Posts tagged ‘EU’

End of the World or Status Quo?

If you were the chief executive of a newspaper, television, or magazine company, what headline stories would you run to generate the most viewers and readers? Which subjects will you choose to make me impulsively grab a magazine in the grocery line, keep me glued to the television news, or suck me in to click-bait advertisements on the web? For example, what topics below would you select to grab the most attention?

· Hurricane or Sunshine?

· High Speed Car Chase or Cat Saved from Tree?

· Bloody Murder or Baby’s Birthday?

· Messy Divorce or Wedding Celebration?

· Impeachment or Bipartisan Legislation

· End of the World or Status Quo?

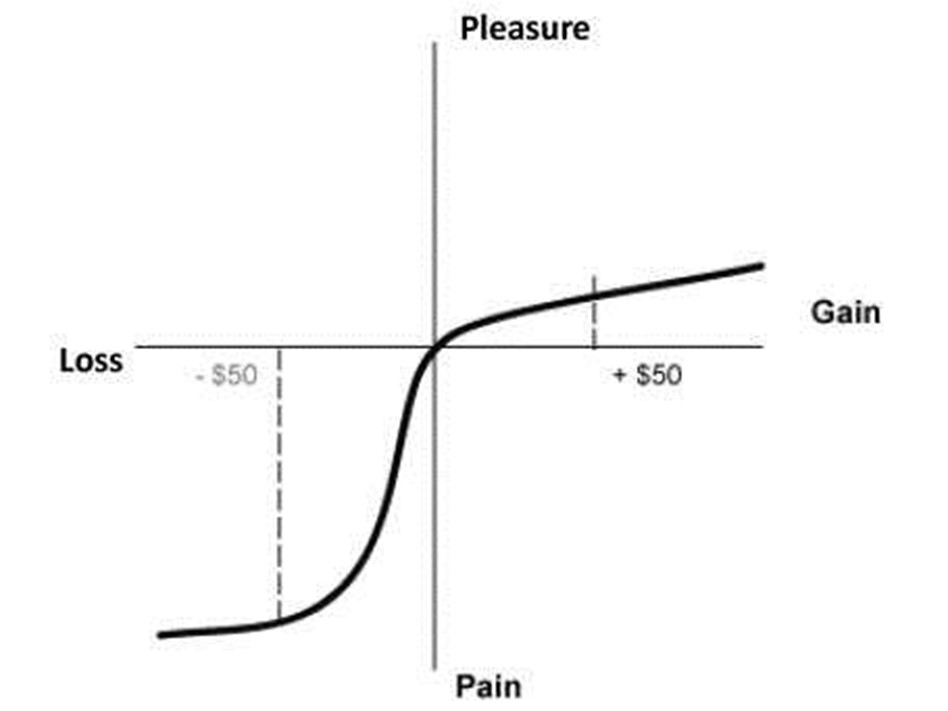

If you selected the first subject in each pair above, you would likely gain much more initial interest. In choosing a winning topic, the saying goes, “what bleeds, leads.” In other words, scary or controversial stories always grab more attention than feel-good or status quo narratives. And that is why the vast majority of media outlets are drawn to negativity, just as mosquitos are attracted to bug zappers. This phenomenon can be explained in part with the help of Nobel Prize winner Daniel Kahneman and his partner Amos Tversky, who conducted research showing the pain from losses is more than twice as painful as are the pleasures experienced from gains (see chart below).

The significant volatility seen in the stock market recently from the Russian war/invasion of Ukraine is further evidence of how this fear dynamic can create short-term panics.

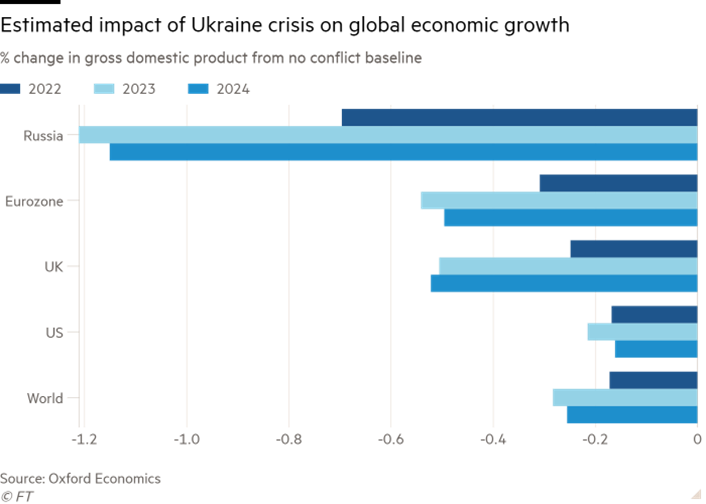

Although the stock market as measured by the S&P 500 index has gone gangbusters over the last three years, almost doubling in value (2019: +29%, 2020: +16%, 2021: +27%), the S&P 500 has hit an air pocket during the first couple months of 2022 (-8%), including down -3% in February. The year started with turbulence as investors became fearful of a Federal Reserve that is entering the beginning stages of interest rate hikes while cutting stimulative bond purchases. And then last month, the Russian-Ukrainian incursion made investors even more skittish. Like always, these geopolitical events tend to be short-lived once investors realize the impact turns out to be less meaningful than initially feared. As you can see below, the worst economic impact is forecasted to be felt by Russia (consensus on 2/24/22 of approximately a -1.0% hit to economic growth), more than twice as bad as the -0.2% to -0.4% knock to growth for the U.S., Europe, and the world (see chart below). The Russian hit will likely be worse after accelerated sanctions.

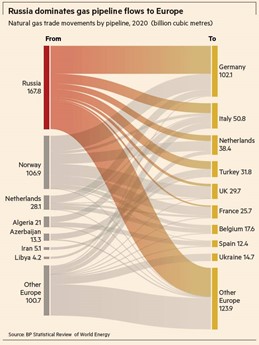

As it relates to Ukraine, many Americans don’t even know where the country is located on a map. Ukraine accounts for about only 0.14% of total global GDP (i.e., a rounding error and less than 1% of total global economic activity). Russia, although larger than Ukraine, is still a relative small-fry and represents only about 3% of total global economic activity. If you live in Europe during the winter, you might be a little more concerned about Vladimir Putin’s recent activities because a lot of Europe’s energy (natural gas) is supplied by Russia through Ukraine. For example, Germany receives about half of its natural gas from Russia (see chart below).

Russia, on the other hand, is larger than Ukraine, but the red country is still a relative small-fry representing only about 3% of total global economic activity. When it comes to energy production however, Russia is more than a rounding error because the country accounts for about 11% of global energy production (#3 country globally behind the United States and Saudi Arabia). By taking all these factors into account, we can confidently state that Russia and Ukraine have a very low probability of solely pulling the global economy into recession.

If history repeats itself, this conflict will turn out to be another garden variety decline in the stock market and an opportunity to buy at a discount. It’s virtually impossible to predict a short-term bottom in stock prices has been reached, but over the long-run, stock investors have been handsomely rewarded for not panicking and staying invested (see chart below).

At the end of the day, the daily headlines will continually attempt to sell the negative story that the world is coming to an end. If you have the fortitude and discipline to ignore the irrelevant noise, the status quo of normal volatility can create more exciting opportunities and better returns for long-term investors.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (March 1, 2022). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Brexit-Schmexit

Do you remember the panic-inducing headlines related to PIIGS, Crimea, Ebola, Cyprus, and the Flash Crash? Probably not. But if you do remember, these false alarms have likely been relegated to the financial memory graveyard, along with the many other sensationalist news events that have been killed off in the post-financial crisis era. Time will tell whether Brexit dies off or becomes a resurrected concern, like the repeating fears of a China slowdown or Greek collapse. Regardless, as the S&P 500 stock index reaches new all-time record highs, investors are currently shrug off the noise while muttering, “Brexit-Schmexit.”

Individuals have tried to use scary headlines as a timing tool to consistently time market corrections for all of recorded history. Unfortunately, emotional, knee-jerk reactions to alarming news stories rarely is the best strategy. Famed fund manager Peter Lynch said it best when he noted,

“Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.”

Having invested for some 25 years, experience has taught me not only is conventional wisdom often wrong, but it also is frequently an accurate contrarian indicator. In other words, frightening news often should be an indicator to buy…not sell. Case in point is the U.K. European Union referendum. The Brexit referendum “Leave” vote caught virtually everyone by surprise, but the rebound in stock prices to new record highs may be even more surprising to most observers. However, for investors following the key factors of interest rates, profits, valuation, and sentiment (see also Don’t Be a Fool, Follow the Stool), may not be shocked by the positive price action.

- Interest Rates: For starters, you don’t have to be a genius to realize that stocks become more attractive when there is a scarcity of investment alternatives. When there are an estimated $13 trillion of negative interest rate bonds, a layman can quickly understand a 2%, 3%, or 4% dividend yield offered on certain stocks (and funds) can represent a much more attractive opportunity. With interest rates at record lows (see chart below), the overall dividend yield of stocks has provided a floor for stock prices and has limited the depth and duration of sell-offs and corrections.

Source: Calafia Beach Pundit

- Profits: Corporate profits are near record highs but have been sluggish due to several factors, including the negative impact of the strong dollar on multinational exports; the depressing effect of declining interest rates on the banking sector’s net interest profit margins; the general decline in oil and commodity prices; and general lethargic economic growth overall in international markets (emerging and developed economies). Encouragingly, a stabilization in the value of the U.S. dollar, along with a rebound in energy prices augurs well for a potential shift back to earnings growth in the coming quarters.

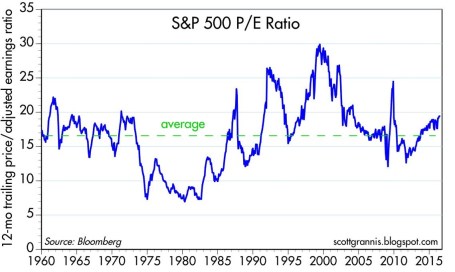

- Valuation: On a valuation basis, the Price/Earnings ratio of the stock market is about 10-15% above historical averages (see chart below). The average S&P 500 stock price trades around 19x’s the value of trailing twelve-month earnings. However, in the context of all-time record low-interest rates, a premium valuation is well deserved, especially for those companies paying a dividend and growing their bottom line.

Source: Calafia Beach Pundit

- Sentiment: Since the Great Financial Crisis / Recession, there has been about $1.5 trillion in equity investments that have been pulled out of U.S. equity mutual funds. This statistic is a clear sign of the extreme risk aversion and pervasive pessimism. Despite money flowing out of equity funds, corporations have bolstered the upward trajectory in stock prices with hundreds of billions in corporate stock buybacks and trillions in mergers & acquisition transactions. With all the universal jitteriness, I like to remind investors of Warren Buffett’s credo, “Buy fear, and sell greed.”

Brexit-Schmexit NOT Brexit-Panic

Despite the risk aversion in the marketplace, stock prices in the U.S. continue to grind higher to record levels. The stock market is currently communicating interest rates, profits, valuation, and sentiment are more important factors to price direction than are Brexit and other geopolitical concerns.

The silver lining behind severe investor skepticism is the creation of additional investment opportunities. As famous investor Sir John Templeton stated regarding stock market cycles, “Bull markets are born on pessimism and they grow on skepticism, mature on optimism, and die on euphoria.” Even the most objective observers have difficulty pointing to a broad set of indicators signaling euphoria, and the recent Turkish military coup attempt and domestic gun violence incidents will not squash out the negativity. Until optimism and elation rule the day, there’s no need to worry-schworry.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds , but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Brexit Briefing

Pair of British Briefs

There is no shortage of Brexit articles, but as I compile information for my monthly newsletter later this week (subscribe at Investing Caffeine – right column), here are some of my favorite links:

1) How to Make Sense of the Brexit Turmoil (FiveThirtyEight)

2) Brexit Meltdown Charts (Ritholtz)

3) House of Commons UK-EU Economic Relations Report (Parliament Research Briefings)

4) What is article 50 and why is it so central to the Brexit debate? (The Guardian)

5) The Difference Between the EU and Euro Zone (Moody’s)

6) Brexit’s First 100 Days (Bloomberg)

7) Brexit Impact on Wimbledon Paychecks (Fox Sports)

8) Relationship Between the U.K., Britain, England, Great Britain, Ireland, Northern Island, Wales, and British Isles (Project Britain)

9) Brexit Voting Results by Age (Ben Riley-Smith – Twitter)

10) Brexit Impact on Global Economy (Wall Street Journal)

11) Brexit is Not the End of the World (Calafia Beach Pundit)

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds , but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Solving Europe and Your Deadbeat Cousin

The fall holidays are quickly approaching, and almost every family has at least one black-sheep member among the bunch. You know, the unemployed second cousin who shows up for Thanksgiving dinner intoxicated – who then proceeds to pull you aside after a full meal to ask you for some money because of an unlucky trip to Las Vegas. For simplicity purposes, let’s name our deadbeat cousin Joe.

Right now the European union (EU) is dealing with a similar situation, but rather than being forced to deal with money-begging cousin named Joe, the EU is being forced to confront the irresponsible debt-binging practices of its own relatives – the PIIGS (Portugal, Ireland, Italy, Greece, and Spain). The European troika (International Monetary Fund/IMF; European Union/EU; and European Central Bank/ECB), spearheaded by German and French persuasion, is contemplating everything from prescribing direct bank recapitalization, bailouts via the leveraging of the EFSF (European Financial Stability Facility), ECB bond purchases, debt guarantees, unlimited central bank loans, and more.

New stress tests are being reevaluated as we speak. Previous tests failed in gaining the necessary credibility because inadequate haircuts were applied to the values of PIIGS debt held by European banks. European Leaders are beginning to gain some religion as to the urgency and intensity of the financial crisis. Just today, Germany’s chancellor (Angela Merkel) and France’s President (Nicolas Sarkozy) announced that they will introduce a comprehensive package of measures to stabilize the eurozone by the end of this month, right before the summit of the G20 leading global economies in Cannes, France.

Pick Your Poison

Whatever the path used to mop up debt excesses, the options for solving the financial mess can be lumped together in the following categories:

1. Austerity: Plain, unadulterated spending cuts is one prescription being administerd in hopes of curing bloated European sovereign debt issues. Negatives: Slowing economic growth, slowing tax receipts, potentially widening deficits (reference Greece), and political reelection self interests call into question the feasibility of the austerity option. Positives: Austerity is a morally correct fiscal response, which has the potential of placing a country’s financial situation back on a sustainable path.

2. Bailouts: The troika is also talking about infusing the troubled banks with new capital. Negatives: This action could result in more debt placed on country balance sheets, a potentially lower credit rating, higher costs of borrowing, higher tax burden for blameless taxpayers, and often an impossible political path of success. Positives: Financial markets may respond constructively in the short-run, but providing an alcoholic more alcohol doesn’t solve long-term fiscal responsibility, and also introduces the problem of moral hazard.

3. Haircuts: Voluntary or involuntary haircuts to principal debt obligations may occur in conjunction with previously described bailout efforts, depending on the severity of debt levels. Negatives: There are many different sets of constituents and investors, which can make voluntary haircut/debt restructuring terms difficult to agree upon. If the haircuts are too severe, banking reserves across the EU will become decimated, which will only lead to more austerity, bailouts, and potential credit downgrades. Such actions could hamper or eliminated future access to capital, and the cost of access to future capital could be cost prohibitive for the borrowing countries that defaulted/restructured. Positives: Haircuts eliminate or lessen the need for other more painful austerity or restructuring measures, and force borrowers to become more fiscally responsible, not to mention, investors are forced to conduct more thorough due diligence.

4. Printing Press: Buying back debt with freshly printed euros hot off the press is another strategy. Negatives: Inflation is an invisible tax on everyone, including those constituents who are behaving in a fiscally responsible manner. Positives: Not only is this strategy more politically palatable because the inflation tax is spread across the whole union, but this path to debt reduction also does not require as painful and unpopular cuts in spending as experienced in other options.

The Costs

What is the cost for this massive European debt-binging rehabilitation? Estimates vary widely, but a JP Morgan analyst sized it up this way as explained in the The Financial Times:

“In a worst-case, severe recession scenario, €230bn in new capital is needed to meet Basel III requirements, assuming a 60 per cent debt writedown on Greece, 40 per cent on Ireland and Portugal and 20 per cent on Italy and Spain, and that banks withhold dividends.”

More bearish estimates with larger bond loss haircuts, stricter regulatory guidelines, and harsher austerity measures have generated recapitalization numbers north of €1 trillion euros. Regardless of the estimates, European governments, regulators, and central banks are likely to select a combination of the poisons listed above. There is no silver bullet solution, and any of the chosen paths come with their own unique set of consequences.

As time passes and the European crisis matures, I am confident that you will be hearing more about ECB involvement and the firing-up of the printing presses. Perhaps the ECB will fund and work jointly with the EFSF to soak up debt and/or capitalize weak banks. Alternatively, and more simply, the ECB is likely to follow the path of the U.S. and implement significant amounts of quantitative easing (i.e., provide liquidity to the financial system via sovereign debt purchases and guarantees).

Dealing with irresponsible and intoxicated deadbeat second cousins (or European countries) fishing for money is never a pleasurable experience. There are many ways to address the problem, but ignoring the issue will only make the situation worse. Fortunately, our European friends on the other side of the pond appear to be taking notice. As in the U.S., if government officials delay or ignore the immediate problems, the financial market cops (a.k.a., “bond vigilantes”) will force them into action. In the recent past, European officials have used a strategy of sober talking “tough love,” but signs that the ECB printing presses are now beginning to warm up are evident. Once the euros come flying off the presses to detoxify the debt binging banks, perhaps the ECB can print a few extra euros for my cousin Joe.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in JPM, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}