Posts tagged ‘interest rates’

Half Trump Empty, or Half Trump Full?

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (December 1, 2016). Subscribe on the right side of the page for the complete text.

It was a bitter U.S. presidential election, but fortunately, the nastiest election mudslinging has come to an end…at least until the next political contest. Unfortunately, like most elections, even after the president-elect has been selected, almost half the country remains divided and the challenges facing the president-elect have not disappeared.

While some non-Trump voters have looked at the glass as half empty, since the national elections, the stock market glass has been overflowing to new record highs. Similar to the unforeseen British Brexit outcome in which virtually all pollsters and pundits got the results wrong, U.S. experts and investors also initially took a brief half-glass full view of the populist victory of Donald Trump. More specifically, for a few hours on Election Day, stock values tied to the Dow Jones Industrial Average index collapsed by approximately -5%.

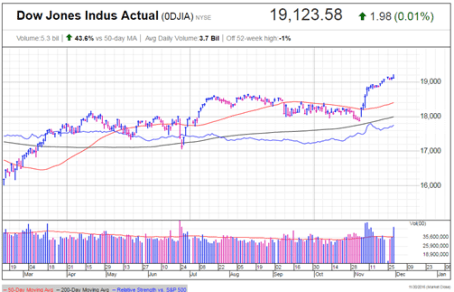

It didn’t take long for stock prices to quickly reverse course, and when all was said and done, the Dow Jones Industrial Average finished the month higher by almost +1,000 points (+5.4%) to finish at 19,124 – a new all-time record high (see chart below). Worth noting, stocks have registered a very respectable +10% return during 2016, and the year still isn’t over.

Source: Investors.com (IBD)

Drinking the Trump Egg Nog

Why are investors so cheery? The proof will be in the pudding, but current optimism is stemming from a fairly broad list of anticipated pro-growth policies.

At the heart of the reform is the largest expected tax reform since Ronald Reagan’s landmark legislation three decades ago. Not only is Trump proposing stimulative tax cuts for corporations, but also individual tax reductions targeted at low-to-middle income taxpayers. Other facets of the tax plan include simplification of the tax code; removal of tax loopholes; and repatriation of foreign cash parked abroad. Combined, these measures are designed to increase profits, wages, investment spending, productivity, and jobs.

On the regulatory front, the President-elect has promised to repeal the Obamacare healthcare system and also overhaul the Dodd-Frank financial legislation. These initiatives, along with talk of dialing back other regulatory burdensome laws and agencies have many onlookers hopeful such policies could aid economic growth.

Fueling further optimism is the prospect of a trillion dollar infrastructure spending program created to fix our crumbling roads and bridges, while simultaneously increasing jobs.

No Free Lunch

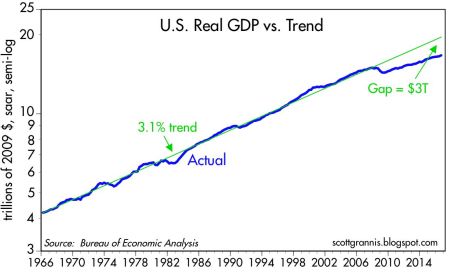

As is the case with any economic plan, there is never a free lunch. Every cost has a benefit, and every benefit has a cost. The cost of the 2008-2009 Financial crisis is reflected in the sluggish economic growth seen in the weak GDP (Gross Domestic Product) statistics, which have averaged a modest +1.6% growth rate over the last year. Scott Grannis points out how the slowest recovery since World War II has resulted in a $3 trillion economic gap (see chart below).

Source: Calafia Beach Pundit

The silver lining benefit to weak growth has been tame inflation and the lowest interest rate levels experienced in a generation. Notwithstanding the recent rate rise, this low rate phenomenon has spurred borrowing, and improved housing affordability. The sub-par inflation trends have also better preserved the spending power of American consumers on fixed incomes.

If executed properly, the benefits of pro-growth policies are obvious. Lower taxes should mean more money in the pockets of individuals and businesses to spend and invest on the economy. This in turn should create more jobs and growth. Regulatory reform and infrastructure spending should have similarly positive effects. However, there are some potential downside costs to the benefits of faster growth, including the following:

- Higher interest rates

- Rising inflation

- Stronger dollar

- Greater amount of debt

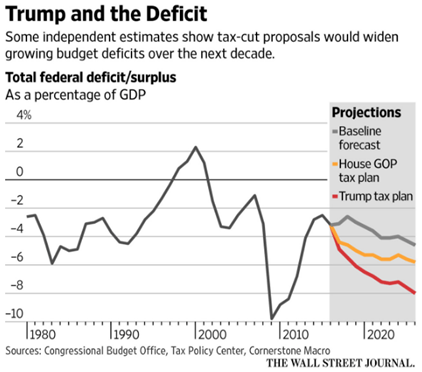

- Larger deficits (see chart below)

Source: The Wall Street Journal

Even though President-elect Trump has not even stepped foot into the Oval Office yet, signs are already emerging that we could face some or all of the previously mentioned headwinds. For example, just since the election, the yield on 10-Year Treasury Notes have spiked +0.5% to 2.37%, and 30-Year Fixed Rate mortgages are flirting with 4.0%. Social and economic issues relating to immigration legislation and Supreme Court nominations are likely to raise additional uncertainties in the coming months and years.

Attempting to anticipate and forecast pending changes makes perfect sense, but before you turn your whole investment portfolio upside down, it’s important to realize that actions speak louder than words. Even though Republicans have control over the three branches of government (Executive, Legislative, Judicial), the amount of control is narrow (i.e., the Senate), and the nature of control is splintered. In other words, Trump will still have to institute the “art of the deal” to persuade all factions of the Republicans (including establishment, Tea-Party, and rural) and Democrats to follow along and pass his pro-growth policies.

Although I do not agree with all of Trump’s policies, including his rhetoric on trade (see Free Trade Boogeyman), I will continue paying closer attention to his current actions rather than his past words. Until proven otherwise, I will keep on my rose colored glasses and remain optimistic that the Trump glass is half full, not half empty.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

What Do You Worry About Next?

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (November 1, 2016). Subscribe on the right side of the page for the complete text.

Boo! Halloween has just passed and frightened investors have still survived to tell the tale in 2016. While most people have gotten spooked by the presidential election, other factors like record-high corporate profits, record-low interest rates, and reasonable valuations have led to annual stock market gains. More specifically, values have risen in 2016 by approximately +4% (or +6% including dividend payments). Despite last week’s accelerating 3rd quarter GDP economic growth figure of +2.9%, which was the highest rate in two years and more than doubled the rate of the previous quarter (up +1.4%), there were still more tricks than treats during October. Recently, scary politics have shocked many Halloween participants into a zombie-like state, as evidenced by stock values declining around -1.7% during October.

This recent volatility is nothing new. Even though financial markets are significantly higher in recent years, that has not prevented repeated corrections over the year(s) as shown below in the 2009 – 2015 chart.

In order to earn higher long-term returns, investors have to accept a certain amount of short-term price movements (upwards and downwards). With a couple months remaining in the year, stock investors have achieved gains through a tremendous amount of economic and geopolitical uncertainty, including the following scares:

- China: A significant fallout from a Chinese slowdown at the beginning of the year (stocks fell about -14%).

- Brexit: A 48-hour Brexit vote scare in June (stocks fell -6%).

- Fed Fears: Threatening comments in September from the Federal Reserve about potentially hiking increasing interest rates (stocks fell -4%).

With the elections just a week away, political anxiety has jolted Americans’ adrenaline levels. The polls continue to move up and down, but as I have repeatedly pointed out, the only certain winner in Washington DC is gridlock. Sure, in a Utopian world, politicians should join hands and compromise to solve all our country’s serious problems. Unfortunately, this is not the case (see Congress’s approval rating). However, there is a silver lining to this dysfunction…gridlock can lead to fiscal discipline.

Our country’s debt/deficit financial situation has been spiraling out of control, in large measure due to rapidly rising entitlement spending, including Medicare, and Social Security. Witnessing all the political rhetoric and in-fighting is very difficult, but as I highlighted in last month’s newsletter, gridlock has flattened the spending curve significantly since 2009 – a positive development.

And although the economic recovery has been one of the slowest since World War II and global growth remains anemic, the U.S. remains a better house in a bad global neighborhood (e.g., Europe and Japan continue to suck wind), as evidenced by a number of these following positive economic indicators:

- Employment Improvement: Unemployment has fallen from 10% to 5% since 2009, and more than 15 million jobs have been added over that period.

- Housing Recovery Continues: Home sales and prices continue their multi-year rise; housing inventories remain tight; and affordability remains strong, given generationally low interest rates.

- Record Auto Sales: Car sales remain near record levels, hovering around 17 million units per year.

- Consumer Confidence on the Rise: Ever since the financial crisis, consumer sentiment figures have rebounded by about 50%.

-

Record Consumer Sales: Consumer spending accounts for approximately 70% of our economy, and as you can see from the chart below, despite consumers saving more, stronger employment and wages are fueling more spending.

Source:Calculated Risk

Source:Calculated Risk

Absent a clean sweep of control by the Democrat or Republican Presidential-Congressional candidates, our democratic system will retain its healthy status of checks and balances. Based on all the current polling data, a split between the White House, Senate, and House of Representatives remains a very high likelihood scenario.

The political process has been especially exhausting during the current cycle, but regardless of whether your candidate wins or loses, much of the current uncertainty will likely dissipate. As the saying goes, at least it is “Better the devil you know than the devil you don’t know.”

After the November 8th elections are completed, there will be one less election to worry about. Thankfully, after 25 years in the industry, I’m not naïve enough to believe there will be nothing else to worry about. When the financial media and blogosphere get bored, at a minimum, you can guarantee yourself plenty of useless coverage regarding the next monetary policy move by the Federal Reserve (see also Fed Fatigue).

Whatever the next set of worries become, U.K. Prime Minister Winston Churchill said it best as it relates to American politics and economics, “You can always count on Americans to do the right thing – after they’ve tried everything else.” If Churchill’s words don’t provide comfort and you had fun getting spooked over the elections on Halloween, feel free to keep wearing your costume. Behind any constructive economic data, the prolific media machine will continue doing their best in manufacturing plenty of fear, uncertainty, and doubt to keep you worried.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Fall is Here: Change is Near

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (October 1, 2016). Subscribe on the right side of the page for the complete text.

Although the fall season is here and the leaf colors are changing, there are a number of other transforming dynamics occurring this economic season as well. The S&P 500 index may not have changed much this past month (down -0.1%), but the technology-laden NASDAQ index catapulted higher (+1.9% for the month and +6.0% for 2016).

With three quarters of the year now behind us, beyond experiencing a shift in seasonal weather, a number of other changes are also coming. For starters, there’s no ignoring the elephant in the room, and that is the presidential election, which is only weeks away from determining our country’s new Commander in Chief. Besides religion, there are very few topics more emotionally charged than politics – whether you are a Republican, Democrat, Independent, Libertarian, or some combination thereof. Even though the first presidential debate is behind us, a majority of voters are already set on their candidate choice. In other words, open-minded debate on this topic can be challenging.

Hearing critical comments regarding your favorite candidate are often interpreted in the same manner as receiving critical comments about a personal family member – people often become defensive. The good news, despite the massive political divide currently occurring in the country and near-record low politician approval ratings in Congress , politics mean almost nothing when it comes to your money and retirement (see also Politics & Your Money). Regardless of what politicians might accomplish (not much), individuals actually have much more control over their personal financial future than politicians.

While inaction may rule the day currently, more action generally occurs during a crisis – we witnessed this firsthand during the 2008-2009 financial meltdown. As Winston Churchill famously stated,

“You can always count on Americans to do the right thing – after they’ve tried everything else.”

Political discourse and gridlock are frustrating to almost everyone from a practical standpoint (i.e., “Why can’t these idiots get something done in Washington?!”), however from an economic standpoint, gridlock is good (see also Who Said Gridlock is Bad?) because it can keep a responsible lid on frivolous spending. Educated individuals can debate about the proper priorities of government spending, but most voters agree, maintaining a sensible level of spending and debt should be a bipartisan issue.

From roughly 2009 – 2014, you can see how political gridlock has led to a massive narrowing in our government’s deficit levels (chart below) – back to more historical levels.This occurred just as rising frustration with Washington has been on the rise.

The Fed: Rate Revolution or Evolution?

Besides the changing season of politics, the other major area of change is Federal Reserve monetary policy. Even though the Fed has only increased interest rates once over the last 10 years, and interest rates are at near-generational lows, investors remain fearful. There is bound to be some short-term volatility if interest rates rise to 0.50% – 0.75% in December, as currently expected. However, if the Fed continues at its current snail’s pace, it won’t be until 2032 before they complete their rate hike cycles.

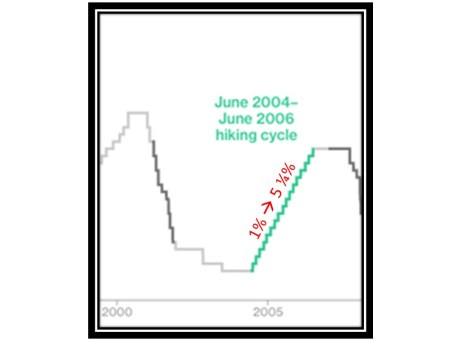

We can put the next rate increase into perspective by studying history. More specifically, the Fed raised interest rates 17 times from 2004 – 2006 (see chart below). Fortunately over this same time period, the world didn’t end as the Fed increased interest rates from 1.00% to 5.25% (stocks prices actually rose around +11%). The same can be said today – the world won’t likely end, if interest rates rise from 0.50% to 0.75% in a few months.

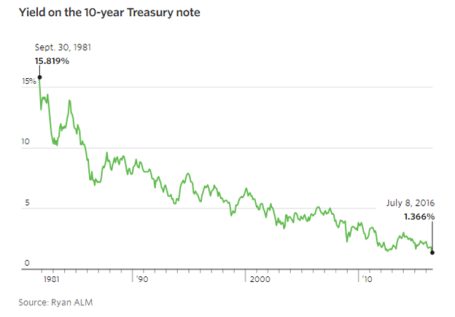

The next question becomes, why are interest rates so low? There are many reasons and theories, but a few of the key drivers behind low rates include, slower global economic growth, low inflation, high demand for low-risk assets, technology, and demographics. I could devote a whole article to each of these factors, and indeed in many cases I have, but suffice it to say that there are many reasons beyond the oversimplified explanation that artificial central bank intervention has led to a 35 year decline in interest rates (see chart below).

Change is a constant, and with fall arriving, some changes are more predictable than others. The timing of the U.S. presidential election outcome is very predictable but the same cannot be said for the timing of future interest rate increases. Irrespective of the coming changes and the related timing, history reminds us that concerns over politics and interest rates often are overblown. Many individuals remain overly-pessimistic due to excessive, daily attention to gloomy and irrelevant news headlines. Thankfully, stock prices are paying attention to more important factors (see Don’t Be a Fool) and long-term investors are being rewarded with record high stock prices in recent weeks. That’s the type of change I love.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Invest or Die

Seventy-six million Baby Boomers are earning near 0% (or negative rates) and aren’t getting any younger in the process, which is forcing them and others to decide…invest or die. The risk of outliving your savings is becoming a larger reality these days. Demographics and economics are dictating that our aging population is living longer and earning less due to generationally low interest rates.

Richard Fisher, the former Dallas Federal Reserve president, understands these looming dynamics. Fisher has identified how low-interest rates are increasing investor discontent by pushing consumers to save more in order to meet retirement needs. The unintended consequence from low rates, he said, is “you’re going to have to save a hell of a lot more before you consume.”

Besides saving, the other option investors have is to lower your standard of living. For example, you could continually eat mac & cheese and sleep in a tent – that is indeed one way you could save money. However, your kids and/or desired lifestyle may make this way of life unpalatable for all. Rather, the proper approach to achieving a comfortable standard of living requires you to invest more efficiently and prudently.

What a lot of individuals fail to understand is that accepting too much risk can be just as dangerous as being too conservative, over the long run. Case in point, depositing your savings into a CD at current interest rates (near 0%) is the equivalent of burning your cash, as any income produced is overwhelmed by the deleterious effects of inflation. It would take more than a lifetime of CD interest income to equal equity returns earned over the last seven years. Since early 2009, stocks have more than tripled in value.

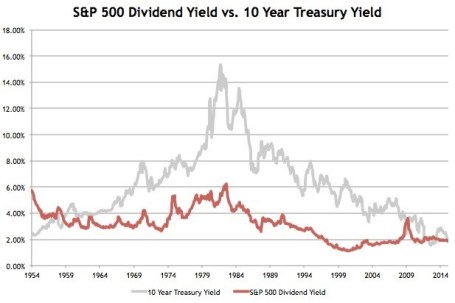

Given the prevailing economic and demographic trends, investors are slowly realizing the attractive income-producing nature of stocks relative to bonds. It has been a rare occurrence, but stocks, as measured by the S&P 500, continue to yield more than 10-Year Treasury Notes (2.0% vs. 1.6%, respectively) – see chart below. The picture for bonds looks even worse in many international markets, where $13 trillion in bonds are yielding negative interest rates. Unlike bonds, which generally pay fixed coupon payments for years at a time, stocks overall have historically increased their dividend payouts by approximately 6% annually.

Source: Avondale Asset Management

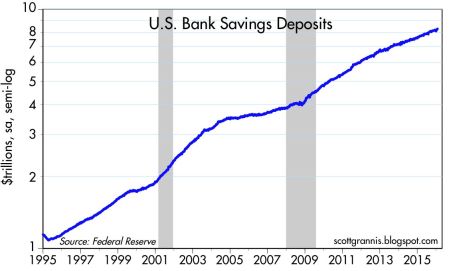

With a scarcity of attractive investment alternatives available, investors will eventually be forced to adopt higher levels of equity risk, like it or not. However, this dynamic has yet to happen. Currently, actions are speaking louder than words, and as you can see, risk aversion reigns supreme with Americans tucking over $8 trillion dollars under their mattress (see chart below), in the form of savings accounts, earning next to nothing and jeopardizing retirements.

Source: Calafia Beach Pundit

Even if you fall into the camp that believes rates are artificially low by central bank printing presses, that doesn’t mean every company is recklessly leveraging their balance sheets up to the hilt. Many companies are still scared silly from the financial crisis and conservatively managing every penny of expense, like a stingy retiree living on a fixed income. Thanks to this reluctance to spend and hire aggressively, profit margins are at/near record highs. This financial stewardship has freed up corporations’ ability to pay higher dividends and implement discretionary stock buybacks as means to return capital to shareholders.

With the dovish Fed judiciously raising interest rates – only one rate hike of 0.25% over a decade (2006 – 2016) – there are no signs this ultra-low interest rate environment is going to turn aggressively higher anytime soon. Until economic growth, inflation, and interest rates return with a vengeance, and the persistent investor risk aversion abates, it behooves all the cash hoarders to….invest or die!

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Huh… Stocks Reach a Record High?

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (September 1, 2016). Subscribe on the right side of the page for the complete text.

The stock market hit all-time record highs again in August, but despite the +6.2% move in 2016 S&P 500 stock prices (and +225% since early 2009), investors continue to scratch their heads in confusion. Individuals continue to ask, “Huh, how can stocks be trading at or near record levels (+6% for the year) when Brexit remains a looming overhang, uncertainty surrounds the U.S. presidential election, global terrorist attacks are on the rise, negative interest rates are ruling the day, and central banks around the globe are artificially propping up financial markets (see also Fed Myths vs. Reality)? Does this laundry list of concerns stress you out? If you said “yes”, you are not alone.

As I’ve pointed out in the past, we live in a different world today. In the olden days, terrorist attacks, natural disasters, currency crises, car chases, bank failures, celebrity DUIs, and wars happened all the time. However, before the internet existed, people either never heard about these worries, or they just didn’t care (or both). Today, we live in a Twitter, Facebook, Instagram, Snapchat, society with 500+ cable channels, and supercomputers in the palm of our hands (i.e., smartphones) with more computing power than existed on the Apollo mission to the moon. In short, doom-and-gloom captures human attention and sells advertising, the status quo does not.

- Record corporate profits are on the rise

- Stabilizing value of the dollar

- Stabilizing energy and commodity prices

- Record low interest rates

- Skeptical investing public

Fortunately, the stock market pays more attention to these important dynamics, rather than the F.U.D. (Fear, Uncertainty, Doubt) peddled by the pundits, bloggers, and TV talking heads. Certainly, any or all of the previously mentioned positive factors could change or deteriorate over time, but for the time being, the bulls are winning.

Let’s take a closer look at the influencing components that are driving stock prices higher:

Record Corporate Profits

Source: Yardeni.com

Profits are the mother’s milk that feeds the stock market. During recessions, profits are starved and stock prices decline. On the flip side, economic expansions feed profits and cause share prices to rise. As you can see from the chart above, there was a meteoric rise in corporate income from 2009 – 2014 before a leveling off occurred from 2015 going into 2016. The major headwinds causing profits to flatten was a spike of 25% in the value of the U.S. dollar relative to the value of other global currencies, all within a relatively short time span of about nine months (see chart below).

Why is this large currency shift important? The answer is that approximately 40% of multinational profits derived by S&P 500 companies come from international markets. Therefore, when the value of the dollar rose 25%, the cost to purchase U.S. products and services by foreign buyers became 25% costlier. Selling dramatically higher cost goods abroad squeezed exports, which in turn led to a flattening of profits. Time will tell, but as I showed in the first chart, the slope of the profit line has resumed its upwards trajectory, which helps explain why stock prices have been advancing in recent months.

Besides a strong dollar, another negative factor that temporarily weakened earnings was the dramatic decline in oil prices (see chart below) Two years ago, WTI oil prices were above $100 per barrel. Today, prices are hovering around $45 per barrel. As you can imagine, this tremendous price decline has had a destructive impact on the profits of the energy sector in general. The good news is that after watching prices plummet below $30 earlier this year, prices have since stabilized at higher levels. In other words, the profits headwind has been neutralized, and if global economic growth recovers further, the energy headwind could turn into an energy tailwind.

Record Low Interest Rates

Stocks were not popular during the early 1980s. In fact, the Dow Jones Industrial Average traded at 2,600 in 1980 vs 18,400 today. The economy was much smaller back then, but another significant overhang to lower stock prices was higher interest rates (and inflation). Back in 1980, the Federal Funds target rate set by the Federal Reserve reached a whopping 20.0% versus today the same rate sits at < 0.5%.

Why is this data important? When you can earn a 16.99% yield in a one-year bank CD (see advertisement below), generally there is a much smaller appetite to invest in riskier, more volatile stocks. Another way to think about rates is to equate interest rates to the cost of owning stocks. When interest rates were high, the relative cost to own stocks was also high, so many investors liquidated stocks. It makes perfect sense that stocks in that high interest rate environment of 1980 would be a lot less attractive compared to a relatively safe CD that paid 17% over a 12-month period.

On the other hand, when interest rates are low, the relative cost of owning stocks is low, so it makes sense that stock prices are rising in this environment. Just like profits, interest rates are not static, and they too can change rapidly. But as long as rates remain near record lows, and profits remain healthy, stocks should remain an appealing asset class, especially given the scarcity of strong alternatives.

Skeptical Investing Public

The last piece of the puzzle to examine in order to help explain the head-scratching record stock prices is the pervasive skepticism present in the current stock market. How can Brexit, presidential election, terrorism, negative interest rates, and uncertain Federal Reserve policies be good for stock prices? Investing in many respects can be like navigating through traffic. When everyone wants to drive on the freeway, it becomes congested and a bad option, therefore taking side-streets or detours is a better strategy. The same principle applies to the stock market. When everyone wants to invest in the stock market (like during the late 1990s) or buy housing (mid-2000s), prices are usually too inflated, and shrewd investors decide to choose a different route by selling.

The same holds true in reverse. When nobody is interested in investing (see also, 18-year low in stock ownership and two trillion of stocks sold), then generally that is a strong sign that it is a good time to buy. Currently, skepticism is plentiful, for all the reasons cited above, which is a healthy investment indicator. Many individuals continue reading the ominous headlines and scratching their heads in confusion over today’s record stock prices. In contrast, at Sidoxia, we have opportunistically benefited from investors’ skepticism by discovering plenty of attractive opportunities for our clients. There’s no confusion about that.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and FB, but at the time of publishing had no direct position in TWTR or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Fed: Myths vs. Reality

Traders, bloggers, media talking heads, and pundits of all stripes went into a feverish sweat as they anticipated the comments of Federal Reserve Chairman Janet Yellen at the annual economic summit held in Jackson Hole, Wyoming. When Yellen, arguably the most dovish Fed Chairman in history, uttered, “I believe the case for an increase in the federal funds rate has strengthened in recent months,” an endless stream of commentators used this opportunity to spout out a never-ending stream of predictions describing the looming consequences of such a potential rate increase.

As I’ve stated before, the Fed receives both too much blame and too much credit for basically doing nothing except moving short-term interest rates up or down (and most of the time they do nothing). However, until the next Fed meeting in September (or later), we all will be placed in purgatory with non-stop speculation regarding the timing of the next rate increase.

The ludicrous and myopic analysis can be encapsulated by the recent article written by Pulitzer Prize-winning Fed writer Jon Hilsenrath, in his piece titled, The Great Unraveling: Fed Missteps Fueled 2016 Populist Revolt. Somehow, Hilsenrath is making the case that a group of 12 older, white people that meet eight times per year in Washington to discuss interest rate policy based on inflation and employment trends has singlehandedly created income inequality, and a populist movement leading to the rise of Donald Trump and Bernie Sanders.

While this Fed scapegoat explanation is quite convenient for the doom-and-gloomers (see The Fed Ate My Homework), it is way off base. I hate to break it to Mr. Hilsenrath, or other conspiracy theorists and perma-bears, but blaming a small group of boring bankers is an overly-simplistic “straw man” argument that does not address the infinite number of other factors contributing to our nation’s social and economic problems.

Ever since the bull market began in 2009, a pervasive skepticism and mistrust have kept the bull market climbing a wall of worry to all-time record levels. In the process, Hilsenrath et. al. have proliferated an inexhaustible list of myths about the Fed and its powers. Here are some of them:

Myth #1: The printing of money by the Fed has led to an artificially inflated stock market bubble and Ponzi Scheme.

- As stock prices have more than tripled over the last eight years to record levels, I’ve reveled in the hypocrisy of the “money printers” contention. First of all, the money printing derived from Quantitative Easing (QE) was originally cited as the sole reason for low, declining interest rates and the rising stock market. The money printing community vociferously predicted once QE ended, as it eventually did in 2014, interest rates would explode higher and stock market prices would collapse. What happened? The exact opposite occurred. Interest rates have gone to record low levels, and stock prices have advanced to all-time record highs.

Myth #2: The Fed controls all interest rates.

- Yes, the Fed can influence short-term interest rates through bond purchases and the targeting of the Federal Funds rate. However, the Fed has little-to-no influence on longer-term interest rates. The massive global bond market dwarfs the size of the Fed and U.S. stock market, and as such, large global financial institutions, pensions, hedge funds, and millions of other investors around the world have more influence on longer-term interest rates. The relationship between the 10-Year Treasury Note yield and the Fed’s monetary policy is loose at best.

Myth #3: The stock market will crash when the Fed raises interest rates.

- Well, we can see that logic is already wrong because the stock market is up significantly since the Fed raised interest rates in mid-December 2015. It is true that additional interest rate hikes are likely to occur in our future, but that does not necessarily mean stock prices are going to plummet. Commentators and bloggers are already panicking about a potential rate hike in September. Before you go jump out a window, let’s put this potential rate hike into context. For starters, let’s not forget the “dove of all doves,” Janet Yellen, is in charge and there has only been one rate increase 0f 0.25% over the last decade. As I point out in one of my previous articles (see Fed Fatigue), stock prices increased during the last rate hike cycle (2004 – 2006) when the Fed raised interest rates from 1.0% to 5.25% (the equivalent of another 16 rate hikes of 0.25%). The world didn’t end in 1994 either, when the Fed Funds rate increased from 3% to 6% over a short time frame, and stocks finished roughly flat for the period. Inflation levels remain at relatively low levels, and the Fed has moved less than 10% of recent hike cycles, so now is not the time to panic. Regardless of what the fear mongers say, the Fed and the bull market fairy godmother (Janet Yellen) will be measured and deliberate in its policies and will verify that any policy action is made into a healthy, strengthening economy.

Myth #4: Stimulative monetary policies instituted by the Fed and other central banks will lead to hyperinflation.

- Japan has done QE for decades, and QE efforts in the U.S. and Europe have also disproved the hyperinflation myth. While commentators, pundits, and journalists like to all point and blame Janet Yellen and the Fed for today’s so-called artificially low interest rates, one does not need to be a genius to realize there are other factors contributing to low rates and inflation. Declining interest rates and inflation are nothing new…this has been going on for over 35 years! (see chart below) As I have discussed previously the larger contributors to declining interest rates and disinflation are technology, globalization, and emerging markets (see Why 0% Interest Rates?). By next year, over one-third of the world’s population is expected to own a smartphone (2.6 billion people), the equivalent of a supercomputer in the palm of their hands. Mobile communication, robotics, self-driving cars, virtual & augmented reality, drones, artificial intelligence, drones, biotechnology, and other technologies are dramatically impacting productivity (i.e., downward pressure on prices and interest rates). These advancements, combined with the billions of low-priced workers in emerging markets, who are lifting themselves out of poverty, are contributing to the declining rate/inflation trend.

Source: Calafia Beach Pundit

As the next Fed meeting approaches, there is no doubt the airwaves and internet will be filled with alarmist calls from the likes of Jon Hilsenrath and other Fed-haters. Fortunately, more informed financial market observers will be able to filter out this noise and be able to separate out the many Fed and interest rate myths from the reality.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Brexit-Schmexit

Do you remember the panic-inducing headlines related to PIIGS, Crimea, Ebola, Cyprus, and the Flash Crash? Probably not. But if you do remember, these false alarms have likely been relegated to the financial memory graveyard, along with the many other sensationalist news events that have been killed off in the post-financial crisis era. Time will tell whether Brexit dies off or becomes a resurrected concern, like the repeating fears of a China slowdown or Greek collapse. Regardless, as the S&P 500 stock index reaches new all-time record highs, investors are currently shrug off the noise while muttering, “Brexit-Schmexit.”

Individuals have tried to use scary headlines as a timing tool to consistently time market corrections for all of recorded history. Unfortunately, emotional, knee-jerk reactions to alarming news stories rarely is the best strategy. Famed fund manager Peter Lynch said it best when he noted,

“Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.”

Having invested for some 25 years, experience has taught me not only is conventional wisdom often wrong, but it also is frequently an accurate contrarian indicator. In other words, frightening news often should be an indicator to buy…not sell. Case in point is the U.K. European Union referendum. The Brexit referendum “Leave” vote caught virtually everyone by surprise, but the rebound in stock prices to new record highs may be even more surprising to most observers. However, for investors following the key factors of interest rates, profits, valuation, and sentiment (see also Don’t Be a Fool, Follow the Stool), may not be shocked by the positive price action.

- Interest Rates: For starters, you don’t have to be a genius to realize that stocks become more attractive when there is a scarcity of investment alternatives. When there are an estimated $13 trillion of negative interest rate bonds, a layman can quickly understand a 2%, 3%, or 4% dividend yield offered on certain stocks (and funds) can represent a much more attractive opportunity. With interest rates at record lows (see chart below), the overall dividend yield of stocks has provided a floor for stock prices and has limited the depth and duration of sell-offs and corrections.

Source: Calafia Beach Pundit

- Profits: Corporate profits are near record highs but have been sluggish due to several factors, including the negative impact of the strong dollar on multinational exports; the depressing effect of declining interest rates on the banking sector’s net interest profit margins; the general decline in oil and commodity prices; and general lethargic economic growth overall in international markets (emerging and developed economies). Encouragingly, a stabilization in the value of the U.S. dollar, along with a rebound in energy prices augurs well for a potential shift back to earnings growth in the coming quarters.

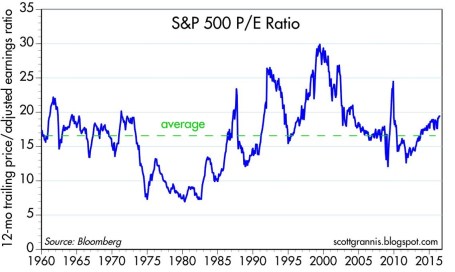

- Valuation: On a valuation basis, the Price/Earnings ratio of the stock market is about 10-15% above historical averages (see chart below). The average S&P 500 stock price trades around 19x’s the value of trailing twelve-month earnings. However, in the context of all-time record low-interest rates, a premium valuation is well deserved, especially for those companies paying a dividend and growing their bottom line.

Source: Calafia Beach Pundit

- Sentiment: Since the Great Financial Crisis / Recession, there has been about $1.5 trillion in equity investments that have been pulled out of U.S. equity mutual funds. This statistic is a clear sign of the extreme risk aversion and pervasive pessimism. Despite money flowing out of equity funds, corporations have bolstered the upward trajectory in stock prices with hundreds of billions in corporate stock buybacks and trillions in mergers & acquisition transactions. With all the universal jitteriness, I like to remind investors of Warren Buffett’s credo, “Buy fear, and sell greed.”

Brexit-Schmexit NOT Brexit-Panic

Despite the risk aversion in the marketplace, stock prices in the U.S. continue to grind higher to record levels. The stock market is currently communicating interest rates, profits, valuation, and sentiment are more important factors to price direction than are Brexit and other geopolitical concerns.

The silver lining behind severe investor skepticism is the creation of additional investment opportunities. As famous investor Sir John Templeton stated regarding stock market cycles, “Bull markets are born on pessimism and they grow on skepticism, mature on optimism, and die on euphoria.” Even the most objective observers have difficulty pointing to a broad set of indicators signaling euphoria, and the recent Turkish military coup attempt and domestic gun violence incidents will not squash out the negativity. Until optimism and elation rule the day, there’s no need to worry-schworry.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds , but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Cleaning Out Your Investment Fridge

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (June 1, 2016). Subscribe on the right side of the page for the complete text.

Summer is quickly approaching, but it’s not too late to do some spring cleaning. This principle not only applies to your cluttered refrigerator with stale foods but also your investment portfolio with moldy investments. In both cases, you want to get rid of the spoiled goods. It’s never fun discovering a science experiment growing in your fridge.

Over the last three months, the stock market has been replenished after a rotten first two months of the year (S&P 500 index was down -5.5% January through February). The +1.5% increase in May added to a +6.6% and +0.3% increase in March and April (respectively), resulting in a three month total advance in stock prices of +8.5%. Not surprisingly, the advance in the stock market is mirroring the recovery we have seen in recent economic data.

After digesting a foul 1st quarter economic Gross Domestic Product (GDP) reading of only +0.8%, activity has been smelling better in the 2nd quarter. A recent wholesome +3.4% increase in April durable goods orders, among other data points, has caused the Atlanta Federal Reserve Bank to raise its 2nd quarter GDP estimate to a healthier +2.9% growth rate (from its prior +2.5% forecast).

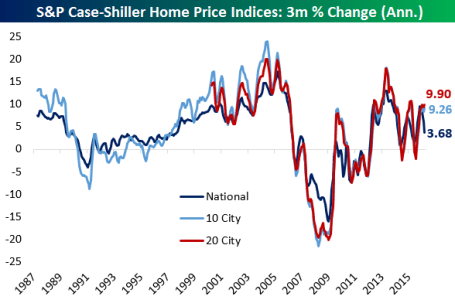

Consumer spending, which accounts for roughly 70% of our country’s economic activity, has been on the rise as well. The improving employment picture (5.0% unemployment rate last month) means consumers are increasingly opening their wallets and purses. In addition to spending more on cars, clothing, movies, and vacations, consumers are also doling out a growing portion of their income on housing. Housing developers have cautiously kept a lid on expansion, which has translated into limited supply and higher home prices, as evidenced by the Case-Shiller indices charted below.

Source: Bespoke

Spoiling the Fun?

While the fridge may look like it’s fully stocked with fresh produce, meat, and dairy, it doesn’t take long for the strawberries to get moldy and the milk to sour. Investor moods can sour quickly too, especially as they fret over the impending “Brexit” (British Exit) referendum on June 23rd when British voters will decide whether they want to leave the European Union. A “yes” exit vote has the potential of roiling the financial markets and causing lots of upset stomachs.

Another financial area to monitor relates to the Federal Reserve’s monetary policy and its decision when to further increase the Federal Funds interest rate target at its June 14th – 15th meeting. With the target currently set at an almost insignificantly small level of 0.25% – 0.50%, it really should not matter whether Chair Janet Yellen decides to increase rates in June, July, September and/or November. Considering interest rates are at/near generational lows (see chart below), a ¼ point or ½ point percentage increase in short-term interest rates should have no meaningfully negative impact on the economy. If your fridge was at record freezing levels, increasing the temperature by a ¼ or ½ degree wouldn’t have a major effect either. If and when short-term interest rates increase by 2.0%, 3.0%, or 4.0% in a relatively short period will be the time to be concerned.

Source: Scott Grannis

Keep a Fresh Financial Plan

As mentioned earlier, your investments can get stale too. Excess cash sitting idly earning next-to-nothing in checking, savings, CDs, or in traditional low-yielding bonds is only going to spoil rapidly to inflation as your savings get eaten away. In the short-run, stock prices will move up and down based on frightening but insignificant headlines. However, in the long-run, the more important issues are determining how you are going to reach your retirement goals and whether you are going to outlive your savings. This mindset requires you to properly assess your time horizon, risk tolerance, income needs, tax situation, estate plan, and other unique circumstances. Like a balanced diet of various food groups in your refrigerator, your key personal financial planning factors are dependent upon you maintaining a properly diversified asset allocation that is periodically rebalanced to meet your long-term financial goals.

Whether you are managing your life savings, or your life-sustaining food supply, it’s always best to act now and not be a couch potato. The consequences of sitting idle and letting your investments spoil away are a lot worse than letting the food in your refrigerator rot away.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Pulling the Band-Aid Off Slowly

Federal Reserve monetary policy once again came to the forefront as the Fed released its April minutes this week. After living through years of a ZIRP (Zero Interest Rate Policy) coupled with QE (Quantitative Easing), many market participants and commentators are begging for a swifter move back to “normalization” (a Federal Funds Rate target set closer to historical averages). The economic wounds from the financial crisis may be healing, as seen in the improving employment data, but rather than ripping off the interest rate Band-Aid quickly and putting the pain behind investors, the dovish Fed Chair Janet Yellen has been signaling for months the Fed will increase rates at a “gradual” pace.

Despite the more hawkish tone regarding the possibility of an additional rate hike in June, Fed interest rate futures are currently still only factoring in about a 26% probability of a rate increase in June. As I have been saying for years (see “Fed Fatigue”), there has, and will likely continue to be, an overly, hyper-sensitive focus on monetary policy and language disseminated by members of the Feral Reserve Open Market Committee.

For example, in 1994, despite the Fed increasing target rates by +2.5% in a single year (from 3.0% to 5.5%), stock prices finished roughly flat for the year, and the market resumed its decade-long bull market run the subsequent year. Today, the higher bound of Fed Funds sits at a mere 0.5%, and the Fed has announced only one target increase this cycle (equaling a fraction of the ’94 pace). Even if investors are panicking over another potential quarter point in June or July, can you say, “overkill?”

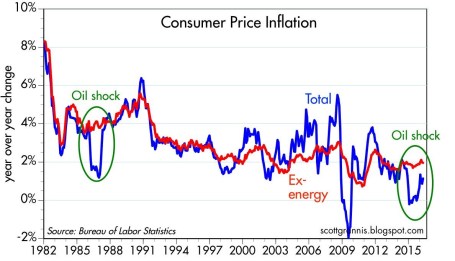

While the Fed is approaching the lower-end of the range for its employment mandate (unemployment currently sitting at 5%), despite the recent bounce in oil prices, core inflation remains in check (see Calafia Pundit chart below). This long-term benign pricing trend gives the Fed a longer leash as it relates to the pace of future rate hikes.

Source: Calafia Beach Pundit

Sure, ripping off the Fed Band-Aid with a small handful of +0.5% (50 bps) hikes might appease hawkish investors, but Janet Yellen, the “Fed Fairy Godmother,” has made it abundantly clear she is in no hurry to raise rates. Whether there is zero, one, or two additional rate hikes this year is much less important than other fundamental factors. Adding fuel to the Fed-speak fire in the short-run will be Yellen speeches on May 27th at Harvard University and on June 6th at the World Affairs Council of Philadelphia. And then following that, we will have the “Brexit” referendum (i.e., the vote on whether Britain should exit the EU); a steady stream of election noise; and many other unanticipated economic/geopolitical headlines.

As I continually state, the key factors driving the direction of long-term stock prices are profits, interest rates, valuations, and sentiment (see Follow the Stool). Profits (ex-energy) are growing near record levels; interest rates are near record lows (even with potential 2016 hikes); valuations remain near historical averages; and sentiment regarding stock ownership is firing strongly as a positive contrarian indicator.

While many pundits have been calling for and predicting the Fed to rip the Band-Aid off with a swift string of rate increases, persistently low inflation, coupled with a consistently dovish Fed Chair are likely to lead to a slow peeling of the monetary policy Band-Aid. Unfortunately, the endless flow of irrelevant monetary policy guesswork regarding the timing of future rate hikes will be more painful than the actual hikes themselves. In the end, any future hikes should be justified with a stronger economic foundation, which should represent future strength, rather than future weakness.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Yield Starving Foreigners Go Muni Hunting

In the current cold, barren, negative interest rate environment, foreign investors are getting hungry and desperate as they hunt for yield. In the hopes of kick-starting economic activity around the globe, central bankers are taking the drastic measure of establishing negative interest rate policies. This unusual endeavor is pressing international investors to chase yield, no matter how small, wherever they can find it.

One of those areas in which foreigners are hunting for yield is the U.S. municipal bond market (see FT article). On the surface, this sounds ludicrous. Why would an outsider living in Germany or Japan invest in a U.S. municipal bond that yields a paltry rate that’s less than 1.7%, especially considering those investors will not benefit from the tax-free income advantages offered to Americans?

As strange as it sounds, Natalie Cohen, Wells Fargo’s head of municipal research correctly pointed out this pursuit for municipal bond yield across continents boils down to simple math. “Even if [foreign investors] are not subject to the US tax code, a plus two is better than a minus one,” Cohen notes.

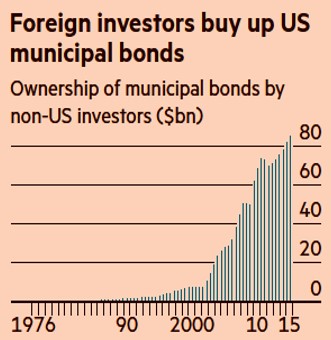

Although foreign investment in the $3.7 trillion municipal bond market is relatively small, the rapidly rising appetite for munis is clearly evident, as shown in the chart below.

Source: The Financial Times

With our country’s crumbling roads and bridges, these ever-increasing piles of foreign cash pouring into our municipal bonds are helping fund a broad array of U.S. infrastructure projects. Given the election season is upon us, this issue may gain heightened attention. Both likely-presidential candidates are highlighting the need for infrastructure investment as part of their platforms, and the NIRP (negative interest rate policies) agenda of international central banks may make these municipal infrastructure dreams a reality.

We Americans are no stranger to the idea of borrowing money from foreigners. In fact, the Chinese own about $1.3 trillion of our Treasury bonds. This is all fine and dandy as long as the international appetite for lending us money remains healthy. If our city, state, and federal governments become too addicted to the Chinese, Europeans, and Japanese loans, financial risks can/will grow to unmanageable levels. Guess what happens once our borrowings swell to a level that forces foreigners to question our ability of repaying their debt? Interest rates will accelerate upwards, our interest payments will balloon, and our deficits will widen. The consequences of these unfavorable outcomes will be devastating budget cuts and/or tax increases.

For the time being, we will gladly accept the charitable donations of foreign investors to help lower funding costs for our sorely needed infrastructure projects. Fortunately, for now fiscal sanity is prevailing. The post financial crisis political environment has scared municipalities from borrowing too much, as explained here by the FT:

“For local and state politicians grappling with pension reforms, new healthcare programs and — in Alaska, Texas and Oklahoma — a drag on finances from lower energy prices, the looming presidential election is also diminishing the appeal of [municipal debt] issuance.”

In a near-zero/negative rate environment, there certainly will be incentives for irresponsible governments and corporations to extend themselves too far with cheap debt. However, in the short-run, as starving foreigners hunt for yield in the U.S. municipal bond market, Americans have the opportunity of exploiting this foreign generosity for the benefit our country’s long-term infrastructure.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}

{kind=link}