Posts tagged ‘IPOs’

Why the Masses Missed the 10-Year Bull Market

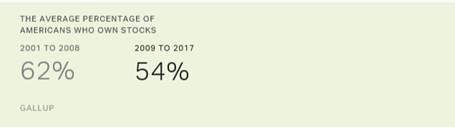

The investing masses generally are notoriously short-termed focused. Although the overall stock market notched another gain this month, stock values are still down roughly -8% from the January peak, which has caused some investor angst. Despite this nervousness, stock prices have quadrupled and the bull market has entered its 10th year after the March 2009 low (S&P 500: 666). Given this remarkable accomplishment, we can now look back and ask, “Did investors take advantage of this massive advance?” The short answer is “No.” For the most part, the fearful masses missed the decade-long, U.S. bull market. We know this dynamic to be true because data regarding stock ownership has gone down significantly, and hundreds of billions of dollars have been pulled from U.S. equity funds over the duration. For instance, Gallup, the survey and analytics company, annually polls the average percentage of Americans who own stocks and they found ownership has dropped from 62% of Americans in 2008 to 54% in 2017 (see chart below).

Much of the negativity that has dominated investor behavior over the last decade can be explained by important behavioral biases. As I describe in Controlling the Investment Lizard Brain, evolution created an almond-sized tissue in the prefrontal cortex of the brain (amygdala), which controls reasoning. Originally, the amygdala triggered the instinctual survival flight response for lizards to avoid hungry hawks and humans to flee ferocious lions. In today’s modern society, the probability of getting eaten by a lion is infinitesimal, so rather than fretting over a potential lion slaughtering, humans now worry about their finances getting eaten by financial crises, Federal Reserve interest rate hikes, and/or geopolitical risks.

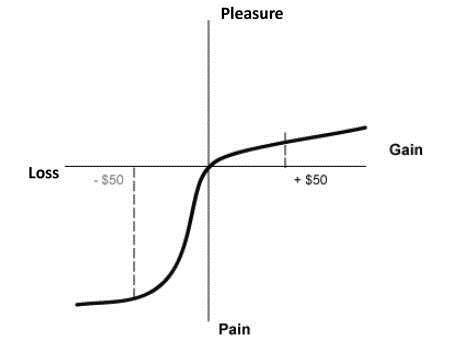

Even with the spectacular +300% appreciation in stock values from early 2009, academic research can help us understand how pessimism can outweigh optimism, even in the wake of a raging bull market. Consider the important risk aversion research conducted by Nobel Prize winner Daniel Kahneman and his partner Amos Tversky (see Pleasure/Pain Principle). Their research pointed out the pain of losses can be twice as painful as the pleasure experienced through gains (see diagram below).

Given this backdrop, how can these gargantuan gains be maintained (or improved upon) when investors are continually draining money out of riskier stocks and pouring cash into more conservative bonds? (see Fund Flows Paradox). There are several major factors that can explain the colossal gains in the face of a stock investor exodus:

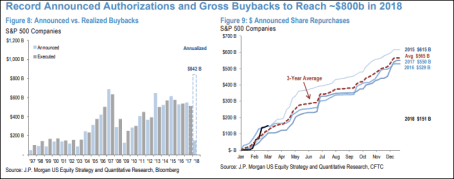

- Share Buybacks: While investors might not be buying loads of stocks, corporations have purchased trillions of dollars in stocks since the financial crisis. As you can see from the chart below, the table is set for 2018 to be a record year in share buybacks ($842 billion estimate), thanks to record profits and tax legislation that is making it cheaper for corporations to bring back foreign profits abroad.

Source: Marketwatch

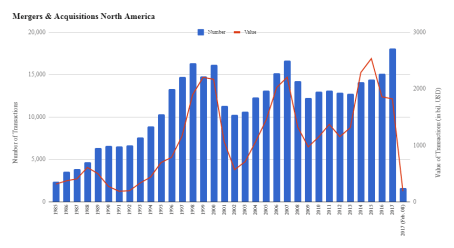

- Mergers & Acquisitions (M&A): Record profits, low interest rates, and high cash levels have led to trillions of dollars in U.S. M&A activity (almost $2 trillion in 2017) – see chart below. Not all of this was funded with cash and debt, but suffice it to say, enormous amounts of equity have been removed from the stock market.

Source: IMAA Institute

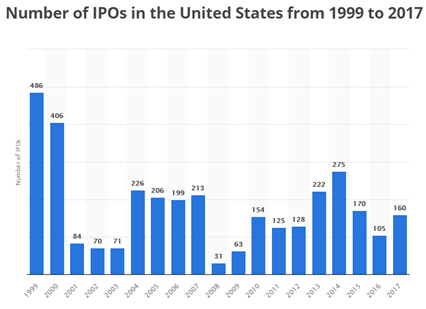

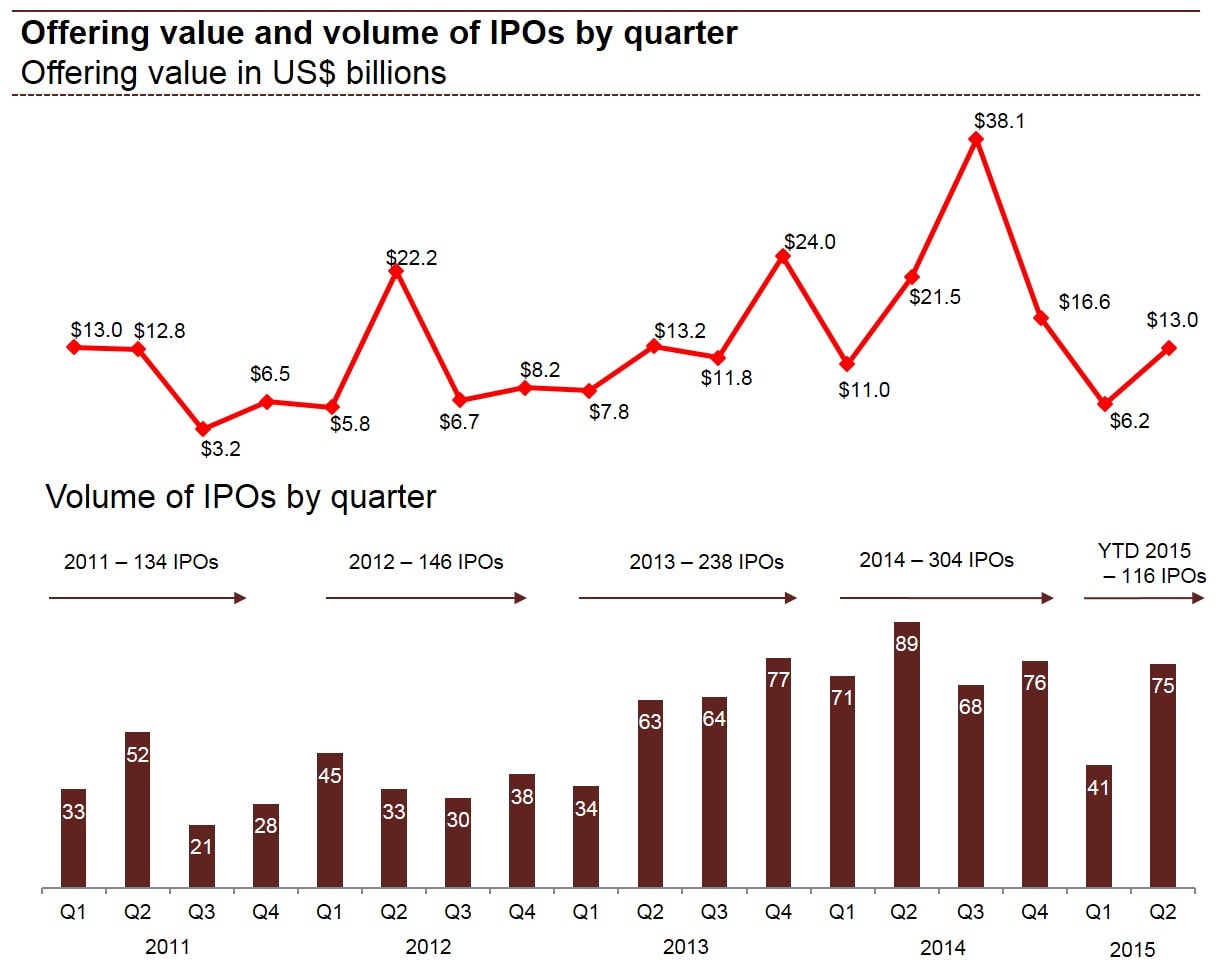

- Limited IPOs: Certainly, we have seen a few high-profile, stock deals hit the market in the form of initial public offerings (IPOs) over the last year. Some prominent IPOs over the last year, include Dropbox Inc. (DBX), Spotify Technology (SPOT), and Snap Inc. (SNAP), however this limited supply of new deals is a drop in the bucket. As you can see from the chart below, the number of IPOs is significantly below the 1999-2000 peak and the recent added supply pales in comparison to the latest supply-sucking share buybacks and acquisitions.

Source: Statista

Just as important as these supply related issues are to the stock market, demand related issues are important as well. While individual U.S. investors have been scarred by the 2008-2009 financial crisis, ultimately, over the long run, money does not care about behavioral biases. Money goes where it is treated best. Theoretically, the best treatment could be in U.S. stocks or U.S. bonds, or it could be in pork bellies or the Thai baht currency, among many other asset classes (e.g., real estate, commodities, venture capital, Bitcoin, etc.). Much like a trip to the grocery store, global money flows search for the best deals. If beef prices spike by +30% and chicken prices drop by -20%, guess what? Shoppers will now buy more chicken and less beef. Similarly, when Japanese 10-year bonds are yielding 0.04%, German 10-year bonds 0.56%, and U.K. 10-year bonds 1.42%, then U.S. 10-year Treasuries with a 2.96% yield don’t look so bad.

More importantly, as it relates to stock prices, there has been a mass divergence between the interest rate yields earned on Treasuries and the earnings yield (E/P or the inverse P/E ratio) since this 10-year bull market began (Ed Yardeni has a great chart of this Fed Valuation chart). Stocks, as they are valued today, are effectively providing double the yield of bonds (roughly a 6% yield vs 3% yield, respectively). As long as this phenomenon remains intact over the medium term, stocks could continue to significantly outperform bonds. Eventually a spike in stock prices and/or an earnings decline caused by a recession will lower the earnings yield on stocks, but until then, nervous investors will likely continue to underperform.

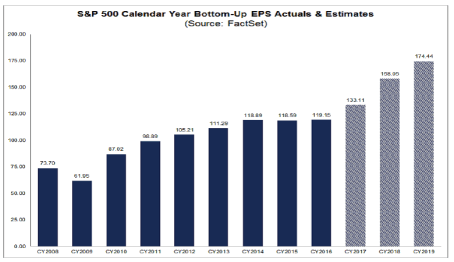

What the almost 10-year bull market teaches us is that our behavioral shortcomings can be a drag on performance and stock values, but the economic laws of supply and demand can play an even more significant role in the direction of the stock market. Learning how to control your lizard brain (amygdala), and understand how the pain of losses (risk aversion) can distort decision making processes can help you more clearly see how record profits (see chart below), share buybacks, M&A activity, and limited stock issuance (i.e. IPOs) will impact stock prices. Understanding these lessons will better prepare the masses in navigating through future bull and bear markets.

Source: FACTSET

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (May 1, 2018). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in DBX, SPOT, SNAP, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Supply & Demand: The Key to Oil, Stocks, and Pork Bellies

Commodity prices, including oil, are “crashing” according to the pundits and fears are building that this is a precursor to another stock market collapse. Are we on an irreversible path of repeating the bloodbath carnage of the 2008-2009 Great Recession?

Fortunately for investors, markets move in cycles and the fundamental laws of supply and demand hold true in both bull and bear markets, across all financial markets. Whether we are talking about stocks, bonds, copper, gold, currencies, or pork bellies, markets persistently move like a pendulum through periods of excess supply and demand. In other words, weakness in prices create stronger demand and less supply, whereas strength in prices creates weakening demand and more supply.

Since energy makes the world go round and the vast majority of drivers are accustomed to filling up their gas tanks, the average consumer is familiar with recent negative price developments in the crude oil markets. Eighteenth-century economist Adam Smith would be proud that the laws of supply and demand have help up just as well today as they did when he wrote Wealth of Nations in 1776.

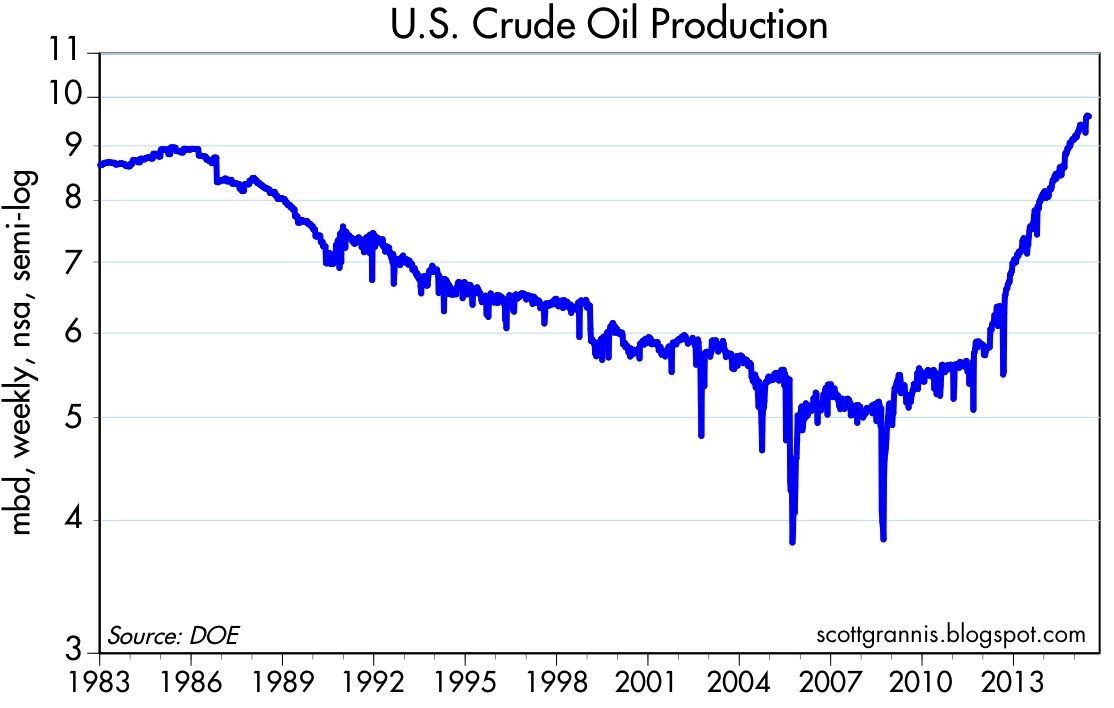

It is true that overall stagnation in global economic demand in recent years, along with the strengthening of the U.S. dollar (because of better relative growth), has contributed to downward trending oil prices. It is also true that supply factors, such as Saudi Arabia’s insistence to maintain production and the boom in U.S. oil production due to new fracking technologies (see chart below), have arguably had a larger negative impact on the more than -50% deterioration in oil prices. Fears of additional Iranian oil supply hitting the global oil markets as a result of the Iranian nuclear deal have also added to the downward pressure on prices.

Source: Scott Grannis

What is bad for oil prices and the oil producers is good news for the rest of the economy. Transportation is the lubricant of the global economy, and therefore lower oil prices will act as a stimulant for large swaths of the global marketplace. Here in the U.S., consumer savings from lower energy prices have largely been used to pay down debt (deleverage), but eventually, the longer oil prices remain depressed, incremental savings should filter into our economy through increased consumer spending.

But prices are likely not going to stay low forever because producers are responding drastically to the price declines. All one needs to do is look at the radical falloff in the oil producer rig count (see chart below). As you can see, the rig count has fallen by more than -50% within a six month period, meaning at some point, the decline in global production will eventually provide a floor to prices and ultimately provide a tailwind.

Source: Scott Grannis

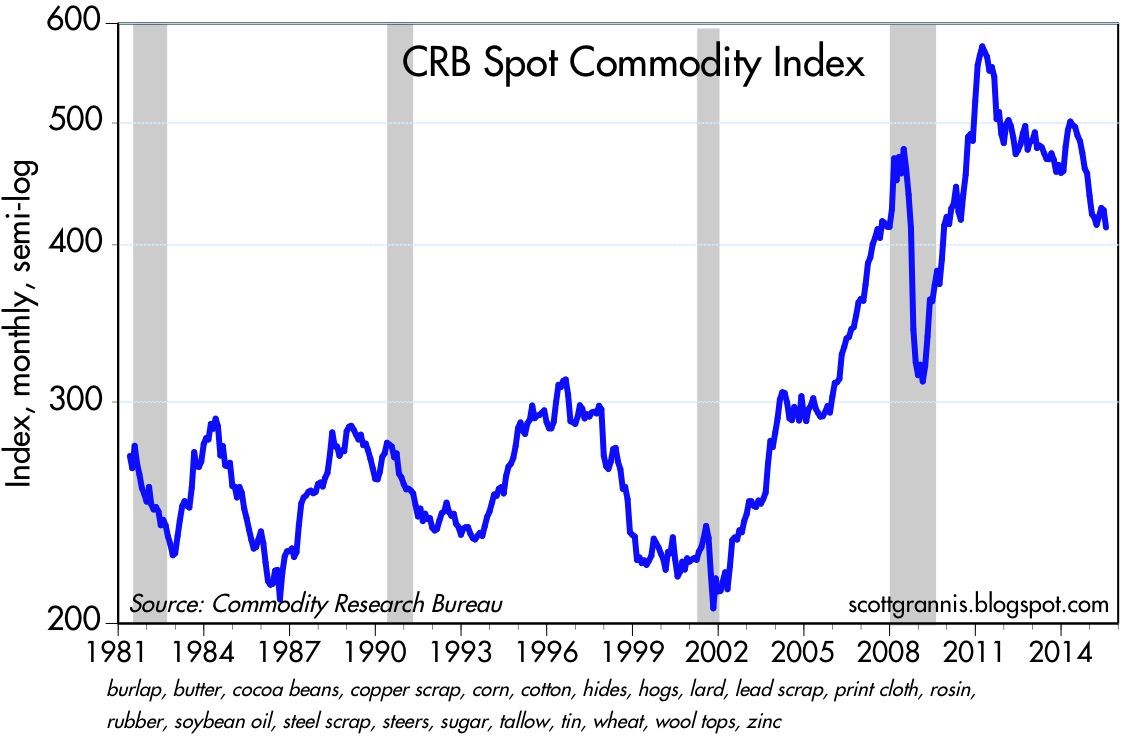

If we broaden our perspective beyond just oil, and look at the broader commodity complex, we can see that the recent decline in commodity prices has been painful, but nowhere near the Armageddon scenario experienced during 2008-2009 (see chart below – gray areas = recessions).

Source: Scott Grannis

Although this conversation has focused on commodities, the same supply-demand principles apply to the stock market as well. Stock market prices as measured by the S&P 500 index have remained near record levels, but as I have written in the past, the records cannot be attributed to the lackluster demand from retail investors (see ICI fund flow data).

Although U.S. stock fundamentals remain relatively strong (e.g., earnings, interest rates, valuations, psychology), much of the strength can be explained by the constrained supply of stocks. How has stock supply been constrained? Some key factors include the trillions in dollars of supply soaked up by record M&A activity (mergers and acquisition) and share buybacks.

In addition to the declining stock supply from M&A and share buybacks, there has been limited supply of new IPO issues (initial public offerings) coming to market, as evidenced by the declines in IPO dollar and unit volumes in the first half of 2015, as compared to last year. More specifically, first half IPO dollar volmes were down -41% to $19.2 billion and the number of 2015 IPOs has declined -27% to 116 from 160 for the same time period.

Price cycles vary dramatically in price and duration across all financial markets, including stocks, bonds, oil, interest rates, currencies, gold, and pork bellies, among others. Not even the smartest individual or most powerful computer on the planet can consistently time the short-term shifts in financial markets, but using the powerful economic laws of supply and demand can help you profitably make adjustments to your investment portfolio(s).

See Also – The Lesson of a Lifetime (Investing Caffeine)

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Investing with the Sentiment Pendulum

Article is an excerpt from Sidoxia Capital Management’s complementary May 2012 newsletter. Subscribe on right side of page.

The last five years have been historic in many respects. Not only have governments and central banks around the world undertaken unprecedented actions in response to the global financial crisis, but investors have ridden an emotional rollercoaster in response to historically unparalleled uncertainties.

While the nature of this past crisis has been unique, experienced investors know these fears continually manifest themselves in different forms over various cycles in time. Despite the more than doubling in equity market values over the last few years, as measured by the S&P 500 index, the emotional pendulum of investor sentiment has only partially corrected. Investor temperament has thankfully swung away from “Panic,” but has only moved closer to “Fear” and “Skepticism.” Here are some of the issues contributing to investors’ current sour mood:

The Next European Domino: The fear of the Greek domino toppling the larger Spanish and Italian economies has investors nervously chewing their finger-nails, and political turmoil in France and the Netherlands isn’t creating any additional warm and fuzzies.

Job Additions Losing Steam: New job creation here in the U.S. weakened to a lethargic monthly rate of +120,000 new jobs in March, while the unemployment rate remains stubbornly high at an 8.2% level.

Domestic Growth Losing Mojo: GDP (Gross Domestic Product) growth of +2.2% during the first quarter of 2012 also opened the door for the pessimists. Consumers are still spending (+2.9% growth), but government spending, business investment, and housing are taking wind out of the economy’s sails.

Emerging Markets Submerging: Unspectacular growth in the U.S. is not receiving any favors from slowing emerging markets like China and Brazil, which took fiscal and monetary actions to slow inflation and housing speculation in 2011.

Humpty Dumpty Politics: Presidential elections, tax policy, and deficit reduction are all concerns that carry the possibility of pushing the economic Humpty Dumpty off the wall, and as a result potentially lead to a great fall. The determination of Humpty Dumpty’s fate will likely have to wait until year-end or 2013.

Any student of history knows these fears and other concerns never go away – they simply change. But like supply and demand, gravitational forces eventually swing the emotional pendulum in the opposite direction. As Sir John Templeton so aptly stated, “Bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria.” Or in other words, escalating bull markets must climb the proverbial “Wall of Worry” in order to sustain upward momentum. If there was nothing to worry about, then all the buyers would already be in the markets. We are nowhere close to experiencing “Euphoria” like we saw in stocks during the late-1990s or in the housing market around 2005.

Positively Climbing the “Wall of Worry”

With all this bad news out there, surprisingly there are some glimmers of hope chipping away at the “Wall of Worry.” Here are some of the positive factors helping turn pessimist frowns upside down:

Slow & Steady Wins the Race: The economic recovery has been weaker than hoped, but I can think of worse scenarios than 11 consecutive quarters of GDP growth and 25 straight months of private job creation, which has reduced the unemployment rate from 10.0% in October 2009 to 8.2% last month.

Earnings Machine Keeps Chugging Along: With the majority of S&P 500 companies having reported their quarterly results for the first quarter, three-fourths of the companies are beating forecasted earnings, which are currently registering in at a respectable +7.1% rate (Thomson Reuters). One company epitomizing this trend is Apple Inc. (AAPL). The near doubling in Apple’s profits during the quarter, thanks to explosive iPhone sales, pushed Apple’s shares over $600 and helped drive the NASDAQ index to its best day of the year.

Super Ben to the Rescue: The Federal Reserve has already stated their intention of keeping interest rates near 0% until 2014. The potential of additional monetary stimulus spearheaded by Federal Reserve Chairman Ben Bernanke, in the form of QE3 (Quantitative Easing Part III), may provide further needed support to the stock market (a.k.a., the “Bernanke Put”).

Return of the IPO: Initial Public Offerings (IPOs) have gained steam versus last year with more than 53 already coming to market in the first four months of 2012. This is no 1999, but a good number of deals have done quite well over the last month. For example, data analysis company Splunk Inc. (SPLK) share price is already up around 100% and the value of leisure luggage company TUMI Holdings (TUMI) has climbed over +40%. In a few weeks, the highly anticipated blockbuster Facebook (FB) IPO is expected to begin trading its shares, so we can see if the chronicled deal can live up to all the hype.

Dividends Galore: Dividend payments to stockholders are flowing at an extraordinary rate so far in 2012. Companies like IBM (increased its dividend by +13%), Exxon Mobil – (XOM +21%); Goldman Sachs – (GS +31%) are but just a few of the dividend raisers this year. Through the first three months of the year, the number of companies increasing their dividend payments was up +45% as compared to the comparable number for all of 2011.

Emerging Growth Not Dead: While worriers fret over slowing growth in China, companies like Apple grew by more than +100% in this region and collected nearly 20% of its revenues from this Asian country (~$8 billion). Coincidentally, China is expected to surpass an incredible one billion mobile connections in May – many of those iPhones. In other related news, Starbucks Corp. (SBUX) plans to triple its workforce and number of stores in China over the next three years. China has also helped fuel a backlog of Caterpillar Inc. (CAT) that is more than triple the level of 2009. Emerging markets may have slowed down in 2011, but with inflation beginning to stabilize, emerging market central banks and governments are now beginning to ease policies and reduce red-tape. For example, Brazil and India have started to lower key benchmark interest rates, and China has started to reverse capital flow restrictions.

Stay Off the Trampled Path

The mantra of “Sell in May and go away” always gets a lot of playtime around this period of the year. Over the last few years, the temporary spring/summer sell-offs have only been followed by stronger price appreciation. Individuals attempting to time the market (see also Getting Off the Treadmill) generally end up in tears. And for those traders who boast about their excellent timing (like those suspicious friends who brag about always winning in Las Vegas), we all know the truth – nobody buys at the lows and sells at the highs…except for liars.

With all the noise and cross-currents flooding the airwaves, investing for individuals without assistance has never been so difficult. But before hiding in your cave or reacting to the next scary headline about Europe, the economy, or politics, do yourself a favor by reminding yourself these chilling news items are nothing new and are often great contrarian indicators (see also Back to the Future). The emotional pendulum is constantly swinging from fear to greed and investors stand to prosper by adjusting sentiment and actions in the opposite direction. To survive in the investing wild, it is best to realize that the grass is greener and the eating more abundant when you stay off the trampled path of the herd.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and AAPL, but at the time of publishing SCM had no direct position in SPLK, TUMI, IBM, XOM, GS, SBUX, CAT, FB, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}

{kind=link}