Posts tagged ‘Fed Funds rate’

A Tale of Two Years: Happy & Not-So-Happy

Happy New Year! If you look at the stock market, 2019 was indeed a happy one. The S&P 500 index rose +29% and the Dow Jones Industrial Average was up +22%. Spectacular, right? More specifically, for the S&P 500, 2019 was the best year since 2013, while the Dow had its finest 12-month period since 2017. Worth noting, although 2019 made investors very happy, 2018 stock returns were not-so-happy (S&P 500 dropped -6%).

Source: Investor’s Business Daily

As measured against almost any year, the 2019 results are unreasonably magnificent. This has many prognosticators worrying that these gains are unsustainable going into 2020, and many pundits are predicting death and destruction are awaiting investors just around the corner. However, if the 2019 achievements are combined with the lackluster results of 2018, then the two-year average return (2018-2019) of +10% looks more reasonable and sustainable. Moreover, if history is a guide, 2020 could very well be another up year. According to Barron’s, stocks have finished higher two-thirds of the time in years following a +25% or higher gain.

With the yield on the 10-Year Treasury Note declining from 2.7% to 1.9% in 2019, it should come as no surprise that bonds underwent a reversal of fortune as well. All else equal, both existing bond and stock prices generally benefit from declining interest rates. The U.S. Aggregate Bond Index climbed +5.5% in 2019, a very respectable outcome for this more conservative asset class, after the index experienced a modest decline in 2018.

Happy Highlights

What contributed to the stellar financial market results in 2019? There are numerous contributing factors, but here are a few explanations:

Source: Dr. Ed’s Blog

Source: Dr. Ed’s Blog

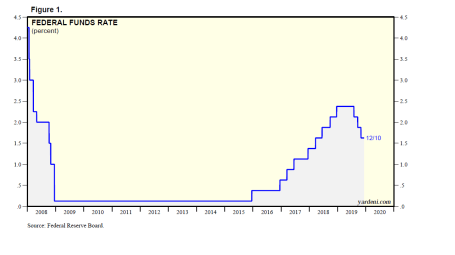

- Federal Reserve Cuts Interest Rates: After slamming on the brakes in 2018 by hiking interest rates four times, the central bank added stimulus to the economy by cutting interest rates three times in 2019 (see chart above).

- Phase I Trade Deal with China: Washington and Beijing reached an initial trade agreement that will reduce tariffs and force China to purchase larger volumes of U.S. farm products.

- Healthy Economy: 2019 economic growth (Gross Domestic Product) is estimated to come in around +2.3%, while the most recent unemployment rate of 3.5% remains near a 50-year low.

- Government Shutdown Averted: Congress approved $1.4 trillion in spending packages to avoid a government shutdown. The spending boosts both the military and domestic programs and the signed bills also get rid of key taxes to fund the Affordable Care Act and raises the U.S. tobacco buying age to 21.

- Brexit Delayed: The October 31, 2019 Brexit date was delayed, and now the U.K. is scheduled to leave the European Union on January 31, 2020. EU officials are signaling more time may be necessary to prevent a hard Brexit.

- Sluggish Global Growth Expected to Rise in 2020: Global growth rates are expected to increase in 2020 with little chance of recessions in major economies. The Financial Times writes, “The outlook from the models shows global growth rates rising next year, returning roughly to trend rates. Recession risks are deemed to be low, currently standing about 5 per cent for the US and 15 per cent for the eurozone.”

- Potential Bipartisan Infrastructure Spend: In addition to the $1.4 trillion in aforementioned spending, Nancy Pelosi, the Speaker of the Democratic-controlled House of Representatives, said she is willing to work with the Republicans and the White House on a stimulative infrastructure spending bill.

2018-2019 Lesson Learned

One of the lessons learned over the last two years is that listening to the self-proclaimed professionals, economists, strategists, and analysts on TV, or over the blogosphere, is dangerous and usually a waste of your time. For stock market participants, listening to experienced and long-term successful investors is a better strategy to follow.

Conventional wisdom at the beginning of 2018 was that a strong economy, coupled with the Tax Reform Act that dramatically reduced tax rates, would catapult corporate profits and the stock market higher. While many of the talking heads were correct about the trajectory of S&P 500 profits, which propelled upwards by an astonishing +24%, stock prices still sank -6% in 2018 (as mentioned earlier). If you fast forward to the start of 2019, after a -20% correction in stock prices at the end of 2018, conventional wisdom stated the economy was heading into a recession, therefore stock prices should decline further. Wrong!

As is typical, the forecasters turned out to be completely incorrect again. Although profit growth for 2019 was roughly flat (0%), stock prices, as previously referenced, unexpectedly skyrocketed. The moral of the story is profits are very important to the direction of future stock prices, but using profits alone as a timing mechanism to predict the direction of the stock market is nearly impossible.

So, there you have it, 2018 and 2019 were the tale of two years. Although 2018 was an unhappy year for investors in the stock market, 2019’s performance made investors happier than average. When you combine the two years, stock investors should be in a reasonably good mood heading into 2020 with the achievement of a +10% average annual return. While this multi-year result should keep you happy, listening to noisy pundits will make you and your investment portfolio unhappy over the long-run. Rather, if you are going to heed the advice of others, it’s better to pay attention to seasoned, successful investors…that will put a happy smile on your face.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (January 2, 2019). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Summer Heats Up

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (August 1, 2017). Subscribe on the right side of the page for the complete text.

The temperature in the stock market heated up again this month. Like a hot day at the beach, the Dow Jones Industrial Average stock index burned +542 points higher this month (+2.5%), while scorching +2,129 points ahead in 2017 (or +10.8%).

Despite these impressive gains (see 2009-2017 chart below), overall, investors remain concerned. Rather than stock participants calmly enjoying the sun, breeze, and refreshingly cool waters of the current markets, many investors have been more concerned about getting sunburned to a geopolitical crisp; overwhelmed by an unexpected economic tsunami; and/or drowned by a global central bank-induced interest rate crisis.

Stock market concerns rise, but so do stock prices.

The most recent cautionary warnings have come to the forefront by noted value investor Howard Marks, who grabbed headlines with last week’s forewarning memo, “Here They Go Again…Again.” The thoughtful, 23-page document is definitely worth reading, but like any prediction, it should be taken with a pound of salt, as I point out in my recent article Predictions – A Fool’s Errand. The reality is nobody has been able to consistently predict the future.

If you don’t believe my skepticism about crystal balls and palm readers, just listen to the author of the cautionary article himself. Like many other market soothsayers, Marks is forced to provide a mea culpa on the first page in which he admits his predictions have been wrong for the last six years. His dour but provocative position also faces another uphill battle, given that Marks’s conclusion flies in the face of value investing god, Warren Buffett, who was quoted this year as saying:

“Measured against interest rates, stocks actually are on the cheap side compared to historic valuations.”

Rather than crucify him, Marks should not be singled out for this commonly cautious view. In fact, most value investors are born with the gloom gene in their DNA, given the value mandate to discover and exploit distressed assets. This value-based endeavor has become increasingly difficult as the economy gains steam in this slow but sustainably long economic recovery. As I’ve mentioned on numerous occasions, bull markets don’t die of old age, but rather they die from excesses. So far the key components of the economy, the banking system and consumers, have yet to participate in euphoric excesses like previous economic cycles due to risk aversion caused by the last financial crisis.

Making matters worse for value investors, the value style of investing has underperformed since 2006 alongside other apocalyptic predictions from revered value peers like Seth Klarman and Ray Dalio, who have also been proved wrong over recent years.

However, worth stating, is experienced, long-term investors like Marks, Klarman, and Dalio deserve much more attention than the empty predictions spewed from the endless number of non-investing strategists and economists who I specifically reference in A Fool’s Errand.

Beach Cleanup in Washington

While beach conditions may be sunny, and stock market geeks like me continue debating future market weather conditions, media broadcasters and bloggers have been focused elsewhere – primarily the nasty political mess littered broadly across our American shores.

Lack of Congressional legislation progress relating to healthcare, tax reform, and infrastructure, coupled with a nagging investigation into potential Russian interference into U.S. elections, have caused the White House to finally lose its patience. The end result? A swift cleanup of the political hierarchy. After deciding to tidy up the White House, President Trump’s first priority was to remove Sean Spicer, the former White House Press Secretary and add the controversial Wall Street executive Anthony Scaramucci as the new White House Communications Chief. Shortly thereafter, White House Chief of Staff Reince Priebus was pushed to resign, and he was replaced by Secretary of Homeland Security, John F. Kelly. If this was not enough drama, after Scaramucci conducted a vulgar-laced tirade against Priebus in a New Yorker magazine interview, newly minted Chief of Staff Kelly felt compelled to quickly fire Scaramucci.

While the political beach party and soap opera have been entertaining to watch from the sidelines, I continue to remind observers that politics have little, if any, impact on the long-term direction of the financial markets. There have been much more important factors contributing to the nine-year bull market advance other than politics. For example, interest rates, corporate profits, valuations, and investor sentiment have been much more impactful forces behind the new record stock market highs.

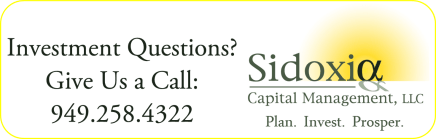

Federal Reserve Chair Janet Yellen may not wear a bikini at the beach, but nevertheless she has become quite the spectacle in Washington, as investors speculate on the future direction of interest rates and other Fed monetary policies (i.e., unwinding the $4.5 trillion Fed balance sheet). In the hopes of not exhausting your patience too heavily, let’s briefly review interest rates, so they can be placed in the proper context. Specifically, it’s worth noting the spotlighted Federal Funds Rate target is sitting at enormously depressed levels (1.00% – 1.25%), despite the fact the Fed has increased the target four times within the last two years. How low has the Fed Funds rate been historically? As you can see from the historical chart below (1970 – 2017), this key benchmark rate reached a level as high as 20.00% in the early 1980s – a far cry from today’s 1.00% – 1.25% rate.

There are two crucial points to make here. First, even at 1.25%, interest rates are at extremely low levels, and this is significantly stimulative to our economy, even after considering the scenario of future interest rate hikes. The second main point is that that Federal Reserve Chair Janet Yellen has been exceedingly cautious about her careful, data-dependent intentions of increasing interest rates. As a matter of fact, the CME Fed Funds futures market currently indicates a 99% probability the Fed will maintain interest rates at this low level when the Federal Open Market Committee (FOMC) meets in September.

Responsibly Have Fun but Use Protection

It’s imperative to remain vigilantly prudent with your investments because weather conditions will not always remain calm in the financial markets. You do not want to get burned by overheated markets or caught off guard by an unexpected economic storm. Blindly buying tech stocks exclusively without a systematic disciplined approach to valuation is a sure-fire way to lose money over the long-run. Instead, protection must be implemented across multiple vectors.

From a broader perspective, at Sidoxia we believe it’s essential to follow a low-cost, diversified, tax-efficient, strategy with a long-term time horizon. Rebalancing your portfolio as markets continue to appreciate will keep your investment portfolio balanced as financial markets gyrate. These investment basics have produced a winning formula for many investors, including some very satisfying long-term results at Sidoxia, which is quickly approaching its 10-year anniversary. You can have fun at the beach, just remember to bring sunscreen and a windbreaker, in case conditions change.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Sky is Falling?

Investors reacted like the sky was falling on Friday. Commentators mostly blamed the -400 point decline in the Dow on heightened probabilities for a September rate hike by Janet Yellen and her fellow Federal Reserve colleagues. Geopolitical concerns over a crazy dictator in North Korea with nuclear weapons were identified as contributing factors to frazzled nerves.

The real question should be, “Are these stories complete noise, or should I pay close attention?” For the vast majority of times, the response to questions like these should be “yes”, the media headlines are mere distractions and you should simply ignore them. During the last rate hike cycle from mid-2004 to mid-2006, guess how many times the Fed raised rates? Seventeen times! And over those 17 rate hikes, stocks managed to respectably rise over 11%.

So far this cycle, Yellen and the Fed have raised interest rates one time, and the one and only hike was the first increase in a decade. Given all this data, does it really make sense to run in a panic to a bunker or cave? Whether the Fed increases rates by 0.25% during September or Decemberis completely irrelevant.

If we look at the current situation from a slightly different angle, you can quickly realize that making critical investment decisions based on short-term Federal Reserve actions would be foolish. Would you buy or sell a house based solely on this month’s Fed policy? For most, the answer is an emphatic “no”. The same response should hold true for stocks as well. The real reason anyone should consider buying any type of asset, including stocks, is because you believe you are paying a fair or discounted price for a stream of adequate future cash flows (distributions) and/or price appreciation in the asset value over the long-term.

The problem today for many investors is “short-termism.” This is what Jack Gray of Grantham, Mayo, Van Otterloo and Company had to say on the subject, “Excessive short-termism results in permanent destruction of wealth, or at least permanent transfer of wealth.” I couldn’t agree more.

Many people like to speculate or trade stocks like they are gambling in Las Vegas. One day, when the market is up, they buy. And the other day, when the market is down, they sell. However, those same people don’t wildly speculate with short-term decision-making when they buy larger ticket items like a lawn-mower, couch, refrigerator, car, or a house. They rationally buy with the intention of owning for years.

Yes, it’s true appliances, vehicles, and homes have utility characteristics different from other assets, but stocks have unique utility characteristics too. You can’t place leftovers, drive inside, or sit on a stock, but the long-term earnings and dividend growth of a diversified stock portfolio provides plenty of distinctive income and/or retirement utility benefits to a long-term investor.

You don’t have to believe me – just listen to investing greats like Warren Buffett:

“If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes. Put together a portfolio of companies whose aggregate earnings march upward over the years, and so also will the portfolio’s market value.”

The common sense test can also shed some light on the subject. If short-term trading, based on the temperature of headlines, was indeed a lucrative strategy, then the wealthiest traders in the world would be littered all over the Forbes 100 list. There are many reasons that is not the case.

Even though the Volatility Index (aka, “Fear Gauge” – VIX) spiked +40% in a single day, that does not necessarily mean stock investors are out of the woods yet. We saw similar volatility occur last August and during January and June of this year. At the same time, there is no need to purchase a helmet and run to a bunker…the sky is not falling.

Other related article: Invest with a Telescope…Not a Microscope

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Fed: Myths vs. Reality

Traders, bloggers, media talking heads, and pundits of all stripes went into a feverish sweat as they anticipated the comments of Federal Reserve Chairman Janet Yellen at the annual economic summit held in Jackson Hole, Wyoming. When Yellen, arguably the most dovish Fed Chairman in history, uttered, “I believe the case for an increase in the federal funds rate has strengthened in recent months,” an endless stream of commentators used this opportunity to spout out a never-ending stream of predictions describing the looming consequences of such a potential rate increase.

As I’ve stated before, the Fed receives both too much blame and too much credit for basically doing nothing except moving short-term interest rates up or down (and most of the time they do nothing). However, until the next Fed meeting in September (or later), we all will be placed in purgatory with non-stop speculation regarding the timing of the next rate increase.

The ludicrous and myopic analysis can be encapsulated by the recent article written by Pulitzer Prize-winning Fed writer Jon Hilsenrath, in his piece titled, The Great Unraveling: Fed Missteps Fueled 2016 Populist Revolt. Somehow, Hilsenrath is making the case that a group of 12 older, white people that meet eight times per year in Washington to discuss interest rate policy based on inflation and employment trends has singlehandedly created income inequality, and a populist movement leading to the rise of Donald Trump and Bernie Sanders.

While this Fed scapegoat explanation is quite convenient for the doom-and-gloomers (see The Fed Ate My Homework), it is way off base. I hate to break it to Mr. Hilsenrath, or other conspiracy theorists and perma-bears, but blaming a small group of boring bankers is an overly-simplistic “straw man” argument that does not address the infinite number of other factors contributing to our nation’s social and economic problems.

Ever since the bull market began in 2009, a pervasive skepticism and mistrust have kept the bull market climbing a wall of worry to all-time record levels. In the process, Hilsenrath et. al. have proliferated an inexhaustible list of myths about the Fed and its powers. Here are some of them:

Myth #1: The printing of money by the Fed has led to an artificially inflated stock market bubble and Ponzi Scheme.

- As stock prices have more than tripled over the last eight years to record levels, I’ve reveled in the hypocrisy of the “money printers” contention. First of all, the money printing derived from Quantitative Easing (QE) was originally cited as the sole reason for low, declining interest rates and the rising stock market. The money printing community vociferously predicted once QE ended, as it eventually did in 2014, interest rates would explode higher and stock market prices would collapse. What happened? The exact opposite occurred. Interest rates have gone to record low levels, and stock prices have advanced to all-time record highs.

Myth #2: The Fed controls all interest rates.

- Yes, the Fed can influence short-term interest rates through bond purchases and the targeting of the Federal Funds rate. However, the Fed has little-to-no influence on longer-term interest rates. The massive global bond market dwarfs the size of the Fed and U.S. stock market, and as such, large global financial institutions, pensions, hedge funds, and millions of other investors around the world have more influence on longer-term interest rates. The relationship between the 10-Year Treasury Note yield and the Fed’s monetary policy is loose at best.

Myth #3: The stock market will crash when the Fed raises interest rates.

- Well, we can see that logic is already wrong because the stock market is up significantly since the Fed raised interest rates in mid-December 2015. It is true that additional interest rate hikes are likely to occur in our future, but that does not necessarily mean stock prices are going to plummet. Commentators and bloggers are already panicking about a potential rate hike in September. Before you go jump out a window, let’s put this potential rate hike into context. For starters, let’s not forget the “dove of all doves,” Janet Yellen, is in charge and there has only been one rate increase 0f 0.25% over the last decade. As I point out in one of my previous articles (see Fed Fatigue), stock prices increased during the last rate hike cycle (2004 – 2006) when the Fed raised interest rates from 1.0% to 5.25% (the equivalent of another 16 rate hikes of 0.25%). The world didn’t end in 1994 either, when the Fed Funds rate increased from 3% to 6% over a short time frame, and stocks finished roughly flat for the period. Inflation levels remain at relatively low levels, and the Fed has moved less than 10% of recent hike cycles, so now is not the time to panic. Regardless of what the fear mongers say, the Fed and the bull market fairy godmother (Janet Yellen) will be measured and deliberate in its policies and will verify that any policy action is made into a healthy, strengthening economy.

Myth #4: Stimulative monetary policies instituted by the Fed and other central banks will lead to hyperinflation.

- Japan has done QE for decades, and QE efforts in the U.S. and Europe have also disproved the hyperinflation myth. While commentators, pundits, and journalists like to all point and blame Janet Yellen and the Fed for today’s so-called artificially low interest rates, one does not need to be a genius to realize there are other factors contributing to low rates and inflation. Declining interest rates and inflation are nothing new…this has been going on for over 35 years! (see chart below) As I have discussed previously the larger contributors to declining interest rates and disinflation are technology, globalization, and emerging markets (see Why 0% Interest Rates?). By next year, over one-third of the world’s population is expected to own a smartphone (2.6 billion people), the equivalent of a supercomputer in the palm of their hands. Mobile communication, robotics, self-driving cars, virtual & augmented reality, drones, artificial intelligence, drones, biotechnology, and other technologies are dramatically impacting productivity (i.e., downward pressure on prices and interest rates). These advancements, combined with the billions of low-priced workers in emerging markets, who are lifting themselves out of poverty, are contributing to the declining rate/inflation trend.

Source: Calafia Beach Pundit

As the next Fed meeting approaches, there is no doubt the airwaves and internet will be filled with alarmist calls from the likes of Jon Hilsenrath and other Fed-haters. Fortunately, more informed financial market observers will be able to filter out this noise and be able to separate out the many Fed and interest rate myths from the reality.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Confessions of a Bond Hater

Source: stock.xchng

Hi my name is Wade, and I’m a bond hater. Generally, the first step in addressing any type of personal problem is admitting you actually have a problem. While I am not proud of being a bond hater, I have been called many worse things during my life. But as we have learned from the George Zimmerman / Trayvon Martin case, not every situation is clear-cut, whether we are talking about social issues or bond investing. For starters, let me be clear to everyone, including all my detractors, that I do not hate all bonds. In fact, my Sidoxia clients own many types of fixed income securities. What I do hate however are low yielding, long duration bonds.

Duration…huh? Most people understand what “low yielding” means, when it comes to bonds (i.e., low interest, low coupon, low return, etc.), but when the word duration is uttered, the conversation is usually accompanied by a blank stare. The word “duration” may sound like a fancy word, but in reality it is a fairly simple concept. Essentially, high-duration bonds are those fixed income securities with the highest sensitivity to changes in interest rates, meaning these bonds will go down most in price as interest rates rise.

When it comes to equity markets, many investors understand the concept of high beta stocks, which can be used to further explain duration. There are many complicated definitions for beta, but the basic principle explains why high-beta stock prices generally go up the most during bull markets, and go down the most during bear markets. In plain terms, high beta equals high octane.

If we switch the subject back to bonds, long duration equals high octane too. Or stated differently, long duration bond prices generally go down the most during bear markets and go up the most during bull markets. For years, grasping the risk of a bond bear market caused by rising rates has been difficult for many investors to comprehend, especially after witnessing a three-decade long Federal Funds tailwind taking the rates from about 20% to about 0% (see Fed Fatigue Setting In).

The recent interest rate spike that coincided with the Federal Reserve’s Ben Bernanke’s comments on QE3 bond purchase tapering has caught the attention of bond addicts. Nobody knows for certain whether this short-term bond price decline is the start of an extended bear market in bonds, but mathematics would dictate that there is only really one direction for interest rates to go…and that is up. It is true that rates could remain low for an indefinite period of time, but neither scenario of flat to down rates is a great outcome for bond holders.

Fixes to Fixed-Income Failings

Even though I may be a “bond hater” of low yield, high duration bonds, currently I still understand the critical importance and necessity of a fixed income portfolio for not only retirees, but also for the diversification benefits needed by a broader set of investors. So how does a bond hater reconcile investing in bonds? Easy. Rather than focusing on lower yielding, longer duration bonds, I invest more client assets in shorter duration and/or higher yielding bonds. If you harbor similar beliefs as I do, and believe there will be an upward bias to the trajectory of long-term interest rates, then there are two routes to go. Investors can either get compensated with a higher yield to counter the increased interest rate risk, and/or they can shorten duration of bond holdings to minimize capital losses.

Worth noting, there is an alternative strategy for low yielding, long duration bond lovers. In order to minimize interest rate risk, these bond lovers may accept sub-optimal yields and hold bonds to maturity. This strategy may be associated with short-term price volatility, but if the bond issuer does not default, at least the bond investor will get the full principal at maturity to help relieve the pain of meager yields.

Now that you’ve survived all this bond babbling, let me cut to the chase and explain a few ways Sidoxia is taking advantage of the recent interest rate volatility for our clients:

Floating Rate Bonds: Duration of these bonds is by definition low, or near zero, because as interest rates rise, coupons/interest payments are advantageously reset for investors at higher rates. So if interest rates jump from 2% to 3%, the investor will receive +50% higher periodic payments.

Inflation Protection Bonds: These bonds come in long and short duration flavors, but if interest rates/inflation rise higher than expected, investors will be compensated with higher periodic coupons and principal payments.

Shorter Duration: One definition of duration is the weighted average of time until a bond’s fixed cash flows are received. A way of shortening the duration of your bond portfolio is through the purchase of shorter maturity bonds (e.g., buying 3-year bonds rather than 30-year bonds).

High Yield Bonds: Investing in the high yield bond category is not limited to domestic junk bond purchases, but higher yields can also be earned by investing in international and/or emerging market bonds.

Investment Grade Corporate Bonds: Similar to high yield bonds, investment grade bonds offer the potential of capital appreciation via credit improvement. For instance, credit rating upgrades can provide gains to help offset price declines caused by rising interest rates.

Despite my bond hater status, the recent taper tantrum and interest rate spike, highlight some advantages bonds have over stocks. Even though prices declined, bonds by and large still have lower volatility than stocks; provide a steady stream of income; and provide diversification benefits.

To the extent investors have, or should have, a longer-term time horizon, I still am advocating a stock bias to client portfolios, subject to each investor’s risk tolerance. For example, an older retired couple with a conservative target allocation of 20%/80% (equity/fixed income) may consider a 25% – 30% allocation. A shift in this direction may still meet the retirees’ income needs (especially if dividend-paying stocks are incorporated), while simultaneously acknowledging the inflation and interest rate risks impacting bond positions. It’s important to realize one size doesn’t fit all.

Higher Volatility, Higher Reward

Frequent readers of Investing Caffeine have known about my bond hating tendencies for quite some time (see my 2009 article Treasury Bubble has not Burst…Yet), but the bond baby shouldn’t be thrown out with the bath water. For those investors who thought bonds were as safe as CDs, the recent -6% drop in the iShares Aggregate Bond Index (AGG) didn’t feel comfortable for most. Although I am still an enthusiastic stock cheerleader (less so as valuation multiples expand), there has been a cost for the gargantuan outperformance of stocks since March of ’09. While stocks have outperformed bonds (S&P vs. AGG) by more than +140%, equity investors have had to endure two -10% corrections and two -20% corrections (e.g.,Flash Crash, Debt Ceiling Debate, European Financial Crisis, and Sequestration/Elections). If investors want to earn higher long-term equity returns, this desire will translate into more volatility than bonds…and more Tums.

I may still be a bond hater, and the general public remains firm stock haters, but at some point in the multi-year future, I will not be surprised to hear myself say, “Hi my name is Wade, and I am addicted to bonds.” In the mean time, Sidoxia will continue to optimize its client bond portfolios for a rising interest rate environment, while also investing in attractive equity securities and ETFs. There’s nothing to hate about that.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), including floating rate bonds/loan funds, inflation-protection funds, corporate bond ETF, high-yield bond ETFs, and other bond ETFs, but at the time of publishing, SCM had no direct position in AGG or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Fed Fatigue Setting In

Uncle…uncle! There you have it – I have finally cried “uncle” because I cannot take it anymore. I don’t think I can listen to another panel or read another story debating about the timing of Fed “tapering”, or heaven forbid the Fed actually “tighten” the Federal Funds rate (i.e., increasing the targeted rate for inter-bank lending). Type in the words “Bernanke” and “tapering” into Google and you will get back more than 41,000,000 results. The build up to the 600-word FOMC (Federal Open Market Committee) statement was almost deafening, so much so that live coverage of Federal Reserve Chairman Ben Bernanke was available at your fingertips:

Source: Yahoo! Finance

Like a toddler (or a California-based, investment blog writer) going to the doctor’s office to receive an inoculation, the anxiety and mental anguish caused in anticipation of the event is often more painful than the actual injection. As I highlighted in a previous Investing Caffeine article, the 1994 interest rate cycle wasn’t Armageddon for equity markets, and the same can be said for the rate hikes from 1.0% to 5.25% in the 2004-20006 period (see chart below). Even if QE3 ends in mid-2014 and the new Federal Reserve Chairman (thank you President Obama) raises rates in 2015, this scenario would not be the first (or last) time the Federal Reserve has tightened monetary policy.

Source: Wikipedia

Short Memories – What Have You Done for Me Lately?

People are quick to point out the one-day -350 Dow point loss earlier this week, but many of them forget about the +3,000 point moon shot in the Dow Jones Industrial index that occurred in six short months (November 2012 – May 2013). The same foggy recollection principle applies to interest rates. The recent rout in 10-year Treasury prices is easily recalled as rates have jumped from 1.5% to 2.5% over the last year, however amnesia often sets in for others if you ask them where rates were a few years ago. It’s easy to forget that 30-year fixed rate mortgages exceeded 5% and the 10-year reached 4% just three short years ago.

Bernanke: The Center of the Universe?

Does Ben Bernanke deserve credit for implementing extraordinary measures during extraordinary times during the 2008-09 financial crisis? Absolutely. But should every man, women, and child wait with bated breath to see if a word change or tonal adjustment is made in the eight annual FOMC meetings?

Like the public judging Ben Bernanke, my Sidoxia clients probably give me too much credit when things go well and too much blame when things don’t. I love how Bernanke gets blamed/credited for the generational low interest rates caused by his money printing ways and QE punch bowl tactics. Last I checked, the interest rate downtrend has been firmly in place over the last three decades, well before Bernanke came into the Fed and worked his monetary magic. How much credit/blame are we forgetting to give former Federal Reserve Chairmen Paul Volcker, Alan Greenspan, and other government policy-makers? Regardless of what happens economically for the remainder of 2013, Bernanke will do whatever he can to solidify his legacy in the waning sunset months of his term.

Another forgotten fact I like to point out: There is more than one central banker living on this planet. If you haven’t been asleep over the last few decades, our financial markets have increasingly become globally interconnected with the assistance of technology. I know our 10-year Treasury rates are hovering around 2.50%, and our egotistical patriotism leads us to hail Bernanke as a monetary god, but don’t any other central bankers or government officials around the world deserve any recognition for achieving yields even lower than ours? Here’s a partial list (June 22, 2013 – Financial Times):

- Japan – 0.86%

- Germany – 1.67%

- Canada – 2.33%

- U.K. – 2.31%

- France – 2.27%

- Sweden – 2.15%

- Austria – 2.09%

- Switzerland – 0.92%

- Netherlands – 2.07%

Although it may be fun to look at Ben Bernanke as our country’s financial Superman who is there to save the day, there are a lot more important factors to consider than the 47 words added and 19 subtracted from the latest FOMC statement. If investing was as easy as following central bank monetary policy, everyone would be continually jet setting to their private islands. Rather than wasting your time listening to speculative blathering about direction of Fed monetary policy, why not focus on finding solid investment ideas and putting a long-term investment plan in place. Now please excuse me – Fed fatigue has set in and I need to take a nap.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and GOOG, but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

1994 Bond Repeat or 2013 Stock Defeat?

Interest rates are moving higher, bond prices are collapsing, and fear regarding a stock market plunge is palpable. Sound like a recent news headline or is this a description of a 1994 financial market story? For those with a foggy, double-decade-old memory, here is a summary of the 1994 economic environment:

- The economy registered its 34th month of expansion and the stock market was on a record 40-month advance

- The Federal Reserve embarked on its multi-hike, rate-tightening monetary policy

- The 10-year Treasury note exhibited an almost 2.5% jump in yields

- Inflation was low with a threat of rising inflation lurking in the background

- An upward sloping yield curve encouraged speculative bond carry-trade activity (borrow short, invest long)

- Globalization and technology sped up the pace of price volatility

Many of these listed items resemble factors experienced today, but bond losses in 1994 were much larger than the losses of 2013 – at least so far. At the time, Fortune magazine called the 1994 bond collapse the worst bond market loss in history, with losses estimated at upwards of $1.5 trillion. The rout started with what might have appeared as a harmless 0.25% increase in the Federal Funds rate (the rate that banks lend to each other) from 3% to 3.25% in February 1994. By the time 1994 came to a close, acting Federal Reserve Chairman Alan Greenspan had jacked up this main monetary tool by 2.5%.

Rising rates may have acted as the flame for bond losses, but extensive use of derivatives and leverage acted as the gasoline. For example, over-extended Eurobond positions bought on margin by famed hedge fund manager Michael Steinhardt of Steinhardt Partners lead to losses of about-30% (or approximately $1.5 billion). Renowned partner of Omega Partners, Leon Cooperman, took a similar beating. Cooperman’s $3 billion fund cratered -24% during the first half of 1994. Insurance company bond portfolios were hit hard too, as collective losses for the industry exceeded $20 billion, or more than the claims paid for Hurricane Andrew’s damage. Let’s not forget the largest casualty of this era – the public collapse of Orange County, California. Poor derivatives trades led to $1.7 billion in losses and ultimately forced the county into bankruptcy.

There are plenty of other examples, but suffice it to say, the pain felt by other bond investors was widespread as a massive number of margin calls caused a snowball of bond liquidations. The speed of the decline was intensified as bond holders began selling short and using derivatives to hedge their portfolios, accelerating price declines.

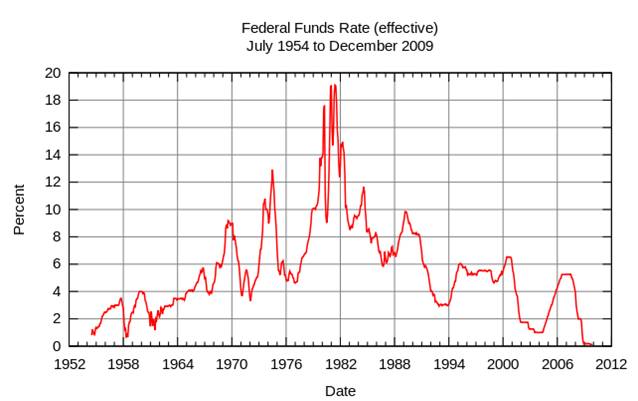

Just as the accommodative interest rate punch bowl was eventually removed by Greenspan, so too is Ben Bernanke (current Fed Chairman) threatening to do today. Even if Bernanke unleashes a cold-turkey tapering of the $85 billion per month in bond-purchases, massive losses in bond values won’t necessarily mean catastrophe for stock values. For evidence, one needs to look no further than this 1994-1995 chart of the stock market:

Source: Ciovaccocapital.com

Volatility for stocks definitely increased in 1994 with the S&P 500 index correcting about -10% early in the year. But as you can see, by the end of the year the market was off to the races, tripling in value over the next five years. Volatility has been the norm for the current bull market rally as well. Despite the more than doubling in stock prices since early 2009, we have experienced two -20% corrections and one -10% pullback.

What’s more, the onset of potential tapering is completely consistent with core economic principles. Capitalism is built on free trading markets, not artificial intervention. Extraordinary times required extraordinary measures, but the probabilities of a massive financial Armageddon have been severely diminished. As a result, the unprecedented scale of quantitative easing (QE) will eventually become more harmful than beneficial. The moral of the story is that volatility is always a normal occurrence in the equity markets, therefore any significant stock pullback associated with potential bond tapering (or fed fund rate hikes) shouldn’t be viewed as the end of the world, nor should a temporary weakening in stock prices be viewed as the end to the bull market in stocks.

Why have stocks historically provided higher returns than bonds? The short answer is that stocks are riskier than bonds. The price for these higher long-term returns is volatility, and if investors can’t handle volatility, then they shouldn’t be investing in stocks.

If you are an investor that thinks they can time the market, you wouldn’t be wasting your time reading this article. Rather, you’d be spending time on your personal island while drinking coconut drinks with umbrellas (see Market Timing Treadmill).

Although there are some distinct similarities between the economic backdrop of 1994 and 2013, there are quite a few differences also. For starters, the economy was growing at a much healthier clip then (+4.1% GDP growth), which stoked inflationary fears in the mind of Greenspan. Moreover, unemployment was quite low (5.5% by year-end vs. 7.6% today) and the Fed did not communicate forward looking Fed policy back then.

It’s unclear if the recent 50 basis point ascent in 10-year Treasury rates was just an appetizer for what’s to come, but simple mathematics indicate there is really only one direction left for interest rates to go…higher. If history repeats itself, it will likely be bond investors choking on higher rates (not stock investors). For the sake of optimistic bond speculators, I hope Ben Bernanke knows the Heimlich maneuver. Studying history may help bond bulls avoid indigestion.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Drought in Higher Rates May Be Over

The drought in higher interest rates may be nearing an end? Ever since the global financial crisis accelerated into full force in the fall of 2008, there were a constant flow of coordinated interest rate cuts triggered around the world with the aim of stimulating global GDP (Gross Domestic Product) and improving credit flow through the clogged financial pipes. Central banks across the world cut key benchmark interest rate levels and the impact of these reductions has a direct influence on what consumers pay for their financial products and services. More recently, we have begun to see the reversal of previous cuts with rate hikes witnessed in several international markets. Last week we saw Norway become the first western European country to raise rates, following an earlier October rate lift by Australia and another by Israel in August. For some countries, the sentiment has switched from global collapse fears to a stabilization posture coupled with future inflation concerns. In the U.S., the data has been more mixed (read article here) and the Federal Reserve has been clear on its intention to keep short-term rates at abnormally low levels for an extended period of time. That stance would likely change with evidence of inflationary pressures or improved job market conditions.

What Does This Mean for Consumers?

Prior to the financial crisis, credit availability flourished at affordably low rates. Now, with signs of a potential global recovery matched with regulatory overhauls, consumers may be impacted in several financial areas:

1) Credit Card Rates: Beyond regulatory changes in Washington (read more), the interest rate charged on unpaid credit card balances may be on the rise. When the Federal Reserve inevitably raises the targeted Federal Funds Rate (the interest rate for loans made between banks) from the current target rate range of 0.00% and 0.25%, this action will likely have direct upward pressure on consumer credit card rates. The associated increase in key benchmark rates such as the Prime Rate (the rate charged to a bank’s most creditworthy customers) and LIBOR (London Interbank Offer Rate) would result in higher monthly interest payments for consumers.

2) Other Consumer Loans: Many of the same forces impacting credit card rates will also impact other consumer loans, like home mortgages and auto loans. Pull out your loan documents – if you have floating or variable rate loans then you may be exposed to future hikes in interest rates.

3) Business Loans / Lines of Credit: Business owners -not just consumers – can also be impacted by rising rates. When the cost of funding goes up (.i.e., interest rates), the banks look to pass on those higher costs to the customer so the account profitability can be maintained.

4) Dollar & Import Prices: To the extent subsequent United States rate hikes lag other countries around the world, our dollar runs the risk of depreciating more in value (currency investors, all else equal, prefer currencies earning higher interest rates). A weaker dollar translates into foreign goods and services costing more. If international central banks continue to raise rates faster than the U.S., then imported good inflation could become a larger reality.

5) Hit to Bond Prices: Higher interest rates can also result in a negative hit to your bond portfolio. Higher duration bonds, those typically with longer maturities and lower relative coupon payments, are the most vulnerable to a rise in interest rates. Consider shortening the duration of your portfolio and even contemplate floating rate bonds.

Interest rates are the cost for borrowed money and even with the recent increase in consumers’ savings rate, consumers generally are still saddled with a lot of debt. Do yourself a favor and review any of your credit card agreements, loan documents, and bond portfolio so you will be prepared for any future interest rate increases. Shopping around for better rates and/or consolidating high interest rate debt into cheaper alternatives are good strategies as we face the inevitable end in the drought of higher global interest rates.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}