Posts tagged ‘Qe3’

Bernanke: Santa Claus or Grinch?

I’ve written plenty about my thoughts on the Fed (see Fed Fatigue) and all the blathering from the media talking heads. Debates about the timing and probability of a Fed “taper” decision came to a crescendo in the recent week. As is often the case, the exact opposite of what the pundits expected actually happened. It was not a huge surprise the Federal Reserve initiated a $10 billion tapering of its $85 billion monthly bond buying program, but going into this week’s announcement, the betting money was putting their dollars on the status quo.

With the holiday season upon us, investors must determine whether the tapered QE1/QE2/QE3 gifts delivered by Bernanke are a cause for concern. So the key question is, will this Santa Claus rally prance into 2014, or will the Grinch use the taper as an excuse to steal this multi-year bull market gift away?

Regardless of your viewpoint, what we did learn from this week’s Fed announcement is that this initial move by the Fed will be a baby step, reducing mortgage-backed and Treasury security purchases by a measly $5 billion each. I say that tongue in cheek because the total global bond market has been estimated at about $80,000,000,000,000 (that’s $80 trillion).

As I’ve pointed out in the past, the Fed gets way too much credit (blame) for their impact on interest rates (see Interest Rates: Perception vs Reality). Interest rates even before this announcement were as high/higher than when QE1 was instituted. What’s more, if the Fed has such artificial influence over interest rates, then why do Austria, Belgium, Canada, Denmark, Finland, France, Germany, Japan, Netherlands, Sweden, and Switzerland all have lower 10-year yields than the U.S.? Maybe their central banks are just more powerful than our Fed? Unlikely.

Dow 128,000 in 2053

Readers of Investing Caffeine know I have followed the lead of investing greats like Warren Buffett and Peter Lynch, who believe trying to time the markets is a waste of your time. In a recent Lynch interview, earlier this month, Charlie Rose asked for Lynch’s opinion regarding the stock market, given the current record high levels. Here’s what he had to say:

“I think the market is fairly priced on what is happening right now. You have to say to yourself, is five years from now, 10 years from now, corporate profits are growing about 7 or 8% a year. That means they double, including dividends, about every 10 years, quadruple every 20, go up 8-fold every 40. That’s the kind of numbers you are interested in. The 10-year bond today is a little over 2%. So I think the stock market is the best place to be for the next 10, 20, 30 years. The next two years? No idea. I’ve never known what the next two years are going to bring.”

READ MORE ABOUT PETER LYNCH HERE

Guessing is Fun but Fruitless

I freely admit it. I’m a stock-a-holic and member of S.A. (Stock-a-holic’s Anonymous). I enjoy debating the future direction of the economy and financial markets, not only because it is fun, but also because without these topics my blog would likely go extinct. The reality of the situation is that my hobby of thinking and writing about the financial markets has no direct impact on my investment decisions for me or my clients.

There is no question that stocks go down during recessions, and an average investor will likely live through at least another half-dozen recessions in their lifetime. Unfortunately, speculators have learned firsthand about the dangers of trading based on economic and/or political headlines during volatile cycles. That doesn’t mean everyone should buy and do nothing. If done properly, it can be quite advantageous to periodically rebalance your portfolio through the use of various valuation and macro metrics as a means to objectively protect/enhance your portfolio’s performance. For example, cutting exposure to cyclical and debt-laden companies going into an economic downturn is probably wise. Reducing long-term Treasury positions during a period of near-record low interest rates (see Confessions of a Bond Hater) as the economy strengthens is also likely a shrewd move.

As we have seen over the last five years, the net result of investor portfolio shuffling has been a lot of pain. The acts of panic-selling caused damaging losses for numerous reasons, including a combination of agonizing transactions costs; increased inflation-decaying cash positions; burdensome taxes; and a mass migration into low-yielding bonds. After major indexes have virtually tripled from the 2009 lows, many investors are now left with the gut-wrenching decision of whether to get back into stocks as the markets reach new highs.

As the bulls continue to point to the scores of gifts still lying under the Christmas tree, the bears are left hoping that new Fed Grinch Yellen will come and steal all the presents, trees, and food from the planned 2014 economic feast. There are still six trading days left in the year, so Santa Bernanke cannot finish wrapping up his +30% S&P 500 total return gift quite yet. Nevertheless, ever since the initial taper announcement, stocks have moved higher and Bernanke has equity investors singing “Joy to the World!”

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

QE: The Greatest Thing Since Sliced Bread*

Quantitative easing (QE), or the Federal Reserve’s bond buying program, has been a spectacular success. Arguably, the greatest innovation since sliced bread. Don’t believe me? I mean, if you listen to many of the experts, strategists, economists, and blogosphere pundits, the magical elixir of QE can be the only explanation rationalizing the multi-year economic recovery and stock market boom. Don’t believe me? Well, apparently many of the bearish pros make sure to credit QE for all our financial/economic positives. For example…

- QE is the reason the stock market is near all-time record highs.

- QE created seven million jobs in the U.S. over the last four years.

- QE turned around the housing market.

- QE turned around the auto market.

- QE weakened the U.S. dollar, resulting in flourishing exports.

- QE has lowered borrowing rates, thereby cleansing consumer balance sheets through deleveraging.

- QE is the reason Facebook Inc. (FB) hired 1,323 employees over the last year.

- QE is the reason Google Inc. (GOOG) has spent $7.8 billion on R&D over the last year.

- QE explains why McDonald’s Corp. (MCD) plans to open more than 1,400 stores this year.

- QE explains why Warren Buffett and 3G capital paid $28 billion to buy Heinz.

- QE is the reason Elon Musk and Tesla Motors (TSLA) invented the model S electric vehicle.

- QE exhibits why Target Corp. (TGT) is expanding outside the U.S. into Canada.

- QE is the reason why S&P 500 companies are expected to pay $300 billion in dividends this year.

- QE is the reason why S&P 500 companies were buying back shares at a $400 billion clip this year.

- QE is the basis for corporations spending billions on efficiency enhancing cloud-based services.

- QE led to a record number of new FDA drug approvals last year.

- QE has caused a natural gas production boom in numerous shale regions.

Wow…the list goes on and on! Heck, I even hear QE can take the corrosion off of a rusted car battery. Given how incredible this QE stuff is, why even consider tapering QE? Financial markets have been volatile on the heels of tapering the 3rd iteration of quantitative easing (QE3), but why slow QE3, when the FED could add more awesomeness with QE4, QE10, QE 100, and QE 1,000?

All of this QE talk is so wonderful, but unfortunately, according to all the bearish pundits, QE has created an artificial sugar high, thus creating an asset bubble that is going to end in a disastrous cratering of financial markets.

I know it’s entirely possible that QE may have absolutely nothing to do with the financial market recovery (other than a bid under Treasury & mortgage backed security prices), and also has no bearing on why I buy or sell stocks, but I guess I will need to hide in a cave when QE3 tapering begins. Although the end of dividends, share buybacks, housing/auto recoveries, acquisitions, expansion, innovation, etc., caused by QE tapering sure does not sound like a cheery outcome, at least I still have a loaf of sliced bread to make a sandwich.

*DISCLOSURE: For those readers not familiar with my writing style, I have been known to use a healthy dose of sarcasm. Call me if you want a deeper explanation.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE II : Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and GOOG, but at the time of publishing, SCM had no direct position in FB, TSLA, MCD, BRKA, TGT, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page

Confessions of a Bond Hater

Source: stock.xchng

Hi my name is Wade, and I’m a bond hater. Generally, the first step in addressing any type of personal problem is admitting you actually have a problem. While I am not proud of being a bond hater, I have been called many worse things during my life. But as we have learned from the George Zimmerman / Trayvon Martin case, not every situation is clear-cut, whether we are talking about social issues or bond investing. For starters, let me be clear to everyone, including all my detractors, that I do not hate all bonds. In fact, my Sidoxia clients own many types of fixed income securities. What I do hate however are low yielding, long duration bonds.

Duration…huh? Most people understand what “low yielding” means, when it comes to bonds (i.e., low interest, low coupon, low return, etc.), but when the word duration is uttered, the conversation is usually accompanied by a blank stare. The word “duration” may sound like a fancy word, but in reality it is a fairly simple concept. Essentially, high-duration bonds are those fixed income securities with the highest sensitivity to changes in interest rates, meaning these bonds will go down most in price as interest rates rise.

When it comes to equity markets, many investors understand the concept of high beta stocks, which can be used to further explain duration. There are many complicated definitions for beta, but the basic principle explains why high-beta stock prices generally go up the most during bull markets, and go down the most during bear markets. In plain terms, high beta equals high octane.

If we switch the subject back to bonds, long duration equals high octane too. Or stated differently, long duration bond prices generally go down the most during bear markets and go up the most during bull markets. For years, grasping the risk of a bond bear market caused by rising rates has been difficult for many investors to comprehend, especially after witnessing a three-decade long Federal Funds tailwind taking the rates from about 20% to about 0% (see Fed Fatigue Setting In).

The recent interest rate spike that coincided with the Federal Reserve’s Ben Bernanke’s comments on QE3 bond purchase tapering has caught the attention of bond addicts. Nobody knows for certain whether this short-term bond price decline is the start of an extended bear market in bonds, but mathematics would dictate that there is only really one direction for interest rates to go…and that is up. It is true that rates could remain low for an indefinite period of time, but neither scenario of flat to down rates is a great outcome for bond holders.

Fixes to Fixed-Income Failings

Even though I may be a “bond hater” of low yield, high duration bonds, currently I still understand the critical importance and necessity of a fixed income portfolio for not only retirees, but also for the diversification benefits needed by a broader set of investors. So how does a bond hater reconcile investing in bonds? Easy. Rather than focusing on lower yielding, longer duration bonds, I invest more client assets in shorter duration and/or higher yielding bonds. If you harbor similar beliefs as I do, and believe there will be an upward bias to the trajectory of long-term interest rates, then there are two routes to go. Investors can either get compensated with a higher yield to counter the increased interest rate risk, and/or they can shorten duration of bond holdings to minimize capital losses.

Worth noting, there is an alternative strategy for low yielding, long duration bond lovers. In order to minimize interest rate risk, these bond lovers may accept sub-optimal yields and hold bonds to maturity. This strategy may be associated with short-term price volatility, but if the bond issuer does not default, at least the bond investor will get the full principal at maturity to help relieve the pain of meager yields.

Now that you’ve survived all this bond babbling, let me cut to the chase and explain a few ways Sidoxia is taking advantage of the recent interest rate volatility for our clients:

Floating Rate Bonds: Duration of these bonds is by definition low, or near zero, because as interest rates rise, coupons/interest payments are advantageously reset for investors at higher rates. So if interest rates jump from 2% to 3%, the investor will receive +50% higher periodic payments.

Inflation Protection Bonds: These bonds come in long and short duration flavors, but if interest rates/inflation rise higher than expected, investors will be compensated with higher periodic coupons and principal payments.

Shorter Duration: One definition of duration is the weighted average of time until a bond’s fixed cash flows are received. A way of shortening the duration of your bond portfolio is through the purchase of shorter maturity bonds (e.g., buying 3-year bonds rather than 30-year bonds).

High Yield Bonds: Investing in the high yield bond category is not limited to domestic junk bond purchases, but higher yields can also be earned by investing in international and/or emerging market bonds.

Investment Grade Corporate Bonds: Similar to high yield bonds, investment grade bonds offer the potential of capital appreciation via credit improvement. For instance, credit rating upgrades can provide gains to help offset price declines caused by rising interest rates.

Despite my bond hater status, the recent taper tantrum and interest rate spike, highlight some advantages bonds have over stocks. Even though prices declined, bonds by and large still have lower volatility than stocks; provide a steady stream of income; and provide diversification benefits.

To the extent investors have, or should have, a longer-term time horizon, I still am advocating a stock bias to client portfolios, subject to each investor’s risk tolerance. For example, an older retired couple with a conservative target allocation of 20%/80% (equity/fixed income) may consider a 25% – 30% allocation. A shift in this direction may still meet the retirees’ income needs (especially if dividend-paying stocks are incorporated), while simultaneously acknowledging the inflation and interest rate risks impacting bond positions. It’s important to realize one size doesn’t fit all.

Higher Volatility, Higher Reward

Frequent readers of Investing Caffeine have known about my bond hating tendencies for quite some time (see my 2009 article Treasury Bubble has not Burst…Yet), but the bond baby shouldn’t be thrown out with the bath water. For those investors who thought bonds were as safe as CDs, the recent -6% drop in the iShares Aggregate Bond Index (AGG) didn’t feel comfortable for most. Although I am still an enthusiastic stock cheerleader (less so as valuation multiples expand), there has been a cost for the gargantuan outperformance of stocks since March of ’09. While stocks have outperformed bonds (S&P vs. AGG) by more than +140%, equity investors have had to endure two -10% corrections and two -20% corrections (e.g.,Flash Crash, Debt Ceiling Debate, European Financial Crisis, and Sequestration/Elections). If investors want to earn higher long-term equity returns, this desire will translate into more volatility than bonds…and more Tums.

I may still be a bond hater, and the general public remains firm stock haters, but at some point in the multi-year future, I will not be surprised to hear myself say, “Hi my name is Wade, and I am addicted to bonds.” In the mean time, Sidoxia will continue to optimize its client bond portfolios for a rising interest rate environment, while also investing in attractive equity securities and ETFs. There’s nothing to hate about that.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), including floating rate bonds/loan funds, inflation-protection funds, corporate bond ETF, high-yield bond ETFs, and other bond ETFs, but at the time of publishing, SCM had no direct position in AGG or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Jobs and the DMV Economy

If you have ever gone to get your driver’s license at the Department of Motor Vehicles (DMV)…you may still be waiting in line? It’s a painful but often a mandatory process, and in many ways the experience feels a lot like the economic recovery we currently have been living through over the last four years. Steady progress is being made, but in general, people hardly notice the economy moving forward.

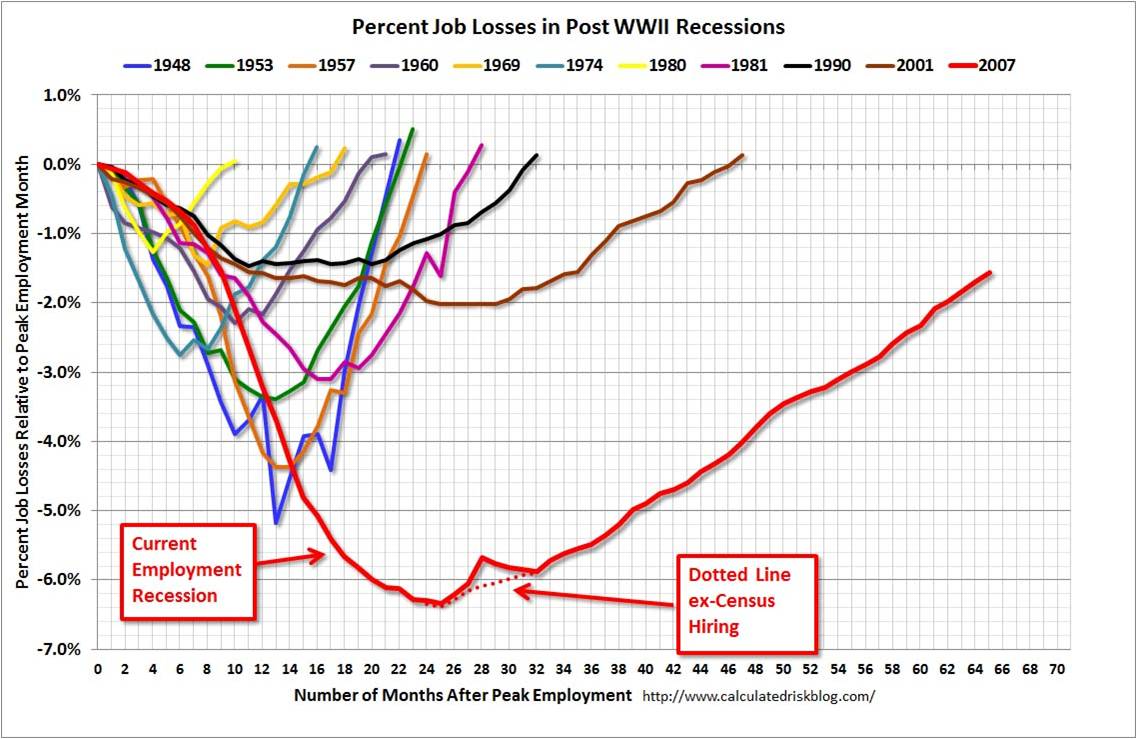

My geographic neighbor and blogger here in Orange County, California (Bill McBride – Calculated Risk) has some excellent visuals that compare our sluggish DMV economy with previous economic cycles dating back to 1948:

Source: Calculated Risk

As you can see from the chart above, the current economic recovery (red-line), as measured by job losses, is the slowest comeback in more than a half-century. Basically, over a two year period, the U.S. lost about nine million jobs, and during the following three years the economy regained approximately seven million of those jobs – still digging out of the hole. Last Friday’s June jobs report was welcomed, as it showed net jobs of +195,000 were added during the month, and importantly the previous two months were revised higher by another +70,000 jobs. These data points combined with last month’s Fed’s QE3 tapering comments by Ben Bernanke help explain why the continued rout in 10 year Treasury rates has continued in recent weeks, propelling the benchmark rate to 2.71% – almost double the 1.39% rate hit last year amidst continued European financial market concerns.

As with most recessions or crashes, the bursting of the bubble (i.e., damage) occurs much faster than the inflation (i.e., recovery), and McBride’s time series clearly shows this fact:

Source: Calculated Risk

While pessimists point to the anemic pace of the current recovery, the glass half-full people (myself included) appreciate that the sluggish rebound is likely to last longer than prior recoveries. There are two other key dynamics underlying the reported employment figures:

- Continued Contraction in Government Workers: Excessive government debt and deficits have led to continued job losses – state and local job losses appear to be stabilizing but federal cuts are ongoing.

- Decline in the Labor Force Participation Rate: Discouraged workers and aging Baby Boomer demographics have artificially lowered the short-term unemployment figures because fewer people are looking for work. If economic expansion accelerates, the participation contraction trend is likely to reverse.

Skepticism Reigns Supreme

Regardless of the jobs picture and multi-year expansion, investors and business managers alike remain skeptical about the sustainability of the economic recovery. Anecdotally I encounter this sentiment every day, but there are other data points that bolster my assertion. Despite the stock market more than doubling in value from the lows of 2009, CNBC viewer ratings are the weakest in about 20 years (see Value Walk) and investments in the stock market are the lowest in 15 years (see Gallup poll chart below):

Source: Gallup

Why such skepticism? Academic research in behavioral finance highlights innate flaws in human decision-making processes. For example, humans on average weigh losses twice as much as gains as economist and Nobel prizewinner Daniel Kahneman explains in his book Thinking Fast and Slow (see Investing Caffeine article: Decision Making on Freeways and in Parking Lots). Stated differently, the losses from 2008-2009 are still too fresh in the minds of Americans. Until the losses are forgotten, and/or the regret of missing gains becomes too strong, many investors and managers will fearfully remain on the sideline.

The speed of our economic recovery is as excruciatingly agonizing, and so is waiting in line at the DMV. The act of waiting can be horrific, but obtaining a driver’s license is required for driving and investing is necessary for retirement. If you don’t want to go to investing jail, then you better get in the investing line now before job growth accelerates, because you don’t want to be sent to the back of the line where you will have to wait longer.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Hammering Heads with Circular Conversations

This article is an excerpt from a previously released Sidoxia Capital Management complementary newsletter (July 1, 2013). Subscribe on the right side of the page for a complete monthly update.

Deciphering what is driving the markets on a day-to-day, week-to-week, or month-to-month basis can feel like repeatedly hammering your head. In order to grasp the reasons why financial markets go up and down, one must have a conversation with your brain explaining that good news can be bad for asset prices, and bad news can be good for asset prices. Huh…how can that be? These circular conversations are what keep newspapers, magazines, media commentators, and bloggers in business… and what baffle many investors.

For example, headlines often reflect sentiments such as these:

- “Unemployment Figures Disappoint…Dow Jones Rallies +200 Points on QE3 Continuation Hopes”

- “Unemployment Figures Delight…Dow Jones Tanks -200 Points on QE3 Discontinuation Fears”

- “Economic Figures Revised Lower by -0.2%…Dow Jones Skyrockets +200 Points as Lower Interest Rates Propel Stock Prices.”

- “Economic Figures Revised Higher by +0.2%…Dow Jones Plummets -200 Points as Higher Interest Rates Deflate Stock Prices.”

On rare occasions these headlines make sense, but often online media outlets are frantically changing the headlines as the markets whip back and forth from positive to negative. News-producing editors are continually forced to create ludicrous and absurd explanations that usually make no sense to informed long-term investors.

It’s important to recognize that if the financial markets made common sense, then investing for retirement would be simple and everyone would be billionaires. Unfortunately, financial markets frequently make no sense in the short-run. Stocks are volatile (often times for no rational reason), which is why stocks offer higher returns over the long-run relative to more stable asset classes.

Explaining the latest spike in stock/bond price volatility has been exacerbated in recent weeks as a result of the nation’s banker (the Federal Reserve) and its boss, Ben Bernanke, attempting to explain their future monetary policy plans. In theory, bringing light to a traditionally mysterious, closed-door Washington process should be a good thing…right?

Well, ever since a few weeks ago when Ben Bernanke and the FOMC (Federal Open Market Committee) disclosed that the stimulative bond buying program (QE3) could be slowed in 2013 and halted in 2014, financial markets globally experienced a sharp jolt of volatility – stock prices dropped and interest rates spiked. Counter-intuitively, Bernanke’s belief that the economy is on a sustained recovery path (expected GDP growth of +3.25% in both 2014 & 2015) spooked investors. More specifically, in the month of June, the S&P 500 index declined -1.5% in June; Dow Jones Industrial Index -1.4%; and the 10-year Treasury note’s yield jumped +0.3% to 2.5%. Greedy investors, however, should not forget that the stock market just posted its 2nd best quarter since 2009 – the S&P 500 climbed +2.4%. What’s more, the S&P 500 is up +13% and the Dow up +14% in the first half of 2013.

Bernanke Threatening to Take Away Investor Lollipops

Another way of looking at the recent volatility is by equating investors to kids and stimulative QE bond buying programs (Quantitative Easing) to lollipops. If the economy continues on this improvement trajectory (i.e., unemployment falls to 7% by next year) and inflation remains benign (below 2.5%), then Bernanke said he will take away investors’ QE lollipops. But like a pushover dad being pressured by kids at the candy store, Bernanke acknowledged that he could continue supplying investors QE lollipops, if the economic data doesn’t improve at the forecasted pace. At face value, receiving a specific timeline given by the Fed should be appreciated and normally people are happy to hear the Chairman speak rosily about the economy’s future. However, the mere thought of QE lollipops being taken away next year was enough to push investors into a “taper tantrum” (see also Investing Caffeine – Fed Fatigue article).

With scary headlines constantly circulating, a large proportion of investors are sitting on their hands (and cash) while staring like deer in headlights at these developments. Rather than a distracted driver texting, investors should be watching the road and mapping out their future investment destinations – not paying attention to irrelevant diversions. Astute investors realize that uncertainty surrounding Greece, Cyprus, fiscal cliff, sequestration, presidential elections, Iran, N. Korea, Syria, Turkey, taxes, QE3, etc., etc., etc., have been a constant. Regrettably the fear mongers paying attention to these useless headlines have witnessed their cash, gold, and Treasuries get trounced by equity returns since early 2009 (the S&P 500 index is up about +150%, including dividends). Optimists and realists, on the other hand, have seen their investment plans thrive. While the aforementioned list of concerns has dangled in front of our noses over the last year, we will have a complete new list of concerns to decipher over the coming weeks, months, and years. That’s the price a long-term investor pays if they want to earn higher returns in the volatile equity markets.

As strategist Don Hays points out, “Nothing is certain. Good investors love uncertainty.” Rather than getting consumed by fear with the endless number of changing uncertainties, the real risk for investors is outliving your savings. Paychecks are being stretched by inflationary pressures across all categories (e.g., healthcare, gasoline, utilities, food, movies, travel, etc.) and entitlements like Social Security and Medicare will likely not mean the same thing to us as it did for our parents. Unless investors plan on working into their 80s as greeters at Wal-Mart, and/or enjoy clipping Top Ramen coupons in a crammed apartment, then they should do themselves a favor by taking a deep breath and turning off the television, so they can be insulated from the constant doom and gloom.

So as intimidating, circular conversations about good news being bad news, and bad news being good news continue to swirl around, focus instead on building a diversified investment plan that can adjust and adapt to the never-ending list of uncertainties. Your head will feel a lot better than it would after repetitive hammer strikes.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and WMT, but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Fed Fatigue Setting In

Uncle…uncle! There you have it – I have finally cried “uncle” because I cannot take it anymore. I don’t think I can listen to another panel or read another story debating about the timing of Fed “tapering”, or heaven forbid the Fed actually “tighten” the Federal Funds rate (i.e., increasing the targeted rate for inter-bank lending). Type in the words “Bernanke” and “tapering” into Google and you will get back more than 41,000,000 results. The build up to the 600-word FOMC (Federal Open Market Committee) statement was almost deafening, so much so that live coverage of Federal Reserve Chairman Ben Bernanke was available at your fingertips:

Source: Yahoo! Finance

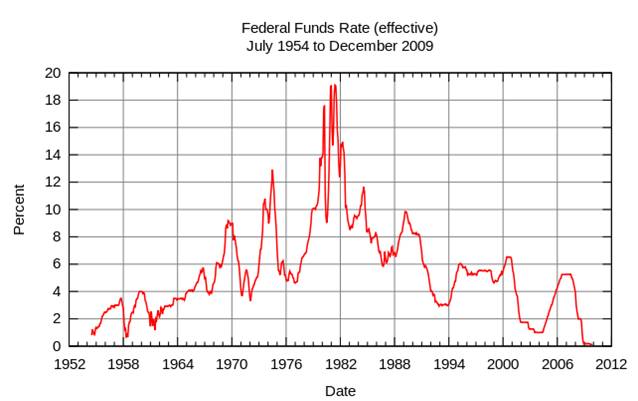

Like a toddler (or a California-based, investment blog writer) going to the doctor’s office to receive an inoculation, the anxiety and mental anguish caused in anticipation of the event is often more painful than the actual injection. As I highlighted in a previous Investing Caffeine article, the 1994 interest rate cycle wasn’t Armageddon for equity markets, and the same can be said for the rate hikes from 1.0% to 5.25% in the 2004-20006 period (see chart below). Even if QE3 ends in mid-2014 and the new Federal Reserve Chairman (thank you President Obama) raises rates in 2015, this scenario would not be the first (or last) time the Federal Reserve has tightened monetary policy.

Source: Wikipedia

Short Memories – What Have You Done for Me Lately?

People are quick to point out the one-day -350 Dow point loss earlier this week, but many of them forget about the +3,000 point moon shot in the Dow Jones Industrial index that occurred in six short months (November 2012 – May 2013). The same foggy recollection principle applies to interest rates. The recent rout in 10-year Treasury prices is easily recalled as rates have jumped from 1.5% to 2.5% over the last year, however amnesia often sets in for others if you ask them where rates were a few years ago. It’s easy to forget that 30-year fixed rate mortgages exceeded 5% and the 10-year reached 4% just three short years ago.

Bernanke: The Center of the Universe?

Does Ben Bernanke deserve credit for implementing extraordinary measures during extraordinary times during the 2008-09 financial crisis? Absolutely. But should every man, women, and child wait with bated breath to see if a word change or tonal adjustment is made in the eight annual FOMC meetings?

Like the public judging Ben Bernanke, my Sidoxia clients probably give me too much credit when things go well and too much blame when things don’t. I love how Bernanke gets blamed/credited for the generational low interest rates caused by his money printing ways and QE punch bowl tactics. Last I checked, the interest rate downtrend has been firmly in place over the last three decades, well before Bernanke came into the Fed and worked his monetary magic. How much credit/blame are we forgetting to give former Federal Reserve Chairmen Paul Volcker, Alan Greenspan, and other government policy-makers? Regardless of what happens economically for the remainder of 2013, Bernanke will do whatever he can to solidify his legacy in the waning sunset months of his term.

Another forgotten fact I like to point out: There is more than one central banker living on this planet. If you haven’t been asleep over the last few decades, our financial markets have increasingly become globally interconnected with the assistance of technology. I know our 10-year Treasury rates are hovering around 2.50%, and our egotistical patriotism leads us to hail Bernanke as a monetary god, but don’t any other central bankers or government officials around the world deserve any recognition for achieving yields even lower than ours? Here’s a partial list (June 22, 2013 – Financial Times):

- Japan – 0.86%

- Germany – 1.67%

- Canada – 2.33%

- U.K. – 2.31%

- France – 2.27%

- Sweden – 2.15%

- Austria – 2.09%

- Switzerland – 0.92%

- Netherlands – 2.07%

Although it may be fun to look at Ben Bernanke as our country’s financial Superman who is there to save the day, there are a lot more important factors to consider than the 47 words added and 19 subtracted from the latest FOMC statement. If investing was as easy as following central bank monetary policy, everyone would be continually jet setting to their private islands. Rather than wasting your time listening to speculative blathering about direction of Fed monetary policy, why not focus on finding solid investment ideas and putting a long-term investment plan in place. Now please excuse me – Fed fatigue has set in and I need to take a nap.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and GOOG, but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

U.S. Small-Caps Become Global Big Dog

With the emerging market currencies and financial markets under attack; Japan’s Nikkei index collapsing in the last three weeks; and the Federal Reserve hinting about its disciplinarian tapering of $85 billion in monthly QE3 bond purchases, one would expect higher beta small cap stocks to get hammered in this type of environment.

Before benchmarking results in the U.S., let’s take a closer look at some of the international carnage occurring from this year’s index value highs:

- Japan: -19% (Nikkei 225 index)

- Brazil: -22% (IBOVESPA index)

- Hong Kong: -12% (Hang Seng index)

- Russia: -19% (MICEX/RTS indexes)

Not a pretty picture. Given this international turmoil and the approximately -60% disintegration in U.S. small-cap stock prices during the 2007-2009 financial crisis, surely these economically sensitive stocks must be getting pummeled in this environment? Well…not necessarily.

Putting the previously mentioned scary aspects aside, let’s not forget the higher taxes, Sequestration, and ObamaCare, which some are screaming will push us off a ledge into recession. Despite these headwinds, U.S. small-caps have become the top dog in global equity markets. Since the March 2009 lows, the S&P 600 SmallCap index has more than tripled in value ( about +204%, excluding dividends), handily beating the S&P 500 index, which has advanced a respectable +144% over a similar timeframe. Even during the recent micro three-week pullback/digestion phase, small cap stocks have retreated -2.8% from all-time record highs (S&P 600 index). Presumably higher dividend, stable, globally-diversified, large-cap stocks would hold up better than their miniature small-cap brethren, but that simply has not been the case. The S&P 500 index has underperformed the S&P 600 by about -80 basis points during this limited period.

How can this be the case when currencies and markets around the world are under assault? Attempting to explain short-term moves in any market environment is a hazardous endeavor, but that has never slowed me down in trying. I believe these are some of the contributing factors:

1) No Recession. There is no imminent recession coming to the U.S. As the saying goes, we hear about 10 separate recessions before actually experiencing an actual recession. The employment picture continues to slowly improve, and the housing market is providing a slight tailwind to offset some the previously mentioned negatives. If you want to fill that half-full glass higher, you could even read the small-cap price action as a leading indicator for a pending acceleration in a U.S. cyclical recovery.

2) Less International. The United States is a better house in a shaky global neighborhood (see previous Investing Caffeine article), and although small cap companies are expanding abroad, their exposure to international markets is less than their large-cap relatives. Global investors are looking for a haven, and U.S. small cap companies are providing that service now.

3) Inflation Fears. Anxiety over inflation never seems to die, and with the recent +60 basis point rise in 10-year Treasury yields, these fears appear to have only intensified. Small-cap stocks cycle in and out of favor just like any other investment category, so if you dig into your memory banks, or pull out a history book, you will realize that small-cap stocks significantly outperformed large-caps during the inflationary period of the 1970s – while the major indexes effectively went nowhere over that decade. Small-cap outperformance may simply be a function of investors getting in front of this potential inflationary trend.

Following the major indexes like the Dow Jones Industrials index and reading the lead news headlines are entertaining activities. However, if you want to become a big dog in the investing world and not get dog-piled upon, then digging into the underlying trends and market leadership dynamics of the market indexes is an important exercise.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) including emerging market ETFs, IJR, and EWZ, but at the time of publishing, SCM had no direct position in Hong Kong ETFs, Japanese ETFs, Russian ETFs, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Uncertainty: Love It or Hate It?

Source: Photobucket

Uncertainty is like a fin you see cutting through the water – many people are uncertain whether the fin sticking out of the water is a great white shark or a dolphin? Uncertainty generates fear, and fear often produces paralysis. This financially unproductive phenomenon has also reared its ugly fin in the investment world, which has led to low-yield apathy, and desensitization to both interest rate and inflation risks.

The mass exodus out of stocks into bonds worked well for the very few that timed an early 2008 exit out of equities, but since early 2009, the performance of stocks has handily trounced bonds (the S&P has outperformed the bond market (BND) by almost 100% since the beginning of March 2009, if you exclude dividends and interest). While the cozy comfort of bonds has suited investors over the last five years, a rude awakening awaits the bond-heavy masses when the uncertain economic clouds surrounding us eventually lift.

The Certainty of Uncertainty

What do we know about uncertainty? Well for starters, we know that uncertainty cannot be avoided. Or as former Secretary of the Treasury Robert Rubin stated so aptly, “Nothing is certain – except uncertainty.”

Why in the world would one of the world’s richest and most successful investors like Warren Buffett embrace uncertainty by imploring investors to “buy fear, and sell greed?” How can Buffett’s statement be valid when the mantra we continually hear spewed over the airwaves is that “investors hate uncertainty and love clarity?” The short answer is that clarity is costly (i.e., investors are forced to pay a cherry price for certainty). Dean Witter, the founder of his namesake brokerage firm in 1924, addressed the issue of certainty in these shrewd comments he made some 78 years ago, right before the end of worst bear market in history:

“Some people say they want to wait for a clearer view of the future. But when the future is again clear, the present bargains will have vanished.”

Undoubtedly, some investors hate uncertainty, but I think there needs to be a distinction between good investors and bad investors. Don Hays, the strategist at Hays Advisory, straightforwardly notes, “Good investors love uncertainty.”

When everything is clear to everyone, including the novice investing cab driver and hairdresser, like in the late 1990s technology bubble, the actual risk is in fact far greater than the perceived risk. Or as Morgan Housel from Motley Fool sarcastically points out, “Someone remind me when economic uncertainty didn’t exist. 2000? 2007?”

What’s There to Worry About?

I’ve heard financial bears argue a lot of things, but I haven’t heard any make the case there is little uncertainty currently. I’ll let you be the judge by listing these following issues I read and listen to on a daily basis:

- Fiscal cliff induced recession risks

- Syria’s potential use of chemical weapons

- Iran’s destabilizing nuclear program

- North Korean missile tests by questionable new regime

- Potential Greek debt default and exit from the eurozone

- QE3 (Quantitative Easing) and looming inflation and asset bubble(s)

- Higher taxes

- Lower entitlements

- Fear of the collapse in the U.S. dollar’s value

- Rigged Wall Street game

- Excessive Dodd-Frank financial regulation

- Obamacare

- High Frequency Trading / Flash Crash

- Unsustainably growing healthcare costs

- Exploding college tuition rates

- Global warming and superstorms

- Etc.

- Etc.

- Etc.

I could go on for another page or two, but I think you get the gist. While I freely admit there is much less uncertainty than we experienced in the 2008-2009 timeframe, investors’ still remain very cautious. The trillions of dollars hemorrhaging out of stocks into bonds helps make my case fairly clear.

As investors plan for a future entitlement-light world, nobody can confidently count on Social Security and Medicare to help fund our umbrella-drink-filled vacations and senior tour golf outings. Today, the risk of parking your life savings in low-rate wealth destroying investment vehicles should be a major concern for all long-term investors. As I continually remind Investing Caffeine readers, bonds have a place in all portfolios, especially for income dependent retirees. However, any truly diversified portfolio will have exposure to equities, as long as the allocation in the investment plan meshes with the individual’s risk tolerance and liquidity needs.

Given all the uncertain floating fins lurking in the economic background, what would I tell investors to do with their hard-earned money? I simply defer to my pal (figuratively speaking), Warren Buffett, who recently said in a Charlie Rose interview, “Overwhelmingly, for people that can invest over time, equities are the best place to put their money.” For the vast majority of investors who should have an investment time horizon of more than 10 years, that is a question I can answer with certainty.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) including BND, but at the time of publishing SCM had no direct positions in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Autumn, Elections and Replacement Refs

Article is an excerpt from previously released Sidoxia Capital Management’s complementary October 1, 2012 newsletter. Subscribe on right side of page.

As September has come to a close, the grand finale of our annual seasons has commenced… autumn. How do we know autumn is here? Well, for starters, the leaves are changing colors; the weather is about to cool; and the NFL replacement referees are watching Sunday football games from their couches.

While 2012 is split into quarters, football games and investment seasons are also divided into four quarters. Right now, the economic fourth quarter has just started and the home team is winning. As we can see from the stock market scoreboard, the S&P 500 index is up +15% this year (+6% in Q3) and the NASDAQ index has catapulted +20% through September (+6% also in Q3). The U.S. home team is winning, but a fumble, blocked kick, or interception could mean the difference between an exciting win and a devastating loss.

Another game divided into four parts is the game of presidential politics. However, presidential elections are divided into four years – not four quarters. Five weeks from now, we’ll find out if our Commander in Chief Obama will get to lead our team for another game lasting four years, or whether backup quarterback Mit Romney will be called into the game. The fans are getting restless due to anemic growth and lingering joblessness, but for now, the coach is keeping the president in the starting lineup. Both President Obama and Governor Romney will take some head-to-head practice snaps against each other in the first of three scheduled presidential debates beginning this week.

Bernanke Changes Rules

The New York Jets have Tim Tebow for their secret weapon (1 for 1 yesterday!), and the United States economy has Ben Bernanke. Although our home team may be winning, it has required some monetary rule-changing policies to be instituted by Federal Reserve Chairman Ben Bernanke to keep our team in the lead. Just a few weeks ago, Mr. Bernake instituted QE3 (3rd round of quantitative easing), which is an open-ended mortgage buying program designed to lower home buying interest rates and stimulate the economy (see Helicopter Ben to QE3 Rescue). The short-term benefits of the $40 billion monthly bond buying binge are relatively clear (lower borrowing costs for homebuyers), but the longer-term costs of inflation are stewing patiently on the backburner.

Source: Calafia Beach Pundit (Scott Grannis)

As you can see from the chart above, August median home prices are up +10% for existing single-family homes over the last year. Housing affordability is at extremely attractive levels, and although the bank loan purse strings are tight, a modest loosening is beginning to unfold.

Economy Playing Injured

Our starters may still be playing, but many are injured, just like the jobless are limping through the employment market. Encouragingly, although unemployment remains stubbornly high, the number of people collecting unemployment checks is a lot lower (-1.25 million fewer than a year ago). Not great news, but at least we are hobbling in the right direction (see chart below).

Source: Calafia Beach Pundit (Scott Grannis)

Time for Fiscal Cliff Hail Mary?

If a team is losing at the end of a game, a “Hail Mary” pass might be necessary. We are quickly nearing this fiscal Armageddon situation as the approximately $700 billion “fiscal cliff” (a painful combo of spending cuts and tax hikes) kicks in at the end of the year (see PIMCO chart below via The Reformed Broker).

Running trillion dollar deficits in perpetuity is not a sustainable strategy, so for most people, a combination of spending cuts and/or tax hikes makes sense to narrow the gap (see chart below). Last year’s recommendations from the bipartisan Simpson-Bowles commission, which were ignored, are not a bad place to start. What happens in the lame-duck session of Congress (after the elections) will dramatically impact the score of the current economic game, and decide who wins and who loses.

Source: Calafia Beach Pundit (Scott Grannis)

Heated debates continue on how the gap between expenses and revenues will be narrowed, but regardless, Democrats will continue to push for capital gains tax hikes on the rich (see tax chart below); and the Republicans will push to cut spending on entitlements, including untenable programs like Medicare and Social Security.

Source: The Wall Street Journal

The game is not quite over, but the fourth quarter promises to be a bloody battle. So while the replacement refs may be back at home, the experienced returning refs have been known to blow calls too. Let’s just hope that autumn, the season of bounteous fecundity, ends up being a continued trend of sweet market success, rather than a political period of botched opportunities.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct positions in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Helicopter Ben to QE3 Rescue

Faster than a speedy credit default swap, more powerful than a federal funds interest rate cut, and able to leap a tall Mario Draghi in a single bound, look…it’s Helicopter Ben! How did Federal Reserve Chairman Ben Bernanke become a monetary superhero with such a cool nickname as Helicopter Ben (a.k.a. “HB”)? Bernanke, a former Princeton University professor, has widely been known to be a diligent student of the Great Depression, and his aviation nickname stems from a 2002 speech in which he referenced dropping money from a helicopter to combat deflation. While investors may worry about HB’s ability to fight the inflation thugs, there should be no questions about his willingness to implement accommodative, deflation-fighting monetary policies.

Chairman Bernanke may not epitomize your ideal superhero, however this slightly past middle-aged bearded and balding man has helped mastermind some of the most creative and aggressive monetary rescue efforts our country and globe has seen in the history of man (and woman). This week’s money-printing QE3 announcement solidified Bernanke’s historic capital saturating ranking.

Since Helicopter Ben’s heroic appointment as Federal Reserve Chairman in 2006 by George W. Bush, Bernanke has instituted numerous monetary gadgets in hopes of meeting the Federal Reserve’s dual mandate, which is i) to achieve low inflation and ii) to strive for maximum employment. Arguably, given the anemic growth here in the U.S.; the recession in Europe; and slowing growth in the emerging markets (i.e., China, Brazil, India, etc.), slack in the economy and static labor wages have largely kept inflation in check. With the first part of the dual mandate met, Bernanke has had no problem putting his monetary superpowers to work.

As referenced earlier, Bernanke’s bazooka launch of QE3, an open ended MBS (Mortgage Back Securities) bond binging program, will add $40 billion of newly purchased assets to the Fed’s balance sheet on a monthly basis until the labor market improves “substantially” (whatever that means). What’s more, in addition to the indefinite QE3, Bernanke has promised to keep the federal funds rate near zero “at least through mid-2015,” even for a “considerable time after the economic recovery strengthens.”

HB’s Track Record

Throughout superhero history, Superman, Spider-man, and Batman have used a wide-array of superhuman powers, extraordinary gadgets, and superior intellect to conquer evil-doers and injustices across the globe. Bernanke has also forcefully put his unrivaled money-printing talents to work in an attempt to cure the financial ills of the world. Here’s a quick multi-year overview of how Bernanke has put his unique talents to print trillions of dollars and keep interest rates suppressed:

Rate Cuts (September 2007 – December 2008): Before “quantitative easing” was a part of our common vernacular, the Fed relied on more traditional monetary policies, such as federal funds rate targeting, conducted through purchases and sales of open market securities. Few investors recall, but before HB’s fed funds rate cut rampage of 10 consecutive reductions in 2007 and 2008 (the fed funds rate went from 5.25% to effectively 0%), Bernanke actually increased rates three times in 2006.

Crisis Actions (2007 – 2009): Love him or hate him, Bernanke has been a brave and busy soul in dealing with the massive proportions of the global financial crisis. If you don’t believe me, just check out the Financial Crisis Timeline listed at the St. Louis Federal Reserve. Many investors don’t remember, but Bernanke helped orchestrate some of the largest and most unprecedented corporate actions in our history, including the $30 billion loan to JPMorgan Chase (JPM) in the Bear Stearns takeover; the $182 billion bailout of AIG; the conversion of Morgan Stanley (MS) and Goldman Sachs Group Inc. (GS) into bank holding companies; and the loan/asset-purchase support to Fannie Mae (FNMA) and Freddie Mac (FMCC). These actions represented just the tip of the iceberg, if you also consider the deluge of liquidity actions taken by the Fed Chairman.

HB Creates Acronym Soup

In order to provide a flavor of the vastness in emergency programs launched since the crisis, here is an alphabet soup of program acronyms into which the Fed poured hundreds of billions of dollars:

- Term Asset-Backed Securities Loan Facility (TALF)

- Term Auction Facility (TAF)

- Money Market Investor Funding Facility (MMIFF)

- Commercial Paper Funding Facility (CPFF)

- Primary Dealer Credit Facility (PDCF)

- Asset-Backed Commercial Paper Money Market Fund Liquidity Facility (AMLF)

- Temporary Reciprocal Currency Arrangements (Swap lines)

- Term Securities Lending Facility (TSLF)

Plenty of acronyms to go around, but these juicy programs have garnered most of investors’ attention:

QE1 (November 2008 – March 2010): In hopes of lowering interest rates for borrowers and stimulating the economy, HB spearheaded the Fed’s multi-step, $1 trillion+ buying program of MBS (mortgage backed securities) and Treasuries.

QE2 (November 2010 – June 2011): Since the Fed felt QE1 didn’t pack enough monetary punch to keep the economy growing at a fast enough clip, the FOMC (Federal Open Market committee) announced its decision to expand its holdings of securities in November 2010. The Committee maintained its existing policy of reinvesting principal payments from its securities holdings and to also purchase a further $600 billion of longer-term Treasury securities by the end of the second quarter of 2011 (an equivalent pace of about $75 billion per month).

Operation Twist (September 2011 – December 2012): What started out as a $400 billion short-term debt for longer-term debt swap program in September 2011, expanded to a $667 billion program in June 2012. With short-term rates excessively low, Bernanke came up with this Operation Twist scheme previously used in the early 1960s. Designed to flatten the yield curve (bring down long-term interest rates) to stimulate economic activity, Bernanke thought this program was worth another go-around. Unlike quantitative easing, Operation Twist does not expand the Fed’s balance sheet – the program merely swaps short-term securities for long-term securities. Currently, the program is forecasted to conclude at the end of this year.

The Verdict on HB

So what’s my verdict on the continuous number of unprecedented actions that Helicopter Ben and the Fed have taken? Well for starters, I have to give Mr. Bernanke an “A-” on his overall handling of the financial crisis. Had his extreme actions not been taken, the pain and agony experienced by all would likely be significantly worse, and the financial hole a lot deeper.

With that said, am I happy about the announcement of QE3 and the explosion in the Fed’s money printing activities? The short answer is “NO”. It’s difficult to support a program with questionable short-run interest rate benefits, when the menacing inflationary pressures are likely to outweigh the advantages. The larger problem in my mind is the massive fiscal problem we are experiencing (over $16 trillion in debt and endless trillion dollar deficits). More importantly, this bloated fiscal position is creating an overarching, nagging crisis of confidence. A resolution to the so-called “fiscal cliff,” or the automated $600 billion in tax increases and spending cuts, is likely to have a more positive impact on confidence than a 0.05% – 0.25% reduction in mortgage rates from QE3. Once adequate and sustained growth returns, and inflation rears its ugly head, how quickly Helicopter Ben tightens policy will be his key test.

Until then, Bernanke will probably continue flying around while gloating in his QE3 cape, hoping his quantitative easing program will raise general confidence. Unfortunately, his more recent monetary policies appear to be creating diminishing returns. Even before QE3’s implementation, Helicopter Ben has witnessed his policies expand the Fed’s balance sheet from less than $900 billion at the beginning of the recession to almost $3 trillion today. Despite these gargantuan efforts, growth and confidence have been crawling forward at only a modest pace.

No matter the outcome of QE3, as long as Ben Bernanke remains Federal Reserve Chairman, and growth remains sluggish, you can stay confident this financial man of steel will continue dumping money into the system from his helicopter. If Bernanke wants to create a true legendary superhero ending to this story, the kryptonite-like effects of inflation need to be avoided. This means, less money-printing and more convincing of Congress to take action on our out-of-control debt and deficits. Now, that’s a comic book I’d pay to read.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct positions in JPM, AIG, MS, GS, FNMA, FMCC, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}