Posts tagged ‘predictions’

Predictions – A Fool’s Errand

Making bold predictions is a fool’s errand. I think Yogi Berra summed it up best when he spoke about the challenges of making predictions:

“It’s tough to make predictions, especially about the future.”

While making predictions might seem like a pleasurable endeavor, the reality is nobody has been able to consistently predict the future (remember the 2012 Mayan Doomsday?), besides perhaps palm readers and Nostradamus. The typical observed pattern consists of a group of well-known forecasters bunched in a herd coupled with a few extreme outliers who try to make a big splash and draw attention to themselves. Due to the law of large numbers, a few of these extreme outlier forecasters eventually strike gold and become Wall Street darlings…until their next forecasts fail miserably.

Like a broken clock, these radical forecasters can be right twice per day but are wrong most of the time. Here are a few examples:

Peter Schiff: The former stockbroker and President of Euro Pacific Capital has been peddling doom for decades (see Emperor Schiff Has No Clothes). You can get a sense of his impartial perspective via Schiff’s reading list (The Real Crash: America’s Coming Bankruptcy, Financial Armageddon, Conquer the Crash, Crash Proof – America’s Great Depression, The Biggest Con: How the Government is Fleecing You, Manias Panics and Crashes, Meltdown, Greenspan’s Bubbles, The Dollar Crisis, America’s Bubble Economy, and other doom-instilled titles.

Meredith Whitney: She made an incredible bearish call on Citigroup Inc. (C) during the fall of 2007, alongside her accurate call of Citi’s dividend suspension. Unfortunately, her subsequent bearish calls on the municipal market and the stock market were completely wrong (see also Meredith Whitney’s Cloudy Crystal Ball).

John Mauldin: This former print shop professional turned perma-bear investment strategist has built a living incorrectly calling for a stock market crash. Like perma-bears before him, he will eventually be right when the next recession hits, but unfortunately, the massive appreciation will have been missed. Any eventual temporary setback will likely pale in comparison to the lost gains from being out of the market. I profiled the false forecaster in my article, The Man Who Cries Bear.

Nouriel Roubini: This renowned New York University economist and professor is better known as “Dr. Doom” and as one of the people who predicted the housing bubble and 2008-2009 financial crisis. Like most of the perma-bears who preceded him, Dr. Doom remained too doom-ful as the stock market more than tripled from the 2009 lows (see also Pinning Down Roubini).

Alan Greenspan: The graveyard of erroneous forecasters is so large that a proper summary would require multiple books. However, a few more of my favorites include Federal Reserve Chairman Alan Greenspan’s infamous “Irrational Exuberance” speech in 1996 when he warned of a technology bubble. Although directionally correct, the NASDAQ index proceeded to more than triple in value (from about 1,300 to over 5,000) over the next three years. – today the NASDAQ is hovering around 6,100.

Robert Merton & Myron Scholes: As I chronicled in Investing Caffeine (see When Genius Failed), another doozy is the story of the Long Term Capital Management hedge fund, which was run in tandem with Nobel Prize winning economists, Robert Merton and Myron Scholes. What started as $1.3 billion fund in early 1994 managed to peak at around $140 billion before eventually crumbling to a capital level of less than $1 billion. Regrettably, becoming a Nobel Prize winner doesn’t make you a great predictor.

Words From the Wise

Rather than paying attention to crazy predictions by academics, economists, and strategists who in many cases have never invested a penny of outside investor money, ordinary investors would be better served by listening to steely investment veterans or proven prediction practitioners like Billy Beane (minority owner of the Oakland Athletics and subject of Michael Lewis’s book, Moneyball), who stated the following:

“The crime is not being unable to predict something. The crime is thinking that you are able to predict something.”

Other great quotes regarding the art of predictions, include these ones:

“I can’t recall ever once having seen the name of a market timer on Forbes‘ annual list of the richest people in the world. If it were truly possible to predict corrections, you’d think somebody would have made billions by doing it.”

-Peter Lynch

“Many more investors claim the ability to foresee the market’s direction than actually possess the ability. (I myself have not met a single one.) Those of us who know that we cannot accurately forecast security prices are well advised to consider value investing, a safe and successful strategy in all investment environments.”

–Seth Klarman

“No matter how much research you do, you can neither predict nor control the future.”

–John Templeton

“Stop trying to predict the direction of the stock market, the economy or the elections.”

–Warren Buffett

“In the business world, the rearview mirror is always clearer than the windshield.”

–Warren Buffett

In the global financial markets, Wall Street is littered with strategists and economists who have flamed out after brief bouts of fame. Celebrated author Mark Twain captured the essence of speculation when he properly identified, “There are two times in a man’s life when he should not speculate: when he can’t afford it and when he can.” Instead of attempting to predict the future, investors will avoid a fool’s errand by simply seizing opportunities as they present themselves in an ever-changing world.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Where are the Economists’ Yachts?

“Where Are the Customers’ Yachts?” was a book first published about 75 years ago in 1940 by Fred Schwed, Jr. Before he became an author, Schwed was a professional trader who eventually left Wall Street after losing a significant amount of money during the 1929 stock market crash. The title of Schwed’s book refers to a story about a visitor to New York who admired the yachts of the bankers and brokers. Naively, the visitor asked where all the customers’ yachts were? Of course, none of the customers could afford yachts, even though they obediently followed the advice of their bankers and brokers.

The same principle applies to economists. The broad investing public, including many professionals, blindly hang on to every economist’s word. And why not? Often these renowned economists are quite articulate – they use big words, crafty jargon, and wear fancy clothes. Unfortunately in many (most) cases the predictions are way off base. What’s more, if these economists/strategists/analysts/etc. were so clairvoyant, then how come we do not find any of them on the Forbes 400 list or see them captaining massive yachts?

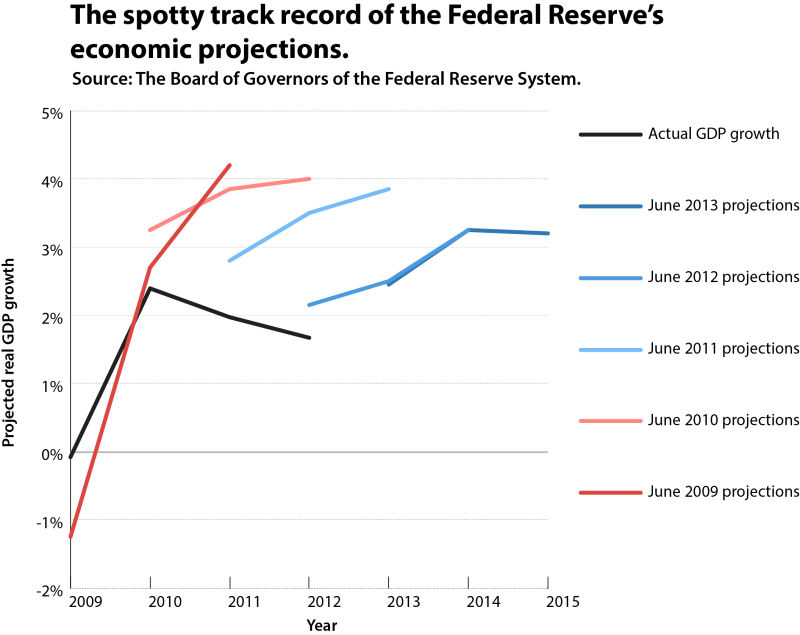

Recently, the Washington Post highlighted the spotty forecasting track record of the Federal Reserve, as it related to past projections of economic growth. As you can see from the chart below, the Board of Governors were consistently too optimistic about future economic growth prospects.

Source: Washington Post

The Federal Reserve has repeatedly proved it is no slouch when it comes to poor forecasting. The example I often point to is the infamous 1996 “irrational exuberance” speech (see also NASDAQ 5,000 Déjà Vu?) given by then Federal Reserve Chairman Alan Greenspan. In the talk, Greenspan warned of escalated asset values and cautioned about a potential decade-long malaise similar to the one experienced by Japan. At the time, the NASDAQ index stood at 1,300, but despite Greenspan screaming about an overvalued market, three years later, the tech-laden index almost quadrupled in value to 5,132.

There are plenty more errant economist forecasts to reference, but despite the economists’ poor batting averages, there is virtually no accountability of the pathetic predictions by the media outlets. Month after month, and year after year, I see the same buffoons on cable TV making the same faulty predictions with zero culpability.

While I have attempted to keep some of the economists/strategists honest (see The Fed Ate My Homework), credit must be given where credit is due. Barry Ritholtz, the lead Editor of The Big Picture, last year wrote a smart piece on the accountability (or lack therof) in the prediction industry.

In the article Ritholtz described some of the shenanigans going on in the loosely regulated prediction industry. Here’s part of what he had to say:

Pundits are highly incentivized to adhere to the following playbook:

- make a brash prediction

- if wrong, don’t worry…. no one will remember

- if right, selectively tout for self-promotion

- repeat cycle

Ritholtz also describes another time-tested strategy I love…The 40% Rule:

“The 40% rule is the perfect way to make a splashy headline and cover your butt at the same time. Forecast that there’s a 40% chance that the Dow Jones Industrial Average clears 12,000 by year end: If it does, you’ll look like a sage, and if it doesn’t, well, you didn’t say it’s the most likely outcome.”

Whatever your views are of predictions made by high profile economists and pundits, the media archives are littered with faulty forecasts. It is difficult to dispute that the projection game is a very tough business, and if you don’t share the same opinion, please explain to me…where are the all the economists’ yachts?

Click Here for Other Bad Predictions

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own a range of positions in certain exchange traded fund positions, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Strategist Predictions and MacGyver Credo

MacGyver: Resourceful dude with sweet mullet (Source: Photobucket).

“Only a fool is sure of anything, a wise man keeps on guessing.” – MacGyver

We have gotten to the part of the year when strategists gather for the annual dart throwing ritual of 2011 price targets. S&P projections get chucked around with the hopes of sticking – like cooked spaghetti to the wall. MacGyver appreciates the fine art of guessing, and so do Wall Street strategists.

How the Game’s Played

You don’t have to be a brain surgeon to figure out how the Wall Street astrology game works. When in doubt, just say the market will be up +10% next year. Hmmm, why +10%?

1) Well, first of all, these strategists work for employers who are in the business of hawking financial products and services to the masses, so if you want to generate revenues, you better attempt to line up some believers with some rosy scenarios.

2) History is on the strategists’ side. Equity markets move up about 70% of the time, so why not make an optimistic bet. Data from Crestmont Research and Roger Ibbotson support the average return over the last 100 years or so has averaged approximately +10% (with a lot of peaks and valleys). Obviously, that hasn’t been the case over the last decade. The PIMCO bond brothers of Bill Gross and Mohamed El-Erian blame the “New Normal” environment despite recently raising their 2011 GDP forecasts to a “Less Sluggish New Normal.” More likely, the decade of the 2000s is more like the “Old Normal” of boom-busts like we experienced in the 1930s and 1970s.

3) The other cardinal rule to be followed religiously: Forecasts made by any Wall Street type need to be made in tight packs like a herd. There is comfort in numbers, and why in the world would someone risk embarrassment or career risk. Fat paychecks abound for these strategists and hugging consensus views is OK, as long as a logical story can be patched together in explaining it.

With all this discussion about +10% average stock market returns, guess what type of returns this year’s Barron’s strategist survey is forecasting? You guessed it…+10% – what a shocker! Let’s hope this guess is more accurate than Barron’s +10% strategist return forecast for 2008 (S&P 500 was actually down -38.5% in 2008). Strategists don’t always get it wrong – the sanguine +12% outlook for 2010 is basically spot on with a few days left in the year. The sanguine 2002 outlook of +13%, however, was about -35% too sanguine (S&P plummeted about -23% that year).

Although most strategists feign absolute knowledge and precision, history shows these projections rarely prove accurate. Like predicting weather, guessers may get the long-term climate forecast fairly close, but the short-term estimates are generally pure speculation. In my book, 12 months is very short-term. Famed investor and author Charles Ellis captures the challenge of market forecasts:

“Predicting the stock market roughly is not hard, but predicting it accurately is truly impossible.”

I ascribe to the Peter Lynch view that speculating about the direction of the market is futile:

“If you spend more than 13 minutes analyzing economic and market forecasts, you’ve wasted 10 minutes.”

Kass Gets Hall Pass

Even though I may relish in flogging strategists, I provide certain professionals a hall pass under the following conditions:

- The educated guesser is putting real, hard-earned money behind their assertions.

- The guesses do not hug a tightly-knit herd.

- Guesses are made transparent and guessers make themselves accountable for bold statements.

- Those making guesses freely admit to the fallibility of making non-consensus suppositions.

One man whom embodies these principles is famed hedge fund manager Doug Kass, whom I have written about on several occasions (read more). Not only are Kass’s 2011 predictions provocative, they are also entertaining. His self proclaimed 40% batting average in 2010 may be a little higher than reality, but I will let you be the judge of his 2010 calls on the dollar, gold, Fed actions, Iran, Goldman Sachs, utilities, Warren Buffett, mutual funds, short-selling, New York Yankees, and more (read full 2010 Kass list).

The herd of strategists may continue having trouble making accurate market forecasts in the future, but perhaps resourcefully adding some duct tape and a Swiss Army knife to their repertoire like MacGyver will help improve accuracy. If not, rest assured, the strategists will sleep well making their +10% forecasts while continuing to collect big fat paychecks.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Professional Double-Dip Guesses are “Probably” Wrong

As you may have noticed from previous articles, I take a significant grain (or pound) of salt when listening to economists and strategists like Peter Schiff, Nouriel Roubini, Meredith Whitney, John Mauldin, et.al. Typically, these financial astrologists weave together convincing, elaborate, grand guesses that extrapolate every short-term, fleeting economic data point into an imposing (or magnificent) long-term secular trend.

With all this talk of “double-dip” recession, I cannot help but notice the latest verbal tool implemented by every Tom, Dick, and Harry economist when discussing this topic… the word “probability”. Rather than honestly saying I have no clue on what the economy will do, many strategists place a squishy numerical “probability” around the possibility of a “double-dip” recession consistent with the news du jour. Over recent weeks, unstable U.S. economic data have been coming in softer than expectations. So, guess what? Economists have become more pessimistic about the economy and raised the “probability” of a double dip recession. Thanks Mr. Professor “Obvious!” I’m going to go out on a limb, and say the probability of a double-dip recession will likely go down if economic data improves. Geez…thanks.

Here is a partial list of double-dip “probabilities” spouted out by some well-known and relatively unknown economists:

- Robert Shiller (Professor at Yale University): “The probability of that kind of double-dip is more than 50 percent.”

- Bill Gross (Founder/Managing Director at PIMCO): The New York Times described Gross’s double-dip radar with the following, “He put the probability of a recession — and of an accompanying bout of deflation — at 25 to 35 percent.”

- Mohamed El-Erian (CEO of PIMCO): “If you wonder how meaningful 25 per cent is, ask yourself the following question: if I offered you that I drive you back to work, but there’s a one in four chance that I get into a big accident, would you come with me?”

- David Rosenberg (Chief Economist at Gluskin Chef): In a recent newsletter, Rosenberg has raised the odds of a double-dip recession from 45 per cent a month ago to 67 per cent currently.

- Nouriel Roubini (Professor at New York University): “As early as August 2009 I expressed concern in a Financial Times op-ed about the risk of a double-dip recession, even if my benchmark scenario characterizes the risk of a W as still a low probability event (20% probability) as opposed to a 60% probability for a U-shaped recovery.”

- Robert Reich (Former Secretary of Labor): According to Martin Fridson, Global Credit Strategist at BNP Paribas, Robert Reich has assigned a 50% probability of a double dip, even if Reich believes we are actually in one “Long Dipper.”

- Graeme Leach (Chief Economist at the Institute of Directors): “I would give a 40 per cent probability to what I call ‘one L of a recovery’, in other words a fairly weak flattish cycle over the next 12 months. A double-dip recession would get a 40 per cent probability as well.”

- Ed McKelvey (Sr. U.S. Economist at Goldman Sachs): “We think the probability is unusually high — between 25 percent and 30 percent — but we do not see double dip as the base case.”

- Avery Shenfeld (Chief Economist at CIBC): “The probability estimate is likely more consistent with a slowdown rather than a true double-dip recession but, given the uncertainties, fiscal tightening ahead and the potential for a slow economy to be vulnerable to shocks, we will keep an eye on our new indicator nevertheless.” This guy can’t even be pinned down for a number!

- National Institute for Economic and Social Research (NIESR) : “The probability of seeing a contraction of output in 2011 as compared to 2010 has risen from 14 per cent to 19 per cent.”

- New York Fed Treasury Spread Model (see chart below): Professor Mark J. Perry notes, “For July 2010, the recession probability is only 0.06% and by a year from now in June of next year the recession probability is only slightly higher, at only 0.3137% (less than 1/3 of 1%).”

Listening to these economic armchair quarterbacks predict the direction of the financial markets is as painful as watching Jim Gray’s agonizing hour-long interview of Lebron James’s NBA contract decision (see also Lebron: Buy, Sell, or Hold?). Just what I want to hear – a journalist that probably has never dribbled a ball in his life, inquiring about cutting edge questions like whether Lebron is still biting his nails? Most of these economists are no better than Jim Gray. In many instances these professionals don’t invest in accordance with their recommendations and their probability estimates are about as reliable as an estimate of the volatility index (see chart below) or a prediction about Lindsay Lohan’s legal system status.

I can virtually guarantee you at least one of the previously mentioned economists will be correct on their forecasts. That isn’t much of an achievement, if you consider all the strategists’ guesses effectively cover every and any economic scenario possible. If enough guesses are thrown out there, one is bound to stick. And if they’re wrong, no problem, the economists can simply blame randomness of the lower probability event as the cause of the miscue.

Unlike Wayne Gretzky, who said, “I skate to where the puck is going to be, not where it has been,” economists skate right next to the puck. Because the economic data is constantly changing, this strategy allows every forecaster to constantly change their outlook in lock-step with the current conditions. This phenomenon is like me looking at the dark clouds outside my morning window and predicting a higher probability of rain, or conversely, like me looking at the blue skies outside and predicting a higher chance of sunshine.

Using this “probability” framework is a convenient B.S. means of saving face if a directional guess is wrong. By continually adjusting probability scenarios with the always transforming economic data, the strategist can persistently waffle with the market sentiment vicissitudes.

What would be very refreshing to see is a strategist on CNBC who declares he was dead wrong on his prediction, but acknowledges the world is inherently uncertain and confesses that nobody can predict the market with certainty. Instead, the rent-o-strategists consistently change their predictions in such a manner that it is difficult to measure their accuracy – especially when there is rarely hard numbers to hold these professional guessers accountable for.

Economists and strategists may be well-intentioned people, just as is the schizophrenic trading advice of Jim Cramer of CNBC’s Mad Money, but the “probability” of them being right over relevant investing time horizons is best left to an experienced long-term investor that understands the pitfalls of professional guessing.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in GS, NYT or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Forecasting Recipe: Trend Analysis & Sustainability

Forecasting financial performance of a company requires a fairly simple recipe: one part trend analysis and one part determining sustainability. On the surface, forecasting sounds pretty easy. While discovering certain financial trends can be straightforward, the ability to ascertain the durability of a trend can become endlessly complex.

Before you become Nostradamus and spreadsheet your way to the Wall Street Hall of Fame, an accurate forecaster must first build a firm understanding of a company and the underlying industry. Unfortunately for the predictor, not all companies and industries are created equally. Evaluating the profit dynamics of Cheesecake Factory Inc. (CAKE), an upscale casual chain of restaurants, is quite different from deciphering the financials of 3SBio (SSRX), a Chinese biotech company focused on recombinant products. Regardless of the thorniness of the company or industry, before you can truly look out into the future, the investor should learn the language of the company. For example, learning the importance of “comparable store sales” and “sales per square foot” for CAKE may be just as important as learning about the “Phase III FDA trial endpoint” and “pipeline” for SSRX.

Because you could spend a lifetime following just one company – for instance General Electric Co. (GE) or Microsoft Corp. (MSFT) – and never make an investment, you would probably be better served by applying a framework that allows you to research and analyze multiple industries and companies. There are various tools, whether you consider Harvard professor Michael Porter’s Five Forces or SWOT analysis (Strengths Weaknesses Opportunities Threats), and each provides a template or process to use when tearing apart specific companies and industries.

Nuts & Bolts of Forecasting

Before you can identify a trend, you first need to gather the data. For all companies I examine, I first compile a quarterly and annual income statement, balance sheet, and cash flow statement – those that have followed me know the extreme importance I place on the cash flows of a business. In general a good start is to create common size financial statements for the income statement and balance sheet. Basically, this exercise creates an income statement and balance sheet in percentage terms – usually expressed as a percentage of net sales (income statement) and as a percentage of total assets (balance sheet). Earnings forecasts are often used as a logical starting point for driving the shape of future results across the financials, but further insight can be gleaned by comparing year-over-year (this year vs. last) and sequential (this quarter vs. last quarter) growth rates for key figures.

These common statements will then serve as the foundation of identifying the trends, and force the forecaster to seek answers to random questions like these?

- Why is depreciation expense going down even though the company is expanding retail stores?

- Gross margins increased for seven consecutive quarters for a total of 250 basis points (2.5%), however in the recent quarter margins declined by 175 basis points…why?

- Long-term debt increased by $200 million in the current quarter, but if the company just issued $325 million in equity last quarter, then why do they need new capital?

Many of these types of questions may have logical explanations, but by getting answers the analyst will be in a position to better understand the business issues affecting financial performance and to better forecast future economic values.

Forecasting Your Way to Wrongness

A lot can go wrong with forecasting, principally in the assumptions used for the forecast. As the character Felix Unger from the Odd Couple stated, “You should never “assume.” You see, when you “assume,” you make an “ass”… out of “you”… and “me.”” Often assumptions do not consider the inclusion of important economic shocks or unexpected factors, such as recessions, currency fluctuations, management turnover, lawsuits, accounting changes, new products, restructurings, acquisitions, divestitures, flash crashes, Greek debt downgrades, regulatory reform…yada…yada…yada (you get the idea). To get a better sense for a range of outcomes, sensitivity analysis can be employed to determine a “base case” outcome in conjunction with a rosier “upside case” and more conservative “downside case.” Worth noting is the impact debt levels can have on the variance of outcomes – I think Bear Stearns and Lehman Brothers would concur with this point.

Pinpointing variable financial figures is quite difficult. Different companies and industries inherently have more or less predictable attributes. Predicting when the sun will rise and set is quite a bit more predictable than predicting what Intel Corp’s (INTC) gross margins will be on a quarterly basis. As mentioned earlier, layering on debt can increase the volatility of earnings forecasts as well.

Forecasting is essential in the investment world, but even if you were the best forecaster in the world, investors cannot disregard the importance of valuation skills. The art of valuation is just as important, if not more important than being right on your financial scenarios.

All in all, the recipe of forecasting sounds simple if you look at the basic ingredients of trend and sustainability analysis. However, before the ultimate forecast comes out of the oven, this straightforward recipe requires a lot of preparation, whether it is slicing and dicing cash flow figures, whipping up some margin trends, or measuring up sales growth. Any way you cut it, systematically following a recipe of trend and sustainability analysis is a non-negotiable requirement if you want to heat up superior financial results.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct positions in GE, MSFT, CAKE, SSRX, INTC, JPM/Bear Stearns, Lehman Brothers, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

John Mauldin: The Man Who Cries Wolf

We have all heard about the famous Aesop fable about The Boy Who Cried Wolf. In that story, a little boy amuses himself by tricking others into falsely believing a wolf is attacking his flock of sheep. After running to the boy’s rescue multiple times, the villagers became desensitized to the boy’s cries for help. The boy’s pleas ultimately get completely ignored by the villagers despite an eventual real wolf attack that kills the boy’s flock of sheep.

Mauldin: The Man Who Cries Bear

John Mauldin, former print shop professional and current perma-bear investment strategist, unfortunately seems to have taken a page from Aesop’s book by consistently crying for a market collapse. After spending many years wrongly forecasting a bear market, his dependable pessimism eventually paid dividends in 2008. Unfortunately for him, rather than reverse his downbeat outlook, he stepped on the pessimism pedal just as the equity markets have exploded upwards more than +80% from the March lows of last year. Mauldin is widely followed in part to his thoughtful pieces and intriguing contributing writers, but as some behavioral finance students have recognized, being bearish or cautious on the markets always sounds smarter than being bullish. I’m not so sure how smart Mauldin will sound if he’s wrong on the direction of the next 80% move?

The Challenged Predictor

I find it interesting that a man who freely admits to his challenged prediction capabilities continues to make bold assertive forecasts. Mauldin freely confesses in his writings about his inability to manage money and make correct market forecasts, but that hasn’t slowed down the pessimism express. Just two years ago as the financial crisis was unfolding, Mauldin admits to his poor fortune telling skills with regards to his annual forecast report each January:

“ I was wrong (as usual) about the stock markets.”

Here’s Mauldin explaining why he decided to switch from investing real money to the simulated version of investment strategy and economic analysis:

“I wanted to begin to manage money on my own… I found out as much about myself as I did about market timing. What I found out was that I did not have the emotional personality (the stomach?) to directly time the markets with someone else’s money… I simply worried too much over each move of the tape.”

Apparently timing the market is not so simple? Readers of Investing Caffeine understand my feelings about market timing (read Market Timing Treadmill piece) – it’s a waste of time. Market followers are much better off listening to investors who have successfully navigated a wide variety of market cycles (see Investing Caffeine Profiles), rather than strategists who are constantly changing positions like a flag in the wind. I wonder why you never hear Warren Buffett ever make a market prediction or throw out a price target on the Dow Jones or S&P 500 indexes? Maybe buying good businesses or investments at good prices, and owning them for longer than a nanosecond is a strategy that can actually work? Sure seems to work for him over the last few years.

When You’re Wrong

Typically a strategist utilizes two approaches when they are wrong:

1) Convert to Current Consensus: Most strategists change their opinion to match the current consensus thinking. Or as Mauldin described last year, “I expect that this year will bring a few surprises that will cause me to change my opinions yet again. When the facts change, I will try and change with them.” The only problem is…the facts change every day (see also Nouriel Roubini).

2) Push Prediction Out: The other technique is to ignore the forecasting mistake and merely push out the timing (see also Peter Schiff). A simple example would be of Mr. Mauldin extending his recession prediction made last April, “We are going to pay for that with a likely dip back into a recession in 2010,” to his current view made a few weeks ago, “I put the odds of a double-dip recession in 2011 at better than 50-50.”

More Mauldin Mistake Magic

Well maybe I’m just being overly critical, or distorting the facts? Let’s take a look at some excerpts from Mauldin’s writings:

A. January 10, 2009 (S&P @ 890):

Prediction: “I now think we will be in recession through at least 2009 before we begin a recovery….We could see a tradable rally in the next few months, but at the very least test the lows this summer, if not set new lows….It takes a lot of buying to make a bull market. It only takes an absence of buying to make a bear market.”

Outcome: S&P 500 today at 1,179, up +32%. Oops, maybe the timing of his recovery forecast was a little off?

B. February 14, 2009 (S&P @ 827):

Prediction/Advice: “Let me reiterate my continued warning: this is not a market you want to buy and hold from today’s level. This is just far too precarious an economic and earnings environment.”

Outcome: S&P 500 up +45%. You pay a cherry price for certainty and consensus.

C. April 10, 2009 (S&P @ 856):

Prediction: “All in all, the next few years are going to be a very difficult environment for corporate earnings. To think we are headed back to the halcyon years of 2004-06 is not very realistic. And if you expect a major bull market to develop in this climate, you are not paying attention.” On the economy he adds, “We are going to pay for that with a likely dip back into a recession in 2010.”

Outcome: S&P 500 up +38%, with the economy currently in recovery. Interestingly, his comments on corporate earnings in February 2009 referenced an estimate of $55 in S&P 2010. Now that we are 14 months closer to the end of 2010, not only is the consensus estimate much firmer, but the 2010 S&P estimate presently stands at approximately $75 today, about +36% higher than Mauldin was anticipating last year.

D. May 2, 2009 (S&P @ 878):

Prediction: “This rally has all the earmarks of a major short squeeze. ..When the short squeeze is over, the buying will stop and the market will drop. Remember, it takes buying and lot of it to move a market up but only a lack of buying to create a bear market.”

Outcome: S&P 500 up +36%.

Now that we have entered a new year and experienced an +80% move in the market, certainly Mauldin must feel a little more comfortable about the current environment? Apparently not.

E. April 2, 2010 (S&P @ 1178):

Prediction: “ I think it is very possible we’ll see another lost decade for stocks in the US. If we do have a recession next year, the world markets are likely to fall in sympathy with ours.”

Outcome: ????

Previous Mauldin Gems

Here are few more gloomy gems from Mauldin’s bearish toolbox of yester-year:

2005: “The market is a sideways to down market, with the risk to the downside as we get toward the end of the year and a possible recession on the horizon in 2006. And not to put too fine a point on it, I still think we are in a long term secular bear market.” Reality: S&P 500 up +5% for the year and up a few more years after that.

2006: “This year I think the market actually ends the year down, and by at least 10% or more during the year. Reality: S&P 500 up +14% (excluding dividends).

2007: Mauldin’s rhetoric was tamed in light of poor predictions, so rhetoric switches to a “Goldilocks recession” and a mere -10-20% range correction. He goes on to dismiss a deep bear market, “In future letters we will look at why a deep (the 40% plus that is typical in recession) stock market bear is not as likely.” Reality: S&P 500 up +5%. Looks like the writing on the wall for 2008 turned out a bit worse than he expected.

2008: Sticking to soft landing outlook Mauldin states, “I think this will be a mild recession … I don’t think we are looking at anything close to the bear market of 2000-2001.” Uggh. Ultimately, the bear market turned out to be the worst market since 1973-1974 – his prediction was just off by a few decades. Reality: S&P 500 down -37%.

Lessons Learned from Market Strategists

I certainly don’t mean to demonize John Mauldin because his writings are indeed very thoughtful, interesting and include provocative financial topics. But put in the wrong hands, his opinions (and dozens of other strategists’ views) can be extremely dangerous for the average investor trying to follow the ever-changing judgments of so-called expert strategists. To Mauldin’s credit, his writings are archived publicly for everyone to sift through – unfortunately the media and many average investors have short memories and do not take the time to hold strategists accountable for their false predictions. Although, Iike Warren Buffett, I do not make market timing predictions or forecast short-term market trends, I see no problem in strategists making bold or inaccurate forecasts, as long as they are held responsible. Every investor makes mistakes, unfortunately, strategist predictions are usually not readily available for analysis, unlike tangible investment manager performance numbers. When forecasting lightning strikes and extreme bets win, every newspaper, radio show, and media outlet has no problem of placing these soothsayers on a pedestal. Thanks to the law of large numbers and the constantly shifting markets, there will always be a few outliers making correct calls on bold predictions. Who knows, maybe Mauldin will be the next CNBC guru du jour in the future for predicting another lost decade of equity market performance (see Lost Decade article)?

Regardless of your views on the market, the next time you hear a financial strategist make a bold forecast, like John Mauldin crying wolf, I urge you to not go running with the motivation to alter your investment portfolio. I suppose the time to become frightened and drive the REAL wolf (bear market) away will occur when consistently pessimistic strategists like Mauldin turn more optimistic. Until then, tread lightly when it comes to acting on financial market forecasts and stick to listening to long-term, successful investors that have invested their own money through all types of market cycles.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct positions in any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Top 10 Predictions for 2010

#10. Federal Reserve Chairman Ben Bernanke decides pundits were wrong on the housing bubble, so he sets Fed Funds target rate at negative -3.0%. Small businesses start receiving loans.

#9. As part of healthcare reform, Medicare is extended to teens for collagen lip augmentation.

#8. Goldman Sachs, Morgan Stanley, and Citigroup form tri-merger to guarantee they are too big to fail.

#7. Tiger Woods poses in Playgirl to pay for pricey revised terms in his prenup. (see previous post)

#6. Gold spikes to $3,000 per ounce as government subsidizes dental chains in “cash for crowns” gold melting campaign. Consumers get extra cash, but Jujube candy sales plummet. (see previous post)

#5. Bernie Madoff escapes from prison. A cigarette Ponzi Scheme created by Madoff generates enough money to bribe guards.

#4. Apple introduces iPot – a combination iPhone and toilet.

#3. Kazakhstan pays Brazil, Russia, India and China a 5% GDP royalty to be added to the emerging B-R-I-C-K countries. A win-win for all parties, including spelling teachers around the world.

#2. Timothy Geithner retires from Treasury after making millions for being cast as Eddie Haskell in new remake of Leave It to Beaver movie. (see previous post)

#1. Oprah decides to halt her retirement plans. Instead, she signs me to a multi-million dollar deal to co-host a stock & gossip show with her.

HAPPY 2010!!

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including BKF) and AAPL, but did not have any direct positions in any stock mentioned in this article at time of publication (including GS, MS, C, and GLD). No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Rogers: Fed Following in Path of Dodo

Jimmy Rogers, the bow-tie boss of Rogers Holdings and past co-founder of the successful Quantum Fund with George Soros, is no stranger to making outrageous predictions. His latest prophetic assessment is the Federal Reserve Bank is on the path of the Dodo bird to extinction:

“Don’t worry – the Fed is going to abolish itself. Between Bernanke and Greenspan, they’ve made so many mistakes that within the next few years the Fed will disappear.”

Given the shock and awe that transpired from the Lehman Brothers collapse, I can only wonder how investors might react to this scenario….hmmm. If this doozy of an outlandish call catches you off guard, please don’t be surprised – Rogers is not shy about sharing additional ones (Read other IC article on Rogers). For example, just six months ago Rogers said the Dow Jones could collapse to 5,000 (currently around 10,472) or skyrocket to 30,000, but “of course it would be in worthless money.” Oddly, the printing presses that Rogers keeps talking about have actually produced deflation (-0.2%) in the most recently reported numbers, not the same 79,600,000,000% inflation from Zimbabwe (Cato Institute), he expects.

I suppose Rogers will either point to a data conspiracy, or use the “just you wait” rebuttal. I eagerly await, with bated breath, the ultimate outcome.

Is U.S. Fed Alone?

If the U.S. Federal Reserve system is indeed about to disappear after over nine decades of operations, does that mean Rogers advocates shutting all of the other 166 global reserve banks listed by the Bank for International Settlement? Should the 3 ½ century old Swedish Riksbank (origin in 1668) and the Bank of England (1694) central banks also be terminated? Or does the U.S. Federal Reserve Bank have a monopoly on incompetence and/or corruption?

Sidoxia’s Report Card on Fed

I must admit, I believe we would likely be in a much better situation than we are today if the Federal Reserve board let Adam Smith’s “invisible hand” self adjust short-term interest rates. Rather, we drank from the spiked punch bowls filled with low interest rates for extended periods of time. The Federal Reserve gets too much attention/credit for the impact of its decisions. There is a much larger pool of global investors that are buying/selling Treasury securities daily, across a wide range of maturities along the yield curve. I think these market participants have a much larger impact on prices paid for new capital, relative to the central bank’s decision of cutting or raising the Federal funds rate a ¼ point.

Although I believe the Fed gets too much attention for its monetary policies, I think Bernanke and the Fed get too little credit for the global Armageddon they helped avoid. I agree with Warren Buffett that Bernanke acted “very promptly, very decisively, very big” in helping us avert a second depression while we were on the “brink of going into the abyss.”

Beyond the monetary policy of fractional rate setting, the Fed also has essential other functions:

- Supervise and regulate banking institutions.

- Maintain stability of the financial system and control systemic risk of financial markets.

- Act as a liaison with depository institutions, the U.S. government, and foreign institutions.

- Play a major role in operating the country’s payments system.

I will go out on a limb and say these functions play an important role, and the Fed has a good chance of being around for the 2012 London Olympic Games (despite Jimmy Rogers’ prediction).

Sidoxia’s Report Card on Rogers

As I have pointed out in the past, I do not necessarily disagree (directionally) with the main points of his arguments:

- Is inflation a risk? Yes.

- Will printing excessive money lower the value of our dollar? Yes.

- Is auditing the Federal Reserve Bank a bad idea? No.

My beef with Rogers is merely in the magnitude, bravado, and overconfidence with which he makes these outrageous forecasts. Furthermore, the U.S. actions do not happen in a vacuum. Although everything is not cheery at home, many other international rivals are in worse shape than we are.

From a media ratings and entertainment standpoint, Rogers does not disappoint. His amusing and outlandish predictions will keep the public coming back for more. Since according to Rogers, Bernanke will have no job at the Fed in a few years, I look forward to their joint appearance on CNBC. Perhaps they could discuss collaboration on a new book – Extinction: Lessons Learned from the Fed and Dodo Bird.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (VFH) at the time of publishing, but had no direct ownership in BRKA/B. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Meredith Whitney’s Cloudy Crystal Ball

Meredith Whitney, prominent banking analyst at her self-named advisory group, should have worn a bib to protect her from the adoring drool supplied by Maria Bartiromo in a recent CNBC interview. Ms. Whitney has quickly become a banking rock star during this “Great Recession” period. She was right at a critical juncture, and as a result she was thrust into the limelight. Much like Abby Joseph Cohen, the perma-bull Goldman Sachs strategist who gained notoriety in the late 1990s, Whitney (the perma-banking bear) will continue having difficulty living up to the lofty expectations demanded of her.

Despite the accolades, Whitney’s crystal ball has gotten cloudy in 2009. I suppose accuracy is not very important, judging by her bottom-half 2007 ranking (year of her major Citigroup call) in recommendation performance and 48%-ile ranking in the first half of 2008. Analysts, much like reporters, can avoid looking dumb by reporting the news du jour and by following the herd. Whitney has followed this formula with her continuous bearishness on the financial sector, excluding a brief but late upgrade of Goldman Sachs in July. Not only was her analysis tardy (Goldman’s stock tripled from the 2009 bottom), but her call has also underperformed the S&P 500 index since the upgrade.

Incoherent Inconsistencies

Like a bobbing and weaving wrestler (her husband John Layfield is a retired staged professional wrestler from the WWE), Whitney tries to concoct a completely mind-boggling narrative to explain her forecasts this year in the CNBC interview with Maria Bartiromo:

11/18/09 (XLF Price $14.60): “For the year, I have been at least ‘cover your shorts, go long.’ I haven’t been this bearish in a year.” (See Maria Bartiromo Interview)

Hmm, really? Are you kidding me? Wait a second…is this the same “go long” Meredith Whitney that expressed the following?

3/17/09: (XLF: 8.55 then, 14.60 now +71% ex-dividends): “These big banks are sitting on loans that were underwritten with bad math, and the stocks are going to go down…these stocks are uninvestable.”

(Fast forward to minute 8:20 for quote above)

2/4/09 (XLF: 8.97 then, 14.60 now +63% ex-dividends): “Investors should not even consider owning banks on an equity basis” (Click here and fast forward to minute 8:10 for quote).

The schizophrenic accounting of her postures are all the more confusing given her stance that the sector was “fairly valued” in October, according to the CNBC Bartiromo interview.

Don’t get me wrong, she made an incredible bearish call on Citigroup in the fall of 2007 and was expecting blood in the streets until a massive rebound in 2009 surprised her. Investors need to be wary of prognosticators that get thrust into the limelight (see Peter Schiff article) for a single prediction. The law of large numbers virtually guarantees a new breed of extreme forecasters will be rotated into the spotlight any time there is a major shift in the market direction. I choose to follow the footsteps of Warren Buffett and stay away from the game of market timing and market forecasts. I believe James Grant from the Interest Rate Observer states it best:

“The very best investors don’t even try to forecast the future. Rather, they seize such opportunities as the present affords them.”

Meredith Whitney may be a bright banking analyst and perhaps she’ll ultimately be proven right regarding the downward banking stock price trajectories, but like all bold forecasters she must live by the crystal ball, and die by the crystal ball.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and its clients own certain exchange traded funds (including VFH), but currently have no direct positions in C, GS, or XLF. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}