Posts tagged ‘Euro’

Greece: The Slow Motion, Multi-Year Train Wreck

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (July 1, 2015). Subscribe on the right side of the page for the complete text.

Watching Greece fall apart over the last five years has been like watching a slow motion train wreck. To many, this small country of 11 million people that borders the Mediterranean, Aegean, and Ionian Seas is known more for its Greek culture (including Zeus, Parthenon, Olympics) and its food (calamari, gyros, and Ouzo) than it is known for financial bailouts. Nevertheless, ever since the financial crisis of 2008-2009, observers have repeatedly predicted the debt-laden country will default on its €323 billion mountain of obligations (see chart below – approximately $350 billion in dollars) and subsequently exit the 19-member eurozone currency membership (a.k.a.,”Grexit”).

Source: MoneyMorning.com and CNN

Now that Greece has failed to repay less than 1% of its full €240 billion bailout obligation – the €1.5 billion payment due to the IMF (International Monetary Fund) by June 30th – the default train is coming closer to falling off the tracks. Whether Greece will ultimately crash itself out of the eurozone will be dependent on the outcome of this week’s surprise Greek referendum (general vote by citizens) mandated by Prime Minister Alexis Tsipras, the leader of Greece’s left-wing Syriza party. By voting “No” on further bailout austerity measures recommended by the European Union Commission, including deeper tax increases and pension cuts, the Greek people would effectively be choosing a Grexit over additional painful tax increases and deeper pension cuts.

Ouch!

And who can blame the Greeks for being a little grouchy? You might not be too happy either if you witnessed your country experience an economic decline of greater than 25% (see Greece Gross Domestic Product chart below); 25% overall unemployment (and 50% youth unemployment); government worker cuts of greater than 20%; and stifling taxes to boot. Sure, Greeks should still shoulder much of the blame. After all, they are the ones who piled on $100s of billions of debt and overspent on the pensions of a bloated public workforce, and ran unsustainable fiscal deficits.

Source: TradingEconomics.com

For any casual history observers, the current Greek financial crisis should come as no surprise, especially if you consider the Greeks have a longstanding habit of not paying their bills. Over the last two centuries or so, since the country became independent, the Greek government has spent about 90 years in default (almost 50% of the time). More specifically, the Greeks defaulted on external sovereign debt in 1826, 1843, 1860, 1894 and 1932.

The difference between now and past years can be explained by Greece now being a part of the European Union and the euro currency, which means the Greeks actually do have to pay their bills…if they want to remain a part of the common currency. During past defaults, the Greek central bank could easily devalue their currency (the drachma) and fire up the printing presses to create as much currency as needed to pay down debts. If the planned Greek referendum this week results in a “No” vote, there is a much higher probability that the Greek government will need to dust off those drachma printing presses.

“Perspective People”

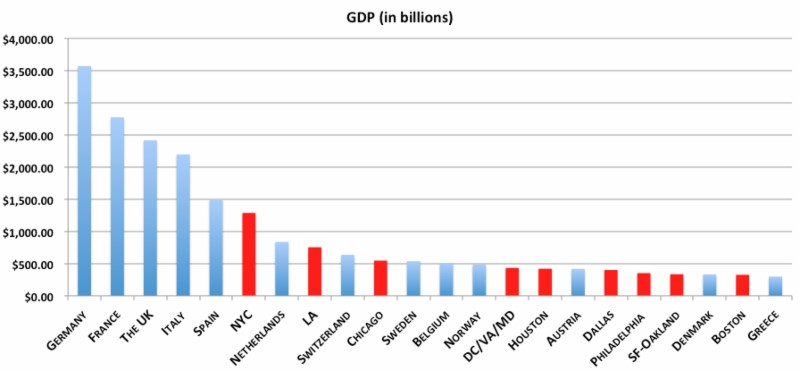

Protest, riots, defaults, changing governments, and new currencies make for entertaining television viewing, but these events probably don’t hold much significance as it relates to the long-term outlook of your investments and the financial markets. In the case of Greece, I believe it is safe to say the economic bark is much worse than the bite. For starters, Greece accounts for less than 2% of Europe’s overall economy, and about 0.3% of the global economy.

Since I live out on the West Coast, the chart below caught my fancy because it also places the current Greek situation into proper proportion. Take the city of L.A. (Los Angeles – red bar) for example…this single city alone accounts for almost 3x the size of Greece’s total economy (far right on chart – blue bar).

Give Me My Money!

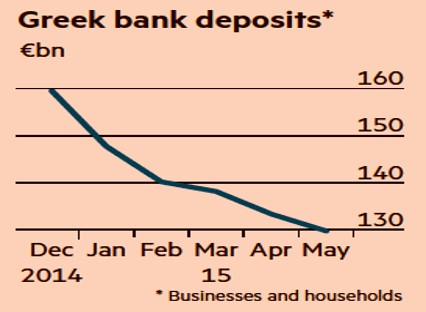

It hasn’t been a fun year for Greek banks. Depositors, who have been flocking to the banks, withdrew about $45 billion in cash from their accounts, over an eight month period (see chart below). Before the Greek government decided to mandatorily close the banks in recent days and implement capital controls limiting depositors to daily ATM withdrawals of only $66.

Source: The Financial Times

But once again, let’s put the situation into context. From an overall Greek banking sector perspective, the four largest Greek Banks (Bank of Greece, Piraeus Bank, Eurobank Ergasias, Alpha Bank) account for about 90% of all Greek banking assets. Combined, these banks currently have an equity market value of about $14 billion and assets on the balance sheets of $400 billion – these numbers are obviously in flux. For comparison purposes, Bank of America Corp. (BAC) alone has an equity market value of $179 billion and $2.1 trillion in assets.

Anxiety Remains High

Skeptical bears will occasionally acknowledge the miniscule-ness of Greece, but then quickly follow up with their conspiracy theory or domino effect hypothesis. In other words, the skeptics believe a contagion effect of an impending Grexit will ripple through larger economies, such as Italy and Spain, with crippling force. Thus far, as you can see from the chart below, Greece’s financial problems have been largely contained within its borders. In fact, weaker economies such as Spain, Portugal, Ireland, and Italy have fared much better – and actually improving in most cases. In recent days, 10-year yields on government bonds in countries like Portugal, Italy, and Spain have hovered around or below 3% – nowhere near the peak levels seen during 2008 – 2011.

Source: Business Insider

Other doubting Thomases compare Greece to situations like Lehman Brothers, Long Term Capital Management, and the subprime housing market, in which underestimated situations snowballed into much worse outcomes. As I explain in one of my newer articles (see Missing the Forest for the Trees), the difference between Greece and the other financial collapses is the duration of this situation. The Greek circumstance has been a 5-year long train wreck that has allowed everyone to prepare for a possible Grexit. Rather than agonize over every news headline, if you are committed to the practice of worrying, I would recommend you focus on an alternative disaster that cannot be found on the front page of all newspapers.

There is bound to be more volatility ahead for investors, and the referendum vote later this week could provide that volatility spark. Regardless of the news story du jour, any of your concerns should be occupied by other more important worrisome issues. So, unless you are an investor in a Greek bank or a gyro restaurant in Athens, you should focus your efforts on long-term financial goals and objectives. Ignoring the noisy news flow and constructing a diversified investment portfolio across a range of asset classes will allow you to avoid the harmful consequences of the slow motion, multi-year Greek train wreck.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and BAC, but at the time of publishing, SCM had no direct position in Bank of Greece, Piraeus Bank, Eurobank Ergasias, Alpha Bank or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on ICContact page.

Rates Dance their Way to a Floor

The globe is awash in debt, deficits are exploding, and the Euro is about to collapse…right? Well, then why in the heck are six countries out of the G-7 seeing their 10-year sovereign debt trade at 2.5% or lower on a consistent downward long-term trajectory? What’s more, three of the six countries witnessing their rates plummet are from Europe, despite pundits continually calling for the demise of the eurozone.

Here is a snapshot of 10-year sovereign debt yields for the majority of the G-7 countries over the last few decades:

Source: TradingEconomics.com

The sole G-7 member missing from the bond yield charts above? Italy. Although Italy’s deficits are not massive (Italy actually has a smaller deficit than U.S. as % of GDP: 3.9% in 2011), its Debt/GDP ratio has been large and rising (see chart below):

Source: TradingEconomics.com

As the globe has plodded through the financial crisis of 2008-2009, investors have flocked to the perceived stability of these larger developed countries’ bonds, even if they are merely better homes in a bad neighborhood right now. PIMCO likes to call these popular sovereign bonds, “cleaner dirty shirts.” Buying sovereign debt from these less dirty shirt countries, without sensitivity to price or yield, has been a lucrative trade that has worked consistently for quite some time. Now, however, with sovereign bond yields rapidly approaching 0%, it becomes mathematically impossible to fall lower than the bottom rate floor that developed countries are standing on.

Bond bears have been wrong about the timing of the inevitable bond price reversal, myself included, but the bulls are skating on thinner and thinner ice as rates continue moving lower. The bears may prolong their bragging rights if interest rates continue downward, or persist at these lower levels for extended periods of time. Eventually the “buy the dips” mentality dies, as we so poignantly experienced in 2000 when the technology dips turned into outright collapse.

The Flies in the Bond Binging Ointment

As long as equities remain in a trading range, the “risk-off” bond binging arguments will continue holding water. If corporate earnings remain elevated and stock buybacks carry on, the pain of deflating real returns will eventually become too unbearable for investors. As the insidious rising prices of energy, healthcare, food, leisure, and general costs keep eating away everyone’s purchasing power, even the skeptics will become more impatient with the paltry returns they are currently earning. Earning negative real returns in Treasuries, CDs, money market accounts, and other conservative investments, is not going to help millions of Americans meet their future financial goals. Due to the laundry list of global economic concerns, large swaths of investors are still running and hiding, but this is not a sustainable strategy longer term. The danger from these so-called “safe,” low-yielding asset classes is actually riskier than the perceived risk, in my view.

With that said, I’ve consistently held there are a subset of investors, including a significant number of my Sidoxia Capital Management clients, who are in the later stage of retirement and have a rational need for capital preservation and income generating assets (albeit low yielding). For this investor segment, portfolio construction is not executed due to an opportunistic urge of chasing potential outsized rates of return, but more-so out of necessity. Shorter time horizons eliminate the prudence of additional equity exposure because of the extra associated volatility. Unfortunately, many of the 76 million Baby Boomers will statistically live another 20 – 30 years based on actuarial life expectations and under-save, so the risks of being too conservative can dramatically outweigh the risks of increasing equity exposure. This is all stated in the context of stocks paying a higher yield than long-term Treasuries – the first time in a generation.

Short-term risks and uncertainties remain high, with Greek election outcomes unknown; a U.S. Presidential election in flux; and an impending domestic fiscal cliff that needs to be addressed. But with interest rates accelerating towards 0% and investors’ fright-filled buying of pricey, low-yielding asset classes, many of these risks are already factored into current valuations. As it turns out, the pain of panic can be more detrimental than being stuck in over-priced assets, driven by rates dancing near an absolute floor.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Solving Europe and Your Deadbeat Cousin

The fall holidays are quickly approaching, and almost every family has at least one black-sheep member among the bunch. You know, the unemployed second cousin who shows up for Thanksgiving dinner intoxicated – who then proceeds to pull you aside after a full meal to ask you for some money because of an unlucky trip to Las Vegas. For simplicity purposes, let’s name our deadbeat cousin Joe.

Right now the European union (EU) is dealing with a similar situation, but rather than being forced to deal with money-begging cousin named Joe, the EU is being forced to confront the irresponsible debt-binging practices of its own relatives – the PIIGS (Portugal, Ireland, Italy, Greece, and Spain). The European troika (International Monetary Fund/IMF; European Union/EU; and European Central Bank/ECB), spearheaded by German and French persuasion, is contemplating everything from prescribing direct bank recapitalization, bailouts via the leveraging of the EFSF (European Financial Stability Facility), ECB bond purchases, debt guarantees, unlimited central bank loans, and more.

New stress tests are being reevaluated as we speak. Previous tests failed in gaining the necessary credibility because inadequate haircuts were applied to the values of PIIGS debt held by European banks. European Leaders are beginning to gain some religion as to the urgency and intensity of the financial crisis. Just today, Germany’s chancellor (Angela Merkel) and France’s President (Nicolas Sarkozy) announced that they will introduce a comprehensive package of measures to stabilize the eurozone by the end of this month, right before the summit of the G20 leading global economies in Cannes, France.

Pick Your Poison

Whatever the path used to mop up debt excesses, the options for solving the financial mess can be lumped together in the following categories:

1. Austerity: Plain, unadulterated spending cuts is one prescription being administerd in hopes of curing bloated European sovereign debt issues. Negatives: Slowing economic growth, slowing tax receipts, potentially widening deficits (reference Greece), and political reelection self interests call into question the feasibility of the austerity option. Positives: Austerity is a morally correct fiscal response, which has the potential of placing a country’s financial situation back on a sustainable path.

2. Bailouts: The troika is also talking about infusing the troubled banks with new capital. Negatives: This action could result in more debt placed on country balance sheets, a potentially lower credit rating, higher costs of borrowing, higher tax burden for blameless taxpayers, and often an impossible political path of success. Positives: Financial markets may respond constructively in the short-run, but providing an alcoholic more alcohol doesn’t solve long-term fiscal responsibility, and also introduces the problem of moral hazard.

3. Haircuts: Voluntary or involuntary haircuts to principal debt obligations may occur in conjunction with previously described bailout efforts, depending on the severity of debt levels. Negatives: There are many different sets of constituents and investors, which can make voluntary haircut/debt restructuring terms difficult to agree upon. If the haircuts are too severe, banking reserves across the EU will become decimated, which will only lead to more austerity, bailouts, and potential credit downgrades. Such actions could hamper or eliminated future access to capital, and the cost of access to future capital could be cost prohibitive for the borrowing countries that defaulted/restructured. Positives: Haircuts eliminate or lessen the need for other more painful austerity or restructuring measures, and force borrowers to become more fiscally responsible, not to mention, investors are forced to conduct more thorough due diligence.

4. Printing Press: Buying back debt with freshly printed euros hot off the press is another strategy. Negatives: Inflation is an invisible tax on everyone, including those constituents who are behaving in a fiscally responsible manner. Positives: Not only is this strategy more politically palatable because the inflation tax is spread across the whole union, but this path to debt reduction also does not require as painful and unpopular cuts in spending as experienced in other options.

The Costs

What is the cost for this massive European debt-binging rehabilitation? Estimates vary widely, but a JP Morgan analyst sized it up this way as explained in the The Financial Times:

“In a worst-case, severe recession scenario, €230bn in new capital is needed to meet Basel III requirements, assuming a 60 per cent debt writedown on Greece, 40 per cent on Ireland and Portugal and 20 per cent on Italy and Spain, and that banks withhold dividends.”

More bearish estimates with larger bond loss haircuts, stricter regulatory guidelines, and harsher austerity measures have generated recapitalization numbers north of €1 trillion euros. Regardless of the estimates, European governments, regulators, and central banks are likely to select a combination of the poisons listed above. There is no silver bullet solution, and any of the chosen paths come with their own unique set of consequences.

As time passes and the European crisis matures, I am confident that you will be hearing more about ECB involvement and the firing-up of the printing presses. Perhaps the ECB will fund and work jointly with the EFSF to soak up debt and/or capitalize weak banks. Alternatively, and more simply, the ECB is likely to follow the path of the U.S. and implement significant amounts of quantitative easing (i.e., provide liquidity to the financial system via sovereign debt purchases and guarantees).

Dealing with irresponsible and intoxicated deadbeat second cousins (or European countries) fishing for money is never a pleasurable experience. There are many ways to address the problem, but ignoring the issue will only make the situation worse. Fortunately, our European friends on the other side of the pond appear to be taking notice. As in the U.S., if government officials delay or ignore the immediate problems, the financial market cops (a.k.a., “bond vigilantes”) will force them into action. In the recent past, European officials have used a strategy of sober talking “tough love,” but signs that the ECB printing presses are now beginning to warm up are evident. Once the euros come flying off the presses to detoxify the debt binging banks, perhaps the ECB can print a few extra euros for my cousin Joe.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in JPM, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

No Respect: The Rodney Dangerfield of the Investment World

Source: Photobucket

Ask any average Joe off the street what investment category is at or near record all-time highs, and a good number of them will confidently answer “gold,” as prices recently eclipsed $1,600 per ounce. But of course this makes perfect sense, right? The Fed is printing money like it’s going out of style, the dollar is collapsing like a drunken sailor, inflation is about to sky-rocket to the moon, and China is on the verge of becoming the world’s new reserve currency. Never mind that Greece, Portugal and Ireland are in shambles with the Euro on its death bed. Or Japan has achieved a debt to GDP ratio that would even make U.S. vote grubbing politicians blush. A sub-3% 10-Year Treasury Note doesn’t appear to discourage fervent gold-bugs either.

No Respect

While gold has experienced an incredible sextupling in prices over the last decade and hit new-all time highs, believe it or not, there is an unlikely asset class that is reaching new historic highs and has outperformed gold for almost 2.5 years. Can you guess what asset class star I am talking about? If I said U.S. “stocks,” would you believe me? OK, well maybe I’m not referring to large capitalization stocks like Johnson & Johnson (JNJ), Microsoft Corp. (MSFT), Wal-Mart Stores (WMT), Intel Corp. (INTC), and AT&T Inc. (T), all of which have effectively gone nowhere in the 21st Century. However, the story is quite different if you look at small and mid capitalization stocks, which have received about as much respect as Rodney Dangerfield.

As a matter of fact, the S&P 400 (MidCap Index) and S&P 600 Index (SmallCap Index) have more than doubled gold’s performance since the lows of March 2009 (SmallCap +149.0%; MidCap +145.1%; Gold/GLD +71.0%). Given the spectacular performance of small and mid-sized companies, I’m still waiting with bated breath for a telemarketer call asking me if I have considered selling my small and mid cap stock certificates for cash – since everyone has melted their gold chains and fillings, a new hobby is needed.

S&P 400 MidCap and S&P 600 SmallCap (Source: Yahoo! Finance)

What Next?

Has the fear trade ended? Perhaps not, if you consider European sovereign debt and U.S. debt ceiling concerns, but what happens if the half empty glass becomes half full. The early 1980s may be a historical benchmark period for comparison purposes. An interesting thing happened from 1980-1982 when Federal Reserve Chairman Paul Volcker began raising interest rates to fight inflation – gold prices dropped -65% (~$800/oz. to under $300/oz.) from 1980-1982 and the shiny metal lived through approximately a 25 year period with ZERO price appreciation. Since there is only one direction for the Fed’s zero interest rate policy (ZIRP) to go, conceivably history will repeat itself once again?

In hindsight gold was a beautiful safe haven vehicle during the panic-filled, nail-biting period during late-2007 throughout 2008. Since then, small and mid cap stocks have trounced gold. Like stocks, Rodney Dangerfield may have gotten no respect, but once fear has subsided and rates start increasing, maybe stocks will steal the show and get the respect they deserve.

See also Rodney Dangerfield’s perspective on Doug Kass and the Triple Lindy

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Performance data from Morningstar.com. Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including small cap and mid cap ETFs), and WMT, but at the time of publishing SCM had no direct position in JNJ, MSFT, INTC, T, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}