Posts tagged ‘china’

Rise of the Robots

We’re losing our jobs to robots, and they will destroy our economy. It makes for a great news soundbite, but has no factual basis in reality, if you look at the actual trajectory of automation and technology innovations throughout history. The global economy did not collapse when the steam engine replaced the oar; the automobile supplanted the horse; the computer became a substitute for the abacus; and the combine killed off the farmer. The same notion holds true today as robots become more ubiquitous in our daily commercial and personal lives.

From the early, post-revolutionary birth of our country in the 18th century, the agrarian economy accounted for upwards of 90% of jobs and financial activity…until farming technology evolved (see chart below). As new agricultural advancements were introduced, like the cotton gin, plow, scythe, chemical fertilizers, tractors, combine harvesters, and genetically engineered seeds, human capital (jobs) were redeployed into other growth sectors of the economy (e.g., factories, aerospace, semiconductors, medicine, etc.).

Source: Carpe Diem

Given that human labor accounts for about 2/3 of an average company’s expense structure, it should come as no surprise that corporations are looking to reduce costs by introducing more robotics and automation into their processes. The advantages to robotics adoption are numerous and I describe many of the reasons in my article, Chainsaw Replaces Paul Bunyan:

A robot won’t ask for a raise; it always shows up on time; you don’t have to pay for its healthcare; it can work 24/7/365 days per year; it doesn’t belong to a union; dependable quality consistency is a given; it produces products near your customers; and it won’t sue for discrimination or sexual harassment.

At Sidoxia Capital Management we opportunistically identified this growing trend quite early as evidenced by our initial 2012 investment in KUKA AG (Ticker: KUKAF), a German manufacturer of industrial robots. KUKA has recently made headlines due to a bid received from Chinese home-appliance company (Midea Group: Ticker – 000333.SZ) that values the dominant German robotics leader at $5 billion. Despite KUKA’s +273% share price appreciation from the end of 2012, not many people have heard of the company. While KUKA may not have caught the attention of many U.S. investors, the company has captured a bevy of blue-chip global customers, including Daimler, Airbus Group, Volkswagen, Fiat, Boeing, and Tesla.

Rather than sitting on its hands, KUKA has done its part to develop a higher profile. In fact, President Barack Obama and German Chancellor Angela Merkel recently received a robotics demonstration from KUKA’s CEO Till Reuter at the world’s largest industrial technology trade fair in Hannover, Germany this April (picture below)

Source: Bloomberg

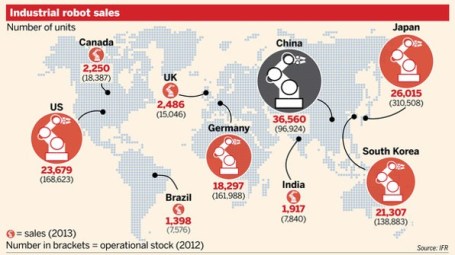

The recent multi-billion dollar bid by Midea Group has turned some onlookers’ heads, but what the potential deal really signals is the vast opportunity for robotics expansion in Asia. Rising labor costs in China, coupled with the enormous efficiency benefits of automation, have pushed China to become the largest purchasing country of robots in the world, ahead of the U.S., Japan, Korea and Germany (see chart below). However, according to the International Federation of Robotics (IFR), in 2015, Japan remained the country with the largest number of installed robots. IFR does not expect Japan to remain the “king” of the installed robotics hill forever. Actually, IFR estimates China will leapfrog Japan over the next few years to become both the largest purchaser of robots, along with maintaining the largest installed base of robots.

Source: Financial Times

In the coming months and years, there will be a steady stream of sensationalist headlines talking about the rise of the robots, and the destruction of jobs. We’ve repeatedly seen this movie before throughout history. Rather than a scary bloodbath ending, over the long-run we’ll likely see another happy ending. Any potential job losses will likely be outweighed by productivity gains, coupled with the benefits associated with more efficiently deployed labor to new growth sectors of the economy.

Even KUKA realizes the automation dynamics of the 21st century will serve as a net labor enhancer not detractor. If you don’t believe me, just ask Timo Boll, world champion table tennis player, who tested this theory vs. a KUKA robot (see video below). Ultimately, the rise of robots will lead to the rise of global growth and productivity.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), KUKAF, BA, and TSLA, but at the time of publishing had no direct position in Daimler, Airbus Group, Volkswagen, Fiat Chrysler, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Chasing Headlines

It’s been an amazing start to the year. First the market cratered on slowing China economic concerns, domestic recessionary fears, deteriorating oil prices, and negative interest rates abroad. In response to all these worries (and others), stocks dove more than -11% (S&P 500 Index) in January, before settling down. Subsequently, the market has made a screaming recovery, in part due to dovish monetary policy comments (i.e., reduction in forecasted interest rate hikes) and diminished anxiety over a potential global collapse. Month-to-date stocks are up an impressive +5.4%, and year-to-date equities are flattish, or down less than -1%.

With an endless amount of information flowing across our smart phones and computers, it becomes quite easy and tempting to chase news headlines, just like a hyper dog chasing a car. But even once an investor catches up (or reacts) to a headline, there’s confusion around how to profit from the fleeting information. First of all, every plugged-in hedge fund and institutional investor has likely already traded on the stale information you received. Second of all, rarely is the data relevant to the long-term cash generating capabilities of the company or economy. And lastly, the news is more often than not, instantly factored into the stock price. Chasing news headlines only eaves individual investors holding the bag of performance-shattering transactions costs, taxes, and worn-out pricing.

The heightened volatility in late 2015 and early 2016 hasn’t however prevented investors and so-called pundits from attempting to time the market. Any battle-tested investment veteran knows it’s virtually impossible to consistently time the market (see also Market Timing Treadmill), but this fact hasn’t prevented speculators from attempting the feat nonetheless. Famed investment guru, Peter Lynch, who earned an average +29% annual return from 1977-1990, summed it up well when he stated the following:

“Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.”

The Important Factors

As I’ve written many times in the past, the keys to long-term stock performance are not knee-jerk reactions to headlines, but rather these following crucial factors (see also Don’t Be a Fool, Follow the Stool):

- Profits

- Interest Rates

- Sentiment

- Valuations

On the profit growth front, corporate income has been pressured by numerous headwinds over the last few years, including an export-shattering increase in the value of the U.S. dollar and a profit-squeezing collapse in energy sector earnings. As you can see from the chart below, the value of the U.S. dollar increased by about 25% from mid-2014 to early-2015, in part because of diverging global central bank policies (more hawkish U.S. Fed vs. more dovish ECB/international central banks). Since that spike, the dollar has settled into a broad range (95 – 100), and the former forceful headwind have now turned into modest tailwinds. This trend is important because an estimated 35-40% of corporate profits are derived from international operations.

Adding insult to injury, the roughly greater than -70% decline in forward energy earnings over the last 18 months has caused a significant hit to overall S&P 500 profits. The tide appears to be finally turning (or at least stabilizing) however, as we’ve seen oil prices rebound by about +30% this year from the lows in January. If these aforementioned trends persist, profit pressures in 2016 are likely to abate significantly, and may actually become additive to growth.

Source: Barchart.com

Profits are important, but so are interest rates. While incessant talk about the path of future Fed policy continues to blanket the airwaves (see also Fed Fatigue), absent a rapid increase in interest rates (say 300-400 basis points), interest rates remain unambiguously positive for equity markets, providing a floor for the oft-repeated volatility in financial markets. As long as stocks are providing higher yields than many bonds, and depositors are earning 0% (or negative rates) on their checking accounts, stocks may remain unloved, but not forgotten.

And speaking of unloved, the sentiment for stocks remains sour. One need look no further than the quarter-billion dollars in hemorrhaging outflows out of U.S. equity funds (see ICI Long-Term Mutual Fund Flows) since 2014. This deep underlying skepticism serves as a positive contrarian indicator for future equity prices. Right now, very few individual investors are swimming in the pool – the time to get out of the stock market pool is when everyone is jumping in.

And lastly, valuations remain very much in line with historical averages (approximatqely 17x 2016 projected earnings), especially considering the generational low in interest rates. Bears continue to point to the elevated CAPE ratio, which has been a disastrous indicator the last seven years (and longer), as a reason to remain cautious. The ironic part is that valuations are virtually guaranteed to improve a few years from now as we roll off the artificially depressed years of 2008-2010.

When you add it all up, zero (or negative) interest rates, combined with the other key factors of profits, sentiment, and valuations, equities remain an important and attractive part of a diversified long-term portfolio. Your objectives, time horizon, and risk tolerance will always drive the proportion of your equity allocation. Nevertheless, some bond exposure is essential to smooth out volatility. Regardless of your investment strategy, chasing headlines, like a dog chasing a car, serves no purpose other than leaving you with a tired, unproductive investment portfolio.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Shoot Now, Ask Later

![940614_83408820[1]](https://investingcaffeine.com/wp-content/uploads/2011/08/940614_834088201.jpg?w=311&h=230)

Since the start of 2016, investor sentiment has led to a shoot now, ask questions later mentality. In the court of economic justice, all stocks have been convicted guilty of recession despite the evidence and defense that proves the economy innocent. Even the Federal Reserve Chair Janet Yellen did not prove to be a great public defender of the economy with her comments that negative interest rates are on the table.

With large cap stocks down -13% and small cap stocks losing -25% from 2015, there are a mixture of indicators suggesting a looming recession could be coming. For example, banking stocks, the beating heart of the U.S. economy, saw prices collapse almost -30% from the 2015 highs this week. As CNBC pointed out, “American Airlines (AAL), United Continental (UAL), General Motors (GM) and Ford (F) all sell for five times 2016 earnings” – about a 70% discount to the average S&P 500 stock. As a group, these economically sensitive cyclical stocks grew earnings per share greater than 50%, while their stock prices are down by more than -30% from their 52-week highs. In general, the cyclicals are serving jail time, even though growth has been gangbusters and the current valuations massively discounted.

On the flip side, defensive stocks with little-to-no revenue growth like “Campbell Soup (CPB) trade at 20 times earnings, Kimberly-Clark (KMB) is at 21 times earnings, Procter & Gamble (PG) is at 22 times earnings and Clorox (CLX) is at 25 times earnings. All of these stocks are near 52-week highs.”

Confused? Well, if we are indeed going into recession, than this valuation dichotomy between cyclicals and staples makes sense. Stocks can be a leading indicator (i.e., predictor) of future recessions, but as the famed Nobel Prize winner in economics Paul Samuelson noted, “The stock market has forecast nine of the last five recessions.”

On the other hand, if this current correction is a false recession scare, then now would be a tremendous buying opportunity. In fact, over the last five years, there have been plenty of tremendous buying opportunities for those courageous long-term investors willing to put capital to work during these panic periods (see also Groundhog Day All Over Again):

- 2011: Debt Downgrade/Debt Ceiling Debate/European PIIGS Crisis (-22% correction)

- 2012:Arab Spring/Greek “Gr-Exit” Fears (-11% correction)

- 2013: Fed Taper Tantrum (-8% correction)

- 2014: Ebola Outbreak (-10% correction)

- 2015: China Slowdown Fears (-13% correction in August)

- 2016 (1st Six Weeks): Strong Dollar, Collapsing Oil, interest Rate Hikes/Negative Rates, Weakening China (-15% correction)

- 2016 (Next 46 Weeks): ??????????

Today’s threats rearing their ugly heads have definite recession credibility, but if you think about the strong dollar, collapsing oil prices, Fed monetary policies, weakening Chinese economy, and negative global interest rates, all of these threats existed well before stock prices nose-dived during the last six weeks. If the economic court is judging the current data for potential recession evidence, making a case and proving the economy guilty is challenging. It’s tough to find a recession when we witness a low unemployment rate (4.9%); record corporate profits (ex-energy); record car sales (17.5 million); an improving housing market; a positively sloped yield curve; healthy banking and consumer balance sheets; sub-$2/gallon gasoline; and a flattening U.S. dollar, among other factors.

Could stock prices be clairvoyantly predicting Armageddon? Sure, anything is possible…but this scenario is unlikely now. Even if the U.S. economy is headed towards a recession, the -20% plunge in stock prices is already factoring in most, if not all, of a mild-to-moderate recession. If the economic data does actually get worse, there is still room for stock prices to go down. Under a recession scenario, the tremendous buying opportunities will only get better. While weak hands may be shooting (selling) first and asking questions later, now is the time for you to use patience and discipline. These characteristics will serve as bullet proof vest for your investment portfolio and lead to economic justice over the long-term.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and non-discretionary positions in PG, and KMB, but at the time of publishing had no direct position in AAL, CLX, CPB, F, GM, UAL, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Don’t Do Something…Just Stand There!

Like a full plane hitting a rough patch of turbulence, investors have been shaken by the recent price volatility in the stock market over concerns of a slowing Chinese economy, plummeting oil prices, and a host of other alarming headlines. As a result, investors are left picking up the pieces of the S&P 500 decline, which currently sits off -11% from its 2015 highs (down -15% at the 1/20/16 low). The picture looks even uglier if you consider the Russell 2000 small cap index, which has collapsed -21% from its 2015 highs (-26% at the 1/20/16 low).

What now, and what does this mean? There has been all kinds of crazy technical trading activity occurring around heavy options expirations, stop-loss selling, and short cover buying. With all the frenetic gyrations in the stock market (e.g., 2,000 point swing in the Dow Jones over the last month), there have been no shortage of opinions on TV, on the internet or at the watercooler. However, the best sage advice probably came from 86-year-old investor legend, John “Jack” Bogle (founder of Vanguard Group – $3.4 trillion in assets under management at 12/31/15), who emphatically told investors to “Don’t do something…just stand there!”

The advice to “stay the course” can be very counter-intuitive to human nature. In periods of stress, our brains tend to revert back to our ancestors’ Darwinian survival instincts, which tell us to flee from the ferocious lion (see also Controlling the Investment Lizard Brain). The fact is these periods of turbulence are normal – no different than a bumpy flight into San Francisco. In fact, we’ve hit quite a few choppy air pockets in recent years:

- Debt Downgrade/Debt Ceiling Debate/European PIIGS Crisis (-22% in 2011)

- Arab Spring/Grexit Fears (-11% in 2012)

- Fed Taper Tantrum (-8% in 2013)

- Ebola Outbreak (-10% in 2014)

- China Slowdown Fears (-13% in 2015)

Through all of this mayhem, including the current 2016 dip, the stock market has still managed to rise an impressive +77% since the 2011 pullback, which sure beats the sub-1% yield earned on bank CDs.

Inevitably, with the recent price breakdown, speculation has begun to swirl around the dreaded “R”-word (aka, recession) again. In general, this is a fruitless effort. When the smartest Nobel Prize winning economists fail miserably at predicting recessions, it’s hard to believe you or I will have a much better success rate. The great investor Peter Lynch astutely summed up recession forecasting as follows:

“It’s lovely to know when there’s recession. I don’t remember anybody predicting 1982 we’re going to have 14 percent inflation, 12 percent unemployment, a 20 percent prime rate, you know, the worst recession since the Depression. I don’t remember any of that being predicted. It just happened. It was there. It was ugly. And I don’t remember anybody telling me about it. So I don’t worry about any of that stuff. I’ve always said if you spend 13 minutes a year on economics, you’ve wasted 10 minutes.”

The noted Nobel Prize winning economist Paul Samuelson offered this shrewd observation on recessions as well:

“The stock market has called nine of the last five recessions.”

In other words, the stock market can predict recessions, but often times it is a horrible indicator for the health of the economy (e.g., see 2011-2015 above).

While I am definitely not a Nobel Prize winning economist, I can objectively point to supporting evidence showing we currently are not on the edge of a new recession. It is certainly true that a strong U.S. dollar and a Q4 energy earnings deterioration has been a drag on earnings, but these factors only paint a small part of the picture. Without going into gory economic detail, you do not need to be an expert to understand basic macro trends like employment, housing, auto sales, gasoline prices, and interest rates are providing a buttress to the economy.

As you can see from the chart below, the -73% cut in Q4 energy sector earnings, along with challenged exports from multinational corporations, has pressured profitability in the S&P 500. However, if you strip out the energy sector, earnings continue to grow. And although it’s early in the 2016 earnings reporting season, so far 73% of companies are beating estimates by 3% on average.

The economic winds are definitely spinning, and we may not be completely through the turbulence, but rather than panicking, you’re probably best served by following the advice of Jack Bogle by standing through the turmoil and look for opportunities when the volatility settles.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Extrapolation: Dangers of the Reckless Ruler

The game of investing would be rather simple if everything moved in a straight line and economic data points could be could be connected with a level ruler. Unfortunately, the real world doesn’t operate that way – data points are actually scattered continuously. In the short-run, inflation, GDP, exchange rates, interest rates, corporate earnings, profit margins, geopolitics, natural disasters, financial crises, and an infinite number of other factors are very difficult to predict with any accurate consistency. The true way to make money is to correctly identify long-term trends and then opportunistically take advantage of the chaos by using the power of mean reversion. Let me explain.

Take for example the just-released October employment figures, which on the surface showed a blowout creation of +271,000 new jobs during the month (unemployment rate decline to 5.0%) versus the Wall Street consensus forecast of +180,000 (flat unemployment rate of 5.1%). The rise in new workers was a marked acceleration from the +137,000 additions in September and the +136,000 in August. The better-than-expected jobs numbers, the highest monthly addition since late 2014, was paraded across television broadcasts and web headlines as a blowout number, which gives the Federal Reserve and Chairwoman Janet Yellen more ammunition to raise interest rates next month at the Federal Open Market Committee meeting. Investors are now factoring in roughly a 70% probability of a +0.25% interest rate hike next month compared to an approximately 30% chance of an increase a few weeks ago.

As is often the case, speculators, traders, and the media rely heavily on their trusty ruler to connect two data points to create a trend, and then subsequently extrapolate that trend out into infinity, whether the trend is moving upwards or downwards. I went back in time to explore the media’s infatuation with limitless extrapolation in my Back to the Future series (see Part I; Part II; and Part III). More recently, weakening data in China caused traders to extrapolate that weakness into perpetuity and pushed Chinese stocks down in August by more than -20% and U.S. stocks down more than -10%, over the same timeframe.

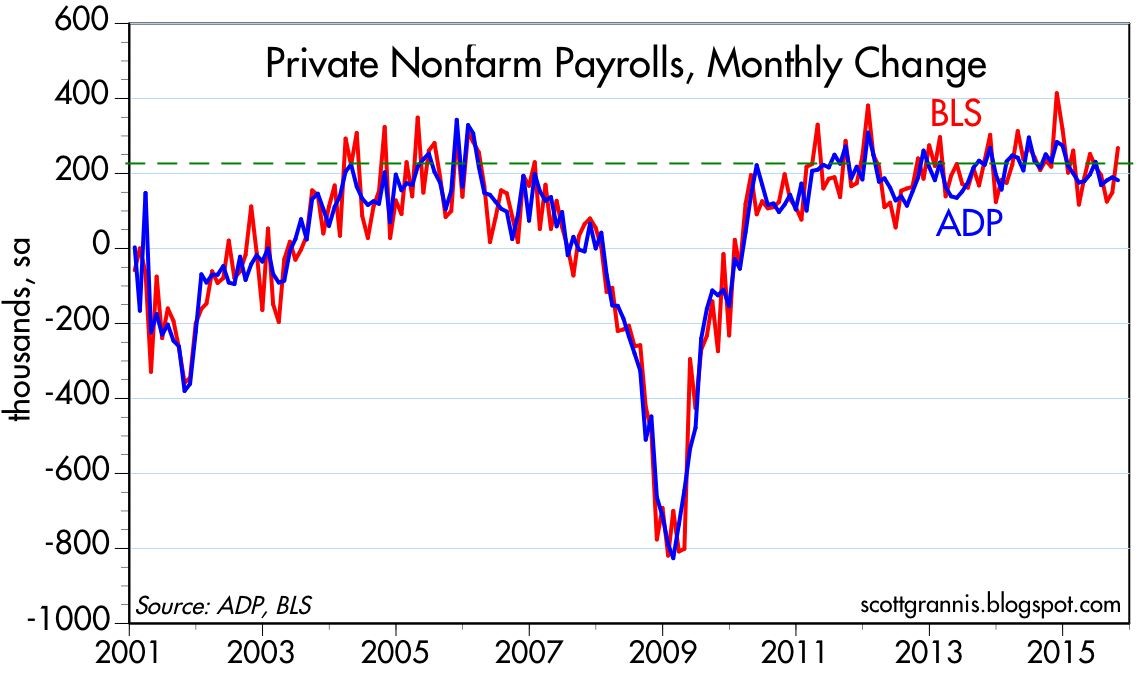

While most of the media coverage blew the recent jobs number out of proportion (see BOOM! Big Rebound in Job Creation), some shrewd investors understand mean reversion is one of the most powerful dynamics in economics and often overrides the limited utility of extrapolation. Case in point is blogger-extraordinaire Scott Grannis (Calafia Beach Pundit) who displayed this judgment when he handicapped the October jobs data a day before the statistics were released. Here’s what Grannis said:

The BLS’s estimate of private sector employment tends to be more volatile than ADP’s, and both tend to track each other over time. That further suggests that the BLS jobs number—to be released early tomorrow—has a decent chance of beating expectations.

Now, Grannis may not have guaranteed a specific number, but comparing the volatile government BLS and private sector ADP jobs data (always released before BLS) only bolsters the supremacy of mean reversion. As you can see from the chart below, both sets of data have been highly correlated and the monthly statistics have reliably varied between a range of +100k to +300k job additions over the last six years. So, although the number came in higher than expected for October, the result is perfectly consistent with the “slowly-but-surely” growing U.S. economy.

Source: Calafia Beach Pundit

While I spend much more time picking stocks than picking the direction of economic statistics, even I will agree there is a high probability the Fed moves interest rates next month. But even if Yellen acts in December, she has been very clear that this rate hike cycle will be slower than previous periods due to the weak pace of economic expansion. I agree with Grannis, who noted, “Higher rates would be a confirmation of growth, not a threat to growth.” Whatever happens next month, do yourself a favor and keep the urge of extrapolation at bay by keeping your pencil and ruler in your drawer.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) , but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Marathon Market Gets a Cramp

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (October 1, 2015). Subscribe on the right side of the page for the complete text.

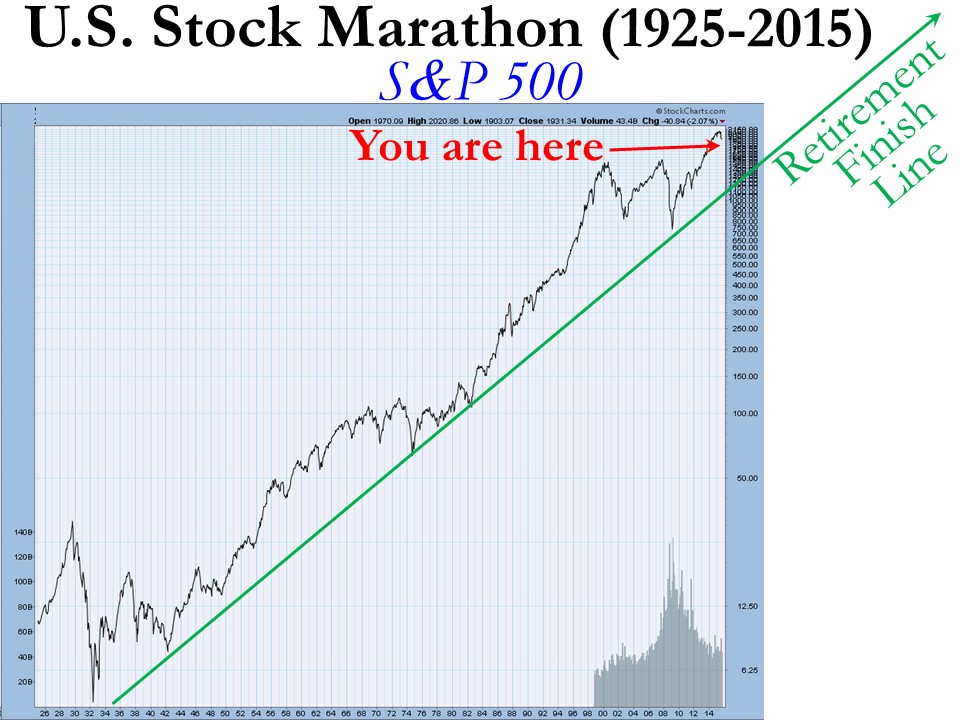

“Anyone can run a hundred meters, it’s the next forty-two thousand and two hundred that count.”

Investing is a lot like running a marathon…but it’s not a sprint to the retirement finish line. The satisfaction of achieving your long-term goal can be quite rewarding, but attaining ambitious objectives does not happen overnight. Along the hilly and winding course, there can be plenty of bumps and bruises mixed in with the elation of a runner’s high. While stocks have been running at a record pace in recent years, prices have cramped up recently as evidenced by the -2.6% decline of the S&P 500 stock index last month.

But the recent correction should be placed in the proper perspective as you approach and reach retirement. Since the end of the 2008 Financial Crisis the stock market has been racing ahead at a brisk rate, as you can see from the total return performance below (excluding 2015):

This performance is more indicative of a triumph than a catastrophe, but if you turned on the TV, listened to the radio, or surfed the web, you may come to a more frightening conclusion.

What’s behind the recent dip? These are some of the key concerns driving the recent price volatility:

- China: Slowing growth in China and collapse in Chinese stock market. China is suffering from a self-induced slowdown designed to mitigate corruption, prick the real estate bubble, and shift its export-driven economy to a more consumer-driven economy. These steps diminish short-term growth (albeit faster than U.S. growth), but nevertheless the measures should be constructive for longer-term growth.

- Interest Rates: Uncertainty surrounding the timing of a 0.25% target interest rate increase by the Federal Reserve. The move from 0% to 0.25% is like walking from the hardwood floor onto the rug…hardly noticeable. The inevitable move by the Fed has been widely communicated for months, and given where interest rates are today, the move will have a negligible impact on corporate borrowing costs. Like removing a Band-Aid, the initial action may cause some pain, but should be comfortably received shortly thereafter.

- Politics: Potential government shutdown / sequestration. The epic political saga will never end, however, as I highlighted in “Who Said Gridlock is Bad?,” political discourse in Washington has resulted in positive outcomes as it relates to our country’s fiscal situation (limited government spending and declining deficits). The government shutdown appears to have been averted for now, but it looks like we will be blanketed with brinkmanship nonsense again in a few months.

- Biotech/Pharmaceuticals: Politics over lofty drug prices and the potential impact of future regulation on the biotech sector. Given the current Congressional balance of power, any heavy-handed Democratic proposals is likely to face rigorous Republican opposition.

- Emerging Markets: Emerging market weakness, especially in Latin America (e.g., Brazil). These developments deserve close monitoring, but the growth in the three largest economic regions (U.S., Europe, and China) will have a much larger effect on the direction of global economic expansion.

- Middle East: Destabilized Middle East and Syria. Terrorist extremism and cultural animosity between various Middle East populations has existed for generations. There will be no silver bullet for a peaceful solution, so baby steps and containment are critical to maintain healthy global trade activity with minimal disruptions.

Worth noting, this current list of anxieties itemized above is completely different from six months ago (remember the Greece crisis?), and the list will change again six months into the future. Investing, like any competitive challenge, does not come easy…there is always something to worry about in the land of economics and geopolitics.

Here’s what the world’s top investor Warren Buffett said a few decades ago (1994) on the topic of politics and economics:

“We will continue to ignore political and economic forecasts which are an expensive distraction for investors and businessmen. Thirty years ago, no one could have foreseen the huge expansion of the Vietnam War, wage and price controls, two oil shocks, the resignation of a president, the dissolution of the Soviet Union, a one-day drop in the Dow of 508 points, or treasury bill yields fluctuating between 2.8% and 17.4%.”

In a world of 7.3 billion people and 196 countries there will never be a shortage of fear, uncertainty, and doubt (F.U.D.) – see events chart in The Bungee Market. In an ever-increasing, globally connected world, technology and the media continually amplify molehills into mountains, thereby making the next imagined Armageddon a simple click of a mouse or swipe of a smartphone away.

Today’s concerns are valid but in the vast majority of cases the issues are completely overblown, sensationalized and over-emphasized without context. Context is an integral part to investing, but unfortunately context usually cannot be explained in a short soundbite or headline. On the flip side, F.U.D. thrives in the realm of soundbites and headlines.

While investors may feel fatigued from a strong flow of headline headwinds, financial market race participants should take a break at the water stop to also replenish themselves with a steady tailwind of positive factors, including the following:

- Employment: The unemployment rate has been cut from a recession peak of 10.0% down to 5.1%, and the economy has been adding roughly +200,000 new monthly jobs on a fairly consistent basis. On top of that, there are a record 5.8 million job openings versus 3.7 million two years ago – a sign that the economy continues to hum along.

- Housing/Commercial Real Estate/Mortgage Rates: Housing prices have rebounded by about +30% from the 2012 lows; Housing starts have increased by +25% in the past year and 120% in the past four years; and 30-Year Fixed mortgage interest rates sit at 3.85% – a highly stimulative level within a spitting distance from record lows.

- Auto Sales: Surged to a post-recession record of 17.8 million units in August.

- Interest Rates: Massively stimulative and near generational lows, even if the Fed hikes its interest rate target by 0.25% in October, December or sometime in 2016.

- Capital Goods Orders: Up for three consecutive months.

- Rail Shipments/Truck Tonnage: Both these metrics are rising by about 3-4%.

- Retail Sales: Rising at a very respectable pace of 7% over the last six months.

- Low Energy & Commodity Prices: Inflation has remained largely in check thanks to plummeting commodity prices. Low oil and gas prices are benefiting consumers in numerous ways, including the contribution to car sales, home sales, and/or debt reduction.

While the -10% dip in stock prices from mid-August might feel like a torn knee ligament, long-term investors know -10% corrections historically occur about one-time per year, on average. So, even though you may be begging for a wheelchair, the best course of action is to take a deep breath, stick to your long-term investment plan, rebalance your portfolio if necessary, and continue staying on course towards your financial finish line.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) , but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Art of Catching Falling Knives

“In the middle of every difficulty lies an opportunity.” ~Albert Einstein

It was a painful week for bullish investors in the stock market as evidenced by the -1,018 point drop in the Dow Jones Industrial Average, equivalent to approximately a -6% decline. The S&P 500 index did not fare any better, and the loss for the tech-heavy NASDAQ index was down closer to -7% for the week.

The media is attributing much of the short-term weakness to a triple Chinese whammy of factors: 1) Currency devaluation of the Yuan; 2) Weaker Chinese manufacturing data registering in at the lowest level in over six years; and 3) A collapsing Chinese stock market.

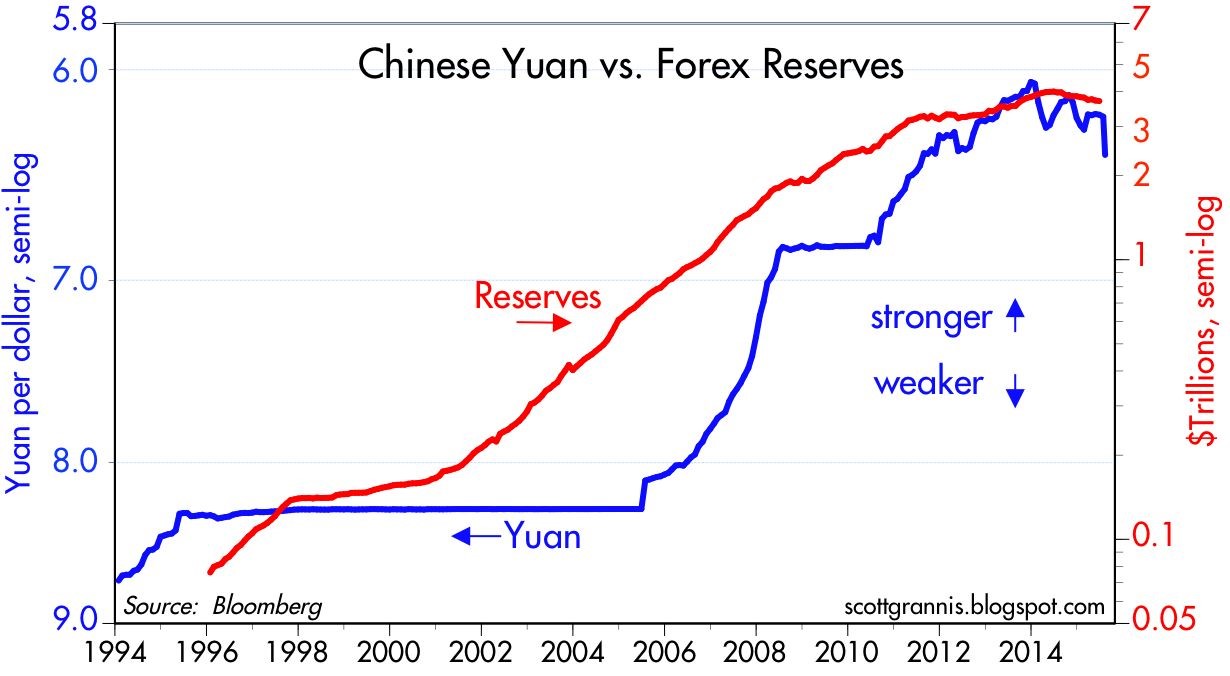

As the second largest economy on the planet, developments in China should not be ignored, however these dynamics should be put in the proper context. With respect to China’s currency devaluation, Scott Grannis at Calafia Beach Pundit puts the foreign exchange developments in proper perspective. If you consider the devaluation of the Yuan by -4%, this change only reverses a small fraction of the Chinese currency appreciation that has taken place over the last decade (see chart below). Grannis rightfully points out the -25% collapse in the value of the euro relative to the U.S. dollar is much more significant than the minor move in the Yuan. Moreover, although the move by the People’s Bank of China (PBOC) makes America’s exports to China less cost competitive, this move by Chinese bankers is designed to address exactly what investors are majorly concern about – slowing growth in Asia.

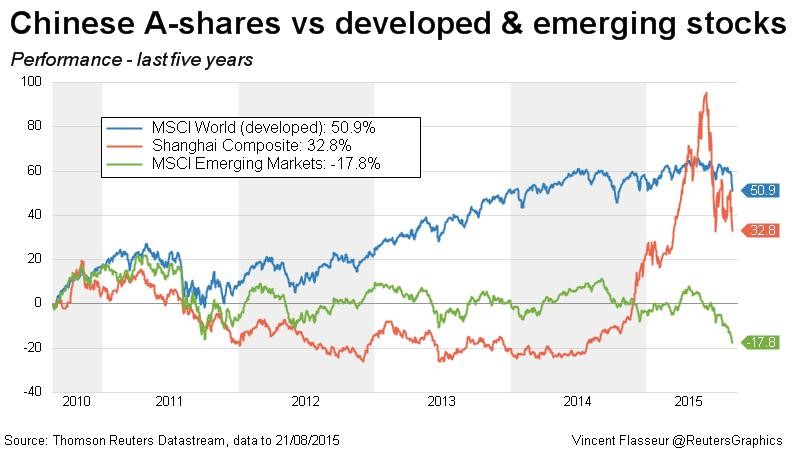

Although the weak Chinese manufacturing data is disconcerting, this data is nothing new – the same manufacturing data has been very choppy over the last four years. On the last China issue relating to its stock market, investors should be reminded that despite the massive decline in the Shanghai Composite, the index is still up by more than +50% versus a year ago (see chart below)

Fear the Falling Knife?

Given the fresh carnage in the U.S. and foreign markets, is now the time for investors to attempt to catch a falling knife? Catching knives for a living can be a dangerous profession, and many investors – professionals and amateurs alike – have lost financial fingers and blood by attempting to prematurely purchase plummeting securities. Rather than trying to time the market, which is nearly impossible to do consistently, it’s more important to have a disciplined, unemotional investing framework in place.

Hall of Fame investor Peter Lynch sarcastically highlighted the difficulty in timing the market, “I can’t recall ever once having seen the name of a market timer on Forbes‘ annual list of the richest people in the world. If it were truly possible to predict corrections, you’d think somebody would have made billions by doing it.”

Readers of my blog, Investing Caffeine understand I am a bottom-up investor when it comes to individual security selection with the help of our proprietary S.H.G.R. model, but those individual investment decisions are made within Sidoxia’s broader, four-pronged macro framework (see also Don’t be a Fool, Follow the Stool). As a reminder, driving our global views are the following four factors: a) Profits; b) Interest rates; c) Sentiment; and Valuations. Currently, two of the four indicators are flashing green (Interest rates and Sentiment), and the other two are neutral (Profits and Valuations).

- Profits (Neutral): Profits are at record highs, but a strong dollar, weak energy sector, and sluggish growth internationally have slowed the trajectory of earnings.

- Valuation (Neutral): At an overall P/E of about 18x’s profits for the S&P 500, current valuations are near historical averages. For CAPE investors who have missed the tripling in stock prices, you can reference prior discussions (see CAPE Smells Like BS). I could make the case that stocks are very attractive with a 6% earnings yield (inverse P/E ratio) compared to a 2% 10—Year Treasury bond, but I’ll take off my rose-colored glasses.

- Interest Rates (Positive): Rates are at unambiguously low levels, which, all else equal, is a clear-cut positive for all cash generating asset classes, including stocks. With an unmistakably “dovish” Federal Reserve in place, whether the 0.25% interest rate hike comes next month, or next year will have little bearing on the current shape of the yield curve. Chairman Yellen has made it clear the trajectory of rate increases will be very gradual, so it will take a major shift in economic trends to move this factor into Neutral or Negative territory.

- Sentiment (Positive): Following the investment herd can be very dangerous for your financial health. We saw that in spades during the late-1990s in the technology industry and also during the mid-2000s in the housing sector. As Warren Buffett says, it is best to “buy fear and sell greed” – last week we saw a lot of fear.

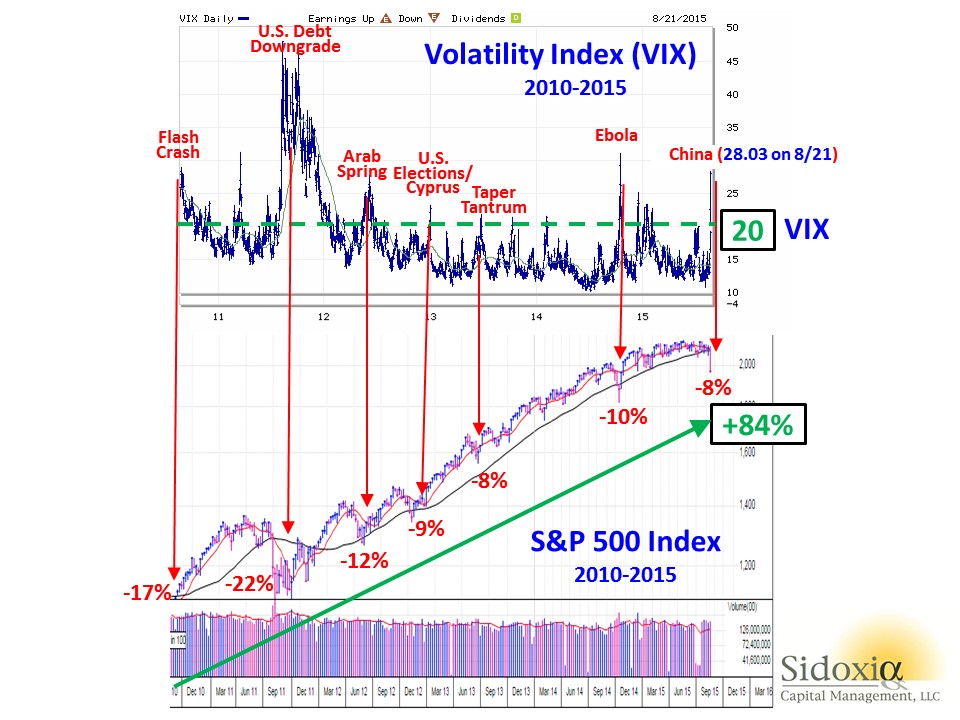

In addition to the immense outflows out of stock funds (see also Great Rotation) , panic was clearly evident in the market last week as shown by the Volatility Index (VIX), a.k.a., the “Fear Gauge.” In general, volatility over the last five years has been on a declining trend, however every 6-12 months, some macro concern inevitably rears its ugly head and volatility spikes higher. With the VIX exploding higher by an amazing +118% last week to a level of 28.03, it is proof positive how quickly sentiment can change in the stock market.

Not much in the investing world works exactly like science, but buying stocks during previous fear spikes, when the VIX level exceeds 20, has been a very lucrative strategy. As you can see from the chart below, there have been numerous occasions over the last five years when the over-20 level has been breached, which has coincided with temporary stock declines in the range of -8% to -22%. However, had you held onto stocks, without adding to them, you would have earned an +84% return (excluding dividends) in the S&P 500 index. Absent the 2011 period, when investors were simultaneously digesting a debt downgrade, deep European recession, and domestic political fireworks surrounding a debt ceiling, these periods of elevated volatility have been relatively short-lived.

Whether this will be the absolute best time to buy stocks is tough to say. Stocks are falling like knives, and in many instances prices have been sliced by more than -10%, -20%, or -30%. It’s time to compile your shopping list, because valuations in many areas are becoming more compelling and eventually gravity will run its full course. That’s when your strategy needs to shift from avoiding the falling knives to finding the bouncing tennis balls…excuse me while I grab my tennis racket.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) including emerging market/Chinese ETFs, but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Is the Stock Market Rigged? Yes…In Your Favor

Is the Market Rigged? The short answer is “yes”, but unlike gambling in Las Vegas, investing in the stock market rigs the odds in your favor. How can this be? The market is trading at record highs; the Federal Reserve is artificially inflating stocks with Quantitative easing (QE); there is global turmoil flaring up everywhere; and author Michael Lewis says the stock market is rigged with HFT – High Frequency Traders (see Lewis Sells Flash Boys Snake Oil). I freely admit the headlines have been scary, but scary headlines will always exist. More importantly for investors, they should be more focused on factors like record corporate profits (see Halftime Adjustments); near generationally-low interest rates; and reasonable valuation metrics like the price-earnings (P/E) ratios.

Even if you were to ignore these previously mentioned factors, one can use history as a guide for evidence that stocks are rigged in your favor. In fact, if you look at S&P 500 stock returns from 1928 (before the Great Depression) until today, you will see that stock prices are up +72.1% of the time on average.

If the public won at such a high rate in Las Vegas, the town would be broke and closed, with no sign of pyramids, Eiffel Towers, or 46-story water fountains. There’s a reason Las Vegas casinos collected $23 billion in 2013 – the odds are rigged against the public. Even Shaquille O’Neal would be better served by straying away from Vegas and concentrating on stocks. If Shaq could have improved his 52.7% career free-throw percentage to the 72.1% win rate for stocks, perhaps he would have earned a few more championship rings?

Considering a 72% winning percentage, conceptually a “Buy-and-Hold” strategy sounds pretty compelling. In the current market, I definitely feel this type of strategy could beat most market timing and day trading strategies over time. Even better than this strategy, a “Buy Winners-and-Hold Winners” strategy makes more sense. In other words, when investing, the question shouldn’t revolve around “when” to buy, but rather “what” to buy. At Sidoxia Capital Management we are primarily bottom up investors, so the appreciation potential of any security in our view is largely driven by factors such as valuation, earnings growth, and cash flows. With interest rates near record lows and a scarcity of attractive alternatives, the limited options actually make investing decisions much easier.

Scarcity of Alternatives Makes Investing Easier

U.S. investors moan and complain about our paltry 2.42% yield on the 10-Year Treasury Note, but how appetizing, on a risk-reward basis, does a 2.24% Irish 10-year government bond sound? Yes, this is the same country that needed a $100 billion+ bailout during the financial crisis. Better yet, how does a 1.05% yield or 0.51% yield sound on 10-year government treasury bonds from Germany and Japan, respectively? Moreover, what these minuscule yields don’t factor in is the potentially crippling interest rate risk investors will suffer when (not if) interest rates rise.

Fortunately, Sidoxia’s client portfolios are diversified across a broad range of asset classes. The quantitative results from our proprietary 5,000 SHGR (“Sugar”) security database continue to highlight the significant opportunities in the equities markets, relative to the previously discussed “bubblicious” parts of the fixed income markets. Worth noting, investors need to also remove their myopic blinders centered on U.S. large cap stocks. These companies dominate media channel discussions, however there are no shortage of other great opportunities in the broader investment universe, including such areas as small cap stocks, floating-rate bonds, real estate, commodities, emerging markets, alternative investments, etc.

I don’t mind listening to the bearish equity market calls for stock market collapses due to an inevitable Fed stimulus unwind, mean reverting corporate profit margins, or bubble bursting event in China. Nevertheless, when it comes to investing, there is always something to worry about. While there is always some uncertainty, the best investors love uncertainty because those environments create the most opportunities. Stocks can and eventually will go down, but rather than irresponsibly flailing around in and out of risk-on and risk-off trades to time the market (see Market Timing Treadmill), we will continue to steward our clients’ money into areas where we see the best risk-reward prospects.

For those other investors sitting on the sidelines due to market fears, I commend you for coming to the proper conclusion that stock markets are rigged. Now you just need to understand stocks are rigged for you (not against you)…at least 72% of the time.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold a range of exchange traded fund positions, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Aaaaaaaah: Turbulence or Nosedive?

We’ve all been there on that rocky plane ride…clammy hands, heart beating rapidly, teeth clenched, body frozen, while firmly bracing the armrests with both appendages. The sky outside is dark and the interior fuselage rattles incessantly until….whhhhhssssshhh. Another quick jerking moment of turbulence has once again sucked the air out of your lungs and the blood from your heart. The rational part of your brain tries to assure you that this is normal choppy weather and will shortly transition to calm blue skies. The irrational and emotional, part of our brains (see Lizard Brain) tells us the treacherous plane ride is on the cusp of plummeting into a nosedive with passengers’ last gasps saved for blood curdling screams before the inevitable fireball crash.

Well, we’re now beginning to experience some small turbulence in the financial markets, and at the center of the storm is a collapsing Argentinean peso and a perceived slowing in China. In the case of Argentina, there has been a century-long history of financial defaults and mismanagement (see great Scott Grannis overview). Currently, the Argentinean government has been painted into a corner due to the depletion of its foreign currency reserves and financial mismanagement, as evidenced by an inflation rate hitting a whopping 25% rate.

On the other hand, China has created its own set of worries in investors’ minds. The flash Markit/HSBC Purchasing Managers’ Index (PMI) dropped to a level of 49.6 in January from 50.50 in December, which has investors concerned of a market crash. Adding fuel to the fear fire, Chinese government officials and banks have been trying to reverse excesses encountered in the country’s risky shadow banking system. While the size of Argentina’s economy may not be a drop in the bucket, the ultimate direction of the Chinese economy, which is almost 20x’s the size of Argentina’s, should be much more important to global investors.

At the end of the day, most of these mini-panics or crises (turbulence) are healthy for the overall financial system, as they create discipline and will eventually change irresponsible government behaviors. While Argentinean and Chinese issues dominate today’s headlines, these matters are not a whole lot different than what we have read about Greece, Ireland, Italy, Spain, Portugal, Cyprus, Turkey, and other negligent countries. As I’ve stated before, money goes where it’s treated best, and the stock, bond, and currency vigilantes ensure that this is the case by selling the assets associated with deadbeat countries. Price declines eventually catch the attention of politicians (remember the TARP vote failure of 2008?).

Is This the Beginning of the Crash?!

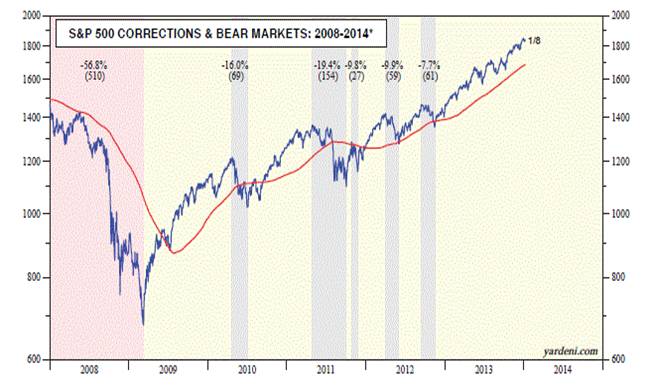

What goes up, must come down…right? That is the pervading sentiment I continually bump into when I speak to people on the street. Strategist Ed Yardeni did a great job of visually capturing the last six years of the stock market (below), which highlights the most recent bear market and subsequent major corrections. Noticeably absent in 2013 is any major decline. So, while many investors have been bracing for a major crash over the last five years, that scenario hasn’t happened yet. The S&P chart shows we appear to be due for a more painful blue (or red) period of decline in the not-too-distant future, but that is not necessarily the case. One would need only to thumb through the history books from 1990-1997 to see that investors lived through massive gains while avoiding any -10% correction – stocks skyrocketed +233% in 2,553 days. I’m not calling for that scenario, but I am just pointing out we don’t necessarily always live through -10% corrections annually.

Source: Dr. Ed’s Blog

Even though we’ve begun to experience some turbulence after flying high in 2013, one should not panic. You may be better off watching the end of the airline movie before putting your head in between your legs in preparation for a nosedive.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Earnings Coma: Digesting the Gains

Over the last five years, the stock market has been an all-you-can-eat buffet of gains for investors. It has been almost two years since the spring of 2012 when the Arab Spring and potential exit of Greece from the EU caused a -10% correction in the S&P 500 index (see Series of Unfortunate Events). Indigestion of this 10% variety is typically on the menu and ordered at least once per year. With stocks up about +50% over the last two years, performance has tasted sweet. But even binging on your favorite entrée or dessert will eventually lead to a food coma. At that bloated point, a digestion phase is required before another meal of gains can be consumed.

So far investors haven’t been compelled to expel their meals quite yet, but it’s clear to me the rate of appreciation is not sustainable over the long-term. Could the incredible returns continue in the short-run during 2014? Certainly. As I’ve written before, the masses remain skeptical of the recovery/rally and any definitive acceleration in economic growth could spark the powder-keg of skeptics to come join the party (see Here Comes the Dumb Money). If and when that happens, I will be gladly there to systematically ring the register of profits I’ve consumed, by locking in gains and reallocating to less loved areas (i.e., go on a stock diet).

Q4 Appetizers Here, Main Course Not Yet

The 4th quarter earnings appetizers have been served, evidenced by the 50-odd S&P 500 corporations that have reported their financial results, and thus far some Tums may be needed to relieve some heartburn. Although about half of those companies reporting have beat Wall Street estimates, 37% of the group have missed expectations, according to Thomson Reuters. It’s still early in the earnings season, but as of now, the ratio of companies beating Wall Street forecasts is below historical averages.

We can put a little meat on the earnings bone by highlighting the disappointing profit warnings and lackluster results from bellwether companies like United Parcel Service (UPS), Intel Corp (INTC), General Electric (GE), CSX Corp (CSX), and Royal Dutch Shell (RDSA), to name a few. Is it time to panic and run for the restroom (or exits)? Probably not. About 90% of the S&P 500 companies still need to give their Q4 profitability state of the union. What’s more, another reason to not throw in the white towel yet is the global economic environment looks significantly better in areas like Europe, China, and other emerging markets.

Worth remembering, the stock market is a discounting mechanism. The market pays much more attention to the future versus the past. So, even if the early earnings read doesn’t look so great now, the fact that the S&P 500 is down less than -1% off of its all-time, record highs may be an indication of better things ahead.

Recipe for a Pullback?

If earnings continue to drag on in a disappointing fashion, and political brinkmanship materializes surrounding the debt ceiling, it could easily be enough to spark some profit-taking in stocks. While Sidoxia is finding no shortage of opportunities, it has become apparent some speculative pockets of euphoria have developed. Areas like social media and biotech are ripe for corrections.

While the gains over the last few years have been tantalizing, investors must be reminded to not overindulge. Carefully selecting stocks to chew and digest is a better strategy than recklessly binging on everything in the buffet line. There are plenty of healthy areas of the market to choose from, so it’s important to be discriminating…or your portfolio could end up in a coma.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in UPS, INTC, GE, CSX, RDSA, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}