Posts tagged ‘Daniel Kahneman’

Brain or Machine? Investing Holy Grail

Source: Photobucket

Paul Meehl was a versatile academic who held numerous faculty positions, covering the diverse disciplines of psychology, law, psychiatry, neurology, and yes, even philosophy. The crux of his research was focused on how well clinical analysis fared versus statistical analysis. Or in other words, he looked to answer the controversial question, “What is a better predictor of outcomes, a brain or an equation?” His conclusion was straightforward – mechanical methods using quantitative measures are much more efficient than the professional judgments of humans in coming to more accurate predictions.

Those who have read my book, How I Managed $20,000,000,000.00 by Age 32 know where I stand on this topic – I firmly believe successful investing requires a healthy balance between both art and science (i.e., “brain and equation”). A trader who only relies on intuition and his gut to make all of his/her decisions is likely to fall on their face. On the other hand, a quantitative engineer’s sole dependence on a robotic multi-factor model to make trades is likely to fail too. My skepticism is adequately outlined in my Butter in Bangladesh article, which describes how irrational statistical games can be misleading and overused.

As much as I would like to attribute all of my investment success to my brain, the emotion-controlling power of numbers has played an important role in my investment accomplishments as well. The power of numbers simply cannot be ignored. More than 50 years after Paul Meehl’s seminal research was published, about two hundred studies comparing brain power versus statistical power have shown that machines beat brains in predictive accuracy in the majority of cases. Even when expert judgments have won over formulas, human consistency and reliability have muddied the accuracy of predictions.

Daniel Kahneman, a Nobel Prize winner in Economics, highlights another important decision making researcher, Robyn Dawes. What Dawes discovers in her research is that the fancy and complex multiple regression methods used in conventional software adds little to no value in the predictive decision-making process. Kahneman describes Dawes’s findings more specifically here:

“A formula that combines these predictors with equal weights is likely to be just as accurate in predicting new cases as the multiple-regression formula…Formulas that assign equal weights to all the predictors are often superior, because they are not affected by accidents of sampling…It is possible to develop useful algorithms without any prior statistical research. Simple equally weighted formulas based on existing statistics or on common sense are often very good predictors of significant outcomes.”

The results of Dawes’s classic research have significant application to the field of stock picking. As a matter of fact, this type of research has had a significant impact on Sidoxia’s stock selection process.

How Sweet It Is!

In the emotional roller-coaster equity markets we’ve experienced over the last decade or two, overreliance on gut-driven sentiments in the investment process has left masses of casualties in the wake of losses. If you doubt the destructive after-effects on investors’ psyches, then I urge you to check out my Fund Flow Paradox article that shows the debilitating effects of volatility on investors’ behavior.

In order to more objectively exploit investment opportunities, the Sidoxia Capital Management investment team has successfully formed and utilized our own proprietary quantitative tool. The results were so sweet, we decided to call it SHGR (pronounced “S-U-G-A-R”), or Sidoxia Holy Grail Ranking.

My close to two decades of experience at William O’Neil & Co., Nicholas Applegate, American Century Investments, and now Sidoxia Capital Management has allowed me to build a firm foundation of growth investing competency – however understanding growth alone is not sufficient to succeed. In fact, growth investing can be hazardous to your investment health if not kept properly in check with other key factors.

Here are some of the key factors in our Sidoxia SHGR ranking system:

Valuation:

- Free cash flow yield

- Price/earnings ratio

- PEG ratio

- Dividend yield

Quality:

- Financials: Profit margin trends; balance sheet leverage

- Management Team: Track record; capital stewardship

- Market Share: Industry position; runway for growth

Contrarian Sentiment Indicators:

- Analyst ratings

- Short interest

Growth:

- Earnings growth

- Sales growth

Our proprietary SHGR ranking system not only allows us to prioritize our asset allocation on existing stock holdings, but it also serves as an efficient tool to screen new ideas for client portfolio additions. Most importantly, having a quantitative model like Sidoxia’s Holy Grail Ranking system allows investors to objectively implement a disciplined investment process, whether there is a presidential election, Fiscal Cliff, international fiscal crisis, slowing growth in China, and/or uncertain tax legislation. At Sidoxia we have managed to create a Holy Grail machine, but like other quantitative tools it cannot replace the artistic powers of the brain.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Controlling the Investment Lizard Brain

“Normal fear protects us; abnormal fear paralyses us.”

– Martin Luther King, Jr.

Investing is challenging enough without bringing emotions into the equation. Unfortunately, humans are emotional, and as a result investors often place too much reliance on their feelings, rather than using objective information to drive rational decision making.

What causes investors to make irrational decisions? The short answer: our “amygdala.” Author and marketer Seth Godin calls this almond-shaped tissue in the middle of our head, at the end of the brain stem, the “lizard brain” (video below). Evolution created the amygdala’s instinctual survival flight response for lizards to avoid hungry hawks and humans to flee ferocious lions.

Over time, the threat of lions eating people in our modern lives has dramatically declined, but the human’s “lizard brain” is still running in full gear, worrying about other fear-inducing warnings like Iran, Syria, Obamacare, government shutdowns, taxes, Cyprus, sequestration, etc. (see Series of Unfortunate Events)

When the brain in functioning properly, the prefrontal cortex (the front part of the brain in charge of reasoning) is actively communicating with the amygdala. Sadly, for many people, and investors, the emotional response from the amygdala dominates the rational reasoning portion of the prefrontal cortex. The best investors and traders have developed the ability of separating emotions from rational decision making, by keeping the amygdala in check.

With this genetically programmed tendency of constantly fearing the next lion or stock market crash, how does one control their lizard brain from making sub-optimal, rash investment decisions? Well, the first thing you should do is turn off the TV. And by turning off the TV, I mean stop listening to talking head commentators, economists, strategists, analysts, neighbors, co-workers, blogger hacks, newsletter writers, journalists, and other investing “wannabes”. Sure, you could throw my name into the list of people to ignore if you wanted to, but the difference is, at least I have actually invested real money for over 20 years (see How I Managed $20,000,000,000.00), whereas the vast majority of those I listed have not. But don’t take my word for it…listen or read the words of other experienced investors Warren Buffett, Peter Lynch, Ron Baron, John Bogle, Phil Fisher, and other investment titans (see also Sidoxia Hall of Fame). These investment legends have successful long-term investment track records and they lived through wars, recessions, financial crises, and other calamities…and still managed to generate incredible returns.

Another famed investor, William O’Neil, summed this idea nicely by adding the following:

“Since the market tends to go in the opposite direction of what the majority of people think, I would say 95% of all these people you hear on TV shows are giving you their personal opinion. And personal opinions are almost always worthless … facts and markets are far more reliable.”

The Harmful Consequence of Brain on Pain

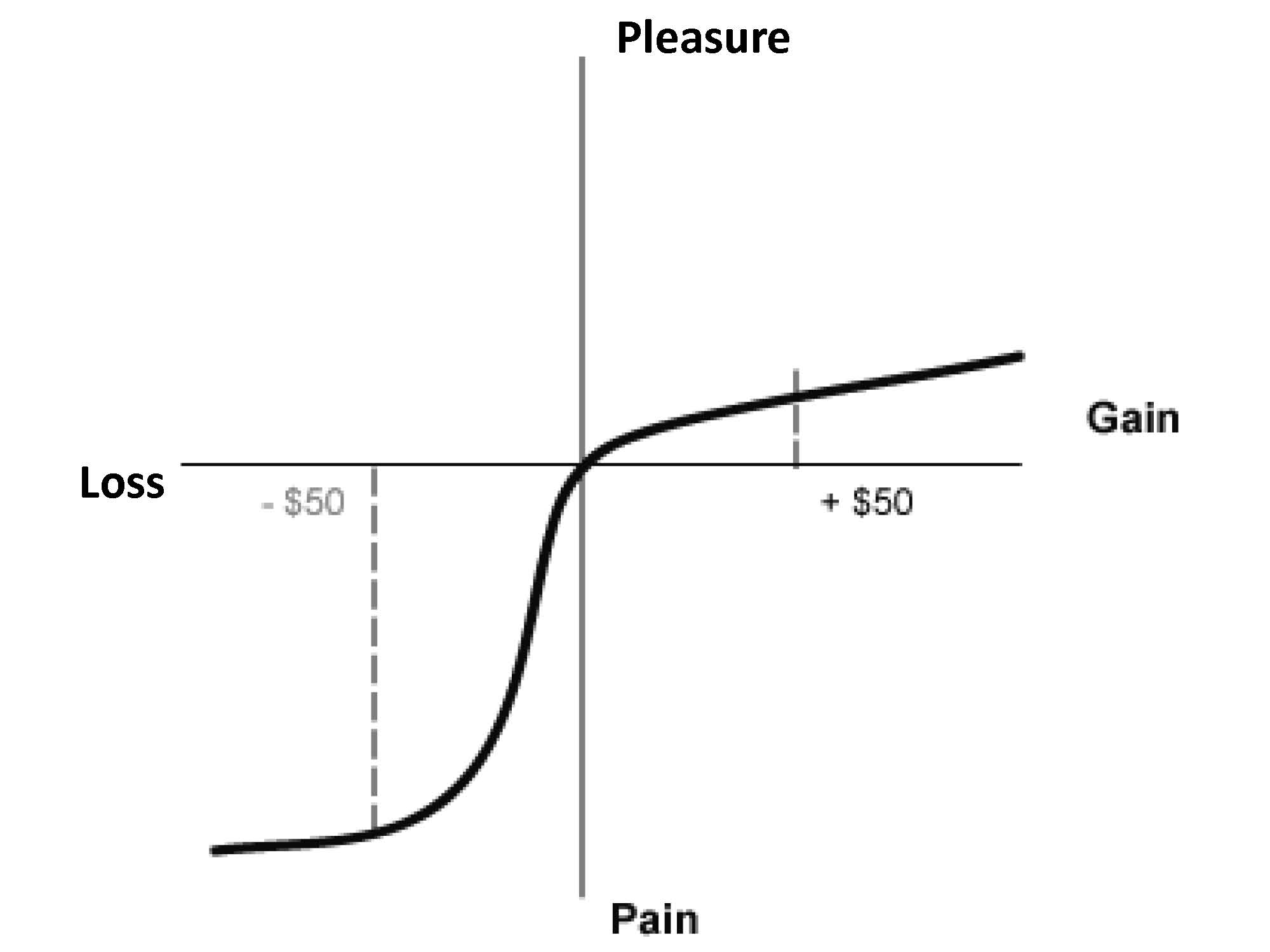

Besides forcing damaging decisions, another consequence of our lizard brain is its ability to distort reality. Behavioral economists Daniel Kahneman (Nobel Prize winner) and Amos Tversky through their research demonstrated the pain of $50 loss is more than twice as painful as the pleasure from $50 gain (see Pleasure/Pain Principle). Common sense would dictate our brains would treat equivalent scenarios in a proportional manner, but as the chart below shows, that is not the case:

Source: Investopedia

Kahneman adds to the decision-making relationship of the amygdala and prefrontal cortex by describing the concepts of instinctual and deliberative choices in his most recent book, Thinking Fast and Slow (see Decision Making on Freeways).

Optimizing Risk

Taking excessive risks in technology stocks in the 1990s or in housing in the mid-2000s was very damaging to many investors, but as we have seen, our lizard brains can cause investors to become overly risk averse. Over the last five years, many people have personally experienced the ill effects of unwarranted conservatism. Investment great Sir John Templeton summed up this risk by stating, “The only way to avoid mistakes is not to invest – which is the biggest mistake of all.”

Every person has a different perception and appetite for risk. The optimal amount of risk taken by any one investor should be driven by their unique liquidity needs and time horizon…not a perceived risk appetite. Typically risk appetites go up as markets peak, and conservatism reaches a fearful apex near market bottoms – the opposite tendency of rational decision making. Besides liquidity and time horizon, a focus on valuation coupled with diversification across asset class (stocks/bonds), geography (domestic/international), size (small/large), style (value/growth) is critical in controlling risk. If you can’t determine your personal, optimal risk profile, then find an experienced and knowledgeable investment advisor to assist you.

With the advent of the internet and mobile communication, our brains and amygdala continually get bombarded with fearful stimuli, leading to disastrous decision-making and damaging portfolio outcomes. Turning off the TV and selectively choosing the proper investment advice is paramount in keeping your amygdala in check. Your lizard brain may protect you from getting eaten by a lion, but falling prey to this structural brain flaw may eat your investment portfolio alive.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Jobs and the DMV Economy

If you have ever gone to get your driver’s license at the Department of Motor Vehicles (DMV)…you may still be waiting in line? It’s a painful but often a mandatory process, and in many ways the experience feels a lot like the economic recovery we currently have been living through over the last four years. Steady progress is being made, but in general, people hardly notice the economy moving forward.

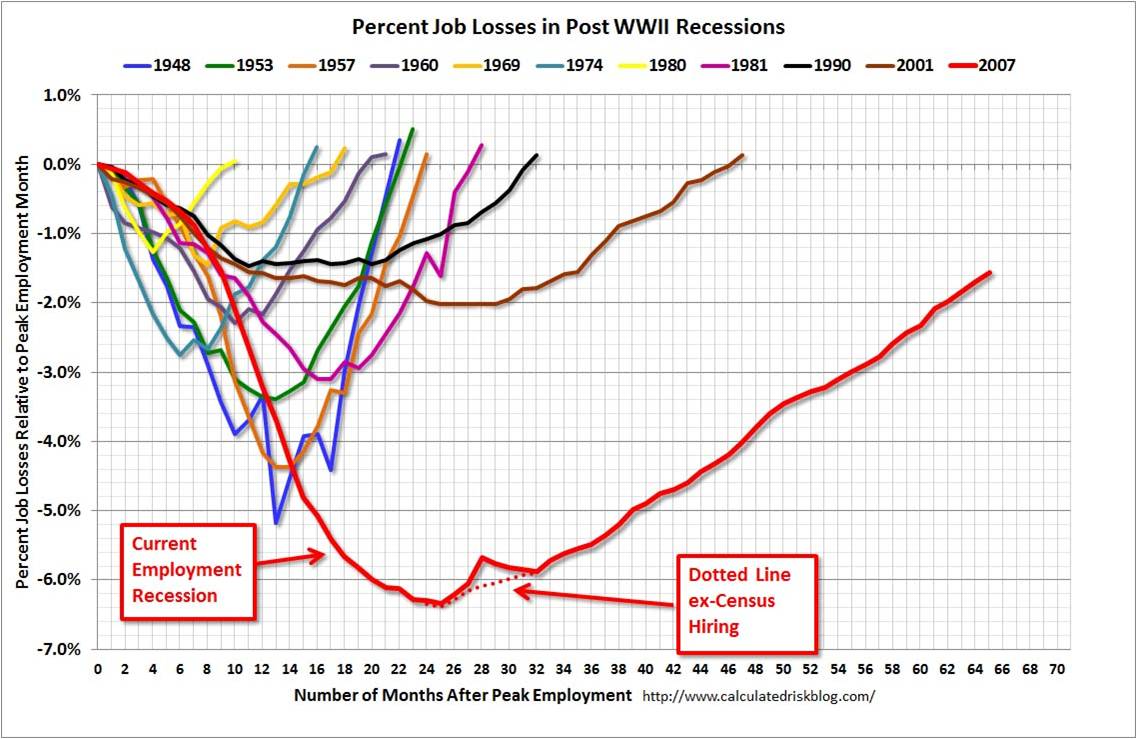

My geographic neighbor and blogger here in Orange County, California (Bill McBride – Calculated Risk) has some excellent visuals that compare our sluggish DMV economy with previous economic cycles dating back to 1948:

Source: Calculated Risk

As you can see from the chart above, the current economic recovery (red-line), as measured by job losses, is the slowest comeback in more than a half-century. Basically, over a two year period, the U.S. lost about nine million jobs, and during the following three years the economy regained approximately seven million of those jobs – still digging out of the hole. Last Friday’s June jobs report was welcomed, as it showed net jobs of +195,000 were added during the month, and importantly the previous two months were revised higher by another +70,000 jobs. These data points combined with last month’s Fed’s QE3 tapering comments by Ben Bernanke help explain why the continued rout in 10 year Treasury rates has continued in recent weeks, propelling the benchmark rate to 2.71% – almost double the 1.39% rate hit last year amidst continued European financial market concerns.

As with most recessions or crashes, the bursting of the bubble (i.e., damage) occurs much faster than the inflation (i.e., recovery), and McBride’s time series clearly shows this fact:

Source: Calculated Risk

While pessimists point to the anemic pace of the current recovery, the glass half-full people (myself included) appreciate that the sluggish rebound is likely to last longer than prior recoveries. There are two other key dynamics underlying the reported employment figures:

- Continued Contraction in Government Workers: Excessive government debt and deficits have led to continued job losses – state and local job losses appear to be stabilizing but federal cuts are ongoing.

- Decline in the Labor Force Participation Rate: Discouraged workers and aging Baby Boomer demographics have artificially lowered the short-term unemployment figures because fewer people are looking for work. If economic expansion accelerates, the participation contraction trend is likely to reverse.

Skepticism Reigns Supreme

Regardless of the jobs picture and multi-year expansion, investors and business managers alike remain skeptical about the sustainability of the economic recovery. Anecdotally I encounter this sentiment every day, but there are other data points that bolster my assertion. Despite the stock market more than doubling in value from the lows of 2009, CNBC viewer ratings are the weakest in about 20 years (see Value Walk) and investments in the stock market are the lowest in 15 years (see Gallup poll chart below):

Source: Gallup

Why such skepticism? Academic research in behavioral finance highlights innate flaws in human decision-making processes. For example, humans on average weigh losses twice as much as gains as economist and Nobel prizewinner Daniel Kahneman explains in his book Thinking Fast and Slow (see Investing Caffeine article: Decision Making on Freeways and in Parking Lots). Stated differently, the losses from 2008-2009 are still too fresh in the minds of Americans. Until the losses are forgotten, and/or the regret of missing gains becomes too strong, many investors and managers will fearfully remain on the sideline.

The speed of our economic recovery is as excruciatingly agonizing, and so is waiting in line at the DMV. The act of waiting can be horrific, but obtaining a driver’s license is required for driving and investing is necessary for retirement. If you don’t want to go to investing jail, then you better get in the investing line now before job growth accelerates, because you don’t want to be sent to the back of the line where you will have to wait longer.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Decision Making on Freeways and in Parking Lots

Many drivers here in California adhere to the common freeway speed limit of 65 miles per hour, while some do not (I’ll take the 5th). In the vast majority of cases, racing to your destination at these faster speeds makes perfect sense. However, driving 65 mph through the shopping mall parking lot could get you killed, so slower driving is preferred in this instance. Ultimately, the specific environment and situation will dictate the rational and prudent driving speed. Decision making works in much the same way, and Daniel Kahneman, a Nobel Prize winner, has encapsulated his decades of research in psychology and economics in his most recent book, Thinking, Fast and Slow.

Much of Kahneman’s big ideas are analyzed through the lenses of “System 1” and “System 2” – the fast and slow decision-making processes persistently used by our brains. System 1 thinking is our intuition in the fast lane, continually making judgments in real-time. Our System 1 hunches are often correct, but because of speedy, inherent biases and periodic errors this process can cause us to miss an off-ramp or even cause a conclusion collision. System 2, on the other hand, is the slower, methodical decision-making process in our brains that keeps our hasty System 1 process in check. Although little mental energy is exerted by using System 1, a great deal of cerebral horsepower is required to use System 2.

Summarizing 512 pages of Kahneman’s book in a single article may be challenging, nevertheless I will do my best to summarize some of the interesting highlights and anecdotes. A multitude of Kahneman’s research is reviewed, but a key goal of the book is designed to help individuals identify errors in judgment and biases, in order to lower the prevalence of mental mistakes in the future.

Over Kahneman’s 50+ year academic career, he has uncovered an endless string of flaws in the human thought process. To bring those mistakes to life, he uses several mind experiments to illustrate them. Here are a few:

Buying Baseball: We’ll start off with a simple Kahneman problem. If a baseball bat and a ball cost a total of $1.10, and the bat costs $1 more than the ball, then how much does the ball cost? The answer is $0.10, right? WRONG! Intuition and the rash System 1 forces most people to answer $0.10 cents for the ball, but after going through the math it becomes clear that this gut answer is wrong. If the ball is $0.10 and the bat is $1 more, then that would mean the bat costs $1.10, making the total $1.20…WRONG! This is clearly a System 2 problem, which requires the brain to see a $0.05 ball plus $1.05 bat equals $1.10…CORRECT!

The Invisible Gorilla: As Kahneman points out, humans can be blind to the obvious and blind to our blindness. To make this point he references an experiment and book titled Invisible Gorilla, created by Chritopher Chabris and Daniel Simons. In the experiment, three players wearing white outfits pass a basketball around at the same time that a group of players wearing black outfits pass around a separate basketball. The anomaly in the experiment occurs when someone in a full-sized gorilla outfit goes prancing through the scene for nine full seconds. To the surprise of many, about half of the experiment observers do not see the gorilla. In addition, the gorilla-blind observers deny the existence of the large, furry animal when confronted with recorded evidence (see video below).

Green & Red Dice: In this thought experiment, Kahneman describes a group presented with a regular six-sided die with four green sides (G) and two red sides (R), meaning the probability of the die landing on green (G) is is much higher than the probability of landing on red (R). To make the experiment more interesting, the group is provided a cash prize for picking the highest probability scenario out of the following three sequences: 1) R-G-R-R-R; 2) G-R-G-R-R-R; and 3) G-R-R-R-R-R. Although most participants pick sequence #2 because it has the most greens (G) in it, if one looks more closely, sequence #2 is the same as #1 except for sequence #2 has an additional green (G). Therefore, the highest probability winning answer should be sequence #1 because sequence #2 adds an uncertain roll that may or may not land on green (G).

While the previous experiments described some notable human decision-making flaws, here are some more human flaws:

Anchoring Effect: Was Gandhi 114 when he died, or was Gandhi 35 when he died? Depending how the question is asked, asking the initial question first will skew the respondents answer to a higher age, because the respondents answer will be somewhat anchored to the number “114”. Similarly, the price a homebuyer would pay for a house will be influenced or anchored to the asking price. Another word used by some for anchoring is “suggestion”. If a subliminal suggestion is planted, people’s responses can become anchored to that idea.

Overconfidence: We encounter overconfidence in several forms, especially from what Kahneman calls the “Illusion of Pundits,” which is the confidence that comes with 20-20 hindsight experienced in our 24/7 media world. Or as Kahneman states in a different way, “The illusion that we understand the past fosters overconfidence in our ability to predict the future.” Driving is another example of overconfidence – very few people believe they are poor drivers. In fact, a well-known study shows that “90% of drivers believe they are better than average,” despite defying the laws of mathematics.

Risk Aversion: In Kahneman’s book, he also references risk aversion studies by Mathew Rabin and Richard Thaler. What the researchers discovered is that people appear to be irrational in the way they respond to certain risk scenarios. For example, people will turn down the following gambles:

A 50% chance to lose $100 and a 50% chance to win $200;

OR

A 50% chance to lose $200 and a 50% chance to win $20,000 .

Although rational math would indicate these are smart bets to take, however most people decline the game because humans on average weigh losses twice as much as gains (see also the Pleasure/Pain Principle). To get a better understanding of predictive human behavior, the real emotional costs of disappointment and regret need to be accounted for.

Truth Illusions: A reliable way to make people believe in falsehoods is through repetition. More exposure will breed more liking. In addition to normal conversations, these repetitive truth illusions can be witnessed in propaganda or advertising. Minimizing cognitive strain also reinforces points. Using bold, colored, and contrasted language is more convincing. Simpler language rather than more complex language is also more credible.

Narrative Fallacies: We humans have an innate desire to continually explain the causation of an event due to skill or stupidity – even if randomness is the best explanation.People try to make sense of the world, even though many outcomes have no straightforward explanation. Often times, a statistical phenomenon like “regression to the mean” can explain the results (i.e., outliers revert directionally toward averages). The “Sports Illustrated Jinx,” or the claim that a heralded cover story athlete will be subsequently cursed with bad performance, is used as a case in point. Actually, there is no jinx or curse, but often fickle luck disappears and athletic performance reverts to norms.

Kahneman on Stocks

Many of the principles in Kahneman’s book can be applied to the world of stocks and investing too. According to Kahneman, the investing industry has been built on an “illusion of skill,” or the belief that one person has better information than the other person. To make his point, Kahneman references research by Terry Odean, a finance professor at UC Berkely, who studied the records of 10,000 brokerage accounts of individual investors spanning a seven-year period and covering almost 163,000 trades. The net result showed dramatic underperformance by the individual traders and confirmed that stocks sold by the traders consistently did better than the stocks purchased.“Taking a shower and doing nothing” would have been better than the value destroying trading activity. In fact, the most active traders did much worse than those who traded the least. For professional managers the conclusions are not a whole lot different. “For a large majority of fund managers, the selection of stocks is more like rolling dice than like playing poker. Typically at least two out of every three mutual funds underperform the overall market in any given year,” says Kahneman. I don’t disagree, but I do believe, like .300 hitters in baseball, there are a few managers that can consistently outperform.

There are a lot of lessons to be learned from Daniel Kahneman’s book Thinking, Fast and Slow and I apply many of his conclusions to my investment practice at Sidoxia. We all race through decisions every day, but as he repeatedly points out, familiarizing ourselves with these common mental pitfalls, and also utilizing our more methodical and accurate System 2 thought process regularly, can create better decisions. Better decisions not only for our regular lives, but also for our investing lives. It’s perfectly OK to race down the mental freeway at 65 mph (or faster), but don’t forget to slow down occasionally, in order to avoid mental collisions.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Investing Holy Grail: Brain or Machine?

Source: Photobucket

Paul Meehl was a versatile academic who held numerous faculty positions, covering the diverse disciplines of psychology, law, psychiatry, neurology, and yes, even philosophy. The crux of his research was focused on how well clinical analysis fared versus statistical analysis. Or in other words, he looked to answer the controversial question, “What is a better predictor of outcomes, a brain or an equation?” His conclusion was straightforward – mechanical methods using quantitative measures are much more efficient than the professional judgments of humans in coming to more accurate predictions.

Those who have read my book, How I Managed $20,000,000,000.00 by Age 32 know where I stand on this topic – I firmly believe successful investing requires a healthy balance between both art and science (i.e., “brain and equation”). A trader who only relies on intuition and his gut to make all of his/her decisions is likely to fall on their face. On the other hand, a quantitative engineer’s sole dependence on a robotic multi-factor model to make trades is likely to fail too. My skepticism is adequately outlined in my Butter in Bangladesh article, which describes how irrational statistical games can be misleading and overused.

As much as I would like to attribute all of my investment success to my brain, the emotion-controlling power of numbers has played an important role in my investment accomplishments as well. The power of numbers simply cannot be ignored. More than 50 years after Paul Meehl’s seminal research was published, about two hundred studies comparing brain power versus statistical power have shown that machines beat brains in predictive accuracy in the majority of cases. Even when expert judgments have won over formulas, human consistency and reliability have muddied the accuracy of predictions.

Daniel Kahneman, a Nobel Prize winner in Economics, highlights another important decision making researcher, Robyn Dawes. What Dawes discovers in her research is that the fancy and complex multiple regression methods used in conventional software adds little to no value in the predictive decision-making process. Kahneman describes Dawes’s findings more specifically here:

“A formula that combines these predictors with equal weights is likely to be just as accurate in predicting new cases as the multiple-regression formula…Formulas that assign equal weights to all the predictors are often superior, because they are not affected by accidents of sampling…It is possible to develop useful algorithms without any prior statistical research. Simple equally weighted formulas based on existing statistics or on common sense are often very good predictors of significant outcomes.”

The results of Dawes’s classic research have significant application to the field of stock picking. As a matter of fact, this type of research has had a significant impact on Sidoxia’s stock selection process.

How Sweet It Is!

In the emotional roller-coaster equity markets we’ve experienced over the last decade or two, overreliance on gut-driven sentiments in the investment process has left masses of casualties in the wake of losses. If you doubt the destructive after-effects on investors’ psyches, then I urge you to check out my Fund Flow Paradox article that shows the debilitating effects of volatility on investors’ behavior.

In order to more objectively exploit investment opportunities, the Sidoxia Capital Management investment team has successfully formed and utilized our own proprietary quantitative tool. The results were so sweet, we decided to call it SHGR (pronounced “S-U-G-A-R”), or Sidoxia Holy Grail Ranking.

My close to two decades of experience at William O’Neil & Co., Nicholas Applegate, American Century Investments, and now Sidoxia Capital Management has allowed me to build a firm foundation of growth investing competency – however understanding growth alone is not sufficient to succeed. In fact, growth investing can be hazardous to your investment health if not kept properly in check with other key factors.

Here are some of the key factors in our Sidoxia SHGR ranking system:

Valuation:

- Free cash flow yield

- Price/earnings ratio

- PEG ratio

- Dividend yield

Quality:

- Financials: Profit margin trends; balance sheet leverage

- Management Team: Track record; capital stewardship

- Market Share: Industry position; runway for growth

Contrarian Sentiment Indicators:

- Analyst ratings

- Short interest

Growth:

- Earnings growth

- Sales growth

Our proprietary SHGR ranking system not only allows us to prioritize our asset allocation on existing stock holdings, but it also serves as an efficient tool to screen new ideas for client portfolio additions. Most importantly, having a quantitative model like Sidoxia’s Holy Grail Ranking system allows investors to objectively implement a disciplined investment process, whether there is a presidential election, Fiscal Cliff, international fiscal crisis, slowing growth in China, and/or uncertain tax legislation. At Sidoxia we have managed to create a Holy Grail machine, but like other quantitative tools it cannot replace the artistic powers of the brain.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Experts vs. Dart-Throwing Chimps

Daniel Kahneman, a professor of psychology at Princeton University, knows a few things about human behavior and decision making, and he has a Nobel Prize in Economics to prove it. We live in a complex world and our brains will often try to compensate by using shortcuts (or what Kahneman calls “heuristics” and “biases”), in hopes of simplifying complicated situations and problems.

When our brains become lazy, or we are not informed in a certain area, people tend to also listen to so-called experts or pundits to clarify uncertainties. In the process of their work, Kahneman and other researchers have discovered something – experts should be listened to as much as monkeys. Frequent readers of Investing Caffeine understand my shared skepticism of the talking heads parading around on TV (read first entry of 10 Ways to Destroy Your Portfolio)

Here is how Kahneman describes the reliability of professional forecasts and predictions in his recently published bestseller, Thinking, Fast and Slow:

“People who spend their time, and earn their living, studying a particular topic produce poorer predictions than dart-throwing monkeys who would have distributed their choices evenly over the options.”

Most people fall prey to this illusion of predictability created by experts, or this idea that more knowledge equates to better predictions and forecasts. One of the factors perpetuating this myth is the rearview mirror. In other words, human’s ability to concoct a credible story of past events creates a false confidence in peoples’ ability to accurately predict the future.

Here’s how Kahneman describes the phenomenon:

“The idea that the future is unpredictable is undermined every day by the ease with which the past is explained…Our tendency to construct and believe coherent narratives of the past makes it difficult for us to accept the limits of our forecasting ability. Everything makes sense in hindsight, a fact financial pundits exploit every evening as they offer convincing accounts of the day’s events. And we cannot suppress the powerful intuition that what makes sense in hindsight today was predictable yesterday. The illusion that we understand the past fosters overconfidence in our ability to predict the future.”

Even when experts are wrong about their predictions, they tend to not accept accountability. Rather than take responsibility for a bad prediction, Philip Tetlock says the errors are often attributed to “bad timing” or an “unforeseeable event.” Philip Tetlock, a psychologist at the University of Pennsylvania did a landmark twenty-year study, which was published in his book Expert Political Judgment: How Good Is It? How Can We Know? (read excellent review in The New Yorker). In the study Tetlock interviewed 284 economic and political professionals and collected more than 80,000 predictions from them. The results? The experts did worse than blind guessing.

Based on the extensive training and knowledge of these experts, many of them develop a false sense of confidence in their predictions. Or as Tetlock explains it, “They [experts] are just human in the end. They are dazzled by their own brilliance and hate to be wrong. Experts are led astray not by what they believe, but by how they think.”

Brain Blunders and Stock Picking

The buyer of a stock thinks the price will go up and the seller of a stock thinks the price will go down. Both participants engage in the transaction because they believe the current stock price is wrong. The financial services industry is built largely on this phenomenon that Kahneman calls an “illusion of skill,” or ability to exploit inefficient market pricing. Relentless advertisements and marketing pitches continually make the case that professionals can outperform the markets, but this is what Kahneman found:

“Although professionals are able to extract a considerable amount of wealth from amateurs, few stock pickers, if any, have the skill needed to beat the market consistently, year after year. Professional investors, including fund managers, fail a basic test of skill: persistent achievement…Skill in evaluating the business prospects of a firm is not sufficient for successful stock trading, where the key question is whether the information about the firm is already incorporated in the price of its stock. Traders apparently lack the skill to answer this crucial question, but they appear ignorant of their ignorance.”

For the few managers that actually do outperform, Kahneman assigns luck to the outcome, not skill:

“For a large majority of fund managers, the selection of stocks is more like rolling dice than like playing poker. Typically at least two out of three mutual funds underperform the overall market in any given year…The successful funds in any given year are mostly lucky; they have a good roll of the dice.”

The picture for individual investors isn’t any prettier. Evidence from Terry Odeam, a finance professor at UC Berkeley, who studied 100,000 individual brokerage account statements and about 163,000 trades over a seven-year period, was not encouraging. He discovered that stocks sold actually did +3.2% better than the replacement stocks purchased. And this detrimental impact on performance excludes the significant expenses related to trading.

In response to Odean’s work, Kahneman states:

“It is clear that for the large majority of individual investors, taking a shower and doing nothing would have been a better policy than implementing the ideas that came to their minds….Many individual investors lose consistently by trading, an achievement that a dart-throwing chimp could not match.”

In a future Odean paper titled, “Trading is Hazardous to your Wealth,” Odean and his colleague Brad Barber also proved that “less is more.” The results showed the most active traders had the weakest performance, and those traders who traded the least had the best returns. Interestingly, women were shown to have better investment results than men.

Regardless of whether someone is listening to an expert, fund manager, or individual investor, what Daniel Kahneman has discovered in his long, illustrious career is that humans consistently make errors. If you are wise, you will heed Kahneman’s advice by stealing the expert’s darts and handing them over to the chimp.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

The Pleasure/Pain Principle

The financial crisis of 2008-2009 was painful, not to mention the Flash Crash of 2010; the Debt Ceiling / Credit Downgrade of 2011; and the never-ending European saga. Needless to say, these and other events have caused pain akin to burning one’s hand on the stove. This unpleasant effect has rubbed off on investors.

Admitting one has a problem is half the battle of conquering a challenge. A key challenge for many investors is understanding the crippling effects fear can have on personal investment decisions. While there are certainly investors who constantly see financial markets through rose-colored glasses (my glasses I argue are only slightly tinted), Nobel Prize winner Daniel Kahneman and his partner Amos Tversky understand the pain of losses can be twice as painful as the pleasure experienced through gains (see diagram below).

Source: Investopedia

Said a little differently, faced with sure gain, most investors are risk-averse, but faced with sure loss, investors prefer risk-taking. Don’t believe me? Well, let’s take a look at some of Kahneman and Tversky’s behavioral finance work on what they called “Prospect Theory” (1979) – the analysis of decisions made under various risk scenarios.

In one specific experiment, Kahneman and Tversky presented groups of subjects with a number of problems. One group of subjects was presented with this problem:

Problem #1: In addition to whatever you own, you have been given $1,000. You are now asked to choose between:

A. A sure gain of $500

B. A 50% change to gain $1,000 and a 50% chance to gain nothing.

Another group of subjects was presented with this problem:

Problem #2: In addition to whatever you own, you have been given $2,000. You are now asked to choose between:

A. A sure loss of $500

B. A 50% chance to lose $1,000 and a 50% chance to lose nothing.

In the first group, 84% of the respondents chose A and in the second group, 69% of the respondents chose B. Both problems are identical in terms of the net cash outcomes ($1,500 for Answer A, and 50% chance of $1,000 or $2,000 for Answer B). Nonetheless, due the different “loss phrasing” in each question, Answer A sounds more appealing in Question #1, and Answer B sounds more appealing in Question #2. The results are irrational, but investors have been known to be illogical too.

In practical trading terms, the application of “Prospect Theory” often manifests itself via the pain principle. Due to loss aversion, investors tend to cash in gains too early and fail to allow their winning stocks to run higher for a long enough period.

The framing of the Kahneman and Tversky’s questions is no different than the framing of political and economic issues by the various media outlets (see Pessimism Porn). Fear can generate advertising revenue and fear can also push investors into paralysis (see the equity fund flow data in Fund Flows Paradox).

Greed can sell in the financial markets too. The main sources of financial market greed have been primarily limited to bonds, cash, and gold. If you caught those trends early enough, you are happy as a clam, but like most things in life, nothing lasts forever. The same principle applies to financial markets, and over time, capital in today’s winners will slowly transition into today’s losers (i.e., tomorrow’s winners).

A healthy amount of fear is healthy, but correctly understanding the dynamics of the “Pleasure/Pain Principle” can turn those fearful tears into profitable pleasure.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including fixed income ETFs), but at the time of publishing SCM had no direct position in GLD, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}