Posts tagged ‘Nobel Prize’

The Traitorous 8 and Birth of Silicon Valley

Over my 25 year investment career, I’ve made quite a few technology investments and visited dozens of Silicon Valley companies. I heard bits and pieces about the story of the Traitorous 8, but I never fully comprehended the technology revolution they started. Out of intellectual curiosity, I decided to delve a little deeper into the topic.

At the heart of this topic is a small device about the size of a fingernail. This object has several different names and can be quite confusing. The official name is an integrated circuit or IC, but usually it’s referred to as a chip, microchip, or semiconductor. These chips have become ubiquitous, scattered invisibly throughout our daily lives in our cars, computers, TVs, cell phones, appliances, and remote controls (an average household is home to about 1,000 of these semiconductors). Despite most people taking the microchip for granted, this diminutive piece of silicon created from our beach’s sand has contributed the largest burst of wealth creation in human history.

Before gaining a true understanding into the birth of Silicon Valley, we have to better understand the historical context in which the global technology capital was created – this takes us back to the early twentieth century when the vacuum tube was invented in 1904. Before Al Gore invented the Internet, we needed computers, and before we had personal computers, we needed integrated circuits, and before we had integrated circuits we had vacuum tubes (see chart below). Vacuum tubes were the electronic circuitry components required to make telephones, radios and televisions work in the early 1900s.

Tech History & the Vacuum Tube

The vacuum tube was invented in 1904 by an English physicist named John Ambrose Fleming. Like semiconductors, the main function of a vacuum tube is to control the flow of electric current. More specifically, a vacuum tube controls the current transferred between cathode and anode to make a circuit. Vacuum tubes were used for amazing applications, but in modern society this technology has been largely replaced by semiconductors, primarily because of cost, scalability and reliability factors.

The first all-electronic digital computer title is usually awarded to the ENIAC computer, which stood for Electronic Numerical Integrator and Calculator. ENIAC was built at the University of Pennsylvania between 1943 and 1945 by two professors, John Mauchly and J. Presper Eckert. World War II, the Soviet Union Cold War, and the space race kicked off by the Sputnik launch all pushed the vacuum tube technology to its limits. To give you an idea of how costly and inefficient vacuum tubes were relative to today’s microchips consider some of the ENIAC statistics. ENIAC filled a 20 x 40 foot room; weighed 30 tons; used more than 18,000 vacuum tubes; and only operated 50% of the time because operators were continuously replacing burned out vacuum tubes. In fact, the ENIAC vacuum tubes generated so much heat, the temperature in the computer room often reached 120 degrees.

Shockley – The Godfather of the Transistor

Something had to change to improve vacuum tube technology, and it did…thanks in large part to a physicist named William Shockley, the so-called “Godfather of the Transistor.” Shockley received his Bachelor of Science degree from Caltech in 1932 and earned his Ph.D. degree from MIT in 1936. After graduation, Shockley left the famous Bell Labs research center, which was a research division of AT&T at the time (now owned by Nokia). As part of Shockley’s work at Bell Labs in the late 1940s, he contributed to the invention of the transistor with experimentalist Walter Brattain and quantum theorist John Bardeen. Fundamentally, the transistor is a switch, which over time has shrunk down to the size of a virus. The transistor is what ultimately replaced the vacuum tubes because it is smaller, more efficient, more reliable, more durable, and cheaper than vacuum tubes. Transistors switch and amplify the flow of electronic signals to create digital ones and zeros that instruct electronic applications. Without the benefits of shrinking transistors, today’s computer servers would be three stories high.

How small have transistors become? Take the iPhone 6 for example – it uses the A8 chip, which is made up of a whopping two billion transistors. To accomplish this feat, engineers are now creating transistors at the atomic level. Large semiconductor manufacturers like Intel Corp (INTC) are now developing transistors at the 10 nanometer level. To put this scale into perspective, consider a sheet of paper is approximately 100,000 nanometers thick. So in order to create a 10 nanometer sheet of paper, one would have to slice a single sheet 10,000 times thinner to reach 10 nanometers…mind-boggling.

Building atomic sized transistor technology is very cool, but also very expensive. Only a handful of semiconductor manufacturers have enough capital to build these new state-of-the art facilities. Case in point is Intel’s D1X fabrication facility in Hillsboro, Oregon, which is estimated to have cost $6 billion. Like seeing the pyramids – it’s difficult to understand the enormity of the structure without visiting it, which I was fortunate to do in 2014. It’s very ironic that in order to build these microscopic transistors and integrated circuits, multi-billion dollar manufacturing facilities the size of 38 football fields (~2.2 million square feet) are required. Another example of a next-generation manufacturing facility is Taiwan Semiconductor’s – Fab 15 (TSM), which was estimated to cost $9.3 billion.

These mega-transistor manufacturing facilities would not have been possible without Shockley’s contributions. Having helped invent the transistor largely replace the dominant computing technology of the last half century (i.e., vacuum tube), Shockley mustered up the courage to leave Bell Labs and start his own company, but he needed some cash to make it happen. He contacted Arnold Beckman, CEO of Beckman Coulter and his old professor at Caltech. Over a boat ride in Newport Beach, California, Shockley asked Beckman for $1 million to start his own lab. Silicon Valley potentially could have started in Southern California, but Shockley explained his aging mother lived in Palo Alto and convinced Beckman to start Shockley Semiconductor Laboratory in Mountain View, California during 1956.

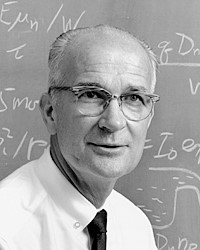

After Shockley Semiconductor began operations, everything appeared to be going according to plan. Shortly after opening shop and recruiting the best and brightest engineers across the country, Shockley and his former Bell Labs colleagues Walter Brattain and John Bardeen were notified they all had won the Nobel Prize in physics (see photo below).

After the Nobel Prize celebrations, everything went downhill quickly. Shockley was known as a brilliant engineer but a horrific manager. He put his employees through a battery of tests including psychological tests, intelligence tests, and even lie detector tests. Shockley also posted employee salaries publicly and recorded phone calls. He was a paranoid individual who believed his workers were stealing trade secrets and sabotaging projects, so therefore he wouldn’t share findings with his research staff. Adding insult to injury, Shockley was a racist, who believed blacks were genetically inferior with subpar IQs, so they shouldn’t have kids.

Here is a video link summarizing William Shockley’s leadership:

The Traitorous 8 Surface

In 1957, the year after Shockley Semiconductor Labs started up, the division reached 30 employees. Eight of the employees, Sheldon Roberts, Eugene Kleiner, Victor Grinich, Jay Last, Julius Blank, Jean Hoerni, Robert Noyce, and Gordon Moore finally said, enough-is-enough and decided mutiny was their best option.

The disgruntled group ended up contacting a 30-year-old, snot-nosed, Harvard MBA graduate named Arthur Rock, the individual who eventually coined the phrase “venture capitalist.” In 1957, Rock was a New York banker working at Hayden Stone & Co. Rock believed the group of eight engineers (six of which had Ph.Ds) deserved attention, given their experience working with a Nobel Prize winner. The Traitorous 8 simply wanted to find an employer that would hire them as a group, but Rock advised them to start their own company – a novel idea during the 1950s.

After making a list and calling about 40 blue chip companies from the Wall Street Journal for funding, Rock almost gave up until they received a lead to contact Sherman Fairchild. Fairchild was a wealthy entrepreneur and playboy who hung out at the El Morocco in New York with Howard Hughes. Rock convinced Fairchild, the CEO of Fairchild Camera & Instrument, to invest $1.5 million into a Traitorous 8 startup.

The rest is history. The Traitorous 8 set up shop as Fairchild Semiconductor (FCS) in Mountain View, about twelve blocks from Shockley’s operations. Over the next 10 years, Fairchild Semiconductor grew from twelve employees to twelve thousand employees, and raked in some $130 million in annual revenues. Of the original Traitorous 8, two have become historical figures – Robert “Bob” Noyce and Gordon Moore. All good things come to an end, and Noyce and Moore increasingly got frustrated with Fairchild’s mismanagement of the semiconductor division.

After Fairchild passed over Noyce for a CEO promotion in 1968, Noyce told Moore, “I’m going to leave, are you interested?” Moore agreed, so he and Noyce contacted Arthur Rock again for his assistance. Rock quickly helped them raise $2.5 million, and Intel Corporation (short for “Integrated Electronics”) was born. Three years later in 1971, Intel launched its IPO at $23.50 per share ($.02 split-adjusted). An investment of $10,000 back then would be worth about $12,000,000 today –about a +120,000% return.

Here’s a video summarizing the creation of Intel:

Thomas Edison of Silicon Valley

Nowadays, Noyce is hailed by many as the “Thomas Edison of Silicon Valley.” Noyce received his Ph.D. from MIT and is most known for his invention of the integrated circuit. During the late 1950s, other engineers also worked on the IC, including Jack Kilby at Texas Instruments, but Noyce received the first patent in 1961. Unlike Kilby, who created his IC from germanium, Noyce created his IC from silicon, the semiconductor of choice still today. After a decade of litigation, Noyce and Kilby settled their differences and decided to cross-license their patents. Unfortunately, the Nobel Foundation doesn’t issue Nobel Prizes posthumously, so when the Nobel Prize was issued for the invention of the integrated circuit in the year 2000 (10 years after Noyce’s death), only Kilby was recognized. To Kilby’s credit, he acknowledged the contributions of Noyce and others in his Nobel speech with a story of a rabbit and beaver looking up at the Hoover Dam, “No, I didn’t build it myself. But it’s based on an idea of mine!”

Moore’s Law Established

Arguably, Moore was just as influential as Noyce, but due to his quiet leadership style, Moore is often overlooked. Moore was a year younger than Noyce and earned his chemistry degree from Berkeley and Ph.D. from Caltech. Unlike Noyce, who grew up in the Midwest (Iowa), Moore was raised near Palo Alto, which made recruiting Moore by William Shockley quite easy. Moore’s largest contribution is considered to “Moore’s Law,” which generally states the number of transistors (i.e., a chip’s computing power) will double every 1-2 years. During the 1980s, Noyce described the implications of Moore’s Law by comparing Moore’s Law to the airline industry. If the airline industry progressed at the trajectory of the semiconductor industry over the last 20 years, then the 767 airplane would cost $500 and travel around the world in 20 minutes on five gallons of gas. Regrettably, not many industries advance at the pace of semiconductors.

Moore came up with “Moore’s Law” when her wrote a seminal article for Electronics magazine in 1965 and in the article he properly predicted that the number of transistors that could be squeezed onto a microchip (around 60 at the time) would increase 1,000-fold to 60,000 transistors by 1975. It would take decades for his projections to come true, but Moore very presciently predicted the explosion of home computers, cell phones (which he called “portable communications equipment”), electronic wrist-watches, digital cars, and a host of other electronic devices and applications. A half century later, Moore’s Law holds true, but the pace of transistor growth admittedly is slowing. The physics behind semiconductor manufacturing is running into serious limitations of quantum mechanics, cost, and heat. Microchips are becoming so dense and fast that the internal components in many cases are melting the chips in research labs.

Here is a video link summarizing Moore’s Law:

While Moore’s Law is approaching diminishing returns, the costs of microchips keep declining, power keeps increasing, and efficiency keeps improving. Despite the slowing in Moore’s Law, as you can see below, the adoption of transistors via microchips is not plateauing. According to Intel, we are now consuming an estimated sextillion transistors!

Source: Intel Corporation

Politics, economics, terrorism, and social issues may dominate the daily headlines, but behind the scenes there are daily miracles occurring due to technology advancements. Driving much of that innovation is the microchip, and without the Traitorous 8, the world would look a lot different and there would be no Silicon Valley as we know it today. Had Robert Noyce and Gordon Moore miserably resigned themselves to remain at Shockley Semiconductor, perhaps mankind would not have achieved the giant strides in global standards of living (see chart below). Thankfully, their contributions live on today and ensure a bright future for our kids, grandchildren, and the world at large.

Source: FRED

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and in INTC (non-discretionary), TXN (non-discretionary), T (non-discretionary), but at the time of publishing had no direct position in TSM, NOK, FCS, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Decision Making on Freeways and in Parking Lots

Many drivers here in California adhere to the common freeway speed limit of 65 miles per hour, while some do not (I’ll take the 5th). In the vast majority of cases, racing to your destination at these faster speeds makes perfect sense. However, driving 65 mph through the shopping mall parking lot could get you killed, so slower driving is preferred in this instance. Ultimately, the specific environment and situation will dictate the rational and prudent driving speed. Decision making works in much the same way, and Daniel Kahneman, a Nobel Prize winner, has encapsulated his decades of research in psychology and economics in his most recent book, Thinking, Fast and Slow.

Much of Kahneman’s big ideas are analyzed through the lenses of “System 1” and “System 2” – the fast and slow decision-making processes persistently used by our brains. System 1 thinking is our intuition in the fast lane, continually making judgments in real-time. Our System 1 hunches are often correct, but because of speedy, inherent biases and periodic errors this process can cause us to miss an off-ramp or even cause a conclusion collision. System 2, on the other hand, is the slower, methodical decision-making process in our brains that keeps our hasty System 1 process in check. Although little mental energy is exerted by using System 1, a great deal of cerebral horsepower is required to use System 2.

Summarizing 512 pages of Kahneman’s book in a single article may be challenging, nevertheless I will do my best to summarize some of the interesting highlights and anecdotes. A multitude of Kahneman’s research is reviewed, but a key goal of the book is designed to help individuals identify errors in judgment and biases, in order to lower the prevalence of mental mistakes in the future.

Over Kahneman’s 50+ year academic career, he has uncovered an endless string of flaws in the human thought process. To bring those mistakes to life, he uses several mind experiments to illustrate them. Here are a few:

Buying Baseball: We’ll start off with a simple Kahneman problem. If a baseball bat and a ball cost a total of $1.10, and the bat costs $1 more than the ball, then how much does the ball cost? The answer is $0.10, right? WRONG! Intuition and the rash System 1 forces most people to answer $0.10 cents for the ball, but after going through the math it becomes clear that this gut answer is wrong. If the ball is $0.10 and the bat is $1 more, then that would mean the bat costs $1.10, making the total $1.20…WRONG! This is clearly a System 2 problem, which requires the brain to see a $0.05 ball plus $1.05 bat equals $1.10…CORRECT!

The Invisible Gorilla: As Kahneman points out, humans can be blind to the obvious and blind to our blindness. To make this point he references an experiment and book titled Invisible Gorilla, created by Chritopher Chabris and Daniel Simons. In the experiment, three players wearing white outfits pass a basketball around at the same time that a group of players wearing black outfits pass around a separate basketball. The anomaly in the experiment occurs when someone in a full-sized gorilla outfit goes prancing through the scene for nine full seconds. To the surprise of many, about half of the experiment observers do not see the gorilla. In addition, the gorilla-blind observers deny the existence of the large, furry animal when confronted with recorded evidence (see video below).

Green & Red Dice: In this thought experiment, Kahneman describes a group presented with a regular six-sided die with four green sides (G) and two red sides (R), meaning the probability of the die landing on green (G) is is much higher than the probability of landing on red (R). To make the experiment more interesting, the group is provided a cash prize for picking the highest probability scenario out of the following three sequences: 1) R-G-R-R-R; 2) G-R-G-R-R-R; and 3) G-R-R-R-R-R. Although most participants pick sequence #2 because it has the most greens (G) in it, if one looks more closely, sequence #2 is the same as #1 except for sequence #2 has an additional green (G). Therefore, the highest probability winning answer should be sequence #1 because sequence #2 adds an uncertain roll that may or may not land on green (G).

While the previous experiments described some notable human decision-making flaws, here are some more human flaws:

Anchoring Effect: Was Gandhi 114 when he died, or was Gandhi 35 when he died? Depending how the question is asked, asking the initial question first will skew the respondents answer to a higher age, because the respondents answer will be somewhat anchored to the number “114”. Similarly, the price a homebuyer would pay for a house will be influenced or anchored to the asking price. Another word used by some for anchoring is “suggestion”. If a subliminal suggestion is planted, people’s responses can become anchored to that idea.

Overconfidence: We encounter overconfidence in several forms, especially from what Kahneman calls the “Illusion of Pundits,” which is the confidence that comes with 20-20 hindsight experienced in our 24/7 media world. Or as Kahneman states in a different way, “The illusion that we understand the past fosters overconfidence in our ability to predict the future.” Driving is another example of overconfidence – very few people believe they are poor drivers. In fact, a well-known study shows that “90% of drivers believe they are better than average,” despite defying the laws of mathematics.

Risk Aversion: In Kahneman’s book, he also references risk aversion studies by Mathew Rabin and Richard Thaler. What the researchers discovered is that people appear to be irrational in the way they respond to certain risk scenarios. For example, people will turn down the following gambles:

A 50% chance to lose $100 and a 50% chance to win $200;

OR

A 50% chance to lose $200 and a 50% chance to win $20,000 .

Although rational math would indicate these are smart bets to take, however most people decline the game because humans on average weigh losses twice as much as gains (see also the Pleasure/Pain Principle). To get a better understanding of predictive human behavior, the real emotional costs of disappointment and regret need to be accounted for.

Truth Illusions: A reliable way to make people believe in falsehoods is through repetition. More exposure will breed more liking. In addition to normal conversations, these repetitive truth illusions can be witnessed in propaganda or advertising. Minimizing cognitive strain also reinforces points. Using bold, colored, and contrasted language is more convincing. Simpler language rather than more complex language is also more credible.

Narrative Fallacies: We humans have an innate desire to continually explain the causation of an event due to skill or stupidity – even if randomness is the best explanation.People try to make sense of the world, even though many outcomes have no straightforward explanation. Often times, a statistical phenomenon like “regression to the mean” can explain the results (i.e., outliers revert directionally toward averages). The “Sports Illustrated Jinx,” or the claim that a heralded cover story athlete will be subsequently cursed with bad performance, is used as a case in point. Actually, there is no jinx or curse, but often fickle luck disappears and athletic performance reverts to norms.

Kahneman on Stocks

Many of the principles in Kahneman’s book can be applied to the world of stocks and investing too. According to Kahneman, the investing industry has been built on an “illusion of skill,” or the belief that one person has better information than the other person. To make his point, Kahneman references research by Terry Odean, a finance professor at UC Berkely, who studied the records of 10,000 brokerage accounts of individual investors spanning a seven-year period and covering almost 163,000 trades. The net result showed dramatic underperformance by the individual traders and confirmed that stocks sold by the traders consistently did better than the stocks purchased.“Taking a shower and doing nothing” would have been better than the value destroying trading activity. In fact, the most active traders did much worse than those who traded the least. For professional managers the conclusions are not a whole lot different. “For a large majority of fund managers, the selection of stocks is more like rolling dice than like playing poker. Typically at least two out of every three mutual funds underperform the overall market in any given year,” says Kahneman. I don’t disagree, but I do believe, like .300 hitters in baseball, there are a few managers that can consistently outperform.

There are a lot of lessons to be learned from Daniel Kahneman’s book Thinking, Fast and Slow and I apply many of his conclusions to my investment practice at Sidoxia. We all race through decisions every day, but as he repeatedly points out, familiarizing ourselves with these common mental pitfalls, and also utilizing our more methodical and accurate System 2 thought process regularly, can create better decisions. Better decisions not only for our regular lives, but also for our investing lives. It’s perfectly OK to race down the mental freeway at 65 mph (or faster), but don’t forget to slow down occasionally, in order to avoid mental collisions.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Gekko & Greed – Friedman & Freedom

Gordon Gekko and Milton Friedman

As the old saying goes, the more things change, the more things stay the same. The topic of greed, fat cat bankers, and political self-preservation is just as prevalent and relevant today as it was three decades ago, as evidenced by Milton Friedman’s past television interview (see video below). Milton Friedman and Gordon Gekko, the conniving financier from Oliver Stone’s movie Wall Street played by Michael Douglas, both may not philosophically agree on all aspects of life and politics but Friedman would likely buy into much of Gekko’s view on greed:

“Greed, for lack of a better word, is good. Greed is right, greed works. Greed clarifies, cuts through, and captures the essence of the evolutionary spirit. Greed, in all of its forms; greed for life, for money, for love, knowledge has marked the upward surge of mankind. And greed, you mark my words, will not only save Teldar Paper, but that other malfunctioning corporation called the USA.”

Although Friedman held some extreme views on certain issues, fundamentally underlying all his principles was his convicted belief in freedom – political, individual, and economic freedom.

Some things never change – Milton Friedman talks about greed and capitalism with Phil Donahue.

Background

Milton Friedman (1912-2006), one of the greatest economists of the 20th Century was a Nobel Prize winner in economics, Professor at the University of Chicago (1946-1977), and an economic advisor to President Ronald Reagan. Friedman’s laissez-faire economic views coupled with his belief that government should be severely restricted, not only had a significant influence on the field of economics in the United States, but also globally. His body of work was expansive, but some major areas of contribution include his impact on Federal Reserve monetary policy; his written work on consumption and the natural rate of unemployment; and his rejection of the Phillips curve (the inverse relation of inflation relative to unemployment), to name a few.

Political & Economic Firestorm on the Horizon

Although Friedman is tightly associated with his Republican advisor work (including Ronald Reagan), he strictly considered himself a Libertarian at the core. As much as politically left leaning Americans are blaming the 2008-2009 financial crisis on Friedman-backed deregulation and a lack of government oversight, Conservatives and Libertarians are screaming bloody murder at the Democratic controlled Congress when it comes to all the bailouts, stimulus, and entitlement legislation. If Milton Friedman is looking down upon us now, my guess is that his vote is to flush all the proposed government spending down the toilet, let the failing financial institutions drown, and for Gordon Gekko’s sake, let the greedy, fat cat bankers thrive.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at time of publishing had no direct position on any security referenced. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}

{kind=link}

{kind=link}

{kind=link}