Posts tagged ‘mergers and acquisitions’

Why the Masses Missed the 10-Year Bull Market

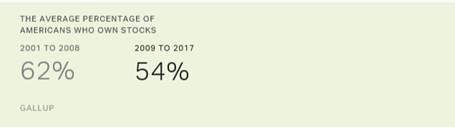

The investing masses generally are notoriously short-termed focused. Although the overall stock market notched another gain this month, stock values are still down roughly -8% from the January peak, which has caused some investor angst. Despite this nervousness, stock prices have quadrupled and the bull market has entered its 10th year after the March 2009 low (S&P 500: 666). Given this remarkable accomplishment, we can now look back and ask, “Did investors take advantage of this massive advance?” The short answer is “No.” For the most part, the fearful masses missed the decade-long, U.S. bull market. We know this dynamic to be true because data regarding stock ownership has gone down significantly, and hundreds of billions of dollars have been pulled from U.S. equity funds over the duration. For instance, Gallup, the survey and analytics company, annually polls the average percentage of Americans who own stocks and they found ownership has dropped from 62% of Americans in 2008 to 54% in 2017 (see chart below).

Much of the negativity that has dominated investor behavior over the last decade can be explained by important behavioral biases. As I describe in Controlling the Investment Lizard Brain, evolution created an almond-sized tissue in the prefrontal cortex of the brain (amygdala), which controls reasoning. Originally, the amygdala triggered the instinctual survival flight response for lizards to avoid hungry hawks and humans to flee ferocious lions. In today’s modern society, the probability of getting eaten by a lion is infinitesimal, so rather than fretting over a potential lion slaughtering, humans now worry about their finances getting eaten by financial crises, Federal Reserve interest rate hikes, and/or geopolitical risks.

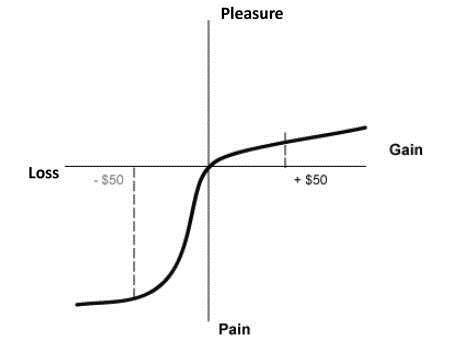

Even with the spectacular +300% appreciation in stock values from early 2009, academic research can help us understand how pessimism can outweigh optimism, even in the wake of a raging bull market. Consider the important risk aversion research conducted by Nobel Prize winner Daniel Kahneman and his partner Amos Tversky (see Pleasure/Pain Principle). Their research pointed out the pain of losses can be twice as painful as the pleasure experienced through gains (see diagram below).

Given this backdrop, how can these gargantuan gains be maintained (or improved upon) when investors are continually draining money out of riskier stocks and pouring cash into more conservative bonds? (see Fund Flows Paradox). There are several major factors that can explain the colossal gains in the face of a stock investor exodus:

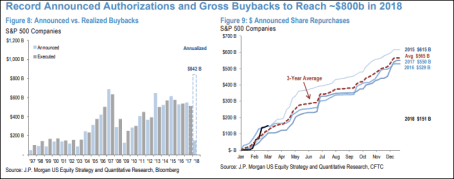

- Share Buybacks: While investors might not be buying loads of stocks, corporations have purchased trillions of dollars in stocks since the financial crisis. As you can see from the chart below, the table is set for 2018 to be a record year in share buybacks ($842 billion estimate), thanks to record profits and tax legislation that is making it cheaper for corporations to bring back foreign profits abroad.

Source: Marketwatch

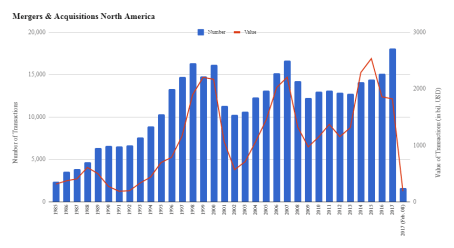

- Mergers & Acquisitions (M&A): Record profits, low interest rates, and high cash levels have led to trillions of dollars in U.S. M&A activity (almost $2 trillion in 2017) – see chart below. Not all of this was funded with cash and debt, but suffice it to say, enormous amounts of equity have been removed from the stock market.

Source: IMAA Institute

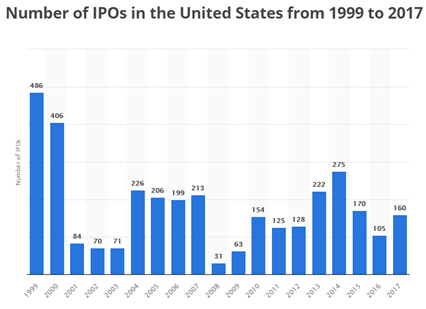

- Limited IPOs: Certainly, we have seen a few high-profile, stock deals hit the market in the form of initial public offerings (IPOs) over the last year. Some prominent IPOs over the last year, include Dropbox Inc. (DBX), Spotify Technology (SPOT), and Snap Inc. (SNAP), however this limited supply of new deals is a drop in the bucket. As you can see from the chart below, the number of IPOs is significantly below the 1999-2000 peak and the recent added supply pales in comparison to the latest supply-sucking share buybacks and acquisitions.

Source: Statista

Just as important as these supply related issues are to the stock market, demand related issues are important as well. While individual U.S. investors have been scarred by the 2008-2009 financial crisis, ultimately, over the long run, money does not care about behavioral biases. Money goes where it is treated best. Theoretically, the best treatment could be in U.S. stocks or U.S. bonds, or it could be in pork bellies or the Thai baht currency, among many other asset classes (e.g., real estate, commodities, venture capital, Bitcoin, etc.). Much like a trip to the grocery store, global money flows search for the best deals. If beef prices spike by +30% and chicken prices drop by -20%, guess what? Shoppers will now buy more chicken and less beef. Similarly, when Japanese 10-year bonds are yielding 0.04%, German 10-year bonds 0.56%, and U.K. 10-year bonds 1.42%, then U.S. 10-year Treasuries with a 2.96% yield don’t look so bad.

More importantly, as it relates to stock prices, there has been a mass divergence between the interest rate yields earned on Treasuries and the earnings yield (E/P or the inverse P/E ratio) since this 10-year bull market began (Ed Yardeni has a great chart of this Fed Valuation chart). Stocks, as they are valued today, are effectively providing double the yield of bonds (roughly a 6% yield vs 3% yield, respectively). As long as this phenomenon remains intact over the medium term, stocks could continue to significantly outperform bonds. Eventually a spike in stock prices and/or an earnings decline caused by a recession will lower the earnings yield on stocks, but until then, nervous investors will likely continue to underperform.

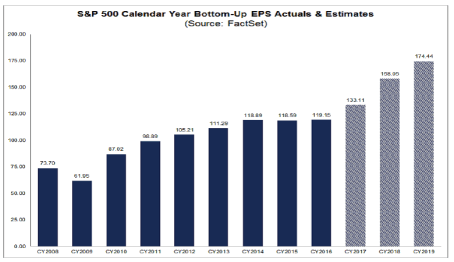

What the almost 10-year bull market teaches us is that our behavioral shortcomings can be a drag on performance and stock values, but the economic laws of supply and demand can play an even more significant role in the direction of the stock market. Learning how to control your lizard brain (amygdala), and understand how the pain of losses (risk aversion) can distort decision making processes can help you more clearly see how record profits (see chart below), share buybacks, M&A activity, and limited stock issuance (i.e. IPOs) will impact stock prices. Understanding these lessons will better prepare the masses in navigating through future bull and bear markets.

Source: FACTSET

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (May 1, 2018). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in DBX, SPOT, SNAP, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

M&A: Top or Bottom?

James Stewart at Smart Money recently wrote a piece attempting to debunk the consensus view, which holds the belief that increased mergers and acquisitions (M&A) activities is a leading indicator of positive market returns. There is no doubt, in the desert of positive news headlines, the bulls are searching for signs of an oasis to rescue them. Temporarily quenching the thirst of the bulls were $90 billion of proposed deals last week, including the hefty $40 billion hostile takeover offer of Potash Corp. (POT) by BHP Billiton Ltd. (BHP).

Is this uptick in deal announcements the sign of greener pastures, or is it what Stewart calls a “reverse indicator” of the market’s direction?

Stewart buttresses his argument by showing how record deal activity occurs at peaks of the market. For example, global M&A activity crested at $4.3 trillion in 2007, right before the market cratered in 2008. This peak can be compared to the previous trough of $1.3 trillion in M&A transactions in 2002, just as the economy was freshly recovering out of the recession. The trough to peak period for this M&A cycle lasted about five years (2002-2007), so I’m having a little trouble understanding how Stewart is claiming a peak is imminent after less than 1 year into the new M&A cycle (the recent M&A trough occurred in 2009 at $1.3 trillion)? Wouldn’t his analysis imply a gradual increase in deals until 2014? Well, for now, let’s just go with his rapid orgasm thesis and move onto his next points.

Stewart proceeds to rationalize the spate of new deal announcements with the following reasons:

- Higher Prices Perk Up Previously Reluctant Sellers: The general price rebound in the market from the nadir in March 2009 is one major contributing factor to why previously reluctant targets are now warming up to fresh overtures.

- Suitors More Comfortable: In 2009, buyers weren’t in the mood for paying top dollar for companies experiencing deteriorating fundamentals. Prices may be higher in 2010, but the Armageddon scenarios of early 2009 have momentarily been put on hold.

- Money Can’t Get Any Tighter: The cheap, loosey-goosy lending standards in the pre-2008 M&A golden era no longer exist, but conditions can’t get much worse than the log-jammed lending standards practiced in 2009.

The Real Reason for Deals Rising

Source: The Wall Street Journal

One word…cash. About $1.8 trillion of it is just piling up on the non-financial balance sheets of domestic companies (Financial Times). The tribes are getting restless with the obscene amounts of money earning 1% or less (read Steve Jobs: Gluttonous Hog article) and shareholders want to see more productive strategies applied to their capital. Frankly, I much prefer organic investment (e.g., R&D and marketing), share buybacks, and dividends over large destructive acquisitions any day. Just ask the executives at AOL/Time Warner, Mercedes Benz/Chrysler, and Sprint/Nextel how those large deals worked out for them. For some reason, many men like driving big macho trucks, just as many CEOs like controlling big companies.

One Reason to Buy and Many Reasons to Sell

I can’t disagree with James’s thesis that M&A markets get overheated near market tops, but I think there is a lot of room in deal announcements between the $90 billion in deals announced last week and the $4.3 trillion peak. I also agree that one good week of M&A announcements should not be extrapolated into eternity.

Worth noting as well, I believe there is a substantial difference in the financing market today versus the prior peak. In the BHP/Potash deal for example, BHP offered $40 billion in cash…not stock. BHP is putting its money where its mouth is, particularly its $18 billion in annual cash flow and its healthy balance sheet. Internal financing wasn’t the main priority in the mid-2000s, when companies (including private equity) were more cavalier with OPM (other people’s money), specifically with the endless pools of cheap bank financing.

Currently, companies have deep pockets, but very short arms, and as a result, companies have been very stingy with their capital. However, if we continue to see more internally financed cash deals, I will view that trend as a tremendously positive signal of longer-term fundamental confidence, a characteristic which was absent last year.

On the topic of insider buying, Peter Lynch pointed out “there is only one reason to buy and many reasons to sell” – the only real reason to purchase is the belief stock prices will move higher. Since the availability of cheap capital has been severely hampered, a wide swath of companies will have to rely on their own cash generation – not OPM. Since outside capital is scarce, the companies with cash flexibility will be more prudent in their M&A due diligence.

Overall, James Stewart may be right about the sustainability of M&A going into next year. However, in the short-run, as the gargantuan corporate cash piles get put to use through more M&A, and share buybacks, simple supply-demand economics indicate a shrinking equity base should bode well for market prices, all else equal. Uncertainty is available in large quantities right now, so time will tell if deal making will diminish into a market top, or gain momentum into a bull market. With all that cash sitting on the sidelines, my guess is we are closer to the trough of the M&A wave versus the top. If I’m wrong, don’t hold your breath for a Microsoft-Google (MSFT/GOOG) or Exxon-Chevron (XOM/CVX) merger anytime soon.

Read Full Smart Money M&A Article Here (Hat-Tip Josh Brown TRB)

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, GOOG, and AAPL, but at the time of publishing SCM had no direct position in BHP, POT, MSFT, XOM, CVX, AOL/Time Warner (TWX), Mercedes Benz/Chrysler, and Sprint/Nextel (S) or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}