Posts tagged ‘globalization’

Investors Slowly Waking to Technology Tailwinds

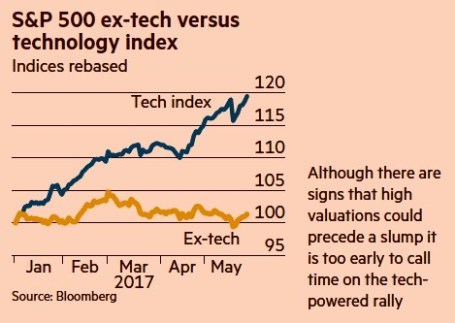

In recent years, investors have been overwhelmingly been distracted by geopolitical headlines and risk aversion caused by the worst financial crisis in a generation. In the background, the tailwinds of technological innovation have been silently gaining momentum. Although this topic is nothing new for Investing Caffeine followers, the outperformance of technology stocks has been pretty stunning in 2017 (see chart below), with the S&P 500 Technology sector rising almost +20% versus the Non-Tech sector eking out a little more than +1% return. Peered through the style lenses of Growth versus Value, technology’s contribution is also evident by the Russell 1000 Growth index’s 2017 outperformance over the Russell 1000 Value index by +11% (approximately +14% vs +3%, respectively).

Source: Bloomberg via The Financial Times

More specifically, what’s driving a significant portion of this outperformance? Robin Wigglesworth from The Financial Times highlighted a key contributing trend here:

“Facebook, Apple, Amazon and Netflix have all gained over 30 per cent this year, and Google is up 24 per cent. Their total market capitalisation now stands at $2.4 trillion. That makes them bigger than the French CAC 40 or Germany’s Dax, and nearly as large as the FTSE 100.”

Technology’s domination has been even more impressive since the cycle bottom of stock prices in 2009, if one contrasts the stark difference in the performance of the tech-heavy NASDAQ versus the more sector-balanced S&P 500. Over this timeframe, the NASDAQ has more than quadrupled in value and beaten the S&P 500 by more than +120%.

While the mass media likes to talk about technology bubbles, artificial money printing by global central banks, and imminent recessions, for years I have been highlighting the importance of the technology revolution and its beneficial impact on stock prices. Here are a few examples:

Technology Does Not Sleep in a Recession (2009)

Technology Revolution Raises Tide (2010)

NASDAQ and the R&D Tech Revolution (2014)

NASDAQ 5,000…Irrational Exuberance Déjà Vu? (2014)

The Traitorous 8 and Birth of Silicon Valley (2016)

As I have explained in many of my previous writings, the important factors of technology, globalization, and demographics have been the key driving forces behind the stock bull market and multi-decade decline in interest rates – not Quantitative Easing (QE) and/or rising debt levels.

Eventually, undoubtedly, euphoria and over-investment will lead to a cyclically-driven recession caused by excess capacity (supply exceeding demand). Regardless of the timing of future economic cycles, the continued multi-generational advance in new technological innovations will continue to drive economic growth, disinflation, improved standards of living, and higher stock prices. Until the animal spirits of the masses fully embrace this technological trend, Sidoxia and its clients will enjoy the tailwind of innovation as I continue to discover attractive investment opportunities.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own FB, AAPL, AMZN, GOOG/L, certain exchange traded funds, and short position in NFLX, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Sweating Your Way to Investment Success

There are many ways to make money in the financial markets, but if this was such an easy endeavor, then everybody would be trading while drinking umbrella drinks on their private islands. I mean with all the bright blinking lights, talking baby day traders, and software bells and whistles, how difficult could it actually be?

Unfortunately, financial markets have a way of driving grown men (and women) to tears, usually when confidence is at or near a peak. The best investors leave their emotions at the door and follow a systematic disciplined process. Investing can be a meat grinder, but the good news is one does not need to have a 90% success rate to make it lucrative. Take it from Peter Lynch, who averaged a +29% return per year while managing the Magellan Fund at Fidelity Investments from 1977-1990. “If you’re terrific in this business you’re right six times out of 10,” says Lynch.

Sweating Way to Success

If investing is so tough, then what is the recipe for investment success? As the saying goes, money management requires 10% inspiration and 90% perspiration. Or as strategist and long-time investor Don Hays notes, “You are only right on your stock purchases and sales when you are sweating.” Buying what’s working and selling what’s not, doesn’t require a lot of thinking or sweating (see Riding the Wave), just basic pattern recognition. Universally loved stocks may enjoy the inertia of upward momentum, but when the music stops for the Wall Street darlings, investors rarely can hit the escape button fast enough. Cutting corners and taking short-cuts may work in the short-run, but usually ends badly.

Real profits are made through unique insights that have not been fully discovered by market participants, or in other words, distancing oneself from the herd. Typically this means investing in reasonably priced companies with significant growth prospects, or cheap out-of-favor investments. Like dieting, this is easy to understand, but difficult to execute. Pulling the trigger on unanimously hated investments or purchasing seemingly expensive growth stocks requires a lot of blood, sweat, and tears. Eating doughnuts won’t generate the conviction necessary to justify the valuation and excess expected return for analyzed securities.

Times Have Changed

Investing in stocks is difficult enough with equity fund flows hemorrhaging out of investor accounts like the asset class is going out of style. Stocks’ popularity haven’t been helped by the heightened volatility, as evidenced by the multi-year trend in the schizophrenic volatility index (VIX) – escalated by the international geopolitics and presidential elections. Globalization, which has been accelerated by technology, has only increased correlations between domestic market and international markets. In decades past, concerns over economic activity in Iceland, Dubai, and Greece may not even make the back pages of The Wall Street Journal. Today, news travels at the speed of a “Tweet” and eventually results in a sprawling front page headline.

The equity investing game may be more difficult today, but investing for retirement has never been more important. Stuffing money under the mattress in Treasuries, money market accounts, CDs, or other conservative investments may feel good in the short run, but will likely not cover inflation associated with rising fuel, food, healthcare, and leisure costs. Regardless of your investment strategy, if your goal is to earn excess returns, you may want to check the moistness of your armpits – successful long-term investing requires a lot of sweat.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in ETFC, VXX, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Don’t Fear the Free Trade Boogeyman

Are you having trouble falling asleep because of a ghostly nightmare? Donald Trump, along with a wide range of pundits and investors have been afraid of globalization and the free trade boogeyman. Donald Trump may or may not win the presidential election, but regardless, his inflammatory rhetoric regarding trade is way off base.

Free trade has been demonized as a job destroyer, however history paints a different picture. I have written on the subject before (see also Invisible Benefits of Free Trade), but with Americans digesting the current debates and the election only a month away, let me make a couple of key points.

Standard of Living Benefits: For centuries, the advantages of free trade and globalization have lifted the standards of living for billions of people. There is a reason the World Trade Organization (WTO) has united more than 160 countries without one country exiting since the global trade group began in 1948. Trade did not suddenly stop working when the Donald began lashing out against NAFTA, TPP and Oreo cookies. Trump rails against trade despite Trump ties being made in China.

Job losses are easy to identify (like the Oreo jobs moved to Mexico from Chicago), but most trade benefits are often invisible to the untrained eye. As Dan Ikenson of the Cato Institute explains, if low-wage labor was not used offshore to manufacture products sold to Americans, many amazing and spectacular products and services would become unaffordable for the U.S. mass markets. Thanks to cheaper foreign imports, not only can a wider population buy iPhones and use services like Uber and Airbnb, but consumers will have extra discretionary income resources that can be redeployed into savings. Alternatively, the extra savings could be spent on other goods and services to help spur U.S. economic growth in various sectors of our nation.

It doesn’t make for a nice, quick political soundbite, but Ikenson highlights,

“The benefits of trade come from imports, which deliver more competition, greater variety, lower prices, better quality, and new incentives for innovation.”

Strong Companies Hire and Grow: Plain and simply, profitable businesses hire employees, and money-losing companies fire employees. Business success boils down to competitiveness. If your product is not better and/or cheaper than competitors, then you will lose money and be forced into stagnation, or worse, be forced to fire employees or shut down your business. Free trade affords businesses the opportunity to improve the cost or quality of a product. Take Apple Inc. (AAPL) for example, the company’s ability to build a global supply chain has allowed the company to offer products and services to more than 1 billion users. If Apple was forced to manufacture exclusively in the U.S., the company’s sales and profits would be lower, and so too would the number of U.S. Apple employees.

Fortunately, no matter who gets elected president, if the rhetoric against free trade reaches a feverish pitch, investors can rest assured that the president’s powers to implement widespread tariffs and rip up longstanding trade deals is limited. He/she will still be forced to follow the authority of Congress, which still controls the nuts and bolts of our economy’s trade policies. In other words, there is nothing to fear…even not the free trade boogeyman.

Other Trade Related Articles on Investing Caffeine:

Jumping on the Globalization Train

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and AAPL, MDLZ, but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Fed: Myths vs. Reality

Traders, bloggers, media talking heads, and pundits of all stripes went into a feverish sweat as they anticipated the comments of Federal Reserve Chairman Janet Yellen at the annual economic summit held in Jackson Hole, Wyoming. When Yellen, arguably the most dovish Fed Chairman in history, uttered, “I believe the case for an increase in the federal funds rate has strengthened in recent months,” an endless stream of commentators used this opportunity to spout out a never-ending stream of predictions describing the looming consequences of such a potential rate increase.

As I’ve stated before, the Fed receives both too much blame and too much credit for basically doing nothing except moving short-term interest rates up or down (and most of the time they do nothing). However, until the next Fed meeting in September (or later), we all will be placed in purgatory with non-stop speculation regarding the timing of the next rate increase.

The ludicrous and myopic analysis can be encapsulated by the recent article written by Pulitzer Prize-winning Fed writer Jon Hilsenrath, in his piece titled, The Great Unraveling: Fed Missteps Fueled 2016 Populist Revolt. Somehow, Hilsenrath is making the case that a group of 12 older, white people that meet eight times per year in Washington to discuss interest rate policy based on inflation and employment trends has singlehandedly created income inequality, and a populist movement leading to the rise of Donald Trump and Bernie Sanders.

While this Fed scapegoat explanation is quite convenient for the doom-and-gloomers (see The Fed Ate My Homework), it is way off base. I hate to break it to Mr. Hilsenrath, or other conspiracy theorists and perma-bears, but blaming a small group of boring bankers is an overly-simplistic “straw man” argument that does not address the infinite number of other factors contributing to our nation’s social and economic problems.

Ever since the bull market began in 2009, a pervasive skepticism and mistrust have kept the bull market climbing a wall of worry to all-time record levels. In the process, Hilsenrath et. al. have proliferated an inexhaustible list of myths about the Fed and its powers. Here are some of them:

Myth #1: The printing of money by the Fed has led to an artificially inflated stock market bubble and Ponzi Scheme.

- As stock prices have more than tripled over the last eight years to record levels, I’ve reveled in the hypocrisy of the “money printers” contention. First of all, the money printing derived from Quantitative Easing (QE) was originally cited as the sole reason for low, declining interest rates and the rising stock market. The money printing community vociferously predicted once QE ended, as it eventually did in 2014, interest rates would explode higher and stock market prices would collapse. What happened? The exact opposite occurred. Interest rates have gone to record low levels, and stock prices have advanced to all-time record highs.

Myth #2: The Fed controls all interest rates.

- Yes, the Fed can influence short-term interest rates through bond purchases and the targeting of the Federal Funds rate. However, the Fed has little-to-no influence on longer-term interest rates. The massive global bond market dwarfs the size of the Fed and U.S. stock market, and as such, large global financial institutions, pensions, hedge funds, and millions of other investors around the world have more influence on longer-term interest rates. The relationship between the 10-Year Treasury Note yield and the Fed’s monetary policy is loose at best.

Myth #3: The stock market will crash when the Fed raises interest rates.

- Well, we can see that logic is already wrong because the stock market is up significantly since the Fed raised interest rates in mid-December 2015. It is true that additional interest rate hikes are likely to occur in our future, but that does not necessarily mean stock prices are going to plummet. Commentators and bloggers are already panicking about a potential rate hike in September. Before you go jump out a window, let’s put this potential rate hike into context. For starters, let’s not forget the “dove of all doves,” Janet Yellen, is in charge and there has only been one rate increase 0f 0.25% over the last decade. As I point out in one of my previous articles (see Fed Fatigue), stock prices increased during the last rate hike cycle (2004 – 2006) when the Fed raised interest rates from 1.0% to 5.25% (the equivalent of another 16 rate hikes of 0.25%). The world didn’t end in 1994 either, when the Fed Funds rate increased from 3% to 6% over a short time frame, and stocks finished roughly flat for the period. Inflation levels remain at relatively low levels, and the Fed has moved less than 10% of recent hike cycles, so now is not the time to panic. Regardless of what the fear mongers say, the Fed and the bull market fairy godmother (Janet Yellen) will be measured and deliberate in its policies and will verify that any policy action is made into a healthy, strengthening economy.

Myth #4: Stimulative monetary policies instituted by the Fed and other central banks will lead to hyperinflation.

- Japan has done QE for decades, and QE efforts in the U.S. and Europe have also disproved the hyperinflation myth. While commentators, pundits, and journalists like to all point and blame Janet Yellen and the Fed for today’s so-called artificially low interest rates, one does not need to be a genius to realize there are other factors contributing to low rates and inflation. Declining interest rates and inflation are nothing new…this has been going on for over 35 years! (see chart below) As I have discussed previously the larger contributors to declining interest rates and disinflation are technology, globalization, and emerging markets (see Why 0% Interest Rates?). By next year, over one-third of the world’s population is expected to own a smartphone (2.6 billion people), the equivalent of a supercomputer in the palm of their hands. Mobile communication, robotics, self-driving cars, virtual & augmented reality, drones, artificial intelligence, drones, biotechnology, and other technologies are dramatically impacting productivity (i.e., downward pressure on prices and interest rates). These advancements, combined with the billions of low-priced workers in emerging markets, who are lifting themselves out of poverty, are contributing to the declining rate/inflation trend.

Source: Calafia Beach Pundit

As the next Fed meeting approaches, there is no doubt the airwaves and internet will be filled with alarmist calls from the likes of Jon Hilsenrath and other Fed-haters. Fortunately, more informed financial market observers will be able to filter out this noise and be able to separate out the many Fed and interest rate myths from the reality.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Invisible Benefits of Trade

Before the Brexit, 28 countries joined the European Union since its inception in 1957, without a single country leaving. The story is similar if you look at the World Trade Organization (WTO), which has witnessed more than 160 countries unite, without one country exiting since it began in 1948. Are the leaders of these countries idiots and blind to the benefits of trade and globalization? I think not.

For centuries, the advantages of free trade and globalization have lifted the standards of living for billions of people. However, pinpointing the timing or attributing the precise actions leading to these tremendous economic advantages is difficult to do because most trade benefits are often invisible to the naked eye.

Today, populist sentiment on both sides of the political aisle has demonized trade, whether referring to TPP (Trans-Pacific Partnership), NAFTA (North America Free Trade Agreement), trade with China, or announcements by corporations to manufacture goods internationally.

Although it would be naïve to adopt a stance that there are no negative consequences to globalization (e.g., lost American jobs due to offshoring), myopically focusing on job displacement is only half the equation.

While I can attempt to articulate the economic costs and benefits of free trade, and I’ve tried (see Productivity & Trade), Dan Ikenson of the Cato Institute explains it much better than I can. Here is a more eloquent synopsis of free trade (hat-tip: Scott Grannis):

“The case for free trade is not obvious. The benefits of trade are dispersed and accrue over time, while the adjustment costs tend to be concentrated and immediate. To synthesize Schumpeter and Bastiat, the “destruction” caused by trade is “seen,” while the “creation” of its benefits goes “unseen.” We note and lament the effects of the clothing factory that shutters because it couldn’t compete with lower-priced imports. The lost factory jobs, the nearby businesses on Main Street that fail, and the blighted landscape are all obvious. What is not so easily noticed is the increased spending power of the divorced mother who has to feed and clothe her three children. Not only can she buy cheaper clothing, but she has more resources to save or spend on other goods and services, which undergirds growth elsewhere in the economy.

Consider Apple. By availing itself of lowskilled, low-wage labor in China to produce small plastic components and to assemble its products, Apple may have deprived U.S. workers of the opportunity to perform that low-end function in the supply chain. But at the same time, that decision enabled iPods and then iPhones and then iPads to be priced within the budgets of a large swath of consumers. Had all of the components been produced and all of the assembly performed in the United States — as President Obama once requested of Steve Jobs — the higher prices would have prevented those devices from becoming quite so ubiquitous, and the incentives for the emergence of spin-off industries, such as apps, accessories, Uber, and AirBnb, would have been muted or absent.

But these kinds of examples don’t lend themselves to the political stump, especially when the campaigns put a premium on simple messages. This is the burden of free traders: Making the unseen seen. It is this asymmetry that explains much of the popular skepticism about trade, as well as the persistence of often repeated fallacies.

The benefits of trade come from imports, which deliver more competition, greater variety, lower prices, better quality, and new incentives for innovation. Arguably, opening foreign markets should be an aim of trade policy because larger markets allow for greater specialization and economies of scale, but real free trade requires liberalization at home. The real benefits of trade are measured by the value of imports that can be purchased with a unit of exports — our purchasing power or the so-called terms of trade. Trade barriers at home raise the costs and reduce the amount of imports that can be purchased with a unit of exports.

Protectionism benefits producers over consumers; it favors big business over small business because the cost of protectionism is relatively small to a bigger company; and, it hurts lower-income more than higher-income Americans because the former spend a higher proportion of their resources on imported goods.

…Even if there were a President Trump or President Sanders, rest assured that the Congress still has authority over the nuts and bolts of trade policy. The scope for presidential mischief, such as unilaterally raising tariffs, or suspending or amending the terms of trade agreements, is limited. But it would be more reassuring still if the intellectual consensus for free trade were also the popular consensus.”

Fortunately, Ikenson supports the case I’ve made repeatedly. The power of presidential politics is limited by the Congress (see Politics and Your Money). Frustration with politics has never been higher, but in many cases, gridlock is a good thing.

The destructive impacts of protectionist, anti-trade policies is unambiguous – just consider what happened from the implementation of Smoot-Hawley tariffs in 1930 around the time of the Great Depression. U.S. imports decreased 66% from $4.4 billion (1929) to $1.5 billion (1933), and exports decreased 61% from $5.4 billion to $2.1 billion. GNP fell from $103.1 billion in 1929 to $75.8 billion in 1931 and bottomed out at $55.6 billion in 1933.

It’s important to remember, any harmful downside to trade is overwhelmed by the upside of growth. Greg Ip of the WSJ used Doug Irwin, a trade historian at Dartmouth College, to make this pro-growth point:

“If two million American workers lose $15,000 in annual income forever—an extreme estimate of the impact of trade with China—while 320 million American consumers gain just $100 from trade, the benefits to all of society still exceed the costs.”

The benefits of free trade may be invisible in the short run, but over the long-run, the growth advantages of free trade are perfectly visible, despite protectionist, anti-trade rhetoric and propaganda dominating the presidential election conversation.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), and AAPL, but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Why 0% Rates? Tech, Globalization & EM (Not QE)

Recently I have written about the head-scratching, never-ending, multi-decade decline in long-term interest rates (see chart below). Who should care? Well, just about anybody, if you bear in mind the structure of interests rates impacts the cost of borrowing on mortgages, credit cards, automobiles, corporate bonds, savings accounts, and practically every other financial instrument you can possibly think of. Simplistic conventional thinking explains the race to 0% global interest rates by the loose monetary Quantitative Easing (QE) policies of the Federal Reserve. But validating that line of thinking becomes more challenging once you consider QE ended months ago. What’s more, contrary to common belief, rates declined further rather than climb higher after QE’s completion.

Source: Calafia Beach Pundit

More specifically, if you look at rates during this same time last year, the yield on the 10-Year Treasury Note had more than doubled in the preceding 18 months to a level above 3.0%. The consensus view then was that the eventual wind-down of QE would only add gasoline to the fire, causing bond prices to decline and rates to extend an indefinite upwards march. Outside of bond guru Jeff Gundlach, and a small minority of prognosticators, the herd was largely wrong – as is usually the case. As we sit here today, the 10-Year Note currently yields a paltry 2.26%, which has led to the long-bond iShares 20-Year Treasury ETF (TLT) jumping +22% year-to-date (contrary to most expectations).

The American Ostrich

Like an ostrich sticking its head in the sand, us egocentric Americans tend to ignore details relating to others, especially if the analyzed data is occurring outside the borders of our own soil. Unbeknownst to many, here are some key country interest rates below U.S. yields:

- Switzerland: 0.33%

- Japan: 0.34%

- Germany: 0.60%

- Finland: 0.70%

- Austria: 0.75%

- France: 0.88%

- Denmark: 0.89%

- Sweden: 0.98%

- Ireland: 1.29%

- Spain: 1.69%

- Canada 1.80%

- U.K: 1.85%

- Italy: 1.93%

- U.S.: 2.26% (are our rates really that low?)

Outside of Japan, these listed countries are not implementing QE (i.e., “Quantitative Easing”) as did the United States. Rather than QE being the main driver behind the multi-decade secular decline in interest rates, there are other more important disinflationary forces at work driving interest rates lower.

Technology, Globalization, and Emerging Market Competition (T.G.E.M.)

While tracking the endless monthly inflation statistics is a useful exercise to understand the tangible underlying pricing components of various industry segments (e.g., see 20 pages of CPI statistics), the larger and more important factors can be attributed to the somewhat more invisible elements of technology, globalization, and emerging market competition (T.G.E.M).

Starting with technology, to put these dynamics into perspective, consider the number of transistors, or the effective horsepower, on a semiconductor (a.k.a. computer “chip”) today. The overall impact on global standards of living is nothing short of astounding. Take an Intel chip for example – it had approximately 2,000 transistors in 1971. Today, semiconductors can cram over 10,000,000,000 (yes billions – 5 million times more) transistors onto a single semiconductor. Any individual can look no further than their smartphone to understand the profound implications this has not only on pricing in general, but society overall. To illustrate this point, I would direct you to a post highlighted by Professor Mark J. Perry, who observed the cost to duplicate an iPhone during 1991 would have been more than $3,500,000!

There are an infinite number of examples depicting how technology has accelerated the adoption of globalization. More recently, events such as the Arab Spring point out how Twitter (TWTR) displaced costly military engagement alternatives. The latest mega-Chinese IPO of Alibaba (BABA) was also emblematic of the hunger experienced in emerging markets to join the highly effective economic system of global capitalism.

I think New York Times journalist Tom Friedman said it best in his book, The World is Flat, when he made the following observations about the dynamics occurring in emerging markets:

“My mom told me to eat my dinner because there are starving children in China and India – I tell my kids to do their homework because Chinese and Indians are starving for their jobs”.

“France wants a 35 hour work week, India wants a 35 hour work day.”

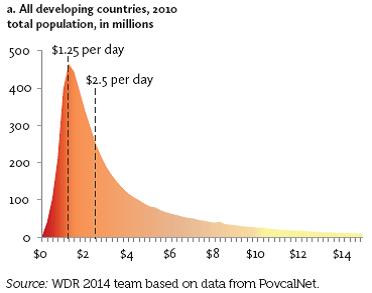

There may be a widening gap between rich and poor in the United States, but technology and globalization is narrowing the gap across the rest of the world. Consider nearly half of the world’s population (3 billion+ people) live in poverty, earning less than $2.50 a day (see chart below). Technology and globalization is allowing this emerging middle class climb the global economic ladder.

These impoverished individuals may not be imminently stealing our current jobs and driving general prices lower, but their children, and the countless educated millions in other international markets are striving for the same economic security and prosperity we have. The educated individuals in the emerging markets that have tasted capitalism are giving new meaning to the word “urgency”, which is only accelerating competition and global pricing pressures. It comes as no surprise to me that this generational migration from the poor to the middle class is putting a lid on inflation and interest rates around the world.

Declining costs of human labor from emerging markets however is not the only issue putting a ceiling on general prices. Robotics, an area in which Sidoxia holds significant investments, continues to be an area of fascination for me. With human labor accounting for the majority of business costs, it’s no wonder the C-suite is devoting more investment dollars towards automation. Rather than hire and train expensive workers, why not just buy a robot? This is not just happening in the U.S. – in fact the Chinese purchased more robots than Americans last year. And why not? An employer does not have to pay a robot overtime compensation; a robot never shows up late; robots never sue for discrimination or harassment; robots receive no healthcare or retirement benefits; and robots work 24 hours/day, 7 days/week, and 365 days/year.

While newspapers, bloggers, and talking heads like to point to the simplistic explanation of loose, irresponsible monetary policies of global central banks as the reason behind a four decade drop in interest rates that is only a small part of the story. Investors and policy makers alike should be paying closer attention to the factors of technology, globalization, and emerging market competition as the more impactful dynamics systematically driving down long term interest rates and inflation.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own a range of positions, including long positions in certain exchange traded fund positions and INTC (short position in TLT), but at the time of publishing SCM had no direct position in BABA, TWTR or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Sweating Your Way to Investment Success

Source: StopSweatyArmpits.com

There are many ways to make money in the financial markets, but if this was such an easy endeavor, then everybody would be trading while drinking umbrella drinks on their private islands. I mean with all the bright blinking lights, talking baby day traders, and software bells and whistles, how difficult could it actually be?

Unfortunately, financial markets have a way of driving grown men (and women) to tears, usually when confidence is at or near a peak. The best investors leave their emotions at the door and follow a systematic disciplined process. Investing can be a meat grinder, but the good news is one does not need to have a 90% success rate to make it lucrative. Take it from Peter Lynch, who averaged a +29% return per year while managing the Magellan Fund at Fidelity Investments from 1977-1990. “If you’re terrific in this business you’re right six times out of 10,” says Lynch.

Sweating Way to Success

If investing is so tough, then what is the recipe for investment success? As the saying goes, money management requires 10% inspiration and 90% perspiration. Or as strategist and long-time investor Don Hays notes, “You are only right on your stock purchases and sales when you are sweating.” Buying what’s working and selling what’s not, doesn’t require a lot of thinking or sweating (see Riding the Wave), just basic pattern recognition. Universally loved stocks may enjoy the inertia of upward momentum, but when the music stops for the Wall Street darlings, investors rarely can hit the escape button fast enough. Cutting corners and taking short-cuts may work in the short-run, but usually ends badly.

Real profits are made through unique insights that have not been fully discovered by market participants, or in other words, distancing oneself from the herd. Typically this means investing in reasonably priced companies with significant growth prospects, or cheap out-of-favor investments. Like dieting, this is easy to understand, but difficult to execute. Pulling the trigger on unanimously hated investments or purchasing seemingly expensive growth stocks requires a lot of blood, sweat, and tears. Eating doughnuts won’t generate the conviction necessary to justify the valuation and excess expected return for analyzed securities.

Times Have Changed

Investing in stocks is difficult enough with equity fund flows hemorrhaging out of investor accounts like the asset class is going out of style (See ICI data via The Reformed Broker). Stocks’ popularity haven’t been helped by the heightened volatility, as evidenced by the multi-year trend in the schizophrenic volatility index (VIX) – escalated by the “Flash Crash,” U.S. debt ceiling debate, and European financial crisis. Globalization, which has been accelerated by technology, has only increased correlations between domestic market and international markets. As we have recently experienced, the European tail can wag the U.S. dog for long periods of time. In decades past, concerns over economic activity in Iceland, Dubai, and Greece may not even make the back pages of The Wall Street Journal. Today, news travels at the speed of a “Tweet” for every Angela Merkel – Nicolas Sarkozy breakfast meeting or Chinese currency adjustment, and eventually results in a sprawling front page headline.

The equity investing game may be more difficult today, but investing for retirement has never been more important. Stuffing money under the mattress in Treasuries, money market accounts, CDs, or other conservative investments may feel good in the short run, but will likely not cover inflation associated with rising fuel, food, healthcare, and leisure costs. Regardless of your investment strategy, if your goal is to earn excess returns, you may want to check the moistness of your armpits – successful long-term investing requires a lot of sweat.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in ETFC, VXX, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

U.S. – Best House in Bad Global Neighborhood

Article below represents a portion of free December 1, 2011 Sidoxia monthly newsletter (Subscribe on right-side of page)

There is no shortage of issues to worry about in our troubled global neighborhood, but then again, anybody older than 25 years old knows the world is always an uncertain place. Whether we are talking about wars (Vietnam, Cold War, Iraq); presidential calamities (Kennedy assassination, Nixon resignation/impeachment proceedings); international turmoil (dissolution of Soviet Union, 9/11 attacks, Arab Spring); investment bubbles (technology, real estate); or financial crises (S&L crisis, Long Term Capital, Lehman Brothers bankruptcy), investors always have a large menu of concerns from which they can order.

Despite the doom and gloom dominating the media airwaves, and the lackluster performance of equities experienced over the last decade, the Dow Jones Industrial Average and the S&P 500 index are both up more than 20-fold since the 1970s (those gains also exclude the positive impact of dividends).

Times Have Changed

Just a few decades ago, nobody would have talked or cared about small economies like Iceland, Dubai, and Greece. Today, technology has accelerated the forces of globalization, resulting in information travelling thousands of miles at the click of a mouse, often creating scary financial mountains out of meaningless molehills. As a result of these trends, news of Italian bond auctions, which normally would be glossed over on the evening news, instantaneously clogs our smart phones, computers, radios, and televisions. The implications of all these developments mean investing has become much more difficult, just as its importance has never been more crucial.

How has investing become more critical? For starters, interest rates are near 60-year lows and Treasury bond prices are at record highs, while inflation (food, energy, healthcare, leisure, etc.) is shrinking the value of people’s savings. Next, entitlement and pension reliability are decreasing by the minute – fiscal imbalances and unrealistic promises have contributed to a less certain retirement outlook. Layer on hyper-manic volatility of daily, multi-hundred point swings in the Dow Jones Industrial index and a less experienced investor quickly realizes investing can become an overwhelming game. Case in point is the VIX volatility index (a.k.a., the “Fear Gauge”), which has registered a whopping +57% increase in 2011.

December to Remember?

After an explosive +23% return in the S&P 500 index for 2009 (excluding dividends) and another +13% return in 2010, equity investors have taken a breather thus far in 2011 – the Dow Jones Industrial Average is up modestly (+4%) and the S&P 500 index is down fractionally (-1%). We still have the month of December to log, but in the short-run the European tail has definitely been wagging the rest of the global dog.

Although the United States knows a thing or two about lack of political leadership and coordination, herding the 17 eurozone countries to resolve the European debt financial crisis has proved even more challenging. As you can see below in the performance figures of the major global equity markets, the U.S. remains the best house in a bad neighborhood:

Our fiscal house undeniably needs some work (i.e., unsustainable deficits and bloated debt), but record corporate profits, record levels of cash, voracious consumer spending, improving employment data, and attractive valuations are all contributing to a domestic house that makes opportunities in our backyard look a lot more appealing to investors than prospects elsewhere in the global neighborhood.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and VGK, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Stretching Rubber Band Creating More Value

Concerns over debt ceiling negotiations, European financial challenges, and overall economic malaise has reached a feverish pitch in the U.S., yet in the background, a valuation rubber band has quietly been stretching to ever more attractive levels. Regardless of whether seniors might not receive Social Security checks, troops not obtain ammunition, and investors not collect credit rating agency love, corporations keep churning profits out like they are going out of style (17%+ growth in 2011 estimated earnings). We have barely scratched the surface on earnings season, and I’m sure better than expected earnings from the likes of Google Inc. (GOOG), JPMorgan Chase & Co. (JPM), FedEx Corp. (FDX), Nike Inc. (NKE), and Bed Bath & Beyond Inc. (BBBY) will not sway the bears, but in the meantime profits keep chugging along. Although profits have more than doubled in the last 12 years, not to mention a halving in interest rates (10-year Treasury yield cut from 6% to about 3%), yet the S&P 500 is still down approximately -4% (June 1999 – June 2011).

What Gives?

Could the valuation stretching continue as earnings continue to grind higher? Absolutely. Just because prices have been chopped in half, doesn’t mean they can’t go lower. From 1966 – 1982 the Dow Jones Industrial index traded at around 800 and P/E multiples contracted to single digits. That rubber band eventually snapped and the index catapulted 17-fold from 800 to almost 14,000 in 25 years. Even though equities have struggled in the 21st century, a few things have changed from the low-point reached about 30 years ago. For starters, we have not hit an inflation rate of 15% or a Federal Funds rate of 20% (4% and 0% today, respectively), so we have a tad bit more headroom before the single digit P/E apocalypse descends upon us. If you listen to Peter Lynch, investor extraordinaire, his “Rule of 20” states a market equilibrium P/E ratio should equal 20 minus the inflation rate. This rule would imply an equilibrium P/E ratio of 16-17 when the current 2011 P/E multiple implies a value slightly above 13 times earnings. The bears may claim victory if the earnings denominator collapses, but if earnings, on the contrary, continue coming in better than expected, then the sun might break through the clouds in the form of significant price appreciation.

Another change that has occurred since the days of Cabbage Patch dolls has been the opening floodgates of globalization. The technology revolution has accelerated the flattening of the globe, which has created numerous new opportunities and threats. Creating a company like Facebook with about 750 million users and an estimated value of $80 billion to $100 billion couldn’t happen 30 years ago, but on the flip side, our country is also competing with billions of motivated brains lurking in the far reaches of the world with a singular focus of sucking away our jobs, resources, and dollars. Winners recognize this threat and are currently adapting. Losers blind to this trend remain busy digging their own graves.

Future is Uncertain

As famous Jedi Master Yoda aptly identified, “Always in motion is the future.” The future is always uncertain, and if it wasn’t, I would be on my private island drinking umbrella drinks all day. With undecided debt ceiling negotiations occurring over the next few weeks, political rhetoric will be blaring and traders will be hyperventilating with defibrillator paddles close at hand. If history is a guide, stupid decisions may be made, but the almighty financial markets (and maybe a few Molotov cocktails at a local protest rally) will eventually slap politicians in the face to wake up to reality. Perhaps you recall the attention the markets earned from legislators when the Dow fell 777 points in a single September 2008 trading session. Blood on the streets forced Congress to approve the Troubled Asset Relief Program hot potato four days after the initial vote failed. And if that wasn’t a gentle enough reminder for Democrats and Republicans, then a few lessons can be learned from the interest rate sledgehammer that capital markets vigilantes have slammed on the Greeks (10-year Greek yields are hovering above 17%+).

Down but Not Out

The stories of debt collapse, hyperinflation, double-dip recessions, plunging dollar, secular bear markets, and government shutdowns are all plausible but remote scenarios. As Winston Churchill so eloquently stated, “You can always count on Americans to do the right thing – after they’ve tried everything else.” Voter moods are so venomous that if fiscal irresponsibility is not changed, politicians will be voted straight out of office – even hardcore, extremist elected officials understand this self-serving point.

Suffice it to say, as the political noise reaches a deafening pitch in the coming weeks and months, a quiet rubber band in the background keeps stretching. When the political noise dies down, you may just hear a noise snapping stock prices higher.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Performance data from Morningstar.com. Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, GOOG, and FDX, but at the time of publishing SCM had no direct position in JPM, NKE, BBBY, Facebook, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Innovative Bird Keeps All the Worms

Source: Photobucket

As the old saying goes, “The early bird gets the worm,” but in the business world this principle doesn’t always apply. In many cases, the early bird ends up opening a can of worms while the innovative, patient bird is left with all the spoils. This concept has come to light with the recent announcement that social networking site MySpace is being sold for a pittance by News Corp. (NWS) to Specific Media Inc., an advertising network company. Although Myspace may have beat Facebook to the punch in establishing a social network footprint, Facebook steamrolled Myspace into irrelevance with a broader more novel approach. Rather than hitting a home run and converting a sleepy media company into something hip, Rupert Murdoch, CEO of News Corp. struck out and received crumbs for the Myspace sale (News Corp. sold it for $35 million after purchasing for $540 million in 2005, a -94% loss).

Other examples of “winner takes all” economics include:

Kindle vs. Book Stores: Why are Borders and Waldenbooks (BGPIQ.PK) bankrupt, and why is Barnes and Noble Inc. (BKS) hemorrhaging in losses? One explanation may be people are reading fewer books and reading more blogs (like Investing Caffeine), but the more credible explanation is that Amazon.com Inc. (AMZN) built an affordable, superior digital mousetrap than traditional books. I’ll go out on a limb and say it is no accident that Amazon is the largest bookseller in the world. Within three years of Kindle’s introduction, Amazon is incredibly selling more digital books than they are selling physical hard copies of books.

iPod vs. Walkman/MP3 Players: The digital revolution has shaped our lives in so many ways, and no more so than in the music world. It’s hard to forget how unbelievably difficult it was to fast-forward or rewind to a particular song on a Sony Walkman 30 years ago (or the hassle of switching cassette sides), but within a matter of a handful of years, mass adoption of Apple Inc.’s (AAPL) iPod overwhelmed the dinosaur Walkman player. Microsoft Corp.’s (MSFT) foray into the MP3 market with Zune, along with countless other failures, have still not been able to crack Apple’s overpowering music market positioning.

Google vs. Yahoo/Microsoft Search: Google Inc. (GOOG) is another company that wasn’t the early bird when it came to dominating a new growth industry, like search engines. As a matter of fact, Yahoo! Inc (YHOO) was an earlier search engine entrant that had the chance to purchase Google before its meteoric rise to $175 billion in value. Too bad the Yahoo management team chose to walk away…oooph. Some competitive headway has been made by the likes of Microsoft’s Bing, but Google still enjoys an enviable two-thirds share of the global search market.

Dominance Not Guaranteed

Dominant market share may result in hefty short-term profits (see Apple’s cash mountain), but early success does not guarantee long-term supremacy. Or in other words, obsolescence is a tangible risk in many technology and consumer related industries. Switching costs can make market shares sticky, but a little innovation mixed with a healthy dose of differentiation can always create new market leaders.

Consider the number one position American Online (AOL) held in internet access/web portal business during the late nineties before its walled gardens came tumbling down to competition from Yahoo, Google, and an explosion of other free, advertisement sponsored content. EBay Inc. (EBAY) is another competition casualty to the fixed price business model of Amazon and other online retailers, which has resulted in six and a half years of underperformance and a -44% decline in its stock price since the 2004 peak. Despite questionable execution, and an overpriced acquisition of Skype, eBay hasn’t been left for complete death, thanks to a defensible growth business in PayPal. More recently, Research in Motion Ltd. (RIMM) and its former gargantuan army of “CrackBerry” disciples have felt the squeeze from new smart phone clashes with Apple’s iPhone and Google’s Android operating system.

With the help of technology, globalization, and the internet, never in the history of the world have multi-billion industries been created at warp speed. Being first is not a prerequisite to become an industry winner, but evolutionary innovation, and persistently differentiated products and services are what lead to expanding market shares. So while the early bird might get the worm, don’t forget the patient and innovative second mouse gets all the cheese.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Performance data from Morningstar.com. Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, AAPL, AMZN, and GOOG, but at the time of publishing SCM had no direct position in BGPIQ.PK, NWS, YHOO, MSFT, SNE, AOL, EBAY, RIMM, Facebook, Skype, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}