Posts tagged ‘risk aversion’

Head Fakes Surprise as Stocks Hit Highs

In a world of seven billion people and over 200 countries, guess what…there are a plethora of crises, masses of bad people, and plenty of lurking issues to lose sleep over.

The fear du jour may change, but as the late-great investor Sir John Templeton correctly stated:

“Bull markets are born on pessimism and they grow on skepticism, mature on optimism, and die on euphoria.”

And for the last decade since the 2008-2009 Financial Crisis, it’s clear to me that the stock market has climbed a lot of worry, pessimism, and skepticism. Over the last decade, here is a small sampling of wories:

With over five billion cell phones spanning the globe, fear-inspiring news headlines travel from one end of the world to the other in a blink of an eye. Fortunately for investors, the endless laundry list of crises and concerns has not broken this significant, multi-year bull market. In fact, stock prices have more than tripled since early 2009. As famed hedge fund manager Leon Cooperman noted:

“Bull markets don’t die from old age, they die from excesses.”

On the contrary to excesses, corporations have been slow to hire and invest due to heightened risk aversion induced by the financial crisis. Consumers have saved more and lowered personal debt levels. The Federal Reserve took unprecedented measures to stimulate the economy, but these efforts have since been reversed. The Fed has even signaled its plan to reduce its balance sheet later this year. As the expansion has aged, corporations and consumer risk aversion has abated, but evidence of excesses remains paltry.

Investors may no longer be panicked, but they remain skeptical. With each subsequent new stock market high, screams of a market top and impending recession blanket headlines. As I pointed out in my March Madness article, stocks have made new highs every year for the last five years, but continually I get asked, “Wade, don’t you think the market is overheated and it’s time to sell?”

For years, I have documented the lack of stock buying evidenced by the continued weak fund flow sales. If I could summarize investor behavior in one picture, it would look something like this:

Corrections have happened, and will continue to occur, but a more significant decline will likely happen under specific circumstances. As I point out in Half Empty, Half Full?, the time to become more cautious will be when we see a combination of the following trends occur:

- Sharp increase in interest rates

- Signs of a significant decline in corporate profits

- Indications of an economic recession (e.g., an inverted yield curve)

- Spike in stock prices to a point where valuation (prices) are at extreme levels and skeptical investor sentiment becomes euphoric

Attempting to predict a market crash is a Fool’s Errand, but more important for investors is periodically reviewing your liquidity needs, time horizon, risk tolerance, and unique circumstances, so you can optimize your asset allocation. There will be plenty more head fake surprises, but if conditions remain the same, investors should not be surprised by new stock highs.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Investors Perilously Wait for Goldilocks Market

Like Goldilocks searching for the “just right” porridge, chair size, and bed, so too are investors searching for the Goldilocks stock market that is not too hot or too cold. Many are aptly calling this the “most hated” bull market in recent history as Goldilock investors have decided to stay home rather than look for an investment prize. What many investors don’t quite realize is that waiting too long for an elusive, perfect Goldilocks scenario will only lead to your portfolio getting eaten by unhappy bears.

Waiting on the sidelines for a perfect buy signal is a hopeless endeavor (see also Getting Off the Market Timing Treadmill). The evidence for extreme risk aversion is extensive. From a corporate standpoint, it’s clear executives and board members have been scarred by the 2008-2009 financial crisis. Management teams have been quick to cut expenses and slow to invest and hire. And speaking of hiring, the post-crisis expansion has led to the slowest job recovery since World War II.

In the face of all the investor pessimism, the economy has been adding a few million jobs per year on average, resulting in a unemployment level below 5%; corporate profits at/near record levels; and trillions of dollars of cash piling up on corporate balance sheets. Rather than accelerate investments, companies have by and large chosen to spend that mountain of cash into trillions of rising dividends and share buybacks.

Risk aversion is evident at the individual level as well. Part of the explanation of why corporations have increased dividends to record levels is due to 76 million Baby Boomers approaching or entering retirement. Boomers need more income just as interest rates are rapidly approaching 0%, and in many cases negative interest rates, which effectively means they are earning $0 on their bank savings and losing to inflation.

Collecting fatter dividend checks from stocks actually sounds pretty attractive when individual investors are scared silly about geopolitics, terrorism, elections, Zika virus, and other horror story headlines of the day. Fortunately, it’s profits, interest rates, valuations, and contrarian sentiment indicators that control the stock market (see Follow the Stool), and not Fox, CNN, ABC, NBC, and internet bloggers (myself included).

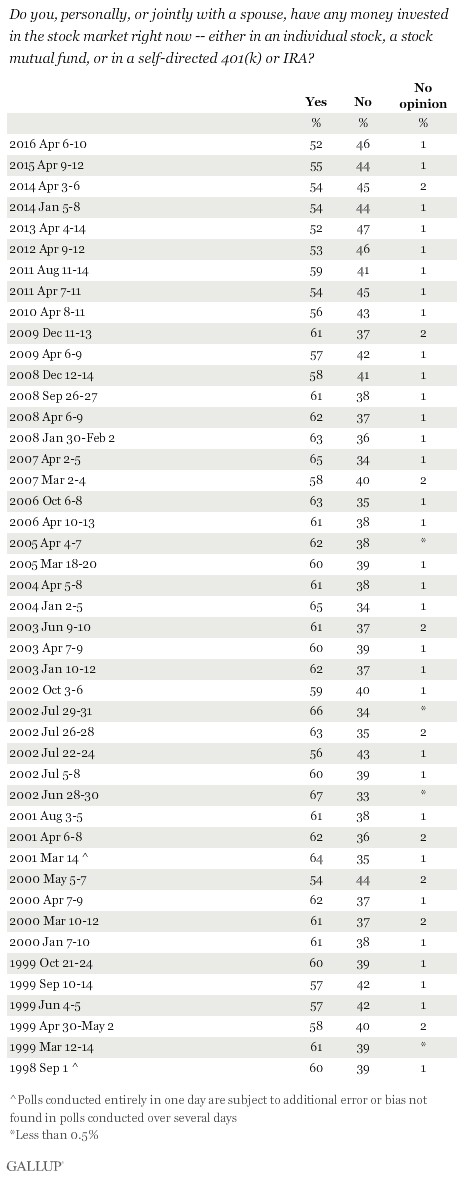

With all this scary news, no wonder investors are afraid to invest. Gallup conducted a survey earlier this year asking investors whether they were invested in the stock market. With the stock market at or near record all-time highs, stock ownership should be up…right? Wrong! The Gallup results showed stock ownership at its lowest level in 18 years, as long as results have been tabulated (1998).

In case you are still skeptical, we can point to other evidence of investor skepticism. If you believe, like I do, that actions speak louder than words, then the actions of individuals are screaming with risk aversion at the top of their lungs. In order to understand how frightened individuals are, all you have to do is look at the more than $8 trillion (with a “t”) of cash sitting in personal savings accounts earning nothing (see chart below).

Source: Calafia Beach Pundit

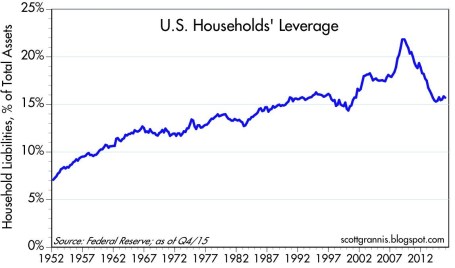

You can see from the chart above, the slope of cash accumulation accelerated at a steeper slope after the Great Recession. Besides allowing the mountain of cash to pile up, what else have investors been doing with their greenbacks? One thing for sure is individuals have been spooked into paying down debt (reducing leverage), as you can see from the chart below.

Source: Calafia Beach Pundit

As Warren Buffett reminds investors, it is best to “buy fear, and sell greed.” There is plenty of other evidence, including the examples above, that shows most average investors are destructive by doing the opposite…they buy greed, and sell fear. Sadly, sitting on the sidelines with cash stuffed under your mattress, earning nothing and losing to inflation, is not the optimal strategy for long-term wealth creation and preservation. Investors can continue waiting for Goldilock conditions, but unfortunately, history reminds us that market timing, sideline-sitters are likely to get eaten by the bears.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The New Abnormal: Living with Negative Rates

Pimco, the $1.5 trillion fixed-income manager located a stone’s throw distance from my office in Newport Beach, famously (or infamously) coined the phrase, “New Normal”. As former Pimco CEO (Mohamed El-Erian) described years ago, around the time of the Great Recession, the New Normal “reflects a growing realization that some of the recent abrupt changes to markets, households, institutions, and government policies are unlikely to be reversed in the next few years. Global growth will be subdued for a while and unemployment high.”

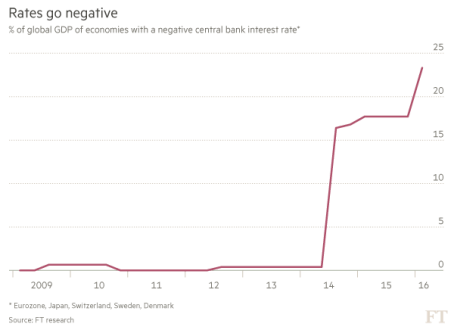

As it turns out, El-Erian was completely wrong in some respects and shrewdly prescient in others. For instance, although the job recovery has been one of the slowest in a generation, 14.5 million private sector jobs have been added since 2010, and the unemployment rate has been more than halved from 10% in early 2009, to below 5% today. However, the pace of global growth has been relatively weak since the 2008-2009 financial crisis, which has forced central banks all over the world to lower interest rates in hope of stimulating growth. Monetary policies around the globe have been cut so much that almost 25% of global GDP is tied to countries with negative interest rates (see chart below).

Source: Financial Times

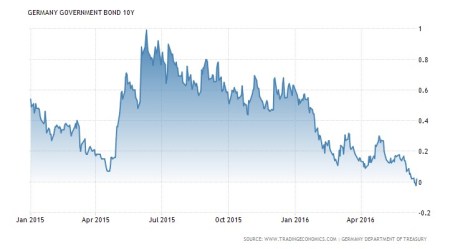

The European central banks started the sub-zero trend in 2014, and the Bank of Japan recently joined the central banks of Denmark, Sweden and Switzerland in negative territory. The negative short-term rate virus has spread further to long-term bonds as well, as evidenced by the 10-Year German Bund (sovereign bond) yield, which crossed into negative territory last week (see chart below).

Source: TradingEconomics.com

The New Abnormal

The unprecedented post-crisis move to a 0% Fed Funds rate target, along with the implementation of Quantitative Easing (QE) by former Federal Reserve Chairman Ben Bernanke, was already pushing the envelope of “normal” stimulative monetary policy. Nevertheless, central banks pushing rates to a negative threshold takes the whole stimulus discussion to another level because investors are guaranteed to lose money if they hold these bonds until maturity.

As we enter this new submerged rate phase, this activity can only be described as abnormal…not normal. Preserving money at a 0% level and losing value to inflation (i.e., essentially stuffing money under the proverbial mattress) is a bitter enough pill to swallow. Paying somebody to lend them money gives “insanity” a good name.

The stimulative objectives of negative interest policies established by central bankers may be purely intentioned, however there can be plenty of unintentional consequences. For starters, negative rates can produce too much of a good thing, in the form of excess borrowing or leverage. In addition, retirees and savers across a broad spectrum of ages are getting crushed by the paltry rates, and bank profit margins (net interest margins) are getting squeezed to boot.

Another unintended consequence of negative rate policies could be a polar opposite outcome to the envisioned stimulative design. Scott Mather, a co-portfolio manager of the $86 billion PIMCO Total Return Fund (PTTRX) is making the case that these policies could be creating more economic contractionary effects than invigorating expansion. More specifically, Mather notes, “It seems that financial markets increasingly view these experimental moves as desperate and consequently damaging to financial and economic stability.”

Eventually, the cheap money deliberately created by central banks will result in a glut of risk-taking and defaults. However, despite all the cries from hawks protesting money printing policies, cautious bank lending behavior coupled with regulatory handcuffs have yet to create widespread debt bubbles. Certainly, oceans of cheap money can create pockets of problems, as I have identified and discussed in the private equity market (see also Dying Unicorns), but supply and demand rule the day at some point.

In the end, as I have repeatedly documented, money goes where it is treated best. Realizing guaranteed losses while trapped in negative rate bonds is no way to treat your investment portfolio over the long-run. In the short-run, the safety and stability of short duration bonds may sound appealing, but ultimately rational and efficient behavior prevails. Why settle for 0% or negative rates when yields of 2%, 4%, and 6% can be found in plenty of other responsible investment alternatives?

Arguably, in this post financial crisis world we live in, we have transitioned from the New Normal to a New Abnormal environment of negative rates. Pundits and prognosticators will continue spewing fear-filled cautionary advice, but experienced, long-term investors will continue taking advantage of these risk averse markets by investing in a quality, diversified portfolio of superior yielding investments. For now, there are plenty of opportunities to choose from, until the next phase of this economic cycle… when the New Abnormal transitions to the New Normalized.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds , but at the time of publishing had no direct position in PTTRX, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Decision Making on Freeways and in Parking Lots

Many drivers here in California adhere to the common freeway speed limit of 65 miles per hour, while some do not (I’ll take the 5th). In the vast majority of cases, racing to your destination at these faster speeds makes perfect sense. However, driving 65 mph through the shopping mall parking lot could get you killed, so slower driving is preferred in this instance. Ultimately, the specific environment and situation will dictate the rational and prudent driving speed. Decision making works in much the same way, and Daniel Kahneman, a Nobel Prize winner, has encapsulated his decades of research in psychology and economics in his most recent book, Thinking, Fast and Slow.

Much of Kahneman’s big ideas are analyzed through the lenses of “System 1” and “System 2” – the fast and slow decision-making processes persistently used by our brains. System 1 thinking is our intuition in the fast lane, continually making judgments in real-time. Our System 1 hunches are often correct, but because of speedy, inherent biases and periodic errors this process can cause us to miss an off-ramp or even cause a conclusion collision. System 2, on the other hand, is the slower, methodical decision-making process in our brains that keeps our hasty System 1 process in check. Although little mental energy is exerted by using System 1, a great deal of cerebral horsepower is required to use System 2.

Summarizing 512 pages of Kahneman’s book in a single article may be challenging, nevertheless I will do my best to summarize some of the interesting highlights and anecdotes. A multitude of Kahneman’s research is reviewed, but a key goal of the book is designed to help individuals identify errors in judgment and biases, in order to lower the prevalence of mental mistakes in the future.

Over Kahneman’s 50+ year academic career, he has uncovered an endless string of flaws in the human thought process. To bring those mistakes to life, he uses several mind experiments to illustrate them. Here are a few:

Buying Baseball: We’ll start off with a simple Kahneman problem. If a baseball bat and a ball cost a total of $1.10, and the bat costs $1 more than the ball, then how much does the ball cost? The answer is $0.10, right? WRONG! Intuition and the rash System 1 forces most people to answer $0.10 cents for the ball, but after going through the math it becomes clear that this gut answer is wrong. If the ball is $0.10 and the bat is $1 more, then that would mean the bat costs $1.10, making the total $1.20…WRONG! This is clearly a System 2 problem, which requires the brain to see a $0.05 ball plus $1.05 bat equals $1.10…CORRECT!

The Invisible Gorilla: As Kahneman points out, humans can be blind to the obvious and blind to our blindness. To make this point he references an experiment and book titled Invisible Gorilla, created by Chritopher Chabris and Daniel Simons. In the experiment, three players wearing white outfits pass a basketball around at the same time that a group of players wearing black outfits pass around a separate basketball. The anomaly in the experiment occurs when someone in a full-sized gorilla outfit goes prancing through the scene for nine full seconds. To the surprise of many, about half of the experiment observers do not see the gorilla. In addition, the gorilla-blind observers deny the existence of the large, furry animal when confronted with recorded evidence (see video below).

Green & Red Dice: In this thought experiment, Kahneman describes a group presented with a regular six-sided die with four green sides (G) and two red sides (R), meaning the probability of the die landing on green (G) is is much higher than the probability of landing on red (R). To make the experiment more interesting, the group is provided a cash prize for picking the highest probability scenario out of the following three sequences: 1) R-G-R-R-R; 2) G-R-G-R-R-R; and 3) G-R-R-R-R-R. Although most participants pick sequence #2 because it has the most greens (G) in it, if one looks more closely, sequence #2 is the same as #1 except for sequence #2 has an additional green (G). Therefore, the highest probability winning answer should be sequence #1 because sequence #2 adds an uncertain roll that may or may not land on green (G).

While the previous experiments described some notable human decision-making flaws, here are some more human flaws:

Anchoring Effect: Was Gandhi 114 when he died, or was Gandhi 35 when he died? Depending how the question is asked, asking the initial question first will skew the respondents answer to a higher age, because the respondents answer will be somewhat anchored to the number “114”. Similarly, the price a homebuyer would pay for a house will be influenced or anchored to the asking price. Another word used by some for anchoring is “suggestion”. If a subliminal suggestion is planted, people’s responses can become anchored to that idea.

Overconfidence: We encounter overconfidence in several forms, especially from what Kahneman calls the “Illusion of Pundits,” which is the confidence that comes with 20-20 hindsight experienced in our 24/7 media world. Or as Kahneman states in a different way, “The illusion that we understand the past fosters overconfidence in our ability to predict the future.” Driving is another example of overconfidence – very few people believe they are poor drivers. In fact, a well-known study shows that “90% of drivers believe they are better than average,” despite defying the laws of mathematics.

Risk Aversion: In Kahneman’s book, he also references risk aversion studies by Mathew Rabin and Richard Thaler. What the researchers discovered is that people appear to be irrational in the way they respond to certain risk scenarios. For example, people will turn down the following gambles:

A 50% chance to lose $100 and a 50% chance to win $200;

OR

A 50% chance to lose $200 and a 50% chance to win $20,000 .

Although rational math would indicate these are smart bets to take, however most people decline the game because humans on average weigh losses twice as much as gains (see also the Pleasure/Pain Principle). To get a better understanding of predictive human behavior, the real emotional costs of disappointment and regret need to be accounted for.

Truth Illusions: A reliable way to make people believe in falsehoods is through repetition. More exposure will breed more liking. In addition to normal conversations, these repetitive truth illusions can be witnessed in propaganda or advertising. Minimizing cognitive strain also reinforces points. Using bold, colored, and contrasted language is more convincing. Simpler language rather than more complex language is also more credible.

Narrative Fallacies: We humans have an innate desire to continually explain the causation of an event due to skill or stupidity – even if randomness is the best explanation.People try to make sense of the world, even though many outcomes have no straightforward explanation. Often times, a statistical phenomenon like “regression to the mean” can explain the results (i.e., outliers revert directionally toward averages). The “Sports Illustrated Jinx,” or the claim that a heralded cover story athlete will be subsequently cursed with bad performance, is used as a case in point. Actually, there is no jinx or curse, but often fickle luck disappears and athletic performance reverts to norms.

Kahneman on Stocks

Many of the principles in Kahneman’s book can be applied to the world of stocks and investing too. According to Kahneman, the investing industry has been built on an “illusion of skill,” or the belief that one person has better information than the other person. To make his point, Kahneman references research by Terry Odean, a finance professor at UC Berkely, who studied the records of 10,000 brokerage accounts of individual investors spanning a seven-year period and covering almost 163,000 trades. The net result showed dramatic underperformance by the individual traders and confirmed that stocks sold by the traders consistently did better than the stocks purchased.“Taking a shower and doing nothing” would have been better than the value destroying trading activity. In fact, the most active traders did much worse than those who traded the least. For professional managers the conclusions are not a whole lot different. “For a large majority of fund managers, the selection of stocks is more like rolling dice than like playing poker. Typically at least two out of every three mutual funds underperform the overall market in any given year,” says Kahneman. I don’t disagree, but I do believe, like .300 hitters in baseball, there are a few managers that can consistently outperform.

There are a lot of lessons to be learned from Daniel Kahneman’s book Thinking, Fast and Slow and I apply many of his conclusions to my investment practice at Sidoxia. We all race through decisions every day, but as he repeatedly points out, familiarizing ourselves with these common mental pitfalls, and also utilizing our more methodical and accurate System 2 thought process regularly, can create better decisions. Better decisions not only for our regular lives, but also for our investing lives. It’s perfectly OK to race down the mental freeway at 65 mph (or faster), but don’t forget to slow down occasionally, in order to avoid mental collisions.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Curious Case of Gen Y and Benjamin Button

If a current Gen Y-er aged backwards like Benjamin Button, he would feel right at home when it comes to investing, because acute conservatism and risk aversion have struck older and younger generations alike. The Curious Case of Benjamin Button is a story that follows the critical peaks and valleys of a boy born in his eighties, who immediately begins to reverse the aging process. Investors of all ages have suffered their peaks and valleys over the last decade, and these experiences have impacted investing attitudes and perceptions heavily during the prime earning years. For retirees, it’s virtually impossible for extreme events like the Great Depression, World War II, Vietnam, Kennedy’s assassination, and Nixon’s impeachment to NOT have had an influence on individuals’ investing behavior.

Investing Consequences on Younger Investors

If a younger Mr. Button were still alive today, there is no doubt the disheartening events experienced in his 80s would only become reinforced by the bleak occurrences in 2008-2009. His reverse aging would not only have allowed him to witness the collapse of Lehman Brothers, but also behold the demise and bailout of other gargantuan financial institutions. Today, if Benjamin wasn’t busy watching the MTV Video Music Awards, he would most likely be diligently managing his bullet-proof portfolio of cash, CDs (Certificates of Deposit), Treasury bills, and maybe some tax-free municipals if he was feeling a little spunky.

The cautious stance of youthful savers was confirmed in a recent study conducted by Merrill Lynch Global Wealth Management. The report demonstrates how the recent financial crisis has had a severe dampening impact on the risk appetites of 18-34 year old “Millennials.” So dramatic an effect was the recession, the nervous conservatism experienced by the 30-somethings was only rivaled by fear from 65 year olds. In fact, the 56% of young investors, who were more cautious today than a year ago, was the highest percentage registered by any age group.

Here’s what Christopher Geczy adjunct associate professor of finance at University of Pennsylvania’s Wharton School had to say about younger Millennials:

“We’re coming off a series of financial crises that hit this young generation at points in their lives where external events shape strong opinions…Many of them have witnessed a decline in the wealth of their families and seen their parents delay retirement or even return to the workforce.”

Beyond witnessing the challenges faced by their parents, the Millennials are encountering their own obstacles – such as joblessness. For those workers under age 35, the unemployment rate in August stood at more than 13% – significantly higher than the 9.6% national rate.

Note to Youths: Stocks for the Long Haul

In the typical life cycle of investing, investors flaunt a higher risk tolerance in their younger years and exhibit more risk aversion as they approach or enter retirement. Historically, this makes perfect sense because workers earlier in their careers have plenty of time to ride out the fluctuations associated with owning equities. Jeremy Siegel, professor at the Wharton University Professor, says stocks significantly outperform bonds by 6% per year over longer timeframes (see Siegel Digs in Heels).

For Gen Y-ers the larger risk is being too conservative, not too aggressive. Barry Nalebuff, a strategy professor at Yale’s School of Management agrees:

“The biggest risk for this generation is that they’ll live too long. With medical breakthroughs, the reality is that many of them will live beyond 100…The only way they have enough assets to last them is to invest in stocks. If they don’t, a lot of people will have to keep working way past when they want to because they won’t have enough money saved up.”

Even for those downbeat on the domestic equity markets – rightfully so with no price gains achieved over the last decade – younger investors should not lose sight of the tremendous equity opportunities available internationally (see the Blowing the Perfect Investment Game).

For many people, reverse aging may be fun for a while, but for Benjamin Button, living through the Great Depression and multiple wars as an adult would likely dampen the mood and increase risk aversion dramatically. Millennials have persevered through difficult times too. Generation Y has survived two recessionary bubbles caused by excessive technology spending and consumer credit binging, both over a short timeframe. Becoming too conservative for these investors will feel comfortable in the short-run if uncertainty continues to prevail. But investing now with adequate, diversified equity exposure is the prudent course of action. Even a wrinkly Benjamin Button could agree, wisely investing in some equities during your earlier career sure beats working as a Wal-Mart (WMT) greeter into your 80s.

Read the full Money-CNN and Newsweek articles on the subject

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and WMT, but at the time of publishing SCM had no direct position in BAC/Merrill, Lehman, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}

{kind=link}