Posts tagged ‘Politics’

Betting Before the Race Starts

The spectators, myself included, are accumulating economic and political information as fast as it’s coming in and placing bets on different horses. Since Election Day, wagers on stocks have pushed the Dow Jones Industrial Average higher by more than 1,400 points (+7.8%) to almost 20,000. The current favorites have names like the banking sector, infrastructure, small caps, commodities, and other cyclical industries like the transports. The only problem…is the race has not even started.

Rather than place all your wagers before the race, when it comes to the stock market, you can still place your bets after the race begins (i.e., the presidency begins). So far, many bets have been made based on rhetoric emanating from the presidential election. Nobody has ever accused President-elect Trump of being short on words, and ever since the campaign process started a few years ago, his gift of the gab has led to many provocative claims and campaign promises. But as we have already learned, actions speak much louder than promises.

The walls of Trump’s pledges are already beginning to collapse, whether you interpret the shifts in his positions as softened stances or pure reversals. Examples of his position adjustments include recent comments regarding the maintenance of Obamacare’s preexisting conditions and universal care access components; immigration policies for illegal immigrants and his protective wall; or promises to lock up Hillary Clinton over her email scandal. The main point is that words are only words, and campaign promises often do not come to fruition.

The President-elect’s definitely has a full plate before his January 20th Inauguration Day, especially if you consider he is responsible for naming his White House and the heads of 100 federal agencies before his swearing in. But this only scratches the surface. When all is said and done, Trump will be making roughly 4,100 appointments, with 1,000 of those needing Senate confirmation.

While we sit here only one month after Trump won the presidential election, he has not sat on his hands. Trump has already made a significant number of his Cabinet announcements (click here for a current tally), with the much anticipated Secretary of State announcement expected to officially come next week.

From an investment standpoint, it makes perfect sense to make some adjustments to your portfolio based on the president-elect’s economic platform and political appointments. However, any shifts to your portfolio should be measured. For example, Hillary’s tweet heard around the world regarding skyrocketing pharmaceutical prices had a significant negative impact on the pharmaceutical/biotech sectors for many months. Expectations were for a more lenient and pharma-supportive administration to take place under Trump until excerpts from his Time magazine interview leaked out, “I’m going to bring down drug prices. I don’t like what has happened with drug prices.” Subsequent to his comments, the sector swiftly came crashing down.

As I have also pointed out previously, although Trump and the Republican Party have control of Congress (House & Senate), the make-up of the Republican majority is limited and quite diverse. I need not remind you that many of Trump’s Republican colleagues either campaigned against him or remained silent through the election process. What’s more, many fiscally conservative Tea Party members are not fully on board with a massive infrastructure bill, coupled with significant tax cuts, which could explode our already elevated deficits and debt loads.

Suffice it to say, there remains a lot of uncertainty ahead, so before you risk making wholesale changes to your portfolio, why not wait for the President-elect’s actions to take shape rather than overreact to fangless rhetoric. In other words, you can save money if you wait for the race to begin before placing all your bets.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Half Trump Empty, or Half Trump Full?

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (December 1, 2016). Subscribe on the right side of the page for the complete text.

It was a bitter U.S. presidential election, but fortunately, the nastiest election mudslinging has come to an end…at least until the next political contest. Unfortunately, like most elections, even after the president-elect has been selected, almost half the country remains divided and the challenges facing the president-elect have not disappeared.

While some non-Trump voters have looked at the glass as half empty, since the national elections, the stock market glass has been overflowing to new record highs. Similar to the unforeseen British Brexit outcome in which virtually all pollsters and pundits got the results wrong, U.S. experts and investors also initially took a brief half-glass full view of the populist victory of Donald Trump. More specifically, for a few hours on Election Day, stock values tied to the Dow Jones Industrial Average index collapsed by approximately -5%.

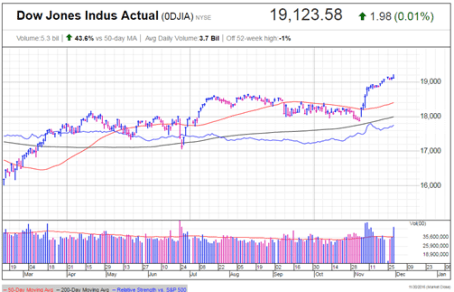

It didn’t take long for stock prices to quickly reverse course, and when all was said and done, the Dow Jones Industrial Average finished the month higher by almost +1,000 points (+5.4%) to finish at 19,124 – a new all-time record high (see chart below). Worth noting, stocks have registered a very respectable +10% return during 2016, and the year still isn’t over.

Source: Investors.com (IBD)

Drinking the Trump Egg Nog

Why are investors so cheery? The proof will be in the pudding, but current optimism is stemming from a fairly broad list of anticipated pro-growth policies.

At the heart of the reform is the largest expected tax reform since Ronald Reagan’s landmark legislation three decades ago. Not only is Trump proposing stimulative tax cuts for corporations, but also individual tax reductions targeted at low-to-middle income taxpayers. Other facets of the tax plan include simplification of the tax code; removal of tax loopholes; and repatriation of foreign cash parked abroad. Combined, these measures are designed to increase profits, wages, investment spending, productivity, and jobs.

On the regulatory front, the President-elect has promised to repeal the Obamacare healthcare system and also overhaul the Dodd-Frank financial legislation. These initiatives, along with talk of dialing back other regulatory burdensome laws and agencies have many onlookers hopeful such policies could aid economic growth.

Fueling further optimism is the prospect of a trillion dollar infrastructure spending program created to fix our crumbling roads and bridges, while simultaneously increasing jobs.

No Free Lunch

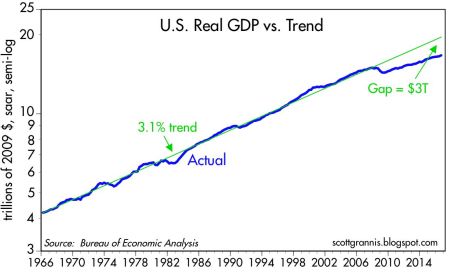

As is the case with any economic plan, there is never a free lunch. Every cost has a benefit, and every benefit has a cost. The cost of the 2008-2009 Financial crisis is reflected in the sluggish economic growth seen in the weak GDP (Gross Domestic Product) statistics, which have averaged a modest +1.6% growth rate over the last year. Scott Grannis points out how the slowest recovery since World War II has resulted in a $3 trillion economic gap (see chart below).

Source: Calafia Beach Pundit

The silver lining benefit to weak growth has been tame inflation and the lowest interest rate levels experienced in a generation. Notwithstanding the recent rate rise, this low rate phenomenon has spurred borrowing, and improved housing affordability. The sub-par inflation trends have also better preserved the spending power of American consumers on fixed incomes.

If executed properly, the benefits of pro-growth policies are obvious. Lower taxes should mean more money in the pockets of individuals and businesses to spend and invest on the economy. This in turn should create more jobs and growth. Regulatory reform and infrastructure spending should have similarly positive effects. However, there are some potential downside costs to the benefits of faster growth, including the following:

- Higher interest rates

- Rising inflation

- Stronger dollar

- Greater amount of debt

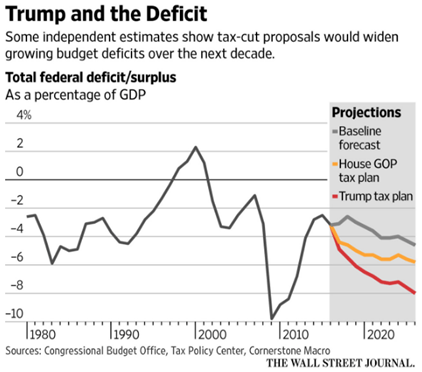

- Larger deficits (see chart below)

Source: The Wall Street Journal

Even though President-elect Trump has not even stepped foot into the Oval Office yet, signs are already emerging that we could face some or all of the previously mentioned headwinds. For example, just since the election, the yield on 10-Year Treasury Notes have spiked +0.5% to 2.37%, and 30-Year Fixed Rate mortgages are flirting with 4.0%. Social and economic issues relating to immigration legislation and Supreme Court nominations are likely to raise additional uncertainties in the coming months and years.

Attempting to anticipate and forecast pending changes makes perfect sense, but before you turn your whole investment portfolio upside down, it’s important to realize that actions speak louder than words. Even though Republicans have control over the three branches of government (Executive, Legislative, Judicial), the amount of control is narrow (i.e., the Senate), and the nature of control is splintered. In other words, Trump will still have to institute the “art of the deal” to persuade all factions of the Republicans (including establishment, Tea-Party, and rural) and Democrats to follow along and pass his pro-growth policies.

Although I do not agree with all of Trump’s policies, including his rhetoric on trade (see Free Trade Boogeyman), I will continue paying closer attention to his current actions rather than his past words. Until proven otherwise, I will keep on my rose colored glasses and remain optimistic that the Trump glass is half full, not half empty.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

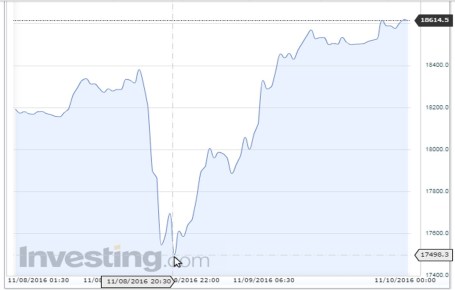

Trump: Bark Worse Than the Bite?

Unless you have been living in a cave this week, you are probably aware the country has elected a new president. Leading up to Election Day, the anxiety was palpable. A populist wave, much like the one experienced in the British Brexit vote earlier this year, resulted in economically disenfranchised voters coming out in full force to vote out the perceived establishment candidate, Hillary Clinton. Financial market pundits and media commentators predicted an immediate 11-13% decline in stock values if Donald Trump were to win. Could they have been more wrong? After a brief -5% decline in pre-trading Dow Jones Industrial Average future prices, the Dow subsequently skyrocketed more than 1,000 points higher to finish up +1.4% for the day (see chart below). For the week, the Dow amazingly rallied by +5.4%.

Source: Investing.com

As I have written on numerous occasions, politics have very little impact on the long-term direction of the financial markets. Yes, it is true that regulations and policies implemented by the president and Congress can influence specific industries or individual companies over the short-run. Hillary Clinton proved this assertion with her pharmaceutical industry tweet, which created a lasting hangover effect on the sector. But guess what? Regulations and politics have always changed throughout our country’s history, with various shifting policies impacting businesses asymmetrically – some positively and some negatively. The good news…in an ever-expanding global economy, accelerated through technology, capitalism forces businesses to adapt to political change.

Considering the amount of our nation’s political variation, what has been our country’s stock market and economic track record over the last 100 years under 17 different presidents (8 Democrats and 9 Republicans)? See chart below:

Source: Macrotrends

Not too shabby judging by the roughly 188x–fold increase in the Dow Jones Industrial Average (or > ~18,700%+ return) to a fresh all-time record high this week. While I am admittedly nervous about a full, Republican tri-power Trump administration (President/House/Senate), the reality is that Trump’s unconventional, unprecedented platform doesn’t fit squarely into the traditional Republican policy boxes. In fact, he has switched his party affiliation five times. President-elect Trump will therefore need to reach across the political aisle to Democrats, and work with Speaker of the House Paul Ryan to accomplish the platform agenda priorities he outlined during his presidential campaign.

While all this political election discussion has been stimulating and exhausting, fortunately, followers of my Investing Caffeine blog understand there are much more important factors than politics affecting the performance of the stock market and economy – namely corporate profits, interest rates, valuations, and sentiment (see Don’t Be a Fool, Follow the Stool).

As mentioned, the market’s returns are influenced by four key factors, but sentiment and stock market values are largely shaped by investor behavior. Trump has less control on investor behavior, but his policies can directly impact corporate profits and interest rates – two critical components of economic health. Part of the reason Trump won the election was due to campaign promises regarding many popular stimulative policies, including personal and corporate tax cuts; infrastructure spending; repatriation of foreign money; tax simplification and reform; Obamacare improvement; and immigration reform.

As it turns out, a good number of the issues relating to these policies happen to be bipartisan in nature. Given the Republican-controlled Congress, investors are perceiving these potential policy changes as positive for the market – at least for the first week of his presidential tenure.

For now, President-elect Trump has struck the proper conciliatory tone and made appropriate comments. In the coming days and weeks, investors are watching closely for tangible evidence and clues of his policy priorities, as he fills key political posts on his presidential team. Time will tell whether the early honeymoon will continue past Trump’s inauguration day, but currently, the consensus is his bark heard during Trump’s heated 18-month presidential campaign is worse than the actual bite of his election victory.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page

Uncertainty: A Love-Hate Relationship

An often over-quoted saying is “The stock market hates uncertainty.” However, the wealthiest investor of all-time has a different perspective about uncertainty:

“The future is never clear. You pay a very high price in the stock market for a cheery consensus. Uncertainty is the friend of the buyer of long-term values.”

-Warren Buffett

Buffett understands the benefits of long-term compounding and the beauty of buying fear and selling greed. Unfortunately, CNBC and every other media outlet do not carry the words “long-term” in their vernacular. Peddling F.U.D. (fear, uncertainty, doubt) equates to eyeballs and clicks, which equates to more advertising dollars. With the volatility index trading at fear-rich Brexit levels above 20, traders are certainly long on F.U.D. Time will tell whether the elections will increase or decrease F.U.D., but unless there is a contested election a la 2000 (Bush-Gore), there will be one less election to worry about and investors can then go back to normal worrying and political bashing.

As I have noted on multiple occasions, from a stock market standpoint, whomever wins (Republican or Democrat) should have no bearing on the performance of the stock market over the medium term as long as there remains gridlock in Washington (see also Fall is Here: Change is Near). Most Americans despise political inactivity, but if like many investors you believe in fiscal discipline, then you prefer fighting over spending, and generally, the more gridlock, the less spending.

In other words, fiscal discipline is likely to win IF there is a split Congress (House & Senate) or if the winning presidential party loses both the Senate and the House. For what it’s worth, Nate Silver, the guy who accurately predicted all 50 states in the 2012 presidential election is currently predicting gridlock (i.e., a split Congress), but the presidential and Congressional polls have been generally tightening across the board. For now, with just three days left before the election, investors have chosen to shoot now, and ask questions later, as evidenced by the 420 point decline in the Dow Jones Industrial Average during the first half of the 4th quarter.

My crystal ball is just as foggy as anybody else’s, and increased volatility in the short-run should come as no surprise to anyone. As in any volatile investment environment, during periods of turbulence, you should compile your shopping list to opportunistically purchase securities selling at a discount. There is no reason to be a hero, but you should prudently deploy cash or readjust your asset allocation, if there is a significant sell-off in risky assets. The same principle works in reverse. If for some unlikely reason, there is a post Brexit-like snapback, one should consider trimming or selling overbought positions.

The main point in periods like these is to let objective reasoning drive your decisions (or lack of decisions), rather than emotions. There has always been a love-hate relationship with uncertainty for traders and investors alike. If you are doing your job correctly, long-term investors should relish F.U.D. because as the saying goes, “This too shall pass.”

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page

What Do You Worry About Next?

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (November 1, 2016). Subscribe on the right side of the page for the complete text.

Boo! Halloween has just passed and frightened investors have still survived to tell the tale in 2016. While most people have gotten spooked by the presidential election, other factors like record-high corporate profits, record-low interest rates, and reasonable valuations have led to annual stock market gains. More specifically, values have risen in 2016 by approximately +4% (or +6% including dividend payments). Despite last week’s accelerating 3rd quarter GDP economic growth figure of +2.9%, which was the highest rate in two years and more than doubled the rate of the previous quarter (up +1.4%), there were still more tricks than treats during October. Recently, scary politics have shocked many Halloween participants into a zombie-like state, as evidenced by stock values declining around -1.7% during October.

This recent volatility is nothing new. Even though financial markets are significantly higher in recent years, that has not prevented repeated corrections over the year(s) as shown below in the 2009 – 2015 chart.

In order to earn higher long-term returns, investors have to accept a certain amount of short-term price movements (upwards and downwards). With a couple months remaining in the year, stock investors have achieved gains through a tremendous amount of economic and geopolitical uncertainty, including the following scares:

- China: A significant fallout from a Chinese slowdown at the beginning of the year (stocks fell about -14%).

- Brexit: A 48-hour Brexit vote scare in June (stocks fell -6%).

- Fed Fears: Threatening comments in September from the Federal Reserve about potentially hiking increasing interest rates (stocks fell -4%).

With the elections just a week away, political anxiety has jolted Americans’ adrenaline levels. The polls continue to move up and down, but as I have repeatedly pointed out, the only certain winner in Washington DC is gridlock. Sure, in a Utopian world, politicians should join hands and compromise to solve all our country’s serious problems. Unfortunately, this is not the case (see Congress’s approval rating). However, there is a silver lining to this dysfunction…gridlock can lead to fiscal discipline.

Our country’s debt/deficit financial situation has been spiraling out of control, in large measure due to rapidly rising entitlement spending, including Medicare, and Social Security. Witnessing all the political rhetoric and in-fighting is very difficult, but as I highlighted in last month’s newsletter, gridlock has flattened the spending curve significantly since 2009 – a positive development.

And although the economic recovery has been one of the slowest since World War II and global growth remains anemic, the U.S. remains a better house in a bad global neighborhood (e.g., Europe and Japan continue to suck wind), as evidenced by a number of these following positive economic indicators:

- Employment Improvement: Unemployment has fallen from 10% to 5% since 2009, and more than 15 million jobs have been added over that period.

- Housing Recovery Continues: Home sales and prices continue their multi-year rise; housing inventories remain tight; and affordability remains strong, given generationally low interest rates.

- Record Auto Sales: Car sales remain near record levels, hovering around 17 million units per year.

- Consumer Confidence on the Rise: Ever since the financial crisis, consumer sentiment figures have rebounded by about 50%.

-

Record Consumer Sales: Consumer spending accounts for approximately 70% of our economy, and as you can see from the chart below, despite consumers saving more, stronger employment and wages are fueling more spending.

Source:Calculated Risk

Source:Calculated Risk

Absent a clean sweep of control by the Democrat or Republican Presidential-Congressional candidates, our democratic system will retain its healthy status of checks and balances. Based on all the current polling data, a split between the White House, Senate, and House of Representatives remains a very high likelihood scenario.

The political process has been especially exhausting during the current cycle, but regardless of whether your candidate wins or loses, much of the current uncertainty will likely dissipate. As the saying goes, at least it is “Better the devil you know than the devil you don’t know.”

After the November 8th elections are completed, there will be one less election to worry about. Thankfully, after 25 years in the industry, I’m not naïve enough to believe there will be nothing else to worry about. When the financial media and blogosphere get bored, at a minimum, you can guarantee yourself plenty of useless coverage regarding the next monetary policy move by the Federal Reserve (see also Fed Fatigue).

Whatever the next set of worries become, U.K. Prime Minister Winston Churchill said it best as it relates to American politics and economics, “You can always count on Americans to do the right thing – after they’ve tried everything else.” If Churchill’s words don’t provide comfort and you had fun getting spooked over the elections on Halloween, feel free to keep wearing your costume. Behind any constructive economic data, the prolific media machine will continue doing their best in manufacturing plenty of fear, uncertainty, and doubt to keep you worried.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Fall is Here: Change is Near

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (October 1, 2016). Subscribe on the right side of the page for the complete text.

Although the fall season is here and the leaf colors are changing, there are a number of other transforming dynamics occurring this economic season as well. The S&P 500 index may not have changed much this past month (down -0.1%), but the technology-laden NASDAQ index catapulted higher (+1.9% for the month and +6.0% for 2016).

With three quarters of the year now behind us, beyond experiencing a shift in seasonal weather, a number of other changes are also coming. For starters, there’s no ignoring the elephant in the room, and that is the presidential election, which is only weeks away from determining our country’s new Commander in Chief. Besides religion, there are very few topics more emotionally charged than politics – whether you are a Republican, Democrat, Independent, Libertarian, or some combination thereof. Even though the first presidential debate is behind us, a majority of voters are already set on their candidate choice. In other words, open-minded debate on this topic can be challenging.

Hearing critical comments regarding your favorite candidate are often interpreted in the same manner as receiving critical comments about a personal family member – people often become defensive. The good news, despite the massive political divide currently occurring in the country and near-record low politician approval ratings in Congress , politics mean almost nothing when it comes to your money and retirement (see also Politics & Your Money). Regardless of what politicians might accomplish (not much), individuals actually have much more control over their personal financial future than politicians.

While inaction may rule the day currently, more action generally occurs during a crisis – we witnessed this firsthand during the 2008-2009 financial meltdown. As Winston Churchill famously stated,

“You can always count on Americans to do the right thing – after they’ve tried everything else.”

Political discourse and gridlock are frustrating to almost everyone from a practical standpoint (i.e., “Why can’t these idiots get something done in Washington?!”), however from an economic standpoint, gridlock is good (see also Who Said Gridlock is Bad?) because it can keep a responsible lid on frivolous spending. Educated individuals can debate about the proper priorities of government spending, but most voters agree, maintaining a sensible level of spending and debt should be a bipartisan issue.

From roughly 2009 – 2014, you can see how political gridlock has led to a massive narrowing in our government’s deficit levels (chart below) – back to more historical levels.This occurred just as rising frustration with Washington has been on the rise.

The Fed: Rate Revolution or Evolution?

Besides the changing season of politics, the other major area of change is Federal Reserve monetary policy. Even though the Fed has only increased interest rates once over the last 10 years, and interest rates are at near-generational lows, investors remain fearful. There is bound to be some short-term volatility if interest rates rise to 0.50% – 0.75% in December, as currently expected. However, if the Fed continues at its current snail’s pace, it won’t be until 2032 before they complete their rate hike cycles.

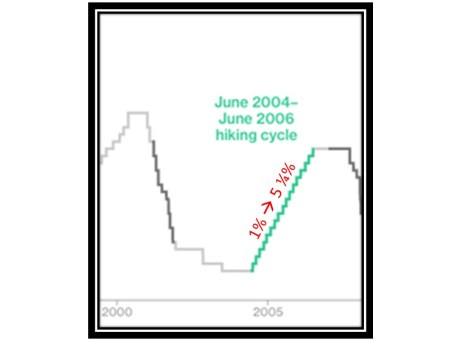

We can put the next rate increase into perspective by studying history. More specifically, the Fed raised interest rates 17 times from 2004 – 2006 (see chart below). Fortunately over this same time period, the world didn’t end as the Fed increased interest rates from 1.00% to 5.25% (stocks prices actually rose around +11%). The same can be said today – the world won’t likely end, if interest rates rise from 0.50% to 0.75% in a few months.

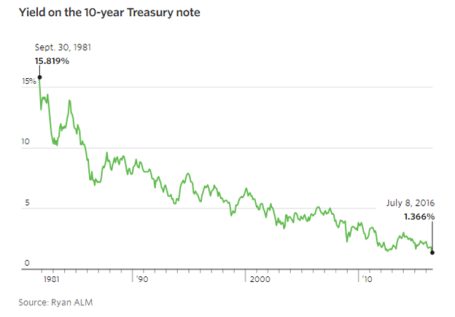

The next question becomes, why are interest rates so low? There are many reasons and theories, but a few of the key drivers behind low rates include, slower global economic growth, low inflation, high demand for low-risk assets, technology, and demographics. I could devote a whole article to each of these factors, and indeed in many cases I have, but suffice it to say that there are many reasons beyond the oversimplified explanation that artificial central bank intervention has led to a 35 year decline in interest rates (see chart below).

Change is a constant, and with fall arriving, some changes are more predictable than others. The timing of the U.S. presidential election outcome is very predictable but the same cannot be said for the timing of future interest rate increases. Irrespective of the coming changes and the related timing, history reminds us that concerns over politics and interest rates often are overblown. Many individuals remain overly-pessimistic due to excessive, daily attention to gloomy and irrelevant news headlines. Thankfully, stock prices are paying attention to more important factors (see Don’t Be a Fool) and long-term investors are being rewarded with record high stock prices in recent weeks. That’s the type of change I love.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Invisible Benefits of Trade

Before the Brexit, 28 countries joined the European Union since its inception in 1957, without a single country leaving. The story is similar if you look at the World Trade Organization (WTO), which has witnessed more than 160 countries unite, without one country exiting since it began in 1948. Are the leaders of these countries idiots and blind to the benefits of trade and globalization? I think not.

For centuries, the advantages of free trade and globalization have lifted the standards of living for billions of people. However, pinpointing the timing or attributing the precise actions leading to these tremendous economic advantages is difficult to do because most trade benefits are often invisible to the naked eye.

Today, populist sentiment on both sides of the political aisle has demonized trade, whether referring to TPP (Trans-Pacific Partnership), NAFTA (North America Free Trade Agreement), trade with China, or announcements by corporations to manufacture goods internationally.

Although it would be naïve to adopt a stance that there are no negative consequences to globalization (e.g., lost American jobs due to offshoring), myopically focusing on job displacement is only half the equation.

While I can attempt to articulate the economic costs and benefits of free trade, and I’ve tried (see Productivity & Trade), Dan Ikenson of the Cato Institute explains it much better than I can. Here is a more eloquent synopsis of free trade (hat-tip: Scott Grannis):

“The case for free trade is not obvious. The benefits of trade are dispersed and accrue over time, while the adjustment costs tend to be concentrated and immediate. To synthesize Schumpeter and Bastiat, the “destruction” caused by trade is “seen,” while the “creation” of its benefits goes “unseen.” We note and lament the effects of the clothing factory that shutters because it couldn’t compete with lower-priced imports. The lost factory jobs, the nearby businesses on Main Street that fail, and the blighted landscape are all obvious. What is not so easily noticed is the increased spending power of the divorced mother who has to feed and clothe her three children. Not only can she buy cheaper clothing, but she has more resources to save or spend on other goods and services, which undergirds growth elsewhere in the economy.

Consider Apple. By availing itself of lowskilled, low-wage labor in China to produce small plastic components and to assemble its products, Apple may have deprived U.S. workers of the opportunity to perform that low-end function in the supply chain. But at the same time, that decision enabled iPods and then iPhones and then iPads to be priced within the budgets of a large swath of consumers. Had all of the components been produced and all of the assembly performed in the United States — as President Obama once requested of Steve Jobs — the higher prices would have prevented those devices from becoming quite so ubiquitous, and the incentives for the emergence of spin-off industries, such as apps, accessories, Uber, and AirBnb, would have been muted or absent.

But these kinds of examples don’t lend themselves to the political stump, especially when the campaigns put a premium on simple messages. This is the burden of free traders: Making the unseen seen. It is this asymmetry that explains much of the popular skepticism about trade, as well as the persistence of often repeated fallacies.

The benefits of trade come from imports, which deliver more competition, greater variety, lower prices, better quality, and new incentives for innovation. Arguably, opening foreign markets should be an aim of trade policy because larger markets allow for greater specialization and economies of scale, but real free trade requires liberalization at home. The real benefits of trade are measured by the value of imports that can be purchased with a unit of exports — our purchasing power or the so-called terms of trade. Trade barriers at home raise the costs and reduce the amount of imports that can be purchased with a unit of exports.

Protectionism benefits producers over consumers; it favors big business over small business because the cost of protectionism is relatively small to a bigger company; and, it hurts lower-income more than higher-income Americans because the former spend a higher proportion of their resources on imported goods.

…Even if there were a President Trump or President Sanders, rest assured that the Congress still has authority over the nuts and bolts of trade policy. The scope for presidential mischief, such as unilaterally raising tariffs, or suspending or amending the terms of trade agreements, is limited. But it would be more reassuring still if the intellectual consensus for free trade were also the popular consensus.”

Fortunately, Ikenson supports the case I’ve made repeatedly. The power of presidential politics is limited by the Congress (see Politics and Your Money). Frustration with politics has never been higher, but in many cases, gridlock is a good thing.

The destructive impacts of protectionist, anti-trade policies is unambiguous – just consider what happened from the implementation of Smoot-Hawley tariffs in 1930 around the time of the Great Depression. U.S. imports decreased 66% from $4.4 billion (1929) to $1.5 billion (1933), and exports decreased 61% from $5.4 billion to $2.1 billion. GNP fell from $103.1 billion in 1929 to $75.8 billion in 1931 and bottomed out at $55.6 billion in 1933.

It’s important to remember, any harmful downside to trade is overwhelmed by the upside of growth. Greg Ip of the WSJ used Doug Irwin, a trade historian at Dartmouth College, to make this pro-growth point:

“If two million American workers lose $15,000 in annual income forever—an extreme estimate of the impact of trade with China—while 320 million American consumers gain just $100 from trade, the benefits to all of society still exceed the costs.”

The benefits of free trade may be invisible in the short run, but over the long-run, the growth advantages of free trade are perfectly visible, despite protectionist, anti-trade rhetoric and propaganda dominating the presidential election conversation.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), and AAPL, but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Politics & Your Money

Will you be able to retire, and what impact will the elections have on your financial future? Answering these questions can be a scary endeavor. And unless you have been living in a cave, you may have noticed we are in the middle of a heated U.S. presidential election campaign between Donald Trump and Hillary Clinton. Regardless of which side of the political fence you stand on, the prospects of your retirement are much more likely to be impacted by your personal actions than by the actions of Washington politicians.

Even if you despise politics and were living in a cave (with WiFi access), there’s a high probability you would be overloaded with detailed and dogmatic online editorials from overconfident Facebook friends. Besides offering self-assured predictions, these impassioned political pleas generally itemize the top 10 reasons your favorite candidate is a moron, and another 10 reasons why their candidate is the greatest.

Your friends’ opinions may have pure intentions, but unfortunately, rarely, if ever, do their thoughts alter your views. A reference from a recent Legal Watercooler article summed it up best:

“Political Facebook rants changed my mind…said nobody, ever.”

Nearly as ineffectual as political Facebook opinions on your politics is the ineffectual influence of presidential elections on your finances. For example, over the last four decades, stock prices have gone up and down during both Republican and Democrat presidential terms. The picture looks much the same, if you analyze the fiscal performance of conservatives and liberals since 1970 – debt burdens as a percentage of economic output have risen and fallen under both political parties. No matter who wins the presidency, many investors forget the ability of that individual to affect change is highly dependent upon the political balance of power in Congress. If Congress holds a split majority in the House and Senate, or the opposition party commands the entire Congress, then the winning presidential candidate will be largely neutered.

Rather than panic over a political loss or celebrate a candidate’s victory, here are some tangible actions to improve your finances:

- Organize. Typically individuals have investment and saving accounts scattered with no cohesive accounting or strategy. Get your financial house in order by gathering and organizing all your accounts.

- Budget. Spend less than you take in. Or in other words…save. You can achieve this goal in one of two ways – cut your spending, or increase your income.

- Create a Plan. When do you plan to retire? How much money do you need for retirement? What asset allocation and risk profile should you adopt to meet your financial goals?

If you have difficulty with any of these actions, then meet with an experienced financial professional to assist you.

Politics can trigger very emotional responses. However, realizing your actions have a much more direct impact on your finances than political Facebook rants and temporary elections will benefit you in achieving your long-term financial goals.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds and FB, but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Dolphin or Shark…Time for Concern?

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (March 1, 2016). Subscribe on the right side of the page for the complete text.

Through the choppy stock market waters of February, investors nervously tried to stay afloat as they noticed a fin cutting through the water. The only problem is determining whether the fin approaching is coming from a harmless dolphin or a ferocious shark? The volatility in 2016 has been disconcerting for many, but a life preserver was provided during the month with the Dow Jones Industrial Average up a modest 50 points (+0.30%).

Remaining calm can be challenging when facing a countless number of ever-changing concerns. Stock investors have caught lots of fish since early 2009 (prices have about tripled), but here are some of the scary headlines (fins) floating out in the financial markets:

- Recession? Overall corporate profits have slowed in the face of plummeting energy prices and the headwind of a strong dollar. However, corporate profit margins remain near record levels and if you exclude the decline in the troubled oil patch, core profits keep chugging along. If an imminent recession were actually on the horizon, you wouldn’t expect to see a 4.9% unemployment rate (8-year low); record auto sales; an improving housing market; and stimulative national gasoline prices at $1.75/gallon (recent recessions have been caused by high energy prices).

- Negative Interest Rates: Would you like to get paid to borrow money? With $6 trillion dollars of negative interest rate bonds in the market (see chart below), that’s exactly what is happening. Just imagine walking into your local Best Buy, and asking the salesman, “Can I borrow $2,000 to buy that big screen TV there…and oh by the way, can you pay me interest every month after you give me the money?” Scary to think many people are panicked over the stock market when they should be more alarmed over negative interest rates. Would you rather earn 6.4% on the average stock (S&P 500 earnings yield) and a 2.2% dividend yield vs negative interest rate bonds? As I always caution investors, even though interest rates are at/near a generational low, diversified portfolios still need exposure to bonds, even if you’re at/near retirement because of the stability they provide. Bonds act like expensive pillows – they are necessary to sleep at night. Although some observers point to negative rates as a sign of a global collapse, low inflation, aggressive foreign central bank monetary policies, and a lingering risk aversion hangover from the 2008-09 financial crisis probably have more to do with the current strange status of interest rates.

Source: Financial Times

- Political Turbulence: Uncertainty abounds in another election year, just as is the case every other four years. As we head into Super Tuesday, the day in the presidential primary season when the largest number of states hold primary elections, the Republicans are set to battle for approximately half of the delegates necessary to secure the party nomination. The Democrats will be competing for about one-third of the delegates. While many individuals are placing paramount importance on the outcomes of the presidential elections, history teaches us otherwise. The ultimate person elected as president will certainly have a significant impact on the direction of the country, but there are other contributing factors as important (or more important) to economic growth, including the Federal Reserve, and the two houses of Congress. On numerous occasions, I have pointed out the irrelevance of presidential politics (see also Who Said Gridlock is Bad?). As the chart shows below, the past confirms there is no consistency to stock market performance based on political party affiliations. Stocks have performed strongly (and poorly) under both party affiliations.

- Brexit? After lengthy negotiations with EU leaders in Brussels, Britain’s Prime Minister David Cameron set June 23rd as the referendum date for voters to determine whether Britain stays in the European Union. Opinions remain divided (see chart below), but we have seen this movie before with Greece’s threat to leave the EU. As we experienced with the Greece exit (“Grexit”) drama, calmer heads are likely to prevail again. Nevertheless, until the end of June, regrettably we will be forced to listen to continued Brexit fears (see also Brexit article in the Economist for a more thorough review).

- Collapsing Oil Prices: The violent decline in oil prices over the last few years has been swift from about $100/barrel to $34/barrel today. However, the economic slowdown in China, coupled with a stronger U.S. dollar, has led to a broad downfall in commodity prices over the last five years as well. As much as declining demand has hurt commodities and been stimulative for buyers, over-building and excess supply has pressured prices equally. Fortunately, there are signs commodity prices could be in the process of bottoming (see CRB Index).

Financial market volatility in early 2016 has frayed some nerves, and the appearance of swirling fins has many investors wondering whether now’s the time to swim for shore or remain calm and catch the next growth wave. Despite the concerns over a potential recession, negative interest rates, bitter politics, Brexit fears, and depressed oil prices, our economy keeps slowly-but-surely powering forward. While U.S. corporations have been negatively impacted by a strong currency, compressed banking profits (i.e., lower interest rates), and a weak energy sector, S&P 500 companies are rewarding investors by returning a record $1 trillion in dividends and share buybacks (up from $500 million in 2005). When swimming in the current financial markets, you will be better served by swimming with the harmless dolphins rather than panicking over imaginary sharks.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in BBY or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Thank You Volatility

“Look at market fluctuations as your friend rather than your enemy; profit from folly rather than participate in it.” -Warren Buffett

We’ve had some choppy markets and that’s fine by me. Great investors love uncertainty because volatility equates to opportunity. Selling or shorting into volatile euphoria and buying into panic is a time-tested, wealth creating strategy. On the other hand, when everything is consistently moving in one direction, either upwards or downwards, investing can be an easy and straight forward momentum game. Buy something and watch it go up…short something and watch it go down.

In tough, choppy, trendless markets, identifying trends by active traders becomes more challenging. During tricky markets like we’re in now is when the wheat gets separated from the chaff. Day traders and speculators act on a zig one day and are forced to zag the next. Because of the volatile, whippy market dynamics, this type of active trading by individuals rapidly destroys portfolios, not only because of the transaction costs and taxes, but also due to impact costs and spread losses (i.e., bid-ask).

Often, the greater losses come from the behavioral aspects of active trading. Performance chasing and/or the pursuit of overzealous loss mitigation frequently are driven by the destructively entrenched emotions of fear and greed. In the past, I can’t tell you how many times I have rushed into a highflying stock, only to see it pull back down -15-20%, in short order. On the flip side, how often have stocks bounced significantly, after I’ve made a panicked sale? Too many, unfortunately. Most investors don’t take to heart the fact that whenever you initiate a trade, you need to be right twice to optimize your profits. In other words, the security you initially sell needs to go lower (i.e., you should have kept the original investment), AND the security you subsequently buy needs to go higher (i.e., you shouldn’t have purchased the new investment in the first place).

Even in the cases in which the balance of the buy/sale trades becomes a wash, the trading costs and taxes will eat the active trader alive. Unfortunately, the other outcome of losing on both sides of the trade (the purchase goes lower and sale goes higher) is all too common. For example, the purchase you falls by -3%, and the investment you sold climbs +10%. Doing nothing would have been the best outcome!

All this investment tail-chasing inevitably results in a lot of portfolio bloodletting. There is plenty of academic research that shows practically all day traders lose money. Terrance Odean from Cal-Berkeley used 14 years of day trader data to conclude that more than 98% of day traders lose money. Even for those traders able to make a profit in the short run, usually the success doesn’t last very long:

- 40% of day traders quit within a month

- 87% of traders quit within 3 years

- 93% of traders quit within 5 years

Other sources besides Odean show the percentage of day trading losers as greater than 95%, and if you don’t trust the academic data, then simply ask your accountant what percentage of his/her active trading clients make a profit, after considering all taxes and trading costs.

While I may not necessarily fully rejoice in the pain and carnage of day traders, I am always thankful for these choppy markets. Without volatility, anybody can make money in upward trending markets (e.g., day traders did better in the mo-mo 1990s), but in those markets long-term opportunities become sparse. Without the transitory headlines of tightening Federal Reserve policy, negative interest rates, a strong dollar, and political dysfunction, I would not have a professional investing job. And for that blessing, I want to sincerely say, “Thank you volatility.”

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}