDs, money market accounts, and Treasury securities. The bunny slope certainly feels safe and secure, but many investors are actually doing more long-term harm than good and could be potentially jeopardizing their retirements.

Let’s take a gander at the cautious returns offered up from the financial bunny slope products:

Source: Bankrate.com

That CD earning 1.21% should cover a fraction of your medical insurance premium hike, or if you accumulate the interest from your money market account for a few years, perhaps it will cover the family seeing a new 3-D movie. If you also extend the maturity on that CD a little, maybe it can cover an order of chicken fingers at Applebees (APPB)?!

We all know, for much of the non-retiree population, the probability that entitlement programs like Social Security and Medicare will be wiped out or severely cut is very high. Not to mention, life expectancies for non-retirees are increasing dramatically – some life insurance actuarial tables are registering well above 100 years old. These trends indicate the criticalness of investing efficiently for a large swath of the population, especially non-retirees.

Let’s Face It, One Size Does Not Fit All

Bodie Miller & Grandpa

As I have pointed out in the past, when it comes to investing (or skiing), one size does not fit all (see article). Just as it does not make sense to have Bode Miller (32 year old Olympic gold medalist) ski down a beginner’s bunny slope, it also does not make sense to take a 75-year old grandpa helicopter skiing off a cornice. The same principles apply to investment portfolios. The risk one takes should be commensurate with an individual’s age, objectives, and constraints.

Often the average investor is unaware of the risks they are taking because of the counterintuitive nature of the financial market dangers. In the late 1990s, technology stocks felt safe (risk was high). In the mid-2000s, real estate felt like a sure bet (risk was high), and in 2010, Treasury bonds and gold are currently being touted as sure bets and safe havens (read Bubblicious Bonds and Shiny Metal Shopping). You guess how the next story ends?

Unquestionably, coasting down the bunny slopes with CDs, money market accounts, and Treasuries is prudent strategy if you are a retiree holding a massive nest egg able to meet all your expenses. However, if you are younger non-retiree and do not want to retire on mac & cheese or work at Wal-Mart as a greeter into your 80s, then I suggest you venture away from the bunny slope and select a more suitable intermediate path to financial success.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, and WMT, but at the time of publishing SCM had no direct position in APPB, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Avoiding Automobile and Portfolio Crashes

Personal opinions of oneself don’t always mirror reality. Self perceptions relating to both driving and investing can be inflated. For example, the National Highway Traffic Safety Administration (NHTSA) reports that 95% of crashes are caused by human error, but 75% of drivers say they are better drivers than most.

Contributing factors to crashes include: 1) Distractions; 2) Alcohol; 3) Unsafe behavior (i.e., speeding); 4) Time of day (fatality rate is 3x higher at night); 5) Lack of safety belt; 6) Weather; and 7) Time of week (weekends are worst crash days).

A spokesman for the Insurance Institute for Highway Safety is quick to point out that driving behind the wheel is the riskiest activity most people engage in on a daily basis – more than 40,000 driving related fatalities occur each year. Careful common sense helps while driving, but driving sober at 4 a.m. (very few drivers on the road) on a weekday with your seatbelt on won’t hurt either.

Avoiding a Portfolio Crash

Another dangerous activity frequently undertaken by Americans is investing, despite people’s inflated beliefs of their money management capabilities. Investing, however, does not have to be harmful if proper precautions are taken.

Here is some of the hazardous behaviors that should be avoided by those maneuvering an investment portfolio:

1) Trading Too Much: Excessive trading leads to undue commissions, transaction costs, bid-ask spread, impact costs. Many of these costs are opaque or invisible and won’t necessarily be evident right away. But like a leaky boat, direct and indirect trading costs have the potential of sinking your portfolio.

2) Worrying about the Economy Too Much: The country experiences about two recessions a decade, nonetheless our economy continues to grow. If macroeconomics still worry you, then look abroad for even healthier growth – considerable international exposure should aid the long-term success of your portfolio and assist you in sleeping better at night.

3) Emotionally Reacting – Not Objectively Planning: News is bad, so sell. News is good, so buy. This type of conduct is a recipe for portfolio disaster. Better to do as Warren Buffett says, “Be fearful when others are greedy, and be greedy when others are fearful.” The long-term fundamental prospects for any investment are much more important than the daily headlines that get the emotional juices flowing.

4) Hostage to Short-term Time Horizon: Rather than worry about the next 10 days, you should be focused on the next 10 years. The further out you can set your time horizon, the better off you will be. Patience is a virtue.

5) Incongruent Portfolio with Risk: Many retirees got caught flat-footed in the midst of the global financial crisis of 2008-09 with investment portfolios heavy in equities and real estate. Diversified portfolios including fixed-income, commodities, international exposure, cash, and alternative investments should be optimized to meet your specific objectives, constraints, risk tolerance, and time horizon.

6) Timing the Market: Attempting to time the market can be hazardous to your investment health (see Market Timing article). If you really want to make money, then avoid the masses – the grass is greener and the eating better away from the herd.

Driving and investing can both be dangerous activities that command responsible behavior. Do yourself a favor and protect yourself and your portfolio from crashing by taking the appropriate precautions and avoiding the common hazardous mistakes.

Read Full Forbes Article on Driving Dangers

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct positions in any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Markowitz’s Five Dimensions of Risk

Eighty-two year old Harry Markowitz, 1990 Nobel Prize winner, is best known for his creation of Modern Portfolio Theory (MPT) in the 1950s. MPT elegantly combines mathematical variables such that investors can theoretically maximize returns while minimizing risk with the aid of diversification. Markowitz’s Efficient Frontier research eventually led to the future breakthrough of the Capital Asset Pricing Model (CAPM).

The Different Faces of Risk

Before we dive further into Markowitz’s dimensions of risk, let’s explore the definitions of the word “risk.” Just like the word “love” is interpreted differently by different people, so too does risk. To some, risk is defined as the probability of loss. To mathematicians, risk often means the historical volatility in returns as measured by standard deviation or Beta. For many individual investors, risk is frequently mischaracterized by emotions – risk is believed to be high after market collapse and low after extended market rallies (see also Wobbling Risk Tolerances article).

The Five Dimensions of Risk

With the procedural definitions of risk behind us, we can take a deeper look at risk from the eyes of Markowitz. Beyond the complex mathematical equations, Markowitz also understands risk from the practical investor’s standpoint. In a recent Financial Advisor magazine article Markowitz reviews the five dimensions of risk exposure:

1) Time Horizon

2) Liquidity Needs

3) Net Income

4) Net Worth

5) Investing Knowledge/Attitudes on Risk

Rather than pay attention to these practical dimensions of individual risk tolerance, countless investors adjust their risk exposure (equity allocation) by speculating on the direction of the stock market, which usually means buying high and selling low at inopportune times. Although it can be entertaining to guess the direction of the market, we all know market timing is a loser’s game in the long-run (see also Market Timing Treadmill article). Markowitz’s first four risk exposures are fairly straightforward, measurable factors, however the fifth exposure (“knowledge and attitude”) is much more difficult to measure. Determining risk attitude can be an arduous process if risk tolerance constantly wavers through the winds of market volatility.

The Double Whammy

Rather than becoming a nervous Nelly, constantly chomping on your finger nails, your investment focus should be on action, and the things you can control. The number one goal is simple….SAVE. How does one save? All one needs to do is spend less than they take in. Like dieting, saving is easy to understand, but difficult to execute. You can either make more money, spend less, or better yet… do both.

The Baby Boomers are not completely out of the woods, but the next generations (X, Y, Z, etc.) is even worse off because they face the “Double Whammy.” Not only are life expectancies continually increasing but the Social Security safety net is becoming bankrupt. Consider the average life expectancy was roughly 30 years old in 1900 and in developed countries today we stand at about 78 years. Some actuarial tables are peaking out at 120 years now (see also Brutal Reality to Aging Demographics). So when considering Markowitz’s risk exposure #1 (time horizon), it behooves you to calibrate your risk tolerance to match a realistic life expectancy (with some built-in cushion if modern medicine does a better job).

Taming the Wild Beast

Every investor’s risk profile is multi-dimensional and constantly evolving due to changes in Markowitz’s five risk exposures (time horizon, liquidity needs, net income, net worth, and knowledge/attitude). Risk can be a wild animal difficult to tame, but if you can create a disciplined, systematic investment plan, you too can reach your financial goals without getting bitten by the numerous retirement hazards.

Read the complete Financial Advisor article on Harry Markowitz

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing had no direct positions in any security mentioned in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Soros on the Super Bubble

Like a bubble formed from chewing gum, the gradual expansion of the spherical formation occurs much slower than the immediacy of the pop. A minority of investors identified the treacherous, credit-induced bubble of 2008 before it burst, however not included in that group are financial regulators. Now we’re left with the task of cleaning up the sticky mess on our faces and establishing measures to prevent future blow-ups.

George Soros, Chairman of Soros Fund Management and author of The Crash of 2008, has been around the financial market block a few times, so I think it pays to heed the regulatory reform recommendations as it relates to the “Super bubble” of 2008. As you probably know, financial bubbles are not a new concept. Beyond the oft-mentioned technology and real estate bubbles of this decade, bubbles such as the “Tulip-mania” of the 1630s serve as a gentle reminder of the everlasting existence of irrational economic behavior. If the Dutch were willing to pay $76,000 for a tulip bulb (inflation-adjusted) almost 400 years ago, then virtually any mania is possible.

Bubbles and Efficiency

Efficient markets are somewhat like UFOs. Some people believe in them, but many do not. In order to believe in the existence of bubbles, one needs to question the validity of the pure form of efficient markets (read more about market efficiency). Here’s how Soros feels about market efficiency:

“I contend that financial markets always present a distorted picture of reality.”

I believe we will be in a hyper-sensitive period of bubble witch-hunting for a while, as the fresh wounds of 2008-09 heal themselves. If you get in early enough, bubbles can be profitable. Unfortunately, like a distracted teen fixated on the sunbathers at a nude beach, the excitement can lead to a painful burn if preventative sunscreen measures are not taken. Most bubble participants are too exhilarated to carry out a thoughtful exit strategy – the news can just be too tempting to jump off the top.

In his analysis of market regulation, Soros lays some of the “Great Recession” blame on the Federal Reserve and Alan Greenspan (Chairman of Fed):

“Instead of a tendency towards equilibrium, financial markets have a tendency to develop bubbles. Bubbles are not irrational: it pays to join the crowd, at least for a while. So regulators cannot count on the market to correct its excesses…The crash of 2008 was caused by the collapse of a super-bubble that has been growing since 1980. This was composed of smaller bubbles. Each time a financial crisis occurred the authorities intervened, took care of the failing institutions, and applied monetary and fiscal stimulus, inflating the super-bubble even further.”

Soros’ Recipe for Reform

What is Soros’ solution for the “Super bubble?” Here are some recommendations from his Op-Ed in the Financial Times:

- Regulator Accountability: First of all, financial authorities need to accept responsibility for preventing excesses – excuses are not an acceptable response.

- Control Credit: Rather than having static monetary targets such as margin requirements, capital reserve requirements, and loan-to-value ratios, Soros argues these metrics can be adjusted in accordance with the swinging moods of economic cycles. He punctuates the point by saying, “To control asset bubbles it is not enough to control the money supply; you must also control credit.”

- Limit Overheating in Specific Sectors: Had regulators limited lending during the real estate explosion or had the SEC limited technology IPOs in the late 1990s, perhaps our country would be in better financial health today.

- Manage Derivatives and Systemic Risk: Basically what Soros is saying here is that many market participants can become overwhelmed by certain exposures or exotic instruments, therefore it behooves regulators to proactively step in and regulate.

- Manage Too Big to Fail (read related Graham IC article): According to Soros a big reason we got into this trouble relates to the irresponsible proprietary trading departments at some of the larger banks. Responsibly separating these departments and limiting the amount of risk undertaken is an important element to the safety of our financial system.

- Reformulate Asset Holding Rules: Underestimating the risk profile of a certain security can lead to concentration issues, which can potentially generate systemic risk. Soros highlights the European Basel Accord rules as an area that can use some improvement.

Soros admits most, if not all, the measures he proposes will choke off the profitability of banks. For this reason, regulators must be very careful with the implementation and timing of these financial strategies. If employed too aggressively, the economy could find itself in a deflationary spiral. Move too slowly, and the loose monetary measures instituted by the Fed could fan the flames of inflation.

Bubbles will never go away. Eventually, the recent panic-induced fear will fade away and the entrepreneurial seeds of greed will germinate into new budding flowers of optimism. As investors nervously chomp away at their chewing gum, I will patiently await for the next financial bubble to form. I echo George Soros’s hope that regulators prick future “mini-bubbles” before they become “super-bubbles.”

Read Full George Soros Op-Ed on The Financial Times 10/25/09

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at time of publishing had no direct positions in an security referenced. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

One Size Does Not Fit All

When you go shopping for a pair of shoes or clothing what is the first thing you do? Do you put on a blindfold and feel for the right size? Probably not. Most people either get measured for their personal size or try on several different outfits or shoes. When it comes to investments, the average investor makes uninformed decisions and in many instances relies more on what other advisors recommend. Sometimes this advice is not in the best interest of the client. For example, some broker recommendations are designed to line their personal pockets with fees and/or commissions. In some cases the broker may try to unload unpopular product inventory that does not match the objectives and constraints of the client. Because of the structure of the industry, there can be some inherent conflicts of interest. As the famous adage goes, “You don’t ask a barber if you need a haircut.”

Tabulate Inventory

A more appropriate way of managing your investment portfolio is to first create a balance sheet (itemizing all your major assets and liabilities) individually or with the assistance of an advisor (see “What to Do” article) – I recommend a fee-only Registered Investment Advisor (RIA)* who has a fiduciary duty towards the client (i.e., legally obligated to work for the best interest of the client). Some of the other major factors to consider are your short-term and long-term income needs (liquidity important as well) and your risk tolerance.

Risk Appetites

The risk issue is especially thorny because the average investor appetite for risk changes over time. Typically there is also a significant difference between perceived risk and actual risk.

For many investors in the late 1990s, technology stocks seemed like a low risk investment and everyone from cab drivers to retired teachers wanted into the game at the exact worst (riskiest) time. Now, as we have just suffered through the so-called Great Recession, the risk pendulum has swung back in the opposite direction and many investors have piled into what historically has been perceived as low-risk investments (e.g., Treasuries, corporate bonds, CDs, and money market accounts). The problem with these apparently safe bets is that some of these securities have higher duration characteristics (higher price volatility due to interest rate changes) and other fixed income assets have higher long-term inflation risk.

Source (6/30/09): Morningstar Encorr Analyzer (Ibbotson Associates) via State Street SPDR Presentation

A more objective way of looking at risk is by looking at the historical risk as measured by the standard deviation (volatility) of different asset classes over several time periods. Many investors forget risk measurements like standard deviation, duration, and beta are not static metrics and actually change over time.

Diversification Across Asset Classes Key

Source: State Street Global Advisors (June 30, 2009)

Correlation, which measures the price relationship between different asset classes, increased dramatically across asset classes in 2008, as the global recession intensified. However, over longer periods of time important diversification benefits can be achieved with a proper mixture of risky and risk-free assets, as measured by the Efficient Frontier (above). Conceptually, an investor’s main goal should be to find an optimal portfolio on the edge of the frontier that coincides with their risk tolerance.

Tailor Portfolio to Changing Circumstances

In my practice, I continually run across clients or prospects that initially find themselves at the extreme ends of the risk spectrum. For example, I was confronted by an 80 year old retiree needing adequate income for living expenses, but improperly forced by their broker into 100% equities. On the flip side, I ran into a 40 year old who decided to allocate 100% of their retirement assets to fixed income securities because they are unsure of stocks. Both examples are inefficient in achieving their different investment objectives, yet there are even larger masses of the population suffering from similar issues.

In my practice, I continually run across clients or prospects that initially find themselves at the extreme ends of the risk spectrum. For example, I was confronted by an 80 year old retiree needing adequate income for living expenses, but improperly forced by their broker into 100% equities. On the flip side, I ran into a 40 year old who decided to allocate 100% of their retirement assets to fixed income securities because they are unsure of stocks. Both examples are inefficient in achieving their different investment objectives, yet there are even larger masses of the population suffering from similar issues.

Financial markets and client circumstances are constantly changing, so the objectives of the portfolio should be periodically revisited. One size does not fit all, so it’s important to construct the most efficient customized portfolio of assets that meets the objectives and constraints of the investor. Take it from me, I’m constantly re-tailoring my wardrobe (like my investments) to meet the needs of my ever-changing waistline.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: For disclosure purposes, Sidoxia Capital Management, LLC is a Registered Investment Advisor (RIA) certified in the State of California. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Howard Right on the Mark(s)

Legendary investor Howard Marks opines on the financial markets in his recently quarterly client memo. One should pay attention to these battle-tested veterans with scars to prove their survival skills. Rather than neatly package a common theme from the long document I will highlight a few areas.

Marks is cautious but sees better buying opportunities ahead.

Recent Past vs. Long Past: For most of the 16 page memo Howard Marks reminisces on his 40+ years in the investment industry and contrasts the 2003-2007 period with the majority of his years. He states in the old days, “There were no swaps, index futures or listed options. Leverage wasn’t part of most institutional investors’ arsenal…or vocabulary. Private equity was unknown, and hedge funds were too few and outré to matter. Innovations like quantitative investing and structured products had yet to arrive, and few people had ever heard of ‘alpha.'”

Marks on Siegel: Marks targets Wharton Professor Jeremy Siegel as a contributor to the overly bullish mentality of 2003-2007, “Siegel’s research was encyclopedic and supported some dramatic conclusions, perhaps foremost among them his showing that there’s never been a 30-year period in which stocks didn’t outperform cash, bonds and inflation…but…30 years can be a long time to wait.”

Marks on Risk: “So yes, it’s true that investor’s can’t expect to make much money without taking risk. But that’s not the same as saying risk taking is sure to make you money…If risky investments always produced high returns, they wouldn’t be risky.” On the psychological impacts of risk, Marks goes on to say, “When investors are unworried and risk-tolerant, they buy stocks at high p/e ratios and private companies at high EBITDA multiples, and they pile into bonds despite narrow yield spreads and into real estate at minimal “cap rates.'”

On Quant Models and Business Schools: Marks quotes Warren Buffet regarding the complexity of quantitative models, “If you need a computer or a calculator to make a calculation, you shouldn’t buy it.” Charlie Munger adds his two cents on why quantitative models exist: “They teach that in business schools because, well, they’ve got to do something.”

Investing as a Mixture of Art & Science: In my book I describe investing as a combination of “Art” and “Science.” Marks addresses a s similar insight through an Albert Einstein quote:

“Not everything that can be counted counts, and not everything that counts can be counted.”

Views on the Credit Rating Agencies: To highlight the absurdity of the mortgage credit rating system, Marks compares the agencies’ ratings to hamburger: “If it’s possible to start with 100 pounds of hamburger and end up selling ten pounds of dog food, 40 pounds of sirloin and 50 pounds of filet mignon, the truth-in-labeling rules can’t be working.”

If you would like to access the remainder of memo, click here to read the rest. Overall, Mr. Marks gives a balanced view of the markets and economy, but feels “better buying opportunities lie ahead.” Thankfully, I’m finding some myself.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

{kind=link}