Posts tagged ‘Japan’

Santa and the Rate-Hike Boogeyman

Boo! … Rates are about to go up. Or are they? We’re in the fourth decade of a declining interest rate environment (see Don’t be a Fool), but every time the Federal Reserve Chairman speaks or monetary policies are discussed, investors nervously look over their shoulder or under their bed for the “Rate Hike Boogeyman.” While this nail-biting mentality has resulted in lost sleep for many, this mindset has also unfortunately led to a horrible forecasting batting average for economists. Santa and many equity investors have ignored the rate noise and have been singing Ho Ho Ho as stock prices hover near record highs.

A recent Deutsche Bank report describes the prognostication challenges here:

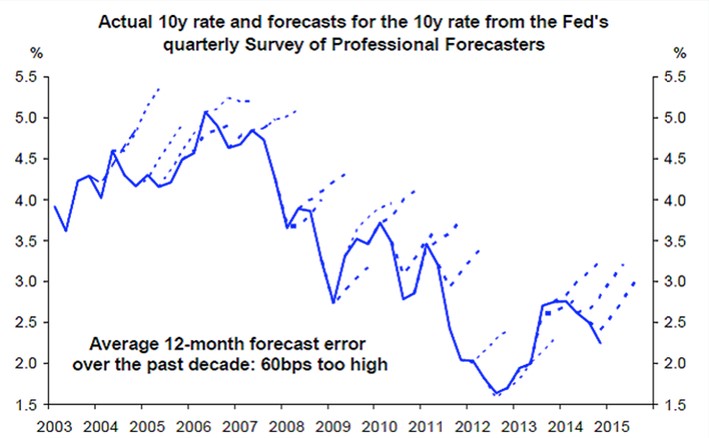

i.) For the last 10 years, professional forecasters have consistently been wrong on their predictions of rising interest rates.

Source: Deutsche Bank via Vox

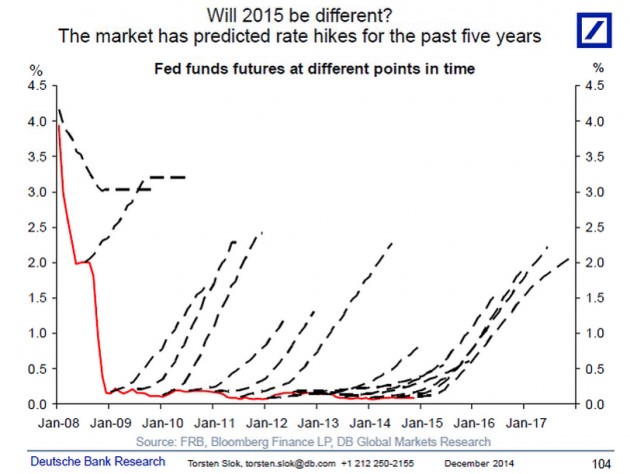

ii.) For the last five years, investors haven’t fared any better. As you can see, they too have been continually wrong about their expectations for rising interest rates.

Source: Deutsche Bank via Vox

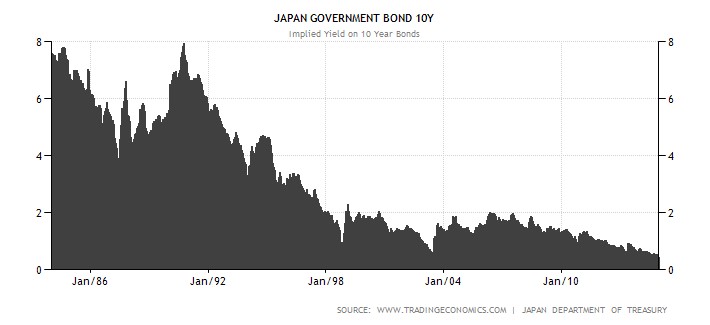

I’m the first to admit that rates have remained “lower for longer” than I guessed, but unlike many, I do not pretend to predict the exact timing of future rate increases. I strongly believe inevitable interest rate rises are not a matter of “if” but rather “when”. However, trying to forecast the timing of a rate increase can be a fool’s errand. Japan is a great case in point. If you take a look at the country’s interest rates on their long-term 10-year government bonds (see chart below), the yields have also been declining over the last quarter century. While the yield on the 10-Year U.S. Treasury Note is near all-time historic lows at 2.18%, that rate pales in comparison to the current 10-Year Japanese Bond which is yielding a minuscule 0.36%. While here in the states our long-term rates only briefly pierced below the 2% threshold, as you can see, Japanese rates have remained below 2% for a jaw-dropping duration of about 15 years.

Source: TradingEconomics.com

There are plenty of reasons to explain the differences in the economic situation of the U.S. and Japan (see Japan Lost Decades), but despite the loose monetary policies of global central banks, history has proven that interest rates and inflation can remain stubbornly low for longer than expected.

The current pundit thinking has Federal Reserve Chairwoman Yellen leading the brigade towards a rate hike during mid-calendar 2015. Even if the forecasters finally get the interest rate right for once, the end-outcome is not going to be catastrophic for equity markets. One need look no further than 1994 when Federal Reserve Chairman Greenspan increased the benchmark federal funds rate by a hefty +2.5%. (see 1994 Bond Repeat?). Rather than widespread financial carnage in the equity markets, the S&P 500 finished roughly flat in 1994 and resumed the decade-long bull market run in the following year.

Currently 15 of the 17 Fed policy makers see 2015 median short-term rates settling at 1.125% from the current level of 0-0.25%. This hardly qualifies as interest rate Armageddon. With a highly transparent and dovish Janet Yellen at the helm, I feel perfectly comfortable the markets can digest the inevitable Fed rate hikes. Will (could) there be volatility around changes in Fed monetary policy during 2015? Certainly – no different than we experienced during the “taper tantrum” response to Chairman Ben Bernanke’s rate rise threats in 2013 (see Fed Fatigue).

As 2014 comes to an end, Santa has wrapped investor portfolios with a generous bow of returns in the fifth year of this historic bull market. Not everyone, however, has been on Santa’s “nice” list. Regrettably, many sideliners have received no presents because they incorrectly assessed the elimination impact of Quantitative Easing (QE). If you prefer presents over a lump of coal in your stocking, it will be in your best interest to ignore the Rate Hike Boogeyman and jump on Santa’s sleigh.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own a range of positions, including certain exchange traded fund positions, but at the time of publishing SCM had no direct position in DB or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

U.S. Small-Caps Become Global Big Dog

With the emerging market currencies and financial markets under attack; Japan’s Nikkei index collapsing in the last three weeks; and the Federal Reserve hinting about its disciplinarian tapering of $85 billion in monthly QE3 bond purchases, one would expect higher beta small cap stocks to get hammered in this type of environment.

Before benchmarking results in the U.S., let’s take a closer look at some of the international carnage occurring from this year’s index value highs:

- Japan: -19% (Nikkei 225 index)

- Brazil: -22% (IBOVESPA index)

- Hong Kong: -12% (Hang Seng index)

- Russia: -19% (MICEX/RTS indexes)

Not a pretty picture. Given this international turmoil and the approximately -60% disintegration in U.S. small-cap stock prices during the 2007-2009 financial crisis, surely these economically sensitive stocks must be getting pummeled in this environment? Well…not necessarily.

Putting the previously mentioned scary aspects aside, let’s not forget the higher taxes, Sequestration, and ObamaCare, which some are screaming will push us off a ledge into recession. Despite these headwinds, U.S. small-caps have become the top dog in global equity markets. Since the March 2009 lows, the S&P 600 SmallCap index has more than tripled in value ( about +204%, excluding dividends), handily beating the S&P 500 index, which has advanced a respectable +144% over a similar timeframe. Even during the recent micro three-week pullback/digestion phase, small cap stocks have retreated -2.8% from all-time record highs (S&P 600 index). Presumably higher dividend, stable, globally-diversified, large-cap stocks would hold up better than their miniature small-cap brethren, but that simply has not been the case. The S&P 500 index has underperformed the S&P 600 by about -80 basis points during this limited period.

How can this be the case when currencies and markets around the world are under assault? Attempting to explain short-term moves in any market environment is a hazardous endeavor, but that has never slowed me down in trying. I believe these are some of the contributing factors:

1) No Recession. There is no imminent recession coming to the U.S. As the saying goes, we hear about 10 separate recessions before actually experiencing an actual recession. The employment picture continues to slowly improve, and the housing market is providing a slight tailwind to offset some the previously mentioned negatives. If you want to fill that half-full glass higher, you could even read the small-cap price action as a leading indicator for a pending acceleration in a U.S. cyclical recovery.

2) Less International. The United States is a better house in a shaky global neighborhood (see previous Investing Caffeine article), and although small cap companies are expanding abroad, their exposure to international markets is less than their large-cap relatives. Global investors are looking for a haven, and U.S. small cap companies are providing that service now.

3) Inflation Fears. Anxiety over inflation never seems to die, and with the recent +60 basis point rise in 10-year Treasury yields, these fears appear to have only intensified. Small-cap stocks cycle in and out of favor just like any other investment category, so if you dig into your memory banks, or pull out a history book, you will realize that small-cap stocks significantly outperformed large-caps during the inflationary period of the 1970s – while the major indexes effectively went nowhere over that decade. Small-cap outperformance may simply be a function of investors getting in front of this potential inflationary trend.

Following the major indexes like the Dow Jones Industrials index and reading the lead news headlines are entertaining activities. However, if you want to become a big dog in the investing world and not get dog-piled upon, then digging into the underlying trends and market leadership dynamics of the market indexes is an important exercise.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) including emerging market ETFs, IJR, and EWZ, but at the time of publishing, SCM had no direct position in Hong Kong ETFs, Japanese ETFs, Russian ETFs, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

No Free Lunch, No Free Sushi

Everybody loves a free lunch, myself included, and many in Japan would like free sushi too. Despite the short term boost in Japanese exports and Nikkei stock prices, there are no long-term free lunches (or free sushi) when it comes to global financial markets. Following in the footsteps of the U.S. Federal Reserve, the Bank of Japan (BOJ) has embarked on an ambitious plan of doubling its monetary base in two years and increasing inflation to a 2% annual rate – a feat that has not been achieved in more than two decades. By the BOJ’s estimate, it will take a $1.4 trillion injection into economy to achieve this goal by the end of 2014.

Lunch is tasty right now, as evidenced by a tasty appetizer of +3.5 % Japanese first quarter GDP and this year’s +46% spike in the value of the Nikkei. Japan is hopeful that its mix of monetary, fiscal, and structural policies will spur demand and increase the appetite for Japanese exports, however, we know fresh sushi can turn stale quickly.

Quantitative easing (QE) and monetary stimulus from central banks around the globe have been hailed as a panacea for sluggish global growth – most recently in Japan. Commentators often oversimplify the benefits of money printing without acknowledging the pitfalls. Basic economics and the laws of supply & demand eventually prevail no matter the fiscal or monetary policy implemented. Nonetheless, there can be temporary disconnects between current equity prices and exchange rates, before underlying fundamentals ultimately drive true intrinsic values.

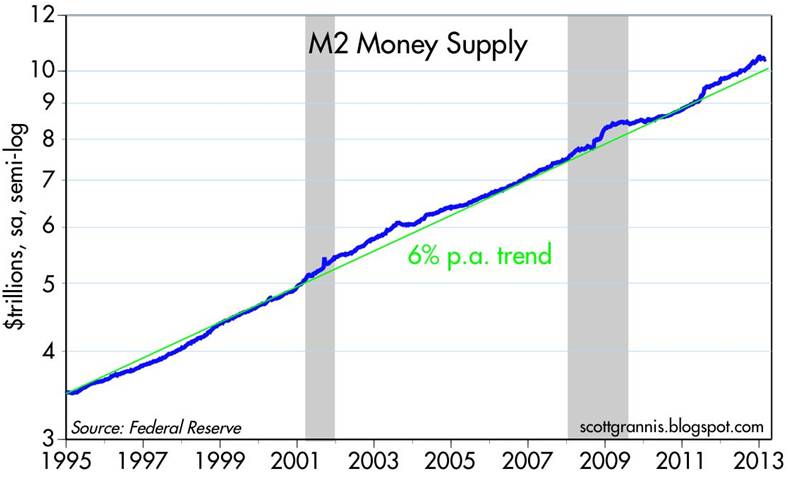

Impassioned critics of the Federal Reserve and its Chairman Ben Bernanke would have you believe the money supply is exploding, and hyperinflation is just around the corner. It’s difficult to quarrel with the trillions of dollars created by the Fed’s printing presses via QE1/QE2/QE3, but the fact remains that money supply growth has continued at a steady growth rate – not exploding (see Calafia Beach Pundit chart below).

Source: Calafia Beach Pundit

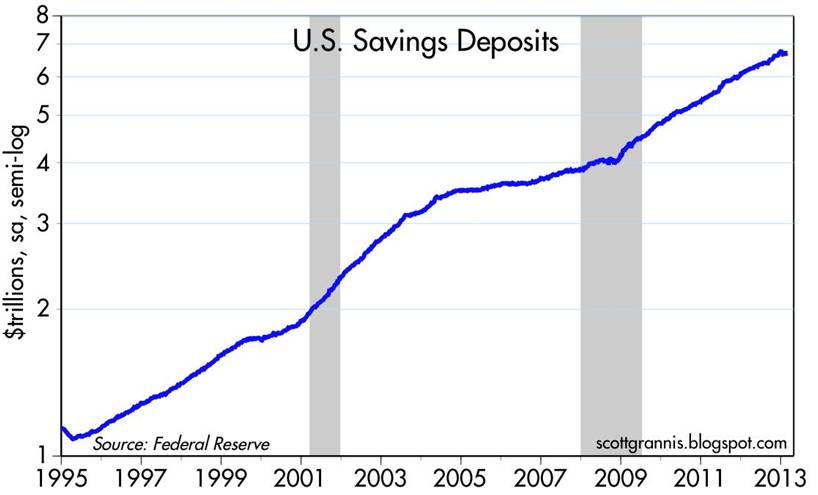

Why no explosion in the money supply? Simply, the trillions of dollars printed by the Fed have sat idly in bank vaults as reserves. Once nervous consumers stop hoarding trillions in cash held in savings deposit accounts (see chart below) and banks begin lending at a healthier clip, then money supply growth will accelerate. By definition, money supply growth in excess of demand for goods and services (i.e., GDP) is the main cause of inflation.

Source: Calafia Beach Pundit

Although inflationary pressure has not reared its ugly head yet, there are plenty of precursors indicating inflation may be on its way. The unemployment rate continues to tick downwards (7.5% in Aril) and the much anticipating housing recovery is gaining steam. Inflationary fear has manifested itself in part through the heightened number of conversations surrounding the Fed “tapering” its $85 billion per month bond purchasing program.

We’ve enjoyed a sustained period of low price level growth, however the Goldilocks period of little-to-no inflation cannot last forever. The differences between current prices and true value can exist for years, and as a result there are many different strategies attempted to capture profits. Like the gambling masses frequenting casinos, speculators can beat the odds in the short-run, but the house always wins in the long-run – hence the ever-increasing size and number of casinos. While a small number of professionals understand how to shift the unbalanced odds into their favor, most lose their shirt. On Wall Street, that is certainly the case. Studies show speculating day traders persistently lose about 80% of the time. Long-term investors are uniquely positioned to exploit these value disparities, if they have a disciplined process with the ability to patiently value assets.

Even though the Japanese economy and stock market have rebounded handsomely in the short-run, there is never a free lunch over the long-term. Unchecked policies of money printing, deficits, and debt expansion won’t lead to boundless prosperity. Eventually a spate of irresponsible actions will result in inflation, defaults, recessions, and/or higher unemployment rates. Unsustainable monetary and fiscal stimulus may lead to a tasty free lunch now, but if investors overstay their welcome, the sushi may turn bad and the speculators will be left paying the hefty tab.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Sidoxia Debuts Video & Goes to the Movies

Article is an excerpt from previously released Sidoxia Capital Management’s complementary February 1, 2013 newsletter. Subscribe on right side of page.

The red carpet was rolled out for the stock market in January with the Dow Jones Industrial Average rising +5.8% and the S&P 500 index up an equally impressive +5.0% (a little higher rate than the 0.0001% being earned in bank accounts). Movie stars are also strutting their stuff down the red carpet this time of the year as they collect shiny statues at ritzy award shows like the Golden Globes and Oscars. Given the vast volumes of honors bestowed, we thought what better time to put on our tuxes and create our own 2013 nominations for the economy and financial markets. If you are unhappy with our selections, you are welcome to cast your own votes in the comments section below.

By award category, here are Sidoxia’s 2013 selections:

Best Drama (Government Shutdown & Debt Ceiling): Washington D.C. has provided no shortage of drama, and the upcoming blockbusters of Shutdown & Debt Ceiling are worthy of its Best Drama nomination. If Congressional Democrats and Republicans don’t vote in favor of a new “Continuing Resolution” by March 27th, then our United States government will come to a grinding halt. At issue is Republican’s desire for additional government spending cuts to lower our deficit, which is likely to exceed $1 trillion for the fifth consecutive year. If you like more heart pumping drama, the Senate has just passed a Debt Ceiling extension through May 18th…mark those calendars!

Best Horror Film (Sequestration): Most people have already seen the scary prequel, The Fiscal Cliff, but the sequel Sequestration deserves the horror film honors of 2013. This upcoming blood-filled movie about broad, automatic, across-the-board government cost cuts will make any casual movie-watcher scream in terror. The $1.2 trillion in spending cuts (over 10 years) are so gory, many viewers may voluntarily leave the theater early. If you are waiting for the release, Sequestration is coming to a theater near you on March 1st, unless Congress, in an unlikely scenario, cancels the launch.

Best Director (Ben Bernanke): Federal Reserve Chairman Ben Bernanke’s film, entitled, The U.S. Economy, had a massive budget of about $16 trillion dollars, based on estimates of last year’s GDP (Gross Domestic Product). Nevertheless, Bernanke managed to do whatever it took (including trillions of dollars in bond buying) to prevent the economic movie studio from collapsing into bankruptcy. While many movie-goers were critical of his directorial debut, inflation has remained subdued thus far, and he has promised to continue his stimulative monetary policies (i.e., keep interest rates low) until the national unemployment rate falls below 6.5% or inflation rises above 2.5%.

Best Foreign Film (China): Americans are not the only people who produce movies globally. A certain country with a population of nearly 1.4 billion people also makes movies too…China. In the most recently completed 4th quarter, China’s economy experienced blockbuster growth in the form of +7.9% GDP expansion. This was the fastest pace achieved by China in two whole years. To put this metric into perspective, compare China’s heroic growth to the bomb created by the U.S. economy, which registered a disappointing -0.1% contraction at the economic box office. China’s popularity should bring in business all around the globe.

Best Special Effects (Japan): After coming out with a series of continuous flops, Japan recently launched some fresh new special effects in the form of a $116 billion emergency stimulus package. The country also has plans to superficially enhance the visual portrayal of its economy by implementing its own faux money-printing program modeled after our country’s quantitative easing actions (i.e., the Federal Reserve stimulus). As a result of these initiatives, the Japanese Nikkei index – their equivalent of our Dow Jones Industrial index – has risen by +29% in less than 3 months to a level of 11,138.66 (click here for chart). But don’t get too excited. This same Nikkei index peaked at 38,957 in 1989, a far cry from its current level.

Best Action Film (Icahn vs. Ackman): This surprisingly entertaining action film features a senile 76-year-old corporate raider and a white-haired, 46-year-old Harvard grad. The investment foes I am referring to are the elder Carl Icahn, Chairman of Icahn Enterprises, and junior Bill Ackman, CEO of Pershing Square Capital Management. In addition to terms such as crybaby, loser, and liar, the 27-minute verbal spat (view more here) between Icahn (his net worth equal to about $15 billion) and Ackman (net worth approaching $1 billion) includes some NC-17 profanity. The clash of these investment titans stems from a decade-old lawsuit, in addition to a recent disagreement over a controversial short position in Herbalife Ltd. (HLF), a nutritional multi-level marketing firm.

Best Documentary (Europe): As with a lot of reality-based films, many don’t receive a lot of attention. So too has been the commentary regarding the eurozone, which has been relatively peaceful compared to last spring. Despite the comparative media silence, European unemployment reached a new high of 11.8% late last year. This European documentary is not one you should ignore. European Central Bank (ECB) President Mario Draghi just stated, “The risks surrounding the outlook for the euro area remain on the downside.”

Best Original Song (National Anthem): We won’t read anything politically into Beyonce’s lip-synced rendition of The Star-Spangled Banner at the presidential inauguration, but she is still worthy of the Sidoxia nomination because music we hear in the movies is also recorded. I’m certain her rapping husband Jay-Z agrees whole-heartedly with this viewpoint.

Best Motion Picture (Sidoxia Video): It may only be three minutes long, but as my grandmother told me, “Great things come in small packages.” I may be a little biased, but judge for yourself by watching Sidoxia’s Oscar-worthy motion picture debut:

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in HLF, Japanese ETFs, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Equity Quicksand or Bond Cliff?

The markets are rigged, the Knight Capital Group (KCG) robots are going wild, and the cheating bankers are manipulating Libor. I guess you might as well pack it in…right? Well, maybe not. While mayhem continues, equity markets stubbornly grind higher. As we stand here today, the S&P 500 is up approximately +12% in 2012 and the NASDAQ market index has gained about +16%? Not bad when you consider 15 countries are offering negative yields on their bonds…that’s right, investors are paying to lose money by holding pieces of paper until maturity. As crazy as buying technology companies in the late 1990s for 100x’s or 200x’s earnings sounds today, just think how absurd negative yields will sound a decade from now? For heaven’s sake, buying a gun and stuffing money under the mattress is a cheaper savings proposition.

Priced In, Or Not Priced In, That is the Question?

So how can stocks be up in double digit percentage terms when we face an uncertain U.S. presidential election, a fiscal cliff, unsustainable borrowing costs in Spain, and S&P 500 earnings forecasts that are sinking like a buried hiker in quicksand (see chart below)?

I guess the answer to this question really depends on whether you believe all the negative news announced thus far is already priced into the stock market’s below average price-earnings (P/E) ratio of about 12x’s 2013 earnings. Or as investor Bill Miller so aptly puts it, “The question is not whether there are problems. There are always problems. The question is whether those problems are already fully discounted or not.”

Source: Crossing Wall Street

While investors skeptically debate how much bad news is already priced into stock prices, as evidenced by Bill Gross’s provocative “The Cult of Equity is Dying” article, you hear a lot less about the nosebleed prices of bonds. It’s fairly evident, at least to me, that we are quickly approaching the bond cliff. Is it possible that we can be entering a multi-decade, near-zero, Japan-like scenario? Sure, it’s possible, and I can’t refute the possibility of this extreme bear argument. However with global printing presses and monetary stimulus programs moving full steam ahead, I find it hard to believe that inflation will not eventually rear its ugly head.

Again, if playing the odds is the name of the game, then I think equities will be a better inflation hedge than most bonds. Certainly, not all retirees and 1%-ers should go hog-wild on equities, but the bond binging over the last four years has been incredible (see bond fund flows).

While we may sink a little lower into the equity quicksand while the European financial saga continues, and trader sentiment gains complacency (Volatility Index around 15), I’ll choose this fate over the inevitable bond cliff.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in KCG or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

2011: Beating Batter into Flat Pancake

As it turns out, 2011 can be characterized as the year of the pancake…the flat pancake. While the Dow Jones Industrial Average (Dow) rose about 6% this year (its third consecutive annual gain), the S&P 500 ended the year flat at 1257.6 (-0.003%), the smallest yearly move in more than four decades. Along the way in 2011, there was plenty of violent beating and whipping of the lumpy pancake batter before the flat cake was cooked for the year. With respect to the financial markets, the 2011 lumps came in the form of various unsavory events:

* Never-Ending Eurozone Financial Saga: After Ireland and Portugal sought bailouts, Greece added its negligent financial storyline to the financial soap opera. Whether European government leaders can manage out-of-control deficits and debt loads will determine if Greece and other peripheral countries will topple larger countries like Italy and Spain.

* Credit Rating Downgrade: Standard & Poor’s, the highest profile credit rating agency, downgraded the U.S.’s long-term debt rating to AA+ from AAA due to high debt levels and Congressional legislators inability to hammer out a deficit-reduction plan during the debt ceiling negotiations.

* Japanese Earthquake and Tsunami: Japan and the global economy were rocked by a magnitude 9.0 earthquake and tsunami on March 11, 2011, which resulted in 15,844 people dead and 3,451 people missing. The ripple effects are still being felt through large industries like the automobile and electronics industries.

* Arab Spring Protests: Protesters throughout the Middle East and North Africa provided additional uncertainty to the global political map as demonstrators demanded regime change and more political freedoms. In the long-run, removing oppressive leaders like Hosni Mubarak (Egypt’s leader for 30 years), Muammar Gadaffi (Libya’s leader for 42 years), and Zine al-Abidine Ben Ali (Tunisia’s president for 23 years) should be beneficial for global stability, but in the short-run, how the new leadership vacuum will be filled remains ambiguous.

* Occupy Movement Voices Disapproval: The Occupy Wall Street movement began on September 17, 2011 in Liberty Square in Manhattan’s Financial District, and spread to over 100 cities in the U.S. There has not been a cohesive articulated agenda, but a common thread underlying all the Occupy movements is a sense that 99% of the population is being treated unfairly due to a flawed corrupt system controlled by Wall Street that is feeding the richest 1%.

All these lumps experienced in 2011 were not settling to investors’ stomachs. As a result individuals continued the trend of piling into bonds, in hopes of soothing their investment tummies. Long-term Treasury prices spiked upwards in 2011 (+29% as measured by TLT Treasury ETF) and soaring 10-year Treasury note prices pushed yields (1.87%) below yields on S&P 500 equities (2.1%). Despite a more than 3,400 point increase in the Dow (+39%) since the end of 2008, investors have still poured $774 billion into bonds versus $33 billion yanked from equities, according to EPFR Global. Over-weighting bonds makes sense for some, including retirees on fixed budgets, but many investors should brace for an inevitable reversal in bond prices. Eventually, the sweet taste of safety achieved from bond appreciation will turn to heartburn, once interest rates reverse their 30 year trend of declines.

Syrupy Factors Help Sweeten Pancakes

Although the aforementioned factors lead to historically high volatility and flat flavors in 2011, there are also some countering sweet reasons that make equities look more palatable for 2012. Here are some of the factors:

* Record Corporate Profits: Even with the constant barrage of fear, uncertainty, and doubt distributed via the media channels, corporations posted record profits in 2011, with an estimated increase of +16% over last year (and another forecasted +10% rise in 2012 – Source: S&P).

* Historic Levels of Cash: Record profits mean record cash, and all those riches have been piling up on non-financial corporate balance sheets at historic levels. At the beginning of Q4 the figure stood at $2.12 trillion. Companies have generally been stingy, but as the recovery progresses, they have increasingly been spending on technology, equipment, international expansion, and even the beginnings of hiring.

* Interest Rates at 60 Year Lows: Interest rates are at record lows and home affordability has never been better with 30-year fixed rate mortgages hovering below 4%. Housing may not come screaming back, but the foundation for a recovery is being laid.

* Improving Economic Variables: Whether you’re looking at broader economic activity (Gross Domestic Product up for nine consecutive quarters); employment growth (declining unemployment rate and 21 consecutive months of private job creation), or consumer spending (consumer confidence approaching multi-year highs), all major signs are currently pointing to an improving outlook.

* Near Record Exports: While the U.S. dollar has made some recent gains against foreign currencies because of the financial crisis in Europe, the relative value of the dollar remains historically low versus the major global currencies. The longer-term depreciation of the dollar has buoyed exports of U.S. goods to near record levels despite the global uncertainty.

* Unprecedented Central Bank Support Globally: Ben Bernanke and the U.S. Federal Reserve is committed to keeping exceptionally low levels of lending interest rates at least through mid-2013, while also implementing “Operation Twist” and potential further quantitative easing (QE3). Translation: Ben Bernanke is going to do everything in his power to keep interest rates low in order to stimulate economic growth. The European Central Bank (ECB) has pulled out its lending fire trucks too, with an unparalleled three-year lending program to extinguish liquidity fires in the European banking sector.

* Improving Mergers & Acquisitions Environment: We may not be back to the 2006 buyout “hay-days,” but U.S. mergers and acquisitions activity increased +24% in 2011. What’s more, high profile potential IPOs like an estimated $100 billion Facebook offering may help kick-start the new equity issuance market in 2012.

* Tasty Fat Dividends: Rarely have S&P 500 dividend yields (currently 2.1%) outpaced the interest rates earned on 10-year Treasury note yields, but now happens to be one of those times. Typically S&P 500 stock dividends have averaged about 40% of the yield on 10-year Treasury notes, and now it is 112%. In Q3 of 2011, dividend increases rose +17% and expectations are for nearly a +11% increase in 2012, said Howard Silverblatt, senior index analyst at S&P.

Any way you cut it (or beat the batter), 2011 was a volatile year. And despite all the fear, uncertainty, and doubt, profits continue to grow and sovereign nations are being forced to deal with their fiscal problems. Unforeseen risks always exist, but if Europe can contain its financial crisis and the U.S. recovery can continue into this new election year, then opportunities in the 2012 attractively priced equity markets should sweeten the flat equity pancake we ate in 2011.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, including a short position in TLT, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Nuclear Knee-Jerk Reaction

It’s amazing how quickly the long-term secular growth winds can reverse themselves. Just a week ago, nuclear energy was thought of as a safe, clean, green technology that would assist the gasoline pump pain in our wallets and purses. Now, given the events occurring in Japan, “nuclear” has become a dirty word equated to a life-threatening game of Russian roulette.

Despite the spotty information filtering in from the Dai-Ichi plant in Japan, we are already absorbing knee-jerk responses out of industrial heavyweight countries like Germany and China. Germany has temporarily closed seven nuclear power centers generating about a quarter of its nuclear capacity, and China has instituted a moratorium on all new facilities being built. How big a deal is this? Well, China is one country, and it alone currently accounts for 44% of the 62 global nuclear reactor projects presently under construction (see chart below).

Source: World Nuclear Association (URRE Presentation)

As a result of the damaged Fukushima reactors, coupled with various governmental announcements around the globe, Uranium prices have dropped a whopping -30% within a month – plunging from about $70 per pound to around $50 per pound today.

Where does U.S. Nuclear Go from Here?

As you can see from the chart below, the U.S. is the largest producer of nuclear energy in the world, but since our small population is such power hogs, this relatively large nuclear capability only accounts for roughly 20% of our country’s total electricity needs. France, on the other hand, manages about half the reactors as we do, but the French derive a whopping 75% of their total electricity needs from nuclear power. According to the Nuclear Energy Institute, Japanese reliance on nuclear power falls somewhere in between – 29% of their electricity demand is filled by nuclear energy. Like Japan, the U.S. imports most of its energy needs, so if nuclear development slows, guess what, other resources will need to make up the difference. OPEC and various other oil-rich, dictators in the Middle East are licking their chops over the future prospects for oil prices, if a cost-effective alternative like nuclear ends up getting kicked to the curb.

Source: The Economist

As I alluded to above, there is, however, a silver lining. As long as oil prices remain elevated, any void created by a knee-jerk nuclear backlash will only create heightened demand for alternative energy sources, including natural gas, solar, wind, biomass, clean coal, and other creative substitutes. While we Americans may be addicted to oil, we also are inventive, greedy capitalists that will continually look for more cost-efficient alternatives to solve our energy problems (see also Electrifying Profits). Unlike other countries around the world, it looks like the private sector will have to do the heavy lifting to solve these resources on their own dime. Limited subsidies have been introduced, but overall our government has lacked a cohesive energy plan to kick-start some of these innovative energy alternatives.

Déjà Vu All Over Again

We saw what happened on our soil in March 1979 when the Three Mile Island nuclear accident in Pennsylvania consumed the hearts and minds of the country. Pure unadulterated panic set in and new nuclear production ground to a virtual halt. When the subsequent Chernobyl incident happened in April 1986 insult was added to injury. As you can see from the chart below, nuclear reactor capacity has plateaued for some twenty years now.

Source: Wikipedia

The driving force behind the plateauing nuclear facilities is the NIMBY (Not In My Back Yard) phenomenon. The Three Mile Island incident is still fresh in people’s minds, which explains why only one nuclear plant is currently under construction in our country, on top of a base of 104 U.S. reactors in 31 states. I point this out as an ambivalent NIMBY-er since I work 30 miles away from one of the riskiest, 30-year-old nuclear plants in the country (San Onofre).

Unintended Consequences

The Sendai disaster is home to the worst Japanese earthquake in 140 years, by some estimates, but history will prove once again what unintended consequences can occur when impulsive knee-jerk decisions are made. Just consider what has happened to oil prices since the moratorium on offshore drilling (post-BP disaster) was instituted. Sure we have witnessed a dictator or two topple in the Middle East, and there currently is adequate supply to meet demand, but I would make the case that we should be increasing domestic oil supplies (along with alternative energy sources), not decreasing supplies because it is politically safe.

Time will tell if the Japanese earthquake/tsunami-induced nuclear disaster will create additional unintended consequences, but I am hopeful the recent events will at a minimum create a serious dialogue about a comprehensive energy policy. If the comfortable, knee-jerk reaction of significantly diminishing nuclear production is broadly adopted around the world, then an urgent alternative supply response needs to occur. Otherwise, you may just need to enjoy that bike ride to work in the morning, along with that nice, romantic candle-lit dinner at night.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and alternative energy securities, but at the time of publishing SCM had no direct position in BP, URRE, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Dealing Currency Drug to Export Addicts

Source: Photobucket

With the first phase of the post-financial crisis global economic bounce largely behind us, growth is becoming scarcer and countries are becoming more desperate – especially in developed countries with challenged exports and high unemployment. The United States, like other expansion challenged countries, fits this bill and is doing everything in its power to stem the tide by blasting foreigners’ currency policies in hopes of stimulating exports.

Political Hot Potato

The global race to devalue currencies in many ways is like a drug addict doing whatever it can to gain a short-term high. Sadly, the euphoric short-term benefit form lower exchange rates will be fleeting. Regardless, Ben Bernanke, the Chairman of the Federal Reserve, has openly indicated his willingness to become the economy’s drug dealer and “provide additional accommodation” in the form of quantitative easing part two (QE2).

Unfortunately, there is no long-term free lunch in global economics. The consequences of manipulating (depressing) exchange rates can lead to short-term artificial export growth, but eventually results convert to unwanted inflation. China too is like a crack dealer selling cheap imports as a drug to addicted buyers all over the world – ourselves included. We all love the $2.99 t-shirts and $5.99 toys made in China that we purchase at Wal-Mart (WMT), but don’t consciously realize the indirect cost of these cheap goods – primarily the export of manufacturing jobs overseas.

Global Political Pressure Cooker

Congressional mid-term elections are a mere few weeks away, but a sluggish global economic recovery is creating a global political pressure cooker. While domestic politicians worry about whining voters screaming about unemployment and lack of job availability, politicians in China still worry about social unrest developing from a billion job-starved rural farmers and citizens. The Tiananmen Square protests of 1989 are still fresh in the minds of Chinese officials and the government is doing everything in its power to keep the restless natives content. In fact, Premier Wen Jiabao believes a free-floating U.S.-China currency exchange rate would “bring disaster to China and the world.”

While China continues to enjoy near double-digit percentage economic growth, other global players are not sitting idly. Like every country, others would also like to crank out exports and fill their factories with workers as well.

The latest high profile devaluation effort has come from Japan. The Japanese Prime Minister post has become a non-stop revolving door and their central bank has become desperate, like ours, by nudging its target interest rate to zero. In addition, the Japanese have been aggressively selling currency in the open market in hopes of lowering the value of the Yen. Japan hasn’t stopped there. The Bank of Japan recently announced a plan to pump the equivalent of approximately $60 billion into the economy by buying not only government bonds but also short-term debt and securitized loans from banks and corporations.

Europe is not sitting around sucking its thumb either. The ECB (European Central Bank) is scooping up some of the toxic bonds from its most debt-laden member countries. Stay tuned for future initiatives if European growth doesn’t progress as optimistically planned.

Dealing with Angry Parents

When it comes to the United States, the Obama administration campaigned on “change,” and the near 10% unemployment rate wasn’t the type of change many voters were hoping for. The Federal Reserve is supposed to be “independent,” but the institution does not live in a vacuum. The Fed in many ways is like a grown adult living away from home, but regrettably Bernanke and the Fed periodically get called by into Congress (the parents) to receive a verbal scolding for not following a policy loose enough to create jobs. Technically the Fed is supposed to be living on its own, able to maintain its independence, but sadly a constant barrage of political criticism has leaked into the Fed’s decision making process and Bernanke appears to be willing to entertain any extreme monetary measure regardless of the potential negative impact on long-term price stability.

Just over the last four months, as the dollar index has weakened over 10%, we have witnessed the CRB Index (commodities proxy) increase over 10% and crude oil increase about 10% too.

In the end, artificially manipulating currencies in hopes of raising economic activity may result in a short-term adrenaline boost in export orders, but lasting benefits will not be felt because printing money will not ultimately create jobs. Any successful devaluation in currency rates will eventually be offset by price changes (inflation). Finance ministers and central bankers from 187 countries all over the world are now meeting in Washington at the annual International Monetary Fund (IMF) meeting. We all want to witness a sustained, coordinated global economic recovery, but a never-ending, unanimous quest for devaluation nirvana will only lead to export addicts ruining the party for everyone.

See also Arbitrage Vigilantes

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and WMT, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Unemployment Hypochondria

Average investors feel ill from the 2008-2009 financial mess, and like hypochondriacs they can only find fleeting reassurances by reviewing endless amounts of unemployment data. Volatile monthly data is not sufficient, so even more erratic weekly jobless claims data are relied upon. Why just stop there? With this insatiable appetite for unemployment rate data right now, people can’t get enough, so I am not only petitioning for the release of a daily jobs report, but also an hourly one.

Jobs data are relatively straightforward and simple for most Americans to understand. However, most people have more difficulty connecting with economic acronyms and data points such as GDP, PPI, CPI, industrial production, Philly Fed, capacity utilization, Conference Board LEI, durable goods, factory orders, energy inventories, trade balance, unit labor costs, and other economic figures.

Normal Progression

What’s the big deal surrounding the infatuation with myopic unemployment data? We have these things called “recessions” about twice every decade, and of the last 11 post-WWII recessions we have had 11 recoveries – not a bad batting percentage. Obviously, unemployment is a big deal if you are one of the 15 million or so people with no job, but as Jim Paulsen, Chief Investment Strategist at Wells Capital Management points out in his August Economic and Market Perspective, this current recovery is progressing at the fastest pace of any recovery over the last 25 years, and yes, jobs are being added (albeit slower than hoped).

“The consensus perception that this recovery is the ‘worst ever’ and consequently extremely vulnerable to a potential double-dip recession is overblown…Even if this recovery is weak compared to older postwar norms, it is still stronger than any other recovery in the last 25 years,” states Mr. Paulsen.

As you can see from Paulsen’s table below, our current recovery is not as brisk as the recoveries in the pre-1983 era, but he chalks up this trend to subpar growth in the United States’ labor force.

Source: James Paulsen, Wells Capital Management

Paulsen identified this dampened worker growth since the mid-1980s. He doesn’t attribute moderate growth to the “New Normal,” as described by PIMCO pals Bill Gross and Mohamed El-Erian (see also New Normal is Old Normal), but rather ascribes the phenomenon to a continuing trend. Paulsen adds:

“Whatever is causing the ‘new-normal’ economy has been doing it for the last 25 years. The ‘new normal’ is actually kind of old—at least a quarter century old.”

If you think about it, what businesses carried out over the last two years is clearly consistent with a normal economic recovery:

1) Businesses fired employees swiftly amid great uncertainty.

2) Businesses cut expenses, especially discretionary ones, and now profits and cash are piling up.

3) Businesses are buying more capital equipment. Spending is up +12% (to ~$1.3 trillion) from early 2009 according to Joe Lavorgna, an economist at Deutsche Bank.

4) Business acquisitions are beginning to heat up. Witness BHP Billiton’s (BHP) bid for Potash Corp (POT), and HP’s (HPQ) bid for 3Par (PAR) as examples (read HP’s Winner’s Curse).

5) Businesses are paying larger dividends and buying back more of their own stock.

All these actions are very reasonable given the continued uncertain economic environment and rapidly building cash war chests. Buying back stock, doing acquisitions, and prudently spending on cost saving equipment are, generally speaking, accretive measures for a company’s profit and loss statement. On the other hand, hiring employees is usually a lagging indicator of economic expansion and acts as diluting profit forces – at least in the short-run until workers become more productive. Eventually cash and/or business confidence will rise enough to push human resource departments over the fence to begin hiring again.

The weekly unemployment claims chart shows how rapidly improvement has been achieved over the last few decades, even though the improvement has stalled at a lofty level.

Source: ScottGrannis.Blogspot.com (8/13/10).

Japan Case Study: Demographic Double Edged Sword

Be careful what you wish for. Low unemployment is not the end-all, be-all of the world we live in. Take Japan for example. From 1953 until 2010, Japan’s unemployment rate averaged about 2.6%. The last reported rate registered 5.2% in July, double Japan’s average, but almost half of the U.S.’s current 9.6% rate.

Why does Japan have lower unemployment? There are numerous reasons cited – everything from over-employment in the agriculture sector to uncounted married women and protective conglomerates to better disincentives in unemployment insurance program. Overshadowing these reasons is the unmistakable aging of the Japanese population. The National Institute of Population and Social Security Research predicts the Japanese population will fall 30% to 90 million by 2055. Low birthrates, limited immigration, and retirement all increase demand for employment, therefore Japan’s younger-age workforce becomes a scarcer resource and will be more likely to secure and maintain employment. Eventually, I will become old enough in retirement that I will need my underwear and bedpan changed, and create a job for someone in the process – a job that cannot be outsourced I may add. Of course there are very few countries that want a declining population, even if it may lead to an improved unemployment rate. A growing country with liberal immigration laws, healthy birthrates, abundant resources, and pro-business initiatives may have higher unemployment rates but also have more jobs available because of the growing workforce.

Source: UN via Financial Times. Declining Japanese population is putting a growing burden on fewer shoulders.

Eventually the 76 million Baby Boomers born between 1946-1964 are going to be exiting the workforce and will increase the burden on our younger workforce. Do we want to follow in the same path of Japan? Or do we want to adjust our legislative process to meet the draining demands of our aging society? My answers are “No,” and “Yes,” respectively.

The unemployment hypochondriacs can take a deep breath knowing the path we are experiencing is nothing new. Certainly I would like to see better policies implemented to accelerate the economic recovery, but regardless of what inept politicians bungle, our innovative companies, and restless voters are waking up to keep our representatives accountable. This is important because we are like a younger but stronger cousin of Japan, and we do not want to follow along the decaying path of an aging indebted country. In the short-run, we all want to see job growth for the millions of unemployed. In the long-run, retiring Boomers will be stretching the resources of our country even more. So although the unemployment hypochondriacs have little to fear in the near-term as the recovery continues, fiscal responsibility needs to be kept in check or hidden economic illnesses may become reality.

Read James Paulsen’s complete August Economic and Market Perspective

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in BHP, POT, HPQ, PAR, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

V-Shaped Recovery or Road to Japan Lost Decades?

The Lost Decades from the 1989 Peak

On the 6th day of March this year, the S&P 500 reached a devilish low of 666. Now the market has rebounded more than 50% over the last five months. So is this a new bull market throttled into gear, or is it just a dead-cat bounce on route to a lost two decades, like we saw in Japan?

Smart people like Nobel Prize winner and economist Paul Krugman make the argument that like Japan, the bigger risk for the U.S. is deflation (NY Times Op-Ed), not inflation.

Now I’m no Nobel Prize winner, but I will make a bold argument of why Professor Krugman is out to lunch and why we will not go in a Japanese death-like, deflationary spiral.

Let’s review why our situation is dissimilar from our South Pacific friends.

Major Differences:

- Japanese Demographics: The Japanese population keeps getting older (see UN chart), which will continue to pressure GDP growth. According to the National Institute of Population and Social Security Research, by 2055 the Japanese population will fall 30% to 90 million (equivalent to 1955 level). Over the same time frame, the number of elderly under age 65 is expected to halve. To minimize the effects of the contraction of the working population, it will be necessary both to increase labor productivity, loosen immigration laws, and to promote the employment of woman and people over 65. Japan’s population is expected to expected contraction in Japan’s labor force of almost 1% a year in 2009-13.

Source: The Financial Times/UN (Declining Workforce Per 65 Year Old)

- Bank of Japan Was Slow to React: Japan recognized the bubble occurring and as a result hiked its key lending discount rate from 1989 through May 1991. The move had the desired effect by curbing the danger of inflation and ultimately popped the Nikkei-225 bubble. Stock prices soon plummeted by 50% in 1990, and the economy and land prices began to deteriorate a year later. Belatedly, Japan’s central bank began a series of interest rate-cuts, lowering its discount rate by 500-basis points to 1% by 1995. But the Japanese economy never recovered, despite $1-trillion in fiscal stimulus programs.

- The Higher You Fly, the Farther You Fall: The relative size of the Japanese bubble was gargantuan in scale compared to what we experienced here in the United States. The Nikkei 225 Index traded at an eye popping Price-Earnings ratio of about 60x before the collapse. The Nikkei increased over 450% in the eight years leading up to the peak in 1989, from the low of about 6,850 in October 1982 to its peak of 38,957 in December 1989. Compare those extreme bubble-icious numbers with the S&P 500 index, which rose approximately a more meager 20% from the end of 1999 to the end of 2007 (U.S. peak) and was trading at more reasonable 18x’s P-E ratio.

Source: Dow Jones

- Debt Levels not Sustainable: Japan is the most heavily indebted nation in the OECD. Japan is moving towards that 200% Debt/GDP level rapidly and the last time Japanese debt went to 200% of GDP (during WWII), hyper-inflation ensued and forced many fixed income elderly into poverty. Although our debt levels have yet to reach the extremes seen by Japan, we need to recognize the inflationary pressure building. Japan’s debt bubble cannot indefinitely sustain these debt increases, leaving little option but to eventually inflate their way out of the problem.

- Banking System Prolongs Japanese Deflation: Despite the eight different stimulus plans implemented in the 1990s, Japan lacked the fortitude to implement the appropriate corrective measures in their banking system by writing off bad debts. An article from July 2003 Barron’s article put it best:

After the collapse of the property bubble, many families and businesses had debts that far exceeded their devalued assets. When a version of this happened in America in the savings-and-loan crisis, the resulting mess was cleaned up quickly. The government seized assets, sold them off, bankrupted ailing banks and businesses, sent a few crooks to jail and everything started fresh, so that deserving new businesses could get loans. The process is like a tooth extraction — painful but mercifully short. In Japan this process has barely begun. Dynamic new businesses cannot get loans, because banks use available credit to lend to bankrupt businesses, so they can pretend they are paying their debts and avoid the pain of write-offs. This is self-deception. The rotten tooth is still there. And the Japanese people know it.

The Future – Rise of the Rest: Fareed Zakaria, Newsweek editor wrote about the “Rise of the Rest” in an incredible article (See Sidoxia Website) describing the rising tide of globalization that is pulling up the rest of the world. The United States population represents only 5% of the global total, and as the technology revolution raises the standard of living for the other 95%, this trend will only accelerate the demand of scarce resources, which will create a constant inflationary headwind.

For those countries in decline, like Japan, demand destruction raises the risk of deflation, but historically the innovative foundation of capitalism has continually allowed the U.S. to grow its economic pie. Economic legislation by our Congress will help or hinder our efforts in dealing with these inflationary pressures. One way is to incentivize investment in innovation and productive technologies. Another is to expand our targeted immigration policies towards attracting college educated foreigners, thereby relieving aging demographics pressures (as seen in Japan). These are only a few examples, but regardless of political leanings, our country has survived through wars, assassinations, terrorist attacks, banking crises, currency crises, and yes recessions, to only end up in a stronger global position.

This crisis has been extremely painful, but so have the many others we have survived. I believe time will heal the wounds and we will eventually conquer this crisis. I’m confident that historians will look at the coming years in favorable light, not the lost decades of pain as experienced in Japan.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

{kind=link}

{kind=link}