Posts tagged ‘bubble’

A Tale of Two Cities

In 1859, Charles Dickens published his timeless historical novel, A Tale of Two Cities, set in London and Paris before and during the French Revolution (1775 – 1789). He opens the book with one of the most famous passages in literary history:

“It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity, it was the season of Light, it was the season of Darkness, it was the spring of hope, it was the winter of despair.”

Nearly 170 years later, Dickens’ words could easily describe today’s stock market.

On one hand, the S&P 500 has climbed +9.6% this year and recently reached another all-time high – the “best of times.” On the other hand, many investors believe the artificial intelligence boom has become dangerously speculative and bears an uncomfortable resemblance to the technology bubble that burst in 2000 – the “worst of times.”

That divergence in sentiment was reflected in last month’s market performance:

- Dow Jones Industrial Average: +2.5%

- S&P 500: -1.1%

- NASDAQ: -2.8%

THE BEST OF TIMES

There are plenty of reasons why this multi-year bull market continues to march higher. Here are three of the most compelling.

AI Boom – Micron

As I discussed in last month’s article, The Multi-Trillion AI Tsunami, trillions of dollars are being invested across the artificial intelligence ecosystem.

Among the biggest beneficiaries are semiconductor memory companies such as Micron Technology, Inc. (MU), whose High-Bandwidth Memory (HBM) chips have become critical components powering next-generation AI data centers.

Micron recently reported extraordinary financial results as demand continues to outstrip supply. In its most recent quarterly report, Micron’s revenues more than quadrupled to $41.5 billion from $9.3 billion (+346%), a year ago. Profits for the three-month period skyrocketed even more by 15-fold to $28.2 billion from $1.9 billion (+1,398%).

Behind this remarkable growth is a structural supply shortage. Unlike software, semiconductor manufacturing capacity cannot be expanded overnight. Building a state-of-the-art memory fabrication facility requires billions of dollars of investment and typically takes three to four years to complete.

That lengthy construction timeline suggests favorable pricing and elevated profitability may persist well beyond the current earnings cycle, which explains Micron’s +837% spike in its stock price over the last year.

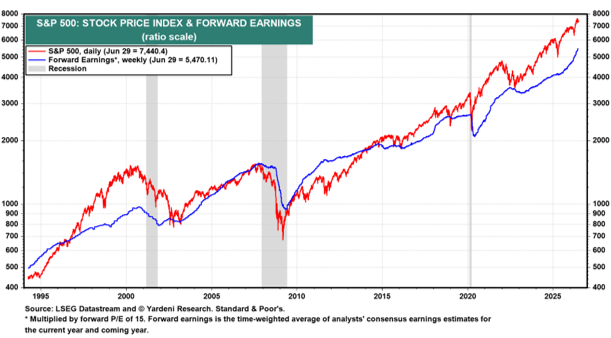

Earnings Are Rising Faster Than Stock Prices

Many investors assume record highs automatically mean expensive valuations. Not necessarily. Valuation depends on both price and earnings. When corporate earnings grow faster than stock prices, the market actually becomes less expensive despite reaching new highs.

Think back to elementary school fractions. If the denominator (earnings) grows faster than the numerator (price), the overall ratio becomes smaller. The same principle applies to the market’s Price-to-Earnings (P/E) ratio.

That is exactly what has occurred this year. Projected corporate profits are expected to surge +31%, causing the S&P 500’s valuation multiple to decline even as the index has reached record levels. One of my favorite long-term charts (below) illustrates this relationship perfectly. While stock prices can deviate from fundamentals over shorter periods, they ultimately follow the direction of corporate earnings.

Source: Yardeni Research

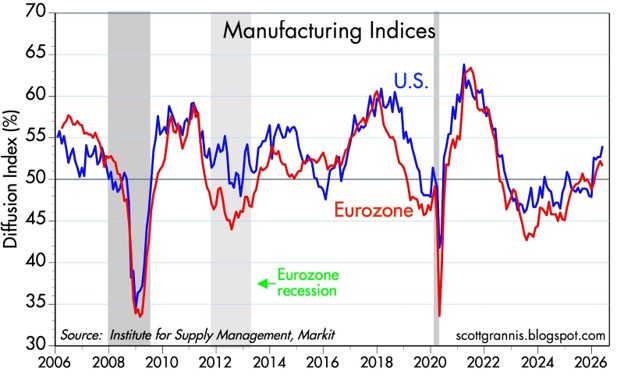

Economic Momentum Is Improving

Another encouraging development is the improving economic backdrop. The ISM Manufacturing Index remains one of the most reliable gauges of economic activity. Readings above 50 signal expansion, while readings below 50 indicate contraction. Recent data show both the United States and the Eurozone moving back into expansionary territory, suggesting manufacturing activity and economic momentum are strengthening after an extended slowdown.

Source: Calafia Beach Pundit

THE WORST OF TIMES

As I discussed in my earlier article, The SaaSpocalypse Has Arrived?, the AI revolution is creating a palpable anxiety attack as broad swaths of Americans worry about AI agents stealing their $180,000 managerial positions for a $200/month subscription fee.

There are many reasons to remain optimistic about AI’s long-term benefits, but investors should also recognize several risks that could quickly shift today’s “best of times” into the “worst of times.”

Speculative Valuations

Although the overall market appears far more reasonably valued than during the peak of the Dot-Com Bubble, speculation has clearly returned to select areas of the market.

The recent public debut of Elon Musk’s SpaceX serves as a prime example. Despite generating billions in operating losses and burning -$9 billion in cash in its recent quarter, investors have assigned the company a valuation exceeding $2 trillion. Based on trailing revenues of approximately $19 billion, investors are effectively paying more than 100 times annual sales. Such valuations require extraordinary execution over many years to ultimately justify today’s prices.

Nor is the enthusiasm limited to SpaceX. Reports indicate AI leaders Anthropic and OpenAI are preparing their own public offerings, with expected valuations approaching $1 trillion despite annual revenues that remain a fraction of those levels. History teaches us that transformative technologies often create enormous long-term winners — but periods of genuine innovation can also produce speculative excess.

Geopolitical Risks

Although a tentative ceasefire currently exists between the United States and Iran, geopolitical conditions remain fluid. Markets have largely looked through the recent conflict, but history reminds us that geopolitical events can change quickly and unexpectedly. A deterioration in the Middle East could rapidly reverse investor sentiment.

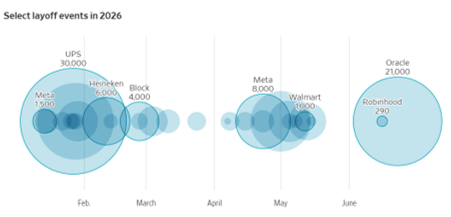

AI-Driven Layoffs

The labor market remains relatively healthy, with unemployment near 4.3%. However, beneath the surface, signs of workforce restructuring continue to emerge as companies invest aggressively in automation and artificial intelligence.

Technology companies have announced approximately 125,000 layoffs this year—roughly 66% more than during the same period last year. Oracle recently announced plans to eliminate an estimated 21,000 positions. Robinhood is reducing its workforce by approximately 10%, while Cisco revealed it is slashing its workforce by 5% (4,000 jobs). Although today’s labor market remains resilient, investors should monitor whether AI-driven productivity gains ultimately translate into broader employment weakness.

Source: Wall Street Journal

Final Thoughts

Last month’s mixed market performance reflects an investment landscape filled with both optimism and uncertainty.

If Charles Dickens were writing today, his Tale of Two Cities might instead be titled A Tale of Two Markets. The speculative excesses we experience in every technological revolution could lead to the “worst of times” but for now, the “best of times” is currently prevailing as investor optimism over AI’s productivity benefits remains front and center.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

Disclosure: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in MU or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Each investor’s situation is unique so please work with a professional financial adviser, tax accountant or legal representative, as applicable, to develop an individualized plan or address any questions you may have. Investing involves risk including the possibility of loss of one’s investment.

Rational or Irrational Exuberance?

The government may be shut down, but the stock market hasn’t noticed. In fact, stocks just capped another record-breaking month. The S&P 500 gained +2.3%, the NASDAQ climbed +4.7%, and the Dow rose +2.5%.

Millions of Americans are feeling the downside of the shutdown—from disrupted travel to stalled services and furloughed workers. Historically, such uncertainty rattles Wall Street. This time? Investors seem more captivated by the transformative promise of artificial intelligence (AI).

So, the key question today: Is this AI-driven exuberance rational—or irrational?

Exuberance Then vs. Exuberance Now

Having invested for more than 35 years, I’ve seen periods of euphoria and fear. I vividly remember December 1996 when Fed Chair Alan Greenspan famously questioned whether markets were becoming “irrationally exuberant.” Back then, the NASDAQ sat near 1,300. Over the next three years it soared past 5,100 (almost quadrupling), only to crash nearly 80% by 2002.

But here’s the twist: it’s true, we did experience a “tech bubble burst”, but where is the NASDAQ index value today? Amazingly, the index stands at 23,000 (see chart below) – an 18x increase above the 1996 level when Greenspan gave his irrational exuberance speech! So, in hindsight, the sound we heard during 2000 was not the tech bubble bursting but rather an internet Big Bang! The internet wasn’t a speculative fad—it was the foundation of a global transformation.

So, what about AI?

Source: Macrotrends LLC

Internet Cycle vs. AI Supercycle

The internet era lifted the number of online users from zero to five billion—over 60% of the planet (see chart below). The AI wave kicked off publicly in November 2022 with ChatGPT’s release. In under three years, the NASDAQ has more than doubled. That pace isn’t sustainable forever, of course. Bubbles form, emotions swing, and markets correct. But dismissing AI as a fad ignores its unmistakable—and accelerating—impact.

Source: BOND – Mary Meeker

With the rapid appreciation in the stock market, it’s important for investors to identify and understand the warning signs of potential bubble bursting or market crash. In fact, I continue to do my part by studying past crashes. My shipment of Andrew Ross Sorkin’s book, 1929: Inside the Greatest Crash in Wall Street History just arrived and all these lessons remind us that not all booms are bubbles, and not all crashes end innovation.

Not All Bubbles are Created Equal

Major market drawdowns are part of a long-term investor’s journey:

- 1929: Great Crash

- 1973-74: Nifty-Fifty

- 1987: Black Monday

- 2000: Dot-com bust

- 2008: Financial crisis

- 2020: COVID crash

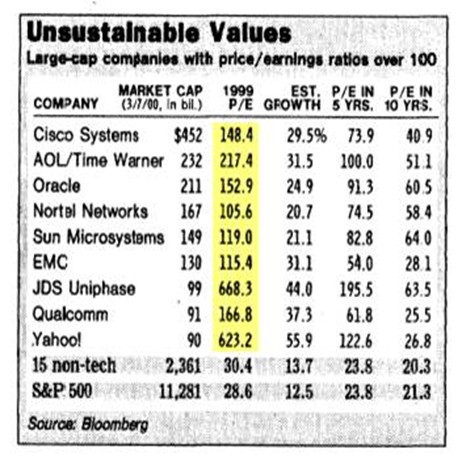

Many pundits today are now asking is this AI surge the next bubble? Valuations, as measured by P/E ratios (Price/Earnings), suggest a very different setup than in 2000.

Back then, many tech leaders traded at 100x+ earnings. Today’s Magnificent Seven tech leaders are elevated, but nowhere near dot-com extremes:

- NVIDIA Corporation (NVDA): 57x

- Apple Inc. (AAPL): 36x

- Microsoft Corp. (MSFT): 36x

- Alphabet Inc. (GOOG): 32x

- Amazon.com, Inc. (AMZN): 31x

- Meta Platforms, Inc. (META): 23x

*Source: MarketSurge – only Tesla, Inc. (TSLA) has a P/E higher than 100x.

For the S&P 500 overall, the index has a forward P/E of 22.8x (Yardeni Research), significantly lower than 2000 levels and nowhere near bubble territory.

Source: Wall Street Journal – March 14, 2000

Life After the Internet and Life After AI Introduction

Think back 25 years:

- Renting movies at Blockbuster before Netflix went digital

- Driving to the bank for deposits

- Buying stamps to mail checks before Venmo or Zelle

Today, those activities feel prehistoric. AI is set to reshape daily life on an even faster timeline — from medicine and logistics to entertainment and marketing.

I’m discovering “AI epiphanies” weekly.

- With a few prompts, I created a beautiful Mother’s Day poem and became a poet hero despite never writing poetry before.

- When I recently needed to write an obituary for my mother, AI helped structure and refine it in minutes instead of taking me hours.

- Just last month I needed to hunt down lobster bisque for a shrimp pasta recipe I wanted to make. It turned into a time-wasting scavenger hunt. Thankfully, AI found it in stock, even when multiple apps insisted it wasn’t available. Needless to say, the recipe was incredibly delicious, and my stomach thanked ChatGPT.

And when it comes to investing? Evaluating biotech companies used to take weeks. Now, detailed research can be synthesized in days without sacrificing rigor. AI isn’t replacing insight — it’s amplifying output.

Not All AI Stories Are “Unicorns and Rainbows”

AI boosts productivity. Higher productivity means some companies need fewer people. Amazon recently announced 14,000 layoffs despite reporting amazing financial results. Microsoft and Meta have also announced thousands of employee layoffs even as profits rise.

This isn’t doom and gloom — it’s innovation cycles in action. Technology displaces tasks before ultimately creating new industries and roles.

So… Rational or Irrational?

Although there has been much debate regarding whether we are in an AI bubble, from my perspective, we are in the very early innings of a long AI revolutionary game. There are definitely pockets of frothiness that expose investors to undue risk, but if you can follow a disciplined, diversified, valuation-sensitive investment strategy, like we implement at Sidoxia Capital Management, I feel that the current exuberance is more rational than irrational.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (Nov. 3, 2025). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in NVDA, AAPL, MSFT, GOOGL, AMZN, META, TSLA, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

From Rocket Ship to Roller Coaster

The stock market has been like a rocket ship over the last three years 2019/2020/2021, advancing +90% as measured by the S&P 500 index, and +136% for the NASDAQ. After this meteoric multi-year rise, stock values started to come back to earth in 2022, and the rocket ship turned into a roller coaster during January. More specifically, the S&P 500 fell -5% for the month and the NASDAQ -9%. Yes, it’s true volatility has increased, and your blood pressure may have risen with all the ups and downs. However, the fact remains the economy remains strong, corporate profits are at record levels, unemployment is low, and interest rates remain at attractive levels despite nagging inflation (see chart below) and the removal of accommodative monetary policies by the Federal Reserve.

Math Matters

I did okay in school and was educated on many different topics, including the basic principle that math matters. This notion rings especially true when it comes to finance and investing. As I have discussed numerous times in the past, money goes where it is treated best, which is why interest rates, cash flows, and valuations play such a key role in ultimately determining long-term values across all asset classes. This concept of money seeking the best home applies equally to stocks, bonds, real estate, commodities, crypto-currencies, and any other asset class you can imagine because interest rates help determine the cost of holding and using money.

Normally, mathematics teaches us the lesson that more is better when discussing financial matters. And currently the stock market is compensating investors significantly more for investing in stocks relative to investing in bonds – I have reviewed this concept repeatedly on my Investing Caffeine blog (see Going Shopping: Chicken vs. Beef ). Currently, investors are getting paid about +5% to hold stocks based on the forward earnings yield (i.e., the inverse of the stock market’s Price-Earnings ratio of 20x) vs. the +2% yield on the 10-Year Treasury Note (1.78% more precisely on 1/31/22). What’s more, historically speaking, stock investors typically get rewarded with an earnings yield that doubles about every 10 years, whereas bond yields usually remain stagnantly flat, if bonds are held until maturity.

With that said, I am always quick to point out that diversification in a portfolio is important (i.e., most people should at least own some bonds), even if bonds are currently very expensive relative to other asset classes (see Sleeping on Expensive Financial Pillows). If bond yields climb significantly to the point where returns are more competitive with stocks, I will likely be buying significantly more bonds for me and my Sidoxia (www.sidoxia.com) clients.

Fed Jitters

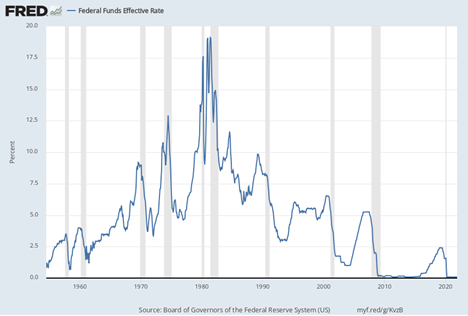

The recent stock market volatility is reinforcing the idea that the Federal Reserve’s more aggressive stance regarding hiking interest rates is making many investors very anxious – just not me. I have lived through many tightening cycles in my lifetime and lived to tell the tale. It is true that all else equal, higher interest rates generally depress asset values, but it is also important to place the current interest rate environment in historical context. Although the Federal Funds interest rate target is expected to increase to 2.5% over the next few years (currently at 0%), this forecast is nothing new and there is no guarantee the Fed can successfully pull off this feat. Many people have short memories and forget the Fed hiked interest rates 10 times from the end of 2015 through 2018. In the face of this scary period, the stock market (S&P 500) still managed to approximately climb a respectable +22% (albeit with some volatility). Furthermore, if you give the Fed the benefit of the doubt of achieving this uncertain target, this 2.5% level is very appealing and still extremely low, historically speaking (see chart below).

When discussing interest rates and inflation, investors should also expand their views globally to the other 95% of the world’s population. Many investors are very myopic in their focus on U.S. interest rates. It is important to understand that rates are not just low here in the United States, but also low almost everywhere else as well. While international interest rates have bounced marginally higher in recent months, those countries’ long-term international rates, by and large, remain tremendously low too – in most cases even lower than rates in the U.S. (see chart below). Yes, the Fed has some control over short-term interest rates in the U.S., but considering other crucial forces that are depressing long-term global rates is worth pondering. Factors such as globalization and the pervading expansion of deflationary technology into our personal and work lives are contributing to disinflation. Valuable conclusions can be synthesized beyond digesting the pessimistic and nauseating analysis of Jerome Powell’s Congressional testimony, along with the needless wordsmithing of recent Fed minutes.

In order to earn above-average, financial returns in your portfolio over the long-run, experiencing unsettling volatility and corrections is the price of doing business. Flying on rocket ships might be fun, but sometimes the rocket can run out of gas, and you are forced to jump on a roller coaster. The ups-and-downs can be frustrating at times, but if you stay on for the full ride, you will almost always end with a smile on your face when it’s over.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (February 1, 2022). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in PFE and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Return to Rationality?

As the worst pandemic in more than a generation is winding down in the U.S., people are readjusting their personal lives and investing worlds as they transition from ridiculousness to rationality. After many months of non-stop lockdowns, social distancing, hand-sanitizers, mask-wearing, and vaccines, Americans feel like caged tigers ready to roam back into the wild. An incredible amount of pent-up demand is just now being unleashed not only by consumers, but also by businesses and the economy overall. This reality was also felt in the stock market as the Dow Jones Industrial Average powered ahead another 654 points last month (+1.9%) to a new record level (34,529) and the S&P 500 also closed at a new monthly high (+0.6% to 4,204). For the year, the bull market remains intact with the Dow gaining almost 4,000 points (+12.8%), while the S&P 500 has also registered a respectable +11.9% return.

The story was different last year. The economy and stock market temporarily fell off a cliff and came to a grinding halt in the first quarter of 2020. However, with broad distribution of the vaccines and antibodies gained by the previously infected, herd immunity has effectively been reached. As a result, the U.S. COVID-19 pandemic has essentially come to an end for now and stock prices have continued their upward surge since last March.

Insanity to Sanity?

With the help of the Federal Reserve keeping interest rates at near-0% levels, coupled with trillions of dollars in stimulus and proposed infrastructure spending, corporate profits have been racing ahead. All this free money has pushed speculation into areas such as cryptocurrencies (i.e., Bitcoin, Dogecoin, Ethereum), SPACs (Special Purpose Acquisition Companies), Reddit meme stocks (GameStop Corp, AMC Entertainment), and highly valued, money-losing companies (e.g., Spotify, Uber, Snowflake, Palantir Technologies, Lyft, Peloton, and others). The good news, at least in the short-term, is that some of these areas of insanity have gone from stratospheric levels to just nosebleed heights. Take for example, Cathie Wood’s ARK Innovation Fund (ARKK) that invests in pricey stocks averaging a 91x price-earnings ratio, which exceeds 4x’s the valuation of the average S&P 500 stock. The ARK exchange traded fund that touts investments in buzzword technologies like artificial intelligence, machine learning, and cryptocurrencies rocketed +149% last year in the middle of a pandemic, but is down -10.0% this year. The Grayscale Bitcoin Trust fund (GBTC) that skyrocketed +291% in 2020 has fallen -5.6% in 2021 and -48.1% from its peak. What’s more, after climbing by more than +50% in less than four months, the Defiance NextGen SPAC fund (SPAK) has declined by -28.9% from its apex just a few months ago in February. You can see the dramatic 2021 underperformance in these areas in the chart below.

Inflation Rearing its Ugly Head?

The economic resurgence, weaker value of the U.S. dollar, and rising stock prices have pushed up inflation in commodities such as corn, gasoline, lumber, automobiles, housing, and a whole host of other goods (see chart below). Whether this phenomenon is “transitory” in nature, as Federal Reserve Chairman Jerome Powell likes to describe this trend, or if this is the beginning of a longer phase of continued rising prices, the answer will be determined in the coming months. It’s clear the Federal Reserve has its hands full as it attempts to keep a lid on inflation and interest rates. The Fed’s success, or lack thereof, will have significant ramifications for all financial markets, and also have meaningful consequences for retirees looking to survive on fixed income budgets.

As we have worked our way through this pandemic, all Americans and investors look to change their routines from an environment of irrationality to rationality, and insanity to sanity. Although the bull market remains alive and well in the stock market, inflation, interest rates, and speculative areas like cryptocurrencies, SPACs, meme-stocks, and nosebleed-priced stocks remain areas of caution. Stick to a disciplined and diversified investment approach that incorporates valuation into the process or contact an experienced advisor like Sidoxia Capital Management to assist you through these volatile times.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (June 1, 2021). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in GME, AMC, SPOT, UBER, SNOW, PLTR, LYFT, PTON, GBTC, SPAK, ARKK or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

‘Tis the Season for Giving

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (December 1, 2017). Subscribe on the right side of the page for the complete text.

Holiday season is in full swing, and that means it’s the primetime period for giving. The stock market has provided its fair share of giving to investors in the form of a +2.7% monthly return in the S&P 500 index (up +18% in 2017). For long-term investors, stocks have been the gift that keeps on giving. As we approach the 10-year anniversary of the 2008 Financial Crisis, stocks have returned +68% from the October 2007 peak and roughly +297% from the March 2009 low. If you include the contributions of dividends over the last decade, these numbers look even more charitable.

Compared to stocks, however, bonds have acted more like a stingy Ebenezer Scrooge than a generous Mother Theresa. For the year, the iShares Core Aggregate bond ETF (AGG) has returned a meager +1%, excluding dividends. Contributing to the lackluster bond results has been the Federal Reserve’s miserly monetary policy, which will soon be managed under new leadership. In fact, earlier this week, Jerome Powell began Congressional confirmation hearings as part of the process to replace the current Fed chair, Janet Yellen. As the Dow Jones Industrial Average rose for the 8th consecutive month to 24,272 (the longest winning streak for the stock index in 20 years), investors managed to take comfort in Powell’s commentary because he communicated a steady continuation of Yellen’s plan to slowly reverse stimulative policies (i.e., raise interest rate targets and bleed off assets from the Fed’s balance sheet).

Because the pace of the Federal Funds interest rate hikes have occurred glacially from unprecedented low levels (0%), the resulting change in bond prices has been relatively meager thus far in 2017. In that same deliberate vein, the Fed is meeting in just a few weeks, with the expectation of inching the Federal Funds rate higher by 0.25% to a target level of 1.5%. If confirmed, Powell plans to also chip away at the Fed’s gigantic $4.5 trillion balance sheet over time, which will slowly suck asset-supporting liquidity out of financial markets.

Economy Driving Stocks and Interest Rates Higher

Presents don’t grow on trees and stock prices also don’t generally grow without some fundamental underpinnings. With the holidays here, consumers need money to fulfill the demanding requests of gift-receiving individuals, and a healthy economy is the perfect prescription to cure consumers’ empty wallet and purse sickness.

Besides the Federal Reserve signaling strength by increasing interest rates, how do we know the economy is on firm footing? While economic growth may not be expanding at a barn-burning rate, there still are plenty of indications the economy keeps chugging along. Here are a few economic bright spots to highlight:

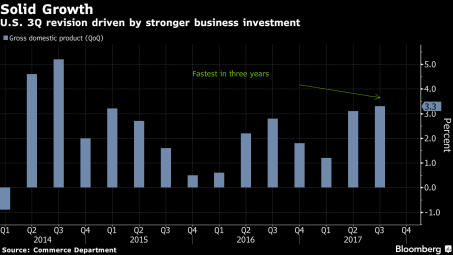

- Accelerating GDP Growth: As you can see from the chart below, broad economic growth, as measured by Gross Domestic Product (GDP), accelerated to a very respectable +3.3% growth rate during the third quarter of 2017 (the fastest percentage gain in three years). These GDP calculations are notoriously volatile figures, nevertheless, the recent results are encouraging, especially considering these third quarter statistics include the dampening effects of Hurricane Harvey and Irma.

Source: Bloomberg

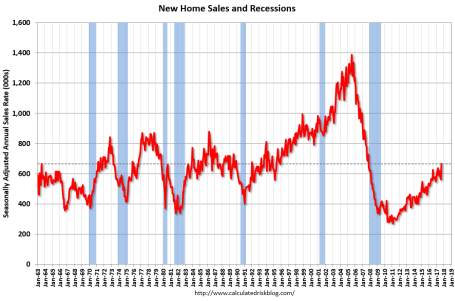

- Recovering Housing Market: The housing market may not have rebounded as quickly and sharply as the U.S. stock market since the Financial Crisis, but as the chart below shows, new home sales have been on a steady climb since 2011. What’s more, a historically low level of housing inventory should support the continued growth in home prices and home sales for the foreseeable future. The confidence instilled from rising home equity values should also further encourage consumers’ cash and credit card spending habits.

Source: Calculated Risk

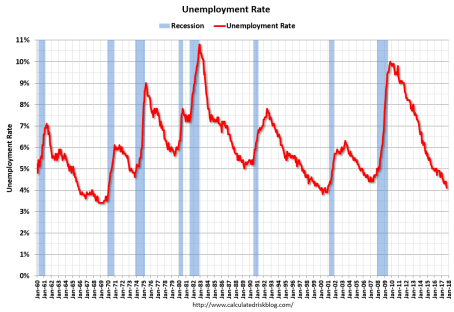

- Healthy Employment Gains: Growth in the U.S. coupled with global synchronous economic expansion in Europe, Asia, and South America have given rise to stronger corporate profits and increased job hiring. The graph highlighted below confirms the 4.1% unemployment rate is the lowest in 17 years, and puts the current rate more than 50% below the last peak of 10.0% hit in 2009.

Source: Calculated Risk

Turbo Tax Time

Adding fuel to the confidence fire is the prospect of the president signing the TCJA (Tax Cuts and Jobs Act). At the time this article went to press, Congress was still feverishly attempting to vote on the most significant tax-code changes since 1986. Republicans by-and-large all want tax reform and tax cut legislation, but the party’s narrow majority in the House and Senate leaves little wiggle room for disagreement. Whether compromises can be met in the coming days/weeks will determine whether a surprise holiday package will be delivered this year or postponed by the Grinch.

Unresolved components of the tax legislation include, the feasibility of cutting the corporate tax rate from 35% to 20%; the deductibility of state and local income taxes (SALT); the potential implementation of a tax cut limit “trigger”, if forecasted economic growth is not achieved; the potential repeal of the estate tax (a.k.a., “death tax”); mortgage interest deductibility; potential repeal of the Obamacare individual mandate; the palatability of legislation expanding deficits by $1 trillion+; debates over the distribution of tax cuts across various taxpayer income brackets; and other exciting proposals that will heighten accountants’ job security, if the TCJA is instituted.

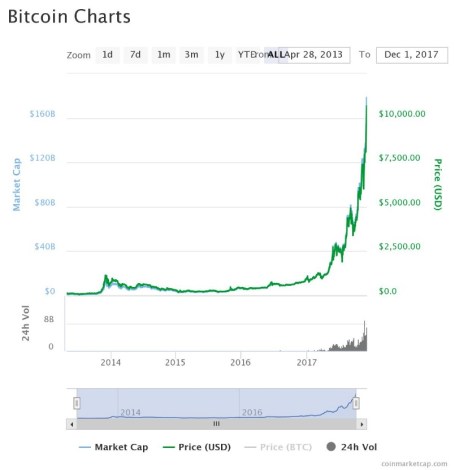

Bitcoin Bubble?

If you have recently spent any time at the watercooler or at a cocktail party, you probably have not been able to escape the question of whether the digital blockchain currency, Bitcoin, is an opportunity of a lifetime or a vehicle to crush your financial dreams to pieces (see Bitcoin primer).

Let’s start with the facts: Bitcoin’s value traded below $1,000 at the beginning of this year and hit $11,000 this week before settling around $10,000 at month’s end (see chart below). In addition, blogger Josh Brown points out the scary reality that “Bitcoin has already crashed by -80% on five separate occasions over the last few years.” Suffice it to say, transacting in a currency that repeatedly loses 80% of its value can pose some challenges.

Source: CoinMarketCap.com

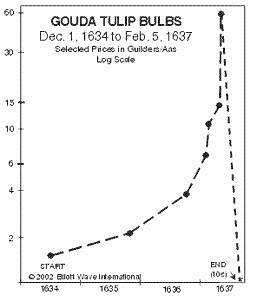

Bubbles are not a new phenomenon. Not only have I lived through numerous bubbles, but I have also written on the topic (see also Sleeping and Napping through Bubbles). I find the Dutch Tulip Bulb Mania that lasted from 1634 – 1637 to be the most fascinating financial bubble of all (see chart below). At the peak of the euphoria, individual Dutch tulip bulbs were selling for the same prices as homes ($61,700 on an inflation-adjusted basis), and one historical account states 12 acres of land were offered for a single tulip bulb.

Forecasting the next peak of any speculative bubble is a fool’s errand in my mind, so I choose to sit on the sidelines instead. While I may be highly skeptical of the ethereal value placed on Bitcoin and other speculative markets (i.e. ICOs – Initial Coin Offerings), I fully accept the benefits of the digital blockchain payment technology and also acknowledge Bitcoin’s value could more than double from here. However, without any tangible or intellectual process of valuing the asset, history may eventually place Bitcoin in the same garbage heap as the 1630 tulips.

For some of you out there, if you are anything like me, your digestion system is still recovering from the massive quantities of food consumed over the Thanksgiving holiday. However, when it comes to your personal finances, digesting record-breaking stock performance, shifting Federal Reserve monetary policy, tax legislation, and volatile digital currencies can cause just as much heartburn. In the spirit of “giving”, if you are having difficulty in chewing through all the cryptic economic and political noise, “give” yourself a break by contacting an experienced, independent, professional advisor. That’s definitely a gift you deserve!

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Who Gives a #*&$@%^?!

The stock market is just a big rigged casino, fueled by a reckless money printing Fed that is artificially inflating a global asset bubble, right? That seems to be the mentality of many investors as evidenced by the lack of meaningful domestic stock fund buying/inflows (see also Digesting Stock Gains). Underlying investor skepticism is a foundation of mistrust and detachment caused by the unprecedented 2008-09 financial crisis, when regulators fell asleep at the switch.

Making matters worse, the proliferation of the Internet, smart phones, and social media, has forced investors to digest a never-ending avalanche of breaking news headlines and fear mongering. Here is a partial list of the items currently frightening investors:

- Interest Rates: Will the Federal Reserve raise interest rates in June or September?

- Volatility: The Dow is up 200 points one day and then down 200 the next day. Keep me away.

- Greece: One day Greece is going to exit the eurozone and the next day it’s going to reach a deal with the IMF (International Monetary Fund) and European leaders.

- Terrorism / Middle East: ISIS is like a cancer taking over the Middle East, and it’s only a matter of time before they invade our home soil. And if ISIS doesn’t get us, then the Iranian boogeyman will attack us with their inevitable nuclear weapons.

- Inflation: The economy is slowing improving and as we approach full employment in the U.S., wage pressure is about to kick inflation into high gear. After falling significantly, oil prices are inching higher, which is also moving inflation in the wrong direction.

- Strong Dollar: Now that Europe is copying the U.S. by implementing quantitative easing, domestic exports are getting squeezed and revenue growth is slowing.

- Bubble? Stocks have had a monster run over the last six years, so we must be due for a crash…correct?

Seemingly, on a daily basis, some economist, strategist, analyst, or talking head pundit on TV articulately explains how the financial markets can fall off the face of the earth. Unfortunately, there is a problem with this type of analysis, if your evaluation is solely based upon listening to media outlets. Bottom line is you can always find a reason to sell your investments if you listen to the so-called experts. I made this precise point a few years ago when I highlighted the near tripling in stock prices despite the barrage of bad news (see also A Series of Unfortunate Events).

While I am certainly not asking anyone to blindly assume more risk, especially after such a large run-up in stock prices, I find it just as important to point out the following:

“Taking too much risk is as risky as not taking enough risk.”

In other words, driving 35 mph on the freeway may be more life threatening than driving 75 mph. In the world of investing, driving too slowly by putting all your savings in cash or low-yielding securities, as many Americans do, may feel safe. However this default strategy, which may feel comfortable for many, may actually make attaining your financial goals impossible.

At Sidoxia, we create customized Investment Policy Statements (IPS) for all our clients in an effort to optimize risk levels in a Goldilocks fashion…not too hot, and not too cold. Retirement is supposed to be relaxing and stress free. Do yourself a favor and create a disciplined and systematic investment plan. Being apathetic due to an infinite stream of worrisome sounding headlines may work in the short-run, but in the long-run it’s best to turn off the noise…unless of course you don’t give a &$#*@%^ and want to work as a greeter at Wal-Mart in your mid-80s.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and WMT, but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on ICContact page.

Siegel & Co. See “Bubblicious” Bonds

Source: Wall Street Journal - March 14, 2000

Siegel compares 1999 stock prices with 2010 bonds

Unlike a lot of economists, Jeremy Siegel, Professor at the Wharton School of Business, is not bashful about making contrarian calls (see other Siegel article). Just days after the Nasdaq index peaked 10 years ago at a level above 5,000 (below 2,200 today), Siegel called the large capitalization technology market a “Sucker’s Bet” in a Wall Street Journal article dated March 14, 2000. Investors were smitten with large-cap technology stocks at the time, paying balloon-like P/E (Price-Earnings) ratios in excess of 100 times trailing earnings (see table above).

Bubblicious Boom

Today, Siegel has now switched his focus from overpriced tech-stock bubbles to “Bubblicious” bonds, which may burst at any moment. Bolstering his view of the current “Great American Bond Bubble” is the fact that average investors are wheelbarrowing money into bond funds. Siegel highlights recent Investment Company Institute data to make his point:

“From January 2008 through June 2010, outflows from equity funds totaled $232 billion while bond funds have seen a massive $559 billion of inflows.”

The professor goes on to make the stretch that some government bonds (i.e., 10-year Treasury Inflation-Protected Securities or TIPS) are priced so egregiously that the 1% TIPS yield (or 100 times the payout ratio) equates to the crazy tech stock valuations 10 years earlier. Conceptually the comparison of old stock and new bond bubbles may make some sense, but let’s not lose sight of the fact that tech stocks virtually had a 0% payout (no dividends). The risk of permanent investment loss is much lower with a bond as compared to a 100-plus multiple tech stock.

Making Rate History No Mystery

What makes Siegel so nervous about bonds? Well for one thing, take a look at what interest rates have done over the last 30 years, with the Federal Funds rate cresting over 20%+ in 1981 (View RED LINE & BLUE LINE or click to enlarge):

Source: dshort.com

As I have commented before, there is only one real direction for interest rates to go, since we currently sit watching rates at a generational low. Rates have a minute amount of wiggle room, but Siegel rightfully understands there is very little wiggle room for rates to go lower. How bad could the pain be? Siegel outlines the following scenario:

“If over the next year, 10-year interest rates, which are now 2.8%, rise to 3.15%, bondholders will suffer a capital loss equal to the current yield. If rates rise to 4% as they did last spring, the capital loss will be more than three times the current yield.”

Siegel is not the only observer who sees relatively less value in bonds (especially government bonds) versus stocks. Scott Grannis, author of the Calafia Report artfully shows the comparisons of the 10-Year Treasury Note yield relative to the earnings yield on the S&P 500 index:

Source: Calafia Report (Scott Grannis)

As you can see, rarely have there been periods over the last five decades where bonds were so poorly attractive relative to equities.

Grannis mirrors Siegel’s view on government bond prices through his chart on TIPS pricing:

Source: Calafia Report (Scott Grannis)

Pricey Treasuries is not a new unearthed theme, however, Siegel and Grannis make compelling points to highlight bond risks. Certainly, the economy could soften further, and trying to time the bottom to a multi-decade bond bubble can be hazardous to your investing health. Having said that, effectively everyone should desire some exposure to fixed income securities, depending on their objectives and constraints (retirees obviously more). The key is managing duration and the risk of inflation in a prudent fashion. If you believe Siegel is correct about an impending bond bubble bursting, you may consider lightening your Treasury bond load. Otherwise, don’t be surprised if you do not collect on another “sucker’s bet.”

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including TIP and other fixed income ETFs), but at the time of publishing SCM had no direct position in any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Mauboussin Takes the Outside View

Michael Mauboussin, Legg Mason Chief Investment Strategist and author of Think Twice, is a behavioral finance guru and in his recent book he explores the importance of seriously considering the “outside view” when making important decisions.

What is Behavioral Finance?

Behavioral finance is a branch of economics that delves into the non-numeric forces impacting a diverse set of economic and investment decisions. Often these internal and external influences can lead to sub-optimal decision making. The study of this psychology-based discipline is designed to mitigate economic errors, and if possible, improve investment decision making.

Two instrumental contributors to the field of behavioral finance are economists Daniel Kahneman and Amos Tversky. In one area of their research they demonstrated how emotional fears of loss can have a crippling effect in the decision making process. In their studies, Kahneman and Tversky showed the pain of loss is more than twice as painful as the pleasure from gain. How did they illustrate this phenomenon? Through various hypothetical gambling scenarios, they highlighted how irrational decisions are made. For example, Kahneman and Tversky conducted an experiment in which participating individuals were given the choice of starting with an initial $600 nest egg that grows by $200, or beginning with $1,000 and losing $200. Both scenarios created the exact same end point ($800), but the participants overwhelmingly selected the first option (starting with lower $600 and achieving a gain) because starting with a higher value and subsequently losing money was not as comfortable.

The impression of behavioral finance is burned into our history in the form of cyclical boom, busts, and bubbles. Most individuals are aware of the technology bubble of the late 1990s, or the more recent real estate/credit craze, however investors tend to have short memories are unaware of previous behavioral bubbles. Take the 17th century tulip mania, which witnessed Dutch citizens selling land, homes, and other assets in order to procure tulip bulbs for more than $70,000 (on an inflation-adjusted basis), according to Stock-Market-Crash.net. We can attempt to delay bubbles, but they will forever be a part of our economic fabric.

The Outside View

Click here for Michael Mauboussin interview with Morningstar

Click here for Michael Mauboussin interview with Morningstar

In his book Think Twice Mauboussin takes tenets from behavioral finance and applies it to individual’s decision making process. Specifically, he encourages people to consider the “outside view” when making important decisions.

Mauboussin makes the case that our decisions are unique, but share aspects of other problems. Often individuals get trapped in their heads and internalize their own problems as part of the decision making process. Since decisions are usually made from our personal research and experiences, Mauboussin argues the end judgment is usually biased too optimistically. Mauboussin encourages decision makers to access a larger outside reference class of diverse opinions and historical situations. Often, situations and problems encountered by an individual have happened many times before and there is a “database of humanity” that can be tapped for improved decision making purposes. By taking the “outside view,” he believes individual judgments will be tempered and a more realistic perspective can be achieved.

In his interview with Morningstar, Mauboussin provides a few historical examples in making his point. He uses a conversation with a Wall Street analyst regarding Amazon (AMZN) to illustrate. This particular analyst said he was forecasting Amazon’s revenue growth to average 25% annually for the next ten years. Mauboussin chose to penetrate the “database of humanity” and ask the analyst how many companies in history have been able to sustainably grow at these growth rates? The answer… zero or only one company in history has been able to achieve a level of growth for that long, meaning the analyst’s projection is likely too optimistic.

Mean reversion is another concept Mauboussin addresses in his book. I consider mean reversion to be one of the most powerful principles in finance. This is the idea that upward or downward moving trends tend to revert back to an average or normal level over time. In describing this occurrence he directs attention to the currently, overly pessimistic sentiment in the equity markets (see also Pessimism Porn article). At end of 1999 people were wildly optimistic about the previous decade due to the significantly above trend-line returns earned. Mean reversion kicked in and the subsequent ten years generated significantly below-average returns. Fast forward to today and now the pendulum has swung to the other end. Investors are presently overly pessimistic regarding equity market prospects after experiencing a decade of below trend-line returns (simply look at the massive divergence in flows into bonds over stocks). Mauboussin, and I concur, come to the conclusion that equity markets are likely positioned to perform much better over the next decade relative to the last, thanks in large part to mean reversion.

Behavioral finance acknowledges one sleek, unique formula cannot create a solution for every problem. Investing includes a range of social, cognitive and emotional factors that can contribute to suboptimal decisions. Taking an “outside view” and becoming more aware of these psychological pitfalls may mitigate errors and improve decisions.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and AMZN, but at time of publishing had no direct positions in LM, or MORN. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Decade in Review

We laughed, we cried, we kissed another ten years goodbye. It is virtually impossible to cram ten years into one article, nonetheless I will attempt to chronicle some of the central and silly events that bubble up in my memory bank.

2000

Capture of Elian Gonzalez

- Technology-heavy NASDAQ index peaks at 5,132 before completing its -78% decline by late 2002.

- Y2K (Year 2000) fears do not materialize and technology orders begin downward slide.

- AOL buys Time Warner for $164 Billion in hopes of converging media and internet worlds.

- Al Gore Democratic nominee for the Presidency wins popular vote but loses election to George Bush after effort for Florida recount fails.

- Elian Gonzalez, six-year old boy returned to Cuba.

- Reality TV show Survivor finishes first season with Richard Hatch winning prize.

2001

Enron Logo at Headquarters

- Apple introduces iPod digital music player.

- Enron files Chapter 11 bankruptcy.

- Wikipedia online community encyclopedia launches.

- 9/11 attacks occur pushing economy further down.

- Alan Greenspan starts 1st of 11 rate cuts in 2001.

- China joins WTO (World Trade Organization).

2002

- Severe Acute Respiratory Syndrome (SARS), an atypical form of pneumonia, rears its ugly head in the Guangdong Province of China.

- SEC files charges against WorldCom and Tyco international in connection with accounting irregularities

- United Airlines files for bankruptcy.

- American Idol television singing contest begins first season.

- Guantanomo Bay detention camp is opened.

2003

- Federal Funds rate reaches a 45 year low at 1.00% – fuel for future credit bubble.

- $350 billion in tax cuts approved, spanning a ten year period.

- Iraqi Gulf War II commences with “shock and awe” military campaign.

- Space Shuttle Columbia disintegrates upon attempted reentry into the Earth’s atmosphere.

- Broad stock market recovery (>90% of stocks in S&P500 climb), including a +50% rise in the NASDAQ index.

- Martha Stewart indicted for using privileged investment information and then obstructing a federal investigation.

- Arnold Schwarzenegger, movie star, becomes governor of California.

2004

- Google (GOOG) goes public with IPO at $85 per share.

- Mark Zuckerberg unveils Facebook and people begin “friending” each other.

- Comcast makes failing unsolicited bid for Disney. K-Mart buys Sears with aid of Eddie Lampert

- Ronald Reagan, 40th President, dies at 93.

- Janet Jackson and Justin Timberlake experience “wardrobe malfunction” on Super Bowl halftime show.

- Boston Red Sox win their first World series since 1918.

2005

- P&G announces $57 billion acquisition of Gillette. Conoco Philips buys Burlington Resources for over $30 billion. Bank of America buys credit card company MBNA.

- Ben Bernanke is nominated as new Federal Reserve Chairman.

- Hurricane Katrina overwhelms New Orleans as 80% of city becomes covered with water.

- North Korea announces its nuclear weapons arsenal.

- YouTube starts sharing online videos before Google Inc. eventually buys company.

- Lance Armstrong wins 7th consecutive Tour de France.

2006

- Inverted yield curve turns out to be an accurate leading indicator for 2008 recession despite markets advance.

- Internet activity accelerates: Google buys YouTube after News Corp buys MySpace. Twitter is introduced.

- Playstation 3 (PS3) and Nintendo Wii unveiled.

- Merger & acquisition activity reaches $3.79 trillion worldwide, surpassing previous 2000 peak (Thomson).

- Options backdating takes center stage. United Health and technology companies were among those dragged into controversy.

- Housing market peaks.

2007

- Markets continue multi-year rally with three major indexes holding single-digit gains. Emerging markets build on previous year gains – Shanghai composite +97%.

- Monoline insurers MBIA and rival Ambac become early canaries in the coal mine given the greater than $1 trillion in exposure on insuring securities.

- Apple presents the iPhone – part phone, part music, part computer.

- KKR (Kohlberg Kravis Roberts & Co.) and TPG complete $44.4 billion buyout of Texas power company TXU Corp.

- Microsoft Vista operating system introduced after five years of development.

- Housing decline accelerates as Countrywide Financial announces 12,000 job cuts (20% of its workforce), New Century Financial (#2 subprime lender at one point) files Chapter 11 bankruptcy, and two Bear Stearns mortgage based hedge funds go under.

- Chuck Prince, Citigroup CEO, steps down.

2008

- Bank of America agrees to buy Countrywide mortgage company for about $4 billion.

- JPMorgan Chase agrees to buy Bear Stearns for $2 per share in a sale brokered by the Fed and the U.S. Treasury – eventually bid revised upwards to $10 per share (~$1.1 billion) to appease angry shareholders.

- Lehman Brothers goes bankrupt.

- Bank of America agrees to acquire Merrill Lynch for about $50 billion.

- Government takes over AIG after providing insurance company $85 billion loan.

- Goldman Sachs and Morgan Stanley become bank holding companies to improve access to capital.

- Washington Mutual Inc. is seized by FDIC and sold to JPMorgan Chase in the biggest U.S. bank failure in history.

- Wells Fargo & Co., agrees to purchase Wachovia for about $15.1 billion, trumping Citigroup’s bid.

- $700 billion TARP (Troubled Asset Relief Program) eventually approved by Congress to stabilize financial system.

- Eliot Spitzer resigns after prostitution scandal.

- Michael Phelps wins eight gold medals at the 2008 Beijing Summer Olympics.

2009

- Barack Obama inaugurated in as 44th President of the United States. Healthcare reform bills pass in both the House and Senate.

- GM and Chrysler declare bankruptcy.

- Recession ends as stimulus kicks in and inventories rebuild. Government announces new PPIP and TALF programs.

- Warren Buffett pays $26 billion to buy Burlington Northern Santa Fe. Other announcements include: Oracle /Sun Microsystems; Pfizer/Wyeth; Merck/Schering Plough; and Pulte Homes/Centex.

- Commodities and emerging markets rebound. Gold tops $1,000 per ounce.

- Signs of housing bottoming as low mortgage rates, tax credits, and declining inventories create a more constructive environment.

- Madoff goes to prison after he was convicted for a $65 billion Ponzi Scheme.

- Chesley B. “Sully” Sullenberger successfully carries out the treacherous crash-landing of US Airways Flight 1549 into the Hudson River.

- Dubai debt debacle forces Abu Dhabi to lend support to calm global markets.

- Tiger Woods admits transgressions after car crash pushes him into spotlight.

2010 ???

Time will tell what the new year will bring. Stay tuned for some iron clad 2010 predictions coming to an Investing Caffeine blog near you in the not too distant future!

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and BAC, AAPL, and GOOG, but did not have any direct positions in the following stocks mentioned in this article at time of publication (including AOL/TWX, VIA/CBS, NWS, TYC, UAUA, MSO, CMCSA, DIS, SHLD, PG, COP, Nintendo, MBI, ABK, MSFT, C, JPM, AIG, MS, WFC, GM, Chrysler, BRKA, ORCL, JAVA, PFE, MRK, PHM, BNI, LCC, GLD, and NKE). No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Back to the Future: Mag Covers (Part II)

In my most recent article, I went Back to the Future to examine the role magazine covers play as a contrarian indicator in fear-driven markets like we experienced in the 1970s (see previous story). Investing is both an art and science. While measuring the scientific aspects of the market can be more straight-forward, the behavioral and emotional sides to investing are more subjective. Magazines act as sentiment sensors to gauge the fear and froth pulses of the general investing public. Since last time we explored fear, let’s check out some froth from the 1990s technology boom.

How to Invest in the Hottest Market Ever

Seeing the forest from the trees can be difficult when you’re trapped in the thick of it, but the March 2000 issue of Money magazine’s “How to Invest in the Hottest Market Ever” is a classic example of the mentality that reigned supreme in the late 1990s technology bubble. Objective, fact-filled articles that challenge the status quo are not necessary to generate sales, but articles and magazine covers that pander to the raw emotions of fear and greed keep the cash register ringing. If you don’t believe me, just read the sensational headlines at your local grocery store explaining how swine flu will kill us all and how there are millions to be made in melting gold coins and jewelry (read gold article).

I love some of the quotes from the article, especially from Pam, the 51 year old divorced New York City art museum volunteer who bought AOL, Microsoft, and Qualcomm (which rose +2,621% in 1999) who dismisses diversification: “I feel pretty safe now. I think we are in a new paradigm now.” Yeah, a “new economy” that catapulted Yahoo to a Price/Earnings ratio of 400x’s earnings; Cisco 109x’s earnings; and Sun Microsystems practically a bargain basement steal at 88x’s earnings. For reference purposes, the S&P 500 index currently trades for about 14.6x’s estimated 2010 earnings and 19.5x on 2009 estimates.

GetRich.com

Another landmark masterpiece I love is the September 1999 Time cover, “GetRich.com.” Never mind the unabated technology boom (excluding a brief hiccup in 1998) that inflated the bubble for a decade – Time still managed to unearth the “Secrets of the New Silicon Valley.” The article goes onto to express the get-rich formula:

“Can’t program a computer? Not a techno savvy? Not a problem. If you’ve got a hot Internet business idea, Silicon Valley’s astonishing start-up machine will do the rest.”

Like a drug dealer pushing heroin on an addict, the article goes on to entice its readers to question “Why have a boss when you and three buddies can build your own publicly traded company in two years? Windows this big don’t open very often.”

A Few More Favorites

Great timing on this February 2000 cover…a month before the crash!

This July 1999 cover captures envy. Everyone's getting rich!

As we saw during the technology boom, media outlets have no shame in shoveling greed inducing slop to the hungry general public. Like all historical events that end tragically, valuable lessons can be learned from our mistakes. Developing a discerning palette for the news we digest is a critical quality to generating an informed investment decision process. With the 1970s and 1990s behind us, as the last of my three part series, we’ll use time travel to another period to see if modern magazine editors fare any better in market timing as compared to their predecessors. Please excuse me while I jump in my time machine.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) or its clients has a long position in CSCO and QCOM at the time this article was originally posted. SCM owns certain exchange traded funds, but currently has no direct position in YHOO, MSFT, or JAVA. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}