Posts tagged ‘headlines’

End of the World or Status Quo?

If you were the chief executive of a newspaper, television, or magazine company, what headline stories would you run to generate the most viewers and readers? Which subjects will you choose to make me impulsively grab a magazine in the grocery line, keep me glued to the television news, or suck me in to click-bait advertisements on the web? For example, what topics below would you select to grab the most attention?

· Hurricane or Sunshine?

· High Speed Car Chase or Cat Saved from Tree?

· Bloody Murder or Baby’s Birthday?

· Messy Divorce or Wedding Celebration?

· Impeachment or Bipartisan Legislation

· End of the World or Status Quo?

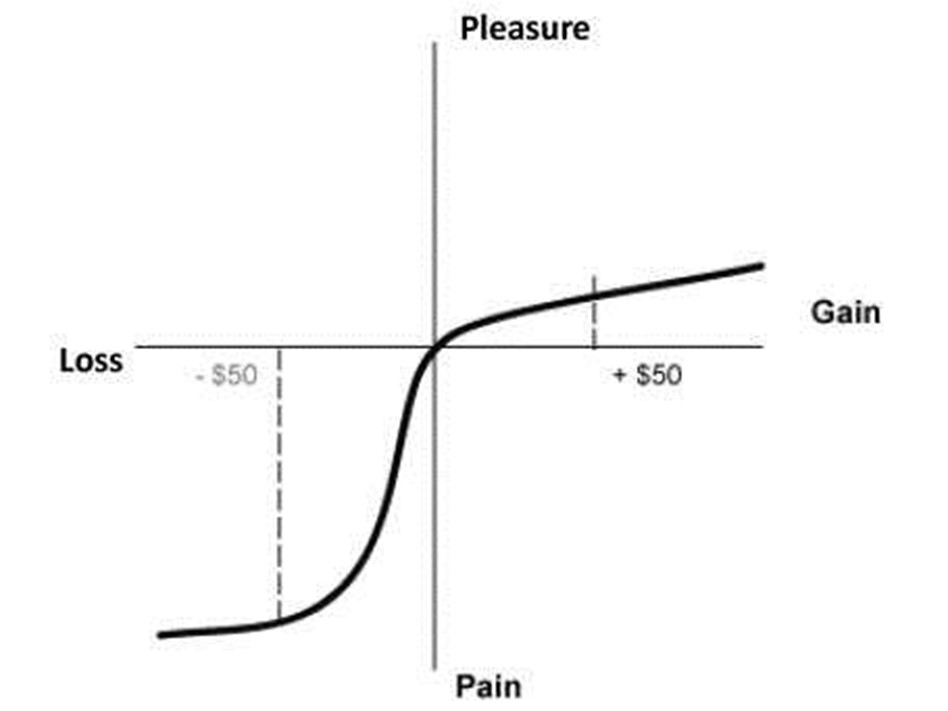

If you selected the first subject in each pair above, you would likely gain much more initial interest. In choosing a winning topic, the saying goes, “what bleeds, leads.” In other words, scary or controversial stories always grab more attention than feel-good or status quo narratives. And that is why the vast majority of media outlets are drawn to negativity, just as mosquitos are attracted to bug zappers. This phenomenon can be explained in part with the help of Nobel Prize winner Daniel Kahneman and his partner Amos Tversky, who conducted research showing the pain from losses is more than twice as painful as are the pleasures experienced from gains (see chart below).

The significant volatility seen in the stock market recently from the Russian war/invasion of Ukraine is further evidence of how this fear dynamic can create short-term panics.

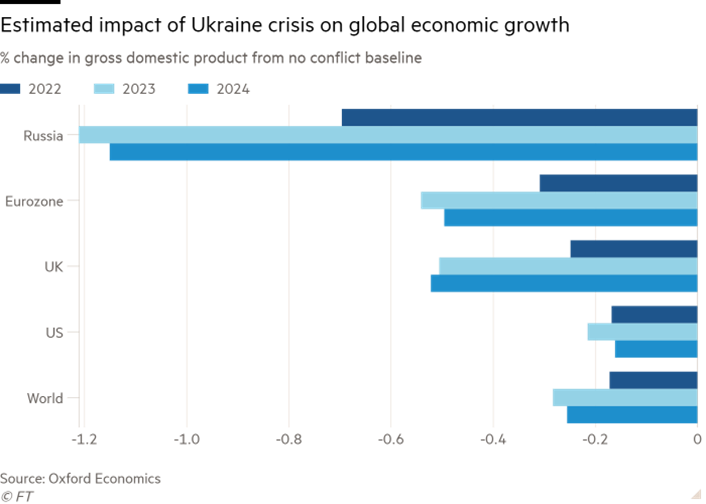

Although the stock market as measured by the S&P 500 index has gone gangbusters over the last three years, almost doubling in value (2019: +29%, 2020: +16%, 2021: +27%), the S&P 500 has hit an air pocket during the first couple months of 2022 (-8%), including down -3% in February. The year started with turbulence as investors became fearful of a Federal Reserve that is entering the beginning stages of interest rate hikes while cutting stimulative bond purchases. And then last month, the Russian-Ukrainian incursion made investors even more skittish. Like always, these geopolitical events tend to be short-lived once investors realize the impact turns out to be less meaningful than initially feared. As you can see below, the worst economic impact is forecasted to be felt by Russia (consensus on 2/24/22 of approximately a -1.0% hit to economic growth), more than twice as bad as the -0.2% to -0.4% knock to growth for the U.S., Europe, and the world (see chart below). The Russian hit will likely be worse after accelerated sanctions.

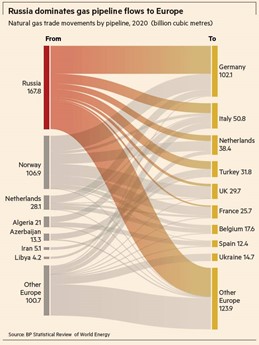

As it relates to Ukraine, many Americans don’t even know where the country is located on a map. Ukraine accounts for about only 0.14% of total global GDP (i.e., a rounding error and less than 1% of total global economic activity). Russia, although larger than Ukraine, is still a relative small-fry and represents only about 3% of total global economic activity. If you live in Europe during the winter, you might be a little more concerned about Vladimir Putin’s recent activities because a lot of Europe’s energy (natural gas) is supplied by Russia through Ukraine. For example, Germany receives about half of its natural gas from Russia (see chart below).

Russia, on the other hand, is larger than Ukraine, but the red country is still a relative small-fry representing only about 3% of total global economic activity. When it comes to energy production however, Russia is more than a rounding error because the country accounts for about 11% of global energy production (#3 country globally behind the United States and Saudi Arabia). By taking all these factors into account, we can confidently state that Russia and Ukraine have a very low probability of solely pulling the global economy into recession.

If history repeats itself, this conflict will turn out to be another garden variety decline in the stock market and an opportunity to buy at a discount. It’s virtually impossible to predict a short-term bottom in stock prices has been reached, but over the long-run, stock investors have been handsomely rewarded for not panicking and staying invested (see chart below).

At the end of the day, the daily headlines will continually attempt to sell the negative story that the world is coming to an end. If you have the fortitude and discipline to ignore the irrelevant noise, the status quo of normal volatility can create more exciting opportunities and better returns for long-term investors.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (March 1, 2022). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Chasing Headlines

It’s been an amazing start to the year. First the market cratered on slowing China economic concerns, domestic recessionary fears, deteriorating oil prices, and negative interest rates abroad. In response to all these worries (and others), stocks dove more than -11% (S&P 500 Index) in January, before settling down. Subsequently, the market has made a screaming recovery, in part due to dovish monetary policy comments (i.e., reduction in forecasted interest rate hikes) and diminished anxiety over a potential global collapse. Month-to-date stocks are up an impressive +5.4%, and year-to-date equities are flattish, or down less than -1%.

With an endless amount of information flowing across our smart phones and computers, it becomes quite easy and tempting to chase news headlines, just like a hyper dog chasing a car. But even once an investor catches up (or reacts) to a headline, there’s confusion around how to profit from the fleeting information. First of all, every plugged-in hedge fund and institutional investor has likely already traded on the stale information you received. Second of all, rarely is the data relevant to the long-term cash generating capabilities of the company or economy. And lastly, the news is more often than not, instantly factored into the stock price. Chasing news headlines only eaves individual investors holding the bag of performance-shattering transactions costs, taxes, and worn-out pricing.

The heightened volatility in late 2015 and early 2016 hasn’t however prevented investors and so-called pundits from attempting to time the market. Any battle-tested investment veteran knows it’s virtually impossible to consistently time the market (see also Market Timing Treadmill), but this fact hasn’t prevented speculators from attempting the feat nonetheless. Famed investment guru, Peter Lynch, who earned an average +29% annual return from 1977-1990, summed it up well when he stated the following:

“Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.”

The Important Factors

As I’ve written many times in the past, the keys to long-term stock performance are not knee-jerk reactions to headlines, but rather these following crucial factors (see also Don’t Be a Fool, Follow the Stool):

- Profits

- Interest Rates

- Sentiment

- Valuations

On the profit growth front, corporate income has been pressured by numerous headwinds over the last few years, including an export-shattering increase in the value of the U.S. dollar and a profit-squeezing collapse in energy sector earnings. As you can see from the chart below, the value of the U.S. dollar increased by about 25% from mid-2014 to early-2015, in part because of diverging global central bank policies (more hawkish U.S. Fed vs. more dovish ECB/international central banks). Since that spike, the dollar has settled into a broad range (95 – 100), and the former forceful headwind have now turned into modest tailwinds. This trend is important because an estimated 35-40% of corporate profits are derived from international operations.

Adding insult to injury, the roughly greater than -70% decline in forward energy earnings over the last 18 months has caused a significant hit to overall S&P 500 profits. The tide appears to be finally turning (or at least stabilizing) however, as we’ve seen oil prices rebound by about +30% this year from the lows in January. If these aforementioned trends persist, profit pressures in 2016 are likely to abate significantly, and may actually become additive to growth.

Source: Barchart.com

Profits are important, but so are interest rates. While incessant talk about the path of future Fed policy continues to blanket the airwaves (see also Fed Fatigue), absent a rapid increase in interest rates (say 300-400 basis points), interest rates remain unambiguously positive for equity markets, providing a floor for the oft-repeated volatility in financial markets. As long as stocks are providing higher yields than many bonds, and depositors are earning 0% (or negative rates) on their checking accounts, stocks may remain unloved, but not forgotten.

And speaking of unloved, the sentiment for stocks remains sour. One need look no further than the quarter-billion dollars in hemorrhaging outflows out of U.S. equity funds (see ICI Long-Term Mutual Fund Flows) since 2014. This deep underlying skepticism serves as a positive contrarian indicator for future equity prices. Right now, very few individual investors are swimming in the pool – the time to get out of the stock market pool is when everyone is jumping in.

And lastly, valuations remain very much in line with historical averages (approximatqely 17x 2016 projected earnings), especially considering the generational low in interest rates. Bears continue to point to the elevated CAPE ratio, which has been a disastrous indicator the last seven years (and longer), as a reason to remain cautious. The ironic part is that valuations are virtually guaranteed to improve a few years from now as we roll off the artificially depressed years of 2008-2010.

When you add it all up, zero (or negative) interest rates, combined with the other key factors of profits, sentiment, and valuations, equities remain an important and attractive part of a diversified long-term portfolio. Your objectives, time horizon, and risk tolerance will always drive the proportion of your equity allocation. Nevertheless, some bond exposure is essential to smooth out volatility. Regardless of your investment strategy, chasing headlines, like a dog chasing a car, serves no purpose other than leaving you with a tired, unproductive investment portfolio.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Confusing Fear Bubbles with Stock Bubbles

With the Dow Jones Industrial Average approaching and now breaking the 16,000 level, there has been a lot of discussion about whether the stock market is an inflating bubble about to burst due to excessive price appreciation? The reality is a fear bubble exists…not a valuation bubble. This fear phenomenon became abundantly clear from 2008 – 2012 when $100s of billions flowed out of stocks into bonds and trillions in cash got stuffed under the mattress earning near 0% (see Take Me Out to the Stock Game). The tide has modestly turned in 2013 but as I’ve written over the last six months, investor skepticism has reigned supreme (see Most Hated Bull Market Ever & Investors Snore).

Volatility in stocks will always exist, but standard ups-and-downs don’t equate to a bubble. The fact of the matter is if you are reading about bubble headlines in prominent newspapers and magazines, or listening to bubble talk on the TV or radio, then those particular bubbles likely do not exist. Or as strategist and investor Jim Stack has stated, “Bubbles, for the most part, are invisible to those trapped inside the bubble.”

All the recent bubble talk scattered over all the media outlets only bolsters my fear case more. If we actually were in a stock bubble, you wouldn’t be reading headlines like these:

From 1,300 Bubble to 5,000

If you think identifying financial bubbles is easy, then you should buy former Federal Reserve Chairman Alan Greenspan a drink and ask him how easy it is? During his chairmanship in late-1996, he successfully managed to identify the existence of an expanding technology bubble when he delivered his infamous “irrational exuberance” speech. The only problem was he failed miserably on his timing. From the timing of his alarming speech to the ultimate pricking of the bubble in 2000, the NASDAQ index proceeded to more than triple in value (from about 1,300 to over 5,000).

Current Fed Chairman Ben Bernanke was no better in identifying the housing bubble. In his remarks made before the Federal Reserve Board of Chicago in May 2007, Bernanke had this to say:

“…We believe the effect of the troubles in the subprime sector on the broader housing market will likely be limited, and we do not expect significant spillovers from the subprime market to the rest of the economy or to the financial system. The vast majority of mortgages, including even subprime mortgages, continue to perform well.”

If the most powerful people in finance are horrible at timing financial market bubbles, then perhaps you shouldn’t stake your life’s savings on that endeavor either.

Bubbles History 101

Each bubble is unique in its own way, but analyzing previous historic bubbles can help understand future ones (see Sleeping Through Bubbles):

• Dutch Tulip-Mania: About 400 years ago in the 1630s, rather than buying a new house, Dutch natives were paying over $60,000 for tulip bulbs.

• British Railroad Mania: The overbuilding of railways in Britain during the 1840s.

• Roaring 20s: Preceding the Wall Street Crash of 1929 (-90% plunge in the Dow Jones Industrial average) and Great Depression, the U.S. economy experienced an extraordinary boom during the 1920s.

• Nifty Fifty: During the early 1970s, investors and traders piled into a set of glamour stocks or “Blue Chips” that eventually came crashing down about -90%.

• Japan’s Nikkei: The value of the Nikkei index increased over 450% in the eight years leading up to the peak of 38,957 in December 1989. Today, almost 25 years later, the index stands at about 15,382.

• Tech Bubble: Near the peak of the technology bubble in 2000, stocks like JDS Uniphase Corp (JDSU) and Yahoo! Inc (YHOO) traded for over 600x’s earnings. Needless to say, things ended pretty badly once the bubble burst.

As long as humans breathe, and fear and greed exist (i.e., forever), then we will continue to encounter bubbles. Unfortunately, we are unlikely to be notified of future bubbles in mainstream headlines. The objective way to unearth true economic bubbles is by focusing on excessive valuations. While stock prices are nowhere near the towering valuations of the technology and Japanese bubbles of the late 20th century, the bubble of fear originating from the 2008-2009 financial crisis has pushed many long-term bond prices to ridiculously high levels. As a result, these and other bonds are particularly vulnerable to spikes in interest rates (see Confessions of a Bond Hater).

Rather than chasing bubbles and nervously fretting over sensationalistic headlines, you will be better served by devoting your attention to the creation of a globally diversified investment portfolio. Own a portfolio that integrates a wide range of asset classes, and steers clear of popularly overpriced investments that the masses are talking about. When fear disappears and everyone is clamoring to buy stocks, you can be confident the stock bubble is ready to burst.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in TWTR, JDSU, YHOO or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Hammering Heads with Circular Conversations

This article is an excerpt from a previously released Sidoxia Capital Management complementary newsletter (July 1, 2013). Subscribe on the right side of the page for a complete monthly update.

Deciphering what is driving the markets on a day-to-day, week-to-week, or month-to-month basis can feel like repeatedly hammering your head. In order to grasp the reasons why financial markets go up and down, one must have a conversation with your brain explaining that good news can be bad for asset prices, and bad news can be good for asset prices. Huh…how can that be? These circular conversations are what keep newspapers, magazines, media commentators, and bloggers in business… and what baffle many investors.

For example, headlines often reflect sentiments such as these:

- “Unemployment Figures Disappoint…Dow Jones Rallies +200 Points on QE3 Continuation Hopes”

- “Unemployment Figures Delight…Dow Jones Tanks -200 Points on QE3 Discontinuation Fears”

- “Economic Figures Revised Lower by -0.2%…Dow Jones Skyrockets +200 Points as Lower Interest Rates Propel Stock Prices.”

- “Economic Figures Revised Higher by +0.2%…Dow Jones Plummets -200 Points as Higher Interest Rates Deflate Stock Prices.”

On rare occasions these headlines make sense, but often online media outlets are frantically changing the headlines as the markets whip back and forth from positive to negative. News-producing editors are continually forced to create ludicrous and absurd explanations that usually make no sense to informed long-term investors.

It’s important to recognize that if the financial markets made common sense, then investing for retirement would be simple and everyone would be billionaires. Unfortunately, financial markets frequently make no sense in the short-run. Stocks are volatile (often times for no rational reason), which is why stocks offer higher returns over the long-run relative to more stable asset classes.

Explaining the latest spike in stock/bond price volatility has been exacerbated in recent weeks as a result of the nation’s banker (the Federal Reserve) and its boss, Ben Bernanke, attempting to explain their future monetary policy plans. In theory, bringing light to a traditionally mysterious, closed-door Washington process should be a good thing…right?

Well, ever since a few weeks ago when Ben Bernanke and the FOMC (Federal Open Market Committee) disclosed that the stimulative bond buying program (QE3) could be slowed in 2013 and halted in 2014, financial markets globally experienced a sharp jolt of volatility – stock prices dropped and interest rates spiked. Counter-intuitively, Bernanke’s belief that the economy is on a sustained recovery path (expected GDP growth of +3.25% in both 2014 & 2015) spooked investors. More specifically, in the month of June, the S&P 500 index declined -1.5% in June; Dow Jones Industrial Index -1.4%; and the 10-year Treasury note’s yield jumped +0.3% to 2.5%. Greedy investors, however, should not forget that the stock market just posted its 2nd best quarter since 2009 – the S&P 500 climbed +2.4%. What’s more, the S&P 500 is up +13% and the Dow up +14% in the first half of 2013.

Bernanke Threatening to Take Away Investor Lollipops

Another way of looking at the recent volatility is by equating investors to kids and stimulative QE bond buying programs (Quantitative Easing) to lollipops. If the economy continues on this improvement trajectory (i.e., unemployment falls to 7% by next year) and inflation remains benign (below 2.5%), then Bernanke said he will take away investors’ QE lollipops. But like a pushover dad being pressured by kids at the candy store, Bernanke acknowledged that he could continue supplying investors QE lollipops, if the economic data doesn’t improve at the forecasted pace. At face value, receiving a specific timeline given by the Fed should be appreciated and normally people are happy to hear the Chairman speak rosily about the economy’s future. However, the mere thought of QE lollipops being taken away next year was enough to push investors into a “taper tantrum” (see also Investing Caffeine – Fed Fatigue article).

With scary headlines constantly circulating, a large proportion of investors are sitting on their hands (and cash) while staring like deer in headlights at these developments. Rather than a distracted driver texting, investors should be watching the road and mapping out their future investment destinations – not paying attention to irrelevant diversions. Astute investors realize that uncertainty surrounding Greece, Cyprus, fiscal cliff, sequestration, presidential elections, Iran, N. Korea, Syria, Turkey, taxes, QE3, etc., etc., etc., have been a constant. Regrettably the fear mongers paying attention to these useless headlines have witnessed their cash, gold, and Treasuries get trounced by equity returns since early 2009 (the S&P 500 index is up about +150%, including dividends). Optimists and realists, on the other hand, have seen their investment plans thrive. While the aforementioned list of concerns has dangled in front of our noses over the last year, we will have a complete new list of concerns to decipher over the coming weeks, months, and years. That’s the price a long-term investor pays if they want to earn higher returns in the volatile equity markets.

As strategist Don Hays points out, “Nothing is certain. Good investors love uncertainty.” Rather than getting consumed by fear with the endless number of changing uncertainties, the real risk for investors is outliving your savings. Paychecks are being stretched by inflationary pressures across all categories (e.g., healthcare, gasoline, utilities, food, movies, travel, etc.) and entitlements like Social Security and Medicare will likely not mean the same thing to us as it did for our parents. Unless investors plan on working into their 80s as greeters at Wal-Mart, and/or enjoy clipping Top Ramen coupons in a crammed apartment, then they should do themselves a favor by taking a deep breath and turning off the television, so they can be insulated from the constant doom and gloom.

So as intimidating, circular conversations about good news being bad news, and bad news being good news continue to swirl around, focus instead on building a diversified investment plan that can adjust and adapt to the never-ending list of uncertainties. Your head will feel a lot better than it would after repetitive hammer strikes.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and WMT, but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Dow Déjà Vu – Shining Rainbow or Bad Nightmare?

Excerpt from Free January Sidoxia Monthly Newsletter (Subscribe on right-side of page)

The Dow Jones Industrial Average is sitting at 11,577 points. Dick Fuld is still CEO of Lehman Brothers, AIG is still trading toxic CDS derivative contracts, and the $700 billion TARP bailout is a pre-idea about to be invented in the brain of Treasury Secretary Hank Paulson. Oops, wait a second, this isn’t the Dow 11,577of September 2008, but rather this is the Dow 11,577 of December 2010 (+11% for the year, excluding dividends). Was the -50% drop we experienced in the equity markets during 2008-2009 all just a bad dream? If not, how in the heck has the stock market climbed spectacularly? Most people don’t realize that stocks have about doubled over the last 21 months (and up roughly +20%-25% in the last 6 months) – all in the face of horrendously depressing news swirling around the media (i.e., jobs, debt, deficits, N. Korea, Iran, “New Normal,” etc.). Market volatility often does not make intuitive sense, and as a result, many market observers have been caught flat-footed.

Here are a few basic factors that average investors have not adequately appreciated:

1) Headlines are in Rearview Mirror: News that everyone reads in newspapers and magazines and hears on the television and radio is all backward looking. It’s always best to drive while looking forward through the windshield and try to anticipate what’s around the corner – not obsess with backward looking activity in the rearview mirror. That’s how the stock market works – tomorrow’s news (not yesterday’s or today’s) is what drives prices up or down. As the economy teetered on the verge of a “Great Depression-like” scenario in 2008-2009, investors became overly pessimistic and stocks became dramatically oversold. More recently, news has been perking up. Previous recessions have seen doubters slowly convert to believers and push prices higher – eventually stocks become overbought and euphoria slows the bull market. I believe we are in phase II of this three-part economic recovery.

2) Ignore Emerging Markets at Own Peril: We Americans tend to wear blinders when it comes to focusing on domestic issues. We focus more on healthcare reform and political issues, such as “Don’t Ask, Don’t Tell,” rather than the billions of foreigners chasing us as they climb the global economic ladder. Citizens in emerging markets are more concerned about out-competing and out-innovating us through educated workforces, so they can steal our jobs and buy more toasters, iPods, and cars – things we Americans have already taken for granted. The insatiable appetite of the expanding global middle class for a better standard of living is also driving ballooning commodity prices – everything from coal to copper and corn to cotton (the 4 Cs). This universal sandbox that we play in offers tremendous opportunities to grasp and tremendous threats to avoid, if investors open their eyes to these emerging market trends.

3) Capital Goes Where it’s Treated Best: Many voters are fed-up with the political climate in Washington and the sad state of economic affairs. The great thing about the global capitalistic marketplace we live in is that it does not discriminate – capital flows to where it is treated best. On a macro basis, money flows to countries that are fiscally responsible, support pro-growth initiatives, harbor educated work forces, control valuable natural resources, and honor the rule of law. On a micro basis, money flows to companies that are attractively priced and/or capable of sustainably growing earnings and cash flow. Voters and politicians will ultimately figure it out, or capital will go where it’s treated best.

Today’s Dow 11,577 is no bad dream, but rather resembles the emergence of a bright shining rainbow after a long, cold, and dark storm. The rainbow won’t stick around forever, but if investors choose to ignore the previously mentioned factors, like so many investors have overlooked, portfolio performance may turn into an ugly nightmare.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, AAPL, and an AIG derivative security, but at the time of publishing SCM had no direct position in GS, any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}